INDUSTRIAL GROWTH PROSPECTS 2010 TO 2015, … · INDUSTRIAL GROWTH PROSPECTS: 2010 TO 2015,...

156

A MACRO-ECONOMIC ASSESSMENT OF THE WESTERN CAPE ECONOMY’S SECTORAL AND INDUSTRIAL GROWTH PROSPECTS: 2010 TO 2015, INCLUDING AN ASSESSMENT OF INTER- INDUSTRY LINKAGES A research report prepared for the Department of Economic Development & Tourism (DEDT), Provincial Government of the Western Cape (PGWC) by P Laubscher 29 June 2011

Transcript of INDUSTRIAL GROWTH PROSPECTS 2010 TO 2015, … · INDUSTRIAL GROWTH PROSPECTS: 2010 TO 2015,...

A MACRO-ECONOMIC ASSESSMENT OF THE WESTERN CAPE ECONOMY’S SECTORAL AND

INDUSTRIAL GROWTH PROSPECTS: 2010 TO 2015, INCLUDING AN ASSESSMENT OF INTER-

INDUSTRY LINKAGES

A research report prepared for the Department of Economic Development & Tourism (DEDT), Provincial Government of the Western Cape (PGWC) by P Laubscher

29 June 2011

Table of Contents

Executive Summary .......................................................................................................................... i

A macro-economic assessment of the Western Cape economy’s sectoral and industrial growth prospects, 2010 to 2015, including an assessment of the inter-industry linkages ............................................................................................................................. 1

Introduction .................................................................................................................................................. 1

Objectives of the research ....................................................................................................................... 2

Methodology ................................................................................................................................................. 2

World economic outlook .......................................................................................................................... 5

Growth........................................................................................................................................................................... 5

Inflation & commodity prices .............................................................................................................................. 8

Currencies .................................................................................................................................................................... 9

South African economic outlook ........................................................................................................... 9

Growth........................................................................................................................................................................ 11

Inflation & interest rates .................................................................................................................................... 15

Balance of payments and the rand exchange rate.................................................................................... 15

Sectoral outlook for the Western Cape economy .......................................................................... 18

Growth & employment, 2000-9 ....................................................................................................................... 18

Employment elasticities ........................................................................................................................................... 25

Growth & employment outlook: 2010-15 ................................................................................................... 27

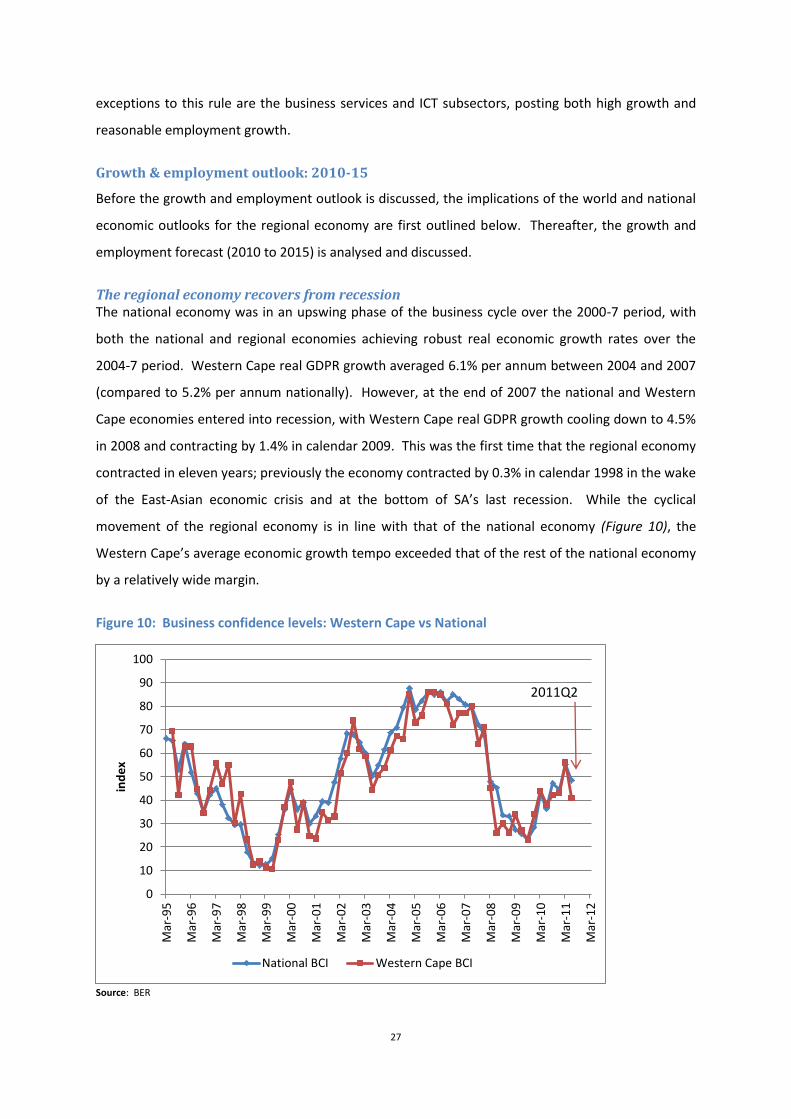

The regional economy recovers from recession ............................................................................................ 27

Macro-economic parameters................................................................................................................................. 29

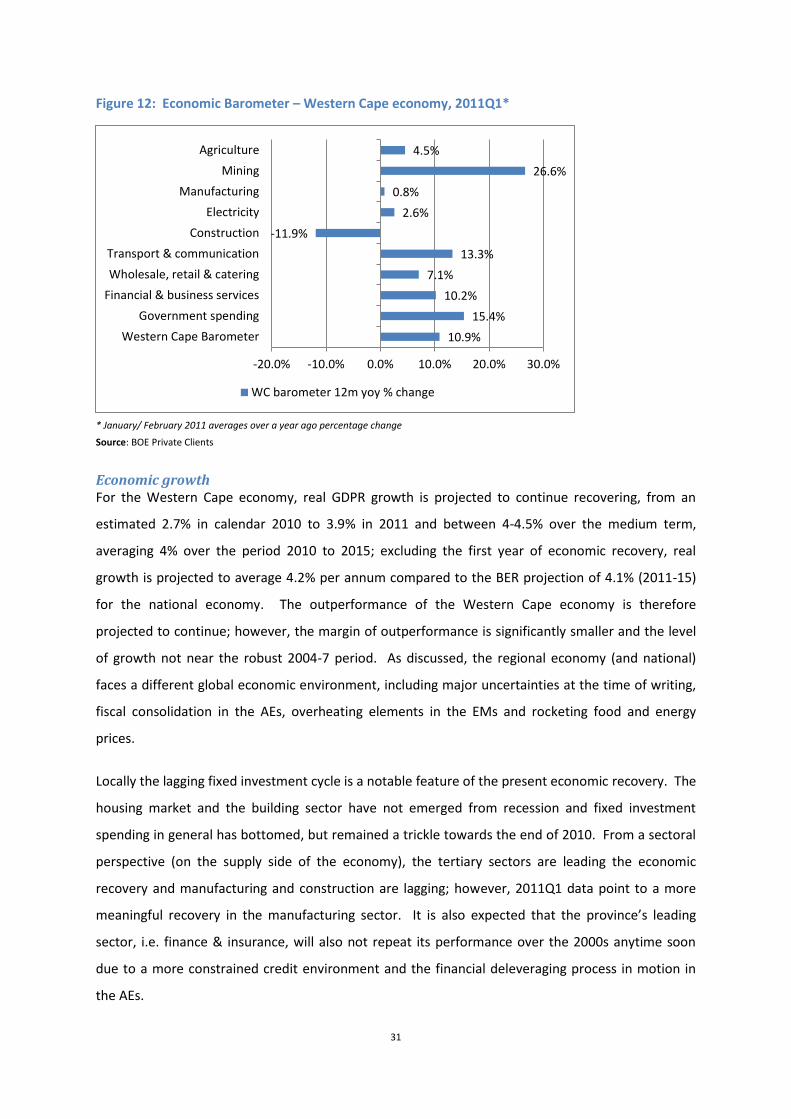

Economic growth ........................................................................................................................................................ 31

Employment ................................................................................................................................................................... 33

Exports ............................................................................................................................................................................. 36

Primary sector – overview ................................................................................................................................. 39

Agriculture ..................................................................................................................................................................... 40

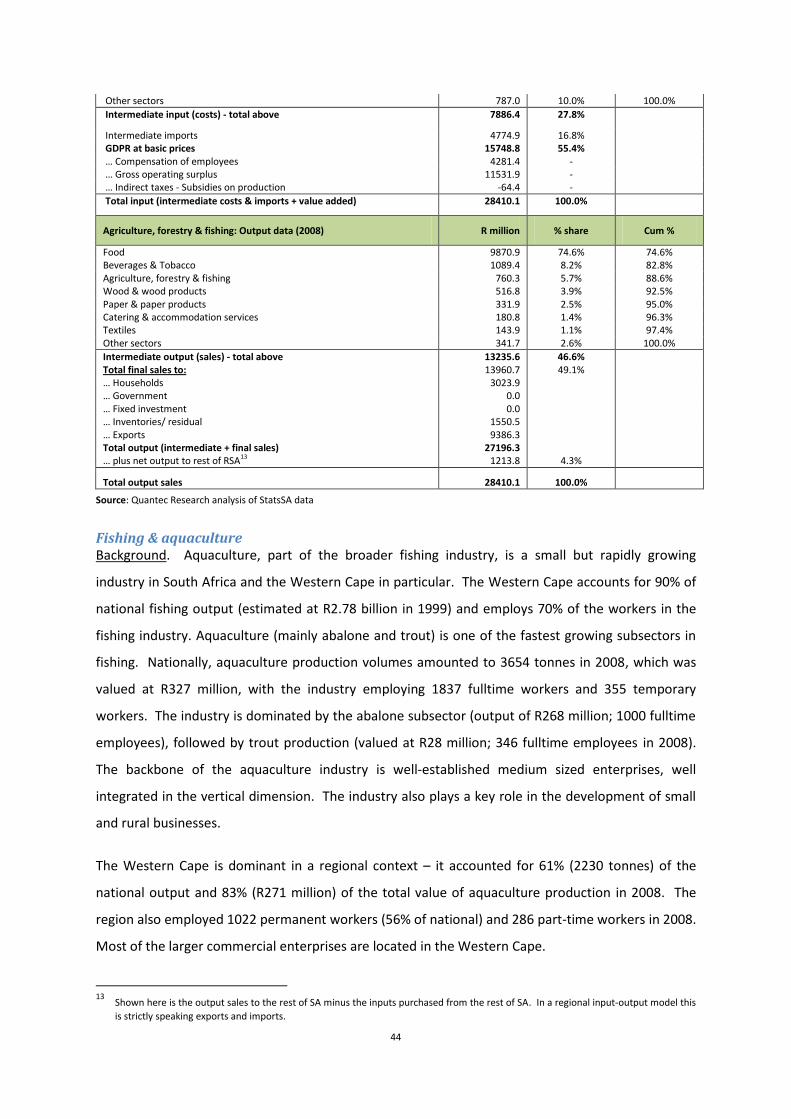

Fishing & aquaculture............................................................................................................................................... 44

Secondary sector – overview ............................................................................................................................ 47

Agriculture processing .............................................................................................................................................. 50

Clothing & textiles ....................................................................................................................................................... 55

Craft industries ............................................................................................................................................................. 59

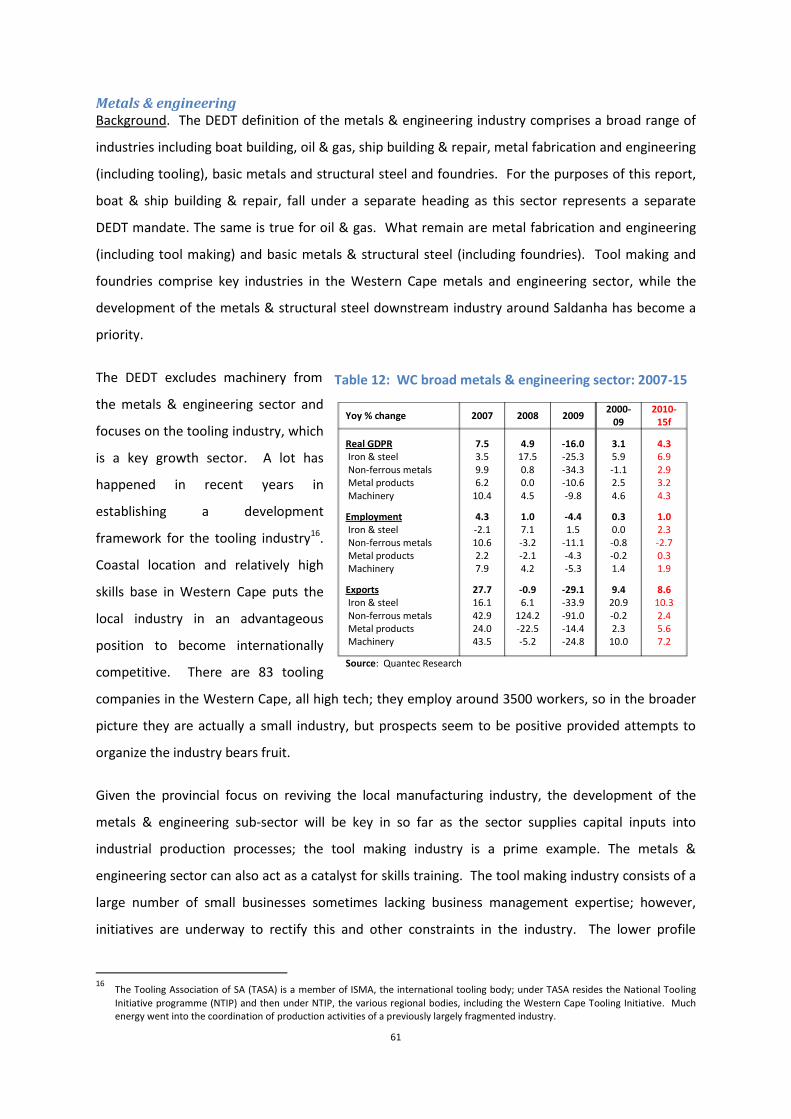

Metals & engineering................................................................................................................................................. 61

