Industry and M&A Update - Sheshunoff Consulting and M&A Update. CEO Affiliation. Fall 2010....

47

Industry and M&A Update CEO Affiliation Fall 2010 Sheshunoff & Co Investment Banking Curtis Carpenter Sheshunoff &Co. Investment Banking

Transcript of Industry and M&A Update - Sheshunoff Consulting and M&A Update. CEO Affiliation. Fall 2010....

Industry and M&A Update

CEO AffiliationFall 2010

Sheshunoff & Co Investment Banking

Curtis CarpenterSheshunoff &Co. Investment Banking

I. The Industry Landscape Today

II. Merger Activity and What it Means

IV. What is Next?

Session Outline

I.The Industry Landscape Today

Asset Distribution

June 30, 2010 Data Consolidated by HCExcludes any bank larger than $1 billion in assets with a deposits to assets ratio of less than 10%

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

JPMorgan Chase & Co.

$2.01 Trillion

Bank of America$2.36 Trillion

Citigroup$1.94 Trillion

$7.5 Trillion (54%)

Top 4 Banks

Asset Size

$100MM - $1B

$0 - $100MM

430 Institutions -$1.11 Trillion

3,391 Institutions $1.00 Trillion

2,322 Institutions $130 Billion

$2.2 Trillion (16%)

$1B - $10B

67 Institutions -$4.2 Trillion

Banks > $10B

$ 4.2 Trillion (30%)

