Indusind Bank Q1FY12 Result Update

4

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd. Email: [email protected] LONG TERM INVESTMENT CALL Accumulate 9 July 2011 Company Report | Q1FY12 Result Update Q1FY12 Result Highlights Indusind Bank (IIB) net profit grew by 52% YoY to INR 1802 Mn mainly driven by robust core fee income growth of 44% YoY. The proportion of core fee income increased due to increase in its third party products, trade and remittances, foreign exchange and Investment banking income. IIB’s net interest income has grown by 32% to INR 3900 Mn as compared to INR 2957 Mn in Q1FY11 & other income increased by 34% YoY to INR 2154 Mn. Advances grew 31.3% YoY to INR 283.8 Bn & deposits grew by 28.7% to INR 352.6 Bn. This was stronger than the industry’s growth rate of ~20% & ~17% respectively. Improvement in deposit mix along with branch expansion (326 from 224 branches) led to higher CASA ratio of 28.2% in Q1FY12 (24.3% in Q1FY11). Reported NIM improved 9 bps YoY to 3.41%, however, on sequential basis it declined 9 bps due to sharp rise in the cost of deposits (68 bps QoQ) while yield on advances increased by 68 bps. IIB continued to improve its asset quality and has brought down the net NPA level to 0.3% in Q1FY12 from 0.38% in Q1FY11. Gross NPA ratio fell to 1.08% in Q1FY12 from 1.26% in Q1FY11, but it increased sequentially by 7 bps and 2 bps. The NPA coverage ratio rose 288 bps YoY to 72.9%. Also the IIB maintained a healthy capital adequacy ratio (CAR) of 14.99% in Q1FY12 as against 13.71% in Q1FY11. The strong traction in CAR is likely to sustain IIB’s growth momentum in coming quarters. Outlook & Valuation Going forward IIB in next 3 years is planning to keep NIMs above 3.5% along with healthy bottom-line, this would be possible through 1. scaling up CASA ratio to 35% with 200 bps to 300 bps improvement every year. 2. Bank plans to take the branch network to 550 by Mar ’13. 3. Bank is expected to expand its product suite a nd services to achieve higher business growth. At the CMP, stock trades at 3x FY12E BV, we have Accumulate rating on the stock with target price of INR 320. Industry Banking CMP (INR) 287 Target (INR) 320 52 week High/Low (INR) 292/200 Market Cap (INR BN) 133571 3M Avg. Daily Volumes 665280 P/BV FY12E 3x Shareholding Pattern (%) Promoters 20% Institutions 42% Others 14% Non- institutions 24% Stock Performance 150 200 250 300 350 400 J u l S e p N o v J a n M a r M a y J u l IIB NSE Ni fty Performance (%) 1 Month 3 Months 1 Year IIB 9.4% 5.7% 31.4% NIFTY 2.5% -2.2% 5.8% * Source: Ace, Unicon Research (INR in mn) Particulars Actual Estimates NII 3900 4137 Operating Profit 3117 3282 PAT 1802 1853 * Source: Company, Unicon Research Analyst Shweta Rane | [email protected]

-

Upload

seema-gusain -

Category

Documents

-

view

224 -

download

0

Transcript of Indusind Bank Q1FY12 Result Update

8/6/2019 Indusind Bank Q1FY12 Result Update

http://slidepdf.com/reader/full/indusind-bank-q1fy12-result-update 1/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

ONG TERM INVESTMENT CALL

Accumulate9 July 2011

Company Report | Q1FY12 Result Update

Q1FY12 Result Highlights

Indusind Bank (IIB) net profit grew by 52% YoY to INR 1802 Mnmainly driven by robust core fee income growth of 44% YoY. The

proportion of core fee income increased due to increase in its third

party products, trade and remittances, foreign exchange and

Investment banking income. IIB’s net interest income has grown by

32% to INR 3900 Mn as compared to INR 2957 Mn in Q1FY11 & other

income increased by 34% YoY to INR 2154 Mn.

Advances grew 31.3% YoY to INR 283.8 Bn & deposits grew by 28.7%

to INR 352.6 Bn. This was stronger than the industry’s growth rate of

~20% & ~17% respectively. Improvement in deposit mix along with

branch expansion (326 from 224 branches) led to higher CASA ratio of

28.2% in Q1FY12 (24.3% in Q1FY11). Reported NIM improved 9 bps

YoY to 3.41%, however, on sequential basis it declined 9 bps due to

sharp rise in the cost of deposits (68 bps QoQ) while yield on

advances increased by 68 bps.

