INFORMATION ASYMMETRY AND RESIDENTIAL MORTGAGE …

183

The Pennsylvania State University The Graduate School The Mary Jean and Frank P. Smeal College of Business INFORMATION ASYMMETRY AND RESIDENTIAL MORTGAGE CHOICES A Dissertation in Business Administration by Xun Bian Copyright 2011 Xun Bian Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy August 2011

Transcript of INFORMATION ASYMMETRY AND RESIDENTIAL MORTGAGE …

The Pennsylvania State University

The Graduate School

The Mary Jean and Frank P. Smeal College of Business

INFORMATION ASYMMETRY AND RESIDENTIAL

MORTGAGE CHOICES

A Dissertation in

Business Administration

by

Xun Bian

Copyright 2011 Xun Bian

Submitted in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

August 2011

The dissertation of Xun Bian was reviewed and approved* by the following:

Brent W. Ambrose

Smeal Professor of Real Estate

Dissertation Advisor

Chair of Committee

Austin J. Jaffe

Chair, Department of Insurance and Real Estate

Philip H. Sieg Professor of Business Administration

Jiro Yoshida

Assistant Professor of Business

N. Edward Coulson

Professor of Economics

*Signatures are on file in the Graduate School

iii

ABSTRACT

When financing real estate properties through a mortgage, borrowers often face a

variety of loan products. During the recent housing bubble the variety of mortgage

products and features proliferated. The recent mortgage foreclosure crisis leads many

commentators to point to the growth in the use of these alternative mortgage features as

being predatory. A number of academic studies provide supporting evidence to this view.

In contrast, economists have long noted that mortgage menus provide an effective

mechanism for reducing the information asymmetry that exists between borrowers and

lenders. This dissertation focuses on the screening mechanisms of mortgage features. One

of the goals is to analyze the welfare implications of allowing for a greater variety of loan

products in the residential mortgage market.

This dissertation also aims to contribute to the existing literature on mortgage

choices by incorporate multiple risk dimensions in a unified framework. Most previous

studies limit their exploration to a single risk dimension, default or prepayment risk.

While examining one risk dimension at a time substantially simplifies the analysis, it also

omits the fact that multiple sources of information asymmetry may be at work in shaping

the mortgage market equilibrium. It is well-known that a mortgage contract contains two

types of risk: default risk and prepayment risk. A single device may possess dual

screening roles.

Chapter 2 of this dissertation illustrates the screening role of prepayment penalty

on default and prepayment risks. It examines the interaction between the two screening

functions of prepayment penalty, and shows that the borrower mobility and default risks

iv

jointly determine the mortgage market equilibrium. In particular, the willingness of a

borrower to accept a prepayment penalty may stem from her low mobility risk and/or

high default risk. The choice of a higher prepayment penalty sends the lender conflicting

signals about the borrower’s mobility versus default risk type; thus rendering the

screening role of prepayment penalty ambiguous. Chapter 3 studies the dual screening

role of mortgage discount points. It shows that there exists a separating equilibrium such

that borrowers with higher (lower) transaction costs pay more (less) discount points to

obtain a lower (higher) interest rate. This theoretical prediction suggests a new screening

function of mortgage points, and it complements the conventional mobility-based theory

that suggests that the choice of discount points is a signal of the borrower’s expected

mobility. Chapter 3 also empirically examines the screening role of discount points from

the lender’s perspective. The empirical results suggest that lenders tend to securitize

loans originated by borrowers with higher transactions cost. Chapter 4 offers a theoretical

model to show that when future income uncertainty is private information, there exists a

separating equilibrium such that borrowers with higher default risk are more likely to

choose mortgage contracts with prepayment penalties. I further test the prediction of my

model using a sample of securitized mortgages that contain loans with and without a

prepayment penalty. I find that the positive correlation between prepayment penalties and

default rates is attributable to information asymmetry.

v

TABLE OF CONTENTS

List of Figures ............................................................................................................. viii

List of Tables ............................................................................................................. ix

Acknowledgements .................................................................................................... x

Chapter 1 Overview of Mortgage Choices under Information Asymmetry ....... 1

Chapter 2 The Dual Screening Role of Prepayment Penalty ................................ 8

Background on Prepayment Penalty ............................................................................ 10

The Model……………………………………………………………………………...13

Equilibrium with Full Information .............................................................................. 21

Equilibrium with Asymmetric Information ................................................................ 24

Heterogeneous Mobility ........................................................................................... 24

Heterogeneous Default Risk ..................................................................................... 27

Heterogeneous Mobility and Default Risk ............................................................... 29

Pooling Equilibrium ......................................................................................... 30

Separating Equilibrium .................................................................................... 38

Discussion and Implications .......................................................................................... 40

Chapter 3 The Screening Role of Mortgage Discount Points on Transactions

Costs .......................................................................................................................... 50

Related Literature .......................................................................................................... 54

The Model ....................................................................................................................... 58

Hypothesis Development ............................................................................................... 67

Empirical Analysis ......................................................................................................... 72

Data ......................................................................................................................... 72

vi

Excess Yield Spread and Prepayment ..................................................................... 73

Mortgage Points, Excess Yield Spread, and Securitization Decisions .................... 83

Summary of Findings ..................................................................................................... 84

Chapter 4 Bad Borrowers or Bad Loans: The Effect of Information

Asymmetry on the Choice of Prepayment Penalty ................................................ 91

Literature Review .......................................................................................................... 95

Prepayment Penalty and Subprime Lending ........................................................... 95

Mortgage Choice under Information Asymmetry ................................................... 98

Empirical Tests of Adverse Selection ...................................................................... 99

The Model ....................................................................................................................... 101

The Setup ................................................................................................................. 101

Zero-Profit Contracts ............................................................................................... 102

Borrower’s Problem ................................................................................................. 105

Equilibrium with Full Information .......................................................................... 108

Equilibrium with Asymmetric Informtion .............................................................. 109

Does Prohibiting Prepayment Penalties Benefit or Hurt Borrowers? ...................... 112

Empirical Analysis .................................................................................................... 114

Hypothesis ................................................................................................................ 114

Data ......................................................................................................................... 115

Methodology ............................................................................................................ 117

Competing-Risks Hazard Model ....................................................................... 117

Bivariate Probit Model ..................................................................................... 119

Sampling ........................................................................................................... 120

Variables Related to Default and Prepayment Options ................................... 121

vii

Variables Related to Borrower and Loan Characteristics ............................... 122

Results ............................................................................................................................. 125

Results of the Competing-Risks Hazard Model ....................................................... 125

Results of the Bivariate-Probit Model ..................................................................... 127

Summary of Findings ..................................................................................................... 129

Chapter 5 Concluding Remarks .............................................................................. 145

Bibliography ............................................................................................................... 149

Appendix A Proofs of Propositions in Chapter 2 ................................................... 156

Appendix B Proofs of Proposition 1 in Chapter 4 ................................................. 171

viii

LIST OF FIGURES

Figure 2.1: Heterogeneous Mobility. ...................................................................................... 44

Figure 2.2: Heterogeneous Default Risk. ................................................................................ 45

Figure 2.3: Heterogeneous Mobility and Default Risk (Pooling Equilibria: Scenario 1) ....... 46

Figure 2.4: Heterogeneous Mobility and Default Risk (Pooling Equilibria: Scenario 2) ....... 47

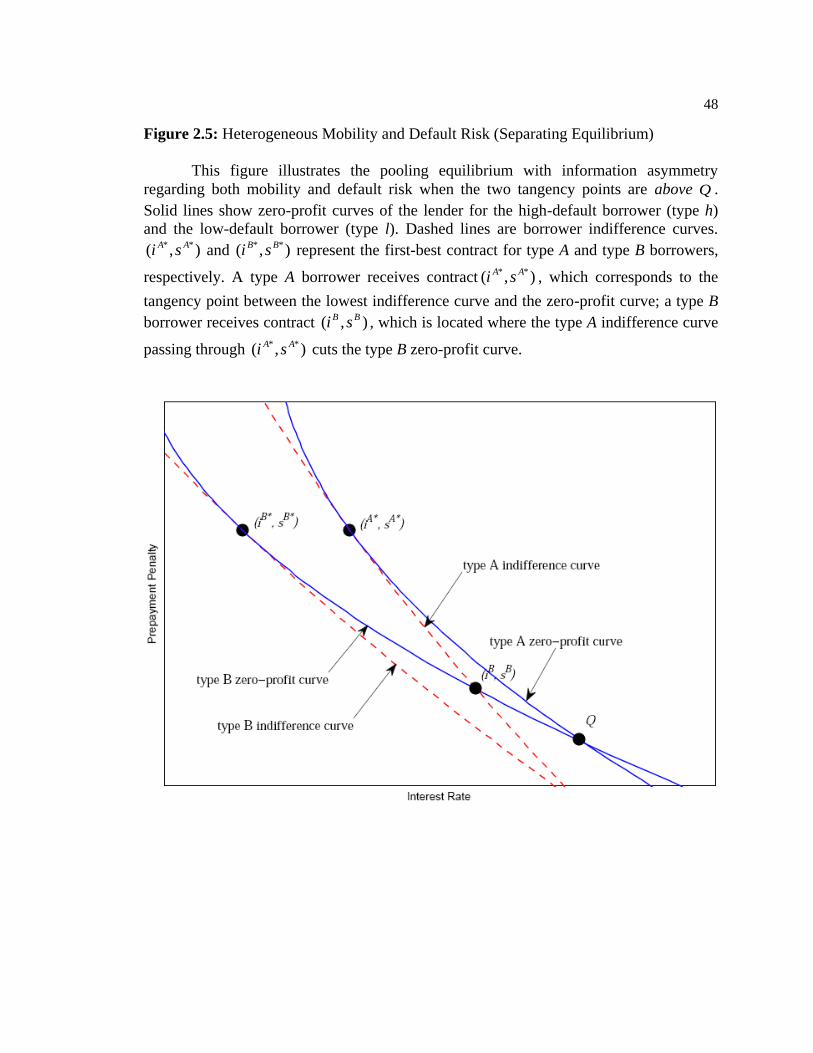

Figure 2.5: Heterogeneous Mobility and Default Risk (Separating Equilibria: Scenario 1) .. 48

