innovation diversification rejuvenation - Estate Intel · annual rEPort 2010 EMIRA Property Fund...

116

ANNUAL REPORT 2010 EMIRA Property Fund annual report 2010 INNOVATION DIVERSIFICATION REJUVENATION

Transcript of innovation diversification rejuvenation - Estate Intel · annual rEPort 2010 EMIRA Property Fund...

a n n u a l r E P o r t 2 0 1 0

EMIRA

Property Fund annual report 2010

innovation diversification rejuvenation

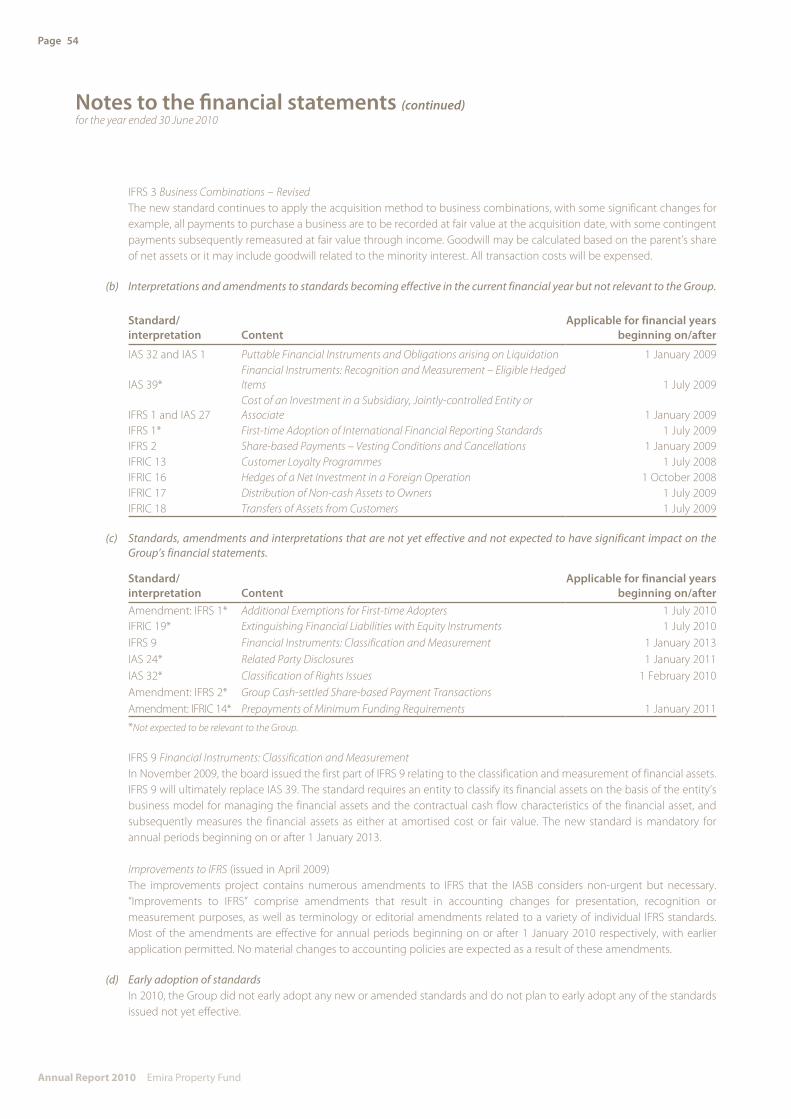

Strategic focus 1

Major achievements 2

Five-year financial review 5

Portfolio of top 10 properties by value 6

Portfolio summary 8

Chief Executive officer’s message 10

Manager’s report 15

Directorate 32

Corporate governance 34

Sustainability 40

annual financial statements 45

Participatory interest holders’ analysis 83

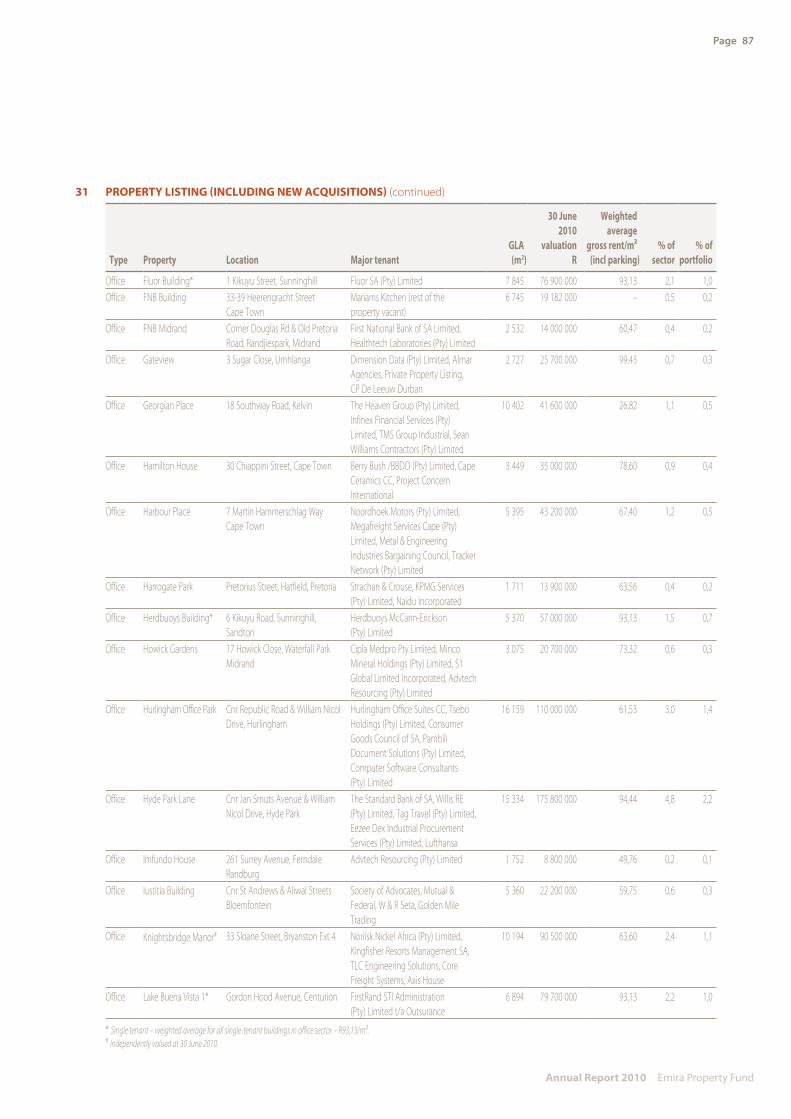

Property listing 85

Strategic real Estate Managers (Pty) limited – Financial statements 97

notice of annual general meeting 108

administration information 110

Form of proxy 111

emira Property fund’s principal objective is to grow earnings from a quality-based property portfolio.

Growth will be sought by making strategic investments where yields are enhancing in the medium to long term.

Management will further maintain the quality of the portfolio by disposing of assets, which no longer meet the strategic objectives of the fund.

www.emira.co.za

A property fund created under the Emira Property Scheme, registered in terms of the Collective Investment Schemes Control Act No 45 of 2002

Share code: EMIISIN: ZAE000050712(“Emira”)

Discovery Health

Technohub

Dalefern

Front cover – Wonderpark Shopping Centre, Boundary Terraces, Southern Sentrum, RTT Acsa Park

• Optimise net income and growth in distributions;

• Apply gearing to the portfolio to the extent that it enhances returns, limited to 40% of total assets as provided for in the Collective Investment Schemes Control Act;

• �Increase market capitalisation, liquidity and spread of investors through selective acquisitions and capital raising;

• Selectively recycle assets;

• Broaden the Fund’s geographic exposure to KwaZulu-Natal and the Western and Eastern Cape;

• Maintain a balanced exposure to the office, retail and industrial property sectors;

• Dispose of non-performing or potentially under-performing properties;

• Reduce vacancies and manage the lease expiry profile of the portfolio; and

• Meet the requirements of the Property Sector Transformation Charter.

Strategic focus

Page 1

Annual Report 2010 Emira Property Fund

R527,2�millionDistributable�income��

108,08�cents�+�6,8%�Distribution�per�participatory�interest�(PI)�

1�133�cents�Net�asset�value�per�PI

+�32,8%�12-month�total�return�

Imfundo House UNDP House

The� announcement� in� July� 2010� that� Emira� would� amend� the� terms� of� its�

asset management fee structure� was� the� culmination� of� extended�

negotiations�between�the�Fund,�the�shareholders�of�the�Manager,�Strategic�

Real� Estate� Managers� (STREM)� and� the� regulatory� authorities.� It� will� bring�

short- and long-term benefits�for�participatory�interest�(PI)�holders�of�

the�Fund.

When�PI�holders�voted�in�favour�of�the�change�to�the�Trust�Deed�of�the�Fund,�

Emira� became� the� first� Collective� Investment� Scheme� in� Property� (CISP)� to�

align�management�and�PI�holders’�interests�by�introducing�a�cost�only�related�

fee�structure.

Under�the�terms�of�the�agreement�the�Manager,�STREM,�agreed�to�amend�the�

terms� of� its� service� charge� arrangement� to� a� monthly fee based on

STREM’s actual operating costs�rather�than�the�historical�arrangement�

whereby� the� monthly� charge� was� based� on� enterprise� value.� A� once-off�

cancellation�payment�of�R197,4�million�was�paid�in�September�2010.

PI� holders� will� benefit� from� a� more� effective� cost� structure� as� the� new�

arrangement�will�be�tangibly�earnings enhancing�from�the�first�year.

Simultaneously,�the�Trust�Deed�was�changed�to�allow�the�Fund�to�invest�in�a�

broader class of assets�and�to�increase the gearing limit from�the�

current�limit�of�30%�to�40%�of�the�value�of�its�underlying�assets.

The� changes� were� overwhelmingly� positively� received� with� between� 94%�

and� 98%� of� eligible� PI� holders� who� responded,� voting� in� favour� of� the�

amendments.

Page 2

Annual Report 2010 Emira Property Fund

Major achievements

Amending the management structure to unlock benefits for all

Geographic diversification provides further balance to portfolioIn� May� 2010� the� Fund� acquired� an� effective� 6,4%� interest� in� Growthpoint�

Properties� Australia� (GOZ)� for� a� total� consideration� of� A$18,0� million�

(R116,9 million).�

The�investment�represents�Emira’s�first�investment�in�an�offshore�jurisdiction.�

It�was�motivated�by�the�opportunity�to�diversify�the�portfolio�by�acquiring�a�

small,�passive�stake�in�a�high�quality�listed�Australian�REIT.�GOZ�is�backed�by�

extremely�secure,� long-term�leases�with�blue-chip�tenants�at�a�higher�yield�

than�that�which�is�achievable�by�buying�South�African�commercial�property.�

FAcTS And FiguRES: gRowThpoinT pRopERTiES AuSTRAliA

• The Trust is listed on the Australian Stock Exchange.

• It beneficially owns interests in 25 industrial properties across Australia,

which are valued at A$756,9 million.

