The URC 522 are the Uniform Rules for Collections. URC 522 came ...

ING Trade Finance Services The Documentary collection

Wholesale Banking

Page 1/19

Contents Introduction................................................................................................................................... 2

Definition........................................................................................................................................ 3

Introduction and notion of risk ................................................................................................. 4

Mechanism .................................................................................................................................... 5

Dispute at the time the documents are presented ............................................................. 7

Methods of utilisation ................................................................................................................. 8

The documentary collection payable at sight .................................................................. 8

The documentary collection payable at usance .............................................................. 8

The documentary collection payable at usance, with aval ........................................... 9

Discounting of a Bill of Exchange in frame of a Documentary Collection ................ 10

Clean collections .................................................................................................................... 11

Collection conditions: scope of the Uniform Rules ............................................................. 13

The documents .......................................................................................................................... 14

Financial documents ............................................................................................................. 14

Commercial documents ....................................................................................................... 14

Procedures ................................................................................................................................... 15

The collection instruction from our client, the exporter. .............................................. 16

Transmission of the collection instruction by the remitting bank (ING) to the presenting bank (foreign correspondent). ....................................................................... 17

Collection by presenting bank and transfer of proceeds. ............................................ 17

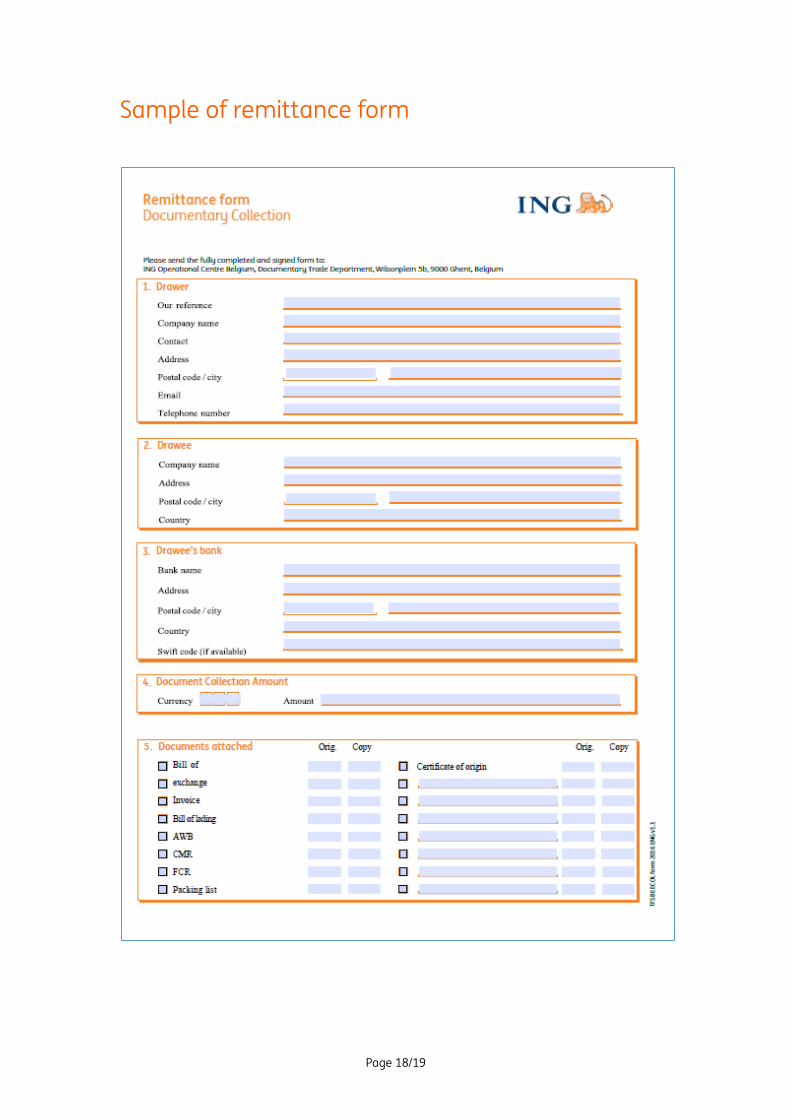

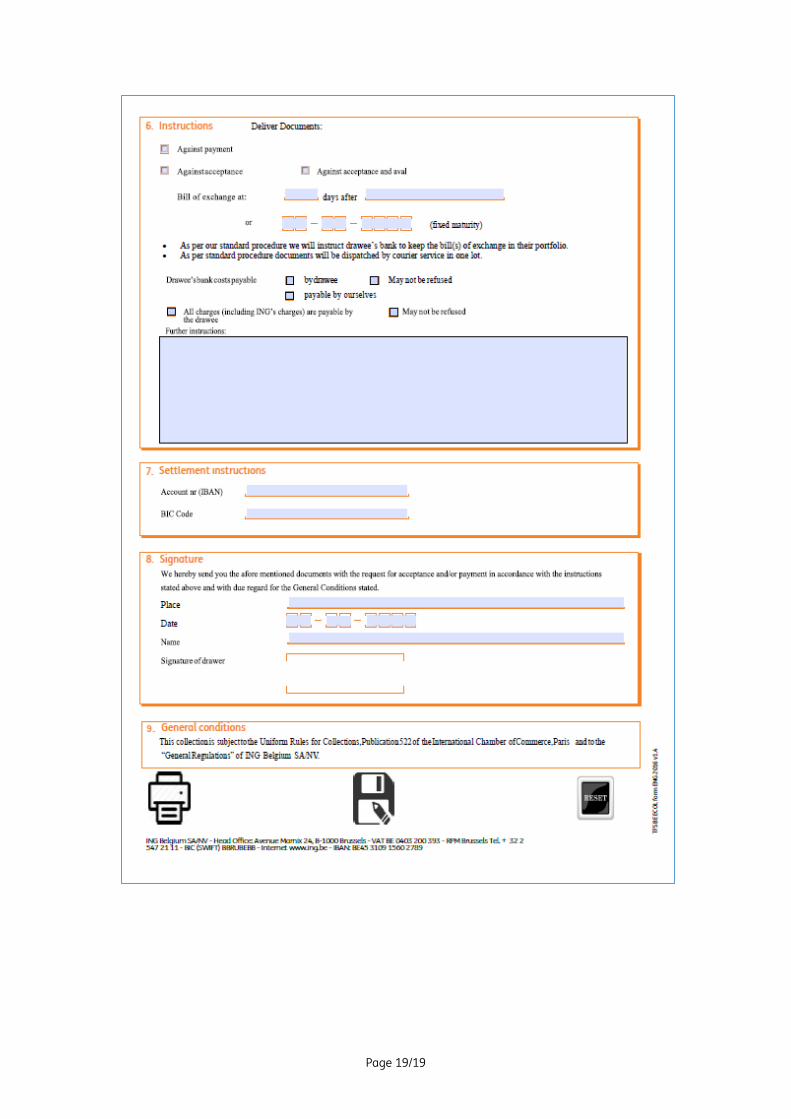

Sample of remittance form ..................................................................................................... 18

Page 2/19

Introduction Businesses trading internationally often need tools to limit trade risk. A documentary collection is an intermediary payment method between your Documentary Credits 1 and your open account business. This brochure explains how documentary collections work, what types of documentary collections exist and what the conditions of such documentary collections are.

1 See our brochure on Documentary Credit available with your usual contact at ING

If having read this brochure, you would like

further information, please contact your usual Trade contact

person at ING

Page 3/19

Definition A Documentary collection is a payment technique whereby the exporter gives collection instructions as well as one or several documents (invoice, transport and insurance documents) to his banker (remitting bank). These documents are then remitted to the importer through the channel of his bank (presenting bank), either against payment or against acceptance of a Bill of Exchange payable at sight or on a given due date.

The deadline for execution depends mainly on the time required to transmit the documents, to present them and to make the payment. In other words, it depends mainly on the country of destination and of the channel of transmission (by post or by courier service).