Figure 2.6: Heterogeneous Mobility and Default Risk (Separating Equilibria: Scenario 2) .. 49

Figure 3.1: Mortgage-Points Choice with Asymmetric Information ...................................... 86

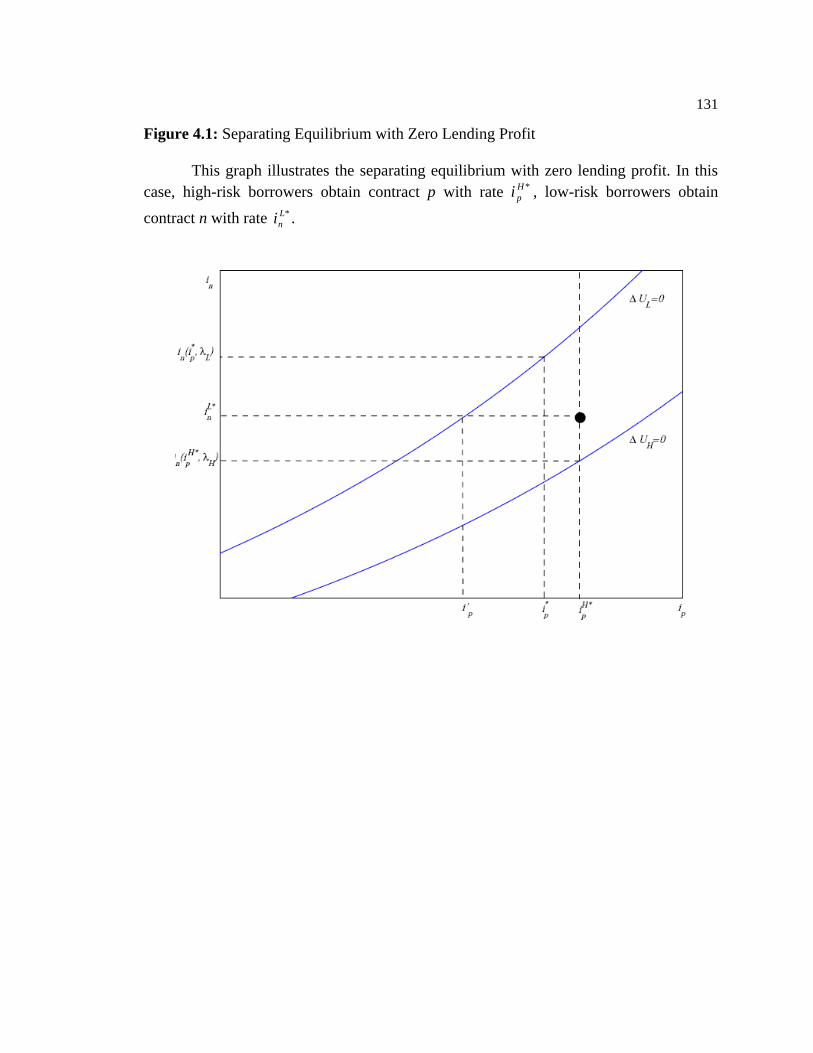

Figure 4.1: Separating Equilibrium with Zero Lending Profit ................................................ 131

Figure 4.2: Subsample Construction ....................................................................................... 132

ix

LIST OF TABLES

Table 2.1: Aggregate Effects of Mobility and Default............................................................ 50

Table 3.1: Descriptive Statistics (Chapter 3). ......................................................................... 87

Table 3.2: Estimation of Excess Yield Spread. ....................................................................... 88

Table 3.3: Comprting-Risks Hazard Model of Mortgage Termination Outcomes. ................ 89

Table 3.4: Mortgage Points, Excess Yield Spread, and Securitization Decisions. ................. 91

Table 4.1: Descriptive Statistics (Chapter 4). ......................................................................... 133

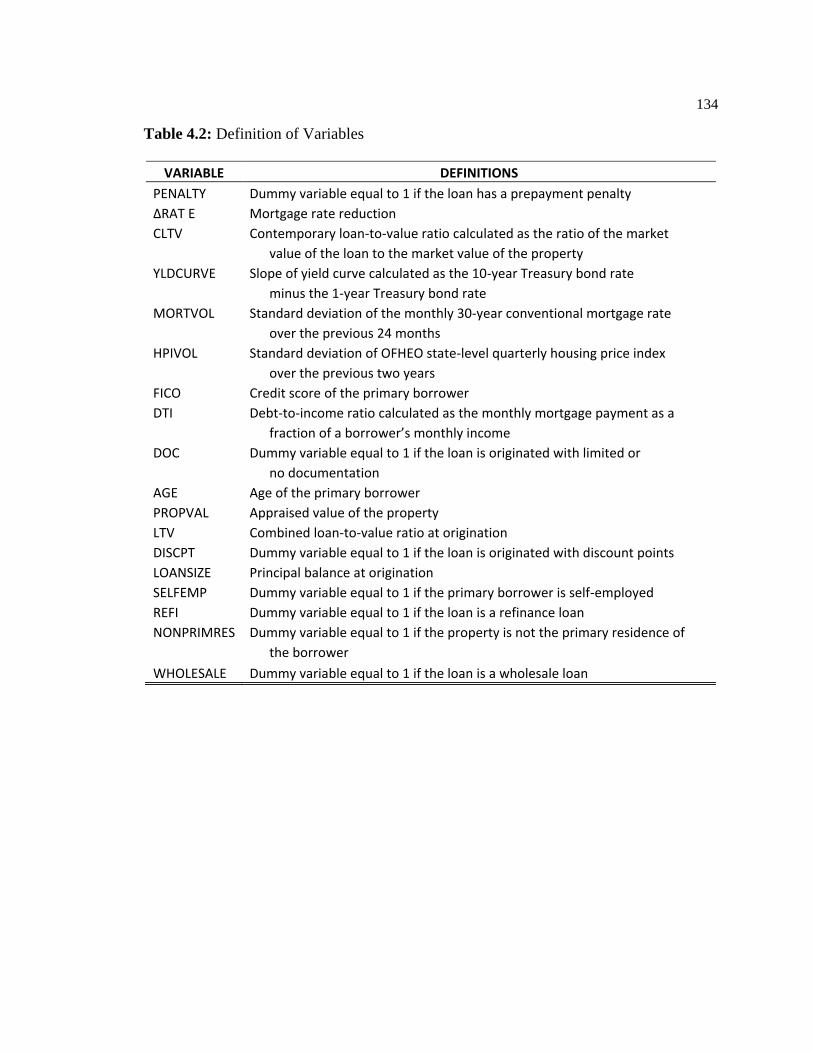

Table 4.2: Definition of Variables. ......................................................................................... 134

