Workspace Group PLC Interim Results For the six months to 30 September 2004.

InfrastructureIndiaplc

Interimresultsforthesixmonthsended30September2012

1

InfrastructureIndiaplc,anAIMlistedinfrastructurefundinvestingdirectlyintoassets in India, is pleased to announce its interim results for the six monthsended30September2012.FinancialPerformance ValueoftheCompany’sinvestmentsincreased2.6percentto£222.4million NAVincreased14.5percent.to£237.3million NAVpersharewas£0.65asat30September2012(2011:£0.88) DepreciationoftheIndianRupeeagainstSterlingresultedinanapproximate

£9millionnegativeimpactontheaggregatevalueoftheportfolioholdingsSignificantDevelopments TheCompanycompletedtheplacingof123,899,118ofnewordinaryshares

of1peachatapriceof33ppershareinAugust2012toraiseapproximately£40.88million(beforeexpenses)

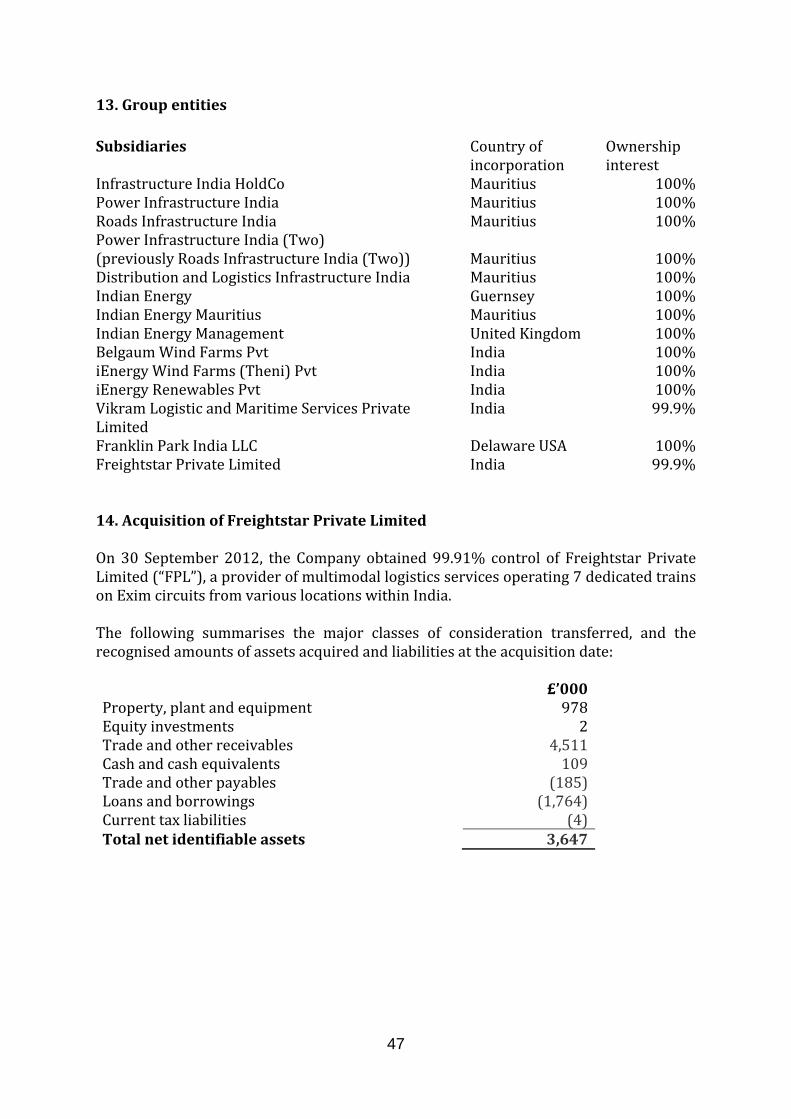

TheproceedsofthefundraisingfromtheplacingwereusedtorepayaUS$25million working capital loan (approximately £15.6 million) to IIP BridgeFunding, LLC, an affiliate of Guggenheim Global Infrastructure CompanyLimited ("GGIC"), fundworking capital, andmake further investments intoVikram Logistic and Maritime Services Limited (“VLMS”) to fund itsexpansion plans (including the acquisition from ETA Engineering PrivateLimited (“ETA”) of inter alia its logistics division and a wholly ownedsubsidiary, Freightstar Private Limited (“FPL”), collectively referred to as“Freightstar”).

FinalisationofGovernmentapprovalsforVLMStoacquireland,buildamulti‐modal logistics terminal, commence constructionand create security of theacquiredlandatBangaloreinfavourofitslenders

ConstructionstartedinJune2012atVLMS’proposedBangaloreandChennaiterminals.

Commencement of initial operations at VLMS’ Chennai and Bangaloreterminals and at Freightstar’s Nagpur terminal pursuant to lenderrequirements.

Acquisitionofsubstantially,theentireissuedequityofETA’ssubsidiaryFPL. Agreements with customers of ETA’s logistics division novated in favor of

FPL. Joint Venture between FPL and Mercurio Pallia a leading automobile

transportationcompanyinIndia,toestablishanautomobile‐logisticsparkatFreightstar’sterminalatNagpur.

ReceiptbyShreeMaheshwarHydelPowerCorporationLimited(“SMHPCL”)of approval from the Government of India’s Ministry of Environment andForests and the National Green Tribunal to commence initial filling ofreservoir and power production from three installed units (of the total 10units). Full commercial operations can only be achieved after additionalequityinvestmentofapproximately£40millionbythepromoterEntegraandthereleaseofproratadebtbySMHPCL’slenders.

2

Weak and delayed monsoon rainfall resulting in lower power productionfrom IHDC’s operating hydropower projects in Maharashtra and HimachalPradeshduringtheperiodsinceJune2012.

Heavyrainsandanoverallslowdownintheeconomymoderatingthegrowthof tolling at Western MP Infrastructure and Toll Roads Private Limited’s(“WMPITRL”)tollroad.

Conversion of Indian Energy Limited’s (“IEL”) Theni project into a GroupCaptive project at a higher overall tariff, significantly improving revenuecollectiontimesandcashflows.

Improved and consistent grid availability in Tamil Nadu and an excellentwind profile during the monsoon period resulting in better than expectedpowerproductionfromIEL’swindenergyprojects.

Postperiodend Completion by ETA of conditions precedent to closing and finalising

agreements to allow VLMS to complete the purchase of remaining landrequiredfortheproposedPalwalfacility.

Approval frommemberbanksofVLMSandFreightstar lenderconsortia forVLMStocompletetheacquisitionofFreightstar.

ConsentbylenderconsortiaofVLMSandFreightstartocommencereleasingdebt funds from existing approved debt facilities to allow expeditedconstruction.

Commencement of the procedural formalities to transfer the assets ofFreightstartoVLMS.

Commentingontheoutlook,TomTribone,ChairmanofIIP,said:“Theseresultsdemonstrategoodmomentum inourbusinessdespitethepresentlydifficultconditionsforinvestinginIndia.NAVhasincreasedduringthefirsthalfasaresultofthecontinuedprogresswehavemadeindevelopingtheportfolio.TheplacingwecompletedinAugusthasreducedthefinancingriskassociatedwithIIPandhasallowedustoworktowardsclosingtheacquisitionofFreightstar.InsodoingwewillbecreatingoneofIndia’stopthreelogisticscompaniesfollowingitsfullintegrationintoVLMS.Wewillneedtoraiseasmallamountofworkingcapitalin theNewYear,whichcould involve thedisposalofnon‐coreandmatureassetsthatarealreadycashgenerative.”SonnyLulla,ChiefExecutiveofIIP,said:“We are pleased to beworking towards the full integration of Freightstar intoVLMS.Thesearetwobusinessesthatdovetailverywellwithoneanotherandwhilstthe logistics segment is currently facing some short‐term cyclical pressure, weexpectthatour integratedsolutionwillbe inconsiderabledemandwhenbusinessactivityinIndiarebounds.

3

Therequirement forenergy in India issignificantandgrowingwhichwillbenefitkeyassetswithinourportfolio.TheShreeMaheshwarhydropowerprojectinwhichwehave investedcontinues itssteadyprogresstowardscompletion.OverthepastfewmonthswehavesecuredahighertariffonIndianEnergy’sTheniprojectandmadeprogress in thedevelopmentof IHDC’sportfolioofprojects..OurconsistentstrategicfocusonthetransportandenergysectorsmeansthatIIP’sgrowthwillbebroadlytiedtoIndia’slong‐terminvestmentprospectsandeconomicdevelopment,andtheseremaincompelling.”

4

JOINTSTATEMENTFROMTHECHAIRMANANDTHECHIEFEXECUTIVEOFINFRASTRUCTUREINDIAPLC

IntroductionWe are pleased to report the results for the six‐month period ended 30September2012onbehalfof Infrastructure Indiaplc ("IIP", the“Company”orthe“IIPGroup”).Inthisstatement,wereviewthefinancialperformanceoftheIIPGroup, including the additional investmentsmade and other developmentssinceourlastfullstatement.InvestmentStrategyThe Company’s investment strategy remains to provide its shareholders withbothcapitalgrowthandincomebyfocusingoninvestinginassetsintheIndianinfrastructure sector, with particular emphasis on energy and transportationbusinesses.InevaluatingpotentialinvestmentsfortheIIPGroup,IIP’smanager,GuggenheimGlobalInfrastructureCompanyLimited("GGIC")(viaitssubsidiaryGuggenheimFranklin Park Management, LLC (“GFPM”)) requires that any investmentproposaldemonstratesthefollowingkeycharacteristics: an investmentreturnappropriate to theassetbutonewhich isexpected to

offerabaseIRRofapproximately15percentperannumtoitsshareholdersintheeventtheprojectisheldtotheendofitslife;

significant minority interests with “negative control”, or outright majorityinterests;

ahighqualitypartnerandmanagementteam;and negotiatedasopposedtoauctionedtransactions.Inaddition,GGICwouldgenerallyfocusonopportunitieswhichareclosetothecommencementofoperations–typicallymakinginvestmentsinassetswhicharein construction at the time of investment but which would be expected tocommenceoperationswithin30months.FinancialPerformanceThe value of the IIP Group’s investments in its subsidiaries increased from£216.7millionto£222.4million,followingadditionalinvestmentsintoVLMS,IEL,IHDC and FPL. The Company’s NAV increased from £207.3 million to £237.3million.NAVpershareasat30September2012was£0.65(at31March2012:£0.95;at30 September 2011: £0.88). The Company’s overall NAV increased during theyear as a result of progress made on investments, while NAV per share fellprimarilyasaresultof thedilutiveshareplacingcompletedinAugust2012. Inretrospect,completingtheplacingandsubstantiallyreducingthe financingriskassociated with the Company and its subsidiaries appears to have been the

5

correct course of action. As a result of the receipt of lender approvals andcompletion of conditions to closing by ETA and VLMS, the closing of theFreightstar acquisition is expected to be completed late in 2012. We remainconfidentthattheclosingofthetransactionandrelatedfinancingwill leadtoasubstantialrecoveryinNAVpershare.There has been an approximate 4 per cent depreciation of the Indian RupeeagainstSterlingfromINR81.45perGBPtoINR84.86perGBP.Thedepreciationoverthetwelvemonthperiodfrom30September2011is9percent(fromINR77.53perGBPtoINR84.86perGBP).Theimpactofthedevaluationonthevalueof the Company’s portfolio holdings during the reporting period was largelyoffsetbyareductioninthe10yearIndianGovernmentbondrate–therisk‐freerate. However, we note that since the end of the reporting period, the IndianRupeehascontinuedtoweakenandstoodatapproximatelyINR88.13perGBPon30November2012.Forconsistency,thefinancialstatementsincludethefinancialstatementsoftheCompanyor"parent‐only"reports,includingtheStatementofFinancialPositionfortheCompany.Inthisstatement,assetvaluesareshownonafairvaluebasis.Additionally, the financial statements include Consolidated Statements which,because the IIP Group now comprises operating subsidiaries, primarily showsassetvaluesatcostasopposedtofairvalue.InvestmentUpdateDuring thereportingperiod, theCompanycontinued tomake investments intoitsportfoliocompaniestoincreasethescaleoftheIIPGroup.TheCompanymadeinvestmentsintoVLMStofundconstructionatitsterminalfacilitiesandprovideworking capital. These investments played a pivotal role in enabling VLMS tomakeprogressonconstructionactivitiesandprovideconfidence to its lenders.In addition, the infusion of working capital enabled VLMS to increase theutilisationof its truck fleet.TheCompany’s investment in IHDChelped to fundtheconstructionofits8MWRauraprojectinHimachalPradesh.TheCompanyalsomadenominalinvestmentsintoIELtofunditsworkingcapitalneeds.VLMSacquisitionofFreightstarOn28October2011theCompanyannouncedthatVLMShadagreedtoacquirethelogisticsbusiness,relatedassetsandassociatedliabilitiesofFreightstar,thelogistics division of ETA for consideration of approximately £9million in cash(lessanyamountsadvancedprior tocompletion).During the reportingperiod,VLMS renegotiated the purchase consideration with ETA to approximately £7million. On account of inordinate delays by ETA in the completion of criticalconditionsprecedenttoclosing(stemmingfromaliquiditycrisisatETA),VLMSfurther renegotiated the purchase terms with ETA. Under the revised terms,VLMSwouldnotmakeany furtherpaymentsofpurchaseconsideration toETAandinsteadwouldusetheremainingamountspayabletoETA,todirectlypayforthe acquisition of certain remaining land parcels at Freightstar’s proposedterminal at Palwal in the national capital region (subject to all other closing