$ Tr

illio

ns

Wells Fargo$1.23 Trillion

Total Industry Assets = $14.0 Trillion

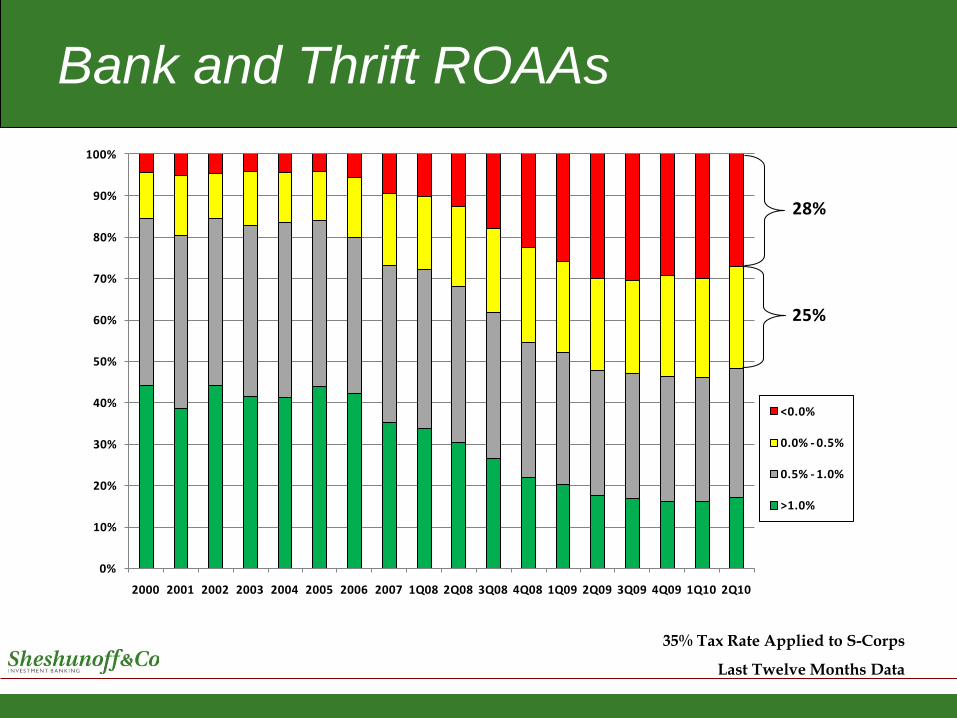

Bank and Thrift ROAAs

35% Tax Rate Applied to S-Corps

Last Twelve Months Data

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

<0.0%

0.0% - 0.5%

0.5% - 1.0%

>1.0%

28%

25%

> $10 Billion$1 Billion - $10 Billion

$500 Million - $1 Billion

$100 Million - $500 Million

< $100 Million

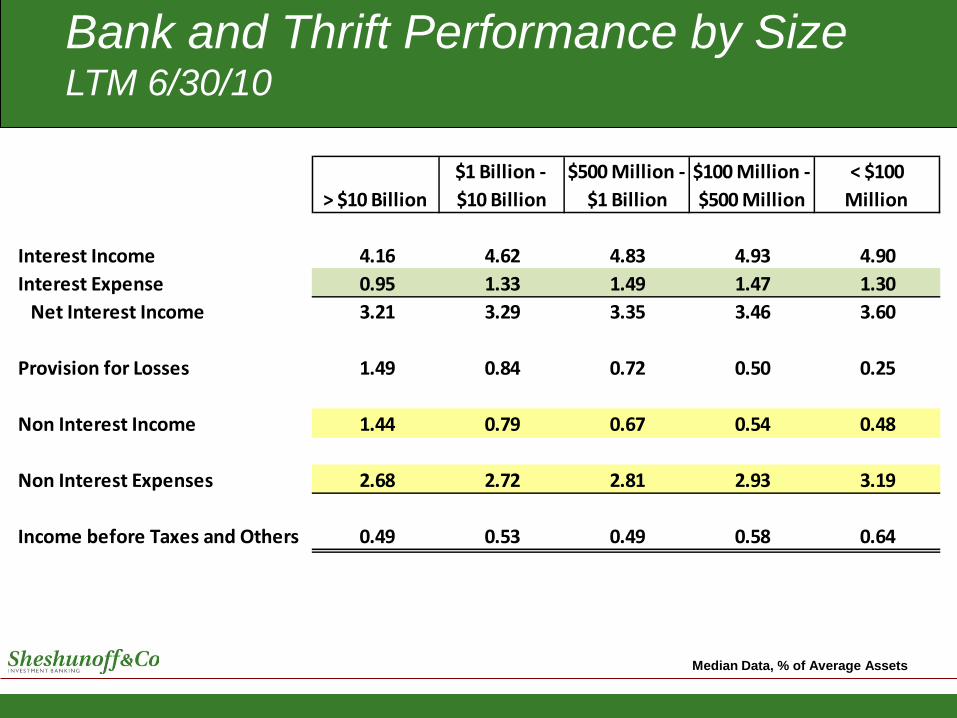

Interest Income 4.16 4.62 4.83 4.93 4.90 Interest Expense 0.95 1.33 1.49 1.47 1.30 Net Interest Income 3.21 3.29 3.35 3.46 3.60

Provision for Losses 1.49 0.84 0.72 0.50 0.25

Non Interest Income 1.44 0.79 0.67 0.54 0.48

Non Interest Expenses 2.68 2.72 2.81 2.93 3.19

Income before Taxes and Others 0.49 0.53 0.49 0.58 0.64

Bank and Thrift Performance by Size LTM 6/30/10

Median Data, % of Average Assets

Cost of Deposits by Quarter

0.50

1.00

1.50

2.00

2.50

3.00

3.50

> $10B $1B - $10B $500MM - $1B $100MM -$500MM

$0 - $100MM

Cost of Interest Bearing Deposits by Size

2008Q3 2008Q4 2009Q1 2009Q2 2009Q3 2009Q4 2010Q1 2010Q2

> $10 Billion$1 Billion - $10 Billion

$500 Million - $1 Billion

$100 Million - $500 Million

< $100 Million

Non Interest Income 1.44 0.79 0.67 0.54 0.48 Non Interest Expenses 2.68 2.72 2.81 2.93 3.19

