INITIAL PUBLIC OFFER

19

-

Upload

omar-sexton -

Category

Documents

-

view

24 -

download

0

description

INITIAL PUBLIC OFFER. INITIAL PUBLIC OFFER (IPO). Governing Laws – Before 1992, Public issues were governed by Chief Controller of Capital Issues (CCCI). In 1992, CCCI has been abolished and SEBI has been formed. Now IPO is governed by Followings: The Companies Act 1956 - PowerPoint PPT Presentation

Transcript of INITIAL PUBLIC OFFER

INITIAL PUBLIC OFFER (IPO) Governing Laws –

Before 1992, Public issues were governed by Chief Controller of Capital Issues (CCCI).

In 1992, CCCI has been abolished and SEBI has been formed.

Now IPO is governed by Followings:

1. The Companies Act 1956

2. SEBI (Disclosure & Investor Protection) Guidelines, 2000

3. Securities Contracts (Regulation) Act, 1956

4. Listing norms/Guidelines of NSE/BSE

PRE REQUISITES OF IPOFiling of draft offer document with SEBI through eligible Merchant Banker at least 30 days prior to filing of prospectus with ROC.Any company prohibited by Board can not make an issue of security.Filing of application with Stock exchange for listing and in principal approval is required.Issue of securities in dematerialized form.Unlisted company can not make allotment pursuant to public issue unless prospective allottees are less than 1000 in numbers. Shares can be offered to public either in the form of IPO or offer for sale.Any company issuing debt instrument which are to convertible or not into share on a later date is required to obtain credit rating of investment grade from at least 2 credit rating agencies before filing the offer document with the SEBI, the company is not a willful defaulters of RBI and Not defaulted in payment of interest or repayment of debentures issued to public for a period of more than 6 months.There should not be any outstanding warrant or financial instrument giving right to holders an option to receive shares after IPO.There should not be partly paid shares.Firm arrangement of 75% means of finance.Grading of IPO from at least one credit rating agency.Disclosure of all grading has been to made.Disclosure of all expenses incurred for obtaining grading for IPO.

IPO- ELIGIBILITYIssue of Equity share or other securities to be converted into equity on later date

by an unlisted company:

A. Companies having track record must fulfill following conditions:

Net tangible assets of at least Rs.3.00 Crore in each of preceding 3 full year (Full 12 months each) of which not more than 50% is held in monetary assets; if excess, than the company must have firm commitment to deploy such excess monetary assets in business or project.- Clause 2.2.1(a)

Company must have track record of distributable profits for at least 3 years out of immediately preceding 5 years. - Clause 2.2.1(b)

Company must have net worth of Rs.1 Crore in preceding 3 years (full 12 months each). - Clause 2.2.1(c)

If name of the Company has been changed in last 1 year, 50% income of the Company must be earned from the activity suggested by new name. Clause 2.2.1(d)

Aggregate of proposed issue & all previous issues made during that financial year does not exceed to 5 times to its pre issue net worth as per the last audited balance sheet. Clause 2.2.1(e)

B. Companies not fulfilling conditions specified in Clause 2.2.1, have to fulfill following conditions:

(i) Issue through book building process with at least 50% of net offer to public to be issued to QIB.Or

Project has been appraised & at least 15% participation by FI/Sched. Commercial banks, of which at least 10% from appraiser & at least 10% of issue size from QIBs.

(ii) Minimum post issue face value of capital Rs.10.00 Crore. Or

Compulsory market making for at least 2 years from the date of listing subject to following: Market maker undertake • to offer buy & sell quotes for a minimum depth of 300 shares.• To ensure bid ask spread for their quotes shall not exceed at any time 10%.• Inventory of market maker on each stock exchange shall be at least of 5% of the proposed issue.

In case of partnership firms are converted into Company, track record for distributable profit shall

be considered, if the accounts are revised in the format prescribed as per companies Act and conforming all accounting standards.

PRICINGCompanies are free to price its share or security to be converted into shares at a later date are: Listed companies for its Public/right issue Unlisted companies Infrastructure Companies IPO by Banks (Subject to approval of RBI).

DIFFERENTIAL PRICING:

Unlisted Company : Firm allotment may be made on higher price than the price officer to Public. If equity shares or securities convertible into shares are issued to retail individual investor/retail individual share holder, the same can be issued at lower price than to other categories. The difference shall not exceed 10%.Listed Company: Differential price may be charged in composite issue of public and right offer.Justification of differential price in the offer document.

