Innovation Update: Annual Benchmarking Results and Take-Aways

19

Transcript of Innovation Update: Annual Benchmarking Results and Take-Aways

Innovation Update: Annual Benchmarking Results and Take-Aways

Edin Imsirovic – Associate Director, AM Best

Bridget Maehr – Associate Director, AM Best

Agenda

• Most innovative lines of business

‒ Reinsurance

‒ Health

‒ Auto

• After the first year, what is the data telling us?

‒ Key observations

• What does the future hold?

‒ Impact of COVID-19

3

Distribution Centered on “Moderate”

19

54

20

6

2

0

10

20

30

40

50

60

Minimal Moderate Significant Prominent Leader

(%)

Innovation Assessments

4

Most Innovative Lines of Business – Reinsurance

• Innovative culture to address significant cat events and competitive pressure

• Structural changes driving innovation in the reinsurance segment:

5

Third-party capital, insurance-linked

securities and sidecars

Data driven product design, risk selection

and pricing Vertical integration

Most Innovative Lines of Business – Health

• Health insurers embrace both new technologies as well as structural or process innovations

• Innovative solutions are sought after to manage both medical expenditures and administrative costs, as well as to improve quality and customer experience

‒ Integrated delivery models, value-based reimbursement models

‒ Advanced data analytics, predictive modeling

‒ Use of AI in customer service as well as medical cost management

‒ Wearable technologies for remote monitoring and data collection

6

Most Innovative Lines of Business – Auto

• Emerging technological trends are having a big impact on less complex lines of business such as auto

• Auto insurers are increasingly employing a range of innovative solutions in areas such as:

7

Telematics Process

automation

Usage-based

insurance

Output Score Lags Input Score

8

11.6 10.78.8 7.7

6.1 5.74.0

10.08.9

7.06.0

4.8 4.8

4.0

21.6

19.6

15.8

13.7

10.9 10.5

8.0

0

5

10

15

20

25

Exceptional Superior Excellent Good Fair Marginal Weak

(%)

Output Score Input Score

Average Innovation Scores by Rating Category

It Starts with Leadership

9

10 16 17 21

5659 54

57

2923

2519

5 2 5 3

0

10

20

30

40

50

60

70

80

90

100

Leadership Score Resources Score Culture Score Process & Structure

(%)

1 2 3 4

Innovation Input Component Score Distribution

Most Innovation Not Transformative … Yet

10

33

48

53

45

136

2 1

0

10

20

30

40

50

60

70

80

90

100

Results Level of Transformation

(%)

1 2 3 4

Innovation Output Scores

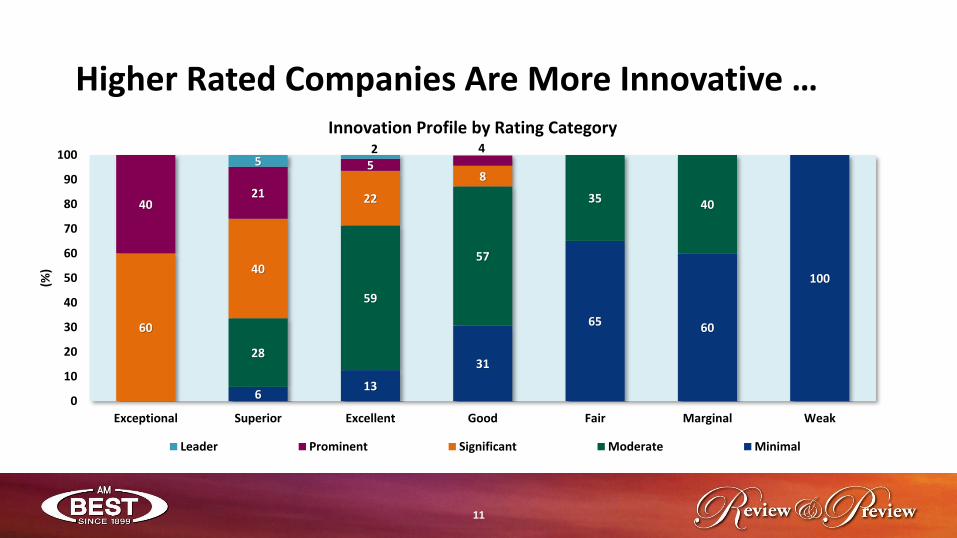

Higher Rated Companies Are More Innovative …

11

613

31

65 60

100

28

59

57

35 40

60

40

22

8

4021

5

45

2

0

10

20

30

40

50

60

70

80

90

100

Exceptional Superior Excellent Good Fair Marginal Weak

(%)

Leader Prominent Significant Moderate Minimal

Innovation Profile by Rating Category

… and Get More Results from the Effort

12

9

28

47

7280

100

20

47

58

49

2820

80

39

1245

2

0

10

20

30

40

50

60

70

80

90

100

Exceptional Superior Excellent Good Fair Marginal Weak

(%)

1 2 3 4

Output Results Score by Rating Category

A Clear Link with Business Profile

13

313

27

44

8

36

56

59

40

28

39

25

11 16

48

19

5

2

163

1 1

0

10

20

30

40

50

60

70

80

90

100

Very Favorable Favorable Neutral Limited Very Limited

(%)