Oil & gas ........................................................................................................................................................................... 65

Electronics ...................................................................................................................................................................... 68

Boat building ................................................................................................................................................................. 71

Furniture ......................................................................................................................................................................... 74

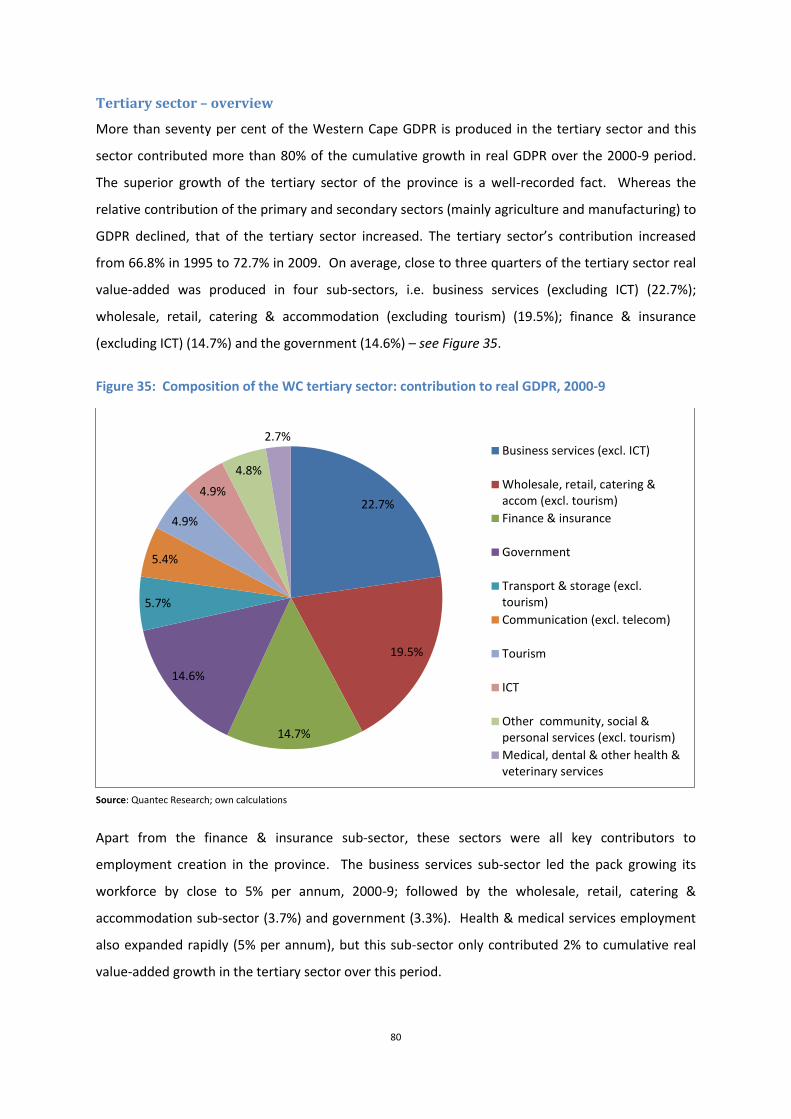

Tertiary sector – overview................................................................................................................................. 80

Tourism ............................................................................................................................................................................ 82

Finance & insurance .................................................................................................................................................. 88

ICT ...................................................................................................................................................................................... 91

Call centres/ BPO ........................................................................................................................................................ 94

An assessment of Western Cape inter-industry linkages ........................................................... 99

Backward and forward linkages ...................................................................................................................... 99

GDPR and employment multipliers.............................................................................................................. 103

Concluding remarks/ summary ........................................................................................................ 106

References ................................................................................................................................................ 114

Appendix 1: The BER macro-economic model ........................................................................... 117

Appendix 2: The Quantec RSA Inter-Industry model ............................................................... 117

Appendix 3: The Quantec Western Cape Input-Output model ............................................. 119

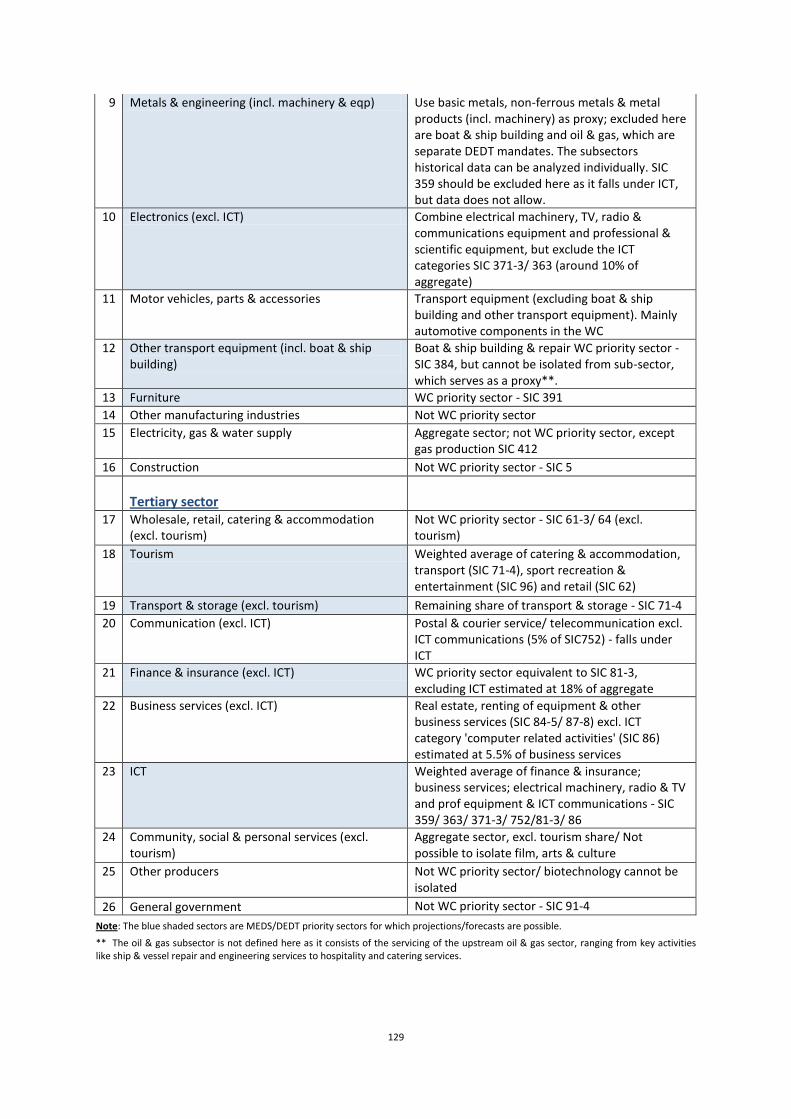

Appendix 4: Sector classification in the Western Cape model – 41 sectors ..................... 127

Appendix 5: Suggested classification for forecasts: SIC & DEDT sector definitions reconciled ................................................................................................................................................. 128

Appendix 6: Calculating weighted proxies .................................................................................. 130

Appendix 7: Western Cape sectoral forecast of real GDPR growth: 2005-2015 ............ 134

Appendix 8: Western Cape sectoral forecast of employment growth: 2005-2015 ....... 135

Appendix 9: Western Cape sectoral forecast of real export growth: 2005-2015 .......... 136

Appendix 10: Quantification of inter-industry linkages (backward and forward) ...... 137

List of Figures Figure 1: Real GDP growth ....................................................................................................................................... 12

Figure 2: Real domestic spending during economic upswings ................................................................. 13

Figure 3: Overall balance on the SA balance of payments vs the rand exchange rate ..................... 16

Figure 4: Tendencies on the SA balance of payments ................................................................................... 16

Figure 5: Contribution to Western Cape average annual real GDPR growth, 2000-9...................... 19

Figure 6: Western Cape: Real GDPR and employment growth: 2000-9 ................................................ 22

Figure 7: Western Cape real GDPR growth across sectors: 2000-9 ........................................................ 23

Figure 8: Western Cape employment growth across sectors, 2000-9.................................................... 24

Figure 9: Western Cape: Employment growth per unit of real value added growth: 2000-9 ...... 25

Figure 10: Business confidence levels: Western Cape vs National .......................................................... 27

Figure 11: The Western Cape economy recovers from recession ............................................................ 28

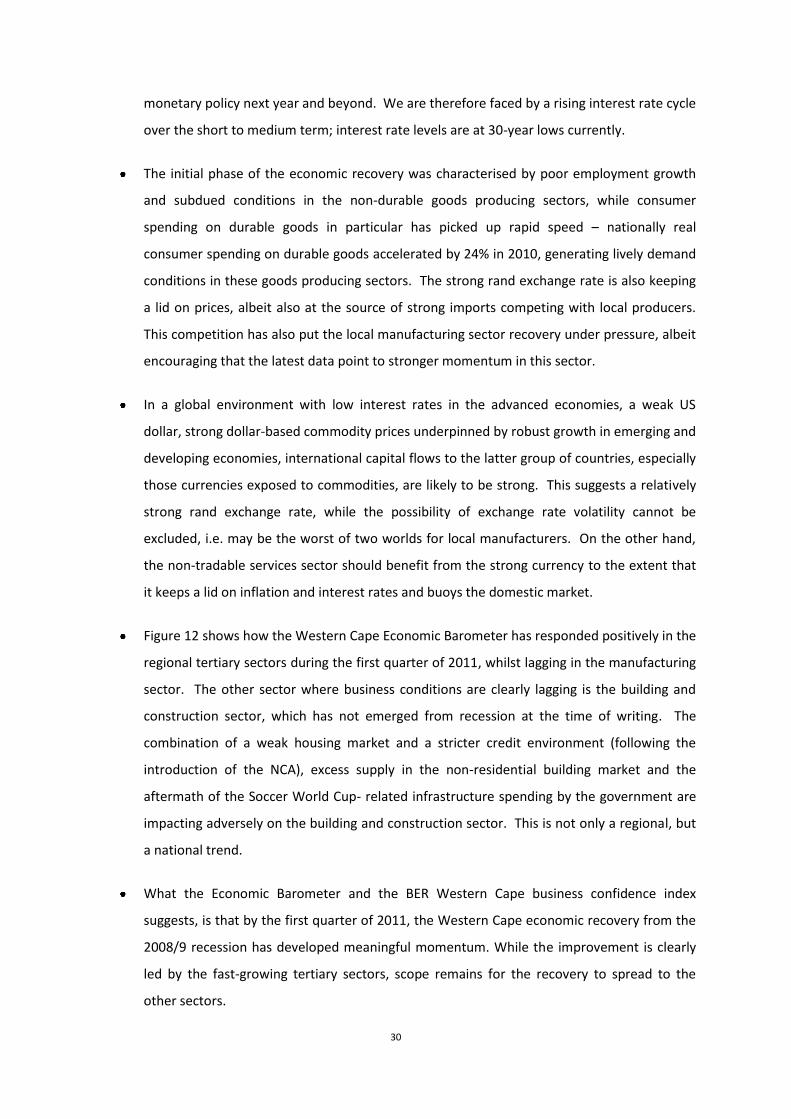

Figure 12: Economic Barometer – Western Cape economy, 2011Q1* ................................................... 31

Figure 13: Western Cape: Average annual real GDPR growth, 2010-2015 .......................................... 32

Figure 14: Western Cape: Average annual employment growth, 2010-2015 ..................................... 34

Figure 15: Western Cape real export growth, 1995 – 2015 ....................................................................... 36

Figure 16: Western Cape: Sectoral contribution to cumulative real export growth, 2000-9 ....... 37

Figure 17: Western Cape: Average real export growth, 2010-15 ............................................................ 38

Figure 18: Composition of the WC primary sector: contribution to real value-add, 2000-9 ........ 39

Figure 19: Western Cape: Primary sector real GDPR growth, 1995 – 2015 ........................................ 39

Figure 20: WC gross farming income (GFI) 2007 R16.6 billion ................................................................ 40

Figure 21: WC real GDPR growth 2005–2015: agri-culture, forestry & fishing ................................. 42

Figure 22: Market channels for aquaculture products ................................................................................. 45