IIB continued to improve its asset quality and has brought down the

net NPA level to 0.3% in Q1FY12 from 0.38% in Q1FY11. Gross NPA

ratio fell to 1.08% in Q1FY12 from 1.26% in Q1FY11, but it increasedsequentially by 7 bps and 2 bps. The NPA coverage ratio rose 288 bps

YoY to 72.9%. Also the IIB maintained a healthy capital adequacy

ratio (CAR) of 14.99% in Q1FY12 as against 13.71% in Q1FY11. The

strong traction in CAR is likely to sustain IIB’s growth momentum in

coming quarters.

Outlook & Valuation

Going forward IIB in next 3 years is planning to keep NIMs above

3.5% along with healthy bottom-line, this would be possible through

1. scaling up CASA ratio to 35% with 200 bps to 300 bps improvement

every year. 2. Bank plans to take the branch network to 550 by Mar

’13. 3. Bank is expected to expand its product suite and services to

achieve higher business growth. At the CMP, stock trades at 3x FY12E

BV, we have Accumulate rating on the stock with target price of INR

320.

Industry Banking

CMP (INR) 287Target (INR) 320

52 week High/Low (INR) 292/200

Market Cap (INR BN) 133571

3M Avg. Daily Volumes 665280

P/BV FY12E 3x

Shareholding Pattern (%)

Promoters

20%

Institutions

42%

Others

14%Non-

institutions

24%

Stock Performance

150

200

250

300

350

400

J u l

S e p

N o v

J a n

M a r

M a y

J u l

IIB NSE Nifty

Performance (%)

1 Month 3 Months 1 Year

IIB 9.4% 5.7% 31.4%

NIFTY 2.5% -2.2% 5.8%* Source: Ace, Unicon Research

(INR in mn)

Particulars Actual Estimates

NII 3900 4137

Operating Profit 3117 3282

PAT 1802 1853* Source: Company, Unicon Research

AnalystShweta Rane | [email protected]

8/6/2019 Indusind Bank Q1FY12 Result Update

http://slidepdf.com/reader/full/indusind-bank-q1fy12-result-update 2/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

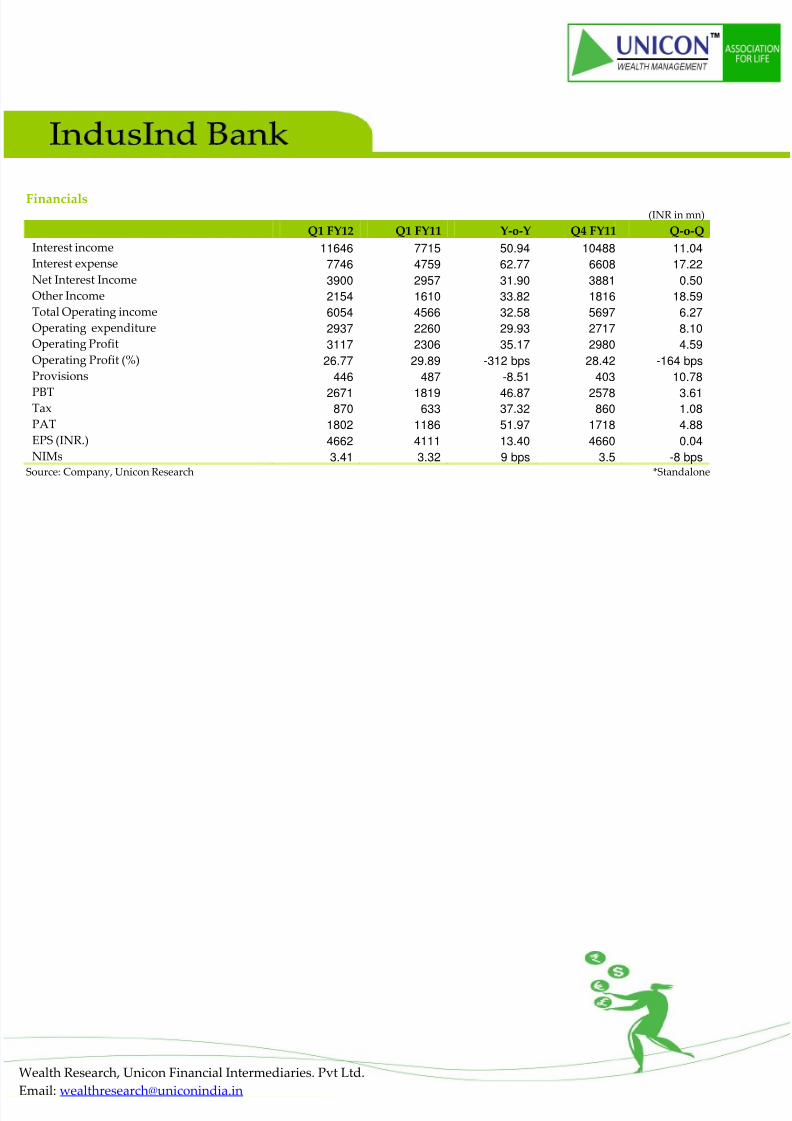

Financials(INR in mn)