6

conditionsbeingcompletedanddocumentationfortheregistrationofsuchlandparcels also being completed). Freightstar also obtained the approval of theIndianRailwaystotransferitsCategoryIraillicensetoVLMS.With complementary attributes and synergies between VLMS and Freightstar,this acquisition will expand the business plan of the combined entity and isexpected toprovideattractivereturns toVLMSand the IIPGroup.Todate, theCompanyhasadvancedapproximately£5.4milliontoETAtowardsthepurchaseconsideration. Part of this considerationwas used to acquire substantially theentire issued equity (99.9 per cent) of ETA’s subsidiary, Freightstar PrivateLimited.Currently,FreightstarPrivateLimited,whichformsapartoftheoverall“Freightstar” transaction,ownsthe landacquiredforestablishingtheproposedterminalfacilityatPalwalandETA’sthird‐partylogisticsbusiness.Attheperiodend, VLMS and ETA were awaiting approvals from their respective lenderconsortia to complete the acquisition of Freightstar. A portion of the workingcapitaladvancesmadebytheIIPGroupwerealsousedtooptimiseFreightstar’srailoperations,whichhasenabledittobecomemoreefficient.VLMSliquiditypositionPrior to thereportingperiod, theCompanyhad investedworkingcapital fundsinto VLMS to retire an unsecured loan facility which had come due. Withsubsequent minor working capital infusions, VLMS’ liquidity position hasimprovedsubstantially.However,wenotethatVLMSisinatransitionphaseandwill be in a position to significantly improve its profitability and liquidityposition only after substantial completion of its terminal facilities and anincreaseincommercialactivityatthesefacilities.TollroadTheCompany’s investment inWesternMP Infrastructure&Toll RoadsPrivateLimited (“WMPITRL”) continues to make steady progress. While tolling hadbeenmuch ahead of initial estimates, the traffic along the toll road started tostabilise,andcoupledwithunusuallyheavyrainsandanoverallslowingdownoftheeconomy,thegrowthoftollrevenuealongthetollroadstartedtomoderateduringthereportingperiod. Severaladjacent tollroadsegmentsarebecomingoperationaland it isexpectedthat tollrevenueswillcontinuetopickuptothelevelsestimatedwhentheprojectwasinitiallyimplemented.HydropowerprojectsThe rainfall during the 2012 Monsoon season was delayed and has beenrelatively weak, resulting in reduced electricity generation since June 2012.ProductionfromtheBirsinghpurproject,beingimmunetoseasonalrainfall,wasnot affected and stayed ahead of expectations. Several of IHDC’s projects arelocated at irrigation dams and production is dependent on regulated releasesfrom these facilities. Depending on how these releases are regulated over the

7

coming months by the state government, performance of several of theseoperatingprojects couldbe affected.At this timewedonotbelieve the effectswillbematerialtotheperformanceofIIP.In the month of May 2012, SMHPCL received approval from the Ministry ofEnvironmentandForests(“MOEF”)tocommencepartial fillingofthereservoirattheprojecttoanelevationof154M,tobeconductedunderthesupervisionofaninter‐ministerialcommittee.Thecompanyfacedoppositiontothisfillingfromgroups opposed to the project,who alleged that filling the reservoir to 154Mwould submerge homes. The complaints were heard by the National Greentribunal,whoruledinfavourofthecompanyanddirectedthecompanyandtheGovernmentofMadhyaPradeshtocompletethefillinginthreemonths.Withtherevised capital structure agreed to with the project’s lenders and variousGovernmental entities, SMHPCL still needs an equity investment ofapproximately£40milliontotriggerproratadisbursementsofdebttocompletethe project. The project’s promoter, Entegra is currently in the process ofarranging the needed equity funding, but is facing delays due to the difficultfinancing environment in the country and associated with the project. Theproject’slenderscontinuetoputasubstantialamountofpressureonEntegratoinjecttheincrementalequityneededassoonaspossible.IntheeventEntegraisunabletoarrangetheequity,thelenderscouldtakeanyandallremedialactionsavailable to them under the project loan agreements, including seeking theremoval of the promoter. It is not possible to predict with any degree ofprecisionwhat impactsuchamovemighthaveon thevalueof the IIPGroup'sinvestmentintheproject.WindenergyInadditiontoamarkedimprovementingridavailabilityinTamilNadu,thewindregime has been quite favorable during the 2012 Monsoon period. This hasresultedinbothIEL’sprojectsoperatingatnearP50levelsandproducingmoreelectricity than they ever did. Further, cash flows from theTheni project havesignificantlyimprovedthroughsalestoprivateoff‐takersatahighertariffunderthe group captive arrangement. Long overdue payments from the Tamil NaduElectricityBoardarealsobeingcollectedbyIEL.Inaddition,IELhasbeenabletoreducetheinterestrateatbothofitsprojectsby0.50percent.Asaconsequenceof the framework agreement it signed with a wind energy developmentcompany, Trishe, IEL continues to make progress on expanding its projectdevelopmentpipeline.PlacingofsharesAsdiscussedintheCompany’sannouncementof24August2012,theCompanyplaced123,899,118newordinarysharesof1peachatapriceof33ppershareon 23 August 2012 to raise approximately £40.88 million (before expenses).With this placing, the Company now has 342,660,000 of ordinary sharesoutstanding.TheplacingwasconductedonthebasisofrecommendationsmadebyanindependentcommitteeoftheBoard(the“Committee”),comprisedofM.S. Ramachandran, Timothy Stocks and Timothy Walker. The directors of the

8

Company appointed by GGIC did not participate in any of the Committee’sdeliberations.ThePlacingwasconductedonbehalfoftheCompanybySmith&WilliamsonCorporate Finance Limited, theCompany’sNominatedAdviser andJointBroker and InvestecBankplc, theCompany’s FinancialAdviser and JointBroker.UseofFundsFundsraisedthroughtheplacingwereutilisedtorepaytheCompany’sexistingtermloan(approximately£15.6million),fundaportionoftheremainingequityneededtocompletetheacquisitionand integrationofFreightstarbyVLMSandfundtheCompany’sworkingcapitalneeds.SubsequentEventsIn early November 2012, VLMS received further written orders from theGovernment of Karnataka that allowed VLMS to acquire the land previouslyconsolidated in Bangalore for the purpose of building its proposed terminalfacilities. These orders provide VLMS with sufficient flexibility to utilise itsfacility for a variety of freight storage, handling and warehousing purposes.Theseordershavealsofacilitatedthecreationofsecurityoverthelandinfavourofitslenders,anactionmuchawaitedbycompanymanagementandthelenders.The process of land transfer and mortgage is currently being coordinated byVLMSwithitslenderconsortium.The lenders of both VLMS and Freightstar recommended a structurewherebyFreightstarwouldbeestablishedasadivisionofVLMSinsteadofthepreviouslyapproved structure of keeping it as a wholly‐owned subsidiary. Subsequently,consortiummembershaveapprovedtheacquisitionofFreightstarbyVLMS. Inan attempt to facilitate expedited construction, the lender consortia areconsidering placing the entire undrawn debt amounts in an escrow accountalongwiththeprorataequityneededtoensurethat fundscanbedrawninanexpeditedmannerforconstruction.While the respective lenders of the two companies had been processing theirindividualapprovals for theacquisitionofFreightstarbyVLMS,VLMSandETAhave taken several additional steps to transfer the entire business activities,substantial assets (including exclusive rights to licenses, personnel andmanagementteam,customercontracts,informationtechnologysystemsandtheFreightstarbrand)ofthelogisticsdivisionofETAtoFPL,nowanIIPsubsidiary.ETAhascompleted theregistrationof46acresof land for itsproposedPalwalfacilityanddocuments for the registrationof the remaining24acresatPalwal(tocompletethetotalrequired70acres)arealsocompleteandwillbeexecutedfollowing closing and subsequent funding of the purchase by VLMS.With this,ETA has completed all outstanding conditions precedent to closing and theproceduralformalitiesforclosingthetransactionhavecommenced.

9

VLMS has signed amemorandum of understandingwith BATCO‐RCM‐CFS, theowner of a road‐linked Inland Container depot (“ICD”) at Hyderabad, to takeover the operations of the facility. Currently, the ICD has a throughput ofapproximately 700 twenty foot equivalent units (“TEUs”) per month. It haswarehousingspaceofover2,000sq.m.andapavedareaofover5,000sq.m.Itisequippedwithareachstacker,acraneandthreeforklifts.TheICDalsohasthefacility for bonded warehousing and a fleet of 21 trailers currently serve therequirement of transportation from the ICD to the gateway ports at JNPT(Mumbai)andChennai.Under theproposedarrangement,VLMSwill takeovermanagementoftheICDinreturnforafixedmanagementfeeandaprovisionforprofitsharing.VLMSwilldeployasmallmanagementteamwithmarketingandterminal operating skills to manage the facilities. This opportunity will giveVLMSapresenceintheHyderabadlogisticsmarketwithoutanyinvestment,andthrough synergies with its current and proposed operations (includingFreightstar), provide an opportunity to expand its business operations to newmarkets.WithsupportfromtheCompany’sworkingcapitaladvancestoVLMS,Freightstarhasbeenabletooptimiseitsrailoperationstoprovideahighqualityofserviceto its customers such as Maersk, the largest carrier of containers across theglobe.ItisalsothelargestshippinglineoperatingoutofIndiawithover23percentmarketshare.MaerskhasbeenusingthetrainservicesofFreightstarforthepasttwoyearsformovingcontainersfromtheportsofNhavaSheva(Mumbai),MundraandPipavavtotheICDatLoni in thenationalcapitalregion.Basedonservice quality,Maerskhas nowdecided to use Freightstar’s trains exclusivelyfor movement of its containers from JNPT, Mundra and Pipavav to Loni witheffectfrom1December2012.IHDC anticipates commencement of commercial operations at its 4MWPanwiprojectinHimachalPradeshinthefirstquarterof2013.IHDCalsoanticipatestoreceive shortly formal notification clarifying certain provisions related toincentivepaymentsinatarifforderfromtheMaharashtraElectricityRegulatoryCommission for its Bhandardara II project. This tariff order is expected toincreaserevenuesandalsoimprovecashflows.Postperiodend,IELwasabletosuccessfullyregisteritsTheniprojectasaCleanDevelopmentMechanismunder theKyoto protocol. Following verification, IELwillnowbeabletomarketemissionsreductionsfromitsTheniproject.CompanyLiquidityandFinancingAsof30November2012, theCompanyhad cashavailableof £14.3million.Asdiscussed,whiletheinvestmentcapitalneedsofVLMShavenowbeenfinancedandtheCompanydoesnotfaceadebtmaturityasitpreviouslydid,theCompanywillneedtoraiseworkingcapitalforitsownexpenses(whichareapproximately£6 million per year) by the end of the first calendar quarter of 2013 asanticipated at the time of the placing in August 2012. The Board is currentlyevaluatingalternativesbywhichthesefundscanberaised,includingbyselectivedisposalofassetsinIIP’sportfolio.

