Infrastructure Financing District Update and Preview of AB2 CRIAcalsaca.org/sites/default/files/IFDs...

27

Infrastructure Financing District Update and Preview of AB2 CRIA October 27, 2015 California State Association of County Auditors – Property Tax Managers’ Sub-Committee

Transcript of Infrastructure Financing District Update and Preview of AB2 CRIAcalsaca.org/sites/default/files/IFDs...

Infrastructure Financing District Update and

Preview of AB2 CRIA

October 27, 2015

California State Association of County Auditors – Property Tax Managers’ Sub-Committee

www.company.com Slide 2

Agenda 1. History - Infrastructure Financing Districts (IFDs)

2. Overview - Carlsbad Ranch IFD

3. Infrastructure Financing Districts in the Border

Development Zone

4. Infrastructure and Revitalization Financing Districts

5. Enhanced Infrastructure Financing Districts

6. Community Revitalization and Investment Authority

(CRIA) AB 2

7. County of San Diego Anticipated Issues

www.company.com Slide 3

1. History - Infrastructure Financing Districts

o Legal Authority

- Created in 1990 – apparently in response to criticism of

perceived abuses of the Community Redevelopment Law

- The legislature enacted the Infrastructure Financing District

Law (Government Code Section 53395 et seq.)

- Affected Taxing Entity (ATE) definition excludes county office

of education, school districts, or community college districts

- Initially, IFD law prohibited an infrastructure financing district

from including any portion of a redevelopment project area.

www.company.com Slide 4

Infrastructure Financing Districts

o Legal Authority continued

- On February 18, 2014 Governor Brown approved AB 471

(Atkins).

• The district was permitted to finance a project or portion of a

project that was located in, or overlaps with, a redevelopment

project area or former redevelopment project area.

• Further, it authorized the legislative body of the city or county

forming the district the ability to choose to dedicate any portion

of its “net available revenue” to the district.

www.company.com Slide 5

Infrastructure Financing Districts

o Use of IFD Tax Increment

- Limited to capital facilities that are:

• Required to serve the development proposed in the IFD area.

• Of community-wide significance.

• Provide significant benefits to an area larger than the district.

- Capital facilities do not have to be located within the district.

www.company.com Slide 6

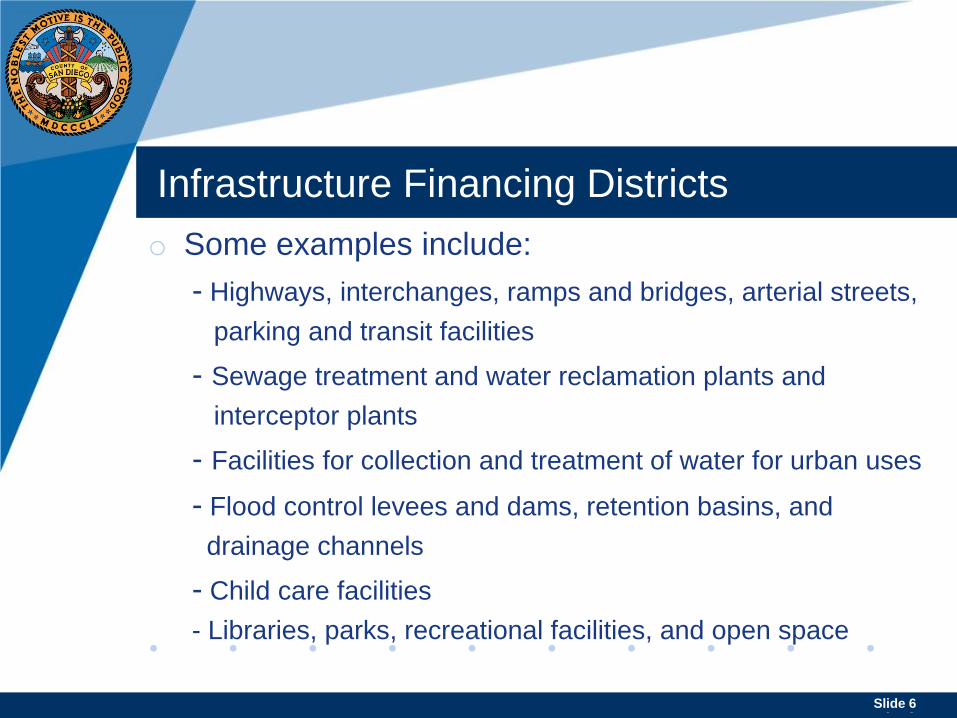

Infrastructure Financing Districts

o Some examples include:

- Highways, interchanges, ramps and bridges, arterial streets,

parking and transit facilities

- Sewage treatment and water reclamation plants and

interceptor plants

- Facilities for collection and treatment of water for urban uses

- Flood control levees and dams, retention basins, and

drainage channels

- Child care facilities

- Libraries, parks, recreational facilities, and open space

www.company.com Slide 7

•Governing body adopts ROI, and ROI is mailed to ATEs and landowners

Adopt Resolution of Intention (ROI)

•Submit plan and required CEQA reports to ATEs and landowners

Prepare Financing Plan

•After 60 days of financing plan submission and required public hearing notifications (4 weeks in general circulation newspaper)

Conduct Public Hearing

•Adopt ROF proposing to adopt financing plan and creating the IFD

•ATEs contribute revenue only if they elect by resolution to approve plan

Adopt Resolution of Formation (ROF)

•Submit to voters in next general election or a special election

Submit Proposal to Vote

• If 2/3 of voters approve, the governing body may adopt the plan and create the IFD by ordinance.

Create the IFD

www.company.com Slide 8

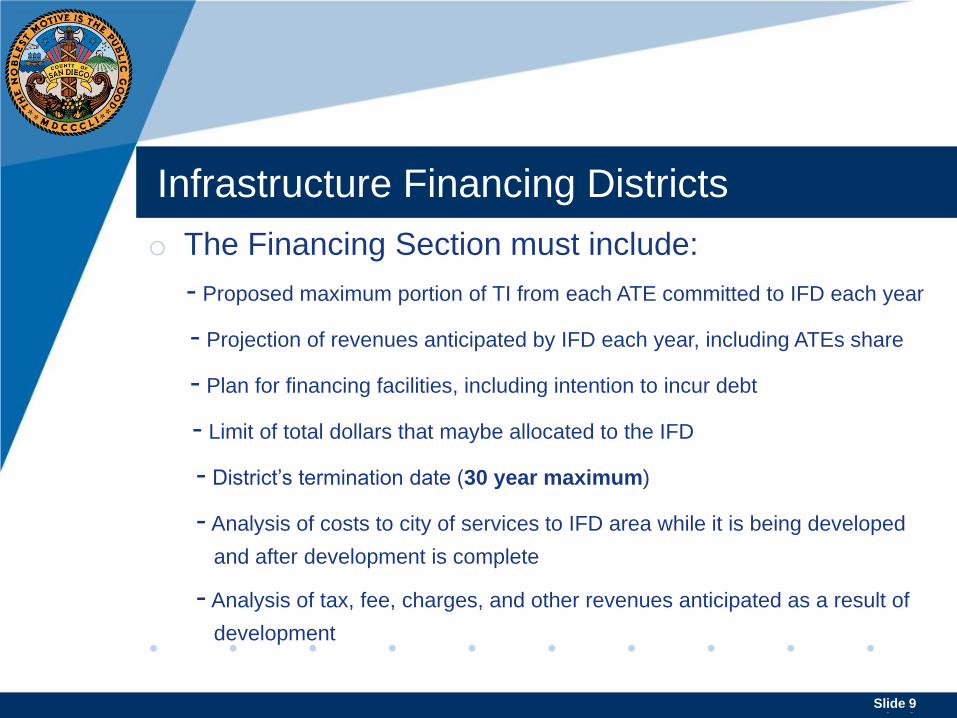

Infrastructure Financing Districts

o The Infrastructure Financing Plan must include:

- Map & legal description of proposed IFD

- Description of public facilities required to serve the IFD

- Facilities location, timing, and cost

- Finding that facilities have community-wide significance and benefit area

larger than IFD

- Financing Section

www.company.com Slide 9

Infrastructure Financing Districts

o The Financing Section must include:

- Proposed maximum portion of TI from each ATE committed to IFD each year

- Projection of revenues anticipated by IFD each year, including ATEs share

- Plan for financing facilities, including intention to incur debt

- Limit of total dollars that maybe allocated to the IFD

- District’s termination date (30 year maximum)

- Analysis of costs to city of services to IFD area while it is being developed

and after development is complete

- Analysis of tax, fee, charges, and other revenues anticipated as a result of

development

-

www.company.com Slide 10

Infrastructure Financing Districts

o The Financing Section continued:

- Projected fiscal impact of IFD and associated development upon each ATE

- Plan for replacement of low-mod units destroyed or removed and relocation

of tenants.

-

www.company.com Slide 11

2. Carlsbad Ranch IFD

o City of Carlsbad formed the IFD in July 2000

- The Infrastructure Financing Plan proposed formation without

allocation of the tax increment revenues of the County of San

Diego or any other affected taxing agency except the City.