Such transactions are governed by the ICC Uniform Rules for Collections (URC), published by the International Chamber of Commerce, publication 522 of 1.1.1996.

You can order it from ING or on the ICC website BusinessBookstore http://store.iccwbo.org/

According to this procedure, banks only act as agents on behalf of their respective customers. They only undertake to execute their customers' instructions.

Banks must verify that the documents received appear to comply with those listed in the collection instructions and must immediately notify the party which sent them the collection instruction of any missing document.

The obligation for banks to examine the documents does not go any further.

That is the fundamental difference between a Documentary Collection and a Documentary Credit.

Page 4/19

Introduction and notion of risk The methods of settlement against documents are especially widespread in the field of marine sales; indeed transport by sea is often the subject of Bills of Lading. A marine bill of lading is the only document representative of the goods. Furthermore, as Bills of Lading can be - and often are - established to order, the transfer of the right to ownership of the goods stems from ordinary endorsement.

Consequently, by stipulating in a sale contract, that a supply will be paid against remittance of Bills of Lading, a condition is added which, in principle, is equivalent to payment against delivery of the goods.

The same is not true for the other methods of transport, such as transport by road for instance: a CMR (convention on the contract for the international carriage of goods

by road) is not a document representative of goods. It merely certifies the dispatch of the goods. Which will be automatically delivered to the addressee whose name is indicated on the CMR.

However if the buyer does not act in good faith or is insolvent, and refuses to accept the documents, the seller is obliged to warehouse the goods, which in the meantime have arrived at destination, and to find another buyer or to repatriate the goods. Both scenarios will incur substantial and unforeseen expenses. Furthermore, he will have to wait a long time before receiving the proceeds from the goods.

Obviously, the exporter can take a legal action in court against the buyer, however a legal action in a foreign country is expensive, not to mention the differences in jurisprudence which can exist between in the countries involved.

There is an additional risk for the seller if the documents are remitted to the buyer against acceptance of a Bill of Exchange. Once the Bill of Exchange has been accepted and the documents are in the hands of the buyer, the seller loses the right of disposal over the goods.

But what guarantee is there that the Bill of Exchange will be paid when it falls due?

Page 5/19

Mechanism Once the goods have been dispatched, the exporter gives the documents representing such goods (invoice, marine bills of lading possibly plus other documents) to ING through a collection form (see sample page 18, available on request).

Unlike the procedure for Documentary Credits, the bank does not verify the documents presented. Nonetheless it will check certain elements: any discrepancies in relation to the method of payment possibly between the documents, signatures, endorsement. The purpose of such check is to allow the unhindered settlement of the Documentary Collection by the various parties involved.

ING (remitting bank) then transmits the documents via courier to the importer's banker (presenting bank) together with a collection form.

This form indicates the various instructions enabling the foreign banker to collect the documents, from the transmission of the documents to the importer up to ultimate payment by the latter.

In particular such instructions include:

• The form of the Documentary Collection (at sight or at usance)

• The instructions in the event of non-payment (at sight) or of non-acceptance of a Bill of Exchange (at usance) and aval as the case may be.

• The description of the documents presented as well as the goods

• The covering banker according to the currency of the Documentary Collection

• The application of the Uniform Rules for Documentary Collections

• ...

Upon receipt of the documents, the presenting bank informs its customer (the importer) of the presentation of the documents.

Finally, the documents are only remitted to the importer against payment (in the case of collections at sight) or against acceptance of a Bill of Exchange and aval (by the drawee’s bank) if any (in the case of collections at usance).

Page 6/19

It is clear that a Documentary Collection is an intermediary process which, although it does not give the exporter the certainty of being paid, nonetheless guarantees that the buyer will not be able to take possession of the goods before having paid for them (documents against payment) or as long as it has not accepted a Bill of Exchange with a specific due date drawn on it by the exporter (documents against acceptance), provided obviously in the case of shipment by sea that the full set of Bills of Lading (sometimes to the order of a bank) transits through the channel of a bank.