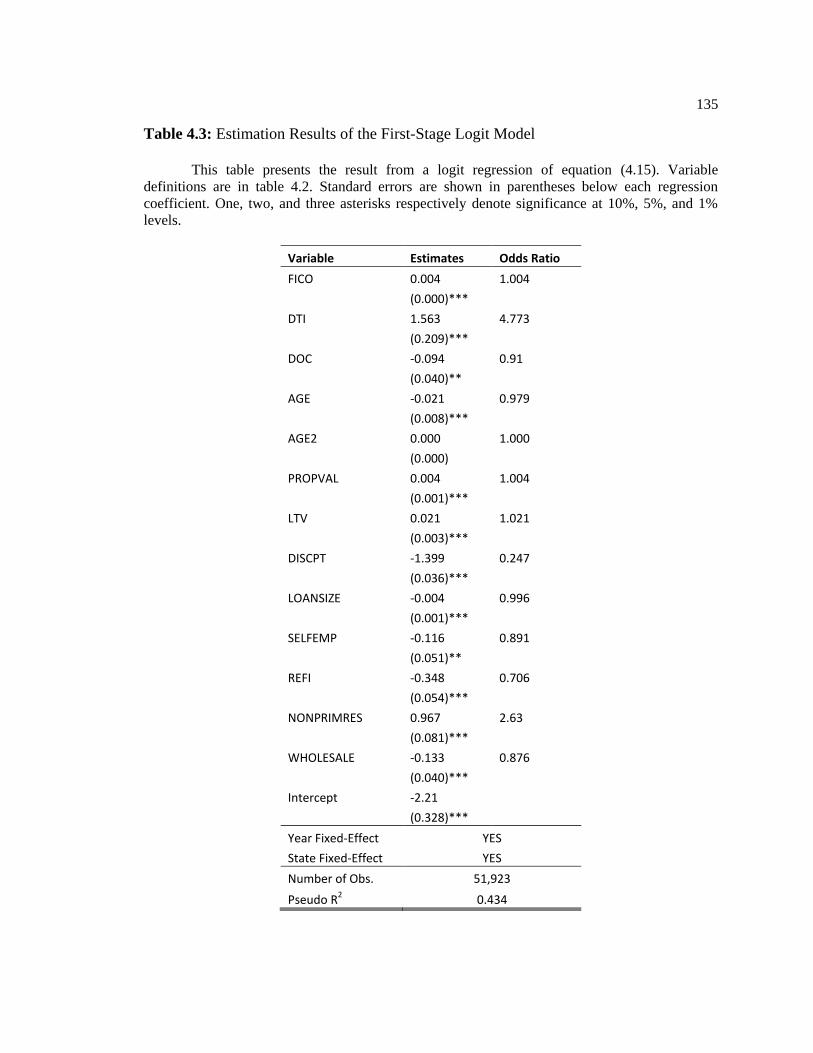

Table 4.3: Estimation Results of the First-Stage Logit Model. ............................................... 135

Table 4.4: Results of Competing-Risk Hazard Model Using the Full Sample. ...................... 136

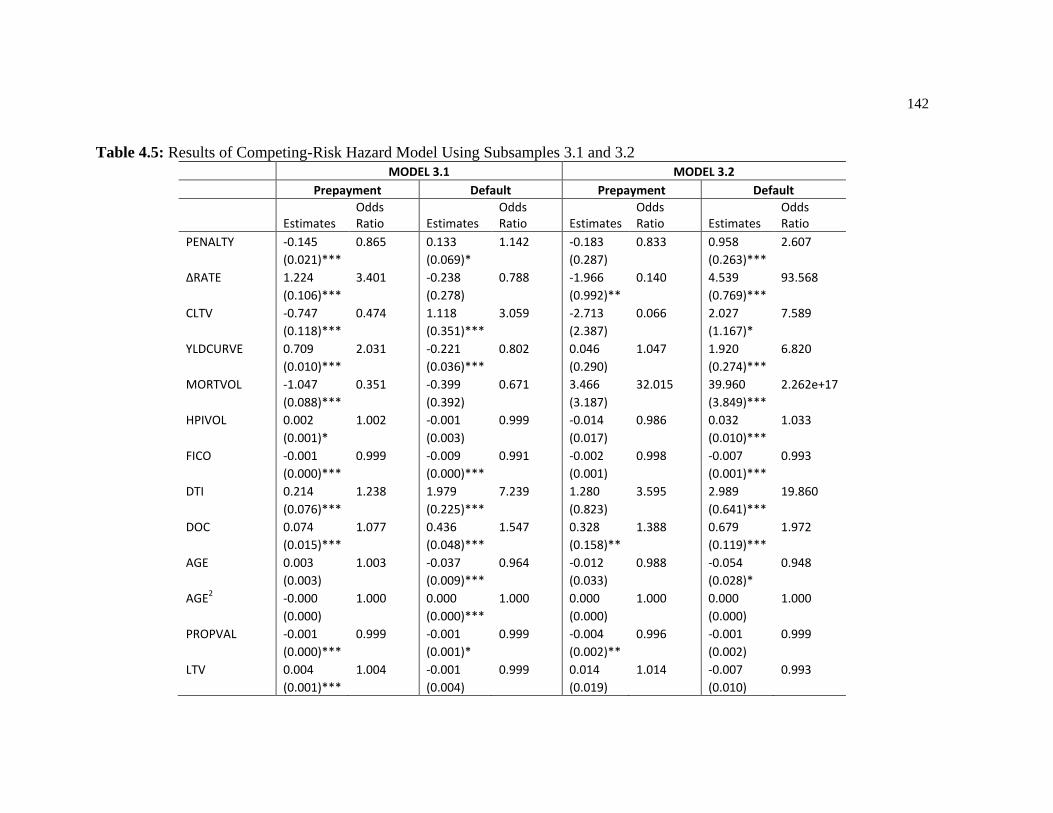

Table 4.5: Results of Competing-Risk Hazard Model Using Subsamples 1.1 and 1.2. .......... 138

Table 4.6: Results of Competing-Risk Hazard Model Using Subsamples 2.1 and 2.2. .......... 140

Table 4.7: Results of Competing-Risk Hazard Model Using Subsamples 3.1 and 3.2. .......... 142

Table 4.8: Results of Bivariate-Probit Models. ....................................................................... 144

x

ACKNOWLEDGEMENTS

First, I would like to express my most sincere gratitude to my adviser, Professor

Brent Ambrose, who has been an exceptional mentor. He has inspired me from the

beginning with his enthusiasm for real estate research. Throughout my study in the past

several years, he gave me invaluable guidance, advice and encouragement. Without his

support, this dissertation would have been impossible.

Second, I want to thank my dissertation committee members: Professor Austin

Jaffe, Professor Ed Coulson and Professor Jiro Yoshida. Their careful reading,

constructive criticism and valuable comments greatly improved this dissertation. I also

want to thank Professor Abdullah Yavas, from whom I built my theoretical modeling

skills. My thanks also go to Professor Michael LaCour-Little, who generously provided

access to the dataset used in Chapter 3 of this dissertation. In addition, his helpful

comments significantly improved my work.

My special thanks are dedicated to my parents, Bian Bian and Heqing Huang.

Their love supported me in every stage of my life. Without them, none of my

achievements would have been possible. I also want to thank my wife Jun Zhang. Her

unconditional support and love makes me a happier person.

1

Chapter 1

Overview of Mortgage Choices under Information Asymmetry

When financing real estate properties through a mortgage, borrowers often face a

variety of loan products. Available mortgage choices include interest rate adjustment

methods (e.g. fixed rate or variable rate), time to maturity, discount points, and

prepayment penalties, among many others. During the recent housing bubble the variety

of mortgage products and features proliferated. For example, instead of offering a simple

choice of fixed-rate (FRMs) or adjustable-rate mortgages (ARMs), lenders began offering

alternative products such as interest-only mortgages (IO mortgages) and hybrid option

adjustable rate mortgages (option ARMs) that often have a variety of adjustable-rate

features and/or negative amortization. Whether the growing variety of mortgage features

has had an effect on consumer welfare is quite controversial. The recent mortgage

foreclosure crisis leads many commentators to point to the growth in the use of these

alternative features as being predatory. A number of academic studies provide supporting

evidence to this view. Complicated loan features may be strategically applied by lenders

to preserve their market power through increasing consumer confusion (Carlin, 2009). In

addition, Bond, Musto, and Yilmaz (2009) suggest that predatory lending tend to be

associated with features such as prepayment penalties and balloon payments.

In contrast, economists have long noted that mortgage menus provide an effective

mechanism for reducing the information asymmetry that exists between borrowers and

lenders. The diverse mortgage choices faced by consumers is functionally similar to the

coverage-price choices commonly observed in the insurance market. Rothschild and

2

Stiglitz (1974) illustrate that the empirically observed positive correlation between

insurance coverage and risk occurrence is attributable to adverse selection. When

information asymmetry is present, allowing for diverse choices is efficiency-enhancing

because an agent’s choice can convey private information. In light of the current financial

crisis, understanding the screening functions of various mortgage contract instruments

becomes particularly important. For example, are massive mortgage defaults exacerbated

by the increasing variety of unfair contracts? Or, do borrowers with greater expected

default risk simply prefer those mortgage features that became available in recent years?

The answers to these questions have important welfare and policy implications. This

dissertation focuses on the screening mechanisms contained in mortgage instruments.

Thus, one of the goals of this dissertation is to analyze the welfare implications of

allowing for a greater variety of loan products in the residential mortgage market.

Studies examining the screening function of mortgage instruments usually assume

that borrowers select among different mortgage products based on their risk profiles to

maximize expected utility. A borrower’s mortgage choice may reveal private information

about her risk type. Thus, lenders can design and offer different mortgage products as a

screening mechanism to separate borrowers of different risk types. Screening devices that

have been extensively studied in mortgage literature include the loan-to-value (LTV)

ratio (Brueckner, 2000, Harrison, Noordewier, and Yavas, 2004), adjustable-rate

mortgage (ARM) versus fixed rate mortgage (FRM) contracts (Brueckner, 1992, Posey

and Yavas, 2000), mortgage points (Brueckner, 1994, Stanton and Wallace 1998) and

prepayment penalty (Brueckner, 1994). This line of research often applies the Rothschild

3

and Stiglitz framework (1976) and shows that a separating equilibrium may be obtained

through borrowers’ self-selection.

This dissertation also aims to contribute to the existing literature on mortgage

choices. Most previous studies limit their exploration to a single risk dimension, default

or prepayment risk. Screening devices concerning default risk include loan-to-value

(LTV) ratio, contract types (FRM versus ARM) and mortgage duration. For example

Bruckner (2000) points out that when the cost of default (e.g. damage to one’s credit

history) is private information and heterogeneous across borrowers, low-cost borrowers

tend to select high LTV loans and pay a price premium (e.g. private mortgage insurance).