- The aggregate reimbursement amount was $1,760,000.

- The plan is still active.

www.company.com Slide 12

3. Infrastructure Financing Districts in the

Border Development Zone o On October 7, 1999 the Governor approved Senate

Bill 207 (Peace).

- The bill established a border development zone; a strip of

land three miles wide with the international border of Mexico

on the south, the mean high tide of the Pacific Ocean on the

west, and the border with the State of Arizona on the East.

- A district may not include any portion of a redevelopment

project area.

- Similar terms to IFD.

www.company.com Slide 13

4. Infrastructure and Revitalization

Financing Districts o On September 29, 2014 Governor Brown approved

AB 229 (Perez).

- Authorizes creation of infrastructure and revitalization

financing district

- Establishes the life of a district at 40 years (and debt with 30

year maturity)

- Authorizes financing of projects in RDA project areas, former

RDAs, and former military bases

- May allow a city to dedicate a portion of its RPTTF funds to

the district

www.company.com Slide 14

Infrastructure and Revitalization

Financing Districts o AB229 continued:

- Expands type of projects eligible for funding, including

purchase of land and property for development purposes

www.company.com Slide 15

5. Enhanced Infrastructure Financing Districts

o On September 29, 2014 Governor Brown approved

Senate Bill 628 (Beall)

- Streamlines process and funds broader array of

projects

- Affected Taxing Entity (ATE) definition excludes county office

of education, school districts, or community college districts

- Before creating an EIFD, the City must have received a

finding of completion

- Partner agencies may allocate tax increment to infrastructure

financing plan

www.company.com Slide 16

IFD EIFD

Formation • Resolution of Intention

• Prepare Financing Plan

• Holds Public Hearing

• Each affected taxing entities governing

body must approve a resolution

accepting the plan

• Resolution of Formation

• Election requiring 2/3 voter approval

• Form a Public Financing Authority (see

below Governing Body for more details)

• Requirements re Successor Agency and

former RDA assets

• Resolution of Intention

• Prepare Financing Plan

• Resolution of Formation (no election

required)

Revenues • Tax increment over and above base AV

(determined when IFD is formed)

• Tax increment over and above base AV

(determined when IFD is formed)

• Other assessments or fees

Bond Issuance

Approval

• Resolution of Intention to Issue Bonds

• Election requiring 2/3 voter approval

• Resolution of Issuance of Bonds

• Resolution of Intention to Issue Bonds

• Election requiring 55% voter approval

• Resolution of Issuance of Bonds

Term 30 years 45 years

Governing Body Existing governmental agency (city or

county)

Public Financing Authority comprising

both public members and members from the

legislative body of participating taxing

entity(ies) must be created

Projects Limited infrastructure projects Broader list of eligible projects

Acquisition, construction, or repair of

industrial structures for private use;

brownfield restoration; transit priority

projects.