In the case of transport by air, the goods are sometimes consigned to the order of a bank.

However the article 10a of URC mentions:

“Goods should not be despatched directly to the address of a bank or consigned to or to the order of a bank without prior agreement on the part of that bank.

Nevertheless, in the event that goods are despatched directly to the address of a bank or consigned to or to the order of a bank for release to a drawee against payment or acceptance or upon other terms and conditions without prior agreement on the part of that bank, such bank shall have no obligation to take delivery of the goods, which remain at the risk and responsibility of the party despatching the goods”.

Page 7/19

Dispute at the time the documents are presented Not including cases where the importer does not act in good faith or is insolvent, the latter will occasionally dispute the payment for various reasons:

• The conditions for delivery of the documents do not comply with the stipulations of the commercial contract (for example the payment terms do not match)

• The amount invoiced is higher than that of the order

• The goods were dispatched late

• The goods have not yet arrived at destination

• The documents arrived after the arrival of the goods, resulting in storage expenses which he is not willing to cover

• He wants to inspect the goods before giving his approval

• The documents required for clearance through customs (e.g. Health certificate, etc.) are missing 2

• The import license has not yet been obtained

• The set of Bills of Lading is incomplete

• Etc.

The presenting bank must, on a case-by-case basis, act in the interests of both parties, in accordance with instructions received and in observance of the Rules.

Nevertheless, with regard to the goods, article 10b of the Uniform Rules stipulates that:

"Banks have no obligation to take any action in respect of goods to which a Documentary Collection relates – including storage and insurance, etc. –, even if specific instructions are given to do so. Banks will only take such action if, when, and to the extent that they agree do so in each case...".

2 The Market Access Database gives information to companies exporting from the EU about import conditions in third country markets - http://madb.europa.eu/madb/indexPubli.htm

Page 8/19

Methods of utilisation A distinction has already been made between - on the one hand - "Documents against payment" and - on the other hand - "Documents against acceptance".

Both systems are examined in detail below:

The documentary collection payable at sight (Documents against Payment D/P – Cash against Documents CAD)

The importer makes the payment against remittance of the documents, which provide him with proof that the goods have actually been dispatched to his address or have been placed aboard a ship.

The exporter remains the owner of the goods until payment, so that if the buyer defaults it can exercise his rights.

The documentary collection payable at usance (Documents against Acceptance D/A)

The exporter will grant a deferred payment, but he will only remit the documents giving right to delivery of the goods against acceptance of a Bill of Exchange by the buyer.

Through the channel of banks, the documents are presented against acceptance and the amounts received on the due date.

The documents are remitted to the drawee (the importer) against acceptance of the Bill of Exchange enclosed, with a due date, which can be:

• To XX days after sight

• On a given due date (for example 60 days from invoice date)

The accepted Bill of Exchange:

• Can be returned to the exporter who will, where appropriate, have it discounted in his country. In that case, on the due date the Bill of Exchange must be again returned in order to be presented to the drawee for payment.

• Can be kept until the due date at the presenting bank. In that case, the presenting bank will notify the remitting bank that the Bill of Exchange has been accepted and will keep it in order to present it for payment on the due date (without commitment).

Page 9/19

The documentary collection payable at usance, with aval

With a D/A, the importer has the advantage of receiving goods, which have not yet been paid for.

To hedge against the risk of non-payment on the due date of an accepted Bill of Exchange (as acceptance is only an undertaking to pay), the exporter can ask for a "Bill of Exchange guarantee clause" to be inserted in the sale contract by a bank established in the country of the buyer. Obviously, the guarantee 'aval' must originate from a safe bank, which is only authorised to deliver the documents to the importer provided the Bill of Exchange has been duly guaranteed. The guarantee 'aval' is given prior to remittance of the documents, and the usual wording is « 'bon pour aval' (approval) of the signature of the drawee » (backing of the drawee's signature). It goes without saying that this formula is more expensive for the importer.

