Loyalty: How to attract & retain customers via mobile. (Vueling)

Industry Monitor. Issue 170. 02/03/2015 Page 1 © EUROCONTROL 2015

European flights decreased by 0.2% in January 2015 compared with January 2014 due to a slow first week and declining traffic to Russia during the month. Preliminary data for February show an increase of 0.7% in flights on February 2014.

IATA reported that European scheduled passenger traffic (RPK) increased by 5.8% in 2014 (vs. 2013). Capacity was up 5.2% and the total passenger load factor was 80.8%

Oil prices rose from an average of €44 per barrel in January towards €52 per barrel in February 2015.

EUROCONTROL statistics and forecasts 1

Other statistics and forecasts 2

Passenger airlines 2

Financial results of airlines 7

Airports 7

Oil 8

Economy 8

Fares 8

EUROCONTROL statistics and forecasts European flights ESRA – EUROCONTROL Statistical Reference Area) decreased by 0.2% in January 2015 compared with January 2014 due to a slow first week and declining traffic to Russia during the month. This was below the low forecast range. Preliminary data for February show an increase of 0.7% in flights on February 2014 (Figure 1). With an increase of 7.4%, the low-cost segment was the only driver of growth in January 2015 (vs. January 2014). The charter segment decreased by 17.3% and was followed by Business Aviation (down 5.6%), Traditional Scheduled and All-Cargo, both segments were down 1.5% on January last year. Turkey and UK were the major contributors to local traffic1 on the European network in January 2015 (vs. January 2014), adding circa 200 daily flights between them. Portugal, Spain and Greece added altogether 160 daily flights and completed the top five contributors. At the other end of the scale, Ukraine remained severely impacted by the closure of some of its airspace and saw an overall flights decrease of 77% (28,400 fewer flights than in January last year) compared to January 2014 (EUROCONTROL, February).

1 International Departures/Arrivals, excluding overflights

Industry Monitor The EUROCONTROL bulletin on air transport trends

Issue N°170. 02/03/2015

Industry Monitor. Issue 170. 02/03/2015 Page 2 © EUROCONTROL 2015

Based on preliminary data from airlines for delays from all causes 37% of flights were delayed on departure (>= 5 minutes) in January 2015; this was an increase of 5.7 percentage points when compared to the same month in 2014. The average all-causes delay per movement in January 2015 increased from 7.8 minutes to 9.8 minutes. Further analysis of the delay reasons shows that Reactionary and Airline delay increased respectively by 0.5 and 0.8 minutes per flight (Figure 2). (EUROCONTROL, February).

Other statistics and forecasts IATA reported that European scheduled passenger traffic (RPK) increased by 5.8% in 2014 (vs. 2013). Capacity was up 5.2% and the total passenger load factor was 80.8% (IATA, 5 February) ACI reported that overall passenger counts at European airports saw an increase of 4.9% in 2014 compared with 2013. Total aircraft movements were up 2.6% in 2014. Cargo tonnage was up 3.6% on last year (ACI, 5 February).

Passenger airlines

Capacity, costs and jobs

Corsair, a subsidiary of TUI Group, is to be sold to Groupe Dubreuil which owns a stake in Air Caraïbes. Both airlines will operate separately from Paris Orly with Air Caraïbes serving the Caribbean while Corsair will focus on the Indian Ocean along with Senegal and Ivory Coast, the West Indies and Montreal. The Group plans a new fleet which will consist of 11 Airbus A350 aircraft to be delivered between 2016 and 2024. The current airlines’ joint fleet amounts to 15 aircraft serving 15 destinations. Reacting to the news, Corsair unions called a 3-day strike (27 Feb – 1 March) on the ground that the takeover by Air Caraïbes will result in job cuts at Corsair. (Groupe Dubreuil, 20 February & Corsair, 27 February).

Feb15 Estimate

Figure 1: Monthly European Traffic and Forecast.