Net Noninterest Expense 1.24 1.92 2.14 2.38 2.71

Net Noninterest Expense by SizeLTM 6/30/10

Median Data, % of Average Assets

0.00

0.50

1.00

1.50

2.00

2.50

3.00

> $10 Billion $1 Billion -$10 Billion

$500 Million - $1

Billion

$100 Million -

$500 Million

< $100 Million

Net Noninterest Expense by SizeLTM 6/30/10

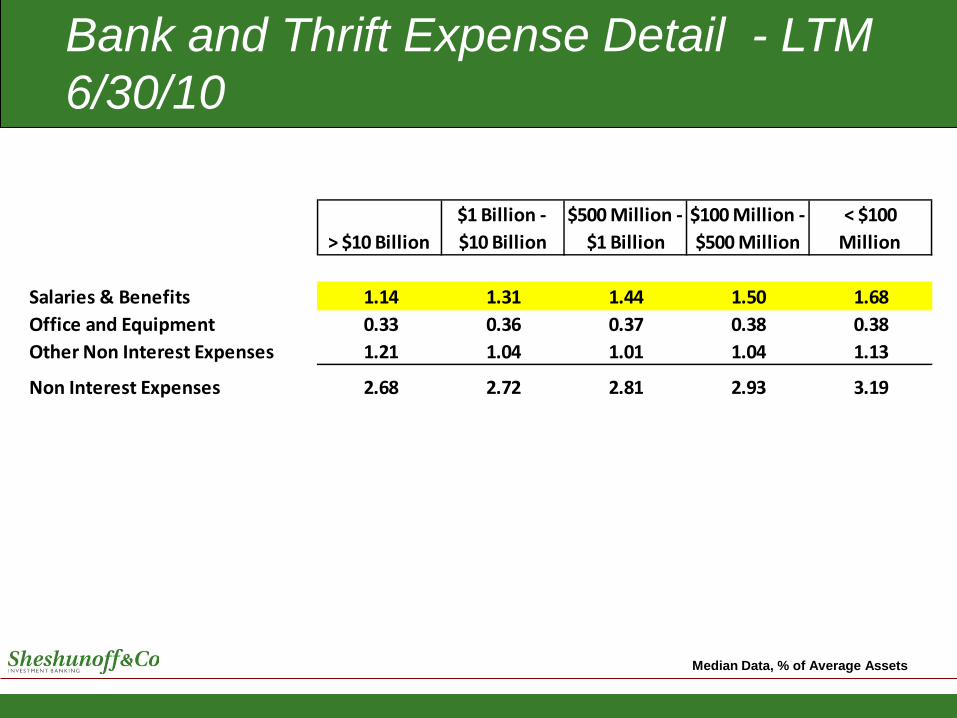

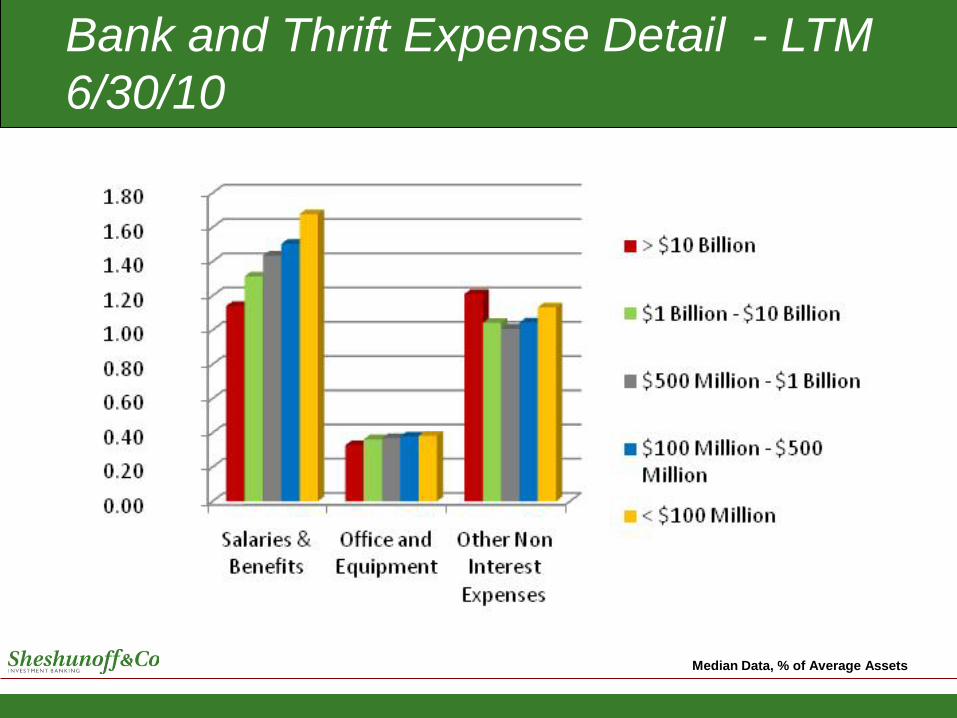

Bank and Thrift Expense Detail - LTM 6/30/10

Median Data, % of Average Assets

> $10 Billion$1 Billion - $10 Billion