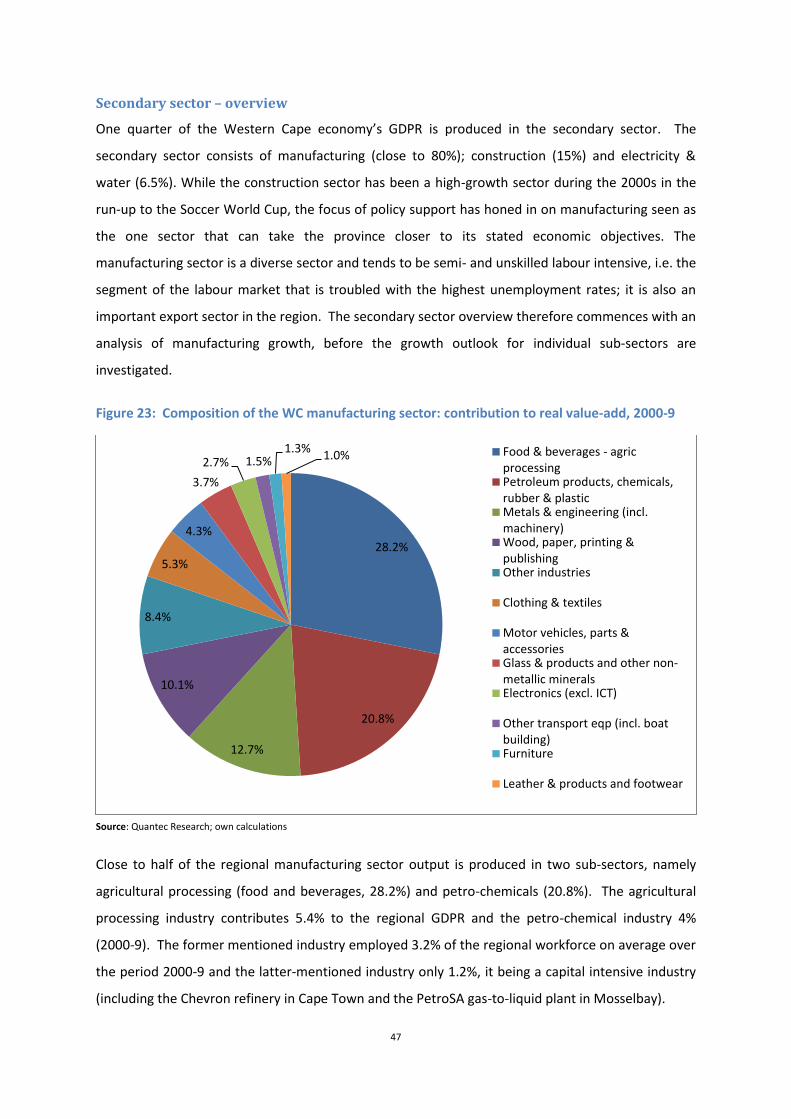

Figure 23: Composition of the WC manufacturing sector: contribution to real value-add, 2000-9

............................................................................................................................................................................................... 47

Figure 24: WC Manufacturing: Contribution to cumulative real GDPR growth, 2000-9 ................ 48

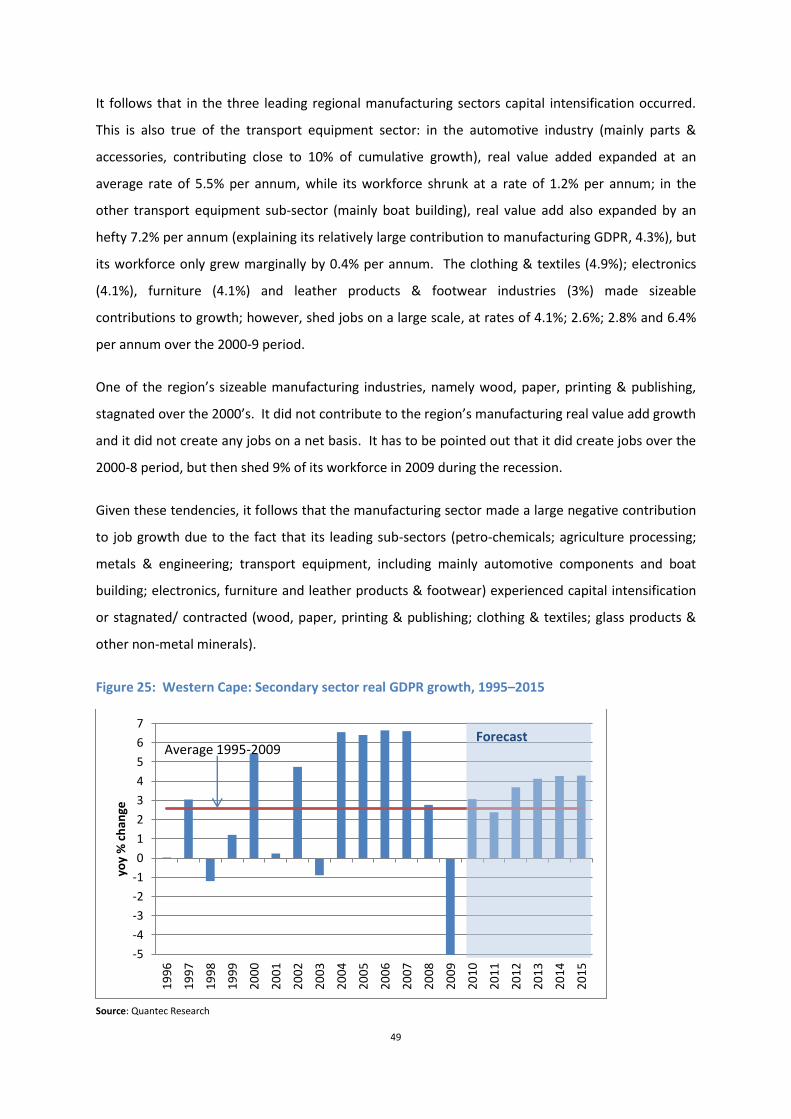

Figure 25: Western Cape: Secondary sector real GDPR growth, 1995–2015 ..................................... 49

Figure 26: WC real GDPR growth 2005–2015: Agriculture processing – food & beverages ........ 52

Figure 27: WC real GDPR growth 2005–15: Clothing & textiles ............................................................... 56

Figure 28: Business confidence (BER survey) .................................................................................................. 57

Figure 29: WC real GDPR growth 2005-2015: Metals & engineering..................................................... 62

Figure 30: Oil & gas industry: Business categories ........................................................................................ 67

Figure 31: WC real GDPR growth 2005-2015: Electronics industry (excl. ICT) ................................. 68

Figure 32: WC boat building support industry: distribution of firms .................................................... 71

Figure 33: WC real GDPR growth 2005-2015: Other transport equipment (incl. boat building) 72

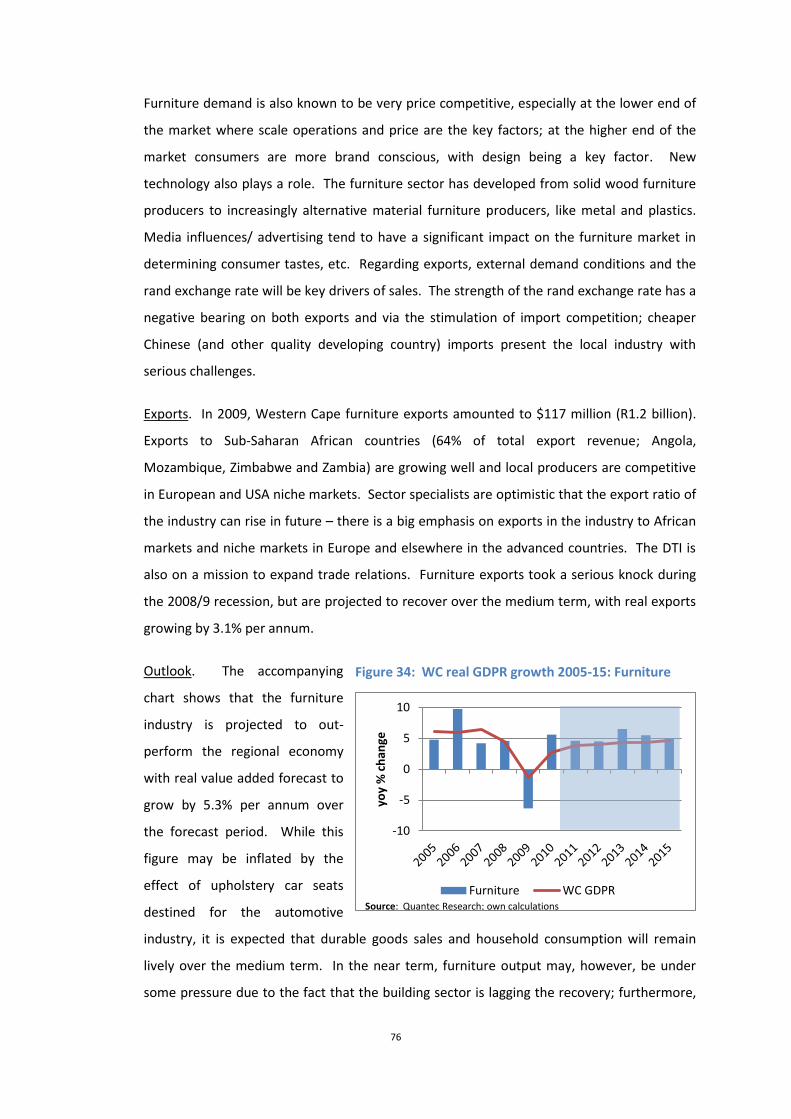

Figure 34: WC real GDPR growth 2005-15: Furniture .................................................................................. 76

Figure 35: Composition of the WC tertiary sector: contribution to real GDPR, 2000-9 ................. 80

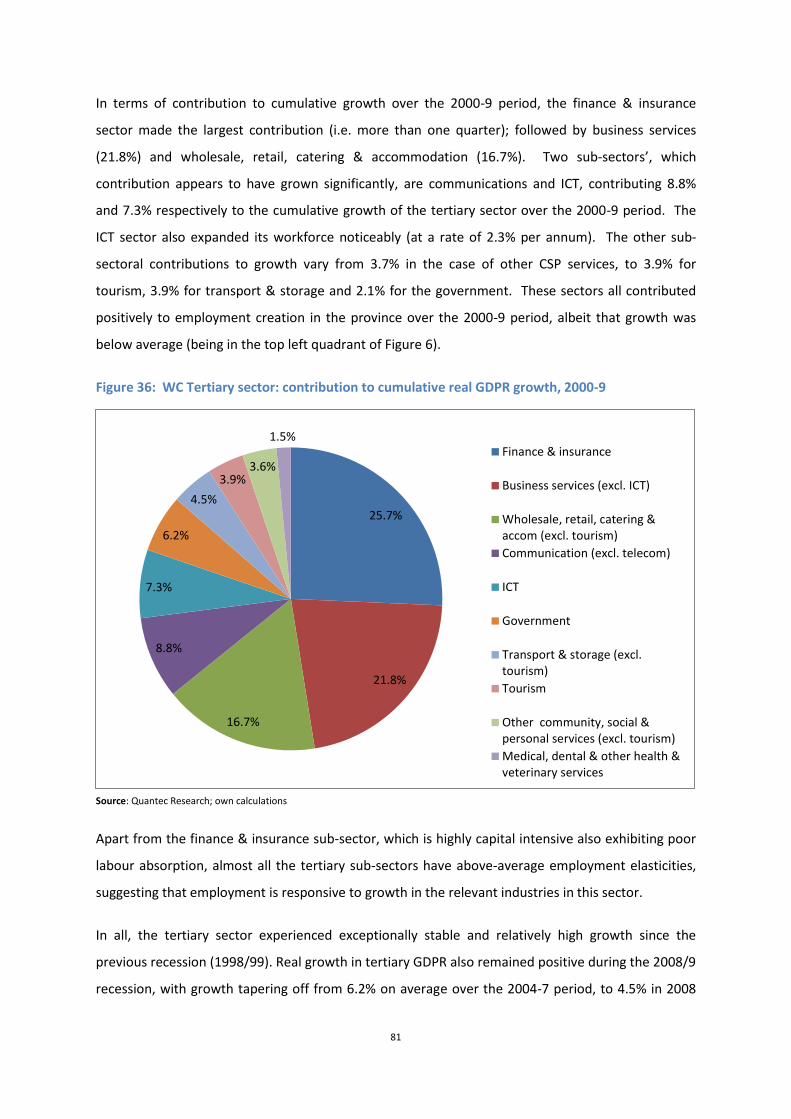

Figure 36: WC Tertiary sector: contribution to cumulative real GDPR growth, 2000-9 ................ 81

Figure 37: Western Cape: Tertiary sector real GDPR growth, 1995–2015 .......................................... 82

Figure 38: Number of international arrivals: 1991–2010: WC vs RSA .................................................. 82

Figure 39: SA overseas tourists: Region of residence ................................................................................... 83

Figure 40: WC real GDPR growth 2005-2015: Tourism ............................................................................... 84

Figure 41: WC real GDPR growth 2005–2015: Finance & insurance...................................................... 88

Figure 42: Ernst & Young Financial Services Index ....................................................................................... 89