Industry Monitor. Issue 170. 02/03/2015 Page 3 © EUROCONTROL 2015

Etihad Regional (flights operated by Swiss Darwin Airlines) plans to restructure its operations and diversify its business model, increasing its activity as a contract services supplier. The airline will cancel its scheduled flights in France and Germany and increase its service in Italy. (Etihad Regional, 18 February). Sun Express, the joint venture of Lufthansa and Turkish Airlines will take delivery of five B737-800 aircraft in the course of 2015 as part of an order for 25 B737-800NG aircraft and 15 B737-8MAX aircraft to be delivered by 2021 (Sun Express, 19 February). Icelandic low-cost WOW Air has leased two A321 aircraft for use on its new transatlantic routes from Reykjavik to Boston (27 March) and Reykjavik to Washington DC (8 May) (WOW Air, February). State-owned B&H Airlines (Bosnia and Herzegovina) will reportedly have to suspend operations due to financial difficulties. The airline is currently operating on a reduced schedule with one ATR72-200 aircraft (ch-aviation, 20 February). Montenegro government is again reportedly planning to privatize loss-making Montenegro Airlines after two failed attempts in the past. Etihad Airways which had previously expressed interest in Montenegro Airlines is again considering acquiring a stake in the airline. In the meantime, Montenegro Airlines and Etihad plan to sign a strategic partnership, including a codeshare agreement in June this year (ch-aviation, 26 February).

SAS has received approval from the Danish Competition and Consumer Authority to complete the acquisition of Cimber on 1 March. SAS will transfer the operation of its 12 Bombardier CRJ900 aircraft to Cimber, the latter’s fleet of ATR72 aircraft will be phased out (SAS, 2 February).

SAS has sold two slot pairs at Heathrow in February. The first slot pair will be transferred on 29 March whereas the second slot pair sold to Turkish Airlines will be taken over from 25 October. Following the transactions, SAS will be left with 19 daily slot pairs at Heathrow. The airline will also consider the user of other airports in the London region (SAS, 4 & 27 February).

Percentage of flights delayed on departure

Breakdown of all-causes delay per flight

Figure 2: Delay statistics (all-causes, airline-reported delay – preliminary data for January 2015).

Industry Monitor. Issue 170. 02/03/2015 Page 4 © EUROCONTROL 2015

Swiss European Air Lines, a subsidiary of Swiss International Air Lines (SWISS) has been renamed Swiss Global Air Lines in view of the delivery of the first of its new fleet of six B777-300ER aircraft in the course of 2015 (SWISS, 3 February).

Belgian start-up Take Air will start operations at the end of March with flights between Antwerp and Zurich and will also launch a London – Paris service in the future. Take Air is the first all-you-can-fly airline in Europe based on a concept offering unlimited flights for a fixed monthly fee (Take Air, February). Luxair plans to renew its fleet in two phases and completed the first step with an order for four Bombardier Q400 aircraft to replace its current Embraer ERJ-145 aircraft, with an option on two additional Q400 aircraft. Delivery is scheduled for 2016. The second phase will be the purchase of new generation jet aircraft to be introduced between 2018 and 2020 (Luxair, 6 February). Austrian Start-up Air Kärnten will start a scheduled service from Klagenfurt to London Southend, effective May. The new airline will also operate charter services on behalf of tour operator Gruber Reisen Kärnten from Klagenfurt to Girona, Lisbon, Naples, Rhodes, Mallorca and from Graz to Preveza and Kos (Air Kärnten and ch-aviation, February). Lufthansa Group, Eurowings will set up its first base outside of Germany in Vienna with two A320-200 aircraft staffed with crews from Austrian Airlines. Lufthansa plans to transform Eurowings to a low-cost short- and long-haul airline by the end of 2015 (Lufthansa, 18 February). Low-cost Transavia has placed an order for 20 B737-800 aircraft (17 firm orders and three options) to support the growth of Transavia France and the development of Transavia Netherlands. Deliveries will take place between 2016 and 2018 (Air France-KLM, 12 February). Turkish Airlines is reportedly planning to lease two A380-800 aircraft from Malaysia Airlines for use on its Istanbul-China routes (Bloomberg, 17 February).

Figure 3: Main carriers’ traffic statistics.

Industry Monitor. Issue 170. 02/03/2015 Page 5 © EUROCONTROL 2015

Routes, Alliances, Codeshares

Air Europa is launching inter-islands flights in the Balearics from Palma to Ibiza and to Menorca, effective 1 May (Air Europa, February). All-business-class La Compagnie which started operations last July on the Paris Charles De Gaulle – Newark route will expand operations in April with London Luton – Newark flights (La Compagnie, 3 February).

Vueling will expand its offer from Barcelona to Africa with new routes to Rabat, Djerba and Accra, effective 20 June. The airline further plans a seasonal route Barcelona - Istanbul (Vueling, 22 January).