As a guarantee 'aval' is a commitment whereby a Bank, which places its signature on a Bill of Exchange jointly and severally, guarantees the payment of the Bill of Exchange on the due date.

The value of this signature obviously depends on the reputation of the bank, which gives its backing. In principle a bank which has given its backing will not renegade on her commitment. Nonetheless, some local Legal rules may force it to delay payment on the due date.

Consequently, exporters should enquire about the legislation in force in the country of destination, restrictions as well as customs and practices.

Your legal department can also provide you with information with regard to the value of the guarantee 'aval' in some countries.

Particularity at the import side

When ING (presenting bank) guarantees a Bill of Exchange on behalf of its importing customer, the bank knows that its signature guarantees the payment of the Bill of Exchange on the due date.

Therefore, ING must first assess the credit risk taken on her customer.

When a line is set up to issue a guarantee, collateral can be required (pledges, sureties etc.) according to the credit risk.

Page 10/19

Discounting of a Bill of Exchange in frame of a Documentary Collection

The exporter can also ask its bank to discount the bills of exchange accepted by the buyer and backed by the latter's banker (aval). In that precise case, the exporter will have the guarantee that it will receive payment on the due date.

As the risk involved is taken on the country and the foreign banks, this kind of discounting is not taken into consideration in the customer's credit facility.

The margin related to the risk premium will depend on the risk taken on the country and the foreign bank.

Page 11/19

Clean collections

Remittance of a Bill of Exchange or draft (= without commercial documents)

Clean Bills of Exchange can be distinguished from Documentary Collections by the fact that they are sent to the importer without any commercial documents.

In accordance with provisions agreed with the exporter, the importer must pay or accept the Bill of Exchange upon first presentation. As it does not provide any guarantee of payment or acceptance, a clean Bill of Exchange is to be used only if the buyer is known to fulfil its commitments.

In comparison with settlement by means of an ordinary invoice, there are some advantages:

• The possibility for the exporter to mobilise its claim with its banker, in other words to convert its term claim into cash;

• As materialisation of the claim into a commercial Bill of Exchange makes it possible, in the event of a payment default, to launch collection proceedings in accordance with the Rules of exchange law applicable in the country of the importer.

By way of a precaution, the seller should make enquiries at the banks about the Rules of exchange law applicable in the country involved.

For information lot of presenting banks refuse to protest the unpaid Bills of Exchange at their maturity.

According to the contract, the Bill of Exchange can be drawn:

• « At sight », when it must be paid on first presentation;

• « At x » days after sight (30 — 60 — 90 days), from the acceptance of the Bill of Exchange;

• « A x » days after sight, from the date of invoice or dispatch.

Page 12/19

Legal mandatory notices on a Bill of Exchange in Belgium:

As an example, to be valid, in Belgium, a Bill of Exchange must include the following eight indications:

1. The term "Bill of Exchange"

2. An ordinary and straightforward instruction to pay a given amount

3. The name of the party which must pay (the drawee)

4. The due date

5. The place where the payment must be paid

6. The name of the party to whom or to whose order the payment must be made

7. The date and the place where the bill is created

8. The signature of the issuer of the bill (principal/drawer).

Although a clean Bill of Exchange does not provide any guarantee of payment on the due date to the exporter, whereas most of the time the goods have been delivered, the possession of such a Bill of Exchange, provided it has been accepted, would facilitate the legal recovery of the claim in some countries.

Page 13/19

Collection conditions: scope of the Uniform Rules Documents sent for collection must be accompanied by a collection instruction (Collection form) giving full and precise directives. Banks are only authorised to act in accordance with the directives stipulated in the aforementioned collection instruction and in accordance with the Rules.

If the bank instructed to make the collection cannot, for whatever reason, comply with the instructions in the collection instruction it has received, it must immediately notify the remitting bank thereof.