PRICE BAND:

For Fixed price issues, there may be price band of 20% at the time of filing offer documents with SEBI.Price shall be freezed in the final offer documents and before filing it to ROC.

DENOMINATION OF SHARE:

If issue price is more than Rs.500/- any face value denomination not less Re. 1/- and not in decimal.If Issue price is less than Rs.500/-, face value shall be Rs.10/-Only one denomination at a given time.

FACTORS DETERMINING PRICE:

Financials of the Company – Net worth, EPS, profit margin.Industry P/E Ratio.Standing of the Company in the relevant industryFuture prospect of the Industry as well as the CompanyBackground of the promoters.

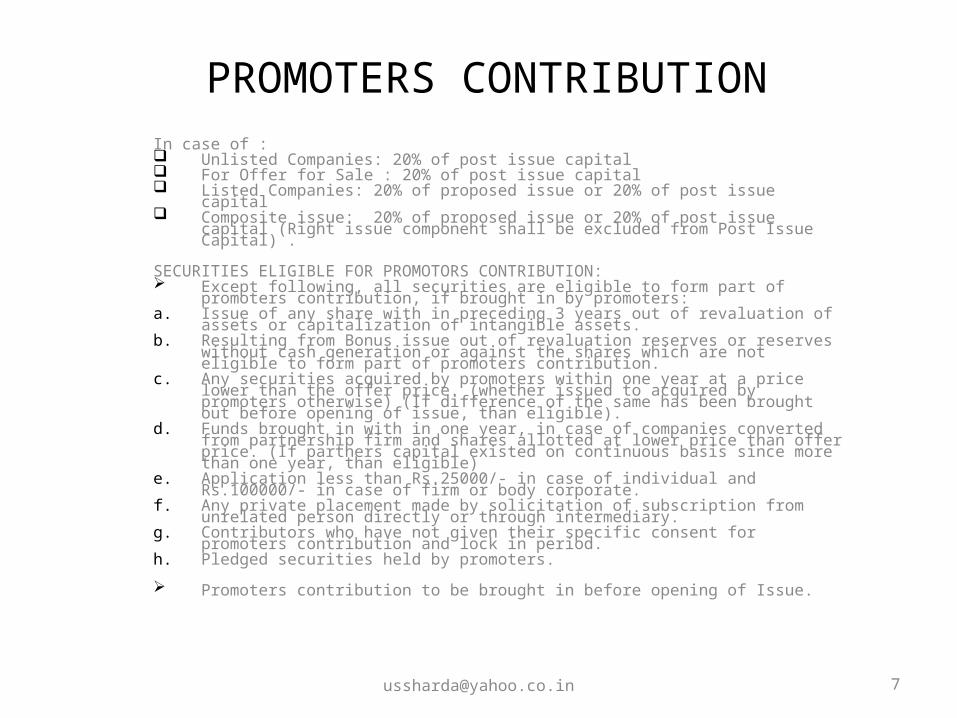

PROMOTERS CONTRIBUTIONIn case of : Unlisted Companies: 20% of post issue capital For Offer for Sale : 20% of post issue capital Listed Companies: 20% of proposed issue or 20% of post issue capital Composite issue: 20% of proposed issue or 20% of post issue capital (Right

issue component shall be excluded from Post Issue Capital) .

SECURITIES ELIGIBLE FOR PROMOTORS CONTRIBUTION: Except following, all securities are eligible to form part of promoters

contribution, if brought in by promoters:a. Issue of any share with in preceding 3 years out of revaluation of assets or

capitalization of intangible assets.b. Resulting from Bonus issue out of revaluation reserves or reserves without cash

generation or against the shares which are not eligible to form part of promoters contribution.

c. Any securities acquired by promoters within one year at a price lower than the offer price. (whether issued to acquired by promoters otherwise) (If difference of the same has been brought out before opening of issue, than eligible).

d. Funds brought in with in one year, in case of companies converted from partnership firm and shares allotted at lower price than offer price. (If partners capital existed on continuous basis since more than one year, than eligible)

e. Application less than Rs.25000/- in case of individual and Rs.100000/- in case of firm or body corporate.

f. Any private placement made by solicitation of subscription from unrelated person directly or through intermediary.

g. Contributors who have not given their specific consent for promoters contribution and lock in period.

h. Pledged securities held by promoters.

Promoters contribution to be brought in before opening of Issue.

LOCK IN PERIODIn case of IPO, the locking period is as under:

Promoters contribution equal to 20% - start from date of allotment & end after 3 years from the date of allotment or date of commencement of commercial production, whichever is later.