• Of its 25 properties, 23 are single tenanted and two are dual tenant

properties.

• Quality tenants, including Woolworths, Coles Group and Star Track

Express, represent more than 75% of overall rental streams.

• The Trust has a total lettable area of 731 798 m2 and its average lease

expiry is 10,6 years.

• The properties are located in Victoria (44%), Queensland (22%), Western

Australia (14%), New South Wales (11%) and South Australia (9%).

The�transaction�will�be�earnings�enhancing�from�the�date�of�purchase.

In�August�2010,�GOZ�announced�the�acquisition�of�seven�direct�properties�

for�a� total�consideration�of�A$171,5�million�with�some�A$101 million�being�

funded� by� a� rights� offer� and� the� balance� from� existing� syndicated� debt�

facilities.� Emira� subscribed� for� A$17,5� million� (R117,3� million)� of� additional�

stapled�securities�bringing�its�total�holding�to�9,1%�of�GOZ.

Page 3

Annual Report 2010 Emira Property Fund

Northcorp Boulevard, Broadmeadows, Victoria, Australia

Sharps Road, Tullamarine, Melbourne, Australia

Continued active asset management to enhance property portfolio

The�Fund�extended�its�track�record�of�investing�to�enhance�the�quality�of�its�

property�portfolio�in�2010,�as�has�been�the�case�in�recent�years.

During�the�past�three�years,�the�Fund�has:

• Acquired 10 properties with a total value of R394,9 million;

• Invested R88,6 million in upgrading eight office properties;

• Refurbished and extended 14 shopping centres with a capital value of

R358,1 million;

• Spent R21,4 million on enhancing two industrial properties; and

• Disposed of 12 non-core buildings for a total consideration

of R258,5 million and four sectional title units worth R9,0 million.

FAcTS And FiguRES: pRopERTy invESTMEnTS in 2010

• Two new properties were purchased for R98,0 million, being a single

tenanted industrial warehouse let to Taylor Blinds and a 50% undivided

share in a multi-tenanted office and retail building located at 80 Strand

Street in the Cape Town CBD.

• Capital investments of some R181,4 million to refurbish and extend

12 properties were completed and ongoing. Seven projects are ongoing

at year-end including a R126,2 million refurbishment and extension of

Randridge Mall.

• The board approved two projects to demolish and rebuild prime office

space to the order of R291,8 million at Podium House in Menlyn, Pretoria

and FNB Heerengracht in the Cape Town CBD which will commence

once a predetermined level of pre-letting has been achieved.�

Page 4

Annual Report 2010 Emira Property Fund

Randridge Mall

Rigel Park

Page 5

Annual Report 2010 Emira Property Fund

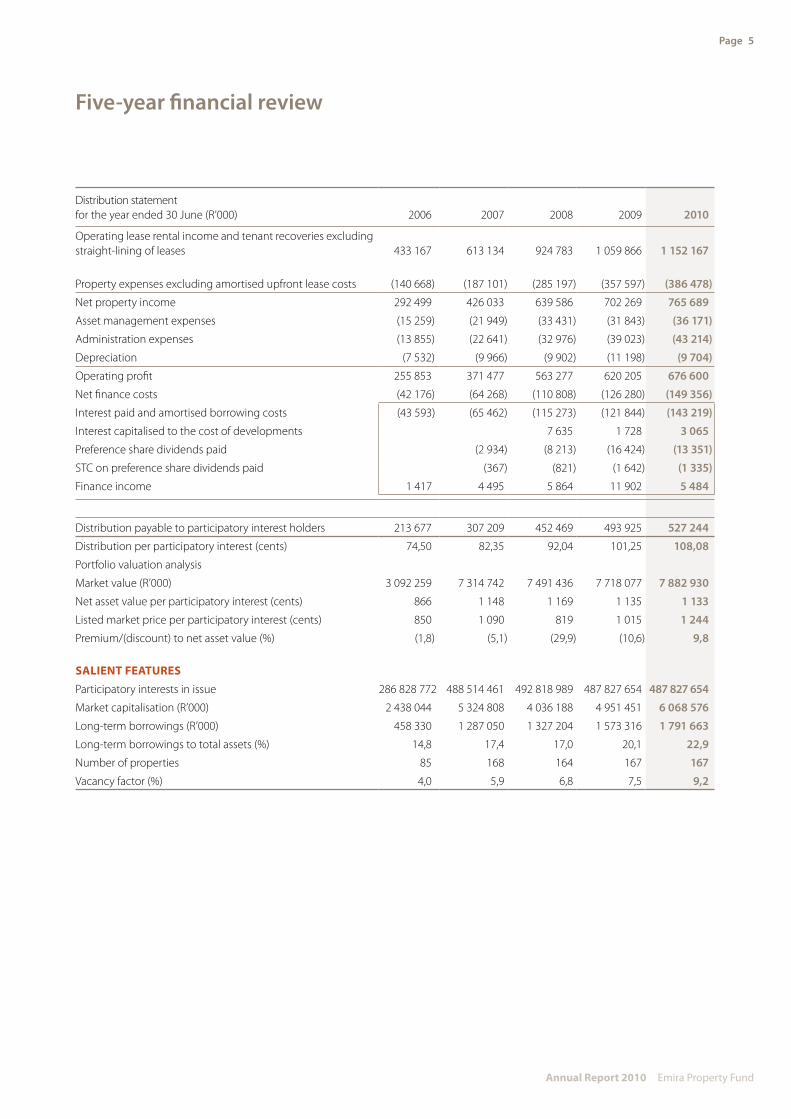

Five-year financial review

Distribution statement for the year ended 30 June (R’000) 2006 2007 2008 2009 2010

Operating lease rental income and tenant recoveries excluding straight-lining of leases 433 167 613 134 924 783 1 059 866 1 152 167

Property expenses excluding amortised upfront lease costs (140 668) (187 101) (285 197) (357 597) (386 478)

Net property income 292 499 426 033 639 586 702 269 765 689

Asset management expenses (15 259) (21 949) (33 431) (31 843) (36 171)

Administration expenses (13 855) (22 641) (32 976) (39 023) (43 214)

Depreciation (7 532) (9 966) (9 902) (11 198) (9 704)

Operating profit 255 853 371 477 563 277 620 205 676 600

Net finance costs (42 176) (64 268) (110 808) (126 280) (149 356)

Interest paid and amortised borrowing costs (43 593) (65 462) (115 273) (121 844) (143 219)

Interest capitalised to the cost of developments 7 635 1 728 3 065

Preference share dividends paid (2 934) (8 213) (16 424) (13 351)

STC on preference share dividends paid (367) (821) (1 642) (1 335)

Finance income 1 417 4 495 5 864 11 902 5 484

Distribution payable to participatory interest holders 213 677 307 209 452 469 493 925 527 244

Distribution per participatory interest (cents) 74,50 82,35 92,04 101,25 108,08

Portfolio valuation analysis

Market value (R’000) 3 092 259 7 314 742 7 491 436 7 718 077 7 882 930

Net asset value per participatory interest (cents) 866 1 148 1 169 1 135 1 133

Listed market price per participatory interest (cents) 850 1 090 819 1 015 1 244

Premium/(discount) to net asset value (%) (1,8) (5,1) (29,9) (10,6) 9,8

SAlient feAtuReSParticipatory interests in issue 286 828 772 488 514 461 492 818 989 487 827 654 487 827 654

Market capitalisation (R’000) 2 438 044 5 324 808 4 036 188 4 951 451 6 068 576

Long-term borrowings (R’000) 458 330 1 287 050 1 327 204 1 573 316 1 791 663

Long-term borrowings to total assets (%) 14,8 17,4 17,0 20,1 22,9

Number of properties 85 168 164 167 167

Vacancy factor (%) 4,0 5,9 6,8 7,5 9,2

Annual Report 2010 Emira Property Fund

Portfolio of top 10 properties by value o f f i c e , R e tA i l A n d i n d u S t R i A l S e c t o R S

3

54

2

1

1. Wonderpark Shopping Centre RetailLocated in middle-LSM market of Akasia, north-west of Pretoria between the Pretoria CBD and Rosslyn/SoshanguveValue at 30 June 2010: R601,5 million Major tenants:Size: 63 360 m2 Pick n Pay (14 000 m²)Number of tenants: 144 Game (3 992 m²)Average net rentals: R78,32/ m2 Builders Express (3 950 m²) Footcount: 9,2 million p.a. Virgin Active Gym (3 500 m²)

Edgars (3 450 m²) Chevron (3 461 m²)

2. Fuel Group Acsa Park Industrial Located in Jet Park adjacent to OR Tambo International Airport just off the N12 and R21Value at 30 June 2010: R298,4 million Single, triple-net tenant:Size: 59 594 m2 Fuel Logistics GroupNumber of tenants: 1Average net rentals: R45,61/ m2

4. Randridge Mall RetailLocated in Randpark Ridge, just off Beyers Naudé Drive in a primarily residential areaValue at 30 June 2010: R207,8 million Major tenants:Size: 22 624 m2 Pick n Pay (4 470 m²)Number of tenants: 86 Dis-Chem (1 400 m²)Average net rentals: R65,55/ m2 Pep Stores (600 m²)Footcount: Not available due to refurbishments Truworths (412 m²)

5. Hyde Park Lane OfficeLocated in Hyde Park, corner of Jan Smuts Avenue and William Nicol Drive opposite Hyde Park Shopping Centre Value at 30 June 2010: R175,8 million Major tenants:Size: 15 334 m2 Standard Bank (1 900 m²)Number of tenants: 44 Tag Travel (1 073 m²)Average net rentals: R82,23/ m2 Lufthansa (730 m²)

WDB Investment Holdings (723 m²)Willis RE (700 m²)

3. Quagga Centre RetailLocated in Pretoria West, within close proximity to Church Street and the Pretoria CBD Value at 30 June 2010: R258,0 million Major tenants:Size: 29 748 m2 Shoprite Checkers (5 715 m²)Number of tenants: 75 Pick n Pay (4 880 m²)Average net rentals: R72,92/ m2 Woolworths (1 800 m²)Footcount: 4,45 million p.a. First National Bank (1 367 m²)

Absa (1 155 m²)

Page 6

Annual Report 2010 Emira Property Fund

6

7

8

9

10. Braamfontein Centre OfficeLocated near the CBD of Johannesburg, in close proximity to the University of the WitwatersrandValue at 30 June 2010: R121,6 million Major tenants:Size: 20 776 m2 Pick n Pay (2 180 m²)Number of tenants: 65 CTH Legal Admin Trust (1 333 m²)Average net rentals: R57,70/ m2 Centre for the Study of Violence

and Reconciliation (1 210 m²)The Ford Foundation (822 m²)

10

6. Woodmead Office Park OfficeLocated within the Woodmead office node with exposure to the M1 highway Value at 30 June 2010: R163,1 million Major tenants:Size: 17 514 m2 DB Thermal (2 400 m²)Number of tenants: 42 ECI Africa Consulting (1 600 m²)Average net rentals: R59,41/ m2 Mine Health and Safety Council

t/a SIMPROSS (1 440 m²)Cummins SA (691 m²)