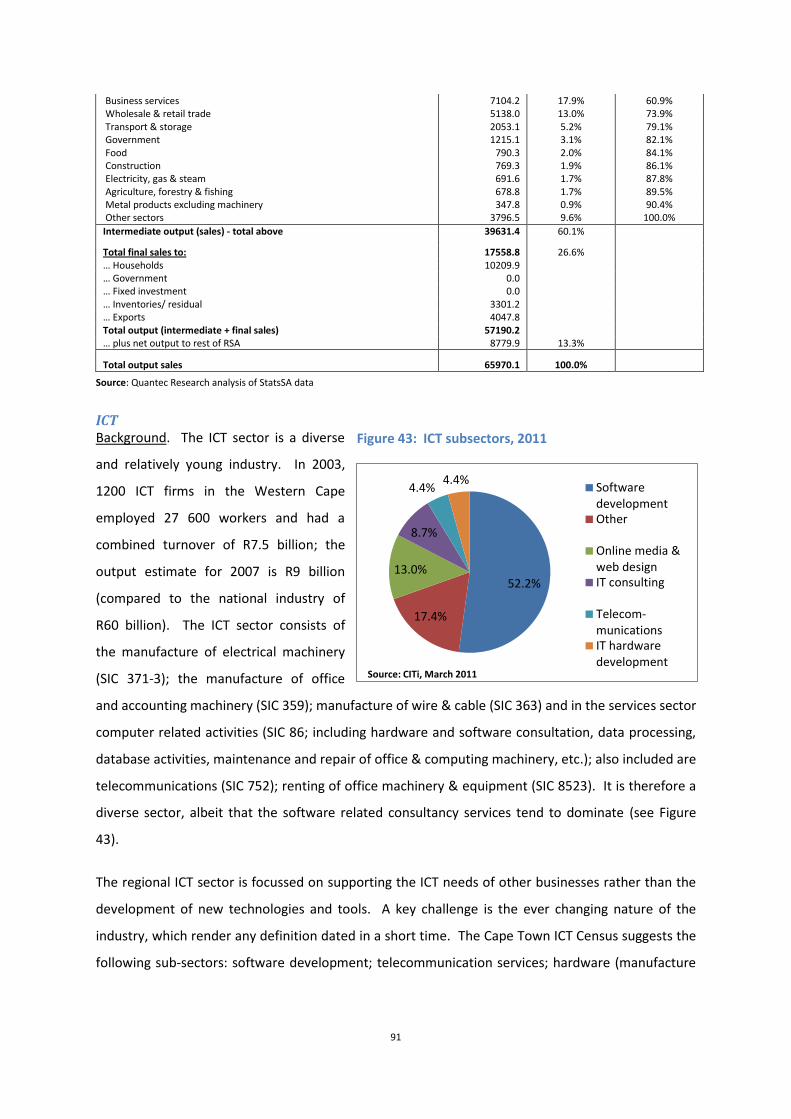

Figure 43: ICT subsectors, 2011 ............................................................................................................................. 91

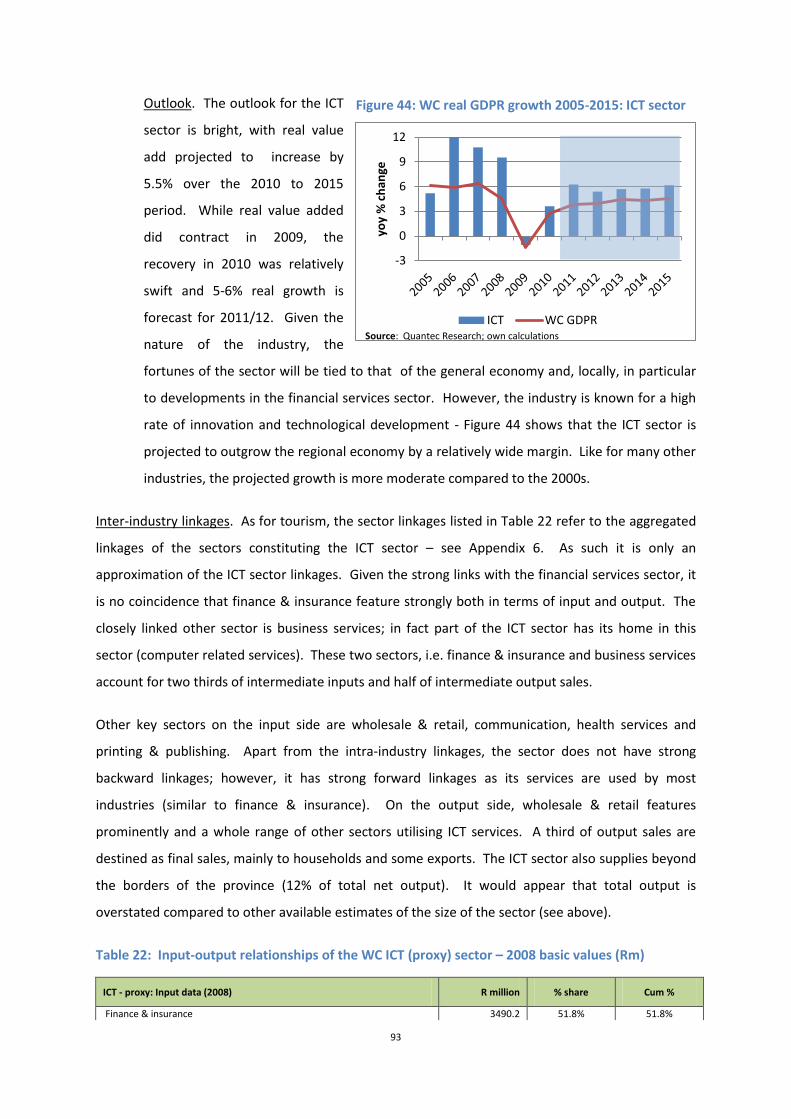

Figure 44: WC real GDPR growth 2005-2015: ICT sector ............................................................................ 93

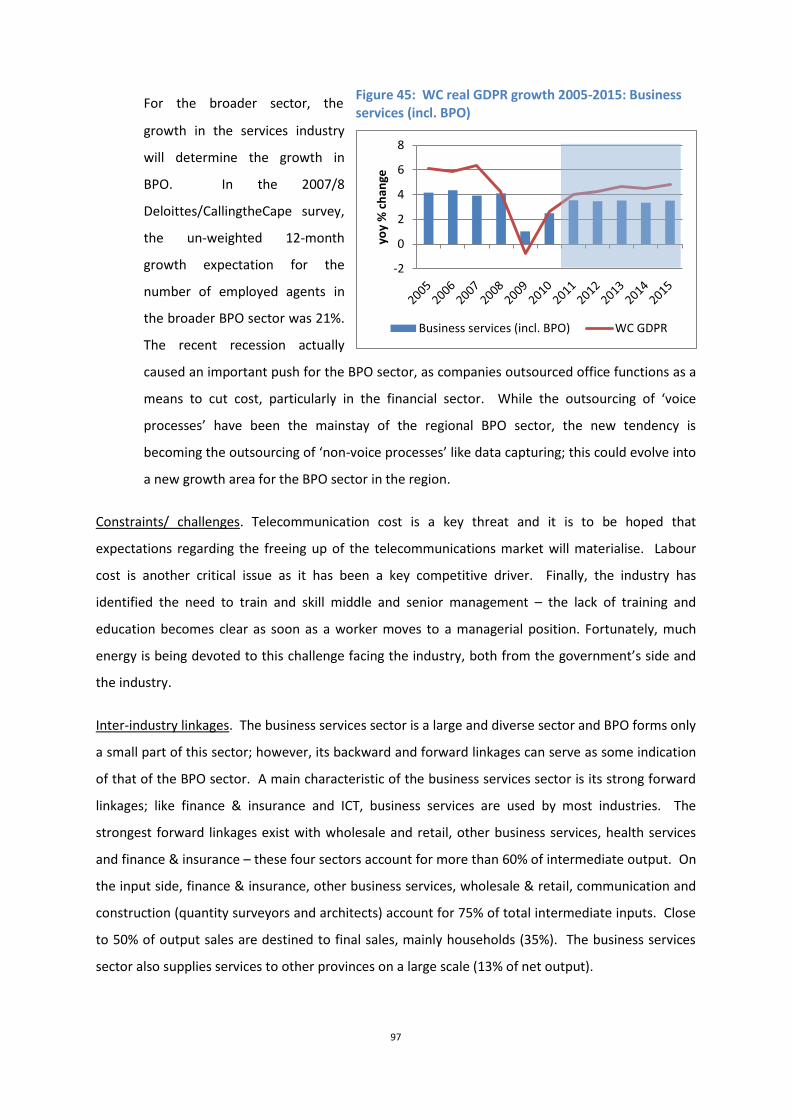

Figure 45: WC real GDPR growth 2005-2015: Business services (incl. BPO) ..................................... 97

List of Tables Table 1: Outlook for world real GDP growth: 2010 to 2012 ......................................................................... 6

Table 2: South Africa – forecasts of key economic variables: 2011-13 .................................................. 12

Table 3: Western Cape real GDPR and employment growth: 2000 to 2009 (yoy % change) ...... 20

Table 4: WC agriculture, forestry & fishing (constant 2005 prices) ....................................................... 40

Table 5: Input-output relationships of the WC agriculture sector – 2008 basic values (Rm) ...... 43

Table 6: WC food & beverages – agriculture processing: 2007–15 (constant 2005 prices) ......... 50

Table 7: Input-output relationships of the WC food processing sector – 2008 basic values (Rm)

............................................................................................................................................................................................... 53

Table 8: Input-output relationships of the WC beverage & tobacco sector – 2008 basic values

(Rm) .................................................................................................................................................................................... 53

Table 9: WC clothing & textile sector: 2007-15 ............................................................................................... 55

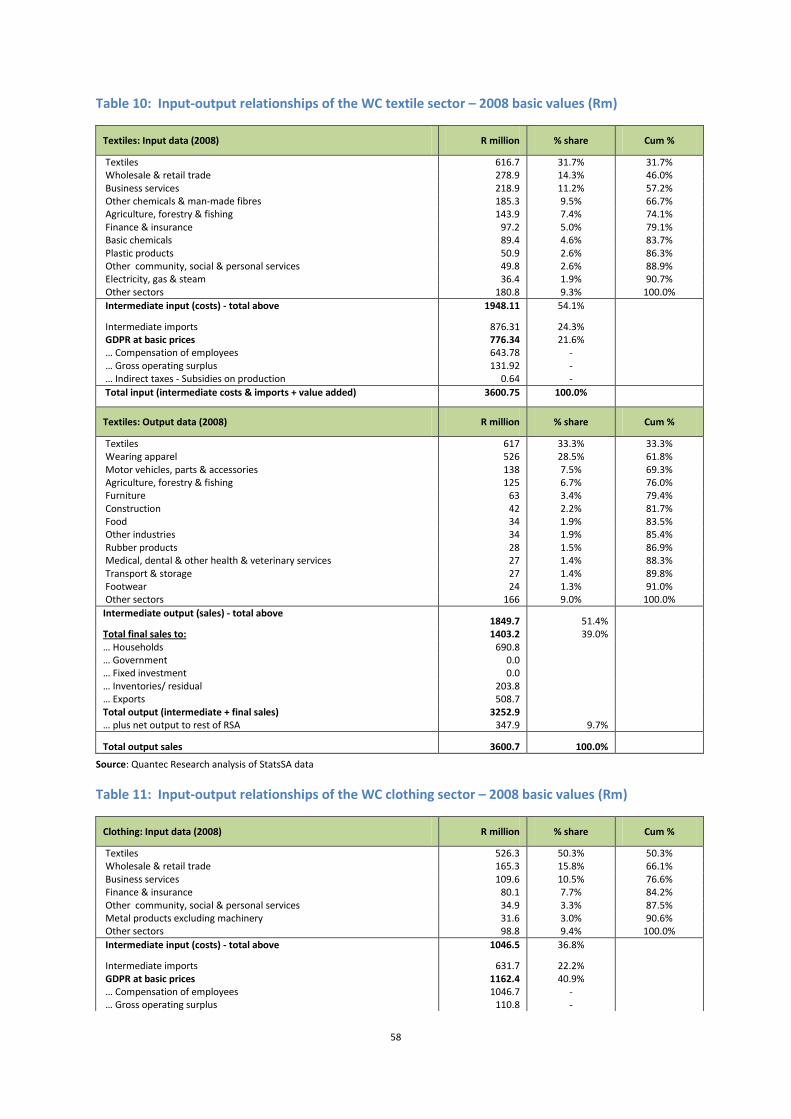

Table 10: Input-output relationships of the WC textile sector – 2008 basic values (Rm) ............. 58

Table 11: Input-output relationships of the WC clothing sector – 2008 basic values (Rm) ......... 58

Table 12: WC broad metals & engineering sector: 2007-15 ....................................................................... 61

Table 13: Input-output relationships of the WC metal products sector – 2008 basic values (Rm)

............................................................................................................................................................................................... 64

Table 14: WC electronics industry (excl. ICT) 2007-15................................................................................ 68

Table 15: Input-output relationships of the WC electronics (proxy) sector – 2008 basic values