Promoters contribution in excess of 20% - 1 year

Pre issue share capital: In excess of promoters contribution equal to 20%, for 1 year.

Basis of Lock in – Last allotted share locked in first – Omitted since 29.11.07.

Lock in of firm allotment security: For one year

Inter se transfer amongst promoter permissible.

PRE ISSUE OBLIGATION & INTERMEDIARIES

APPOINTMENT OF LEAD MANAGER(S) Due diligence procedure by Lead Manager. Appointment of intermediariesLead Manager will appoint:a. Registrar to issueb. Legal Advisorc. Bankers to Issued. Underwriters

Filing of Offer Documents with SEBI & S/E Documents to be submitted with Draft offer documents:a. MOU between Lead Manager & Issuerb. Inter se allocation of responsibilitiesc. Due Diligence Certificated. Undertaking of promoters for their transactions.e. List of promoters’ group etc.f. Other documents,

• Offer Documents to be made public – for Minimum 21 Days.• Pre issue advertisement.• Dispatch of Issue Material.• No Complaint Certificate – after 21 days from the date of making prospectus in public.• Agreement with Depositories• Receipt of In principal approval from Stock Exchange (s) within 15 days from the date of filing.• Collection centre – Four Metro Cities and cities where stock exchanges in the region.• Collection agents.• Appointment of Compliance Officer

MARKETING OF IPO AND ISSUE PROCESS

• WHOLESALE MARKETING

• Meetings with mutual funds, Private Equity players and FIIs.

• Tie up for firm allotments

• RETAIL MARKETING:

• Road Shows and presentation

• Meeting with leading brokers

• Advertisement in Print & Electronic Media

• Press Coverage

• ISSUE PROCESS:

• Issue remain open for minimum 3 days and maximum for 10 days.

• Collection of application/ real time reporting of bids.

• Periodical report by Lead Bankers.

• Allotment of shares in consultation with stock exchanges and lead manager(s).

POST ISSUE OBLIGATIONS

Post issue monitoring reports: These reports shall be submitted with in 3 days from the due dates. Due dates:

- 3rd day monitoring report - for book building portion – 3rd day from the date of allocation of book building portion

-In other cases – 3rd day from the date of closure of issue. - Final post issue monitoring report: 3rd day from the date of listing or 78 days from the date of closure

of issue, whichever is earlier. - Due diligence certificate with final report

Redressal of Investor Grievance – related to refund, allotment and other grievences.

Coordination with intermediaries• a. Underwriters• b. Bankers to the issue

Basis of allotment

Post issue advertisement : giving detail about oversubscription, basis of allotment etc. within 10 days from the date of

LISTING WITH BSE

A. In respect of Large Cap Companies with a minimum issue size of Rs. 10 crores and market capitalization of not less than Rs. 25 crores.

The minimum post-issue paid-up capital of the applicant company (hereinafter referred to as "the Company") shall be Rs. 3 crores; and

The minimum issue size shall be Rs. 10 crores; and The minimum market capitalization of the Company shall be Rs. 25 crores (market

capitalization shall be calculated by multiplying the post-issue paid-up number of equity shares with the issue price).

B. In respect of Small Cap Companies other than a large cap company.

The minimum post-issue paid-up capital of the Company shall be Rs. 3 crores; and The minimum issue size shall be Rs. 3 crores; and The minimum market capitalization of the Company shall be Rs. 5 crores (market capitalization

shall be calculated by multiplying the post-issue paid-up number of equity shares with the issue price); and

The minimum income/turnover of the Company should be Rs. 3 crores in each of the preceding three 12-months period; and

The minimum number of public shareholders after the issue shall be 1000. A due diligence study may be conducted by an independent team of Chartered Accountants or

Merchant Bankers appointed by the Exchange, the cost of which will be borne by the company. The requirement of a due diligence study may be waived if a financial institution or a scheduled commercial bank has appraised the project in the preceding 12 months.

LISTING WITH BSE Permission to use the name of the Exchange in an Issuer Company's prospectus:

• The Exchange follows a procedure in terms of which companies desiring to list their securities offered through public issues are required to obtain its prior permission to use the name of the Exchange in their prospectus or offer for sale documents before filing the same with the concerned office of the Registrar of Companies. The Exchange has since last three years formed a "Listing Committee" to analyse draft prospectus/offer documents of the companies in respect of their forthcoming public issues of securities and decide upon the matter of granting them permission to use the name of "Bombay Stock Exchange Limited" in their prospectus/offer documents. The committee evaluates the promoters, company, project and several other factors before taking decision in this regard.