7. Lynnridge Mall Retail

Located in Lynnwood Ridge, in the eastern suburbs of Pretoria Value at 30 June 2010: R156,4 million Major tenants:Size: 14 220 m2 Pick n Pay (3 930 m²)Number of tenants: 59 Mr Price Home (1 700 m²)Average net rentals: R106,06/ m2 Absa (1 190 m²)Footcount: 3,26 million p.a. Lion Bridge Hardware (915 m²)

Jimnetts Arts and Crafts (792 m²)Pep Home (556 m²)

8. Faerie Glen Office Park OfficeSituated east of Pretoria close to Menlyn overlooking Atterbury Drive, a short drive from Menlyn Shopping Centre Value at 30 June 2010: R131,2 million Major tenants:Size: 10 324 m2 Softline VIP (5 755 m²)Number of tenants: 10 FirstRand Bank (1 300 m²)Average net rentals: R91,56/ m2 SA Local Government Association (960 m²)

WesBank (600 m²)

9. Southern Sentrum Retail Located between Benade Drive and Charlie Sutton Road in Fichardt Park,

Bloemfontein, south of the CBDValue at 30 June 2010: R125,0 million Major tenants:Size: 21 224 m2 Pick n Pay (13 950 m2)Number of tenants: 59 Shell SA Marketing (1 700 m²)Average net rentals: R49,80/ m2 First National Bank (613 m²)Footcount: 4,37 million p.a. Cash Crusaders (495 m²)

Page 7

Page 8

Annual Report 2010 Emira Property Fund

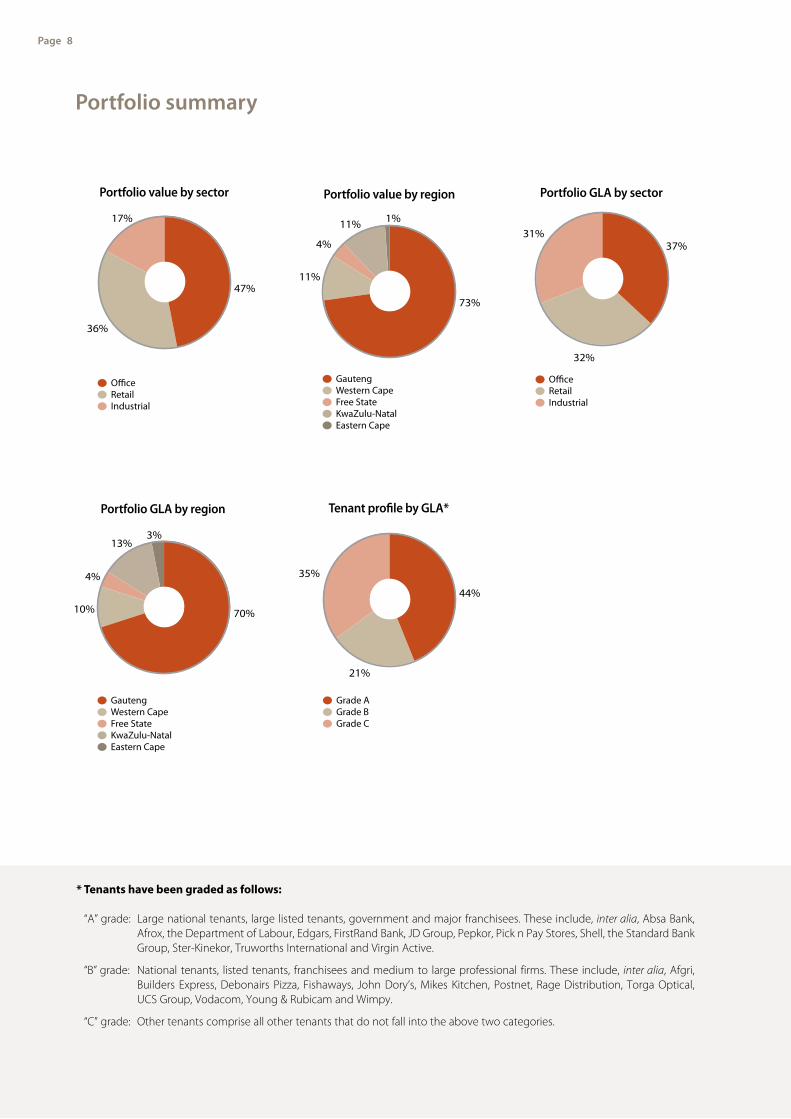

Portfolio summary

* tenants have been graded as follows:

“A” grade: Large national tenants, large listed tenants, government and major franchisees. These include, inter alia, Absa Bank, Afrox, the Department of Labour, Edgars, FirstRand Bank, JD Group, Pepkor, Pick n Pay Stores, Shell, the Standard Bank Group, Ster-Kinekor, Truworths International and Virgin Active.

“B” grade: National tenants, listed tenants, franchisees and medium to large professional firms. These include, inter alia, Afgri, Builders Express, Debonairs Pizza, Fishaways, John Dory’s, Mikes Kitchen, Postnet, Rage Distribution, Torga Optical, UCS Group, Vodacom, Young & Rubicam and Wimpy.

“C” grade: Other tenants comprise all other tenants that do not fall into the above two categories.

Portfolio value by sector

17%

36%

47%

O�ceRetailIndustrial

31%

32%

37%

O�ceRetailIndustrial

31%

32%

37%

O�ceRetailIndustrial

Portfolio GLA by sector

11%

11%

73%

4%

1%

GautengWestern CapeFree StateKwaZulu-NatalEastern Cape

11%

11%

73%

4%

1%

GautengWestern CapeFree StateKwaZulu-NatalEastern Cape

Portfolio value by region

13%

10% 70%

4%

3%

GautengWestern CapeFree StateKwaZulu-NatalEastern Cape

13%

10% 70%

4%

3%

GautengWestern CapeFree StateKwaZulu-NatalEastern Cape

Portfolio GLA by region

35%

21%

44%

Grade AGrade BGrade C

35%

21%

44%

Grade AGrade BGrade C

Tenant profile by GLA*

Page 9

Annual Report 2010 Emira Property Fund

Lease expiry profile (% of GLA)

Lease expiry profile by sector (% of revenue)

Vacancy profile (% of GLA)

Lease expiry profile by sector (% of GLA)

Weighted average lease escalation (%)

Vacancy profile by sector (% of GLA)

9,2

28,2

15,3

11,8

Year 5+

Year 3

Year 4

Year 2

Year 1

Vacant

18,6

16,9

■ O�ce ■ Retail ■ Industrial

16,1 9,7 4,6

10,6 7,0 2,9

16,9 7,2 2,9

3,0 2,13,5

3,5 3,26,8Year 5+

Year 3

Year 4

Year 2

Year 1

8,6

9,2

9,2

9,0

June 2010

March 2010

December 2009

September 2009

June 2009 7,5

■ O�ce ■ Retail ■ Industrial

5,9 1,7 1,6

12,2 7,2 8,8

7,5 5,5 5,6

6,5 5,2 5,2

2,1 3,8 5,9

2,7 7,9 4,7Year 5+

Year 3

Year 4

Year 2

15,3

11,8

16,9

18,6

28,2

9,2

Year 1

Vacant

■ O�ce ■ Retail ■ Industrial

9,3

Industrial

Retail

O�ce

8,0

8,9

5,1

5,5

■ O�ce ■ Retail ■ Industrial

5,0

4,8

5,9

4,9

5,3

14,7

15,3

16,2

15,8

5,3

5,2

3,0

June 2010

March 2010

December 2009

September 2009

June 2009 13,6

5,1

5,5

Page 10

Annual Report 2010 Emira Property Fund

Chief Executive Officer’s message

The directors of STREM (“the Manager”) are pleased to present their report on Emira’s performance for the year ended 30 June 2010.

cHief eXecutiVe officeR’S MeSSAGeBusiness environmentThe financial year was characterised by two very distinct halves. In the six months to December 2009, the market was uncertain and tenants operated under highly challenging conditions, resulting in pressure on rentals. The South African economy came out of recession early in 2010, which provided some relief to tenants in the second half of the financial year.

As the economic climate in South Africa and globally improved, Emira observed definite signs of recovery in the domestic property market, but progress has been slower than anticipated.

Although the South African consumer remains highly indebted, lower interest rates and the end of the domestic recession led to some improvement in consumer sentiment in the second half of the financial year when new vehicle sales, a leading indicator of the economy, showed a strong turnaround. Following the uptick in economic activity during the first quarter of the calendar year,

Admiral House

Granada Square

R527,2 millionDistributable income

108,08 cents + 6,8% Distribution per participatory interest (PI)

1 133 cents Net asset value per PI

+ 32,8% 12-month total return

questions arose with regard to the fundamentals for global

economic growth once stimulus packages in developed

economies come to an end. Accordingly, economists’ trimmed

their local GDP growth expectations, now ranging between 2%

and 3%.

On the downside, the market has been highly sensitised to

negative newsflow and the Greek credit crisis which started in

March 2010 unleashed concerns that the global economy could

revert back into recession, with a resultant contagion in global

equity and bond markets.

Rental arrears, a lagging indicator of economic activity, continued

to increase. At the same time vacancies took time to respond to

the improved economy as tenants waited for confirmation of

sustainable economic recovery before committing to additional

rental space. These have now stabilised with letting interest

improving since December 2009.

The tighter credit environment has been associated with higher

debt margins which in turn led to more demanding return

requirements on new investments, be they improvements to

existing properties or acquisitions of new buildings. As a result,

the occurrence of feasible brownfields projects has slowed,

especially given the current downward rental pressures. In the

wake of limited building opportunities, contractors slashed their

prices to support waning utilisation levels. In evaluating the

feasibility of new projects, this dampened some of the impact

from lower rentals when evaluating returns on potential new

projects. Unrealistic expectations of sellers have also made

acquisitions difficult.

A benefit of the tighter property market has been a marked

reduction in speculative activity and a slower rate of new

development. This has stemmed the risk of oversupply from new properties as the number of developers with the financial wherewithal to commit to new investments

Page 11

Annual Report 2010 Emira Property Fund

declined substantially. Accordingly, the supply and demand dynamics are now more balanced.

By way of evidence, the real growth of investment by value in non-residential property moderated to 1,9% in 2009, compared to 7,8% in 2008 and was flat in the second half of the financial year. The number of square metres approved for new non-residential construction fell by 35,8% year on year in the first quarter of 2010 although activity in the renovations segment increased.

Retailer and wholesaler confidence improved during the first quarter of 2010. Retailer confidence rose from 41 to 51 index points (RMB/BER Business Confidence) due to a stabilising labour market, lower interest rates and better affordability while wholesaler confidence jumped from 27 to 50 index points. This provides further evidence of improving market conditions.

PerformanceEmira once again delivered a solid performance despite the tighter prevailing market conditions. The more stable operating environment which emerged in the second half underpinned the Fund’s performance for the full year. It continued to deliver against its strategic objectives, investing to enhance the quality of its portfolio, however the availability of value accretive opportunities was lower than in previous years.