www.company.com Slide 17

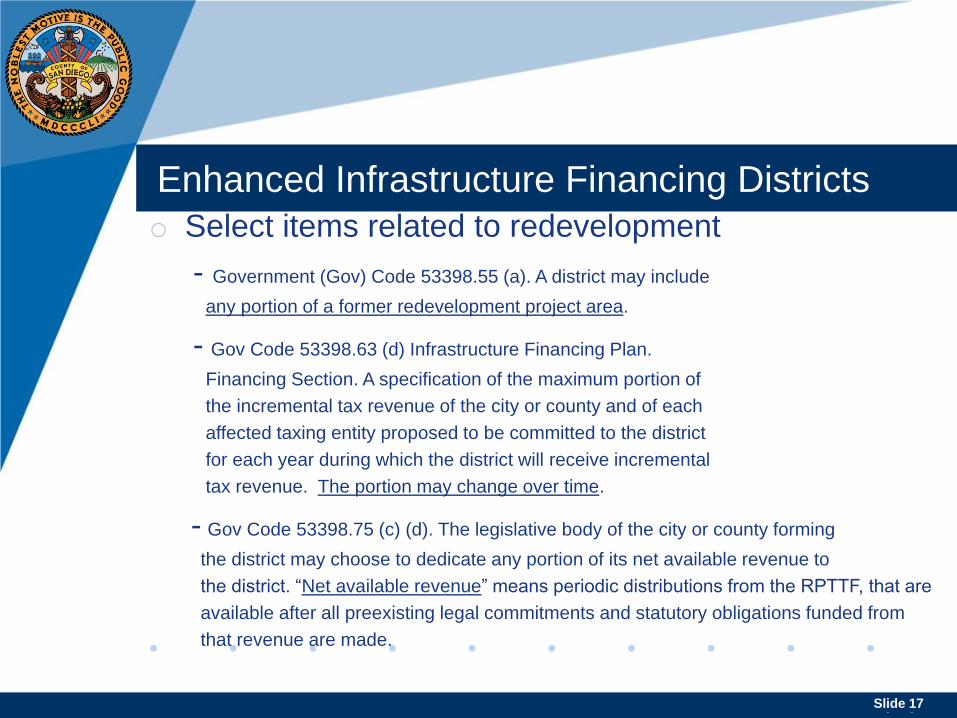

Enhanced Infrastructure Financing Districts

o Select items related to redevelopment

- Government (Gov) Code 53398.55 (a). A district may include

any portion of a former redevelopment project area.

- Gov Code 53398.63 (d) Infrastructure Financing Plan.

Financing Section. A specification of the maximum portion of

the incremental tax revenue of the city or county and of each

affected taxing entity proposed to be committed to the district

for each year during which the district will receive incremental

tax revenue. The portion may change over time.

- Gov Code 53398.75 (c) (d). The legislative body of the city or county forming

the district may choose to dedicate any portion of its net available revenue to

the district. “Net available revenue” means periodic distributions from the RPTTF, that are

available after all preexisting legal commitments and statutory obligations funded from

that revenue are made.

www.company.com Slide 18

• Describe boundaries

• State type of facilities and development to be funded by EIFD

• State that incremental property tax revenue may be used to finance

these facilities

• Fix time and place for a public hearing

• Sent to all land owners and affected taxing entities (taxing entities)

within EIFD

Resolution

of Intention

to establish

the district

(ROI)

1

• Must be created prior to formation of EIFD

• Membership consists of members of participating taxing entities and

the public

• Governing body of each participating taxing entity that will commit a

portion of tax revenue approves the proposed Plan

Creation of

Public

Finance

Authority

(PFA)

2

• Specify maximum portion tax increment from each participating

taxing entity

• Analysis of costs and projected revenues from tax increment and

resulting development

• Detailed description of any intention to incur debt

• Sent to all land owners and taxing entities within EIFD, any taxing

entity may propose revisions

Preparation of

Proposed

Infrastructure

Financing

Plan (Plan)

3

• Approve the Plan

• Adopt a resolution forming the EIFD

Public

Hearing /

Resolution

of Formation

4

Enhanced Infrastructure Financing Districts

www.company.com Slide 19

Enhanced Infrastructure Financing Districts

o On September 22, 2015, Governor Brown approved

AB 313 (Atkins).

- The bill revised the duties of the public financing authority after the resolution

of intention to establish the proposed district has been adopted.

- The public financing authority, instead of the legislative body, will perform the

specified duties related to the preparation, proposal and adoption of the

infrastructure financing plan and the adoption of the formation of the district.

www.company.com Slide 20

6. Community Revitalization and Investment

Authority (CRIA) AB 2 o On September 22, 2015 Governor Brown approved

Assembly Bill 2 (Alejo)

- Authorized certain local agencies to form a community revitalization

authority within a community revitalization and investment area.

- Authority may carry out a community revitalization plan within a community

revitalization and investment area.

- Revitalization project means a physical improvement to real property funded

by the authority.

- A school entity, as defined in subdivision (f) of Section 95 of the Revenue

and Taxation Code may not participate in an authority created pursuant to

this part.

www.company.com Slide 21

Community Revitalization and Investment

Authority (CRIA) AB 2 o AB 2 Requirements Continued

- Not less than 80% of the land calculated by census tracts, or census block

groups, as defined by the US Census Bureau, within the area shall be

characterized by both the following conditions:

• An annual median household income that is less than 80 percent

of the statewide annual median income

• Three of the following 4 conditions:

A. Non-seasonal unemployment that is at least 3 percent higher than statewide

median unemployment (published by EDD in January of the year the community

revitalization plan is prepared.)

B. Crime rates that are 5 percent higher than the statewide median crime rate, as

defined by the Criminal Justice Statistics Center within the Dept. of Justice.

C. Deteriorated or inadequate infrastructure

D. Deteriorated commercial or residential structures (May include a former military base)

www.company.com Slide 22

Community Revitalization and Investment

Authority (CRIA) AB 2 o AB 2 Requirements Continued

- Gov. Code. 62003. An authority shall adopt a community revitalization and

investment plan that may include a provision for the receipt of tax increment

funds generated within the area according to Section 62005.