10

DividendObjectiveIt is the Company’s objective to pay a covered dividend as soon as practical.However,giventhefactthatinitialoperationsatSMHPCLareyettocommence,theCompany isunlikely tocommencepaymentofa covereddividend in2013.The Board will periodically review and report on progress towardscommencementofadividend.OutlookIEL andWMPITRLarenoweach in aposition toprovide the returns and cashflowsanticipatedtoGroupeitherbywayofreturningcash flowintheyearstocomeorbymeansoftradesale.IHDCisfinancingtheremainingconstructionofits portfolio via its own operating cash flow and all indications, including bytradeofcomparableassetsinIndia,arethatitsNAVisintact.Wearehopefulthatthe ongoing financing activity by SMHPCL’s promoterEntegrawill provide thefunds needed to complete the project and offer IIP the ability to realise itsforecastedinvestmentreturns.UponthecompletionbyVLMSoftheacquisitionofFreightstarandrelatedfinancing,theGroupwillownoneofthethreelargestprivatesectorlogisticscompaniesinthecountry.EachoftheassetsintheIIPGroupportfolioaredescribedinmoredetail inthesection headed, “Review of Investments” below, including an update on therevisedvalueofeachinvestment.TomTribone SonnyLullaChairman ChiefExecutive

11

REVIEWOFINVESTMENTSIndianEconomyandInfrastructureIndia’srealGDPgrowthforthecurrentfiscalyearisprojectedtobebelow6percent, the lowest in a decade. This can be attributed to a variety of global anddomestic factors, including slow growth and policy uncertainty in OECDeconomies, and structural issues suchaspower shortages, poor infrastructure,uncertaintyonpendinglegislationandtaxesonthedomesticfront.As one of the principal drivers of the nation’s economic growth, theinfrastructure sector has been directly impacted by this trend. While theGovernmentofIndiahastargetedinfrastructureinvestmentsofUS$1trillioninthe12thFiveYearPlan(2012‐2017),recentperformancehasnotkeptpacewiththe investment levels needed to meet this target. The principal challengesinclude slow policy reform, delays in land acquisitions and Governmentalclearances,uncertaintyovercoalandwaterlinkages,thepoorfinancialconditionof state‐ownedelectricutilities,difficult financing conditions, andhigh interestrates.TheGovernmentof Indiahasannouncedseveral initiativesandmadeprogressonpreviouslyannouncedactionstotacklemanyoftheseissues.Theseinclude:

Draftsofnewlandacquisitionandminingbills Establishment of a new National Investment Board (“NIB”)to expedite

clearancesforlargeprojects Progress in defining the operational structure of the previously

announcedInfrastructureDebtFunds(“IDFs”).TheIDFsareexpectedtofacilitate the availability of long term debt funding for infrastructureprojectsandalso tocreate liquidity in thebankingsector for fundingofnewinfrastructureprojects

LiberalisingExternalCommercialBorrowings(“ECB”s)forinfrastructureandpermittingtheuseofECBstorepayexistingRupeeloans

ReductioninwithholdingtaxoninfrastructurebondsandECBs AllowingForeignDirectInvestment(“FDI”)inmuti‐brandretail TaxreformincludingthelongdelayedDirectTaxCodeandtheGoodsand

ServiceTax(“GST”)Additionally, economistswidely expect inflationary pressures to ease allowingtheReserveBankofIndia(“RBI”)tolowerinterestrates.Many of these reforms, when enacted, should have a positive impact on thebusinessactivitiesofeachofIIP’sportfoliocompanies.

12

PowerSectorIndia addednearly 9GWof installed capacity in the first sevenmonths of the2012‐2013 fiscal year (approximately 50 per cent of its targeted capacityaddition for the year) to achieve a total installed capacity of 209 GW as ofOctober2012.Whilethisisasignificantaccomplishment,theCentralElectricityAuthority (“CEA”)estimates that thecountryexperiencedanactual shortfall inelectricityproductionofapproximately8.5%inthefirstsixmonthsofthe2012‐2013fiscalyearandprojectsashortfallof9.3%forthefullfiscalyear.TheCEAalso projects a shortfall of 10.6% in peak demand for the year. Amid thebackdropof continuing shortfalls, theGovernmentof India revised its capacityadditiontargetsforthe12thFiveYearPlanfrom76GWto88GW.Renewables,atabout30GW, constituteamuch larger shareof this target thanpreviously.Tomeet these ambitious targets, the Government has estimated a fundingrequirementofUS$275billionoverthePlanperiod.In the lastweekof July2012, thecountrywitnessed theworld’s largestpowerblackoutrenderingover700millionindividualswithoutpoweracross22Indianstates. This blackoutwas caused by a failure of the country’s northern powergridwhiletransferringover4GWofpowersupplyfromthewesterngridtomeetpeakdemand. Toprevent a recurrence of such an event, theGovernment hastakenpreliminarystepstooverhaulthecurrentpowergrid,involvingaplannedexpenditure of overUS$18 billion over the upcoming five‐year plan period ongrid improvements. The improvements will include provisions for linkagesbetween the various grids comprising the network to facilitate transfer ofsurpluspowerfromsurplustodeficientregions.The12thPlanalsoaimstoplacea major emphasis on grid optimization by expanding privatization of utilities,reducingnetworklosses,andimprovingefficiencyofservice.As reported in IIP’s review of investments as at 31March, 2012, the financialcrisis being faced by many state‐owned electricity distribution companies(“Discoms”)hascontinued tobeadragon thepowersector.TheaccumulatedlossesbyDiscomsareestimatedtoexceedUS$36billion.Thereasonsfortheselosseshavebeenwell documented and includeunfundedmandates fromStateGovernments, high arrears, low tariffs causing anunder‐recoveryof costs, andhighaggregatetechnicalandcommerciallosses.TheGovernmentofIndiatookamajorstepinaddressingtheprobleminlateSeptember2012,whenitapprovedabailoutplanfordistressedDiscoms.Theplaninvolvestheassumptionof50percentoftheDiscom’soutstandingshort–termliabilitiesbytheStateGovernmentandareschedulingoftheremaining50percentthroughinstrumentsbackedbyState Government Guarantees. The latter involves the Discoms agreeing to“concrete, measurable actions to improve their operational performance”.ThoughthisrestructuringplanisexpectedtoimprovethefinancialconditionofDiscoms (especially in seven states that have been particularly affected), asustainedimprovementinthepowersectorisonlylikelytooccurwhenDiscomscan improve service delivery, reduce losses and be allowed tariffs that permitappropriateandtimelycostrecovery.

13

Afterseeingrobusttradingactivityandattractivepricingintheearlypartofthecurrentfiscalyear,bothtradingvolumesandpricesofRenewableEnergyCredits(“REC”s) have stalled as of September 2012. The principal reasons relate toelectricity utilities in several states not meeting their Renewable PurchaseObligations (“RPO”s) on account of financial constraints. While penalties areprovidedforintheregulations,thedefaultingutilitiesinsomestateshavebeengiven a reprieve by their respective state regulatory commissions. TheGovernmentofIndiahasrecognizedtheimpacttotheRECmarketresultingfromalackofconsistentenforcementoftheRECregulationsandiscurrentlyplanningcorrectiveactions.AnimprovementintheenforcementofRPOscoupledwiththefinancial bailout plan for distressed utilities is likely to improve the tradingvolumesandpricesofRECs.In an effort to attract long‐term foreign investments in the power sector, theGovernment amended itsFDIpolicy tonowallow investmentsofup to49percentinpowerexchangesinthecountry.Thepolicyalreadyallowed100percentinelectricitygeneration,transmission,distributionandpowertrading.RoadsSectorPolicy reforms in 2009 led to robust pace of project award and constructionactivityintheroadssectorinIndia.However,theeffectsofthereformsstartedtotaper off mainly due to high financing costs, intense competition for projects,lower than expected traffic, andhighly leveraged balance sheets of developers(including from project delays and lower traffic growth). To attract higherinterestand investments fromtheprivate sector, the roadssectorhas recentlywitnessedtwosignificantpolicyreformmovesfromtheGovernmentofIndia.Under the first policy reform, the Cabinet Committee of Infrastructure (“CCI”)approved the Engineering, Procurement, and Construction (“EPC”) model ofconstruction for two‐laning projects. As per the new approved model, EPCprojects are to be awarded on a turnkey basis assigning investigation, design,andconstructionresponsibilitiesontothecontractorforalump‐sumprice.ThenewEPCmodelisexpectedtoeffectivelyaddressdrawbacksoftheearliermodelofitem‐ratecontracts.DuringFiscalYear2012‐2013,MinistryofRoadTransportandHighwaysandNationalHighwayAuthorityofIndia(“NHAI”)areexpectedtoaward3,000–4,000kilometersofEPCprojectsrepresenting32‐42percentoftotalexpectedprojectawards.In thesecondpolicyreform, theCCIalsoapprovedtheOperation,MaintenanceandTransfer(“OMT”)policy.Underthispolicy,theOMTconcessionairewillberesponsibleforperiodicmaintenanceoftheroadwaystretchincludinglevyandcollection of toll tax. The concession period is likely to range between 4 yearsand 9 years. In return, the concessionaire will be required to pay a fixedpremium to thegovernment,which isdecidedduring thebiddingprocess.TheCCI has approved six OMT projects with a total length of 963 kilometers. Forfiscal year 2012‐2013, the CCI is expected to award OMT projects for a totallengthofapproximately4,000kilometers.

14

Despite the difficult economic environment, the road sector had made steadyprogress in terms of awarding new projects and completing earlier awardedprojects.Inthefirstsixmonthsoffiscalyear2012‐2013,NHAIawardedprojectsforatotallengthofapproximately575kilometers.Withthenewpolicyreforms,the Government expects the project award rate and construction progress topickupsignificantlyinthesecondhalfoftheyear.Existing operational toll road projects, such as IIP’s portfolio companyWMPITRL, are likely to benefit as other connecting stretches of high qualityroads become operational. Access to cheaper, long‐term debt and the widelyanticipatedlooseningofmonetarypolicybyRBIarealsolikelytoimprovecashflowforoperationalprojects.LogisticsSectorTheLogisticssectorinIndiagrewslowerthanexpected,astheoveralleconomicenvironmentremaineduncertaindomesticallyandglobally.Althoughthesectoris likely to face near‐term cyclical pressure, it is also expected to benefitsignificantly with improving visibility on medium to longer‐term key growthdriverssuchasdevelopmentoftheDedicatedFreightCorridor(“DFC”)andFDIintheretailsector.TheDFCproject entails building two corridors connecting key trade hubs andmetropolitancities inWesternandEastern India.Havingsecuredamajorityofthedebtrequirementfortheproject,theIndianRailwayshasstartedthebiddingprocessforthefirstphaseoftheEasternandWesterncorridors.PhaseIofboththecorridorsareexpectedtobecompletedby2017.ContainerTrainOperators(“CTO”)areexpectedtobenefitastheirunitcostsshouldreducewithincreasedasset turnover and faster turnaround. Trailing loads are expected to increasefromapproximately4,000tonstoapproximately15,000tons,carryingcapacitytoincreasefrom90containersto400containers(bydoublestacking),maximumspeedtoincreasefrom75kmphto100kmphandstationspacingtoreduceto7‐10kilometersfrom40kilometers.InSeptember2012,theGovernmentofIndiaannouncedapolicyallowing51percentFDIinmulti‐brandretailand100percentinsinglebrandretail. Ifpassed,thispolicymoveislikelytohaveasignificantimpactonthetransportationandlogisticssectorinIndia.Aspertheproposedpolicy, foreigncompaniesarealsorequiredto invest50percentoftheirexpenditures indevelopingandbuildingfront‐endandback‐endsupplychainsystems.Thisislikelytobenefitcompaniesprovidinglastmiledelivery,warehousing,andthelogisticservicesbusiness.Withthefundamentalgrowthdriversremaining intact, therecentslowdowninthelogisticssectorisnotexpectedtobesustained.Companieswithasset–basedbusiness models and those currently in the investment mode are expected togainsignificantlyastheeffectofpolicyreforms,anup‐turninconsumptioncycle,developmentofDFC,andaneasingofmonetarypolicyleadtochangeinbusinessandinvestmentsentiment.IIP’sportfoliocompany,VLMS,hasremainedfocusedon developing and completing assets (container terminals and Free Trade

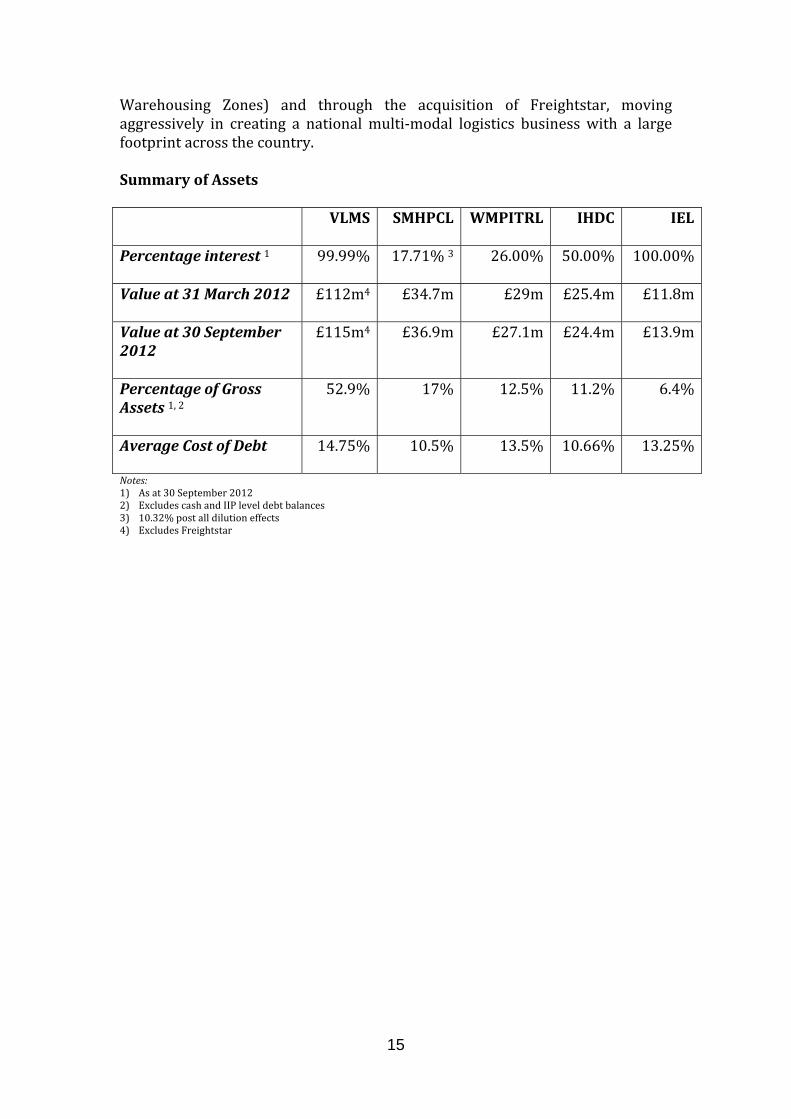

15

Warehousing Zones) and through the acquisition of Freightstar, movingaggressively in creating a nationalmulti‐modal logistics business with a largefootprintacrossthecountry.SummaryofAssets

VLMS SMHPCL WMPITRL IHDC IEL

Percentageinterest1

99.99% 17.71%3 26.00% 50.00% 100.00%

Valueat31March2012

£112m4 £34.7m £29m £25.4m £11.8m

Valueat30September2012

£115m4 £36.9m £27.1m £24.4m £13.9m

PercentageofGrossAssets1,2

52.9% 17% 12.5% 11.2% 6.4%

AverageCostofDebt

14.75% 10.5% 13.5% 10.66% 13.25%

Notes:1) Asat30September20122) ExcludescashandIIPleveldebtbalances3) 10.32%postalldilutioneffects4) ExcludesFreightstar

16

VikramLogisticandMaritimeServicesPrivateLimited(“VLMS”)SummaryDescription: Supplychaintransportationandcontainer

infrastructurecompanybasedinSouthernIndia.Promoter: IIPDateofInvestment: 3March2011 15October2011AmountofInvestment: £34.8million(implied

value)£58.3million(impliedvalue)

AggregatePercentageInterest:

37.39percent. 99.99percent.