The Fund delivered 6,8% growth in distributions per participatory interest (PI) which amounted to 108,08 cents as it reaped the rewards of consistent year-on-year progress towards its strategic objectives. The management team’s conservative yet consistent and proactive approach to managing the portfolio over the long term is clearly reflected in these results.

Revenue from operating lease rentals and tenant recoveries increased 8,7% to R1,2 billion (2009: R1,1 billion). Net income from property rental operations showed a 9% increase to R765,7 million because of good cost control.

Net asset value per PI remained virtually stable at 1 133 cents from 1 135 cents. It was impacted by a marginal reduction in the fair value of derivative financial instruments amounting to R63,8 million. Excluding the provision for deferred tax, net asset value per PI declined by 4% from 1 232 cents to 1 186 cents.

The price of Emira PIs on the JSE Limited continued its strong performance, increasing by 23% to 1 244 cents at 30 June 2010 from 1 015 cents the previous year. This compares favourably to a return of 19% on the listed property sector. Emira’s closing price at year-end reflected a premium of 10% to its net asset value of 1 133 cents per PI. The PIs reached a maximum level of 1 270 cents on 3 April 2010, recovering from a low of 980 cents on 3 July 2009. The total returns of PIs

diStRiBution StAteMent

for the year ended 30 June 2010

R’000 2009 2010%

change

Operating lease rental income and tenant recoveries excluding straight-lining of leases 1 059 866 1 152 167 8,7

Property expenses excluding amortised upfront lease costs (357 597) (386 478) 8,1

Net property income 702 269 765 689 9,0

Asset management expenses (31 843) (36 171) 13,6

Administration expenses (39 023) (43 214) 10,7

Depreciation (11 198) (9 704) (13,3)

Net finance costs (126 280) (149 356) 18,3

Interest paid and amortised borrowing costs (121 844) (143 219) 17,5

Interest capitalised to the cost of developments 1 728 3 065 77,4

Preference share dividends paid (16 424) (13 351) (18,7)

STC on preference share dividends paid (1 642) (1 335) (18,7)

Finance income 11 902 5 484 (53,9)

distribution payable to participatory interest holders 493 925 527 244

Number of units in issue 487 827 654 487 827 654

distribution per participatory interest (cents) 101,25 108,08 6,8

Page 12

Annual Report 2010 Emira Property Fund

Chief Executive Officer’s message (continued)

were boosted to 33% with the payment of distributions amounting to 104,3 cents which were actually paid to PI holders during the year.

As a result of a rising Emira PI price, the Fund did not engage in any PI buybacks during the year, preserving its capital resources for opportunities to enhance its positioning in terms of its long-term strategic objectives and provide incremental yield improvements.

The challenging environment in the first half of the year led to pressure on rentals and rising vacancies which increased from 7,5% in June 2009 to 9,2% in December 2009. The market improved in the second half of the year buoying Emira’s performance for this period, as evidenced by the stabilisation in vacancies.

Emira came under less pressure on rental negotiations to secure tenants in areas of high demand during the second half of the financial year. However in secondary nodes, the Fund became more amenable to negotiating more favourable terms in order to retain tenants and let vacant space, thus sustaining the growth of its long-term distributions. Accordingly, the rental reversions of the Fund on renewals and new leases combined slowed to an increase of 3,2% from 6,8% in 2009.

Emira continued to pursue projects to enhance the overall quality of its property portfolio, but opportunities meeting its return requirements were less prevalent than in previous years. However, the Fund continually evaluates prospects and proceeded with the following projects during the year:• The Fund acquired two new properties for a total consideration

of R98,0 million. Taylor Blinds, which was purchased for R36,0 million on a forward yield of 10,8%, was transferred in September 2009. The Fund also purchased a 50% undivided share in a multi-tenanted office and retail building located at

80 Strand Street in the Cape Town CBD with a GLA of 12 500 m2. Major tenants include De Vries Inc, CK Friedlander and Medway Holdings. Its share of the purchase price was R62,0 million on a forward yield of 10,4%. Transfer was pending at year-end.

• The Fund completed projects to the value of some R20,0 million to enhance the quality of five properties. Extensions were carried out for existing blue-chip and long-standing tenants at Southern Sentrum, Wonderpark Shopping Centre, Ingwavuma Shopping Centre, One Highveld and the creation of additional parking at Tuinhof in Centurion.

• Progress is underway on seven projects valued at approximately R161,4 million. These include a R126,2 million refurbishment and extension of Randridge Mall to accommodate additional national tenants. A R14,7 million project was initiated at Rigel Park after the previous tenant vacated the property. A general upgrade valued at R11,0 million is in progress at WesBank House in the Cape Town CBD to capitalise on higher rentals. The Market Square Shopping Centre in Plettenberg Bay is being extended to accommodate additional space for Woolworths, at a cost of R4,0 million.

• The board approved two projects comprising the complete demolition of the existing building and reconstruction of 15 600 m2 of prime office space at Podium House in Menlyn, Pretoria (R255,6 million) and the refurbishment of 6 745 m2 of office space at FNB Heerengracht in the Cape Town CBD (R36,2 million). However, in line with the Fund’s conservative investment philosophy, these projects will not commence until a predetermined level of pre-letting has been achieved. Marketing of the space continues and, although letting has been slower than expected, the Manager is confident that given the buildings’ exceptional locations and attractive rental levels, tenants will be secured.

• The disposal of non-core buildings continued during the period, with three sectionalised units at Georgian Place being transferred out of the Fund as well as Rinaldo Park, a small industrial unit located in KwaZulu-Natal. Four buildings,

Lincoln Wood Office Park

Bradenham Hall

Page 13

Annual Report 2010 Emira Property Fund

namely Nampak, Howick Gardens, QD House and Standard Bank, Glenwood were sold for R62,8 million and all with the exception of the Nampak Building were transferred out of the Fund after year-end. A total of nine non-core properties with a total value of R288,9 million remain on the disposal list.

• In May 2010 the Fund acquired 10,25 million stapled securities* or an effective 6,4% interest in Growthpoint Properties Australia (GOZ) for a total consideration of A$18,0 million (R116,9 million). This represents Emira’s first investment in an offshore jurisdiction and was motivated by the opportunity to diversify the portfolio by acquiring a small, passive stake in a high quality listed Australian REIT, backed by extremely secure, long-term leases with blue-chip tenants at a yield higher than that which is achievable by buying South African commercial property. It has a high quality portfolio consisting of 25 properties which are mainly situated in Brisbane and Melbourne, with a few properties in Perth and Sydney. The transaction will be earnings enhancing from the date of purchase.

* A stapled security is security that is contractually bound to one or more other securities to form a single saleable unit.

The long-term debt facility which Emira secured from Rand Merchant Bank in the previous year continued to provide the Fund with a relative advantage in the current market, especially against the context of higher prevailing lending margins. These have settled at lower levels of between 160 and 170 basis points, compared to 200 basis points at the peak of the economic crisis.

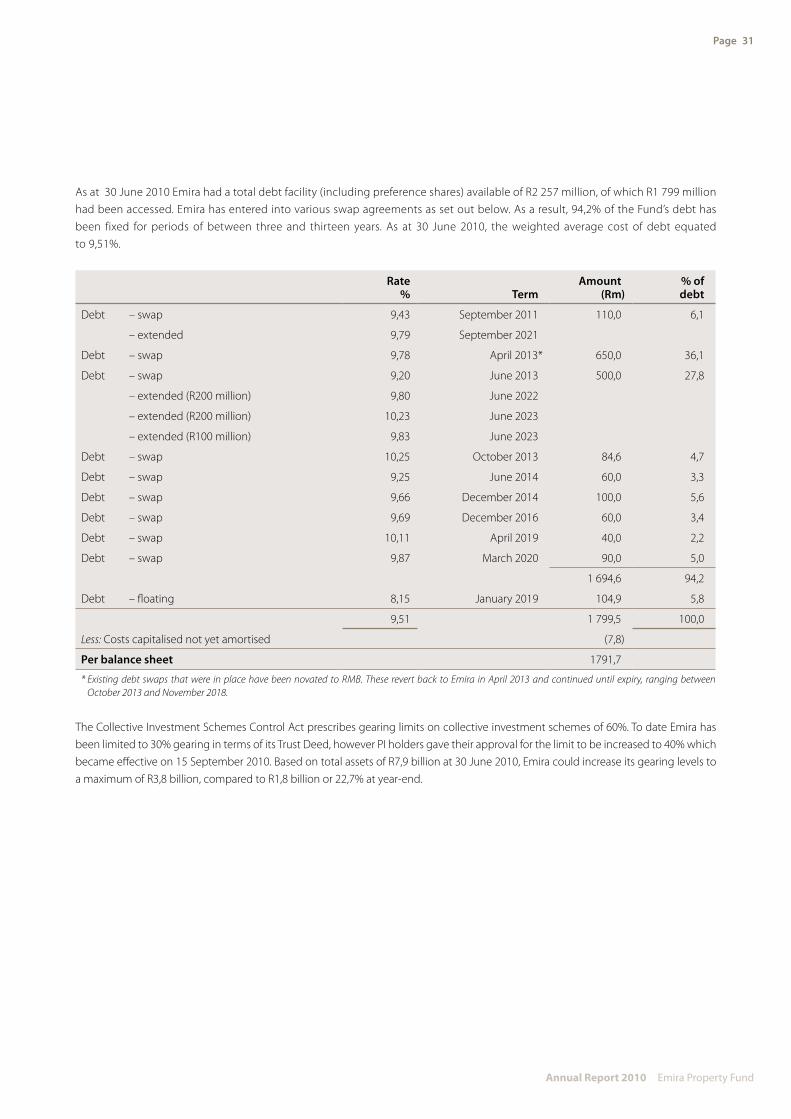

As at June 2010 Emira had a total debt facility (including preference shares) available of R2 257 million, of which R1 799 million had been accessed. Of the Fund’s total debt, 94,2% has been fixed for periods of between three and thirteen years. At 30 June 2010, the weighted average cost of debt equated to 9,51% and the Fund’s overall gearing level increased

marginally to 22,7% from 20,4% in 2009, in line with its strategic objectives.

PoSt yeAR-end eVentSAfter year-end, Emira announced a proposed amendment to its management fee structure, becoming the first Collective Investment Scheme in Property (CISP) on the JSE Limited to do so. Emira and the Manager, Strategic Real Estate Managers (STREM), agreed to amend the terms of its service charge arrangement to a monthly fee based on STREM’s actual operating costs as announced to PI holders on 14 July 2010. The change in management fee structure will result in the calculation of the existing service charge arrangement changing from a monthly charge based on enterprise value to a monthly charge equal to the actual operating costs incurred by the Manager in administering the Fund and a once-off cancellation payment of R197,4 million to the Manager.

The Manager and the Trustee agreed to enter into supplemental deeds to amend the Trust Deed and approval was received from the regulatory authorities with effect from 15 September 2010. The Trust Deed was also amended to allow the Fund to invest in a broader class of assets and to increase the limit of borrowing by the Emira Property Scheme from the current limit of 30% to 40% of the value of its underlying assets.

