Infrastructure Investment in China - Tufts Fletcher...

12

Transcript of Infrastructure Investment in China - Tufts Fletcher...

Infrastructure Investment in China Weiping Wu Professor Tufts University [email protected]

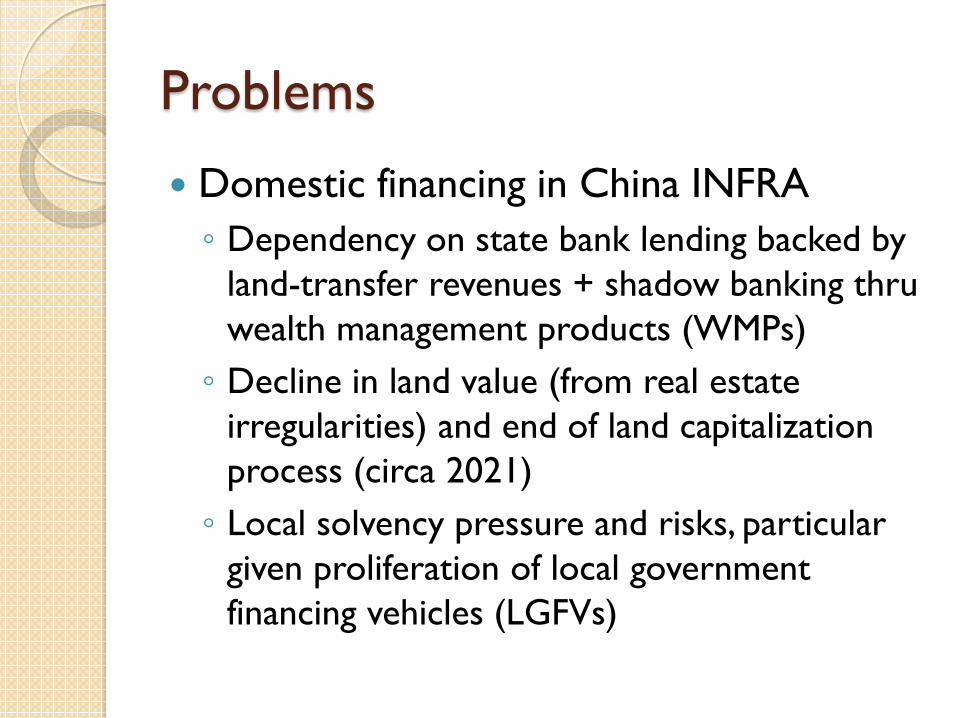

Problems

Domestic financing in China INFRA ◦ Dependency on state bank lending backed by

land-transfer revenues + shadow banking thru wealth management products (WMPs) ◦ Decline in land value (from real estate

irregularities) and end of land capitalization process (circa 2021) ◦ Local solvency pressure and risks, particular

given proliferation of local government financing vehicles (LGFVs)

Knowledge asymmetry

Intl investor preference (mainstream) ◦ GP/LP with private sector players ◦ Unlisted funds ◦ Late-stage, brownfield projects ◦ Multiple risk premiums for EMs

Chinese perception ◦ Low-cost capital (vs. Chinese bank lending) ◦ Social responsible investing ◦ Access to other markets