Allotment of Securities

• As per Listing Agreement, a company is required to complete allotment of securities offered to the public within 30 days of the date of closure of the subscription list and approach the Regional Stock Exchange, i.e. Stock Exchange nearest to its Registered Office for approval of the basis of allotment.

• In case of Book Building issue, Allotment shall be made not later than 15 days from the closure of the issue failing which interest at the rate of 15% shall be paid to the investors.

Trading Permission

• As per SEBI Guidelines, the issuer company should complete the formalities for trading at all the Stock Exchanges where the securities are to be listed within 7 working days of finalization of Basis of Allotment.

• A company should scrupulously adhere to the time limit for allotment of all securities and dispatch of Allotment Letters/Share Certificates and Refund Orders and for obtaining the listing permissions of all the Exchanges whose names are stated in its prospectus or offer documents. In the event of listing permission to a company being denied by any Stock Exchange where it had applied for listing of its securities, it cannot proceed with the allotment of shares. However, the company may file an appeal before the Securities and Exchange Board of India under Section 22 of the Securities Contracts (Regulation) Act, 1956.

BOOK BUILDING

It is a process used for marketing a public offer of equity shares of a company. It is a mechanism where, during the period for which the book for the IPO is open, bids are collected from investors at various prices, which are above or equal to the floor price. The process aims at tapping both wholesale and retail investors. The offer/issue price is then determined after the bid closing date based on certain evaluation criteria.

The Process:

• The Issuer who is planning an IPO nominates a lead merchant banker as a 'book runner'. • The Issuer specifies the number of securities to be issued and the price band for orders. • The Issuer also appoints syndicate members with whom orders can be placed by the investors. • Investors place their order with a syndicate member who inputs the orders into the 'electronic

book'. This process is called 'bidding' and is similar to open auction. • A Book should remain open for a minimum of 3 days and maximum for 10 days. • Bids cannot be entered less than the floor price. • Bids can be revised by the bidder before the issue closes. • On the close of the book building period the 'book runner evaluates the bids on the basis of the

evaluation criteria which may include - – Price Aggression – Investor quality – Earliness of bids, etc.

• The book runner and the company conclude the final price at which it is willing to issue the stock and allocation of securities.

• Generally, the number of shares are fixed, the issue size gets frozen based on the price per share discovered through the book building process.

• Allocation of securities is made to the successful bidders. • Book Building is a good concept and represents a capital market which is in the process of

maturing.

BOOK BUILDING Guidelines for Book Building•

Rules governing book building is covered in Chapter XI of the Securities and Exchange Board of India (Disclosure and Investor Protection) Guidelines 2000.

• Book building is a process by which demand of securities which are being offered, is elicited and price is determined.

BSE's Book Building System

• BSE offers the book building services through the Book Building software that runs on the BSE Private network. • This system is one of the largest electronic book building networks anywhere spanning over 350 Indian cities through

over 7000 Trader Work Stations via leased lines, VSATs and Campus LANS • The software is operated through book-runners of the issue and by the syndicate member brokers. Through this book,

the syndicate member brokers on behalf of themselves or their clients' place orders. • Bids are placed electronically through syndicate members and the information is collected on line real-time until the bid

date ends. • In order to maintain transparency, the software gives visual graphs displaying price v/s quantity on the terminals.

Initial Public Offerings Corporates may raise capital in the primary market by way of an initial public offer, rights issue or private placement.

An Initial Public Offer (IPO) is the selling of securities to the public in the primary market. This Initial Public Offering can be made through the fixed price method, book building method or a combination of both.

In case the issuer chooses to issue securities through the book building route then as per SEBI guidelines, an issuer company can issue securities in the following manner:

• 100% of the net offer to the public through the book building route. • 75% of the net offer to the public through the book building process and 25% through the fixed price portion.

•

DIFFERENCE IN FIXED PRICE OFFER AND BOOK BUILDING

• Fixed Price process • Price at which the securities are

.offered/allotted is known in advance to the investor.

• Demand for the securities offered is known only after the closure of the issue .

• Payment if made at the time of subscription wherein refund is given after allocation

• Book Building process • Price at which securities will be

offered/allotted is not known in advance to the investor. Only an indicative price range is known.

• Demand for the securities offered can be known everyday as the book is built.