$500 Million - $1 Billion

$100 Million - $500 Million

< $100 Million

Salaries & Benefits 1.14 1.31 1.44 1.50 1.68 Office and Equipment 0.33 0.36 0.37 0.38 0.38 Other Non Interest Expenses 1.21 1.04 1.01 1.04 1.13

Non Interest Expenses 2.68 2.72 2.81 2.93 3.19

Bank and Thrift Expense Detail - LTM 6/30/10

Median Data, % of Average Assets

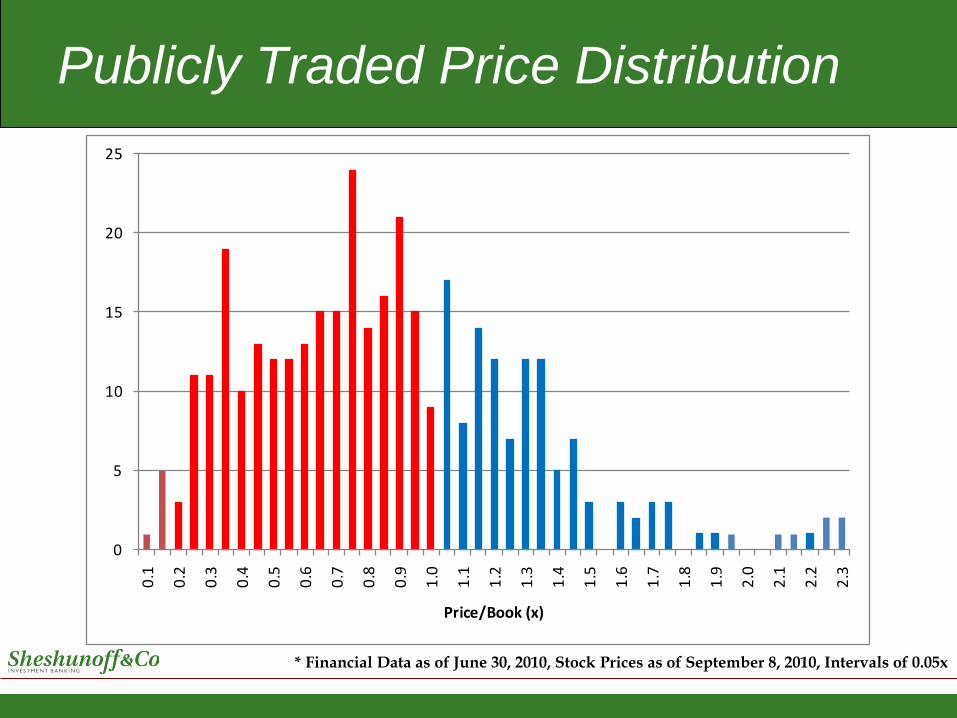

Publicly Traded Price Distribution

* Financial Data as of June 30, 2010, Stock Prices as of September 8, 2010, Intervals of 0.05x

0

5

10

15

20

250.