AdditionalInvestment:

£8.9million(betweenJanuaryandMarch2012)

£6.3million(betweenAprilandSeptember2012)

Valuationasat30Sep2012: £114.9million ProjectDebt:EquityRatio(basedonconstructioncosts):

65:35

KeyHighlights: ‐ WrittenapprovalfromtheGovernmentofKarnatakatoconstructamulti‐modallogisticsterminalatitsBangalorefacilityandtheissuanceofagovernmentnotificationfortransferandregistrationoflandinthenameofthecompany.ThisallowsVLMStomortgagethelandtoitslenders

‐ CommencementofconstructionatitsBangaloreandChennaiterminalsites

‐ CommencementofinitialcommercialoperationsatChennaiandBangaloreasrequiredunderVLMS’debtfacilities

‐ AcquisitionofsubstantiallyalloftheissuedequityofFreightstarPrivateLimited,asubsidiaryofETA

‐ TransfertoFPLofmanagementandcontrolofallbusinessactivitiesofETA’slogisticsdivision,includingexclusiverightstotheuseoflicensesandassets,andallstaffandmanagementteam

‐ ConsentbylenderconsortiaofVLMSandETAtotheproposedownershipstructureforETA’slogisticsdivisionwithinVLMS

‐ ApprovaloflendersfromboththeVLMSandETAconsortiafortheacquisitionofFreightstarbyVLMS

‐ Consentby lender consortiaofbothVLMSandETAfordisbursementof funds to complete constructionof facilities previously approved in their individualbusinessplans

17

‐ CompletionbyETAofCPstoclosingandagreementforacquisitionofremainingland(24Acres)atFreightstar’sPalwalsitedirectlybyVLMS,inlieuofpaymentofremainingacquisitionpricetoETA

‐ Completion of land acquisition documents for theremaining24acreslandatFreightstar’sPalwalsite

InvestmentdetailsFollowing the acquisition of all outstanding shares in VLMS fromAnuradhaHoldingsPrivateLimited("AHPL") inOctober2011, the IIPGroupnowowns99.99percentofVLMS. During the reporting period, the Company made equity investments ofapproximately£6.3millionintoVLMS.ThesefundswereutilisedlargelytomeetprojectconstructioncostsandalsotoprovideworkingcapitaltoVLMS.TheIIPGrouphasalsoadvanced approximately £5.4 million to Freightstar between October 2011 andSeptember2012asadvancepurchaseconsideration. VLMS is a supply chain transportation and container infrastructure companyheadquarteredinBangalorewithastrongpresenceinSouthernIndia.VLMSprovidesabroadrangeoflogisticsservicesincluding,trucking,customsclearingandhandling,andbonded warehousing to customers from a range of companies such as Coca Cola,ReserveBankofIndia,CredenceLogistics,PearlHarbour,AmericanPowerCorporationandQatarCargo.VLMSoperatesafleetofmorethan125trucksandanexportorientedContainerFreightStation(‘CFS”)atHassaninwesternKarnataka.Inaddition,VLMSisdeveloping a Free TradeWarehousing Zone (“FTWZ”), bonded container warehousefacilityandDomesticterminals(“DT”)inthecitiesofBangaloreandChennai.Revenue streams fromVLMS’s various business units including FTWZ,DTs, CFSs andservices(includesTransportationandFreightForwarding)arecomprisedof,interalia,handlingcharges, transportation (containersandbulk),warehousing, rent, shipments,leasing, access charges and certain other categories. Market data indicates a steadygrowth in container and freight volumes nationwide, although the global economicslowdown isexpectedtomoderate thisgrowth.With theirproximity tooneof India’smajor ports at Chennai, VLMS’ container terminals at Chennai and Bangalore areexpectedtobenefit from thevolumesatChennaiport.VLMSprovidesvarious serviceofferings and has a leadership position in Southern India, thereby positioning it verywelltotakeadvantageofthegrowthopportunitiesinthelogisticsector.DevelopmentsVLMS has made significant progress towards completing construction work at itsplannedBangaloreandChennaiterminalsandmakingtheseterminalsfullyoperational.Aswas reported in theGroup’s31March2012annual report,VLMS faced significantchallenges ingetting its facilitiesoperational. These includeddelays inregistrationofland acquired for its terminals, receiving required government approvals, creation ofsecurity over the acquired land in favour of its lenders and receiving pro ratadisbursementsofpreviouslyapproveddebtfacilities.TheCompanyishappytoreportthatVLMShascompleted the requireddocumentation in respectof the landacquiredforitsBangaloreterminal,receiveddetailedordersfromtheGovernmentofKarnataka

18

for setting up the requisite infrastructure facility alongwith a permission to transferand register the land in thenameof the company, allowing the land tobeused for avariety of freight handling, storage,warehousing and logistics purposes and allowingthemortgageofthelandinfavourofprojectlenders.Apart from continued construction progress at its Bangalore and Chennai terminalfacilitiessupportedbyequityinvestmentbytheIIPGroup,VLMSalsocommencedinitialcommercial operations at these facilities. Initial operations included storage andhandling of empty containers for shipping lines using its own container handlingequipment.While the formal process of perfecting the security on the project land isprogressing in co‐ordination with lenders, the lenders have taken a much more co‐operativeapproachtowardsthecompanyandhaveindicatedawillingnesstodisbursefurther tranches of debt already approved to facilitate the completion of remainingconstruction activities. Construction at VLMS’ Chennai terminal was held up in lateOctoberandearlyNovemberduetounseasonalrainsandatropicalcyclone.However,construction activities are ongoing and VLMS estimates that construction of theterminal facilitiesatBangaloreandChennaiwillbe substantially complete in the firstquarterof2013.VLMShasalsomadesignificantprogresstowardsacquiringFreightstarandclosingthetransaction.Basedoninvestmentsmade,theGroupcurrentlyownsamajoritystakeinETA’ssubsidiary,FreightstarPrivateLimited.LenderconsortiaforbothVLMSandETA,in separate consortiummeetings proposed a revised structure for the acquisition ofFreightstar wherein the business would be operated as a separate division of VLMSinsteadofbeingawholly‐ownedsubsidiary.Subsequently,membersof theVLMSandFreightstarlenderconsortiahaveapprovedtheacquisitionofthebusinessbyVLMS.Inaddition, the Freightstar lender consortium has consented to funding all remainingapproveddebtfortheFreightstarprojectscopeintoanescrowaccountalongwiththeremaining equity from the Group to ensure that funding is available as needed toexpeditetheremainingconstructionactivities.Further,ETAhasobtainedapprovalfromtheIndianRailwaystotransferitsCategoryIRaillicensetoVLMS.Ithascompletedthedocumentation to register 46 acres of land (of the total 70 acres required) for itsproposedterminal facilityatPalwal in thenationalcapitalregion.Pursuant torevisedacquisitiontermsbetweenVLMSandETAaspreviouslyreported,VLMSwoulddirectlypay for the acquisition of the remaining 24 acres of land at Palwal (subject tocompletion of the documentation for the registration of the land and closing of thetransactionwithETA)foracorrespondingreductioninpurchaseconsiderationpayableto ETA. In this respect, documentation for the registration of the 24 acres of land iscurrentlycomplete.VLMS has taken several steps to consolidate its control over the business andoperationsofFreightstar.Theseinclude: AgreementwithETAallowingFPL,nowanIIPsubsidiary,theexclusiveuseofits

concessionagreementwiththeIndianRailwaysfortheremainderofitstermandallofitsrakesfortheremainderoftheirusefullife

NovationofallofFreightstar’scustomercontractsinfavorofFPL Transferofallmanagement,operationsandadministrativepersonneltoFPL

19

Assignmentofallinformationtechnologysystemsandthe“Freightstar”brandtoFPL

FPL has already executed an agreement with Mercurio Pallia, a leading Indiantransporter of automobiles, to establish an automobile logistics park at Freightstar’sNagpur facility. FPLalsoownsall the land currently acquired forFreightstar’sPalwalfacility.These steps allow VLMS to begin to realise the benefits of the synergies of the twoentities and efficiently manage the combined operations while the process oftransferringtheassetsofFreightstartoVLMSisimplemented.The combined entity is expected to be one the largest private multi‐modal logisticservices providers in Indiawith presence across the country.The combinedbusinessplanexpandstheexistingscopeforthetwoindividualcompaniesandentails,interalia:

developing four container handling terminals at NCR, Nagpur, Bangalore andChennai,

DevelopingoneFTWZatChennai, Operatingcontainertrains(owned&leased)toproviderailconnectivity, Increasing fleet size of trailers to approximately 300 to provide road

connectivity, ExpandingitsThirdPartyLogistic(“3PL”)servicesbusiness

The total project cost of the combined entity is estimated to be approximately INR13,820million(£163million).TheexpandedprojectplanwillbefundedbyINR4,320million(£50.9million)inequityandINR9,500million(£111.9million)indebt.Whilethemajorityoftheequityhasbeeninvested,additionalequityofapproximatelyINR960million(£11million)isneededtocompletethefinancingplan,whichhasalreadybeenraisedbyIIP.Tofullyfundthecombinedexpandedbusinessplan,VLMSisnegotiatingwithseverallendersincludingmembersoftheexistinglenderconsortiaforfundingtherequireddebt.This financingplanwill includerefinancing theexistingdebt.Basedonthe status of the current discussions, VLMS is expecting to receive in‐principleapprovalsandtermsheetsfortherequireddebtinearly2013.InthefirstsixmonthsofFY2012‐2013,VLMS(standalone)reportedtotalrevenueINR77.6 million compared to INR 110.6 million during the same period last year. Asdiscussed in the March 2012 report, VLMS is currently transitioning from being aservice provider to one owning and operating its own container terminals.Historicalrevenues from terminal operating contracts are therefore not currently available toVLMSandthecompany’srevenueslargelycomefromitsroadtransportationbusiness.As a result of working capital support received from the IIP Group, VLMS hassignificantly increased the number of trailers available for its road transportationbusiness.TheIIPGroup’ssupporthasalsoenabledFreightstartoimprovetheefficiencyofitsrailbusinessandnegotiatecontractsforexpandedbusinesswithlargeshippingcompaniesandindustrialcustomers.FreightstarhasbeenselectedbyMaersk,thelargestcarrierofcontainersacrosstheglobe,forexclusivemovementofitscontainersbyrailfrom

20

India’s western ports to the national capital region. These developments allow thecompanytoutilisetheirrakestofullcapacity.Further, VLMS has signed amemorandum of understandingwith BATCO‐RCM‐CFS, aroad‐linkedICDintheCityofHyderabadinsouthernIndiatotakeoverthemanagementoftheterminal.Inadditiontothehandlingofcontainercargo,theICDhasthefacilitytoprovide bondedwarehousing and provides transportation services tomajor ports atMumbaiandChennai.ManagementoftheICDwillbesynergistictoVLMS’currentandfuture operations (including Freightstar) and will allow VLMS to expand businessactivities at the ICD. VLMSwill earn a management fee for its services along with aprovision forprofitsharing.A formalagreement isexpectedtobeexecutedshortly toallowVLMStotakeoverthemanagementfunctionsinthefirstquarterof2013.Asof30September2012,totallongtermdebtwasINR2,240millioncomparedtoINR2,162millionon31March2012.Inthecurrentfiscalyear,IIPinvestedapproximatelyINR557million(£6.3million)tofundconstructionworkatBangaloreandChennaiandotherworkingcapitalrequirements.ValuationAs at 30 September 2012, the asset was valued at £115 million (not including theproposedacquisitionofFreightstar),ascomparedwiththevaluationof£112millionat31March, 2012. The valuationwas conducted using a discounted cash flow (“DCF”)methodologywiththefollowingkeyassumptions:

Riskfreeratebenchmarkedtotheyieldon10‐yearIndianGovernmentbond Risk premiumof 6 per cent, consistentwith IIP’s stated risk premium for “in‐

construction”projects(theprojectriskhasreducedsignificantlyduetoreceiptofthegovernmentapprovals,hencethereductionintheriskpremiumfrom7percentinMarch2012to6percentforthecurrentperiodisconsideredreasonable)

Deriveddiscountrateof14.3percent(basedonabovementionedfactors) Terminalgrowthrateof2percentafter10years

Accounting for IIP’s equity investmentof £6.3millionduring the six‐month reportingperiod, the net asset value of VLMS has declined slightly. This decrease is largelyattributable to delays in completion of its project facilities, which have resulted inincreased project costs and delays in revenue realisation. While the currencydevaluationcontributedtoanapproximately4percentreductionintheNPV,thiseffecthaslargelybeenoffsetbytheimpactfromthereductionoftherisk‐freerate.The valuation of £115 million is reflected in the Company Statement of FinancialPosition, inwhich theCompany’s investments in subsidiariesare shownat fairvalue.However, as VLMS was a wholly owned subsidiary at that date, the ConsolidatedStatementofFinancialPositionincludesaconsolidationofVLMS,asrequiredbyIFRS.Suchaconsolidationbydefinitiondoesnotincorporatethevaluationoftheinvestment.InlightofrecentpositivedevelopmentstowardstheacquisitionofFreightstar,IIPhasconductedapro‐formavaluationexerciseforthecombinedentityusingIIP’sstatedDCFvaluationmethodology.TheproformaNPVofthecombinedentity,postacquisitionandrefinancing,ispreliminarilyestimatedtobehighlyaccretive.

21

WesternMPInfrastructure&TollRoadsPrivateLimited(“WMPITRL”or“WMP”)SummaryDescription: 125kmlong,fourlanehighwaytollroadinWestern

MadhyaPradesh,witha25yearconcessioncommencinginApril2008.

Promoter: EsselGroupDateofInvestment: 30September2008 25June2010AmountofInvestment: £11.3million £0.4millionAggregatePercentageInterest:

26.0percent. 26.0percent.

Valuationasat30Sep2012: £26.07million ProjectDebt:EquityRatio(basedonconstructioncosts):

68:32

KeyHighlights: ‐ UnexpectedheavyrainsandslowereconomicactivityledtolowerthanexpectedtrafficgrowthbetweenAprilandJuly,2012.

InvestmentDetailsOn30September2008, IIP investedapproximately£11.3million(INR960million) inWMPITRL,whichrepresenteda26percentshareholding.WMPITRL,promotedbytheEssel Group,was awarded the concession to a toll road project in central India on aBuild‐Own‐Transfer(“BOT”)basisinAugust2007foratermof25years,commencingfromMarch2008.TheCompanyhasrepresentationontheboardofWMPITRL.OverviewofProjectPerformanceFull commercial tollingbeganalong theentire lengthof the toll roadon4 June2011.Theroadisa125km,four‐lanehighway(StateHighway“SH”31)betweenthetownsofLebadandJaora,whichreplacedtheprevioussinglecarriagewayroad.SH31provideavital connection between the towns along National Highway 8 ("NH8") in easternRajasthanandtheCityofIndore,acommercialhubintheStateofMadhyaPradesh.Thissection of the toll road also provides a connection with NH3, the national highwayconnecting thecitiesofMumbaiandAgra. TheWMPITRL toll roadprovides theonlyhigh quality route to transit the region resulting in a reduction in travel times fromnearlytenhourstoapproximatelytwohourstotravelthe125kmstretch.Thisattributecontributedtoinitialtrafficvolumesandgrowthalongthetollroadtobewellaheadofprojections. TheconcessionagreemententitlesWMPITRLtoescalate the tollchargedeach year by 7 per cent and WMPITRL is applying this annual escalator in full.Approximately80percentofalltollrevenueisderivedfrommulti‐axletrucktraffic.The commencementof operations at theproject hasbeen staged; the first half of theroad began tolling inNovember 2009 (some fivemonths ahead of schedule) and thesecondphasebegantollinginJune2011.Thesecondphasewasdelayedduetochangesin the scope of three railway bridges along the toll road. Since this delay was notattributabletoWMPITRL,thescheduledcommercialoperationsdatewasextendedand

22

penalty avoided. This extension effectively results in an extension of the concessionperiodofapproximately18months.Therearetwotollplazas(TP1andTP2)alongthelengthoftheroadwhicharecontinuouslymonitoredonareal‐timebasis,bothlocallyandattheprojectcompanyheadquartersinMumbai.Thetollcollectionissplitroughlyinhalfbetweenthetwoplazas(67kmforTP1and58kmforTP2).TP1hasnowbeeninoperationforovertwoyears,whereasTP2hasbeenoperationalforover15months.The change in quarterly toll collection observed at TP1 from the same period thepreviousyear,were43percent,48percent,32percentand23percentforthefourquartersinFY2011‐2012.Theprogressivereductiontowardstheendofthefiscalyearislikelyattributabletotrafficvolumesapproachingasteadystateaswellasanoverallslowdownineconomicactivity.Nevertheless,thesetollvolumegrowthlevelswerewellahead of initial projections.While sufficient data is not available to track toll volumegrowthtrendsforthecorrespondingperiodatTP2,thetollvolumesaresimilartothoseforTP1, indicating that the trend is likely similar. The first twoquarters of FY2012‐2013 saw unusually heavy rains in the project region and the growth in toll volumestagnated,withtheoveralltollingstayingnearlyconstant.Thegrowthrateofquarterlytollingforquarterended30September,2012standsatapproximately6percentoverthecorrespondingperiodayearbefore.Trafficvolumesdoexhibit seasonalityduringthe year and there is not sufficient data to project long‐term trends based on theavailable data. However,WMPITRLmanagement believes that some of the seasonalfactors thatcontributedto the lowtolling in the lastsixmonthshavepassedandthattollingwillpickuptoexpectedlevels.Further,projectedcompletioninthenearfutureofadjacent toll roadsectionsconnecting theWMPITRL toll road to thecityof Indore,will positively impact tolling along the roadway. Two connecting state highways(ManpurtoLebadandJaoratoNayagaon)arenowfullyoperational.ThesehighqualityandbroaderstatehighwaysareexpectedtofurtherreducethetraveltimeandprovidebetterconnectivitytothecityofIndore.Asof30September2012, longtermsecureddebtwasINR5621.7million.Short‐termborrowingsandtradepayableswereINR932.4milliononthereportingdate.ValuationWhile TP1, having been operational for over two years represents a “normaloperations”state,TP2atonly15months is still ina “ramp‐up”phase.Analysisof thetrafficvolumedataforTP1andTP2indicatesahighdegreeofcorrelationbetweenthetoll growth rates at TP1 and TP2. In view of this correlation, it was consideredreasonabletouseacompositeriskpremiumof3percentovertheriskfreerateofthe10‐year government bond yield of 8.35 per cent to discount the future cash flows.Further, to account for the observed lower tolling, toll growth rates were furthermoderatedinestimatingthefuturecashflows.The WMPITRL toll road asset was valued at £26.07 million, a reduction ofapproximately 10 per cent compared with the value reported as at 31 March 2012.Approximately 4 per cent of the reduction in NPV was attributable to the observeddepreciationoftheIndianRupeeagainstthePoundSterling.

23

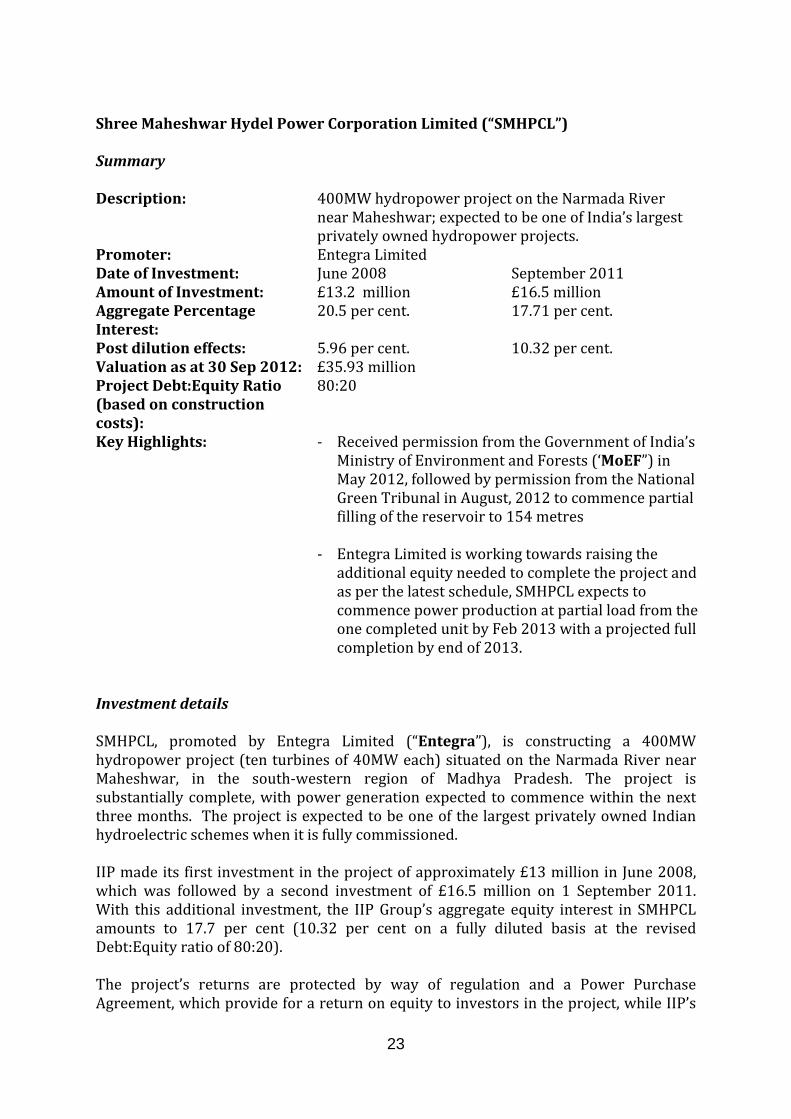

ShreeMaheshwarHydelPowerCorporationLimited(“SMHPCL”)SummaryDescription: 400MWhydropowerprojectontheNarmadaRiver

nearMaheshwar;expectedtobeoneofIndia’slargestprivatelyownedhydropowerprojects.

Promoter: EntegraLimitedDateofInvestment: June2008 September2011AmountofInvestment: £13.2million £16.5millionAggregatePercentageInterest:

20.5percent. 17.71percent.

Postdilutioneffects: 5.96percent. 10.32percent.Valuationasat30Sep2012: £35.93million ProjectDebt:EquityRatio(basedonconstructioncosts):

80:20

KeyHighlights: ‐ ReceivedpermissionfromtheGovernmentofIndia’sMinistryofEnvironmentandForests(‘MoEF”)inMay2012,followedbypermissionfromtheNationalGreenTribunalinAugust,2012tocommencepartialfillingofthereservoirto154metres

‐ EntegraLimitedisworkingtowardsraisingtheadditionalequityneededtocompletetheprojectandasperthelatestschedule,SMHPCLexpectstocommencepowerproductionatpartialloadfromtheonecompletedunitbyFeb2013withaprojectedfullcompletionbyendof2013.