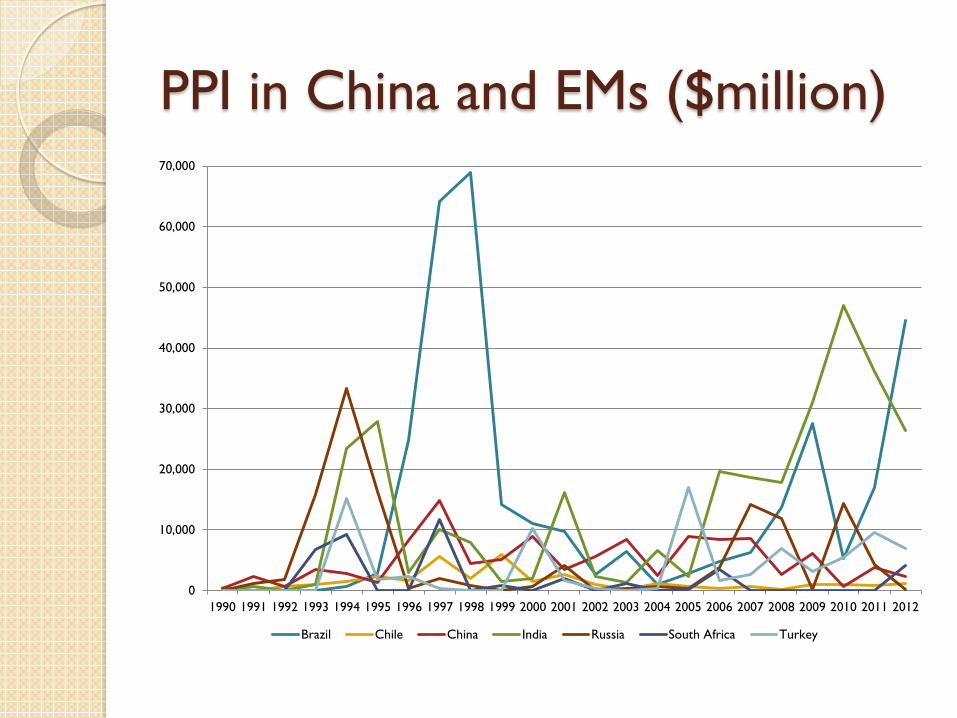

PPI in China and EMs ($million)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Brazil Chile China India Russia South Africa Turkey

Intl investor preference

Based on Preqin survey of 75 institutional investors (2012).

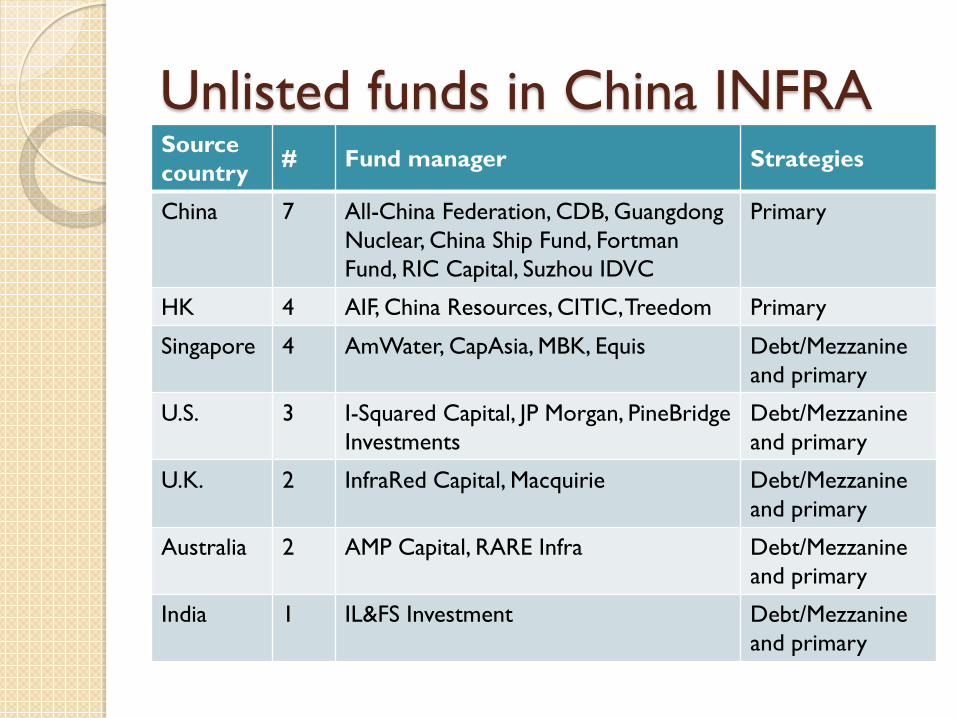

Unlisted funds in China INFRA Source country # Fund manager Strategies

China 7 All-China Federation, CDB, Guangdong Nuclear, China Ship Fund, Fortman Fund, RIC Capital, Suzhou IDVC