1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

Price/Book (x)

Publicly Traded Banks and Thrifts>2B and < $100B in Assets

Price to Tangible Book as of September 9, 2010

11

101

39

140

20

40

60

80

100

120

> 2.0x >1.0x < 2.0x >0.5x < 1.0x < 0.5x

Comparison of Median ROA, NPA’s and Dividend Yield

Price to Tangible Book

Publicly Traded Banks and Thrifts>2B and < $100B in Assets

As of September 9, 2010

1.34%0.59%

-0.48%

-2.23%

0.93%

1.87%

3.72%

9.72%

3.50%

2.52%

0.39%0.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

> 2.0x >1.0x < 2.0x >0.5x < 1.0x < 0.5x

ROAANPA'sDividend

Publicly Traded Banks and ThriftsPrice-to-Tangible Book > 2.0x

As of September 9, 2010

Bank and Thrift NPAs / Assets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

> 4.0%

2.0% - 4.0%

1.0% - 2.0%

0.5% - 1.0%

< 0.5%

Non-Performing Assets / AssetsNumber of Banks and Thrifts

1,755

700840

1,767

753

1,034

1,763

794

1,123

1,809

790

1,183

1,767

868

1,169

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2% - 4% 4% - 6% > 6%

2009Q2 2009Q3 2009Q4 2010Q1 2010Q2

Texas Ratio Definition

Texas Ratio = Loans 90+ Days Past Due + Non Accrual Loans + OREO

Tangible Equity + Loan Loss Reserves

Texas Ratio – Quarterly Trend

0

100

200

300

400

500

600

700

50% - 75% 75% - 100% 100% - 150% 150% - 200% >200%

Texas Ratio Breakdown by Number of Institutions

2009Q1 2009Q2 2009Q3 2009Q4 2010Q1 2010Q2

Institutions With Texas Ratio Above 200%

11

June 30, 2010 Data

114

63

1

19

43

113

2

2

1

2

33

33

13

1

1

1

1

11

1 1

5

1

Institutions With Texas Ratio 100%-200%States with more than three institutions

3

June 30, 2010 Data

8

633

1211

40

36

436

3

7

10

26

15

6

8

3

8

4

3

5

78

10

6 6

16

9

Number of Institutions with Texas Ratio > 100%Metro Areas With Five or More

June 30, 2010 Data

Denovo = Established since 1/1/2000

Metro Area Total Banks DenovosChicago, IL 50 9Atlanta, GA 42 20Minneapolis-St. Paul, MN 22 6Seattle-Tacoma, WA 17 4Miami, FL 15 5Kansas City, MO-KS 11 3Dallas-Fort Worth, TX 9 1New York, NY 9 3Tampa-St.Petersburg, FL 8 3Philadelphia, PA 8 3Saint Louis, MO 8 4Detroit, MI 7 0Las Vegas, NV 6 6Phoenix, AZ 6 3Jacksonville, FL 6 1Washington, DC 6 1