Subsequently, those borrowers are more likely to default on their loan. Harrison et al.

(2004) further emphasize the important role of default costs in determining the screening

role of LTV ratios. In their model, information asymmetry comes from expected future

income. The authors show that the correlation between greater default risk and high LTV

choice holds only when the cost of default is relatively modest. In contrast, when default

cost is high, a high-default-risk borrower will select a low LTV loan to avoid the adverse

consequence from default. In addition, the choice between ARM and FRM contracts may

also serve as a screening mechanism of default risk. Posey and Yavas (2000) show that

borrowers with low (high) expected future income tend to select the ARM (FRM)

contract.

On the other hand, choices about mortgage discount points and prepayment

penalty are traditionally considered to convey private information on borrower’s

prepayment risk (mobility). Dunn and McConnell (1981) first suggested that mortgage

points serve as a back-door prepayment penalty for the lender to charge for the embedded

4

prepayment option. In contrast, Kau and Keenan (1987) pointed out that tax

considerations may play a crucial role in determining points paid on purchase loans.1

Because discount points on purchase mortgage may be deducted all at once at origination

while the interest rate deduction is spread across the life of the loan, borrowers with high

marginal tax rates are more willing to pay points in order to receive a low interest rate.

While examining one risk dimension at a time substantially simplifies the

analysis, it also omits the fact that multiple sources of information asymmetry may be at

work in shaping the mortgage market equilibrium. It is well-known that a mortgage

contract contains two types of risk: default risk and prepayment risk. A single device may

possess dual screening roles. For instance, the choice of contract types, FRM versus

ARM, may reflect the borrower’s self-selection based on both mobility (Brueckner,

1992) and default risk (Posey and Yavas, 2001). Therefore, to fully understand borrower

mortgage choices, it is necessary to incorporate multiple screening functions

simultaneously into a unified framework. This dissertation fills this gap by exploring the

multiple screening functions of mortgage instruments. In each of the following three

chapters, more than one type of risk is considered. Collectively, the dissertation answers

two important questions. First, how do multiple sources of information asymmetry

interact with each other and jointly determine a borrower’s mortgage choice? Second, if

one screening mechanism possesses a multi-dimensional screening role, how do lenders

interpret the realized mortgage choices?

1 Points paid for purchase loan are deducted at the year of origination; points paid for refinance loan are

amortized over the life of the loan.

5

Chapter 2 illustrates the screening role of prepayment penalty on default and

prepayment risks. The screening function of prepayment penalty on default risk has been

largely ignored by previous studies. The study shows that borrowers with higher default

risk are more willing to accept prepayment penalty in exchange for a lower interest rate.

It then examines the interaction between the two screening functions of the prepayment

penalty, and shows that the borrower mobility and default risk jointly determine the

mortgage market equilibrium. In particular, the willingness of a borrower to accept

prepayment penalty may stem from her low mobility risk and/or high default risk. The

choice of a higher prepayment penalty sends the lender conflicting signals about the

borrower’s mobility versus default risk type; thus rendering the screening role of

prepayment penalty ambiguous. As a result, for certain parameter combinations, the

model also generates a pooling equilibrium where all borrower types obtain the same

contract.

Chapter 3 focuses on the dual screening role of mortgage discount points. It

proposes to show that there exists a separating equilibrium such that borrowers with

higher (lower) transaction costs pay more (less) discount points to obtain a lower (higher)

interest rate. This equilibrium is also characterized by the low-cost (higher prepayment

risk) borrower imposing a negative externality on the high-cost (lower prepayment risk)

borrower. The proposed study suggests a new screening function of mortgage points, and

it complements the conventional mobility-based theory that suggests that discount points

are a signal of the borrower’s expected mobility. Given this potential dual screening role,

it remains unclear that how lenders interpret the signals generated from realized points-

coupon choices. Thus, in contrast to previous studies that focus solely on the borrower’s

6

choice, the study empirically examines the screening role of discount points from the

lender’s perspective. The empirical results suggest that lenders are more likely to

securitize loans originated by borrowers with high cost of refinance.

Chapter 4 studies the correlation between default and prepayment risk in a

screening framework. Borrowers with different risk profiles exhibit distinct preferences

for prepayment penalties. This heterogeneity can emerge from the link between default

and prepayment risks established by common residential mortgage underwriting practice.

Typically, income level is used as one of the important criteria in residential mortgage

underwriting for determining a borrower’s qualification. However, an often overlooked

fact is that income level is also a crucial determinant of prepayment probability. A

borrower considering refinancing must qualify for a new loan first (Archer, Ling, and

McGill, 1996). Although a borrower may wish to refinance when the prepayment option

is sufficiently in the money, his ability to do so may be impeded by insufficient income.

Thus, compromised financial strength not only may trigger default but also increase the

probability that a borrower is ineligible for a new loan. When facing the penalty-coupon

trade-off, borrowers with a greater probability of experiencing future income reduction

(high-risk borrowers) would rationally choose to have prepayment penalties in their

contracts. The intuition behind this separation is that with a higher chance of being

ineligible for a new loan, the willingness to pay an interest rate premium to maintain an

unconstrained prepayment option is reduced. I first construct a theoretical model to

illustrate this intuition. I show that when future income uncertainty is private information,

there exists a separating equilibrium such that borrowers with higher default risk are

more likely to choose mortgage contracts with prepayment penalties.

7

I test the prediction of my model using a sample of securitized mortgages that

contain loans with and without a prepayment penalty. In my sample, all prepayment

penalties expire within a relatively short period of time (e.g. 1, 2, or 3 years). I find that

the positive correlation between prepayment penalties and default rates is attributable to

information asymmetry. The option-based mortgage pricing literature suggests that the

values of the prepayment option and default options are jointly determined. To eliminate

the confounding effect that prepayment penalties may increase default risk through

limiting the value of prepayment option, I examine mortgages that survive beyond the

prepayment penalties’ expiration dates. Variation on mortgage terminations after the

expiration dates are unlikely to be affected by the prepayment penalty. I then compare the

termination outcomes between loans with and without a prior prepayment penalty. I find

that loans that had a prior prepayment penalty continue to default at a higher rate even

after their prepayment penalties expired.

8

Chapter 2

The Dual Screening Role of Prepayment Penalty2

What makes the role of prepayment penalty interesting and more complicated is

that, while high-default-risk borrowers would prefer a contract with a high prepayment

penalty and a low interest rate, high-mobility borrowers would prefer a contract with a

low prepayment penalty and a high interest rate. Thus, a borrower’s contract choice could

send conflicting signals to the lender about her default and prepayment risk type.

Conventional wisdom considers adding a prepayment penalty to a mortgage

contract as a way to separate borrowers based on their expected mobility. Borrowers with

higher (lower) probability of moving would be less (more) willing to exchange

prepayment penalty for a lower interest rate (Brueckner, 1994). Another screening

instrument is mortgage points, which is the upfront fee paid by borrowers at the time of

loan origination. Previous studies on mortgage points include those by Dunn and Spatt

(1985), Chari and Jagannathan (1989), Yang (1992), Brueckner (1994), LeRoy (1996),

Stanton and Wallace (1998), and Chang and Yavas (2009). In general, borrowers who

expect to prepay soon would avoid paying points, and only borrowers with limited

prepayment risk are willing to exchange upfront points for a lower interest rate. A related

and important question is that, if both prepayment penalty and mortgage points can be

used to screen borrower mobility, why is it that the prepayment penalty is used so much

less than mortgage points? In fact, Chari and Jagannathan (1986) suggest that prepayment

2 This chapter is derived from a co-authored paper with Abdullah Yavas entitled ―Prepayment Penalty as a

screening mechanism for default and prepayment risks‖.

9

penalty and mortgage points are perfect substitutes. Brueckner (1994) qualifies this

argument by pointing out the differential welfare effects of prepayment penalty verses

mortgage points. Specifically, the introduction of prepayment penalty can either increase

or decrease welfare. Chapter 2 provides another possible explanation to the limited use of

prepayment penalty by pointing out the conflicting signaling roles of the prepayment

penalty with respect to the mobility versus default risk. The choice of points signals both

a lower mobility risk and a lower default risk. As a result, prepayment penalty is a less

effective screening mechanism than mortgage points.