In August 2010, GOZ announced the acquisition of seven direct properties comprising two office buildings, a car park and four industrial properties for a total price of A$171,5 million at a weighted average yield of 8,4%. The

Highway Business Park

Brandwag

The Tramshed

Page 14

Annual Report 2010 Emira Property Fund

Chief Executive Officer’s message (continued)

acquisition will diversify the 100% industrial portfolio of GOZ into the office sector. The properties are located in the attractive Brisbane property market in Queensland with quality tenants and good lease covenants. The acquisition will be funded by a 1-for-3 pro rata renounceable rights offer at A$1,90 per stapled security, providing approximately A$101 million, and the balance from existing syndicated debt facilities. Emira has subscribed for A$17,5 million (R117,3 million) worth of additional stapled securities bringing its total holding to 9,1% of GOZ.

The Fund also purchased a 50% undivided share in a multi-tenanted office and retail building located at 80 Strand Street in the Cape Town CBD with a GLA of 12 500 m2. Transfer into Emira had not taken place at time of going to print.

The transfer of Howick Gardens, QD House and Standard Bank, Glenwood which were disposed of during the year, took place after year-end.

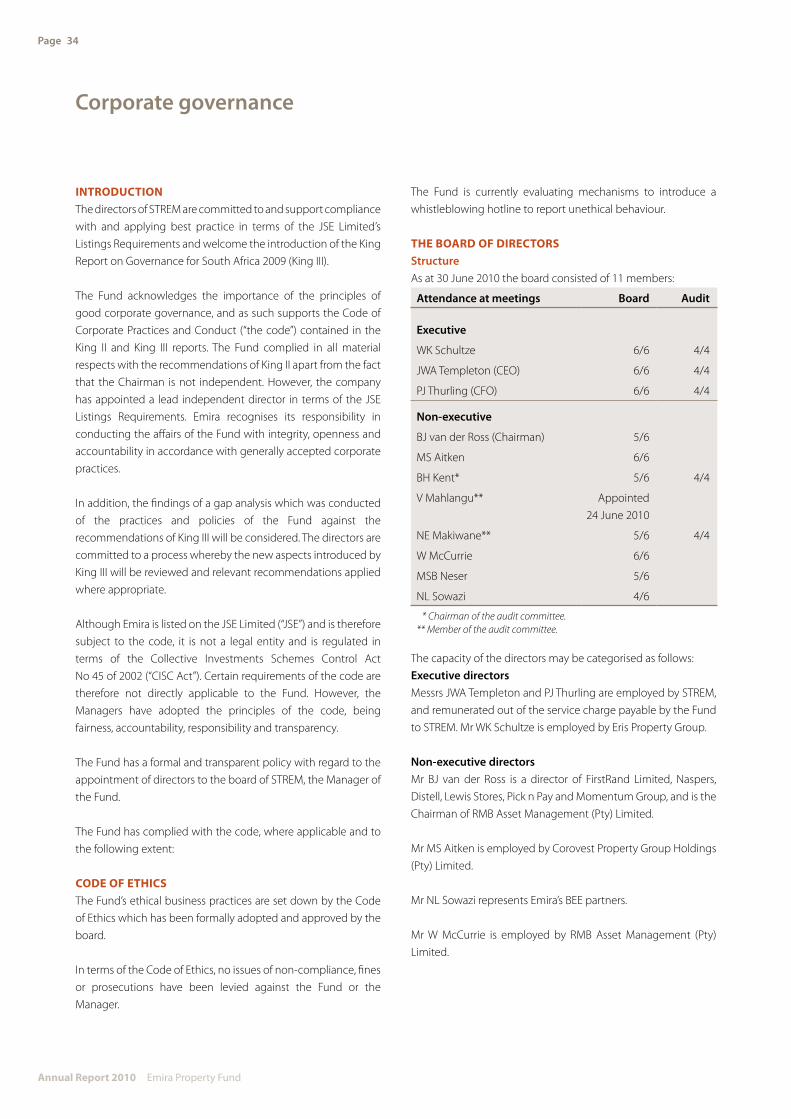

BoARd of diRectoRSMr BH Kent, an independent non-executive director of STREM since April 2007, was appointed as lead independent director on 20 May 2010.

On 24 June 2010, Mr V Mahlangu was appointed to the board of STREM as an independent non-executive director. Mr Mahlangu qualified as a chemical engineer at UCT and has an MBA from Harvard. He has extensive experience in structured finance and investment banking, as well as mezzanine funding and currently manages his own investment company. Mr Mahlangu was also appointed to the audit committee.

Prospects and outlookDuring the year under review, Emira has been highly proactive in initiating positive changes to ensure the Fund’s ability to deliver long-term benefits to PI holders and to continue delivering on its strategic objectives.

Not only was it one of the first JSE-listed CISPs to diversify its assets by investing offshore, but it is also the pioneer in effectively restructuring the fee payable to its Manager, both of which hold significant potential to provide value for PI holders. Over and above the cost benefits for PI holders, the new structure will also result in the greater alignment of the interests of the management company, while creating a vehicle to incentivise management and staff, which was not possible under the previous structure. In line with its strategic objectives, the Fund once again delivered above average growth in distributions as the underlying portfolios continued to perform well.

In the year ahead, the portfolio is positioned to continue showing good growth in distributions underpinned by its diversified pool of long-term tenants and contractual escalations. While the economic recovery has been confirmed with several consecutive quarters of GDP growth, the recent Eskom price hikes and future escalation rates are certain to limit the affordability of higher rentals and curtail tenants’ propensity to commit to new leases.

Throughout its office, retail and industrial property portfolio, Emira has a good pipeline of capital projects to continue improving the quality of its asset base. The board has approved several projects which the Fund will initiate once it has achieved the requisite levels of pre-letting.

Page 15

Annual Report 2010 Emira Property Fund

PeRfoRMAnceSouth African listed property sectorTotal returns to June 2010The overall equity markets, which had trended strongly up since early in 2009, corrected sharply after the Greek credit crisis which started in 2010 and sent global and domestic equities into a correction.

The JSE All Share Index and the JSE FINDI 30 Index showed total returns of 21,5% and 22,7% respectively for the 12 months ended 30 June 2010. However, in the fourth quarter of the financial year, they lost -9,5% and -8,4% respectively. PLSs and PUTs continued to perform well despite the volatility which affected the general equity markets in the fourth quarter, with an annualised return of 26,5% and 27,3% respectively over the same time horizon.

Compound annual total returns to 30 June 2010 (pretax) (%)

PeriodAll

Share FINDI 30 PLSs PUTs R153

1 year 21,5 22,7 26,5 27,3 7,43 year 0,6 1,9 8,5 7,1 6,55 year 14,8 13,4 17,2 12,2 5,510 year 14,0 9,8 17,4 14,6 8,3

Source: Inet-Bridge

The listed property sector and bond yield differentialThe listed property sector continued to perform well although its performance lagged general equities until December 2009. However with the European credit issues in April 2010, investors sought out the relative security of the listed property sector which showed a strong outperformance compared to general equities. Indications that domestically the market is moving towards a low inflation environment have also been positive for long bond and property yields. The capital growth of the listed property sector for the year ended 30 June 2010 was in line with the previous year at 19,1%. Most South African listed property funds continued to show positive distribution growth albeit at a slower pace during the period under review, as a result of more challenging conditions in the local property sector.

Over the 12 months ended 30 June 2010, the yield differential between the historic listed property yield and the R153 traded in a narrow band ranging from 0,25% to -0,25%, indicating that market expectations for growth were positive but not at levels experienced in recent years.

0,0135

0,0130

0,0125

0,0120

0,0115

0,0110

South African listed Property Index relative to All Share Index

Source: Inet-Bridge

Jul 09 Aug 09 Sep 09 Oct 09 Nov 09 Dec 09 Feb 10Jan 10 Mar 10 Apr 10 May 10 Jun 10

3,5

2,5

1,5

0,5

-0,5

-1,5

-2,5

16

15

14

13

12

11

10

9

8

7

R157 and yield di�erential (%)*

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Inet-Bridge

Di�erential Long bond (R157)

* South African listed property yield less the R157 yield.

Manager’s report

South African listed Property Index

South African listed Property Index relative to All Share Index

R157 and yield differential (%)*

360

350

340

330

320

310

300

290

280

270

Source: Inet-Bridge

Jul 09 Aug 09 Sep 09 Oct 09 Nov 09 Dec 09 Feb 10Jan 10 Mar 10 Apr 10 May 10 Jun 10

Page 16

Annual Report 2010 Emira Property Fund

Manager’s report (continued)

Physical property marketIn 2007, the South African property sector produced the highest returns of all the countries analysed by the Investment Property Databank (IPD). The UK was already showing signs of a downturn with negative returns, the only country to be doing so. In 2008, South Africa once again showed the strongest returns but according to IPD analyses no countries were experiencing accelerated returns. In 2009 some countries once again started showing higher returns.

There are signs that the global property sector is recovering with the UK, Ireland, Denmark, and Sweden having seen an improvement in returns since 2008 while in South Africa, Australia, New Zealand, Canada, USA, Netherlands and Finland, results are still deteriorating. South Africa remains the strongest performer even though it has been in a slowing trend.

40,0

20,0

0

-20,0

-40,0

Total return % per annum

Sout

h Afric

aNew

Zeala

ndAus

tralia

Norway

Cana

daSw

eden

Polan

dUSA CE

ESp

ainPo

rtuga

lJa

pan

Finlan

dNet

herla

nds

Denm

arkIre

land

Belgi

um Italy

Switz

erlan

dAus

tria

Germ

any UK

Franc

e

Korea

Source: IPD

■ 2007 ■ 2008 ■ 2009

According to the IPD, a synchronised downturn occurred in many property markets around the world because of common factor risks, but the severity varied from country to country, reflecting country-specific risk.

The IPD South Africa Annual Property Index, which measures ungeared total returns in respect of direct property investments, showed that total returns remained in a downward trend in 2009, declining to 8,7% from 12,9% in 2008, and 27,7% the year before. This reflects a 1,6% real return when adjusting for the 2009 CPI metro average of 7,1%.

While income returns across all property sectors have trended down during the last three years, reflecting the rising capital values, they showed signs of stabilising in 2009. The retail sector continued to lead the overall property sector with an income return of 7,9% (reflecting higher capital values) while the office and industrial sectors lagged with income yields of 9,3% and 9,4% respectively.

Long-term leases with contractual escalations of between 8% and 9% are prevalent in South Africa as a result of the relatively high interest rate environment compared to global norms. This has enabled the property sector to continue showing strong returns despite the tight economic conditions in the past two years.