Leader Prominent Significant Moderate Minimal

Innovation Profile by Business Profile Assessment

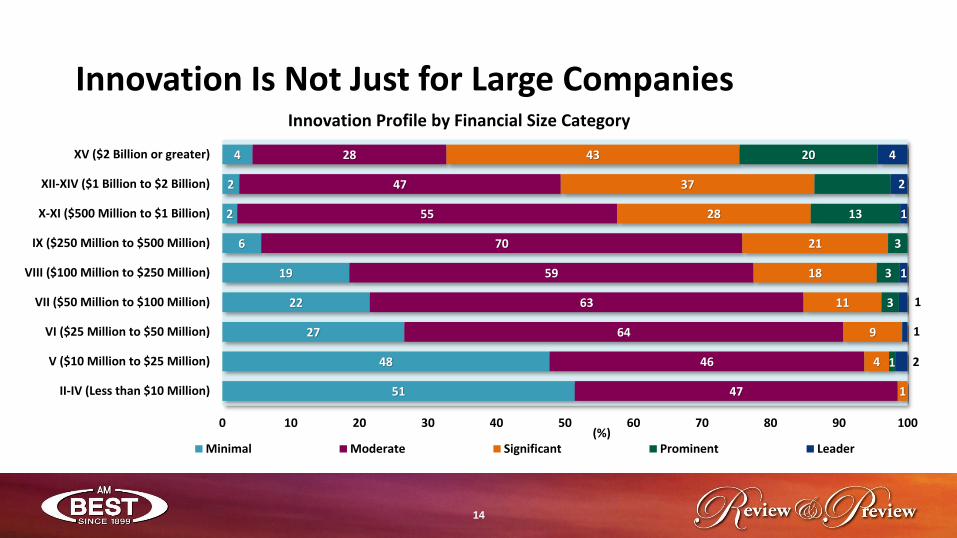

Innovation Is Not Just for Large Companies

1

14

51

48

27

22

19

6

2

2

4

47

46

64

63

59

70

55

47

28

1

4

9

11

18

21

28

37

43

1

3

3

3

13

20

2

1

1

1

1

2

4

0 10 20 30 40 50 60 70 80 90 100

II-IV (Less than $10 Million)

V ($10 Million to $25 Million)

VI ($25 Million to $50 Million)

VII ($50 Million to $100 Million)

VIII ($100 Million to $250 Million)

IX ($250 Million to $500 Million)

X-XI ($500 Million to $1 Billion)

XII-XIV ($1 Billion to $2 Billion)

XV ($2 Billion or greater)

(%)Minimal Moderate Significant Prominent Leader

Innovation Profile by Financial Size Category

It Is a Global Phenomenon

71

23

31

27

17

38

29

5

29

67

64

57

53

48

44

58

0

9

5

15

22

14

18

19

0

1

6

0

9

16

2

1

0 10 20 30 40 50 60 70 80 90 100

Sub-Saharan Africa

Caribbean

MENA

Asia

North America

Oceania

Latin America

Europe

(%)Minimal Moderate Significant Prominent Leader

Innovation Profile by Geographic Region

15

Impact of COVID-19 on Innovation

16

COVID-19 has accelerated digital transformation

initiatives for many insurers as digital experience is becoming the priority across all lines of

business.

Product innovation is becoming increasingly

important as consumers are seeking new types of products such as usage based insurance.

Future Drivers of Innovation

Evolving Use of Technology and Innovative Thinking Required to Address Need for

Contactless Interactions

• Remote workforce• Virtual sales • Automated underwriting• Virtual claims adjustment• Parametric coverages• Expansion of telehealth beyond

physician visits – vision, dental, diagnostics

Product Development to Meet Changing Coverage Needs

• Hybrid or combination products

• Usage based insurance

• Parametric coverages

• Virtual care focused health products

17

© AM Best Company, Inc. (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT

LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED,

DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM

OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR WRITTEN CONSENT. All information contained herein is obtained

by AMB from sources believed by it to be accurate and reliable. AMB does not audit or otherwise independently verify the accuracy or reliability of information

received or otherwise used and therefore all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall AMB have

any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other

circumstance or contingency within or outside the control of AMB or any of its directors, officers, employees or agents in connection with the procurement, collection,

compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory

or incidental damages whatsoever (including without limitation, lost profits), even if AMB is advised in advance of the possibility of such damages, resulting from the

use of or inability to use, any such information. The credit ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the

information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold

any securities, insurance policies, contracts or any other financial obligations, nor does it address the suitability of any particular financial obligation for a specific

purpose or purchaser. Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. Credit ratings do not address any

other risk, including but not limited to, liquidity risk, market value risk or price volatility of rated securities. AMB is not an investment advisor and does not offer

consulting or advisory services, nor does the company or its rating analysts offer any form of structuring or financial advice. NO WARRANTY, EXPRESS OR

IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH

RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AMB IN ANY FORM OR MANNER WHATSOEVER. Each credit rating or other opinion

must be weighed solely as one factor in any investment or purchasing decision made by or on behalf of any user of the information contained herein, and each such

user must accordingly make its own study and evaluation of each security or other financial obligation and of each issuer and guarantor of, and each provider of

credit support for, each security or other financial obligation that it may consider purchasing, holding or selling.

19