A single device may possess dual screening roles. For instance, Brueckner (1992)

shows that the choice of contract types—FRM or ARM—reflects the borrower’s self-

selection based on mobility. Specifically, more mobile borrowers favor ARM, and less

mobile borrowers select FRM. Posey and Yavas (2001) suggest that the ARM-or-FRM

choice also may serve as a screening device of default risk. When the default cost is large

enough, borrowers with high (low) probability of income reduction are more likely to

choose ARM (FRM). Collectively, these studies suggest that to fully understand

borrower mortgage choices, it is necessary to incorporate multiple screening functions

simultaneously into a unified framework. Chapter 2 fills this gap by first illustrating the

screening role of prepayment penalty on default risk, which has been largely ignored by

previous studies. I show that borrowers with high default risk are more willing to accept a

prepayment penalty in exchange for a lower interest rate. I then examine the interaction

between the two screening functions of the prepayment penalty. I show that the borrower

mobility and default risk jointly determine the mortgage market equilibrium. In

particular, the willingness of a borrower to accept a prepayment penalty may stem from

10

her low mobility risk and/or high default risk. I establish the conditions under which a

separating equilibrium exists, where borrowers with certain combinations of mobility and

default risks select a mortgage with a prepayment penalty and lower interest rate, and the

remaining borrowers choose a mortgage without a prepayment penalty and a higher

interest rate. The fact that the choice of a higher prepayment penalty sends the lender

conflicting signals about the borrower’s mobility versus default risk type might render the

screening role of prepayment penalty ambiguous. As a result, for certain parameter

combinations, the model also generates a pooling equilibrium where all borrower types

obtain the same contract.

Background on Prepayment Penalty

Prepayment penalty is a charge that a lender makes when a borrower repays part

of or the entire mortgage balance before a certain period of time. Lenders often permit

partial prepayments of up to 20 percent of the mortgage balance in any one year without a

penalty. As is the case with discount points, a prepayment penalty helps the lender recoup

some or all of the expenses associated with putting a loan together, and a contract with a

prepayment penalty has a lower mortgage rate than a contract without one. Unlike points,

which become sunk costs once incurred, a prepayment penalty helps the lender

discourage prepayment and avoid realizing significant losses due to a drop in interest

rates.

Almost every commercial mortgage loan includes a prepayment penalty. The

traditional prepayment penalty is the declining balance, where the penalty is a percentage

of the loan amount, and this percentage declines over time. Another form of prepayment

11

penalty for commercial mortgage loans is yield maintenance, whereby the borrower is

required to make up the difference between the amount of interest that would be earned if

the loan were carried to maturity and the amount of interest that would be earned if the

lender reinvested the prepaid amount in U.S. Treasury securities of the same term.

According to a third type of prepayment penalty—a defeasance clause—the borrower is

required to provide the lender with Treasury securities that yield the same stream of

interest payments and the same balloon payment as the original mortgage. Prepayment

penalties on commercial mortgages may also involve a lockout period during which

prepayment is not allowed under any circumstances. The typical prepayment penalty on

residential loans is a fixed percentage of the loan balance at the time of prepayment if the

loan is prepaid within the first three to five years—although, in some cases, the

percentage amount decreases with time.

Prepayment penalties also exist in residential mortgages. In fact, the majority of

subprime mortgages contain prepayment penalties. According to Standard & Poor’s

(2004), approximately 80 percent of subprime loans contained prepayment penalties as of

2000. The substantial use of prepayment penalty is confirmed by Elliehausen, Staten, and

Steinbuks (2008) and LaCour-Little and Holmes (2008), who respectively reported that

about 60 percent and 90 percent of their subprime loan samples contained a prepayment

penalty.

Although prepayment penalties are much more common on subprime mortgages,

they also exist on prime mortgages. According to the online edition of the Wall Street

12

Journal,3 borrowers generally obtain a reduction in the interest rate of about one-eighth to

three-eighths of a point in return for accepting the prepayment penalty. According to the

same article, seventy percent of the mortgage customers of World Savings Bank in

Oakland, California, opt for a loan with a prepayment penalty, and such major lenders as

Bank of America, Countrywide, and Washington Mutual have prepayment penalties on

some of their prime mortgage loans. In recent years, the proportion of prime loans

containing prepayment penalties have declined significantly, in part because of loan

purchasing standards set by housing Government Sponsored Enterprises (Fannie Mae and

Freddie Mac) and legislative efforts restricting the use prepayment penalties.

The penalty can be applied to prepayment due to a home sale as well as

refinancing, although the latter is more common than the former. Most often, the

prepayment penalty is ―hard,‖ meaning that it is applied whether the borrower refinances

or sells the home. Sometimes, the prepayment penalty is ―soft,‖ meaning that it is applied

only when the borrower refinances.

Whether the lender can charge a prepayment penalty if the lender forces the

borrower to prepay upon the sale of the property as the result of the borrower’s violation

of the due-on-sale provision is a frequently litigated issue with residential mortgages. In

McCausland v. Bankers Life Ins. Co. (Wash. 1988), the court held that the lender should

not be allowed to charge a prepayment penalty upon the sale of the property, because it is

the lender who is requiring the prepayment of the loan. In Eyde v. Empire of America

Fed. Sav. Bank (Mich. 1988), the court held that it was irrelevant why the loan was

prepaid, because the intent of the parties in signing the contract was that the lender had

3 See http://www.realestatejournal.com/buysell/mortgages/20011218-simon.html

13

the right to collect prepayment penalty regardless of the reason for prepayment.4 Even

though federal regulators do not prohibit prepayment penalties, many states restrict the

use of prepayment penalties by state-chartered lenders. Federally chartered lenders in

those states can still charge prepayment penalties if they are adequately disclosed.

The Model

Consider a competitive lending market in which lenders offer a menu of fixed-rate

mortgage contracts with different combinations of interest rate i and prepayment penalty

s. All mortgages mature in three periods. In the first period, a borrower obtains a

mortgage with an outstanding balance of L to purchase a property with a value of P . For

the sake of simplicity, I follow Brueckner (1992) and Posey and Yavas (2001) to assume

that all loans are interest-only loans with a loan-to-value ratio of 100 percent. This

assumption implies that LP . Each borrower has an identical initial income 0y , which

qualifies a borrower for all mortgage contracts available in the menu. A random event,

which determines whether a borrower has to move, occurs in the second period. Each

borrower has a probability of 1 to relocate. A borrower does not sell her property

unless she has to relocate. I assume income uncertainty is associated with moving. If a

borrower moves, her income changes to y, which is a random variable distributed

between y and y according to a density function )( f . This variation of income captures a

4 For a more detailed discussion of these cthet cases, see dirt.umkc.edu/files/prepay.htm

14

borrower’s uncertain job prospects at the new location.5 On the other hand, if relocation

does not occur, the borrower’s second-period income remains at the same level as the

initial income 0y . I also model housing price uncertainty by assuming that there is a

probability of such that property price decreases from P to dP and triggers default in

the second period. For simplification, I assume neither relocation nor property price

change occur in the third period. Both the borrower and the lender are assumed to be risk

neutral.6

First, I examine the borrower’s objective function. It is worth emphasizing that

there exist two sources of default. First, default may be caused by a decline in property

value. Second, default can occur even with constant property price; since relocation

induces income uncertainty, default happens when the second-period income level y is

insufficient to cover the prepayment penalty s plus the interest payment i.7 Hence, the

expected utility for a borrower choosing a contract with interest rate i and prepayment

penalty s, ),( si , is

5 A borrower may lose her job and be forced to take an inferior position at a different location. In this case,

the realized value of y would be lower than y0. On the other hand, relocation may be driven by better job

opportunities and, therefore, is associated with y greater than y0.

6 I avoid prepayments driven by refinancing by assuming a constant interest rate. Allowing the possibility

of refinancing would make the model extremely difficult to track. Instead, I capture the prepayment risk for

the lender by capturing the damage to the lender’s cash flows caused by a possible drop in the borrower’s

income stream due to relocation.

7 Because property value is always equal to the loan balance, the borrower can avoid default by selling the

property in the absence of any prepayment penalty.

15

.))(1)(1(

)()()1(

)()()1(

))(1(

)()()(),(

2

1

0

0

0

j

j

y

is

is

y

y

y

hiy

dyyfisy

dyyfDy

Dy

dyyfDyhiPLysiU

(2.1)

All borrowers have an inter-temporal discount factor . The first term indicates

that a borrower obtains a loan with an outstanding balance of L to purchase a property

with a value of P. With an initial income 0y , the borrower is able to make the first

period’s interest payment i . In return, the borrower receives positive utility h from

housing services. Given the assumption that PL , the first term simplifies to

)( 0 hiy . A number of possible outcomes may occur in the second period. A drop in

property price from P to dP would cause a borrower to default regardless of whether the

borrower is moving. Default imposes a cost D on the borrower (second term and third

term). D represents non-monetary costs such as damage to the borrower’s credit history

and reputation as well as transaction, social, and psychological costs of default. Three

other possible outcomes can occur provided the property value stays at P. The borrower

has a probability of to move and incur the prepayment penalty s. Relocation results in a

change in income and hence may trigger one of two events: default or prepayment.

Default occurs if the realized income y is less than prepayment penalty s plus the interest

payment i (fourth term). On the other hand, if y is greater than s+i, the borrower is able to

avoid default (fifth term). With a probability of 1 , the borrower does not move and

16

holds the loan to maturity. In this case, her income level remains at 0y , she makes interest

payment i and receives the ownership benefit h in both period 2 and 3 (sixth term). The

loan balance is omitted from the loan termination outcomes, because (1) if the property

price drops to dP or the second-period income drops below s+i, the borrower loses the

property to the lender, and (2) if the property value remains at P=L, then P is used to pay

off the loan balance.

A couple of restrictions on the values of s and i are crucial. First, I need to ensure

that when the borrower moves, she does not choose default over prepayment in order to

avoid the prepayment penalty. For this, I will assume D is large enough so that:

Assumption 1: s+i < D.