Capital values across all property sectors grew marginally by 0,3% in 2009, showing a further slowdown from the positive returns of 4,2% and 17,6% in 2008 and 2007 respectively. The retail sector recorded positive capital returns of 0,9% (2008: 3,0%) while the value of industrial property declined by -0,6% in 2009 after producing the highest sector capital growth of 8,4% in 2008. In the office sector negative capital returns of -1,2% were recorded (2008: 4,5%). Capital growth, which is a function of property valuation, has been under severe pressure in the past year due to the combined impact of increased vacancies and lower rentals. The overall property market showed a slowing in total return, as a result of capital growth which declined during the year.

Total return % per annum

Annual Report 2010 Emira Property Fund

Page 17

IPD total returns for 2009 (2008) (%) Total

return Income

returnCapitalgrowth

All property 8,7 (12,9) 8,4 (8,5) 0,3 (4,2)Retail 8,8 (11,1) 7,9 (7,9) 0,9 (3,0)Office 8,0 (13,9) 9,3 (9,1) -1,2 (4,5)Industrial 8,7 (18,1) 9,4 (9,1) -0,6 (8,4)Other 11,9 (18,8) 7,8 (10,3) 3,8 (7,8)Source: IPD

Total returns annualised (%)

Period Retail Office IndustrialAll

Property

One year 8,8 8,0 8,7 8,7Three year 15,0 17,1 20,2 16,2Five year 20,8 20,2 25,0 21,0Ten years 18,2 15,0 18,8 17,3Source: IPD

The property market started showing signs of stabilisation as increasing vacancy rates started levelling out towards the end of the financial year. In a market characterised by increasing arrears, rental pressure and higher vacancies, landlords nevertheless need to remain amenable to innovative ways to retain existing tenants and attracting new tenants.

Overall vacancies increased to 7,1% at the end of 2009 (2008: 4,3%) according to the IPD annual survey.

An IPD survey of participants in the South African property market indicates that 75% are expecting that 2010 returns will exceed 2009 levels.

Emira’s performance and property portfolioEmira’s performance and tradability on the JSEReflecting the continued strength of the listed property sector during the year ended 30 June 2010, the price of Emira’s PIs increased by 22,6% to 1 244 cents from 1 015 cents at 30 June 2009. The total return on PIs for the year increases to 32,8% if the total distributions paid during the year, amounting to 104,3 cents are included.

164,8 million PIs traded during the year ended 30 June 2010, representing 33,4% of the weighted average number of PIs.

Performance relative to the IPD indexThe 2009 IPD index survey, which aggregates the capital and income of listed and unlisted portfolios to provide a measure of total annual performance, reported that Emira achieved a total return of 6,1%, an improvement from the 5,6% return in 2009.

At 9,3%, the Fund’s income return was 0,4% higher than the benchmark income return of 8,9% for the period and was accordingly ranked second out of the seven listed property funds constituting the IPD South African Benchmark. As a result of its cautious stance on valuations, the Fund was ranked fifth out of the seven listed funds in the universe using total returns.

Despite the Manager’s conservative approach to property valuations given the current economic climate, the Fund has outperformed the benchmark on a three and five year time horizon:

Total return to 2009 (%)Emira Benchmark

One year 6,1 8,6Three year 15,7 15,6Five year 24,5 21,7Source: IPD

Portfolio exposureAt 30 June 2010, Emira’s portfolio consisted of 167 properties, with a total GLA of 1 217 990 m2, which was valued at R7,9 billion, translating into an average value of R47,2 million per property.

Page 18

Annual Report 2010 Emira Property Fund

Refurbishments and extensionsEmira continued to actively evaluate opportunities to improve the quality of its properties throughout the year. However, given the current environment where tenants’ appetite to pre-commit to the higher rentals associated with upgraded premises or increased rental area has been low, fewer projects have met the Fund’s return threshold requirements.

Emira invested a total of R181,4 million in its property portfolio during the year under review, which was focused predominantly in its office and retail portfolios and includes both ongoing and completed projects. The most substantial project is a refurbishment and extension to the Randridge Mall amounting to R126,2 million, which will be completed in October 2010.

DisposalsAn important component of Emira’s active asset management approach is to continually evaluate properties to ensure that they enhance the overall quality and total value of the property portfolio, contributing to higher returns and thereby improving the Fund’s investor appeal.

At the end of the 2009 financial year, the Manager had 14 non-core properties identified for sale. In 2010, three sectionalised units at Georgian Place were sold for R6,6 million and transferred out of the Fund as well as Rinaldo Park, a small industrial unit located in KwaZulu-Natal which was sold

Manager’s report (continued)

for R6,0 million and transferred in June 2010. The Fund accepted offers for the sale of four properties, two industrial properties being the Nampak Building (Denver, Johannesburg) and QD House (Kyalami); the Howick Gardens Office Park (Midrand) and the Standard Bank retail property in Glenwood (Durban). The properties were sold for a total consideration of R62,8 million and all but the Nampak Building were transferred out of the Fund after year-end.

Nine non-core properties remain on the disposal list, with a total value of R288,9 million.

AcquisitionsAlthough the Fund continued to actively evaluate prospective purchases, prevailing asking prices were not in line with its return threshold. One property was purchased during the year, namely a 50% undivided share in 80 Strand Street a multi-tenanted office building in the Cape Town CBD which has a GLA of 12 500 m2 for R62 million, but was yet to be transferred into Emira at time of going to print.

A single tenanted industrial warehouse in Montague Gardens which is occupied by Taylor Blinds was transferred into Emira in September 2009.

A detailed breakdown of Emira Property Fund’s portfolio is disclosed on pages 85 to 96.

Notes to the financial statements (continued)for the year ended 30 June 2010

Page 19

Annual Report 2010 Emira Property Fund

optimising on an excellent location to upgrade building to A-grade specifications

Value at June 2010: R45,1 m

Gross lettable area: 4 417 m²

o f f i c e

The property:Rigel Park consists of two multi-level, face brick office buildings and parking facilities. It was developed in the late 1980s for the Financial Services Board and has a total lettable area of 4 417m². The Financial Services Board relocated to new premises in November 2009.

The property is well located next to the improved Rigel Road/N1 intersection and is highly visible from the adjacent routes and the highway. In its previous state prior to the refurbishment, the building was classified as B-grade which could command gross rentals of R70/m² to R80/m².

The opportunity:An opportunity was identified to upgrade the building into an A-grade property which would attract better quality tenants and higher rentals based on its location close to major access routes and it being less than 5 km from the important Menlyn node.

The upgrade:The board approved a R14,7 million proposal on risk in November 2009 to substantially refurbish the property. The new design included internal upgrades and modernising the facades which are exposed to the national road. The aesthetics of the building were cost effectively updated using a combination of plaster and paint. All brick balconies were replaced with steel balustrades to improve the visual impact of the building and give it a modern finish.

All common areas of the building received a face lift by introducing new floor finishes, ceiling lay-outs, down lighters and wall finishes. All toilet facilities and kitchenettes were renovated and lifts were upgraded, both aesthetically and mechanically.

The updated configuration of the buildings also allowed more flexibility in letting to new tenants as they can either be leased to a single tenant, one tenant per block or the two blocks can be configured to accommodate a maximum of 12 tenants.

The outcome:The renovation was completed subsequent to year-end and the buildings are being marketed at market related rentals of R110/m² to R115/m² gross. Two tenants committed to leases for some 70% of the lettable area in August 2010. The incremental yield on the project is some 12,9%, based on 100% occupancy. The investment enabled the Fund to take full advantage of the location of the Rigel Park office building, upgrading it into an A-grade property which has enhanced its lettability in the current competitive market.

The board’s decision to proceed with the project on risk has been justified by the successful letting of the majority of the office space at budgeted rentals.

office case study: Rigel Park

Page 19

Page 20

Annual Report 2010 Emira Property Fund

Manager’s report (continued)o f f i c e

office MARket conditionSThe fundamentals for the office property segment started turning in

2010 as the financial services industry which represents about one fifth

of South Africa’s GDP and provides a similar proportion of the country’s

non-agricultural formal employment started showing signs of a

rebound. As a major tenant class in the office sector, this had a positive

impact on the sector. Of the eight industries surveyed in SAPOA’s

Property Market Trends Report for 2009 five showed increased turnover,

but mining and quarrying and real estate and other business services

were still in decline.

According to the IPD, office vacancies, which generally lag the

economy, continued to increase during the year, reflecting the highest

vacancy rate in the property sector at 10,6% for 2009 (2008: 7,2%). As a

result of the tighter market, the lower availability of credit and a more

cautious approach, fewer new office developments came to market in

2009 although activity levels have started recovering since the

beginning of 2010.

The oversupply of office space persisted in 2009, although the excess is

lower than in the late 1990s when vacancies increased to more than

20%. Accordingly the recovery, when it takes place, is expected to be

quicker than in the previous cycle.

The main office hubs of Johannesburg and Cape Town have been

worst affected by the current downturn.

Prime grade offices continue to outperform and the volatility of their

returns has been more favourable than the second grade offices over

the last 15 years.

According to the Rode’s Report on the SA Property Market, the overall

growth in office rentals to the end of 2009 was weak and a

decentralisation trend was in evidence. The rental market in Cape Town

and Johannesburg declined by -6% and -4% respectively while Pretoria

and Durban showed growth of 9% and 10% respectively over the same

period.

Revenue of R510,2 million which represents an increase of 5%

Operating profit of R320,0 million showing an increase of 5%

Office portfolio valued at R3,7 billion comprising 47% of the Fund’s total portfolio by value

Dorbyl Parktown

Century Gate

100 on Armstrong

Page 21

Annual Report 2010 Emira Property Fund

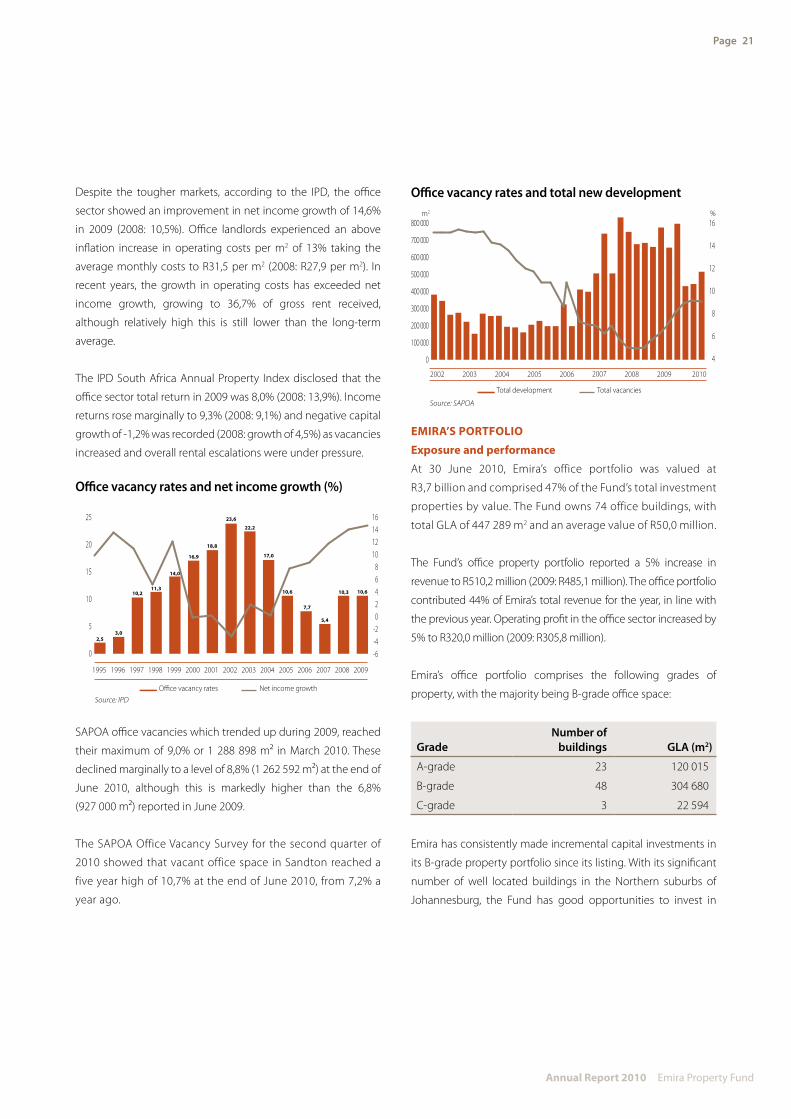

Despite the tougher markets, according to the IPD, the office

sector showed an improvement in net income growth of 14,6%

in 2009 (2008: 10,5%). Office landlords experienced an above

inflation increase in operating costs per m2 of 13% taking the

average monthly costs to R31,5 per m2 (2008: R27,9 per m2). In

recent years, the growth in operating costs has exceeded net

income growth, growing to 36,7% of gross rent received,

although relatively high this is still lower than the long-term

average.