Primary

HK 4 AIF, China Resources, CITIC, Treedom Primary

Singapore 4 AmWater, CapAsia, MBK, Equis Debt/Mezzanine and primary

U.S. 3 I-Squared Capital, JP Morgan, PineBridge Investments

Debt/Mezzanine and primary

U.K. 2 InfraRed Capital, Macquirie Debt/Mezzanine and primary

Australia 2 AMP Capital, RARE Infra Debt/Mezzanine and primary

India 1 IL&FS Investment Debt/Mezzanine and primary

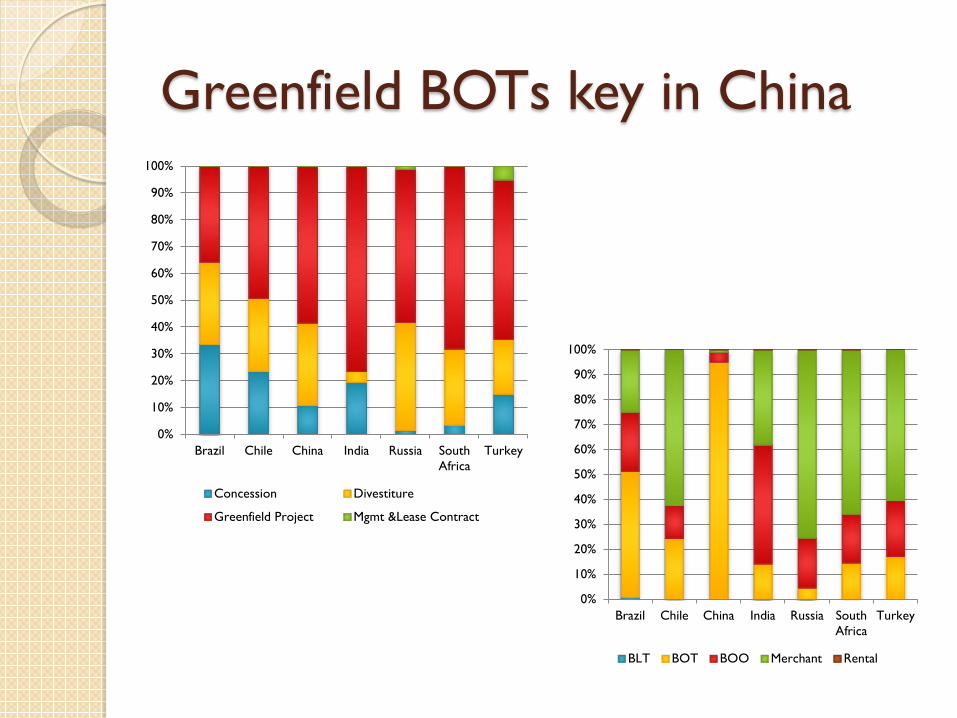

Greenfield BOTs key in China

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil Chile China India Russia SouthAfrica

Turkey

Concession Divestiture

Greenfield Project Mgmt &Lease Contract

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil Chile China India Russia SouthAfrica