Otherwise, a borrower is better off to always default when moving occurs.

Second, I assume that the values of y and y are such that s+i falls between y

and y . If s+i is greater than y , the borrower can never afford s+i, and hence only

default can occur upon moving. Similarly, if s+i is less than y , a borrower can always

afford to incur prepayment penalty, and hence a drop in her income would never lead to

default.

Assumption 2: yyis , .

17

This assumption ensures that both default and prepayment can occur when a

borrower moves, depending on the realization of the borrower’s second-period income.

The decision to own a house is rational only if the periodic ownership

benefit h is greater than the periodic interest payment i . For this reason, I assume h to be

large enough so that the following constraint always holds:

Assumption 3: ih .

Assumption 3 implies that the borrower would not want to give up the ownership

benefit by prepaying in the second period when she does not need to move.

All lenders have a discount rate of . I assume that lenders are more patient than

borrowers, . With risk neutrality, the lender’s objective is to maximize the expected

profits:

).)(1)(1(

)1)(1(

)()()1(

)()()1(

)()(),(

2 iL

i

dyyfisL

dyyfcP

cPiLsi

y

is

is

y

d

(2.2)

In the first period, the lender transfers the loan amount L to the borrower and

collects interest payment i (first term). If the property price declines, default occurs

regardless of whether relocation happens. The lender forecloses the property and sells it

18

for its decreased value dP and incurs the foreclosure cost of c (second term).8 If the

property value stays at P, three possible outcomes can take place. First, if the borrower

moves and the realized income of the borrower turns out to be lower than s+i, default

occurs. The lender forecloses the property and collects cP (third term). Second, if

relocation is accompanied with high income (greater than s+i), the borrower prepays. In

addition to receiving the loan amount L, The lender also collects the prepayment penalty

s and the interest payment i (fourth term). Third, if there is no relocation, the lender

receives the interest payment i in the second period and is repaid with the loan amount L

plus the earned interest i when the mortgage matures in the third period (fifth and sixth

terms).

To characterize the competitive market equilibrium, I first examine the

indifference curve of the borrower and the iso-profit curve of the lender. These curves

respectively describe the borrower’s and lender’s trade-off between prepayment penalty s

and contract rate i . To derive the slope of the borrower’s indifference curve, I implicitly

differentiate s with respect to i holding ),( siU constant. This gives us the marginal rate of

substitution between s and i .

8 Lenders incur foreclosure costs due to 1) legal costs associated with the foreclosure process, 2) negative

publicity and damage to reputation, and 3) depreciated property value. Campbell, Giglio, and Pathak (2009)

find that foreclosed properties are sold at a substantial discount as opposed to their fair market value. I

capture these costs in c.

19

.

)()()()1(

)1)(1()()()()1(12

1

y

is

j

jy

is

s

iU

dyyfisfDis

dyyfisfDis

U

U

i

sMRS

(2.3)

The numerator is positive, and the denominator is negative since is is strictly

less than D. Hence, indifference curves are downward sloping. This indicates that the

borrower’s disutility as a result of accepting greater prepayment penalty must be

compensated through a lower interest rate in order for the borrower to remain on the

same indifference curve.

To derive the slope of the lender’s iso-profit curves, s is implicitly differentiated

with respect to i holding profit constant. The slope is given by

.

)()()()1(

)1)(1()()()()1(12

1

y

is

j

jy

is

s

i

isfcisdyyf

isfcisdyyf

i

sMRS

(2.4)

Following Brueckner (2000) and Harrison et al. (2004), I simplify the analysis by

assuming uniform density for the distribution of income contingent on moving. With this

assumption, the slope of the borrower’s indifference curve and the lender’s iso-profit

curve can be obtained by substituting the uniform density function for )( f into equations

(2.3) and (2.4). It follows that

20

,1

)22)(1(

)1)(1(12

1

yDis

yy

MRSj

j

U

(2.5)

.1

)22)(1(

)1)(1(12

1

ycis

yy

MRSj

j

(2.6)

Note that the indifference curves and iso-profit curves are convex, because

assumptions 1 and 2 yield 0/ sMRSU and 0/ sMRS ; that is, as s increases,

the indifference curves and iso-profit curves become steeper (more negative).9 Both low

interest rate and low prepayment penalty are desirable from a borrower’s perspective.

Thus, indifference curves located on the lower left-hand side correspond to higher utility.

Aligned with this intuition, I have both marginal utilities, sU and iU , less than zero. In

order for an equilibrium to exist, zero-profit curves need to be downward sloping and

have a tangency point with the borrower indifference curves. That is, MRSMRSU has

a solution ),( ** si . This implies that the following must be true in equilibrium:

2/)( cyis .10

Before analyzing the mortgage market equilibrium under asymmetric information,

it is useful to first consider the equilibrium with homogeneous borrowers. When all

borrowers are identical, the equilibrium mortgage contract must lie on the zero-profit

9 Strict convexity of indifference and zero-profit curves ensure that the indifference curve of a borrower

type cannot be tangent to the zero-profit curve from below for that type at more than one point.

10 UMRS is strictly negative, and the numerator in the first term of MRS is strictly positive.

MRSMRSU implies that the denominator in the first term of MRS must be strictly negative.

Simplification yields 2/)( cyis .

21

line, defined by 0),( si . The borrower’s utility is greater on lower indifference curves

(lower penalty and lower interest rate). Thus, the point where the lowest indifference

curve is tangent to the zero-profit curve gives the equilibrium contract. The optimality

requires the zero-profit curves to be more convex than the indifference curves.11

This

requirement is satisfied with )( f being uniform.

Now that I have derived the properties of indifference curves and zero-profit

curves, I can characterize the mortgage market equilibrium. I define equilibrium as a set

of mortgage contracts such that (1) each borrower chooses the contract that maximizes

her expected utility, and (2) lenders earn nonnegative profit and have no incentive to

offer contracts outside the equilibrium set. I first consider the equilibrium under full

information.

Equilibrium with Full Information

Suppose there exist two types of borrowers—type A and type B—which are

different in mobility, , and/or default risk y . I characterize the heterogeneity of income

uncertainty using different levels of the lower bound of second-period income y .12

With

second-period income being uniformly distributed, a lower y implies a greater

probability of y falling below s+i. In other words, borrowers with lower (higher) y are

11 The slope difference between zero-profit lines and indifference curves is negative (positive) when s is

less (greater) than s*, where s* is the s value at the tangency point of the zero-profit and indifference

curves. It indicates that the zero-profit curve is flatter than the indifference curve for s < s* and steeper for

s > s*.

12 One could alternatively model the heterogeneity of default risk by having borrowers differ with respect to

y . The results are similar.

22

more (less) likely to default. The mobility-default combinations of type A and type B

borrowers are respectively ),(AA y and ),(

BB y . The full information assumption

implies that borrower types are known to the lender. The first-best contracts are those that

maximize utility for each borrower type while ensuring nonnegative lender profit. The

lender’s problem is simple. Because lenders can observe each borrower’s risk type and

because the mortgage market is competitive, each lender in equilibrium offers the

combinations of prepayment penalty and interest rate that earn zero profit for each

borrower type. These contracts can be obtained by substituting ),(AA y and ),(

BB y ,

respectively, into equations (2.1) and (2.2). For each type of borrower, the point where

the lowest indifference curve is tangent to the zero-profit curve yields the equilibrium

contract.

To illustrate, consider the cases when borrowers are heterogeneous only in one

risk dimension—mobility or default risk. Figure 1 illustrates the full information

equilibrium contract when the borrowers differ with respect to mobility risk only.

Mobility affects the relative positions of the zero-profit curves for the two borrower

groups. The difference in heights of the lender’s zero-profit curves can be obtained by

setting equation (2.2) to zero and differentiating s with respect to , which yields

s / . Because 0 s

13, this derivative is positive if 0 and negative if

0 . While is mathematically ambiguous in sign, I restrict the attention to the

13 As established earlier, 2/)( cyis is necessary for the equilibrium requirement that zero-profit

curves are downward sloping and has a tangency point with a borrower’s indifference curve. This yields

.0)22)(1( yciss

23

case that 0 to later study the interesting dynamics of mobility risk and default

having opposite effects on borrower’s preference.14

Intuitively, 0 implies that the

high-mobility borrower’s zero-profit curve is above the low-mobility borrower’s zero-

profit curve, which in turn implies that serving the high-mobility borrower is less

profitable from lender’s perspective for any given ),( si . To be more precise, I only

consider the markets where the following condition is satisfied.

yy

yyiPiisyisPyiscP

)()())(())(()1( < 0 .

(2.7)

A high enough foreclosure cost for the lender, c, for instance, will suffice to meet this

condition. The first-best contracts are shown in figure 2.1 as ),( ** hh si for the high-

mobility type and ),( ** ll si for the low-mobility type.