Vueling will set up a new base in Santiago de Compostela and operate one A320-200 aircraft to new domestic flights to Palma, Menorca, Ibiza, Tenerife Sur and Fuerteventura in June (ch-aviation, 4 February). Czech Airlines postponed the launch of new routes to Russia following the significant drop in demand to travel from Russia to the Czech Republic and Europe. The airline has used the freed capacity by adding up to 19 new destinations to its network in its summer 2015 schedule. New routes include flights from Prague to Liverpool, Cork, Oslo, Billund, Stavanger, Kristiansand, Växjö, Linköping, Bologna, Venice, Porto, Poznan, Gdansk, Athens, Bordeaux. Czech Airlines will also launch direct flights from Stuttgart to Prague, Bologna and Marseille via Geneva using its fleet of ATR42-500 aircraft (Czech Airlines, 13 February). Start-up Skygreece airlines plans transatlantic flights to Toronto and Montreal from Athens and to Toronto from Thessaloniki operating a B767-300ER aircraft, effective May. The carrier will also launch a seasonal service from Zagreb to Toronto and from Budapest to Toronto (routesonline, 13 February).

Figure 4: Main carriers’ load factors.

Industry Monitor. Issue 170. 02/03/2015 Page 6 © EUROCONTROL 2015

Belgian VLM airlines will launch in April scheduled flights between Rotterdam-Hamburg and Antwerp-Hamburg with its fleet of Fokker 50 aircraft. The airlines started an Antwerp-Geneva service last month and plans to further launch routes from Liège to Avignon, Nice Bologna and Venice (VLM Airlines, February). Aegean Airlines will be operating up to 50 new routes during the summer from its bases in Athens, Heraklion, Rhodes, Corfu and Larnaca (Aegean Airlines & anna.aero, 17 February).

Failures

Polish state-owned EuroLOT will cease operations on 31 March and go into liquidation. It is reported that part of the airline’s fleet of 11 Bombardier Q400 aircraft will be transferred to LOT Polish Airlines (EuroLOT & ch-aviation, February). The Italian Civil Aviation Authority (ENAC) revoked MiniLiner’s Air Operator’s Certificate on 31 January. The airline operated cargo services with a fleet of eight Fokker aircraft (ENAC, 30 January).

Traffic statistics: January update

Figure 3 and Figure 4 compare January 2015 figures with January 2014 figures. In addition to the number of passengers (PAX), passenger capacity is measured in available seat kilometres (ASK) and traffic is measured in revenue passenger kilometres (RPK).

Figure 5: Financial results of airlines.

Industry Monitor. Issue 170. 02/03/2015 Page 7 © EUROCONTROL 2015

Financial results of airlines Some of the main airlines have posted their financial results for 2014 (Figure 5). Lufthansa Group, airberlin and Alitalia results were not available at the time of publication of this bulletin. Air France-KLM reported a drop in full year profits mainly due to last year’s pilots’ strike which had a negative impact of €425 million on the Group’s operating results but also the weaker euro. IAG Group reported strong results, up 81% on 2013. Iberia made an operating profit of €50 million (vs. a loss of €166 million in 2013). British Airways operating profit increased to €1,215 million from €762 million last year. The negative result of Norwegian, the first in eight years, was mainly caused by fuel hedging, a weak Norwegian krone and the delayed foreign air carrier permit for its subsidiary to fly in the US (source: Company reports, February).

Airports Aéroports de Paris (ADP) reported 2014 EBITDA up 3.4% compared with 2013. The forecast for 2015 is for a 2.6% growth in traffic (ADP, 19 February). Heathrow reported 2014 adjusted EBITDA up 10.3% compared with 2013 (Heathrow, 23 February). Schiphol Group reported EBITDA up 11.3% on 2013 (Schiphol Group, 19 February).

Passenger traffic and aircraft movements in January 2015 at the top five European airports in numbers of departures compared with the same period a year ago were as follows (Growth on January 2014): Passenger traffic Aircraft movements 1 London Heathrow 5.5 million (+1.3%) 37.1K (-0.8%) 2 Paris CDG 4.7 million (+2.5%) 35.7K (-0.9%) 3 Istanbul Atatürk 4.5 million (+8.6%) 34.5K (+6.8%) 4 Frankfurt 4.1 million (+1.3%) 34.6K (-2.6%) 5 Amsterdam Schiphol 3.7 million (+2.9%) 32.0K (+2.0%)