(Rm) .................................................................................................................................................................................... 70

Table 16: Input-output relationships of the WC other transport equipment (incl. boat building)

sector – 2008 basic values (Rm) ............................................................................................................................. 73

Table 17: WC furniture sector: 2007-15 ............................................................................................................. 75

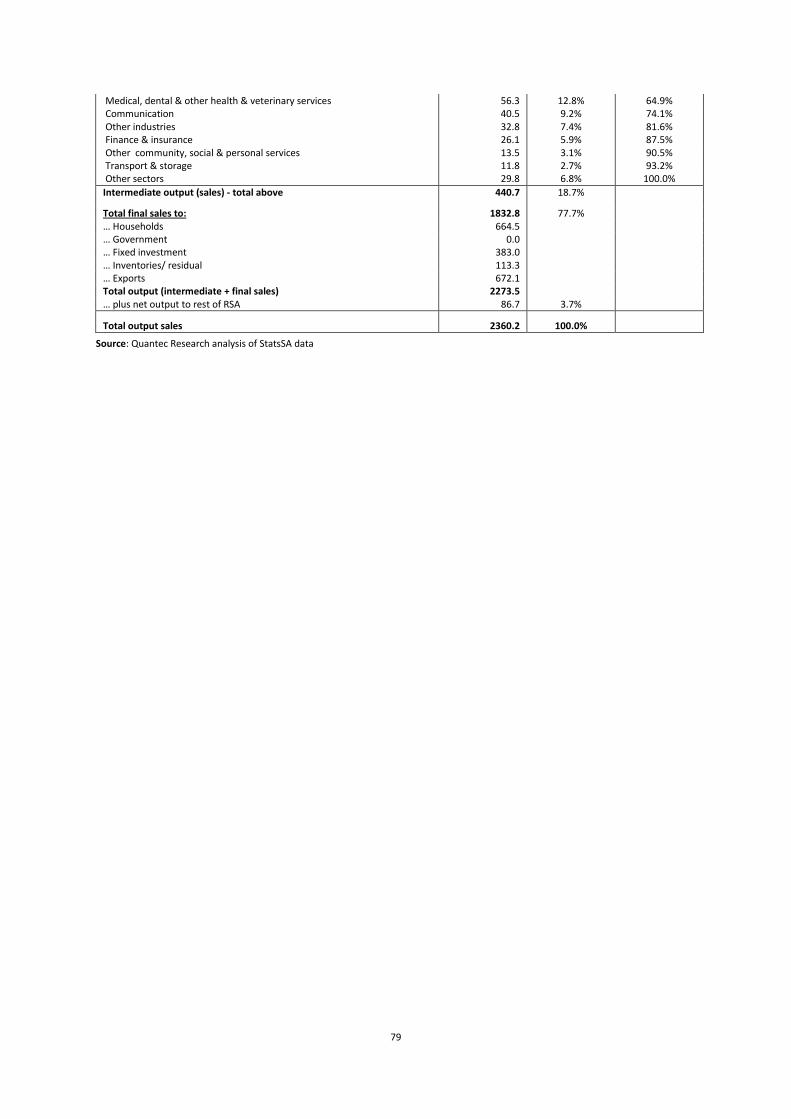

Table 18: Input-output relationships of the WC furniture sector – 2008 basic values (Rm) ....... 78

Table 19: Input-output relationships of the WC tourism (proxy) sector – 2008 basic values (Rm)

............................................................................................................................................................................................... 87

Table 20: Input-output relationships of the WC finance & insurance sector – 2008 basic values

(Rm) .................................................................................................................................................................................... 90

Table 21: WC ICT sector (proxy): 2007-15 ........................................................................................................ 92

Table 22: Input-output relationships of the WC ICT (proxy) sector – 2008 basic values (Rm) .. 93

Table 23: Input-output relationships of the WC business services sector – 2008 basic values

(Rm) .................................................................................................................................................................................... 98

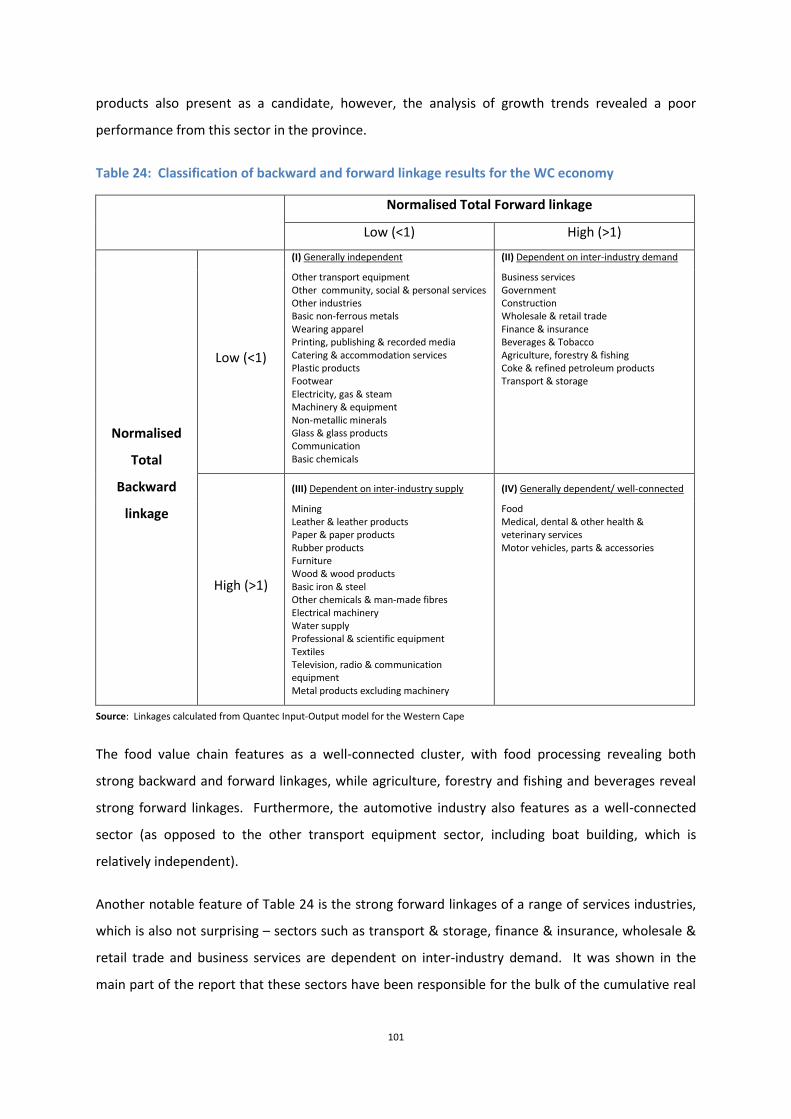

Table 24: Classification of backward and forward linkage results for the WC economy ............. 101

Table 25: Classification of WC industries i.r.o. their ‘induced effect’ multipliers ............................ 102

Table 26: Classification of WC sectors’ economy-wide GDPR and employment multipliers* .... 105

Table 27: Schematic layout of a two region input-output table .................................................................. 125

Table 28: SA Tourism expenditure by product, 2008 ................................................................................. 131

List of Abbreviations AEs: Advanced economies

AISA: Aquaculture Institute of South Africa

BER: Bureau for Economic Research

BFAP: Bureau for Food & Agricultural Policy

BPO: Business Process Outsourcing

CCDI: Cape Craft & Design Institute

CITI: Cape Information Technology Initiative

COGSI: Cape Oil & Gas Supply Initiative

CPI: Consumer Price Index

CSP: Community, Social and Personal services

CTBi: Cape Town Boatbuilding Initiative

CTICC: Cape Town International Convention Center

CTRU: Cape Town Routes Unlimited

DEDT: Department of Economic Development and Tourism

ECB: European Central Bank

EMs: Emerging economies

EU: European Union

FAO: Food & Agriculture Organization

GDE: Gross Domestic Expenditure

GDP: Gross Domestic Product

GDPR: Gross Domestic Product Regional

GVA: Gross Value Added

ICT: Information & Communications Technology

IMF: International Monetary Fund

LSM: Living Standards Measure

MEDS: Micro-Economic Development Strategy

MENA: Middle East & North Africa

NCA: National Credit Act

NTIP: National Tooling Initiative Program

OECD: Organization for Economic Cooperation & Development

OEM: Original Equipment Manufacturers

PERO: Provincial Economic Review and Outlook

PGWC: Provincial Government of the Western Cape

RSA: Republic of South Africa

SA: South Africa

SACU: South African Customs Union

SAGOA: South African Oil & Gas Alliance

SARB: South African Reserve Bank

SIC: Standard Industrial Classification

SPV: Special Purpose Vehicle

StatsSA: Statistics South Africa

TASA: Tooling Association of South Africa

TSA: Tourism Satellite Account

WC: Western Cape

WCFI: Western Cape Furniture Initiative

i

Executive Summary

Introduction. The Department of Economic Development & Tourism (DEDT), Provincial

Government of the Western Cape (PGWC) identified a need to analyse and assess the Western Cape

economy from a macro-economic perspective. The current study is a response to this need. The

study was conducted in order to obtain a real sense of the (relative) growth potential of the various

industries and the input-output modelling infrastructure was also utilised to investigate the region’s

inter-industry linkages.

The methodology followed was to feed the Bureau for Economic Research’s (BER’s) 5-year forecast

for the expenditure side of the SA economy into Quantec’s Inter-industry and Western Cape Input-

Output models. An attempt was made to reconcile the standard industry classification with the DEDT

working definitions as followed in the MEDS. The resultant projections were judgementally adjusted

where hands-on industry information/ desk research dictated that. The forecast results in respect of

the Western Cape economy, including more detailed discussions of key industry outlooks and

linkages, were presented in the main section of the report.

International economy. Whilst the anticipated shape and length of the ensuing business cycle

remains uncertain, it seems clear that the global, national and regional economies have all

embarked on a recovery from what is being described as the Great Recession (2008/9). At the global

level the recovery is characterised by a two speed expansion, with advanced economies (AEs)

expected to grow by a relatively modest 2.5% per annum and emerging market economies (EMs) by

6.5% per annum over the short to medium term. The major challenge for AEs is to exit their

stimulatory macro-economic policy stances (read: tighter national budgets and higher interest rates)

and for EMs to strike pre-emptively at nascent inflationary pressures, not only due to cost-push

factors (food and energy prices), but also due to overheating elements in some developing

economies (e.g. China). At the time of writing global economic forecasts were being scaled down

somewhat in respect of 2011, mainly as a result of the impact of the Japanese earthquake and

tsunami (March 2011) and the drag from the higher oil price. Global inflation is on the rise, albeit

that much slack remains in the AEs. The ECB already commenced with its normalisation of interest

rate levels and in the USA this is expected over the short term. The US dollar remains weak and is

likely to remain so in view of the US’s precarious fiscal position, which is only projected to unwind

slowly.

Provided relatively slow growth in the AEs, combined with a bullish commodity outlook,

international capital flows to commodity-based economies are expected to remain lively. The risk

ii

here is a harder landing in EMs. Other global economic risks, which have tended to intensify in

recent months, include possible debt restructuring in southern European sovereigns (e.g. Greece),

fiscal policy-related events in AEs, and political unrest in the MENA region, with its attendant

implications for the international oil price. Uncertainty is a hallmark of the global economy following

the financial crisis.

South African economy. In view of this global outlook, the domestic and regional economic

outlooks are somewhat uncertain. However, it seems that the specific constellation of global forces

dictates an economic environment where the rand exchange rate is likely to remain relatively strong

with no end in sight of potential volatility. This is negative for the tradable goods sectors, whilst the

tertiary sectors tend to benefit from lively domestic demand conditions, stimulated by the positive

income effects tied to a favourable terms of trade and low inflation and interest rates. It is

somewhat worrying that the initial phase of the economic recovery is dominated by the consumer,

with business confidence and fixed investment expenditure lagging and therefore employment

creation. In the absence of more meaningful fixed investment expenditure of the labour absorbing

kind, the sustainability of the business cycle upswing comes into question.

South Africa’s real GDP growth rate is projected to accelerate from 2.8% in 2010 (i.e. the first

calendar year of economic recovery, to around 3.5% in 2011 and 4-4.5% over the medium term. In a

different global economic climate and with a less robust domestic fixed investment prospect, this

outlook does not compare well with the high growth achieved over the 2004-7 period (5.2% per

annum); however, should be slightly above trend economic growth. Inflation is projected to

accelerate over the short term and possibly breach the upper range of the inflation target towards

the end of the year; however, is projected to remain inside but close to the upper 6% range of the

inflation target over the medium term. In the absence of unexpected shocks, prime interest rates

are projected to increase by 300 basis points (end 2011-13). The current account deficit on the

balance of payments is projected to increase from 2.8% in 2010 close to 6% in 2013/14.

Western Cape economic outlook. In the Western Cape, the tertiary sectors are again leading the

economic recovery and benefit from the macro-economic conditions (favourable terms of trade,

strong currency, low inflation and interest rates and a buoyant domestic market). Whilst this

represents a continuation of the structural trend in the regional economy, it runs counter to the

PGWC’s stated objective to stimulate semi- and unskilled labour intensive manufacturing activity.