Turkey

BLT BOT BOO Merchant Rental

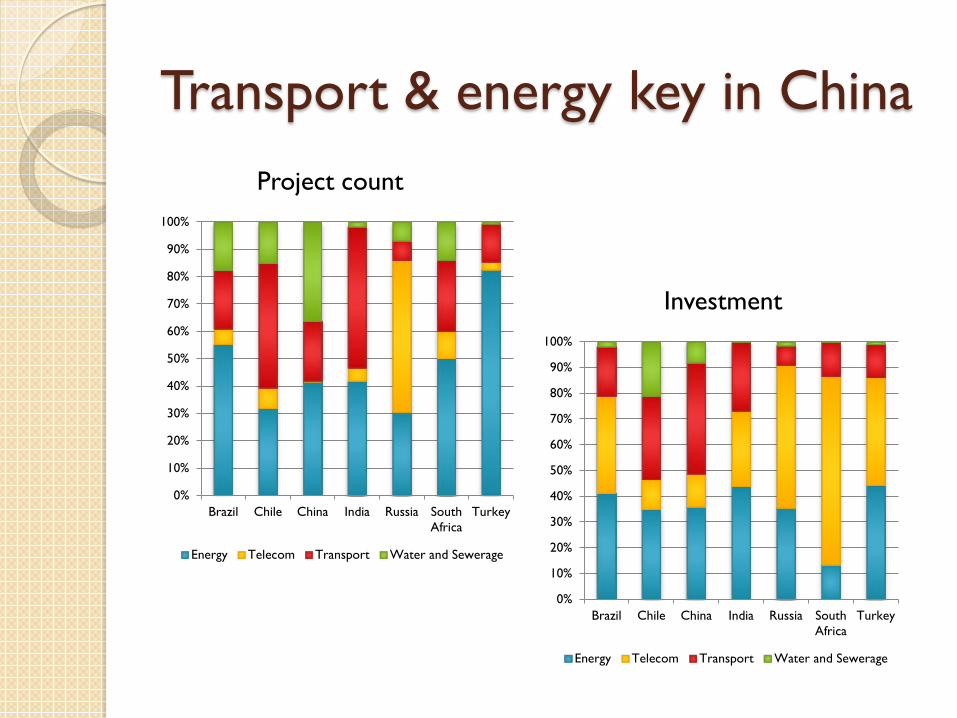

Transport & energy key in China

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil Chile China India Russia SouthAfrica

Turkey

Energy Telecom Transport Water and Sewerage

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Brazil Chile China India Russia SouthAfrica

Turkey

Energy Telecom Transport Water and Sewerage

Project count

Investment

Risk premiums Regulatory risk ◦ “Regulatory environment is first-order issue:

with transparent, published rules, and independent of politics” ◦ “Chinese infrastructure space is ‘a black box’

due to unpredictable regulations” Currency risk ◦ Higher than expected by domestic investors