InvestmentdetailsSMHPCL, promoted by Entegra Limited (“Entegra”), is constructing a 400MWhydropowerproject(tenturbinesof40MWeach)situatedontheNarmadaRivernearMaheshwar, in the south‐western region of Madhya Pradesh. The project issubstantiallycomplete,withpowergenerationexpected tocommencewithin thenextthreemonths. TheprojectisexpectedtobeoneofthelargestprivatelyownedIndianhydroelectricschemeswhenitisfullycommissioned.IIPmadeitsfirstinvestmentintheprojectofapproximately£13millioninJune2008,which was followed by a second investment of £16.5 million on 1 September 2011.With this additional investment, the IIPGroup’s aggregate equity interest in SMHPCLamounts to 17.7 per cent (10.32 per cent on a fully diluted basis at the revisedDebt:Equityratioof80:20).The project’s returns are protected by way of regulation and a Power PurchaseAgreement,whichprovideforareturnonequitytoinvestorsintheproject,whileIIP’s

24

returnsare furtherprotectedbywayofanIRRguaranteearrangementoncash flows.TheIIPGroupisexpectedtoearnaminimumIRRof15percentonthefirst£13millioninvestmentandaminimumIRRof17percentonthesecond£16.5millioninvestment.WhilethemaximumIRRfortheIIPGroupisnotcontractuallylimited,theIIPGrouphasagreedtosharereturnsabovecertainthresholdsonthesecondroundinvestmentwithcertain co‐investors in SMHPCL. If the guaranteed IRRs are not achieved on the IIPGroup’sexit,certainescrowedsharesinSMHPCLwillbetransferredtotheIIPGroupatnoadditionalcosttotheIIPGroup,untilthisminimumreturnisreachedorthesupplyof escrowed shares is exhausted. In addition, IIP has representation on the board ofSMHPCL.ThetariffunderthePPAallowsafullpass‐throughofallcostsincurred.Duringthetimebetweenpartialoperationsandfullcommercialoperations,SMHPCLanticipatessellingthepowergeneratedtothird‐partyconsumers.CurrentStatusofProjectFurthertothereceiptoftheapprovalfromMoEFinMay2012tofillthereservoirto154meters abovemean sea level (“MSL”), SMHPCL faced local opposition to filling fromvillagersandoppositiongroupswhoclaimed thathomeswouldbesubmergedeven ifthereservoirwasfilledtothislevel.ThecomplaintswereheardattheNationalGreenTribunal and SMHPCL received permission from the tribunal on August 8, 2012 tocommencepartial fillingof thereservoirat thedamsiteup to154metersaboveMSLandcommencegenerationof40MWofelectricityontrialbasiswithinaperiodofthreemonths. SMHPCL and the Madhya Pradesh Government were also directed by thetribunal to complete the entire process of rehabilitation and resettlement work,includingthesupplyofdrinkingwaterandelectricitytotheaffectedpersons.SMHPCL currently plans to complete the rehabilitation of villagers affected by thereservoirfillingupto160metersaboveMSLandcommencepartialproductionfromthefacility thereafter. Timely completion of these activities is contingent upon SMHPCLraising the remaining equity needed to complete the project. SMHPCL’s promoter,Entegra, is in the process of arranging the remaining equity for the project but issuffering constant delays due to difficult financing conditions in India generally, andmoreimportantly,difficultfinancingconditionsforthisproject.SMHPCL’scurrentplanscallforcompletingtherehabilitationactivitiesandcommencinginitialproductionfromtheplantbyFebruary2013withfullcommercialoperationsbytheendof2013.Theseplans are, however, contingent upon their ability to fund the additional equityrequirementsandobtainproratadebtdisbursementsfromlenders.Once the project is fully operational, it is expected that SMHPCL will, subject tosatisfactionofcustomarylendercovenants,declaredividendsonanannualbasis,basedontheproject’sperformanceandcashflows.FinancingUpdateThe overall cost of the project is approximately £504million (of which project debttotalsapproximately£403millionpertherevisedDebt:Equityratioof80:20asagreedtowithitslendersandtheGovernmentofIndia’sMinistryofPower).Undertherevised

25

financingplan,SMHPCLneedstoraiseanadditional£92millionofdebtand£40millionofequitytocompleteconstructionontheproject.Basedondiscussionswithitslenders,SMHPCLbelievesthatitscurrentconsortiumoflenderswill investtheremainingdebtsubject to theremainingequitybeing funded.Thedelayssufferedby theprojecthaveled its lenders to put a substantial amount of pressure on Entegra to inject theincrementalequityneededassoonaspossible.IntheeventEntegraisunabletoarrangetheequity,thelenderscouldtakeanyandallremedialactionsavailabletothemunderthe project loan agreements, including seeking the removal of the promoter. It is notpossibletopredictwithanydegreeofprecisionwhatimpactsuchamovemighthaveonthevalueoftheIIPGroup'sinvestmentintheproject.ValuationThe asset is valued following the Company's stated valuation methodology (adiscountedcash flowanalysis)whereariskpremium isadded to therisk freerate inIndia(givenby long‐termIndiangovernmentbonds) togivethediscountrateusedintheanalysis.ThestatedmethodologyofIIPistouseariskpremiumof6percentoverthe risk‐free rate for assets in “construction”. Although construction activity on theproject is substantially complete, the project had not commenced operation as at 30September2012.Applyingthediscountrate(6percentplustherisk‐freerate)toIIP’sshareof theproject’scash flowsanddiscounting toavalueasat30September2012,givesavalueforthisholdingof£35.9million(31March2012:£34.7million).Thevaluethereforeremainedsteady,despiteaslightdevaluationoftheIndianRupee.Inconsideringthevaluationoftheproject,therisksdiscussedintheparagraphheaded,“FinancingUpdate”shouldbeconsidered.

26

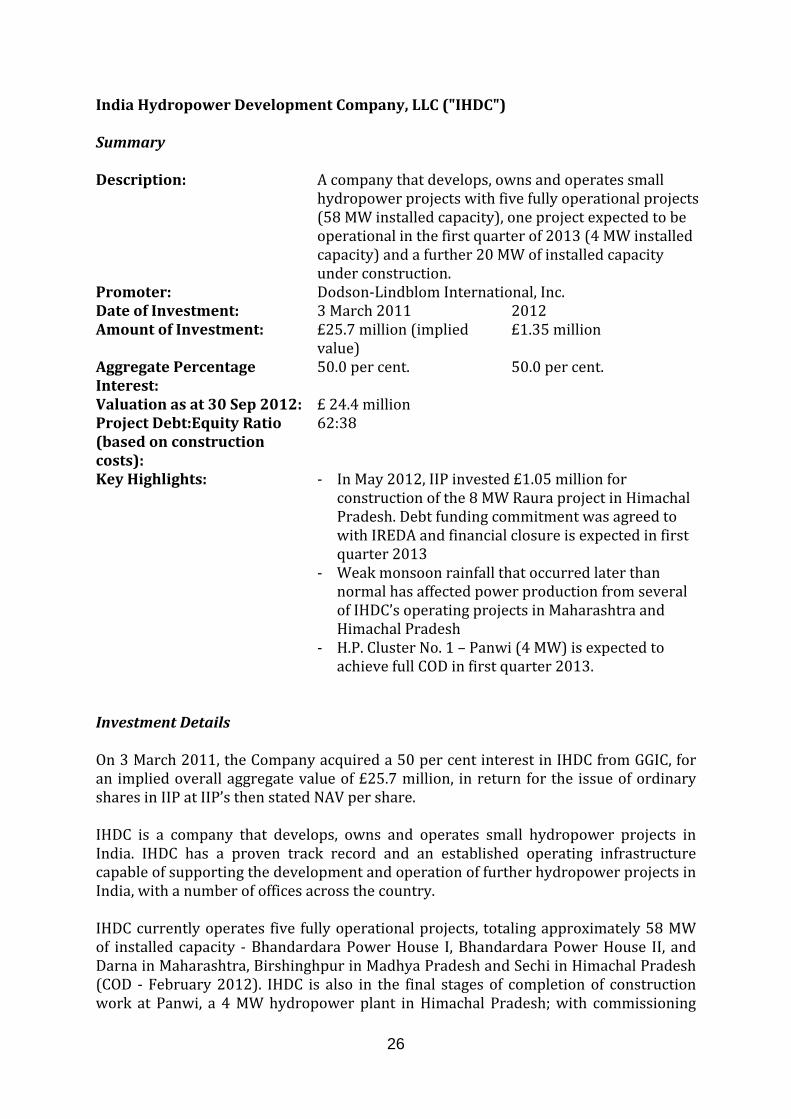

IndiaHydropowerDevelopmentCompany,LLC("IHDC")SummaryDescription: Acompanythatdevelops,ownsandoperatessmall

hydropowerprojectswithfivefullyoperationalprojects(58MWinstalledcapacity),oneprojectexpectedtobeoperationalinthefirstquarterof2013(4MWinstalledcapacity)andafurther20MWofinstalledcapacityunderconstruction.

Promoter: Dodson‐LindblomInternational,Inc.DateofInvestment: 3March2011 2012AmountofInvestment: £25.7million(implied

value)£1.35million

AggregatePercentageInterest:

50.0percent. 50.0percent.

Valuationasat30Sep2012: £24.4million ProjectDebt:EquityRatio(basedonconstructioncosts):

62:38

KeyHighlights: ‐ InMay2012,IIPinvested£1.05millionforconstructionofthe8MWRauraprojectinHimachalPradesh.DebtfundingcommitmentwasagreedtowithIREDAandfinancialclosureisexpectedinfirstquarter2013

‐ WeakmonsoonrainfallthatoccurredlaterthannormalhasaffectedpowerproductionfromseveralofIHDC’soperatingprojectsinMaharashtraandHimachalPradesh

‐ H.P.ClusterNo.1–Panwi(4MW)isexpectedtoachievefullCODinfirstquarter2013.

InvestmentDetailsOn3March2011,theCompanyacquireda50percentinterestinIHDCfromGGIC,foran impliedoverallaggregatevalueof£25.7million, inreturnforthe issueofordinarysharesinIIPatIIP’sthenstatedNAVpershare.IHDC is a company that develops, owns and operates small hydropower projects inIndia. IHDC has a proven track record and an established operating infrastructurecapableofsupportingthedevelopmentandoperationoffurtherhydropowerprojectsinIndia,withanumberofofficesacrossthecountry.IHDCcurrentlyoperates five fullyoperationalprojects, totalingapproximately58MWof installed capacity ‐BhandardaraPowerHouse I,BhandardaraPowerHouse II, andDarnainMaharashtra,BirshinghpurinMadhyaPradeshandSechiinHimachalPradesh(COD ‐ February2012). IHDC is also in the final stagesof completionof constructionwork at Panwi, a 4MWhydropower plant inHimachal Pradesh;with commissioning

27

expectedinthefirstquarterof2013.Withcapacityenhancementsbeingimplemented,IHDC’sotherprojectsunderconstruction/developmenttotalanapproximate20MWininstalled capacity. In addition, IHDC has a pipeline of identified projects for futuredevelopment.MaharashtraMaharashtrawitnessedaweakermonsoonrainfallin2012comparedto2011,resultingincomparativelylowerenergygenerationinthehydroprojectsinthestate.BhandardaraI:TheBhandardaraPowerHouse1continuestooperateefficiently.Theprojectgeneratedover34GWhduringJanuarytoOctober2012period.DependingontheirrigationwaterreleasepatternadoptedbytheWaterResourcesDepartmentoftheGovernmentofMaharashtra,productionfromtheprojectintheupcomingwateryearislikelytobelowerthanthathistoricallyobserved.IHDCexpectsthatoncethecontrolofirrigation shifts from thedamatLakeArthurHill to thenewNilwandedam,which iscurrentlyunderconstructionandexpectedtobecompletedinFY2014‐15,theannualproductionfromBhandardaraIwillsignificantlyincrease.BhandardaraII:TheBhandardaraPowerHouseIIproducedover52GWhofelectricityduringJanuarytoOctober2012,ascomparedto53GWhforthefullyearin2011.Theprojectoperatedasexpectedandnonoteworthyissueswerereported.Darna:IHDCcommissionedDarna,a4.9MWhydropowerprojectinJanuary2011.Dueto delayedmonsoon season this year and the slowwater releases from the dam, theenergy generation has been impacted. Darna project generated approx. 11.3 GWh ofelectricityduringJanuarytoOctober2012.BetweenJuneandOctober,2012,theprojectproducedapproximately6.6GWh,whichisnearly2.1GWhlowerthanexpected.IHDCexpects that production from the project will significantly improve once theconstructionofthreeupstreamirrigationdamprojectsiscompleted.Vaitarna: Vaitarna is a 3 MW hydropower project in Maharashtra located close toIHDC’s three existing plants – Bhandardara I, II & Darna. The Group invested £0.3million in early 2012 for the construction of this project. The Government ofMaharashtra’s Water Resource Department iscurrently re‐evaluating acomprehensivewaterresourceplanforthedistrictwithinwhichtheprojectislocated.Consequently,constructionworkhasnotcommencedatthesiteandIHDCisevaluatingspecificactionstotakeinconsultationwiththeGovernmentofMaharashtraintheeventtheimplementationoftheprojectisdelayed.