The regional manufacturing sector has shed jobs on a large scale over the past decade and this

tendency needs to be arrested should the province want to achieve its socio-economic objectives

premised on poverty alleviation. This does not mean the tertiary sectors must be neglected, as the

iii

growth of these sectors is employment elastic, e.g. business services (including BPO) contribute and

have shown strong employment growth; wholesale & retail, catering & accommodation and tourism

are all responsive in terms of employment creation in a growing economy. However, special efforts

are required regarding the manufacturing industries, faced not only by an adverse track record, but

relatively hostile macro-economic conditions. Ultimately the tertiary industries are derived

industries, which imply that should the primary and secondary industries struggle, it will spin-off on

the tertiary sectors as well.

Sectoral growth pattern, 2000-9. The Western Cape economy has out-performed the national

economy, growing by 4.3% per annum versus 3.6% per annum over the period 2000 to 2009;

however, labour absorption in the region was poorer compared to national. The overall

employment elasticity for the regional economy is 0.28 compared to 0.40 for national; both ratios

are low, but especially true for the Western Cape economy. This state of affairs results from the

following tendencies in the regional economy:

Firstly, the high-growth sectors (7-9% real value-added growth) in the province (e.g. finance

& insurance, construction, communication; furniture, other transport equipment, including

boat building) are poor labour absorbers; furniture, leather & footwear and the automotive

sectors grew strongly and actually shed jobs on balance over the 2000s. It follows that for

these sectors favourable economic conditions are required only to maintain their work

forces, if at all.

Secondly, the leading employment creating sectors (e.g. the broad community, social &

personal services sector, the trade sector, electricity, mining, transport & storage and

tourism) exhibited relatively moderate growth rates (2-4% in real terms), i.e. the

employment creating sectors tend to be moderate to average growers. The business

services and ICT sectors are exceptions to this rule, showing both strong growth (5-8%

range) and meaningful job growth (2-5% per annum).

Thirdly, a whole range of primary and secondary industries shed jobs despite the relatively

lively general economic conditions over the biggest part of the 2000-9 period. This group is

led by the job-shedding that occurred in the agricultural and clothing & textile sectors; other

sectors included here are non-metal minerals, electronics, food & beverages, petro-

chemicals (all exhibiting below-average growth) and furniture, leather & footwear and

automotive (exhibiting high growth). These tendencies point to a higher degree of capital

intensity in most of the region’s primary and secondary industries.

iv

The outperformance of the Western Cape economy in terms of real GDPR growth is explained by the

strong contribution to growth made by the broad financial and business services sector, growing by

6.5% per annum and creating jobs at a rate of 3.8% per annum (with all the job growth accounted

for by the business services subsector). This sector, as well as the wholesale, retail, catering &

accommodation sector (including tourism), remain the mainstay of the regional economy; the trade

sector grew by 4.2% per annum and created jobs at a rate of 3.2% per annum. Transport, storage &

communication also made a significant contribution (3.9% per annum real GDPR growth and 1.7%

per annum employment growth) as did community, social & personal services (2.6% and 3.2%

respectively). The contribution by the manufacturing sector is also substantial (explaining close to

10% of the cumulative growth in the province over the 2000s); however, this is mainly due to its size

as the growth was anaemic (2.3%) and jobs were shed at a rate of 1.5% per annum.

From an employment perspective, the large job shedders were agriculture, forestry & fishing

(accounting for close to 50% of job losses in the province over the 2000s) and manufacturing

(accounting for 17% of the job losses). Within the manufacturing sector, clothing & textiles, leather

& footwear, furniture, electronics, and non-metal minerals were the leading job shedders as noted

above; the food & beverage subsector, automotive and petro-chemicals also shed jobs on balance,

however, only marginally so.

Industry outlook for the Western Cape economy, 2010 to 2015. A range of economic

indicators is conclusive that the regional economic recovery was well-established by the first quarter

of 2011. The recovery commenced during the third quarter of 2009 and has been led by improving

business conditions in the tertiary sectors, i.e. the mainstay of the Western Cape economy.

However, at the time of writing manufacturing conditions improved more meaningfully; it is only the

building & construction sector clearly lagging the economic recovery. Real GDPR growth is projected

to continue recovering, from an estimated 2.7% in 2010 to 3.9% in 2011 and between 4-4.5% over

the medium term, averaging 4% over the 2010-15 period. While the region’s outperformance of the

national economy is projected to continue, the margin of outperformance may decline and the level

of growth is likely to be well below that over the 2004-7 period. The province is faced with a

different global economic environment and its leading growth industry, i.e. financial services, is

unlikely to repeat its spectacular growth over the 2000s.

Considering the sectoral picture forecast over the 2010-15 period, three groups of industries are

identified, namely the high-growth sectors, the medium/ average growth sectors and the low-

growth sectors. It needs to be emphasised the sectors classified in this way include only those for

which real value added growth rates could be quantified; there are a number of smaller industries

v

growing rapidly off a low base for which growth projections could not be quantified and are

discussed qualitatively in the report (see below). Furthermore, the quantification of the growth

prospects was conducted for 26 industry groups, more or less at a 2-digit SIC level, including an

attempt to come closer to the DEDT’s working classification of industries – see Appendix 5. This

included the calculation of proxy sectors and growth rates (see Appendix 6).

The high-growth sectors, projected to grow between 4.4% and 8% per annum (2010-15),

include: communication (8%); finance & insurance (6%); ICT (5.5%); furniture (5.3%);

automotive (5.1%); other transport equipment (incl. boat building) (5.1%); construction

(5%); leather products & footwear (4.5%); and tourism (4.4%).

The medium/ average growth sectors, projected to grow by between 3% to 4.3% per annum,

include: metals & engineering (4.3%); electronics (4.2%); other manufacturing industries

(4.2%); petro-chemicals (4.1%); wholesale, retail, catering & accommodation (3.8%);

transport & storage (3.4%); business services (3.4%); other CSP services (3.2%); and

electricity (3.1%).

The low-growth sectors, i.e. subsectors projected to grow by less than 3% per annum are:

food & beverages (2.8%); agriculture, forestry & fishing (2.3%); government (2.1%); clothing

& textiles (1.9%); medical & health services (1.3%); wood, paper, printing & publishing (1%);

non-metal minerals (0.9%); and mining (-0.7%).

In terms of projected employment growth, a similar grouping of industries can be made. Whilst the

forecast employment growth rates tend to be optimistic compared to the 2000-9 history, the

emphasis should be on the relative employment performance rather than the absolute levels of the

projected growth.

The high employment growth sectors, with employment expanding at rates between 2.5%

and 3.5% are: automotive (3.1% per annum, 2010-15); business services (excl. ICT) (2.8%);

tourism (2.7%) and wholesale, retail, catering & accommodation (2.5%). The fast projected

employment growth for the automotive sector is surprising in view of the historical

experience, but could be linked to an optimistic export assumption.

The average-growing sectors in terms of employment are ICT (1.8%); other manufacturing

industries (1.6%); government (1.4%); medical & health services (1.3%); agriculture (1.3%);

metals & engineering (1%); other transport equipment (incl. boat building) (0.8%);

electronics (0.8%) and other CSP services (0.8%).

vi

Low job growth sectors include communications; wood, paper, printing & publishing; finance

& insurance, furniture, food & beverages and petro-chemicals and zero growth in the case of

construction. The work forces in these latter-mentioned subsectors are essentially projected

to remain stable. Subsectors projected to marginally shed jobs over the medium term

include: electricity & water supply, non-metal minerals, transport & storage, mining and

leather products & footwear. In the clothing & textiles sector job shedding is projected at a

rate of 2% per annum. As noted in the report, key policy intervention initiatives may prove

these projections, informed by the historical trends and relationships, overly pessimistic.

Regarding exports, the projected real growth (5.2% per annum, 2010-15), is likely to be below that

achieved over the 1995-2009 period (5.9%) and particularly over the 2000-7 period (6.8%). Demand

conditions abroad, particularly in the AE’s, are projected to be less robust compared to the 2000s.

Furthermore, the domestic macro-economic environment (read: buoyant domestic market and a

strong rand exchange rate) shaping up again may dictate against strong export growth. While the

agriculture and food (and beverages) processing sectors are likely to remain the mainstay of regional

exports, in terms of projected growth rates, leading the pack are:

The high export growth sectors, namely automotive (10.3% per annum); communications

(9.5%); metals & engineering (8.6%); agriculture (8.1%); electronics (7.8%) and business

services (including BPO) (7.4%).

Medium export growth sectors include: transport & storage (6.3%); electricity (6.3%); leather

products & footwear (6.3%); medical services (6.2%); tourism (6.2%); other transport

equipment (5.5%); other CSP services (4.9%); ICT (4.9%); petro-chemicals (4.8%) and

wholesale/ retail (4%).

Low export growth sectors include: furniture (3.1%); finance & insurance (2.3%); mining

(2.3%); food & beverages (1.7%); non-metal minerals (1.1%); and wood & paper (0.4%).

Clothing & textile exports are projected to contract by 3.3% per annum over the forecast

period. It needs to be emphasized, while food & beverages export growth is projected at a

relatively low level, this remains the province’s leading export sector in terms of size.

Finally, not appearing in these growth statistics, are the stellar performances of a number of small

industries, growing off a small base, but with huge potential (as discussed in the report). Included

here are the aquaculture industry, the (upstream) oil & gas subsector; boat building; crafts and call

centres/ BPO. Other sectors, which have been identified by DEDT but not discussed in this report,

vii

include arts & culture and film making. Whilst small, these industries all make an important

contribution to the growth and development of the Western Cape economy.

Inter-industry linkages. One of the novelties of input-output analysis is the fact that it facilitates

an analysis and understanding of the inter-connectedness of industries, both in a vertical and

horizontal dimension. The analysis of the growth outlook was complemented by an analysis of (the

intra-regional) forward and backward linkages (focussing on intermediate sales and supply) and

(value added and employment) multipliers (which includes the induced effects when the household

sector is made endogenous in the model). The following results emerged:

Regarding backward and forward linkages, the analysis revealed somewhat mixed results: the

relatively long list of generally independent manufacturing industries (with one or two services

sectors, e.g. other CSP services, catering & accommodation and communication) contrasts with

an equally long list of strong backwardly linked manufacturing industries, some with strong

forward links (e.g. beverages and petroleum products) and a list of services industries with

strong forward linkages (e.g. business services, finance & insurance, wholesale & retail, transport

& storage and government). Agriculture, forestry & fishing also reveal strong forward linkages.

Only the food, automotive and medical & health services sectors reveal both strong backward

and forward linkages.

Regarding the value-added and employment economy-wide multipliers, the analysis has shown a

long list of mainly manufacturing industries, which are relatively unresponsive in terms of value-

added and employment; the exceptions are food and plastic products in terms value-added and

furniture, clothing, leather products and textiles in terms of employment. The whole range of

services industries exhibit above average value-added multipliers; however, some combined

with weak employment responsiveness (e.g. finance & insurance, medical & health services,

business services, transport & storage and communication) and a few with above average

employment responsiveness (e.g. other CSP services, government, wholesale & retail and

catering & accommodation).

Concluding remarks. In all, the structural trend over the past decade in the Western Cape, namely

a rising contribution by the tertiary sectors of the regional economy, is expected to continue. The

province has a revealed comparative advantage in a number of these sectors (e.g. finance &

insurance, business services, wholesale & retail and tourism) and the macro-economic environment

is expected to benefit these sectors. For the most part these services sectors are dependent on

inter-industry sales, have strong links with the household sector and other provinces.

viii

In addition to the favourable prospects in the tertiary industries, the outlook for agriculture, forestry

& fishing and the food processing cluster appears promising from a price perspective and global food

shortages, with new opportunities opening up in South Africa’s trade with developing countries

(such as China and India). The food value chain is a well-connected industry, albeit that the

agriculture sector has disappointed from a growth and employment perspective.

Finally, while manufacturing prospects remain sub-par, there appears to be serious intent, both from

national and provincial government, to arrest the under-performance of a number of industries. The

analysis has shown some mixed results in respect of the regional manufacturing sector inter-industry

linkages, with a (somewhat surprisingly long) list of generally independent industries and industries

exhibiting below average value-added and employment multipliers, which tend to disqualify these

industries from receiving policy support. However, it should be emphasised that the current analysis

is of a cursory nature and aims to complement the existing MEDS research and any further research

required. There is also a relatively long list of strong backwardly linked secondary industries and

industries with above-average employment multipliers, which require the attention of the policy

authorities.

Pieter Laubscher1

Independent Economist

29 June 2011

1 I would like to acknowledge and am indebted for the guidance and inputs of Prof Philip Black (CER) and Claude van der Merwe

(Quantec Research).

1

A macro-economic assessment of the Western Cape economy’s sectoral and industrial growth prospects, 2010 to 2015, including an assessment of the inter-industry linkages

Introduction

The Western Cape regional economy is situated in the national and global economies. It is true that

the macro-economic context in which the regional economy grows and prosper exercises a

determining influence on the performance of the Western Cape economy. It is also true that this

macro-economic context changes over time and this change can be dramatic, both from a cyclical

and a structural point of view. Firstly, there are structural changes to consider at the global, national

and regional levels and, secondly, there is the issue of cyclical change. An assessment of the growth

potential of regional industries has to be located within this dynamic context.