Demand risk General business risk

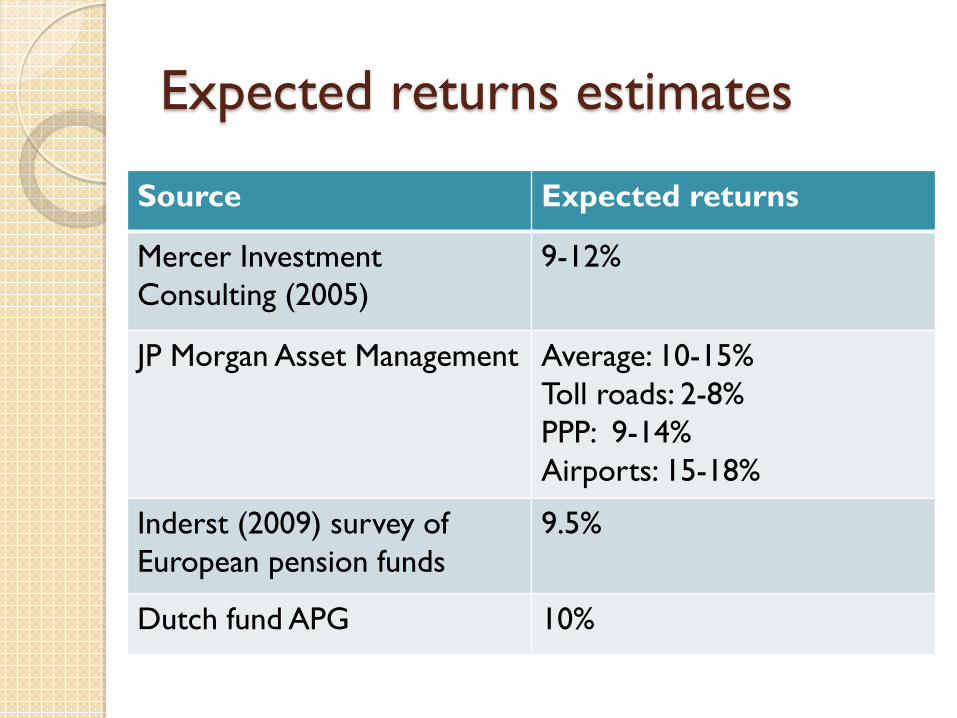

Expected returns estimates

Source Expected returns

Mercer Investment Consulting (2005)

9-12%

JP Morgan Asset Management Average: 10-15% Toll roads: 2-8% PPP: 9-14% Airports: 15-18%

Inderst (2009) survey of European pension funds

9.5%

Dutch fund APG 10%

Investment vehicles in China

Common

• Bank loans + fiscal allocation • Corporate bonds issued by LGFVs • Equity in registered service providers • WMPs by non-bank financial intermediaries

Potential

• Municipal bonds (piloting in 10 cities) • Regional infra banks • Municipal development funds

Difficult

• Foreign equity in RMB funds • Chinese insurance companies equity in RMB funds

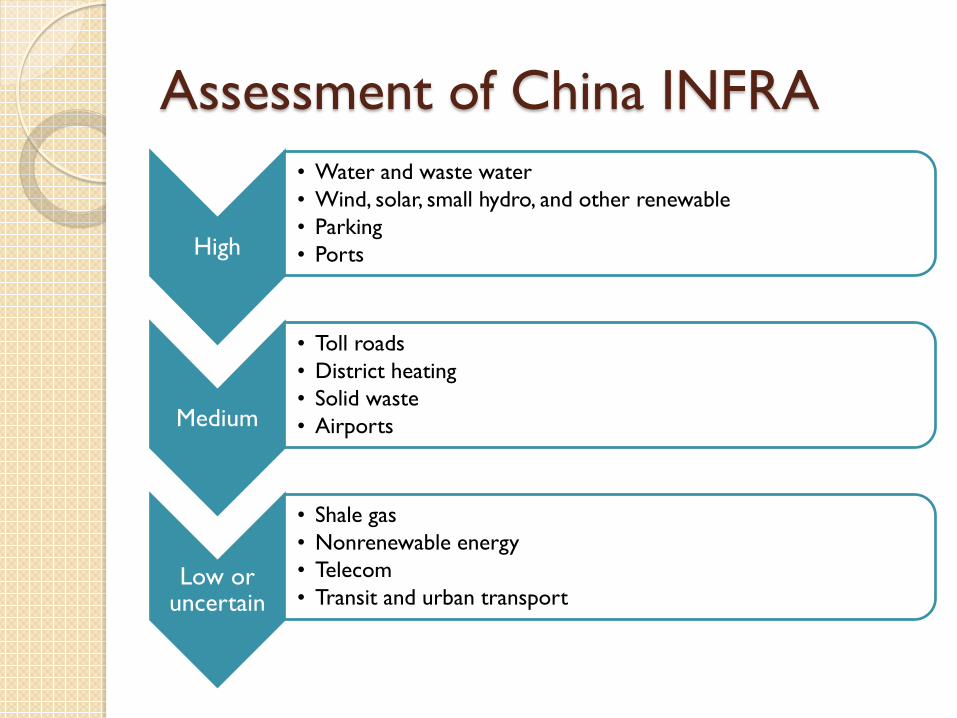

Assessment of China INFRA

High

• Water and waste water • Wind, solar, small hydro, and other renewable • Parking • Ports

Medium

• Toll roads • District heating • Solid waste • Airports

Low or uncertain

• Shale gas • Nonrenewable energy • Telecom • Transit and urban transport