The IPD South Africa Annual Property Index disclosed that the

office sector total return in 2009 was 8,0% (2008: 13,9%). Income

returns rose marginally to 9,3% (2008: 9,1%) and negative capital

growth of -1,2% was recorded (2008: growth of 4,5%) as vacancies

increased and overall rental escalations were under pressure.

25

20

15

10

5

0

16141210

86420

-2-4-6

O�ce vacancy rates and net income growth (%)

200019991997 199819961995 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: IPDO�ce vacancy rates Net income growth

2,53,0

10,211,3

14,0

16,9

18,8

23,6

22,2

17,0

10,6

7,7

5,4

10,3 10,6

SAPOA office vacancies which trended up during 2009, reached

their maximum of 9,0% or 1 288 898 m² in March 2010. These

declined marginally to a level of 8,8% (1 262 592 m²) at the end of

June 2010, although this is markedly higher than the 6,8%

(927 000 m²) reported in June 2009.

The SAPOA Office Vacancy Survey for the second quarter of

2010 showed that vacant office space in Sandton reached a

five year high of 10,7% at the end of June 2010, from 7,2% a

year ago.

800 000

700 000

600 000

500 000

400 000

300 000

200 000

100 000

0

16

14

12

10

8

6

4

O�ce vacancy rates and total new developmentm2 %

2002 2003 2004 2005 2006 20082007 2009 2010

Source: SAPOA

Total development Total vacancies

eMiRA’S PoRtfolio

exposure and performance

At 30 June 2010, Emira’s office portfolio was valued at

R3,7 billion and comprised 47% of the Fund’s total investment

properties by value. The Fund owns 74 office buildings, with

total GLA of 447 289 m2 and an average value of R50,0 million.

The Fund’s office property portfolio reported a 5% increase in

revenue to R510,2 million (2009: R485,1 million). The office portfolio

contributed 44% of Emira’s total revenue for the year, in line with

the previous year. Operating profit in the office sector increased by

5% to R320,0 million (2009: R305,8 million).

Emira’s office portfolio comprises the following grades of

property, with the majority being B-grade office space:

GradeNumber of

buildings GLA (m2)

A-grade 23 120 015

B-grade 48 304 680

C-grade 3 22 594

Emira has consistently made incremental capital investments in

its B-grade property portfolio since its listing. With its significant

number of well located buildings in the Northern suburbs of

Johannesburg, the Fund has good opportunities to invest in

Annual Report 2010 Emira Property Fund

Page 22

order to upgrade and extend these into A-grade office buildings

which command higher rentals and are less impacted by

economic downturns. In addition, B-grade properties which are

centrally located in the Northern suburbs and which have good

access to major arterial routes will increase in value over time.

This has been the case with properties close to Gautrain stations

and along its bus routes. Buildings which cannot be turned

around or generate income which meets the Fund’s required

rate of return, will be earmarked for sale.

While the Fund did not embark on any substantial upgrade

projects in its office portfolio during the year, it obtained board

approval for two refurbishment projects which will commence

once sufficient commitment from new tenants has been

achieved. The properties are Podium House in Menlyn, Pretoria

which will be demolished and completely rebuilt, at a cost of

R255,6 million to build 15 600 m2 of prime office space and FNB

Heerengracht in the Cape Town CBD where a R36,2 million

project will comprise the refurbishment of 6 745 m2 of office

space. Marketing of the space continues and, although letting

has been slower than expected, management is confident that

given the buildings’ exceptional locations and attractive rental

levels, occupancies will be secured.

New parking facilities were completed at the Tuinhof building in

Centurion at a cost of R750 000 with a high incremental yield of

20,0%.

Refurbishments with total investments of R25,7 million were still

in progress at the end of the financial year:

• The R14,7 million refurbishment of the Rigel Park office

building in Pretoria East (see case study on page 19); and

• WesBank House in the Cape Town CBD was being

refurbished at year-end. The installation of more efficient

air conditioning will reduce the operating costs of the

property. The R11,0 million project has an incremental

yield of 11,0% with completion in September 2010.

Vacancies and letting

Emira’s office vacancies increased to 16,2% (2009: 13,6%) in line

with the tighter rental market.

Major office vacancies include the following:

• The FNB Building Heerengracht in the Cape Town CBD is

100% unoccupied as its 6 745m² GLA has been vacated in

anticipation of a refurbishment. The project will commence

once there is sufficient commitment from tenants to take

up space in the completed building. It is currently being

held vacant in anticipation of the project going ahead

in 2011.

• Vacancies at the Hurlingham Office Park (total GLA 16 159 m2)

remain high at 6 264 m2, but space is mainly available in the

refurbished blocks and letting is expected to improve as the

market recovers.

• A major redevelopment is planned at Podium House

(GLA 4 832 m²) which is 100% vacant and marketing is under

way to initiate work on the new building.

• The Rigel Park (GLA 4 417 m²) refurbishment is nearing

completion and two tenants have already committed to

leases on some 70% of the office space.

Prospects and outlook

The fortunes of the office portfolio are linked to the speed of the

domestic recovery. Office vacancies are off their peak of 9,2%,

and fortunately there are no indications that the office sector

could be faced with the vacancies of some 20% which plagued

the sector in the late 1990s and early 2000s. Accordingly, the

uplift and speed of the recovery is expected to be more

favourable this time around. With GDP growth forecasts of

between 2,0% and 3,0% for the next 12 months, there are signs

that vacancies will start trending down, although the recovery is

fragile at this stage.

Continual improvement is essential to sustainable success and

Emira has identified two capital projects which it expects to start

work on in 2011 once sufficient pre-letting is in place to mitigate

the risks.

Manager’s report (continued)o f f i c e

Annual Report 2010 Emira Property Fund

Page 23

M A j o R t e n A n t S• Pick n Pay• Dis-Chem• Pep Stores• Foschini Group• Ackermans• Mr Price • Truworths• Woolworths

Value at June 2010: R207,8 m

Gross lettable area: 22 624 m²

Weighted average rental/ m2: R65,28

The property:Randridge Mall is located in the Western suburbs of Johannesburg and was built in 1983 with a GLA of 18 957 m2. Its national tenants include Pick n Pay (4 500 m2), Woolworths (2 140 m2) and Dis-Chem (1 400 m2) among others. The centre was acquired by Emira in 2003 as part of its original listing.

The opportunity:In order to capitalise on the current trend among retailers to increase the size of successful stores instead of opening new stores which is seen as more risky, the Manager embarked on an extension of the Randridge Mall. The feasibility of the project was backed by strong tenant demand. The centre also had demand for space from new national retail tenants which enhanced the feasibility of the project.

The upgrade:The board approved a R126,2 million refurbishment and extension of the mall with a projected yield of 9,4% in August 2009.

The project was split into two phases to minimise disruption and income loss.

Certain tenants were relocated to more suitable positions which also allowed for the enlargement of several larger tenants’ stores. At the same time, floor tiles, ceilings and air conditioners were upgraded to give the centre a more modern atmosphere. An external addition was built onto the existing centre into the parking area to accommodate new tenants, adding 3 667 m² in rentable space and bringing the total GLA to 22 624 m². Foschini Group has taken up 1 700 m2 to open several new branded stores in the centre, while Woolworths has committed to an extension of trading area measuring some 500 m2.

Both Pick n Pay and Dis-Chem have refurbished their stores.

The outcome:The upgrade and extension has rejuvenated the centre while renewing its ability to attract better quality tenants such as the Foschini Group. It has also secured the ongoing commitment of existing nationals such as Truworths, Woolworths, Ackermans and Mr Price.

Historically 48% of the retail area has been rented to national tenants, but this is set to increase to 79% once the project has been completed.

The upgrade has ensured that the Randridge Mall is a compelling destination in the face of increasing competition from more recently developed centres in the area.

Cost savings have been realised on the project, which will increase the yield to Emira PI holders.

R e tA i l

capitalising on existing anchor tenants and central location to enhance return

Retail case study:Randridge Mall

Page 23

Annual Report 2010 Emira Property Fund

Page 24

Manager’s report (continued)R e tA i l

RetAil MARket conditionS There are indications of good news in the retail sector which had led the downward cycle. South Africa’s retail sales recorded its sixth consecutive month of improvement in June 2010, reflecting a year-on- year increase of 7,4% compared to a year ago although the impact of the 2010 FIFA Soccer World CupTM was lower than anticipated. Recent retail sales data suggests a gradual improvement in consumption. This is a key contributor to the economy but has lagged the rest of the economy’s recovery. Consumer spending remains under pressure due to high levels of household debt and unemployment.

Performance has been mixed across the sector. Shopping centres targeted at higher and very low income brackets are performing well but centres targeted at middle income consumers are under more pressure in line with their target market’s limited discretionary income and higher levels of personal debt. Accordingly the rate of rental growth has also varied from one centre to another. Foot traffic is stable with some improvement in places.

During 2009, the retail sector, traditionally the least volatile commercial property category, continued to be the most resilient class, with an annual total return of 8,8% (2008: 11,1%) according to the IPD South Africa Annual Property Index.

The retail sector reported an income return of 7,9% (2008: 7,9%) which was the lowest of the three property classes (reflecting higher capital value). Retail property was the only category to show a positive capital growth of 0,9% (2008: 3,0%).

Retailers are faced with increasing operating costs, especially with the recent electricity tariff hikes. Landlords are finding it difficult to pass all of these increases on to tenants. According to SAPOA, operating costs have reflected a 27,6% year-on-year increase per square metre to R49,3 per m2 (2008: R38,7 per m2). These account for 41,7% of average gross rental received which is the highest recorded level by SAPOA in the history of its index.