The Department of Economic Development & Tourism (DEDT), Provincial Government of Western

Cape (PGWC) has identified a need to analyse and assess the Western Cape economy from a macro-

economic perspective in order to come to grips with the sectors and industries in the region

displaying high growth and/or potential to grow. In conjunction with the vast micro-economic

research that has been undertaken in the Micro-Economic Development Strategy (MEDS) project,

such a macro-economic assessment of regional growth prospects, where the emphasis is to come as

close as possible to the DEDT’s ‘working’ industry classification, could be useful in informing policy

interventions.

As changes in the macro-economic environment can exercise substantial influences on the economic

performance of businesses over the short to medium term, it is useful to periodically assess the

macro-economic prospects and how the bigger picture translates to and impact on the outlook for

individual industries and businesses.

The current report sets out outlining the international (first section) and national economic outlooks

(second section) before the focus moves to the regional economy (third section). In the third and

main section of the report, the implications of the global and national economic trends for the

regional industries are considered. First an analysis is conducted of the historical growth trends

(2000-9) in respect of GDPR growth, employment and exports. Secondly, the sectoral outlook (2010-

15) in respect of GDPR growth, employment and exports is considered, including an assessment of

the current cyclical state of the regional economy.

The general economic outlook for the primary, secondary and tertiary sectors of the province are

considered respectively. Within each of these broad categories, a template is constructed for

2

individual industries that have been identified by DEDT and the previous work done in terms of the

MEDS research. Each industry template contains data relating to the growth and employment of the

industry/ subsector, the main growth drivers, exports and including a brief outlook, as well as a

consideration of key constraints/ challenges faced by the industry/ subsector. The final section of

each industry template contains a brief analysis of the forward and backward inter-industry linkages.

The report ends with some concluding remarks and a summary of the main findings.

Objectives of the research

The central objective of the study is to assess the region’s industrial growth prospects across

industry groups as identified by the DEDT of the Provincial Government of the Western Cape (PGWC)

in order identify fast-growing industries. From one perspective, the study translates the implications

of the global and national economic outlooks for the regional economy at the sectoral level.

However, it also draws on ‘bottom-up’ information obtained by way of desk research in respect of

the individual industries/ sectors. The primary objective is to arrive at an assessment and five-year

forecast of each identified individual industry/ subsector in the Western Cape economy. A

secondary objective is to outline the inter-industry linkages of each industry/ subsector considered.

A novelty of the study is the fact that the sector definitions attempt to correspond with that of

DEDT’s working definitions, e.g. including an assessment of the tourism and ICT subsectors.

The proposed work was completed in three phases: during the first phase of the project a

preliminary sectoral forecast (2011-15) was prepared (the methodology and technical aspects

relevant to this stage are explored below and in the relevant Appendices); during the second phase

the forecasts were refined and finalized and written up in a report (and reproduced in the current

report); and during the third stage the inter-industry linkages were investigated to conclude with a

comprehensive and final research report.

Methodology

The first step in the first phase of the study was to come to grips with the macro-economic outlook

over the next five years. To this end, the BER five-year macro-economic forecast for the South

African economy (Economic Outlook, April 2011) and its short-term forecast (Economic Prospects,

2011Q2), were sourced, studied and prepared for input into the Quantec Inter-Industry model. The

macro-economic forecasts of the National Treasury and Reuters Consensus (2011 to 2014) were also

consulted.

The second step in the first phase of the study was to derive sectoral projections at the national

level. The expenditure variables of GDP (i.e. the demand side of the economy, contained in the BER

3

forecast) were fed into the Quantec Inter-Industry model in order to derive sectoral projections (i.e.

the supply side of the economy) of, inter alia, GDP, employment, exports and imports. The sectoral

output was disaggregated into 41 industry groups (see below).

In the third step of the first phase of the study, Quantec’s expanded (and existing) input-output

modelling infrastructure was utilised to generate a regional forecast for the Western Cape by sector.

The model projections were evaluated and adjusted where necessary in an iterative process

informed by extensive desk research, including in-depth interviews with Western Cape sector

specialists. Generic explanations of (1) the BER macro-econometric model used to generate the 5-

year forecast, (2) the Quantec Inter-industry model and (3) the Quantec Western Cape model are

provided in the relevant Appendices at the end of the report.

A standard sectoral forecast for the Western Cape economy already exists (see PERO, 2010). A key

challenge of the first phase of the project was to recalibrate the process in order to arrive at a

sectoral forecast which contains the industry groups as identified by MEDS/DEDT for the Western

Cape. The aim was to develop the existing modelling infrastructure further in order to generate

alternative industrial sector definitions in line with DEDT’s working industry definitions. Appendix 5

shows a reconciliation of the standard industrial classification (SIC) and the DEDT working sector

definitions, which guided the current study.

In order to adjust the forecast in terms of the standard classification of industries, a two-step

process was followed:

Firstly, the regional model was expanded to generate forecasts at a more disaggregated

level, i.e. 41 sectors instead of 26 as contained in the PERO forecast. A list of these 41

sectors is provided in Appendix 4.

Secondly, the forecasts of GDPR for the 41 sectors were then adjusted in one of three ways

to arrive at the 26 forecast sectors listed in Appendix 5, page 1282:

o Simply maintained if the definitions matched, e.g. agriculture; mining; motor

vehicles, parts & accessories; other transport equipment (incl. boat building);

furniture; other manufacturing industries; construction; finance & insurance;

medical & health services and government.

o Or sub-sectors were simply combined where the aggregate corresponded with the

suggested (DEDT) forecast definition if a priority sector or otherwise, e.g.

2 Please note that some of these sectors are DEDT non-priority sectors; however, forecasts were generated and included.

4

agriculture-processing (food and beverages)3; clothing & textiles; leather products &

footwear; wood, paper, printing & publishing; petroleum products, chemicals,

rubber & plastic; glass products & non-metal minerals; metals & engineering and

electricity & water supply.

o Or, in the case of some sectors, weighted proxies – corresponding with the DEDT

definition – were calculated, e.g. electronics; tourism and ICT. The method/research

used in order to calculate these proxies is discussed in Appendix 6, page 130. These

sectors were therefore combined across other sub-sectors (see Appendix 5); in

order, for the total over all sectors to add up, the shares of the proxies had to be

excluded, giving rise to new definitions of the SIC, e.g. wholesale, retail, catering &

accommodation (excl. tourism); transport & storage (excl. tourism); communication

(excl. ICT); business services (excl. ICT) and community, social & personal service

(excl. tourism).

The following DEDT priority sectors were not modelled as they were too disaggregated: aqua-

culture; crafts; oil & gas; call centres & BPO; film making; and arts & culture. Except for the latter-

mentioned two sectors, these sectors were studied on an individual basis during the second and

third phases of the project. Boat-building is also not forecast directly; however, the ‘other transport

equipment’ sub-sector can be used as a proxy in this regard.

During the second phase of the project, the assumptions and industry projections were refined and

finalised and the results were written up (and reproduced here). The third phase of the project,

involved the determination and outlining of the sectoral backward and forward linkages at the

regional level. For those industries included in the modelling, the derivation of the relevant

backward and forward linkages is a straightforward mechanical exercise where the relevant input-

output/ technical coefficients determine the respective linkages. Where modelling was not possible

recourse to other available research was taken.

3 It needs to be pointed out that a measure of approximation was allowed regarding industry/sector definitions as the current study is

concerned with growth trends. The aggregated food and beverage sector is not strictly defined as the agriculture processing industry; however, in a modeling context such approximation was thought to be acceptable; similar comments apply to the broad metals and engineering sector, assumed in the study to be approximated by the metals, metal products and machinery sector. For more detail, see Appendix 4, page 85.

5

World economic outlook

In its January 2011 update of the world economic outlook, the IMF stated that the 2009 contraction

of global economic activity was milder than expected and that the recovery momentum through

2010, particularly during the second half of the year, evolved somewhat stronger compared to

expectations. While substantial slack remains in the advanced economies (AEs), with lingering

unemployment, the economic recovery is well established; in the emerging economies (EMs) growth

has rebounded to pre-crisis levels, amidst signs of overheating in some economies.

The fact of the matter is that the world economy is moving beyond the Great Recession, sparked by

the onset of the 2007/8 financial crisis in the US subprime market. Current expectations are that the

recovery is set to continue, albeit not without attending risks – real GDP growth of around 2.5% per

annum is foreseen in the AEs (2011-12), while growth in excess of 6% per annum is forecast for EMs.

The IMF did not revise this forecast in its April 2011 World Economic Outlook; however, since

January the risks have intensified (see below). While growth is projected to be below par in the AEs,

the heartening development of recent months is the fact that the US and – to a lesser extent – the

Euro area are moving beyond the financial crisis as the financial institutions gradually return to

business as usual. Apart from the financial troubles in the Euro area periphery (and financial sector

solvency issues in the core European countries), financial conditions are more stable and should

continue to improve according to the IMF. However, the IMF did adjust its inflation forecast

noticeably upwards.

Growth

The consensus forecast for global growth during 2011/12 is around 4.5% per annum; however, we

have a two-speed recovery – as noted, much slack remains in the AEs with real GDP forecast to

expand around 2.5% per annum; in contrast, the growth momentum in EMs has picked up to pre-

crisis levels around 6.5% and expected to continue. Table 1 shows the forecast growth rates for

individual countries and regions, 2011/12. At the time of writing global economic forecasts were

being scaled down somewhat in respect of 2011, mainly as a result of the impact of the Japanese

earthquake and tsunami (March 2011) and the drag from the higher oil price.

An outstanding characteristic of the growth pattern in the AEs, is the expansionary monetary and

fiscal policies that prepared the way for the economic recovery. A central challenge for the AEs will

be the exit of these stimulatory policy stances. In terms of sequencing, the expectation is that fiscal

consolidation needs to happen first and in time the normalisation of interest rate levels. Fiscal

consolidation is much stronger in force in the Euro area periphery (beset by sovereign debt

problems), for instance, compared to core European countries and – for that matter – the USA,

6

where the latest moves have tended to be additional stimulus (e.g. the extension of the Bush tax

cuts, announced in December 2010 – see footnote). Monetary policy also remains – and according

to the IMF, should remain – stimulatory; core-inflation is not a problem (in the USA at 1.5%; Euro

area 1.1%) given the lingering output gaps and high rates of unemployment; inflation expectations

are also well-anchored. Fiscal consolidation in the AEs will be an enduring theme on the global front

and is the main reason why economic growth is forecast to moderate over the short term. The ECB

has already commenced the process of normalising interest rates due to the cost-push inflationary

effect of the increase in energy and food prices.

Table 1: Outlook for world real GDP growth: 2010 to 2012

2009 2010 2011F 2012F

Advanced economies (AEs) -3.4 3.0 2.4 2.6 USA -2.6 2.8 2.8 2.9 Euro area -4.1 1.7 1.6 1.8 Japan -6.3 3.9 1.4 2.1

Emerging economies (EMs) 2.7 7.3 6.5 6.5 Central & Eastern Europe -3.6 4.2 3.7 4.0 CIS -6.4 4.6 5.0 4.7 Developing Asia 7.2 9.5 8.4 8.4 China 9.2 10.3 9.6 9.5 India 6.8 10.4 8.2 7.8 Latin America -1.7 6.1 4.5 4.1 Middle East & North Africa 1.8 3.8 4.1 4.2 Sub-Sahara Africa 2.8 5.0 5.5 5.9

World real GDP -0.5 5.0 4.4 4.5

Source: IMF World Economic Outlook, April 2011

The household sectors in the USA and Euro area absorbed serious knocks during the recession and

are only now emerging from it; business fixed investment is also recovering driven by improved

profitability. However, while these developments on the expenditure side of the economy should

assist in closing the output gaps, a lengthy period of fiscal consolidation (the US budget deficit

measures in excess of 10% of GDP) is likely to exert an opposing influence for some time to come.

The financial systems of the US and Europe also need to be repaired and reformed while Japan has

reached the limits of fiscal sustainability. The short- to medium-term outlook is therefore for sub-

par economic growth in the major AEs – USA around 3% per annum; Euro area 1.7-2.5%; Japan 1.8%.

While the emerging and developing economies were affected by the sharp contraction of economic

activity in the AEs (-3.4% in 2009), the growth momentum in many of these economies (led by China,

India and East Asia and followed by Australia, Latin America and Africa) remained positive.

Developing Asia registered a 7% real GDP growth rate in 2009 according to IMF calculations (China

9.2% and India 6.8%), Latin America contracted by a mild 1.7% and sub-Sahara Africa continued to

grow by 2.8%. Most EMs rebounded strongly in 2010. Real economic growth in China and India re-

accelerated to above 10%, with these economies exerting a positive influence on commodity

7

markets. Commodity producing developing economies benefited from the associated positive terms

of trade effects tied to the sharp increase in commodity prices over the past year, as well as strong

capital inflows, which boosted the domestic demand components of these economies. The IMF

notes that signs of overheating have emerged in a number of EMs, which calls for a tightening of

economic policies. The IMF remains optimistic regarding the outlook for EM growth over the short

term, forecasting 6.5% real GDP growth during 2011/12; the corresponding forecast of the Sub-

Sahara region is 5.5% and 5.9% respectively.