Figure 2.2 illustrates the full information equilibrium when the borrowers differ

with respect to default risk only. I examine the difference in heights of the lender’s zero-

profit curves between the two risk types by setting equation (2.2) to zero and

differentiating s with respect to y , which yields sy / . Because y is strictly less than

zero, this derivative is negative since the zero-profit curves are downward sloping

)0( s . It implies that the low-default-cost borrower’s zero-profit curve is located in

the lower left-hand side of the high-default-cost borrower’s zero-profit curve. The first-

14 If 0 , higher mobility corresponds to lower risk. In this case, mobility risk and default risk will

work in the same direction in affecting the borrower’s preference. Both lower mobility (higher risk) and

higher default probability will provide incentive for borrowers to accept a prepayment penalty.

24

best contracts are shown in figure 2.2 as ),( ** hh si for the high-default type and ),( ** ll si

for the low-default type.

However, the first-best contracts are often not feasible for two reasons. First,

lenders usually do not possess the information necessary to identify borrower types,

because mobility and default likelihood are private information. Second, even if lenders

can correctly infer a borrower’s type using observed borrower characteristics (e.g., age,

gender, etc.), legal restrictions against lending discrimination may prevent a lender from

imposing different contracts based on those borrower characteristics. Hence, the lender

must allow the borrower to choose among the set of offered contracts. If the lender were

to offer the two first-best contracts in the case shown in Figure 1, high-mobility

borrowers would prefer low-mobility borrowers’ first-best contract ),( ** ll si , which lies

on the southwest side of ),( ** hh si , to their own first-best contract. If both borrower types

would select the contract ),( ** ll si , the lender earns a negative profit. This outcome is

inconsistent with equilibrium. Thus, first-best contracts cannot be an equilibrium

outcome under asymmetric information.

Equilibrium with Asymmetric Information

I now turn to the dual screening role of prepayment penalty under asymmetric

information. I first hold default risk constant across borrowers and only consider the

prepayment penalty’s screening function on mobility. Then I shift focus on default risk to

examine how the mortgage market equilibrium is shaped when borrowers are

25

heterogeneous in their default risk only. Finally, I examine the case where heterogeneities

of both mobility and default risk are allowed.

Heterogeneous Mobility

I assume that all borrowers are identical in all aspects except for their probability

of moving. Suppose there exist two types of borrowers: borrowers with high mobility and

borrowers with low mobility. The probabilities of relocation are h and l for high- and

low-mobility borrowers, respectively, with hl . It is common knowledge that the

proportions of high-mobility type and low-mobility type borrowers in the population are,

respectively, and 1 . I first focus on the borrower’s indifference curve. In

particular, the relative slope of the indifference curves of the two borrower types is

critical in shaping the equilibrium. Differentiating the slope of the indifference curve with

respect to a borrower’s probability of moving for any given ),( si point yields

.0)22)(1(

)()1(1

2

2

1

isDy

yyMRS j

j

U

(2.8)

Equation (2.8) is strictly positive, since s+i is strictly less than both D and y . As

increases, the slope of the borrower’s indifference curve becomes greater (less

negative). Thus, the low-mobility borrower’s indifference curve passing through a given

),( si point is steeper than the high-mobility borrower’s indifference curve. The steeper

indifference curves of low-mobility borrowers suggest that they are more willing than

high-mobility borrowers to trade a prepayment penalty for a lower interest rate.

26

Proposition 2.1: When borrowers are different only in their mobility, there exists

a separating equilibrium such that low-mobility borrowers obtain loans with greater

prepayment penalty and lower interest rate than high-mobility borrowers.

Proof. See appendix A.

The equilibrium is illustrated in figure 2.1. The high-mobility borrower receives

her first-best contract ),( ** hh si , which corresponds to the tangency point between the

lowest indifference curve and the zero-profit curve for the high-mobility borrower. As I

have discussed previously, the low-mobility borrowers cannot be offered their first-best

contract ),( ** ll si because the lender would incur a loss by offering ),( ** hh si and ),( ** ll si

simultaneously. To satisfy the incentive compatibility constraint, the low-mobility

borrower’s contract must not be strictly preferred by high-mobility borrowers. Hence,

low-mobility borrowers receive contract ),( ll si , which is located where the low-mobility

indifference curve passing through ),( ** hh si cuts the low-mobility zero-profit curve.

Similar to the Rothschild-Stiglitz model (1976), an equilibrium does not always

exists. When the proportion of high-mobility type is sufficiently small, the separating

equilibrium described in proposition 1 is unsustainable. One can break the separation by

offering a pooling contract ),( pp si located between the two zero-profit curves but below

both indifference curves passing through ),( ll si . However, such a pooling contract would

27

not be sustainable in itself because one can simply offer an alternative contract above the

high-risk indifference curve and below the low-risk indifference curve passing this

pooling contract. Thus, to have the separating equilibrium described in proposition 1, it is

necessary that is sufficiently large, such that ),( pp si , if offered, generates negative

lending profit.

It is worth pointing out that high-mobility borrowers receive their first-best

contract ),( ** hh si , and their welfare is unaffected by asymmetric information. In contrast,

low-mobility borrowers are deprived from obtaining their first-best contract ),( ** ll si and

offered contract ),( ll si instead, which is inferior to their first-best contract. This is

consistent with the standard screening model in that the high-risk type (high-mobility

borrower) imposes a negative externality on the low-risk type (low-mobility borrower).

The difference between ),( ** ll si and ),( ll si represents the signaling cost that low-risk

borrowers would have to incur in order to signal their type to the lender.

Heterogeneous Default Risk

I now turn to the screening function of the prepayment penalty with respect to

default risk. To highlight the screening role of the prepayment penalty with respect to

default risk, I assume that borrowers are identical in all respects except for their

probability of default.

To characterize different levels of default risk, I assume borrowers are different in

their income uncertainty upon moving. Suppose there exist two types of borrowers:

28

borrowers with high default risk and borrowers with low default risk. Let h

y and l

y

represent the lower bounds of income for the high- and low-default-risk borrowers,

respectively, with hl

yy . It is common knowledge that the proportions of high-default

type and low-default type borrowers in the population are, respectively, y and y1 . To

examine how heterogeneous default risk influences the borrower’s mortgage choice, I

perform a similar analysis as I did previously for mobility. Differentiating the slope of the

borrower indifference curve in equation (2.5) with respect to y for any given ),( si yields

.0)22)(1(

)1)(1(12

1

isDyy

MRS j

j

U

(2.9)

As suggested by equation (2.9), the high-default-risk borrower’s indifference

curve passing through a given ),( si point is steeper than the low-default-risk borrower’s

indifference curve. The steeper indifference curves of high-default-risk borrowers suggest

that they are more willing than low-default-risk borrowers to trade prepayment penalty

for a lower interest rate.

Proposition 2.2: When borrowers differ in their default risk only, there exist a

separating equilibrium such that high-default-risk borrowers obtain loans with a greater

prepayment penalty and a lower interest rate than low-default-risk borrowers.

Proof. See appendix A.

29

It is necessary to assume the proportion of high-default type, y , is large enough

to rule out the no-equilibrium situation, the equilibrium is illustrated in figure 2. The

high-default borrower receives contract ),( ** hh si , which corresponds to the tangency point

between the lowest indifference curve and the zero-profit curve for the high-default

borrower type. The low-default borrower receives contract ),( ll si , which is located

where the low-default borrower’s indifference curve passing through ),( ** hh si cuts the

zero-profit curve for the low-default risk type. Again, I obtain the standard result in that

the high-risk type (high-default borrowers) imposes a negative externality on the low-risk

type (low-default borrowers), and the difference between the payoff of contract ),( ** ll si

and ),( ll si is the signaling cost that low-risk borrowers would have to incur.

Heterogeneous Mobility and Default Risk

I have shown that the screening roles of prepayment penalty differ with respect to

mobility versus default risk. I now study the role that prepayment penalty plays in

inducing self-selection when borrowers are heterogeneous in both risk attributes. It is

useful to first examine the aggregated effects of mobility and default risks on the slope of

a borrower’s indifference curves and overall risk type. As an example, consider a

borrower with high mobility and high default risk. Mobility and default risk work in

opposite directions in affecting the slope of the borrower’s indifference curve. High-

mobility borrowers are less willing to accept a prepayment penalty, while high-default

borrowers are more willing to do so. But the two risk attributes work in the same

30

direction in elevating the borrower’s risk for the lender. Therefore, a borrower with high

mobility and high default risk will be considered as very risky from the lender’s

perspective. Table 2.1 summarizes the aggregated effects on the slope of the borrower’s

indifference curves and on her overall risk type for the four combinations of mobility and

default risks.

Consider two borrower types—type A and type B—who are different in both

mobility and default risk. Let the mobility-default combinations of the two types be given

by ),(AA

y and ),(BB

y , respectively, withBA

andAA

yy .15

I assume it is

common knowledge that the proportions of type A and type B borrowers in the population

are, respectively, A and A1 . I first consider the existence of pooling equilibria. I then

discuss separating equilibria that emerge from different mobility-default combinations.