28

MadhyaPradeshBirsinghpur:TheBirsinghpurprojectlocatedonthecoolingwaterreturncanalintheSanjayGandhiThermalPowerStation inMadhyaPradeshproduced12.9GWhduringthe January toOctober2012period, approximately10per centhigher than the sameperiodforthepreviousyear.Noproblemswerereportedandtheprojectisexpectedtocontinuetooperatesmoothlyintheupcomingyear.HimachalPradeshH.P.ClusterNo.1Sechi:IHDCcommissionedSechi,a4.5MWhydropowerprojectinHimachalPradeshinFebruary2012.IHDChasenteredintoalong‐termPPAwiththeHimachalPradeshStateElectricityBoard("HPSEB")attheHPERCapprovedrateofINR2.50perKWh.ThisratehasbeenfurtherincreasedtoINR2.72perKWhbutHPSEBhasgonetotheHighCourtagainsttheOrderofRegulatorHPERCinothersimilarcasesandcurrentlynotallowingtheincreasetoIHDCpendingappeal.Theresolutionmaytake4‐6monthsatthecurrentlevel of progress at High Court. Himachal Pradesh, like Maharashtra experienced aweakeranddelayedmonsoonin2012.Coolertemperaturesearlyintheyearresultedindelayedsnowmelt.Bothof these factorshavecontributedtoreducedgeneration fromIHDC’sSechiproject.Panwi: IHDC is currently in the final stages of completing the construction work atPanwi,a4MWhydropowerplant inHimachalPradesh.TheprojectwasdelayedbyafewmonthsduetoissueswiththeElectrical&Mechanicalcontractor;however,thingsare back on track and final installations in the powerhouse are underway. Panwi isexpected to commission in the first quarter of 2013. The energy generated from theprojectwillbesoldunderalong‐termPPAtotheHPSEBatratesapprovedbythestateelectricityregulatorycommission.Melan:TheMelanprojectisa4.5MWsmallhydropowerprojectlocatedonatributaryof the Satluj river inHimachal Pradesh and is fed by snowmelt and annualmonsoonflows.Basedontechnicalstudies,IHDChasdeterminedthatthecapacityofthisprojectcanbeenhanced toapproximately9MW.Constructionactivitiescanbe initiatedonlyupon completion of the necessary documentation and required approvals for therevisedprojectarrangement.H.P.ClusterNo.2Raura: Raura is an 8 MW greenfield run‐of‐the‐river hydropower plant in HimachalPradesh.TheGroupinvested£1.05millioninMay2012forconstructionoftheproject.This equity contribution will be used for land acquisition, final engineering design,contractoradvancesandconstruction.ThetotalanticipatedequityinvestmentrequiredforRaura(at8MW)isapproximately£3million,ofwhichtheremainingamountswillbemet out of internal accruals from existing operating plant cash flows. FollowingcommitmentfordebtfundingwiththeIndianRenewableEnergyDevelopmentAgency,constructionactivitieshavecommencedfortheproject.Basedontechnicalparameters

29

observed,IHDCbelievesthatthecapacityoftheprojectcanbeenhancedto12MWandisincorporatingtheflexibilitytoinstallhighercapacityequipmentatthesite.Overall, the actual production during the January to October, 2012 period wasapproximately127GWh,whichisabout5percentbelowtheproductionbudgetedbyIHDC. However, during the June to October, 2012 period the actual production wasnearly16percentbelow thebudgeted figures, indicating the impactof theweakanddelayed monsoon in 2012. Since several of IHDC’s projects produce electricity fromregulated releases, the full impact on revenues for the current fiscal year cannot beaccuratelypredictedatthisstage.ValuationTheIHDCportfolioisvaluedusingtheCompany’sstatedvaluationmethodology,butbyusingacompositeriskpremiumof3.35percentovertherisk‐freerateat8.33percent.The composite risk premium is computed by using aMWbasedweighted average ofrisk premia of individual assets related to their stage of operation. A 2 per cent riskpremiumwasused for theBhandardara I, II andBirsinghpurprojects, the “ramp‐up”risk premium of 4 per cent was used for the Darna and Sechi projects, and a“constructionphase”riskpremiumforPanwiandRaura.Wehaveassumedahigherriskpremium of 7 per cent due to regulatory & governmental challenges on Vaitarna.Additionally,onaccountfortheinherentrisksassociatedwithupsizingaconstructionproject,wecontinuetouseahigherriskpremiumof7percentforMelan.Thevalueforthe IHDC investment as on 30 September 2012was £24.4million (31March 2012 ‐£25.41 million, 30 September 2011 ‐ £24.8 million), valuing Melan and Raura atcapacities of 4.5 MW and 8 MW, respectively. Although currency devaluationcontributedtoa4percentreductioninvaluationbetweenMarch2012andSeptember2012, the NPV has seen an overall reduction in valuation mainly on account ofanticipatedcommissioningdelaysatPanwi,VaitarnaandMelan.

30

IndianEnergyLimited("IEL")SummaryDescription: Anindependentpowerproducerfocusedon

windfarms,with41.3MWproductioncapacityovertwooperatingwindfarms.

Promoter: IIPDateofInvestment: 21September2011 October2011to

August2012AmountofInvestment: £10.57million(implied

value)£0.81million

AggregatePercentageInterest:

100percent. 100percent.

Valuationasat31Mar2012:

£13.87million

ProjectDebt:EquityRatio(basedonconstructioncosts):

60:40

KeyHighlights: ‐ ReductioninaverageinterestcostsatGadag(13.50percent)andTheni(13.00percent)

‐ Betterthanexpectedgenerationnumbers–Gadag(approx.35MU)&Theni(approx.40MU)(Apr‐Sep2012)

‐ HighPLF(closetoP50values)observedforthesixmonthreportingperiod‐Gadag(approx.32.4percent.)andTheni(46.4percent.)

‐ TheniprojectsuccessfullyconvertedtoaGroupCaptiveproject,resultingintimelypaymentsandimprovedcashflows.

‐ TheniprojectsuccessfullyregisteredasaCleandevelopmentmechanismundertheKyotoprotocol

InvestmentDetailsIELisanindependentpowerproducerfocusedonowningandoperatingwindfarmsinIndia.Itcurrentlyoperates41.3MWacrosstwowindfarmsinthestatesofKarnatakaandTamilNadu.

31

ProjectInformationGadagTheGadagProject isa24.8MWwindfarmsituated inKarnataka,nowin its third fullyear of operation. Thepower generated atGadag is sold to theBangaloreElectricitySupplyCompanyundera20‐yearpowerpurchaseagreementatRs.3.40perkWh forthe first 10 years. IELexpects that at the endof the10‐year period, the then currenttariff order from the Karnataka Electricity Regulatory Commission will apply, andanticipatesthetarifftobehighertoreflectinflationduringtheintervening10years.The Gadag Project is registered as a CleanDevelopmentMechanismunder theKyotoProtocolandisearningCERs. CERshavebeenforwardsoldtoStandardBankplcatapriceof€11.50perCERfortheperiodto31December2012.TheCERsfortheperiod1January2013to31December2016hadbeenpre‐soldatapriceof€8.50perCERwhichcontracthasbeenunwoundgenerating further revenue for IEL in the currentperiod.GadagisexpectedtoreceivethethirdtrancheofCER’softheprojectissuedundertheUNFCCCforthegenerationfrom1January2012to30June2012.TheCERsissuanceisexpectedtohappenbymidDecember2012withmonetizationbymid‐January2013.Gadag managed to produce better than expected energy generation in the April toSeptember 2012 period, generating over 35 million kWh. This production was atapproximatelytheP50forecastedvalue.TheprojectoperatedataPLFofover32.4percentduringthereportingperiod,whichisapproximately11percenthighercomparedtothesameperiodin2011.TheniTheTheniProject,a16.5MWwind farm,was fullycommissionedon13August2010andhascompletedtwofullyearsofoperation.ThepowerfromtheTheniProjectwasbeingsoldtotheTamilNaduElectricityBoardunder a 20‐year power purchase agreement at Rs. 3.39 per kWh. The project is alsoapprovedundertheGenerationBasedIncentiveschemeintroducedbytheGovernmentofIndiaandasaresultearnedadditionalrevenueofRs.0.50perkWh.InJuly2012,IELsuccessfullyconvertedtheTheniwindfarmtoagroupcaptivepowerproject.TheprojectisnowprovidingpowertofourindustrialcustomersatagrosstariffofINR5.25perkWhandIELanticipatesreceivingpaymentswithin45daysofinvoicing.Theni managed to produce better than expected energy generation in the April toSeptember,2012reportingperiod,generatingapproximately40millionkWh,i.e.,nearP50 forecasts.TheprojectoperatedataPLFofover46percentduring thereportingperiod, which is approximately 23 per cent higher compared to the same period in2011.IEL has also successfully registered the project as a Clean Development MechanismundertheKyotoProtocolandassuchitwillbeeligible,subjecttoverification,toearnCERs

32

TheexistingprojectdebtisprovidedbyStateBankofIndiawithafloatinginterestratelinkedtothebank’sBaseRate.Gadaghasanapplicableinterestrateof13.50percent(0.25percentbase‐ratereduction);whereasTheninowhasanapplicableinterestrateof 13.00 per cent (0.50 per cent rate reduction + 0.25 per cent base‐rate reduction).Dividend restrictions involve financial covenants linked to the debt service coverageratio(DSCRmustbe>1.30),minimumagreedcashreservesandacashsweepof50percentoftheexcesscashforprepaymentofprincipal.FuturePlansAspartoftheCompany’sexpansionplans,ithasenteredintoaframeworkagreementwithTrisheDevelopersPrivateLimited(“Trishe”)forthedevelopmentandacquisitionof up to 1,000 MW of wind farms in India. The agreement provides for Trishe toundertakethedevelopmentoftheprojects,whichIELwillacquireoncecertaincriticalmilestones have been reached. The wind turbines will be supplied by variousmanufacturers,witheachprojectutilisingthemostappropriateturbinetechnologyfortheprojectsite.Asaresultoftheframeworkagreement,IELhasenteredintoaLetterofIntent with Trishe for the acquisition of a wind farm project with up to 200MW ofcapacitybeingdevelopedbyTrisheinTamilNadu.In addition, IEL has also entered into a framework agreement with KenergyInfrastructurefor100MWwindprojectsinthestateofMaharashtra.ValuationAsat30September,2012,theIELassetswerevaluedinaccordancewiththeCompany’sstatedvaluationmethodologybyapplyinga2.0percentriskpremiumabove theriskfree rate of 8.35 per cent. The risk premium of 2 per cent representing “normaloperations” is utilised for both projects as they have been operational for over twoyears.Thevalue sodetermined for the IELassets is£13.86million. Thisvaluation isreflected in the Company Statement of Financial Position, in which the Company’sinvestments in subsidiaries are shown at fair value. However, as IEL was a whollyownedsubsidiaryatthatdate,theConsolidatedStatementofFinancialPositionincludesaconsolidationofIEL,asrequiredbyIFRS.Suchaconsolidationbydefinitiondoesnotincorporatethevaluationoftheinvestment.

33

ConsolidatedStatementofComprehensiveIncomeforthesixmonthsended30September2012

(Unaudited)6months

ended30September

2012

(Unaudited)6months

ended30September

2011

(Audited)Year

ended31March

2012 Note £’000 £’000 £’000Salesrevenueandotherincome 4,174 ‐ 1,860Costofsales (2,474) ‐ (4,655)Nettradingloss 1,700 ‐ (2,795) Interestincomeonbankbalances 40 36 81Movementinfairvalueofinvestmentsatfairvaluethroughprofitorloss 9 (3,732) (2,210) (4,252)Otherincome 84 ‐ 163Gainonbargainpurchase 14 ‐ 1,905 1,905Foreignexchangegain/(loss) (200) (3) 54Assetmanagementandvaluationservices 7 (1,969) (1,220) (2,815)Otheradministrationfeesandexpenses 6 (1,470) (768) (3,045)Operating(loss) (5,547) (2,260) (10,704)

Financecosts (3,172) ‐ (2,091)(Loss)fortheperiod/yearbeforetaxation (8,719) (2,260) (12,795) Taxation 578 ‐ 919(Loss)fortheperiod/year (8,141) (2,260) (11,876) Othercomprehensiveincome (595) ‐ (2,376)Totalcomprehensive(loss)fortheperiod/year (8,736)

(2,260) (14,252)

Basicanddilutedearningspershare(pence) 8 (3.56)p (1.49)p (6.5)pTheDirectorsconsiderthatallresultsderivefromcontinuingactivities.Thenotesbelowformanintegralpartofthefinancialstatements.

34

CompanyStatementofComprehensiveIncomeforthesixmonthsended30September2012

(Unaudited)6months

ended30September

2012

(Unaudited)6months

ended30September

2011

(Audited)Year

ended31March

2012 Note £’000 £’000 £’000Income Interestincomeonbankbalances 3 36 40Interestonintercompanyloans 10 1,067 551 1,558Movementinfairvalueofinvestmentsatfairvaluethroughprofitorloss 10 (7,505) (4,376) 1,550Total(loss)/income (6,435) (3,789) 3,148 Expenses Financecosts (1,774) ‐ (172)Otheradministrationfeesandexpenses (806) (674) (2,010)Foreignexchange(loss)/gain (198) (2) 58Totalexpenses (2,778) (676) (2,124) (Loss)/profitfortheperiod/yearbeforetax (9,213) (4,465) 1,024Taxation ‐ ‐ ‐ (Loss)/profitfortheperiod/year (9,213) (4,465) 1,024 Othercomprehensiveincome ‐ ‐ ‐Totalcomprehensive(loss)/profitfortheperiod/year (9,213) (4,465) 1,024 Basicanddilutedearningspershare(pence) 8 (3.76)p (2.95)p 0.6pTheDirectorsconsiderthatallresultsderivefromcontinuingactivities.Thenotesbelowformanintegralpartofthefinancialstatements.