2009 and 2010 Bank Failures

*As of July 28, 2010

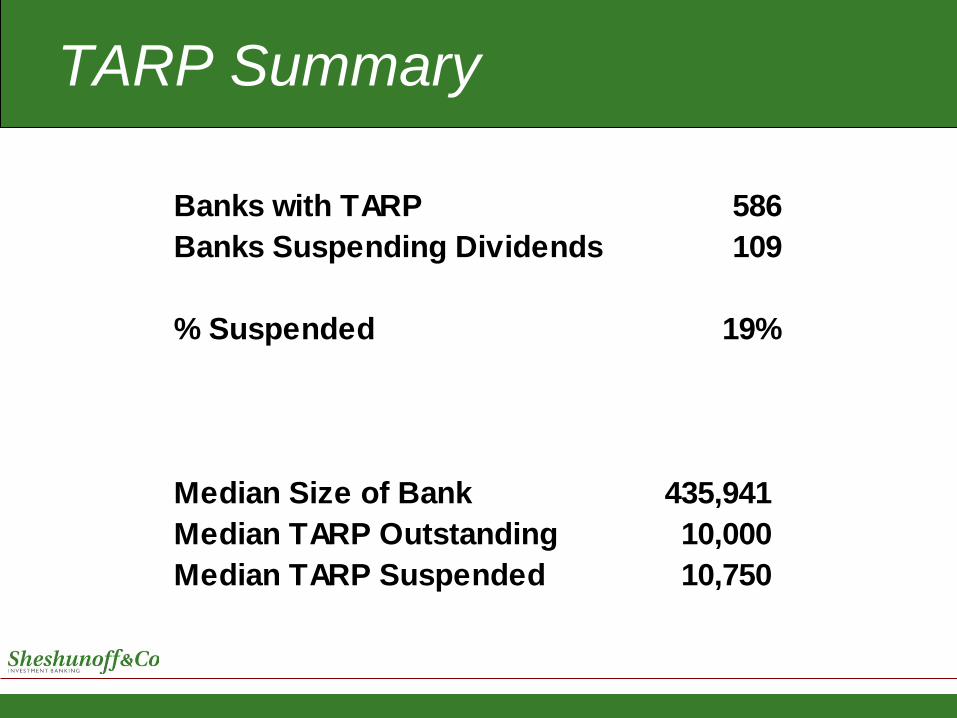

TARP Summary

Banks with TARP 586Banks Suspending Dividends 109

% Suspended 19%

Median Size of Bank 435,941 Median TARP Outstanding 10,000 Median TARP Suspended 10,750

III.Merger Activity and What it Means

Recapitalizations in 2010 (Change of control between 50% and 85%)

11

2010 Recapitalizations

Recapitalizations – Common Terms

• New money establishes its own terms

• Often results in a change-in-control

• Very dilutive to existing shareholders

• Typically from existing shareholder base

• Frequently in form of convertible debt or preferred

• Preserving existing NOL’s can be tricky

• Even though dilutive – often the best alternative

38 37

24 24

34

22

34

22

40

32

53

28

0

10

20

30

40

50

60

2Q 3Q 4Q 1Q 2Q 3Q*

Bank & Thrift Transaction Volume Analysis

2008 201020092010200920102009200920082009200820092008

*As of September 1, 2010

National Bank Acquisition PricingDeal Volume & Price / Book

34 22 40 32 53 28

1.16

0.90

1.10

1.00

1.261.23

0

10

20

30

40

50

60

70

80

2Q09 3Q09 4Q09 1Q10 2Q10 3Q10*0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Deal Volume Price/Book (x)