The Uniform Rules cover:

• General provisions and definitions

• Form and structure of collections

• Form of presentation

• Liabilities and responsibilities

• Payment

• Interest, charges and expenses

• Other provisions

The scope of application of these Rules covers both the relationship between the exporter (principal) and the bank to which the collection transaction is entrusted, and the relationship, which could exist between the aforementioned bank, and its correspondent empowered to carry out the transaction, as well as the importer (drawee).

Page 14/19

The documents Financial documents

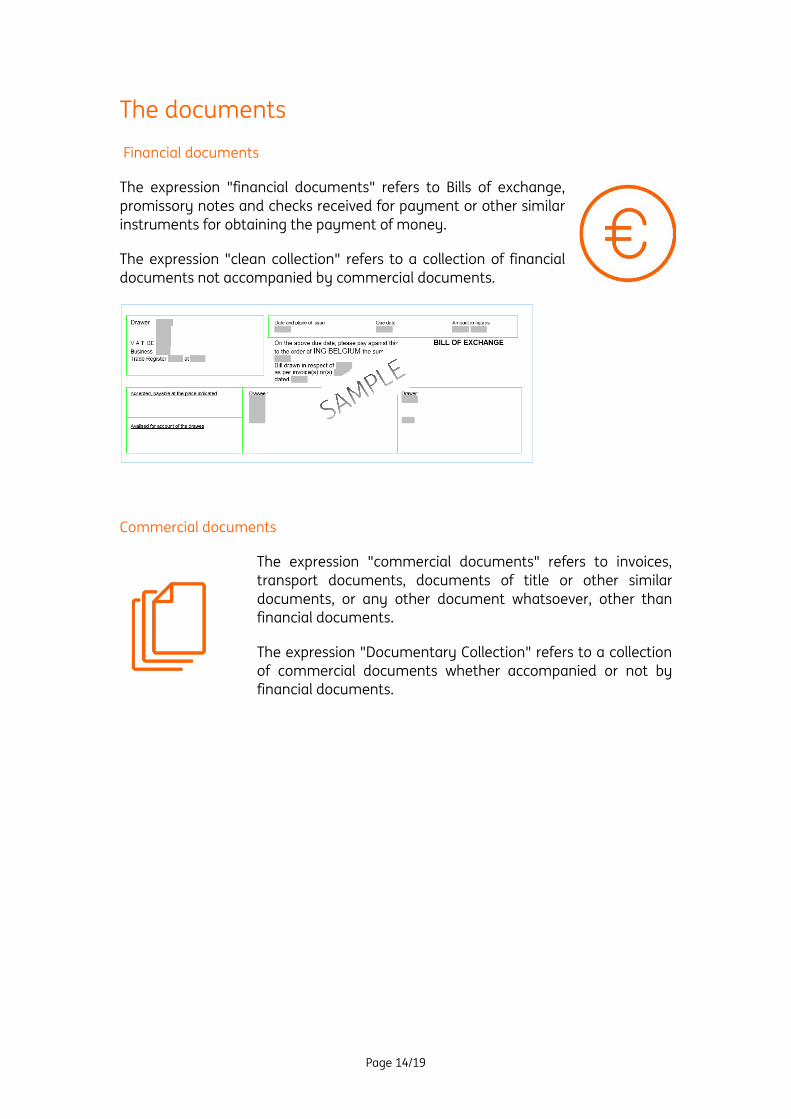

The expression "financial documents" refers to Bills of exchange, promissory notes and checks received for payment or other similar instruments for obtaining the payment of money.

The expression "clean collection" refers to a collection of financial documents not accompanied by commercial documents.

Commercial documents

The expression "commercial documents" refers to invoices, transport documents, documents of title or other similar documents, or any other document whatsoever, other than financial documents.

The expression "Documentary Collection" refers to a collection of commercial documents whether accompanied or not by financial documents.

Page 15/19

Procedures The Rules related to the Collections of the International Chamber of Commerce ("collection" means treatment by banks, according to the instructions received, of financial documents - bills of Exchange issued for obtaining a payment - and commercial - invoices, title documents, for insurance, etc.) codify the conditions that apply to any collection of documents and specify the responsibilities of the banks involved.