35

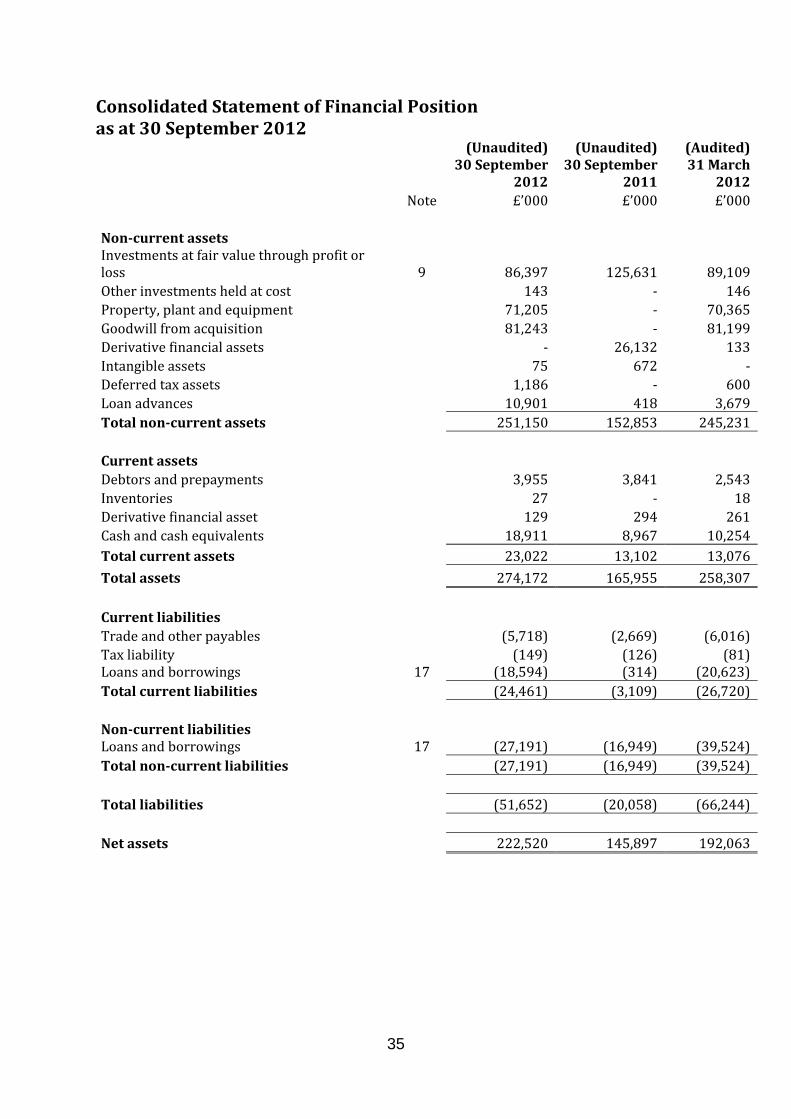

ConsolidatedStatementofFinancialPositionasat30September2012

(Unaudited)30September

2012

(Unaudited)30September

2011

(Audited)31March

2012 Note £’000 £’000 £’000 Non‐currentassets Investmentsatfairvaluethroughprofitorloss 9 86,397 125,631 89,109Otherinvestmentsheldatcost 143 ‐ 146Property,plantandequipment 71,205 ‐ 70,365Goodwillfromacquisition 81,243 ‐ 81,199Derivativefinancialassets ‐ 26,132 133Intangibleassets 75 672 ‐Deferredtaxassets 1,186 ‐ 600Loanadvances 10,901 418 3,679Totalnon‐currentassets 251,150 152,853 245,231 Currentassets Debtorsandprepayments 3,955 3,841 2,543Inventories 27 ‐ 18Derivativefinancialasset 129 294 261Cashandcashequivalents 18,911 8,967 10,254Totalcurrentassets 23,022 13,102 13,076

Totalassets 274,172 165,955 258,307 Currentliabilities Tradeandotherpayables (5,718) (2,669) (6,016)Taxliability (149) (126) (81)Loansandborrowings 17 (18,594) (314) (20,623)Totalcurrentliabilities (24,461) (3,109) (26,720) Non‐currentliabilities Loansandborrowings 17 (27,191) (16,949) (39,524)Totalnon‐currentliabilities (27,191) (16,949) (39,524) Totalliabilities (51,652) (20,058) (66,244) Netassets 222,520 145,897 192,063

36

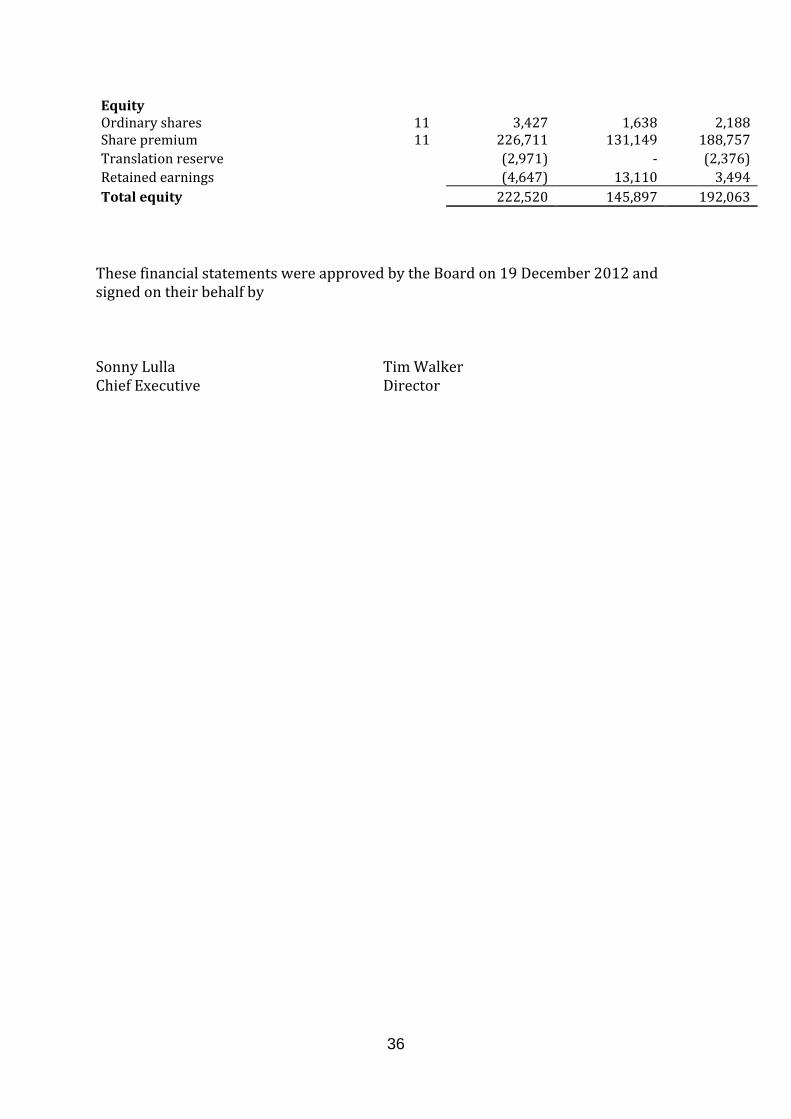

Equity Ordinaryshares 11 3,427 1,638 2,188Sharepremium 11 226,711 131,149 188,757Translationreserve (2,971) ‐ (2,376)Retainedearnings (4,647) 13,110 3,494Totalequity 222,520 145,897 192,063 ThesefinancialstatementswereapprovedbytheBoardon19December2012andsignedontheirbehalfbySonnyLulla TimWalkerChiefExecutive Director

37

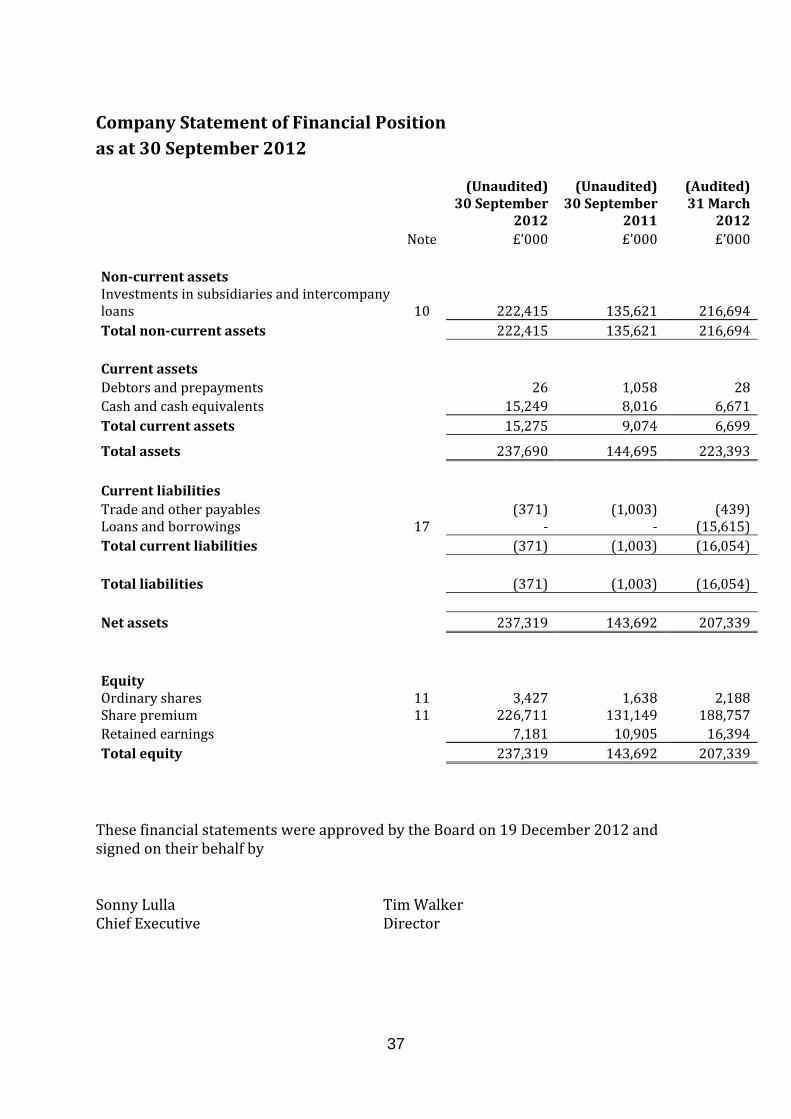

CompanyStatementofFinancialPositionasat30September2012

(Unaudited)30September

2012

(Unaudited)30September

2011

(Audited)31March

2012 Note £’000 £’000 £’000 Non‐currentassets Investmentsinsubsidiariesandintercompanyloans 10 222,415 135,621 216,694Totalnon‐currentassets 222,415 135,621 216,694 Currentassets Debtorsandprepayments 26 1,058 28Cashandcashequivalents 15,249 8,016 6,671Totalcurrentassets 15,275 9,074 6,699

Totalassets 237,690 144,695 223,393 Currentliabilities Tradeandotherpayables (371) (1,003) (439)Loansandborrowings 17 ‐ ‐ (15,615)Totalcurrentliabilities (371) (1,003) (16,054) Totalliabilities (371) (1,003) (16,054) Netassets 237,319 143,692 207,339 Equity Ordinaryshares 11 3,427 1,638 2,188Sharepremium 11 226,711 131,149 188,757Retainedearnings 7,181 10,905 16,394Totalequity 237,319 143,692 207,339 ThesefinancialstatementswereapprovedbytheBoardon19December2012andsignedontheirbehalfbySonnyLulla TimWalkerChiefExecutive Director

38

ConsolidatedStatementofChangesinEquityforthesixmonthsended30September2012

Sharecapital

Sharepremium

Translationreserve

Retainedprofit Total

Note £’000 £’000 £’000 £’000 £’000 Balanceat1April2011 1,506 121,133 ‐ 15,370 138,009

Totalcomprehensiveincomefortheyear

Lossfortheyear ‐ ‐ ‐ (11,876) (11,876)Totalothercomprehensiveincome ‐ ‐ (2,376) ‐ (2,376)Totalcomprehensiveincomefortheyear ‐ ‐ (2,376) (11,876) (14,252)Contributionsbyanddistributionstoowners

Issueofordinaryshares 682 68,196 ‐ ‐ 68,878

Shareissuecosts ‐ (572) ‐ ‐ (572)TotalcontributionsbyanddistributionstoownersoftheCompany 682 67,624 ‐ ‐ 68,306

Balanceat31March2012 2,188 188,757 (2,376) 3,494 192,063

Balanceat1April2012 2,188 188,757 (2,376) 3,494 192,063

Totalcomprehensiveincomefortheyear

Lossfortheyear ‐ ‐ ‐ (8,141) (8,141)Totalothercomprehensiveincome ‐ ‐ (595) ‐ (595)Totalcomprehensiveincomefortheyear ‐ ‐ (595) (8,141) (8,736)Contributionsbyanddistributionstoowners