• Payment only after allocation

CONTENTS OF PROSPECTUS

• Definitions & Abbreviations • Risk Factors & Proposals to address the risks thereof• Highlights PART I • I. General information• II. Capital structure of the company• III. Terms of the present issue• IV. Particulars of the issue• V. Description of industry and business• VI. Company, management and project• VII. Management discussion and analysis of the financial condition and results of the

operations as reflected in the financial statements. • VIII. Financial of group companies • IX. Basis for issue price • X. Outstanding litigations or defaults • XI. Risk factors and Proposals to address the risks on the same, if any PART II • I. General information• II. Financial information• III. Statutory and other information PART III • Declaration

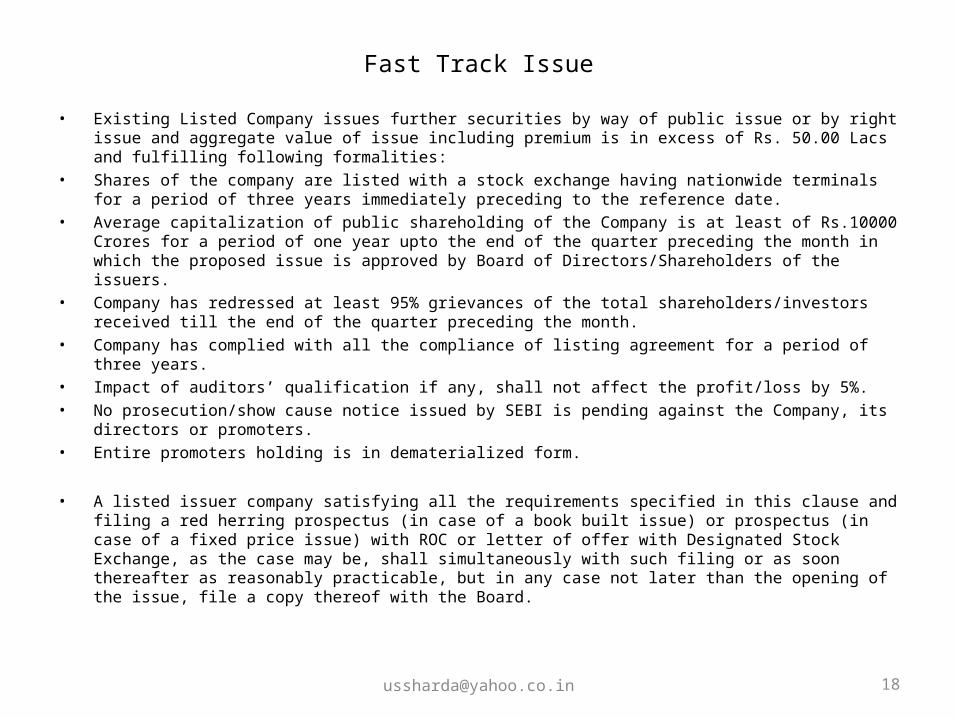

Fast Track Issue

• Existing Listed Company issues further securities by way of public issue or by right issue and aggregate value of issue including premium is in excess of Rs. 50.00 Lacs and fulfilling following formalities:

• Shares of the company are listed with a stock exchange having nationwide terminals for a period of three years immediately preceding to the reference date.

• Average capitalization of public shareholding of the Company is at least of Rs.10000 Crores for a period of one year upto the end of the quarter preceding the month in which the proposed issue is approved by Board of Directors/Shareholders of the issuers.

• Company has redressed at least 95% grievances of the total shareholders/investors received till the end of the quarter preceding the month.

• Company has complied with all the compliance of listing agreement for a period of three years.• Impact of auditors’ qualification if any, shall not affect the profit/loss by 5%.• No prosecution/show cause notice issued by SEBI is pending against the Company, its directors or

promoters.• Entire promoters holding is in dematerialized form.

• A listed issuer company satisfying all the requirements specified in this clause and filing a red herring prospectus (in case of a book built issue) or prospectus (in case of a fixed price issue) with ROC or letter of offer with Designated Stock Exchange, as the case may be, shall simultaneously with such filing or as soon thereafter as reasonably practicable, but in any case not later than the opening of the issue, file a copy thereof with the Board.

Application supported by Blocked Amount (ASBA) : Application for subscribing an issue with an authorization to block the amount in Bank account

ASBA Investor : an investor who is oa residential retail investor onot applying under any reservation, obidding on cut off price with single option and not revising his bid and oapplying through SCSB banks.

Self Certified Syndicate Bank (SCSB): Banker to the issue registered with SEBI, which offers the services of making ASBA.