Pooling Equilibrium

I discuss two scenarios from which a pooling equilibrium can emerge. First, a

pooling equilibrium is feasible when borrowers have indifference curves with identical

slopes (identical UMRS for both types). As suggested by Table 2.1, the two risk attributes

may work in opposite directions in such a magnitude that they equalize the slopes of the

indifference curves across borrower types. In this case, prepayment penalty fails to serve

15 When

BA , the problem reduces to the case where borrowers are only heterogeneous with respect

to default risk. When BAyy , the problem reduces to the case where borrowers are heterogeneous only

with respect to mobility. When both are equal, I have trivial case where borrowers are completely

homogeneous. I do not impose restrictions on the size of A relative to B and the size of Ay relative to

By . Hence, I are able to consider all four possible combinations of ),(

AA y and ),(BB y : 1) BA and

BAyy ; 2) BA and BA

yy ; 3) BA and BAyy , and 4) BA and BA

yy .

31

as a screening device in distinguishing risk types. Second, a pooling equilibrium is

possible when the two zero-profit curves cross each other.

Scenario 1

A sufficient condition for a pooling equilibrium is that the slopes of borrowers’

indifference curves are identical across different risk types. To derive the mobility-default

combinations that fulfill this requirement, I substitute ),(AA

y and ),(BB

y ,

respectively, into equation (2.5) and set them to be equal. Thus, I have

.

)22)(1(

)1)(1(1

)22)(1(

)1)(1(12

1

2

1

yDis

yy

yDis

yy

MRSMRS

B

B

j

Bj

A

A

j

Aj

B

U

A

U

(2.10)

Simplifying yields

.

))1)(1(1

)1)(1(1

2

1

2

1

A

B

A

j

Bj

B

j

Aj

yy

yy

(2.11)

In the special case when equation (2.11) is satisfied, the indifference curves of the

two borrower types have the same slope at any ),( si point. The relative profitability of

serving each group of borrower depends on both and y . For equation (2.11) to hold, I

must have either BA and BA

yy or BA and BA

yy . In other words, high

mobility must be matched with high default risk. The intuition can be seen in table 2.1.

32

Because greater mobility reduces the slope of the indifference curves, it must be paired

with high default risk that has the opposite effect. It is clear that the borrower type with

high mobility and high default risk (H/H) must have her zero-profit curve located to the

northeast of that of the borrower type with an L/L combination.16

I define the borrower

type L/L (H/H), which has a lower (higher) zero-profit curve, as low- (high-) risk type.

When two distinct zero-profit contracts are offered to different types of borrowers, the

zero-profit contract for the low-risk type is strictly preferred by all borrowers. Because of

the identical slopes of the indifference curves of the two borrower types, the high-risk

type borrower would always imitate the low-risk borrower, which makes it impossible for

a separating equilibrium to exist.

Proposition 2.3: When the parameters of the model satisfy equation (2.11), there exists a

pooling equilibrium where both borrower types obtain the same contract.

Proof. See appendix A.

The equilibrium, which is illustrated in figure 2.3, is similar to the pooling

equilibrium characterized by Harrison et al. (2004) in the sense that the feasibility of a

separating equilibrium is eliminated by parallel indifference curves of different borrower

types. In Harrison et al. (2004), the parallel property relies on default cost satisfying

certain parameter conditions. In the model, default and prepayment risk work in opposite

16 I use the format mobility/default to denote the risk combinations where M and D stand for mobility and

default risks, and take the value of high (H) and low (L). For example, H/H indicates a borrower has

relatively high mobility and high default risk.

33

directions. When considered separately, each force may produce distinct contractual

outcomes by altering the relative slopes of indifference curves of different borrower

types. In fact, in the model, when the borrowers differ in only one dimension—that is,

when either )(BA

or )(BA

yy —then equation (2.11) would never hold. In the

special situation when the borrowers differ with respect to both risk dimensions, then it

becomes possible for the two opposing risk dimensions to exactly offset each other, in

which case the slopes of indifference curves become identical for the two borrower types

and only a pooling equilibrium exists.

Scenario 2

I now turn to the second scenario for a pooling equilibrium. When borrowers are

different in both mobility and default risk, the relative positions of the zero-profit curves

depend on the parameter combination of ),(AA

y and ),(BB

y . I have shown that both

high mobility and high default risks are undesirable from the lender’s perspective. When

both risk attributes can vary, then depending on the combinations of the two risk

attributes possessed by the borrower, the zero-profit curve of type A borrower may lie

above or below the zero-profit curve of type B borrower. The two zero-profit curves may

also intersect each other, in which case the mobility and default risks of the two borrower

types are canceling each other out, making profitability from the two types relatively

similar. Specifically, high mobility risk must be matched with low default risk and vice

versa. I denote the L/H borrowers as type A and the other (H/L borrowers) as type B.

Table 2.1 suggests that a type-A borrower must have a steeper indifference curve than a

34

type-B borrower. To formally establish this, I can write the slope differential between

type A and type B as the following:

.y

MRSyy

MRSMRSMRS UBAUBAB

U

A

U

(2.12)

From equations (2.8) and (2.9), I know both /UMRS and yMRSU / are

strictly positive. Provided BA and BA

yy , (2.12) is strictly negative. Thus, type-A

indifference curves must be steeper than type-B indifference curves.

When borrowers are heterogeneous in both mobility and default risks, the two

zero-profit curves may intersect each other. Let us denote this intersection by ),( QQ siQ

The height differential of the two zero-profit curves between type A and type B is given

by

,y

syy

s BABA

(2.13)

holding 0 BA . When there is an intersection, (2.13) must be equal to zero

for some i and s. This condition trivially holds when BA and BA

yy for any i and

s. When BA and BA

yy , the existence of Q implies there exist ),( QQ si that solves

./

/

y

yyAB

BA

(2.14)

The right-hand side of (2.14) is strictly negative because 0/ y and

0/ . If BA , B

y must be less than A

y for (2.14) to hold. In other words,

high mobility must be matched with low default risk for Q to exist. When there is a Q, it

35

is unique because type-A zero-profit curve is always steeper than type-B indifference

curve.17

Conditioned on the existence of Q, it is possible for the tangency points between

the indifference curves and the zero-profit curves to lie on the same or different sides of

Q. I show that there exists a pooling equilibrium when the two zero-profit curves

intersect each other and the two tangency points lie on different sides of Q.

As illustrated in figure 2.4, when zero-profit curves intersect and the tangency

points lie on different sides of Q, it must be the case that the tangency point of type B

borrowers, who have a steeper indifference curve, lies above Q, and the tangency point of

type A borrower lies below Q. To establish this fact, I equate the slopes expressions in

equations (2.5) and (2.6). After simplification, I obtain

.)22(

)22(

)1)(1(1

)1)(1(1

2

1

2

1

ycis

yDis

j

j

j

j

(2.15)

The left-hand side of equation (2.15) is increasing in , and the right-hand side is

increasing in s+i. Therefore, I must have 0/)( ** is at the tangency points. In

addition, *s and *i must also satisfy equation (2.2), the zero-profit condition. Thus, by

solving equation (2. 2), I can write *s in terms of *i and other parameters and have

.01

)( *

*

****

i

i

siis (2.16)

17 I can write the slope differential between type A and type B zero-profit curve as

yMRSyyMRSMRSMRSBABABA // . Both /MRS and

yMRS / are strictly positive. Provided

BA and BA

yy , BA MRSMRS is strictly

negative. Thus, type-A zero-profit curves must be steeper than type-B zero-profit curves.

36

From equation (2.6), I know that 1/ ** is . Thus, /*i must be strictly

negative for (2.16) to hold. 0/)( ** is and 0/* i collectively imply

0/* s . In addition, equation (2.15) is independent of default risk y . At a tangency

point, It must be true that 0/)( ** yis . Combine it with the zero-profit condition, I

have

.01

)( *

*

****

y

i

i

s

y

iis (2.17)

Equation (2.17) implies that 0/* yi . 0/)( ** yis and 0/* yi

collectively imply 0/* ys . Hence, when the tangency points lie on different sides of

the intercept, it must be that the tangency point of type B borrower (H/L borrower with

flatter indifference curves) lies above that of type A borrower, ** AB ss .

If there exists an intersection Q between the two zero-profit curves, it must be the

case that the type A zero-profit curve, which is steeper, is above (below) that of the type

B zero-profit curve for s values above (below) Q. If the intersection Q lies between the

two tangency points, it must be the case that, conditional on *Ass , the i value on zero-

profit curves must be smaller for type A than for type B, and, conditional on *Bss , the

i value on zero-profit curves must be greater for type A than for type B. Mathematically,

I state those two conditions as

),,(),( *** ABAA sisi (2.18)

),,(),( *** BBBA sisi (2.19)

37

where BAji j ,, denotes the zero-profit contract rates of types A and B. I use

BAkBAjsi kj ,;,),,( * to denote the i values on a zero-profit contract rate of type j

borrower when s takes the tangency-point value. I illustrate the underlining intuition in

figure 4. Expressions (2.18) and (2.19) collectively state that ),( ** BB si is located on the

left-hand side of ),( *BA si , and ),( ** AA si is located on the right-hand side of ),( *AB si .

This leads to the following proposition:

Proposition 2.4: When ),(),( *** ABAA sisi and ),(),( *** BBBA sisi , there exists a pooling

equilibrium at Q, the intersection of the zero-profit curves for the two borrower types,

where both borrower types obtain the same contract.

Proof. See appendix A.

Additional assumptions on A and A1 are necessary to rule out the no-

equilibrium situation. A pooling contract that is between the zero-profit curves and below