The following risks are identified and have intensified in recent months:

While the sovereign debt and financial troubles in the European periphery were contained

(i.e. they did not spark wide contagion such as the US sub-prime debacle), the risk remains,

and particularly should the fiscal strategies in these economies (e.g. Greece, Ireland,

Portugal, Spain, and Italy) become unstuck. While the core EU countries’ economies – led by

Germany – are emerging robustly from the recession and the financial crisis, the financial

institutions in these economies have vast exposures to the troubled sovereigns in the south.

Any attempt at debt restructuring (in Greece, for instance, this looks imminent) could have

adverse implications for the banks in the core European countries. Tensions in the euro area

periphery could therefore spread to the core of Europe and from there beyond. Some

commentators are very negative on the potential repercussions a debt restructuring in

Europe may have.

While the political, social and economic tensions and instability in the Middle East & North

African (MENA) region has had in minimal impact on global economic activity thus far, the

increase of the oil price to above $120/b is ominous. The rising oil price, combined with

higher non-oil commodity prices, is lifting inflation levels throughout the globe, affecting real

household spending power. Further increases in commodity prices could cause economic

slowdown in both AEs and EMs.

The fiscal consolidation project in the major AEs (to a lesser extent in Europe) still need to

materialise and could deliver unwelcome surprises. Both the US and Japan recently

announced additional fiscal stimulation, which – according to the IMF – threatens medium-

term fiscal sustainability4.

4 The US budget deficit for fiscal 2011 is estimated at 10.9% of GDP following the extension of the Bush tax cuts and other fiscal

stimulation measures announced in December 2010. In Japan, the reconstruction effort following the earthquake and tsunami currently receives priority; however, the IMF urges that strategies be put in place to ensure medium-term fiscal sustainability.

8

The major risk in EMs is overheating economies, i.e. the policy authorities fail to act

decisively/ pre-emptively to contain nascent inflationary pressures. With the oil price (and

other commodity prices, e.g. food) having increased strongly in 2010 and jumping sharply in

January 2011 due to the political unrest in the MENA region, supply shocks to inflation are

already on the cards. EM central banks already faced with overheating economies, positive

terms of trade effects and strong capital inflows will have little option but to tighten policy

with the attendant risk of a boom-bust cycle/ hard economic landing. EMs account for 40%

of global household consumption and more than two thirds of global growth (IMF).

Inflation & commodity prices

The Economist $-based commodity price index increased by 47% in 2010 compared to 2009; the

North Sea Brent crude oil price increased by 30% on average. This sharp rebound in commodity

prices, which fell sharply in 2009, is driven by the demand stemming from China, India and other

commodity-intensive developing countries, the recovery of industrial demand in the major industrial

countries and food & oil price supply shocks. Oil prices have risen 30% since the fourth quarter of

last year due to the political upheaval in the MENA region. As a result, food prices have come under

renewed pressure following the heavy flooding-induced pressures during the winter months in the

Northern hemisphere. International food price inflation is running at close to 30% year-on-year

(wheat, sugar and edible oil prices have all raised sharply towards the end of 2010).

These supply shocks to inflation does not seriously threaten the economic conditions in the AEs

where substantial economic slack remains (a tightening of monetary policy – as opposed to a mere

normalisation of interest rate levels – is, for instance, not in prospect soon)5, but the picture is

different in EMs, notably China. Rising food & energy prices will in itself put poorer household

budgets under pressure and should second round inflationary pressures demand additional policy

tightening these economies can experience a harder landing. (These economies accord a higher

weighting to food & energy prices in their CPI baskets.)

The expectation is that headline inflation numbers in the AEs will rise over the short term due to the

impact of higher oil and food prices, but that core inflation and inflation expectations will remain

well-behaved in these economies (USA 1-2%; Euro area 1-2% and Japan 0-0.5%). The headline CPI

inflation forecast for the AEs has been revised upwards (in April from January) with 0.6 percentage

points to 2.2% in respect of 2011. In EMs, CPI inflation already measured above 6% on average in

5 JPM calculates that the 20% increase in oil price since the fourth quarter of 2010 will shave off 0.25% points from annualized global

growth during the first half of 2011. The impact is expected to be mild (obviously in the absence of additional shocks) as the oil price increases have not been accompanied by monetary policy tightening and/or an increase in risk aversion (geo-political concerns) which tend to affect business and consumer confidence.

9

2010 and is projected to approach 7% (2011) and to recede to between 5% and 6% over the

medium-term.

The oil price is projected to recede from recent spikes as the MENA political troubles stabilise and

due to the fact that crude oil stocks are at a five-year high. However, for other metal commodities,

e.g. copper and platinum, industrial demand is likely to underpin prices and as long as the Chinese

growth momentum in particular and the EM growth momentum in general persist, the fundamental

tendency in commodity prices is likely to remain favourable. The attendant risk here is clearly a hard

EM landing (led by China) noted above.

Currencies

The fundamental tendency in the US dollar has been to weaken against the euro and the yen, albeit

not without the accompanying volatility. Weakness against the yen is dictated by the savings surplus

Japanese economy with Japanese investors favouring to keep investments onshore due to the level

of uncertainty in the wake of the global financial crisis and recession. The destruction accompanying

the earthquake, tsunami and nuclear crisis boosted the yen further as Japanese firms/ investors

repatriated funds to finance reconstruction; the G7 major economies had to intervene in currency

markets to stem the appreciation of the yen. Weakness of the US dollar against the euro has not

been consistent – it gyrated along with the dictates of the sovereign debt problems in the Euro area

periphery countries, i.e. appreciates in times of crisis (Greece, 2010Q2; Ireland 2010Q4) and

depreciates when these ructions subside. While there is no view that the dollar will either

appreciate or depreciate sharply over the medium term, the unfavourable US fiscal position dictates

a weak dollar for the foreseeable future. The interest rate differential has also started to move

against the dollar following the ECB increasing its lending rate. The counter-balancing factor remains

Chinese and oil-exporting country purchases of US treasuries; this factor may avert a dollar crash.

South African economic outlook

The SA economy is a mixed economy sharing features both with the AEs (e.g. financial sector;

infrastructure) and the EM’s (e.g. poverty & unemployment levels). As a middle income developing

economy, real economic growth contracted during calendar 2009 along with the contraction in

global growth, but not as sharp as the AEs (1.7% versus 3.4%); EMs, in turn, grew by 2.8% in

aggregate, led by sustained high growth in China, India and other developing Asian economies. SA’s

GDP growth rebounded to 2.8% in 2010, ending the year with a higher than expected 4.4%

annualised growth rate (10Q4). CPI inflation bottomed at 3.2% in September 2010 and has since

accelerated to 4.2% (April 2011) mainly due to supply-side cost pressures, i.e. higher food and petrol

prices and some exchange rate depreciation; PPI inflation came in at 7.3% in March 2011. The

10

monetary policy stance remains accommodative, albeit that the next move in interest rates is likely

to be upwards (somewhere through 2011); fiscal policy also remains accommodative, but the recent

budget plans to reduce the deficit from the current 5.3% of GDP to 3.8% of GDP by the 2013/14

fiscal year.

Before the SA outlook is discussed, it is necessary to briefly consider the broad implications of the

international outlook:

With the global recovery expected to continue, external demand for SA’s exports is likely to

continue picking up; commodity prices should also benefit the SA terms of trade. The latter

index is currently at a multi-decade high, which provides a strong stimulus to the economy.

The prospect of low inflation in the AEs and accompanying low interest rates for the

foreseeable future implies that capital flows to EMs are likely to remain strong.

Unfortunately these capital flows consist mainly of portfolio investments (bonds & equities)

and tend to be volatile during periods of elevated risk aversion (e.g. during the Greece and

Irish sovereign debt crisis periods in 2010). This has implications for rand exchange rate

volatility, which has become an established trend in the SA economy6. The prospect of rand

exchange rate volatility will intensify once monetary policy tightening commences in the

AEs.

EM currencies are likely to be subject to appreciating pressure, given the outlook for a weak

dollar and strong inward capital flows. This is presenting the policy authorities with

headaches in terms of macro-management. The IMF prescription is contractionary fiscal

policy to counter the financial stimulus effect on domestic demand (witness the local

conditions, 2004-7). Such a macro environment is conducive to the non-tradable goods

(tertiary) sectors benefiting from buoyant domestic market conditions, but is adverse for the

tradable goods sectors such as manufacturing having to contend with stiffer import

competition and uncompetitive exports.

The higher oil and food prices still have to filter through fully to the local inflation indices

and this will be exacerbated in the event of currency depreciation. Whilst South Africa

shares the AE experience in terms of lingering unemployment/ a positive output gap and

well-anchored inflation expectations, the outlook for inflation is less favourable due to the

6 The IMF points out that the global current account imbalance remains in favour of the surplus countries/ regions (i.e. China and East

Asia, Japan, Germany and the oil-exporting countries), suggesting substantial excess savings globally flowing into and out of EM capital

markets depending on the degree of risk, real or perceived.

11

impact of rising food, petrol and electricity prices. The projected increase in inflation will put

disposable household incomes under pressure and invite first a normalisation and then a

tightening of monetary policy.

Towards the end of 2010 and during the early part of 2011 there was clear evidence of

buoyancy in the domestic market, benefiting from the combined stimulus tied to an

improved terms of trade and strong capital inflows (strong rand exchange rate, low inflation

& interest rates). The latest information on the domestic economic performance (2011Q2),

however, point to some slowdown in the consumer sector, possibly adjusting to a more

sustainable pace. While the recovery in the building and manufacturing sectors are shaping

up, this appears to be a slow process. Therefore, despite the increase in headline inflation,

the danger of secondary inflation appears limited and it is expected that the SARB will be

able to delay action on the monetary policy front. Interest rates are only expected to begin

increasing towards the end of the year/ early next year.

Growth

Real GDP began to expand again during the third quarter of 2009 following the recessionary

contraction during 2009 (-1.7% for the calendar year). From the third quarter of 2009 year-on-year

real GDP growth has accelerated from -2.4% to 3.7% at the end of 2010 and remained at that tempo

during the first quarter of 2011 – see Figure 1. While the SA Reserve Bank has not officially called the

end of the recession, indications are that the economy registered a lower turning point during the

third quarter of 2009. This would suggest that the recession was on a par with the shortest in the

post-WWII period. Amongst other, this is some reflection of the extent to which SA was shielded

from the impact of the global financial crisis and what has become known as the Great Recession.

Table 2 shows that most forecasts agree that economic growth is expected to continue accelerating

over the short- to medium term. Real GDP growth of 3.5% - 4% is forecast for 2011 (from 2.8% in

2010 and -1.7% in 2009), around 4% in 2012 and 4%-4.5% in 2013. The SARB reported huge upward

revisions to personal disposable income growth and household consumption expenditure during the

third quarter of 2010 – the household consumption expenditure annualised growth rate has picked

up to a 5-6% pace during the second half of 2010 according to the fourth quarter 2010 Quarterly

Bulletin. In contrast, the growth – albeit turning positive during the second quarter of 2010 – in

gross domestic fixed investment expenditure remains anaemic.

12

Figure 1: Real GDP growth

Source: SA Reserve Bank

Table 2: South Africa – forecasts of key economic variables: 2011-13

2009 2010est 2011F 2012F 2013F

Real GDP growth National Treasury -1.7 2.7 3.4 4.1 4.4 BER 2.8 3.7 3.8 3.8 Reuters Consensus - 3.5 3.8 4.1

CPI inflation National Treasury 7.1 4.3 4.9 5.2 5.5 BER 4.3 5.0 5.8 5.4 Reuters Consensus - 4.8 5.7 5.7

Prime overdraft interest rate (eop) National Treasury - - - - - BER 10.50 9.00 10.00 11.00 12.00 Reuters Consensus - 9.38 10.79 11.53

Current account balance (% of GDP) National Treasury -4.1 -3.2 -4.2 -4.9 -5.0 BER -2.8 -3.3 -4.9 -5.4 Reuters Consensus -3.7 -4.9 -5.4

Source: National Treasury: Budget Review 2011 / BER / Reuters Econometer, March 2011

Therefore, while domestic expenditure has become lively (real growth of 4.2% registered during

calendar 2010), the composition of growth is heavily in favour of the consumer at this stage of the

economic recovery. Consumer spending is running ahead at a similar stage (i.e. 6 quarters into the

economic recovery) compared to earlier economic upswing phases of the business cycle, while gross

domestic fixed investment is lagging badly (except compared to the weak trend in GDFI during the

late 1980s/ early 1990s) – see Figure 2.

-8

-6

-4

-2

0

2

4

6

8

10

Mar

-94

Mar

-95

Mar

-96

Mar

-97

Mar

-98

Mar

-99

Mar

-00

Mar

-01

Mar

-02

Mar

-03

Mar

-04

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

yoy

% c

han

ge

Recession GDP GDP (qoq ann%)

13

Figure 2: Real domestic spending during economic upswings7

Household consumption expenditure (HCE) Gross domestic fixed investment (GDFI)

Source: SARB / BER

More detail regarding the projected tendencies are provided below.

The unfortunate fallout from a weak fixed investment trend is that employment creation is

lagging as well. The acceleration in household consumption spending has been driven by