Revenue of R463,8 million which represents an increase of 9%

Operating profit of R266,5 million showing an increase of 3%

Retail portfolio valued at R2,9 billion comprising 36% of the Fund’s total portfolio by value

Epsom Downs Shopping Centre

Dundee Boulevard

Market Square

Annual Report 2010 Emira Property Fund

7

6

5

4

3

2

1

0

25

20

15

10

5

0

-5

Retail vacancy rates and net income growth (%)

200019991998199719961995 2001 2002 2003 2004 2005 2006 2007 2008 2009

0,40,6

2,3

2,9

4,3

5,2

6,26,5

5,9

4,6

3,83,5

2,3

3,6

4,8

Source: IPDRetail vacancy rates Net income growth

The organisation further reports that in 2009 retail centres in the traditional economic hubs of the country produced the lowest retail returns, while the smaller provincial markets performed at a higher level. This could be attributable to a slight lag in smaller regional markets compared to the overall national economy. Emira has evidenced this trend with its portfolio of small regional shopping centres which once again reported good rental growth with low vacancies and minimal arrears. Spending in rural areas has been buoyed by the proportion of consumers benefiting from government grants.

The IPD reported that industry wide vacancies in the retail sector increased to 4,8% in 2009 from 3,6% in the previous year and in line with the constrained consumer spending environment.

eMiRA’S PoRtfolioexposure and performanceAt 30 June 2010, Emira’s retail portfolio was valued at R2,9 billion and comprised 36% of the Fund’s total investment properties by value. The Fund owns 42 shopping centres, with total GLA of 384 640 m2 and an average value of R67,8 million.

The Fund’s retail property portfolio delivered a 9% increase in revenue to R463,8 million (2009: R423,8 million). The retail portfolio contributed 40% of Emira’s total revenue for the year, in line with 2009. The retail sector produced a 3% increase in operating profit of R266,5 million (2009: R258,1 million).

Emira invested R149,8 million to improve the quality of six shopping centres in its retail portfolio during the year, which

includes one major refurbishment and several other smaller projects:• An investment of R126,6 million at the Randridge Mall which

will be completed in October 2010 (see case study on page 23). • Extensions to the Market Square Shopping Centre in

Plettenberg Bay to accommodate a Woolworths store valued at R4,0 million which were still in progress at year-end.

• A 950 m2 extension at the Southern Sentrum in Bloemfontein valued at R14,9 million which was completed in May 2010.

Vacancies and lettingEmira’s retail vacancies increased marginally to 5,3% at 30 June 2010 (2009: 5,0%), confirming that the retail sector is showing signs of stabilising as the consumer outlook slowly improves. Major retail vacancies include the following:• The Montana Value Centre which has vacancies measuring

4 507 m² as it has been affected by the tight consumer environment in the middle income bracket resulting in slow uptake of the 12 retail units currently available. The centre is well placed to benefit from improving retail sales with its location in a growing residential hub.

• Cresta Corner has vacant space measuring 2 574 m² with six retail units vacant as well as office space. Subsequent to year-end, Emira agreed to redevelop the building and construct a new motor dealership for Audi Northcliff.

• Vacancies increased to 2 206 m² at the WorldWear Fashion Mall and the Manager continues to explore all avenues to improve the take-up of space.

• The Manager continues to negotiate with tenants to take up the 1 809 m² of available space at Gift Acres.

• Kokstad Shopping Centre has three vacant shops measuring 1 229 m² with a potential tenant showing interest in more than half of this space.

Prospects and outlookRetail sales, the driver of activity in retail property, are showing signs of improvement although consumer debt levels remain high.

In order to generate growth, the Fund will maintain its more conservative growth strategy, investing to improve its existing portfolio of properties in order to generate higher incremental returns while also increasing the value of the portfolio without unnecessarily increasing the risks.

Page 25

Page 26

Annual Report 2010 Emira Property Fund

Value at June 2010: R23,6 m

Gross lettable area: 4 460 m²

The property:Admiral House is an industrial property located in Corporate Park South, Midrand comprising four adjoining warehouse units attached to a double storey office building. The property historically measured 5 116 m² with 42% being office space which had led to challenges in letting the property. The site measures 10 000 m2, has excellent exposure to the M1 highway and is zoned Special for industrial use.

The opportunity:The property was identified as non-core by the Manager because it did not meet the Fund’s rental growth or capital return hurdles. It had been earmarked for sale, but following a fire in 2009 which started on the tenants’ premises and caused extensive damage, the Manager re-evaluated the potential of the property. A proposal was put forward to unlock the value inherent in its good location to redesign and rebuild the building in such a manner as to improve the asset for Emira in the long term. The capital expenditure was fully covered by the proceeds of the insurance claim.

The upgrade:While the office portion of Admiral House was deemed to have value, the new building was designed to be more efficient by reducing the office space to 20% of GLA, in line with current tenant demand in the industrial sector and in order to enhance the rental appeal of the industrial property.

The warehouse portion of the building was increased from its original GLA of 2 981 m² to 3 571 m². In addition, a courtyard which previously separated the offices and the warehouse was removed to allow better vehicle access to the warehouse.

As a result of these changes, the renovated building’s GLA decreased but its new design is more generic. It should therefore attract the interest of a broader range of potential tenants at better rentals and thereby exceed Emira’s income streams from the old building prior to demolition even though the total GLA has decreased from GLA 5 116 m² to 4 460 m². The project was completed in August 2010 and letting is currently in progress.

The outcome:The redevelopment design has improved the quality of the asset and therefore Emira’s overall portfolio while strengthening its lettability. The refurbishment has also taken full advantage of the location by offering an A-grade building.

Projected monthly rentals for the industrial space which has been upgraded from B-grade to A-grade should increase by between 6% and 14%.

Manager’s report (continued)i n d u S t R i A l

taking advantage of opportunity to create a modern, sought-after lettable industrial building

industrial case study: Admiral House

Page 26

Page 27

Annual Report 2010 Emira Property Fund

induStRiAl MARket conditionS According to the IPD, the industrial sector was also faced with slowing total returns in 2009 which dropped to 8,7% (2008: 18,1%). This was due to capital growth moving into negative territory after having shown the strongest capital growth in the property sector for the past decade. A negative capital return of -0,6% was recorded for industrial properties (2008: growth of 8,4%). Income returns rose to 9,4% in 2009 (2008: 9,1%), reflecting a capital value decline.

The industrial sector has been relatively resilient in the market downturn partly because it did not attract the same speculative development activity in the height of the property boom which came to an end in 2008. As a result, the sector has not been as severely affected by oversupply as the office and retail sectors.

Vacancies in the sector increased to 6,7% in 2009 (2008: 2,6%), as a result of the economic downturn.

14

12

10

8

6

4

2

0

15

10

5

0

-5

Industrial vacancy rates and net income growth (%)

200019991998199719961995 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: IPDIndustrial vacancy rates Net income growth

0,4 0,7

5,3

79

9,3

10,9

12,3

10,4

3,32,6

3,12,2 2,6

6,76,5

Revenue of R188,2 million which represents an increase of 8%

Net income of R136,8 million increased by 11%

Industrial portfolio valued at R1,3 billion comprising 17% of the Fund’s total portfolio by value

Industrial Village Jet Park

Mitek South Africa

Freeway Park

Page 28

Annual Report 2010 Emira Property Fund

Manager’s report (continued)i n d u S t R i A l

eMiRA’S PoRtfolioexposure and performanceAt 30 June 2010, Emira’s industrial portfolio was valued at R1,3 billion and comprised 17% of the Fund’s total investment properties by value. The Fund owns 51 industrial properties, with total GLA of 386 061 m2 and an average value of R26,3 million.

The Fund’s industrial property portfolio’s revenue totalled R188,2 million, which represents an increase of 8% (2009: R173,8 million). The industrial portfolio’s contribution to Emira’s revenue increased slightly to 16%. Operating profit in the industrial sector increased by 11% to R136,8 million (2009: R122,7 million).

The Fund did not conclude the purchase of any new properties during the year, but Taylor Blinds in Montague Gardens in Cape Town (GLA 7 794 m2) which was purchased in the previous financial year for R36,0 million, was transferred in September 2009. Investments to improve the quality of the industrial portfolio during the year amounted to R5 million. In addition, Admiral House (see case study on page 26) which suffered extensive damage after a fire which started in the tenants’ premises, was rebuilt using the proceeds of the insurance claim.

Vacancies and lettingEmira’s industrial vacancies increased to 5,1% as at 30 June 2010 (2009: 3,0%), but the figure was slightly down from vacancies of 5,2% reported at the end of March 2010.

The Technohub industrial property in Midrand which was purchased in the previous financial year with an 18-month rental warranty from the developer, Eris Property Group, has been fully let. New leases were concluded with Vodacom and Paramount Logistics Corporation (Pty) Limited on more than 6 000 m2.

Major industrial vacancies at year-end included the following:• A vacant unit measuring 4 970 m² at Isando-Unitrans which is

being marketed.• Approximately a third of Midline Business Park located in the

active business node in Midrand is currently vacant, comprising 2 416 m² of offices and 1 727 m² of industrial space and is being marketed.

• Industrial Village Kya Sands has 3 851 m² of vacant warehousing space, comprising five vacant units. The industrial node has been affected by the downturn and letting has been slow although interest has picked up subsequent to year-end as a result of various incentives being put in place by Emira.

• Cambridge Park where a 1 957 m² unit is currently vacant. • One Highveld which has vacant units measuring 1 106 m² but

leases are currently under negotiation.

Prospects and outlookGiven the relatively low vacancy levels in the industrial sector, combined with the difficulty in bringing new developments on stream at prevailing rentals, the fundamentals for the sector are in place. The priority for Emira is to retain its existing tenants and attract new tenants to maximise the occupancy of its portfolio.

Page 29

Annual Report 2010 Emira Property Fund

Acquisitions and capital projectsAcquisitions and capital projects totalling R243,4 million were concluded during the year.

capital expenditure projects completed

Project Sector Location GLA (m2)

Capitalconsideration

(Rm)Effective

dateKey

tenants

One Highveld Industrial Centurion 5 932 0,9 Nov-09 V CustomMotorcycles

Wonderpark Shopping Centre Retail Karenpark, Pretoria

63 360 2,0 Nov-09 IncredibleConnection,

MaxisIngwavuma Shopping Centre Retail Ingwavuma 4 886 1,3 Dec-09 Spar, Build-ItSouthern Sentrum Retail Bloemfontein 21 224 14,9 May-10 Pick n Pay

and VariousTuinhof Office Centurion 9 182 0,8 May-10 Various

capital expenditure projects in progress

Project Sector Location GLA (m2)

Capital consideration

(Rm)

Expectedcompletion

dateKey

tenants

Randridge Mall Retail Randpark Ridge

22 624 126,2 Oct-10 Pick n Pay,Dis-Chem,

Woolworths, Foschini