The following parties can be involved in Documentary Collections:

• The exporter or principal, who draws a Bill of Exchange (draft) on his customer, gives it to his banker and asks him to proceed with his collection;

• The remitting bank, who receives the documents from the exporter or principal, and who has the mission of collecting payment;

• The correspondent bank, who is instructed by the remitting bank to proceed with collection or acceptance;

• The presenting bank, banker of the foreign buyer, who will be instructed to pay, on behalf of the said buyer, the amount of the Bill of Exchange domiciled with it. The correspondent bank can also be the presenting bank;

• The importer, or drawee, on whom the Bill of Exchange, documents against payment or against acceptance is/are drawn.

Page 16/19

The collection instruction from our client, the exporter.

The exporter has dispatched the goods. He now has the transport document with which it will enclose the invoice and, where appropriate the insurance certificate and the certificate of origin, the packing and weight lists, etc.

Checklist prior to exporting (non-limitative):

• Are all the documents required by the buyer and agreed in the sale contract present?

• Are they complete and have they been compiled properly?

• Are all the documents absolutely required by the country of destination enclosed and have the stipulations with regard to the establishment of these documents been respected (authenticated, language stipulations, etc.?)

• Have these documents been validly signed?

• If the Bills of Lading, insurance certificates and bills of exchange have not been compiled to the order of the buyer or the presenting bank, have they been endorsed as required for negotiation?

In order to realise a Documentary Collection, the exporter will send a letter of instructions, (form) together with the Bill of Exchange and the commercial documents pertaining to the transaction to his bank.

In particular the following indications should be mentioned on this remittance form:

• The parties

• The remittance conditions of the documents (D/P – D/A)

• The stipulations with regard to the goods description and the conditions of dispatch

• The details of the documents – the banks must check the nature and the number of documents announced

• The charges and their distribution

In the case of documents to be delivered against acceptance:

• The instructions relating to the Bill of Exchange after acceptance by the drawee: either to be returned, or to be kept by the banker in the country of the drawee, with a view to collection on the due date.

Page 17/19

Transmission of the collection instruction by the remitting bank (ING) to the presenting bank (foreign correspondent).

Upon receipt of the form and the documents, ING will check the documents exclusively on the basis of the Uniform Rules, where article 12a stipulates: "banks must determine that the documents received appear to be as listed in the collection instruction and advise by telecommunication or, if that is not possible, by other expeditious means, without delay, the party from whom the collection instruction was received of any documents missing, or found to be other than listed".

Following this check, ING will send the documents to the bank instructed to make the collection in the country of the drawee, with all the required instructions.

The banks' obligation to examine the documents does not go any further.

Collection by presenting bank and transfer of proceeds.

In the case of a collection in the form of documents against payment, normally the drawee will take possession of the documents by paying the amount owed to the presenting bank who will transfer this amount to the remitting bank.

NB. Article 18 stipulates: "In the case of documents payable in a currency other than that of the country of payment (foreign currency), the presenting bank must, unless otherwise instructed in the collection instruction, release the documents to the drawee against payment in the designated foreign currency only if such foreign currency can immediately be remitted, in accordance with instructions given in the collection instruction".

In the case of a collection in the form of documents against acceptance, the drawee will accept a Bill of Exchange whereby it undertakes to pay on the due date. According to the instructions of the collection instruction, the acceptance will remain with the presenting bank or it will be returned to the remitting bank.

Page 18/19

Sample of remittance form

Page 19/19

Although this brochure has been written with the greatest care, ING accepts no liability for its contents.

ING Belgium SA/NV – Bank – Marnixlaan 24, B-1000 Brussels – Brussels RPM/RPR - VAT BE 0403.200.393 - BIC: BBRUBEBB – IBAN: BE45 3109 1560 2789.

Publisher: Inge Ampe – Sint-Michielswarande 60, 1040 Brussels © Editing Team & Graphic Studio – Marketing ING Belgium – TFS008E – 01/17