*As of September 1, 2010

2010 Deal Activity Map

*As of September 1, 2010

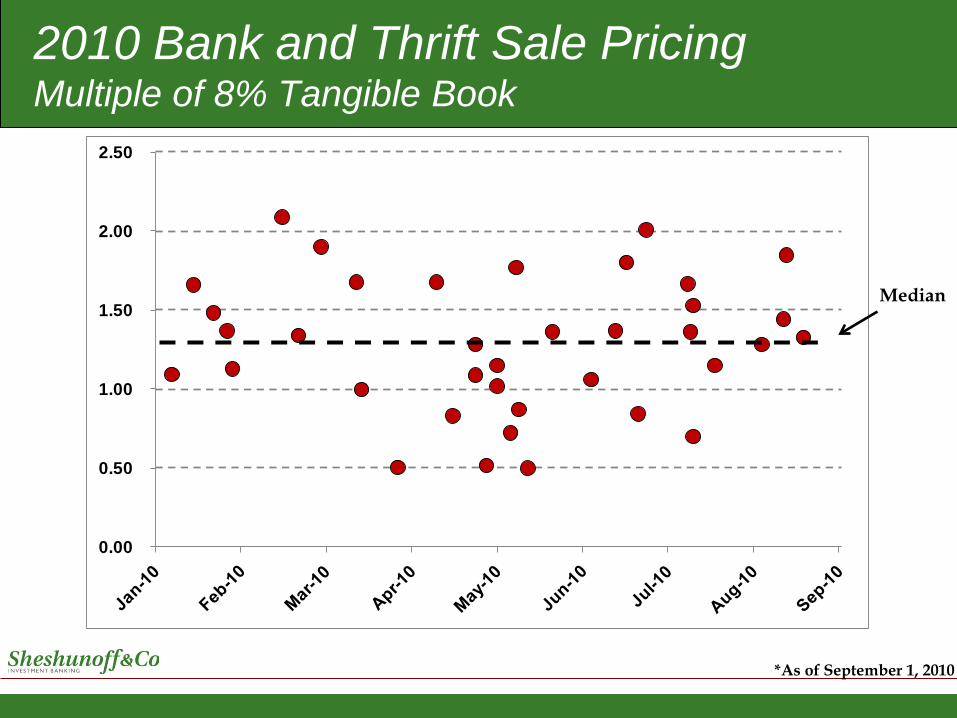

0.00

0.50

1.00

1.50

2.00

2.50

2010 Bank and Thrift Sale PricingMultiple of 8% Tangible Book

Median

*As of September 1, 2010

Buyer Seller

Total Assets 905,609 153,957

T. Equity to T. Assets 9.70 8.48

NPA's/Total Assets 1.58 2.79

2010 Median Characteristics of Buyers and Sellers (excludes charter acquisitions)

Through August 25, 2010

Common Deal Terms in Acquisitions

• Pricing based upon “adjusted” book value

• Cash is most common

• Seeing some non-liquid stock

• Escrows, carve-outs, and/or write downs are common

• Carve-outs provide upside to sellers and entice buyers

• Some survival of representations and warranties

• Buyer’s ability to close is major consideration

51,33327,164

3.40

4.48

0

10,000

20,000

30,000

40,000

50,000

60,000

2009 2010*0.0

1.0

2.0

3.0

4.0

5.0

Deposits Transferred ($000) Franchise Premium/ Deposits (%)

Recent Branch Sale Summary

*As of July 28, 2010**Not all Deals Reported Franchise Premiums

Historical Premiums to Deposits

8.0%

5.8% 5.6%

6.7%

6.0%

7.3%7.0%

4.6%5.0%

3.4%

4.5%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Median Deposit Premiums

*As of July 28, 2010

Historical Branch Transaction Volume

2007 2008 2008 2008 2008 2009 2009200820092009118 150 165 132 234 236 187 246 179 167 140 211 150 126 112 86 106 72 64 82

697

269194

157

240190

300

185

525408

441

554

875

463316

776 757

832

1020948

0

50

100

150

200

250

300

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

200

400

600

800

1000

1200

Number of Branch Sales Number of Branches Sold

III.What is Next?

New regulations surrounding home mortgages are too complex for small banks

Declining interchange fee income with few choices to replace it (i.e. limited menu of fee-based products)

Standardization of banking products favors the larger, low-cost distributors

Higher capital requirements favor larger banks who have more access to capital

Increased regulatory burden favors larger banks who can spread the cost over more assets

Challenges Facing Smaller Banks

Pressure on Deal Prices

Publicly-traded banks have depressed currency

Regulatory pressure on capital ratios

Number of problem banks creates expectations of bargains among directors

Lower earnings and growth projections translate into lower enterprise value

Weak economic growth and pervasive asset quality challenges produce a downward pull on pricing

Expecting More Deal Volume

Perception of having tapped the bottom

Regulatory reform is intensifying the need and/or desire for size

Hundreds of banks have been waiting to sell for the past two years – now they may finally have the opportunity

Many bankers feel they will not earn more in future years

Exasperation threshold with the regulatory climate

Increasing number of serious buyers

or both?

Are you a buyer? a seller?

“Life is a shipwreck, but we must not forget to sing on the life boats.”

Voltaire

Opportunities abound…

Five deals in the past 4 months

Page 45

Questions?

Thank You!

Updated Slides are available at:

www.Sheshunoffib.com

Contact Information

Sheshunoff & Co. Investment BankingAustin, Texas

800-279-2241

Curtis CarpenterManaging Director

John AdamsDirector of Mergers and Acquisitions

www.Sheshunoffib.com

![Investment banking []](https://static.fdocuments.us/doc/165x107/55a493e51a28ab131b8b45a1/investment-banking-wwwlearnerareablogspotcom.jpg)