- Gov. Code. 62005 (f). If an area includes, in whole or in part, land formerly or

currently designated as a part of a redevelopment project area, as defined in

Section 33320.1 of the Health and Safety Code, any plan adopted pursuant

to this part that include a provision for the receipt of tax increment revenues

according to subdivision (a) shall include a provision that tax increment

amounts payable to an authority are subject and subordinate to any

preexisting enforceable obligation as that term is defined by Section 34171

of HSC.

www.company.com Slide 23

Community Revitalization and Investment

Authority (CRIA) AB 2 o CRIA may do all of the following:

- Provide funding to rehabilitate, repair, upgrade, or construct infrastructure

- Provide for low- and moderate income housing

- Remedy or remove a release of hazardous substances pursuant to the

Polanco Redevelopment Act.

- Provide for seismic retrofits of existing buildings

- Acquire and transfer real property in accordance with Part 3 (commencing

with Section 62200).

- Issue bond in conformity with Article 4.5 (commencing with Section 53506).

www.company.com Slide 24

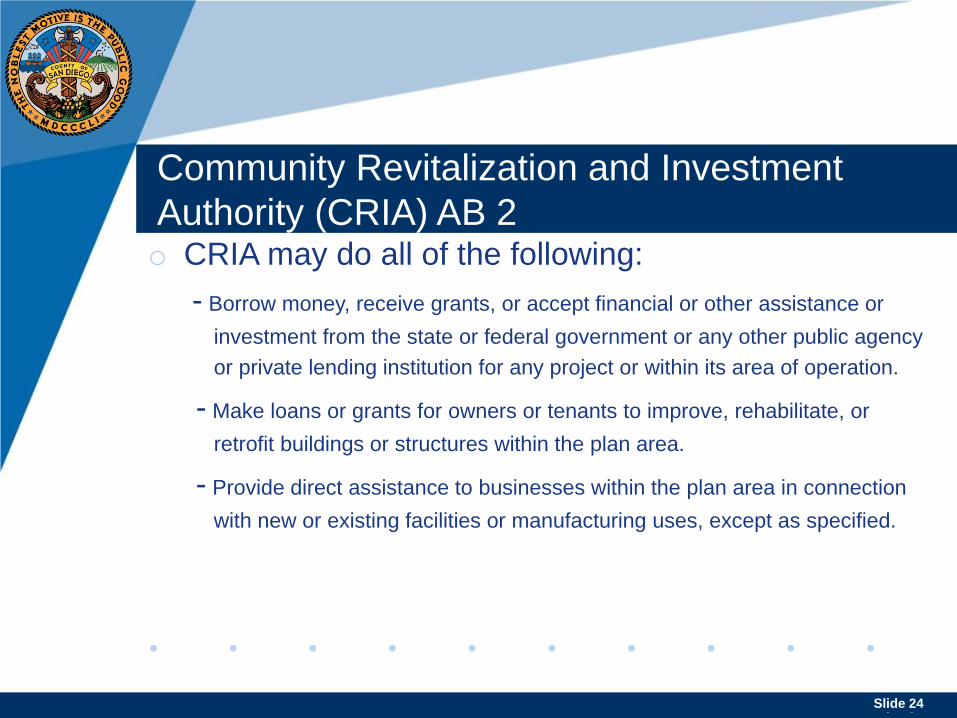

Community Revitalization and Investment

Authority (CRIA) AB 2 o CRIA may do all of the following:

- Borrow money, receive grants, or accept financial or other assistance or

investment from the state or federal government or any other public agency

or private lending institution for any project or within its area of operation.

- Make loans or grants for owners or tenants to improve, rehabilitate, or

retrofit buildings or structures within the plan area.

- Provide direct assistance to businesses within the plan area in connection

with new or existing facilities or manufacturing uses, except as specified.

www.company.com Slide 25

7. County of San Diego Anticipated Issues

- The district was permitted to finance a project or portion of a project that

was located in, or overlaps with, a redevelopment project area or former

redevelopment project area.

• How many counties have the capability of tracking IFD increment on top

of redevelopment increment?

• This would appear to necessitate tracking ROPS at the project and very

likely at the sub-project level. (San Diego County tracks ROPS at the

successor agency level.)

- “Net available revenue”

Seek clarification on whether this is Opening Charges or Collected

Revenue (1% AB 8)

What other types of revenues is this entity entitled to receive? Refunds,

Unitary, Supplemental, Roll Correction Adjustments, Escapes?

www.company.com Slide 26

County of San Diego Anticipated Issues

- Administrative cost reimbursement?

www.company.com Slide 27

Questions?

Presented by:

Jon Baker

County of San Diego

858.694.2290