Q1 FY12 Q1 FY11 Y-o-Y Q4 FY11 Q-o-Q

Interest income 11646 7715 50.94 10488 11.04

Interest expense 7746 4759 62.77 6608 17.22

Net Interest Income 3900 2957 31.90 3881 0.50

Other Income 2154 1610 33.82 1816 18.59

Total Operating income 6054 4566 32.58 5697 6.27

Operating expenditure 2937 2260 29.93 2717 8.10

Operating Profit 3117 2306 35.17 2980 4.59

Operating Profit (%) 26.77 29.89 -312 bps 28.42 -164 bps

Provisions 446 487 -8.51 403 10.78

PBT 2671 1819 46.87 2578 3.61Tax 870 633 37.32 860 1.08

PAT 1802 1186 51.97 1718 4.88

EPS (INR.) 4662 4111 13.40 4660 0.04

NIMs 3.41 3.32 9 bps 3.5 -8 bpsSource: Company, Unicon Research *Standalone

8/6/2019 Indusind Bank Q1FY12 Result Update

http://slidepdf.com/reader/full/indusind-bank-q1fy12-result-update 3/3

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

Unicon Investment Ranking Methodology

Rating Buy Accumulate Hold Reduce Sell

Return Range >= 20% 10% to 20% -10% to 10% -10% to -20% <= -20%

Disclaimer

This document has been issued by Unicon Financial Intermediaries Pvt. Ltd. (“UNICON”) for the information of its customers only. UNICON is governed by

the Securities and Exchange Board of India. This document is not for public distribution and has been furnished to you solely for your information and must

not be reproduced or redistributed to any other person. Persons into whose possession this document may come are required to observe these restrictions. The

information and opinions contained herein have been compiled or arrived at based upon information obtained in good faith from public sources believed tobe reliable. Such information has not been independently verified and no guarantee, representation or warranty, express or implied is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. This document has been produced independently of any

company or companies mentioned herein, and forward looking statements; opinions and expectations contained herein are subject to change without notice.

This document is for information purposes only and is provided on an “as is” basis. Descriptions of any company or companies or their securities mentioned

herein are not intended to be complete and this document is not, and should not be construed as an offer, or solicitation of an offer, to buy or sell or subscribe

to any securities or other financial instruments. We are not soliciting any action based on this document. UNICON, its associate and group companies its

directors or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action

taken on basis of this document, including but not restricted to, fluctuation in the prices of the shares and bonds, reduction in the dividend or income, etc. This

document is not directed to or intended for display, downloading, printing, reproducing or for distribution to or use by any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or would subject UNICON or its associates or group companies to any registration or licensing requirement within such

jurisdiction. If this document is inadvertently sent or has reached any individual in such country, the same may be ignored and brought to the attention of the

sender. This document may not be reproduced, distributed or published for any purpose without prior written approval of UNICON. This document is for

the general information and does not take into account the particular investment objectives, financial situation or needs of any individual customer, and itdoes not constitute a personalised recommendation of any particular security or investment strategy. Before acting on any advice or recommendation in this

document, a customer should consider whether i t is suitable given the customer’s particular circumstances and, if necessary, seek professional advice. Certain

transactions, including those involving futures, options, and high yield securities, give rise to substantial risk and are not suitable for all investors. UNICON,

its associates or group companies do not represent or endorse the accuracy or reliability of any of the information or content of the document and reliance

upon it is at your own risk.

UNICON, its associates or group companies, expressly disclaims any and all warranties, express or implied, including without limitation warranties of

merchantability and fitness for a particular purpose with respect to the document and any information in it. UNICON, its associates or group companies, shall

not be liable for any direct, indirect, incidental, punitive or consequential damages of any kind with respect to the document. No part of this publication may

be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise,

without the prior written permission of Unicon Financial Intermediaries Pvt. Ltd.

Address:

Wealth ManagementUnicon Financial Intermediaries. Pvt. Ltd.

VILCO Center, 2nd Floor,

8 Subhash Road, Vile Parle (E)

Mumbai 400 057Ph: 022-3390 1234

Email: [email protected]

Visit us at www.unicon.in