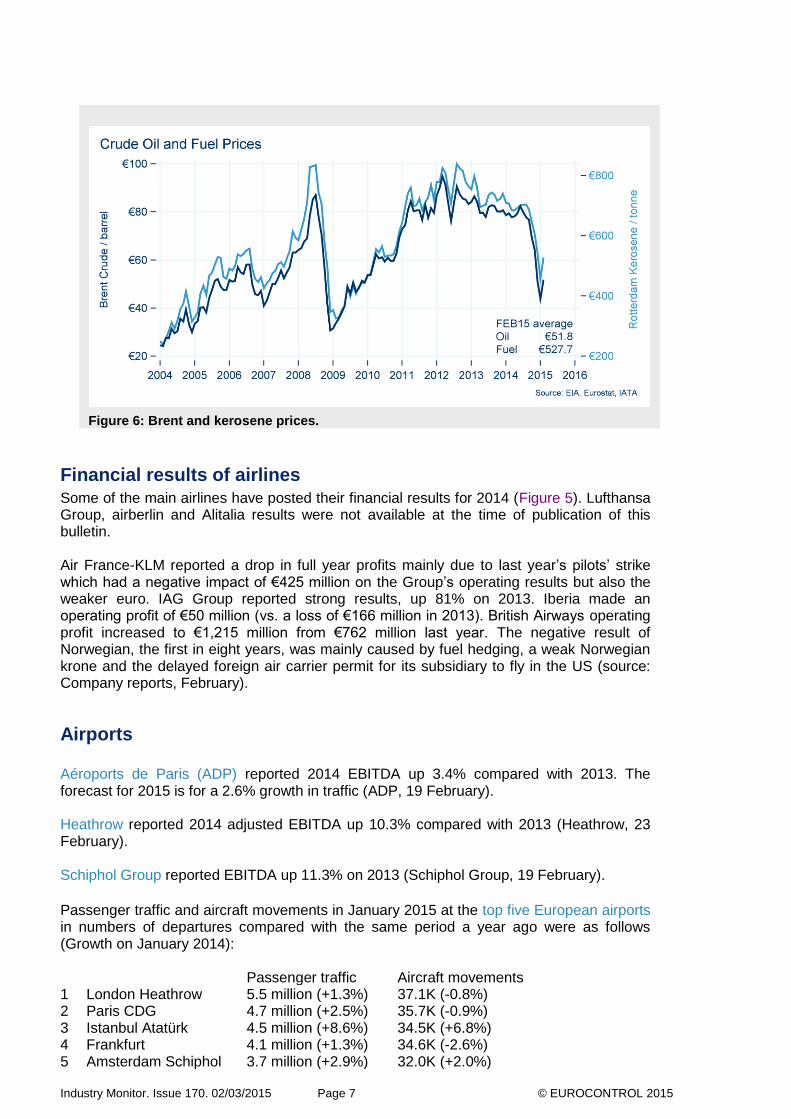

Figure 6: Brent and kerosene prices.

Industry Monitor. Issue 170. 02/03/2015 Page 8 © EUROCONTROL 2015

Plans to expand London City Airport have been approved. The airport will be able to operate up to 111,000 flights a year from the current 70,000 flights and handle 6 million passengers a year by 2023 (vs. 3.7 million in 2014). The plans include an extended terminal, a new taxi way and seven new aircraft stands to accommodate larger aircraft. These aircraft have longer ranges and will open up new destinations not currently served from London City (London City Airport, 4 February).

Oil

Oil prices rose from an average of €44 per barrel in January towards €52 per barrel in February 2015. Converted indices for Kerosene and Brent are shown in Figure 6.

Economy Eurostat estimated that GDP increased by 0.3% in the euro area and by 0.4% in the EU28 during 4Q14 (vs. 4Q13). For 2014 as a whole, GDP was up 0.9% in the euro area and 1.4% in the EU28. In its Economic Forecast, Winter 2015, EC expects GDP to grow in all EU28 states, the first time since 2008. Growth in 2015 is forecast to increase by 1.7% for the EU28 and by 1.3% for the euro area. In 2016 GDP will accelerate to rise to 2.1% for the EU28 and to 1.9% for the euro area (Eurostat, 5 & 13 February).

Fares

Deflated ticket prices in Europe increased by 1.6% in January year-on-year, based on preliminary values. This is above the trend (12-month trailing average) shown in Figure 7 (Eurostat, 24 February).

Figure 7: Deflated ticket prices in Europe.

Industry Monitor. Issue 170. 02/03/2015 Page 9 © EUROCONTROL 2015

© 2015 European Organisation for the Safety of Air Navigation (EUROCONTROL) This document is published by EUROCONTROL for information purposes. It may be copied in whole or in part, provided that EUROCONTROL is mentioned as the source and it is not used for commercial purposes (i.e. for financial gain). The information in this document may not be modified without prior written permission from EUROCONTROL. STATFOR, the EUROCONTROL Statistics and Forecast Service [email protected] www.eurocontrol.int/statfor