Indonesian Position on Bioenergy and Biorenewable Position on Bioenergy and Biorenewable Kuala...

25

Indonesian Position on Bioenergy and Biorenewable Kuala Lumpur, 14 - 16 th June 2010 The Global Sustainable Bioenergy (GSB) Convention For The Asia - Oceania Region The Department of Chemical Engineering Center for Research on Energy Policy (CREP) INSTITUT TEKNOLOGI BANDUNG Dr Retno Gumilang Dewi Presentation Outline Background Indonesian Energy Situation Indonesian Position on ‘New’ Bioenergy and Biorenewable (the Latest Development and Future Scenario) Policy Issues of Biofuel Development in Indonesia Land Use Competion (Bioenergy vs Food and Forestry) Dynamic model of future Indonesian bioenergy development Findings and Strategy

Transcript of Indonesian Position on Bioenergy and Biorenewable Position on Bioenergy and Biorenewable Kuala...

Indonesian Position onBioenergy and Biorenewable

Kuala Lumpur, 14 - 16th June 2010

The Global Sustainable Bioenergy (GSB) ConventionFor The Asia - Oceania Region

The Department of Chemical EngineeringCenter for Research on Energy Policy (CREP)

INSTITUT TEKNOLOGI BANDUNG

Dr Retno Gumilang Dewi

Presentation Outline

Background

Indonesian Energy Situation

Indonesian Position on ‘New’ Bioenergy and Biorenewable(the Latest Development and Future Scenario)

Policy Issues of Biofuel Development in Indonesia

Land Use Competion (Bioenergy vs Food and Forestry)

Dynamic model of future Indonesian bioenergy development

Findings and Strategy

BiorenewableFor Bioenergy and Biobased Product in

Indonesia

Background

Biorenewable (Bioenergy & Bioproduct)

Biorenewable biomass (organic compound generated fromplant/animal, product/waste of agriculture, plantation, forestry)

Biofuel fuel made/derived from biomass; biofuel is part ofbioenergy (including biomass-based electricity)

Among renewable energy resources, biomass is the onlyresource that can be converted in relatively direct way into fuels(to substitute petroleum fuels); other renewables (solar, wind,hydro, geotherrmal, etc) can only be converted to electricity[Soerawidjaja, 2008].

Biobased product materials/products derived from biomass(bioplastics, biosurfactant, oleochemical, bioalcohol basedolefin (replace the petrochemical product), etc)

Bio-energy and bio-renewable in “general terms” have beendeveloped and utilized in Indonesia.Palm oil waste and bagasse have long been used as energysources in crude palm oil and sugar cane mills;Wood pulp or rice stalk used as feed stock in paper mills.

Several new types of bio-energy and bio-renewable thatcurrently receives “renewed interest” in Indonesia.In bioenergy, the latest hottest issue is the development ofbiofuel (biodiesel, bioethanol, biooil, etc)Oleochemicals (CPO based) conversion to substitute petroleumbased chemicals and bioalcohol conversion to olefin are twoexamples of biorenewable (under consideration).

Bioenergy and Biorenewable in Indonesia

This discussion limited to bioenergy (biofuel)

Indonesian Energy SituationRoles of Bioenergy in Energy Supply – Demand System

GOI has relalized the importance of reducing imported oildependence main focus of energy sector is “supply security“

To full fill energy demand, Indonesia still relies on fossil energy.New-renewable is still low (4.5% or 44.55 mmboe in 2008).

Presidential Decree no.5/2006, in blue print of national energymanagement, has targeted that in 2025 share of energy mix:– new-renewable energi will increase to 17%– oil will decrease from 52 % to 20%– natural gas will increase 28 % to 30%– coal will increase from 15 % to 33%.

New–renewable energy target is bio-fuel 5%, geothermal 5%nuclear and other energy is 5%, and liquified coal is 2%.

Energy supply mix target is formulated regarding cost andresources potential (it is not ‘climate change’)

ENERGY SECURITY

Source: Data and Information Center, MEMR, 2009

Indonesian Energy Resource Potential, 2008

Fossil Energy ResourcesReserves Annual

ProductionR/P,

(Proven + Possible) year (*)

Oil 56.6 BBarels 8.2BBarels (**) 357 MBarels 23Natural Gas 334.5 TCF 170 TCF 2.7 TSCF 63Coal 104.8 Btons 18.8 Btons 229.2 Mtons 82Coal Bed Methane 453 TCF - - -(*) assuming no new discovery; (**) including Cepu Block

New and RenewableEnergy Resources Installed Capacity

Hydro 75.670 MW 4.200 MW

Geothermal 27.510 MW 1.052 MW

Mini/Micro Hydro 500 MW 86,1 MW

Biomass 49.810 MW 445 MW

Solar Energy 4,80 kWh/m2/day 12,1 MW

Wind Energy 9.290 MW 1,1 MWUranium (***) 3 GW for 11 years*) (e.q. 24,112 ton) 30 MW

***) Only at Kalan – West Kalimantan

Energy suply – demand trends

0

200

400

600

800

1000

1200

1400

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Million BOE

BiomassGeothermalHydropowerNatural GasOilCoal

Primary energy supply

Note: Growth : 3.3% per year; Biomass is used in rural household

0

50

100

150

200

250

300

350

400

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Million barrel

AMCCommerceIndustryTransportHousehold

Oil Fuels Consumption

Notes:• Mostly used in transport• Household demand will decrease significantly, substituted by LPG

0

20

40

60

80

100

120

140

160

180

200

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Million barrels

AvturDieselGasoline

Transportation fuels

Note: Other transport fuels (gas, electricity and other liquid fuels) are much smaller

Move away from oil

Figure 1

Indonesian Position on ‘New’ Bioenergy and Biorenewable(The Latest Development and Future Scenario)

The rationale of biofuels development

Developed countries : Energy supply security (resource scarcity) Greenhouse (CO2) gas emission abatement commitment

“climate change” consideration

Developing countries : Energy security (reducing oil import) Improving balance of payment Jobs creation Poverty alleviation Greenhouse (CO2) gas emission abatement

“climate change” consideration

Indonesia has changed from ‘oil exporter’ to ‘net oil importer’ Country’s potential to supply biofuel feedstock is high; area for

planting biofuel feedstock is available, agroclimate is appropriatefor biofuel plants

Biofuel technology begin to be mastered by Indonesian Biofuel industry has potential to create large employment

including farmers and therefore could function as one of thedrivers of national economy

Biofuel has high export potential Biofuel is one of renewable energy that is developed to meet

energy security and ‘non-binding commitment’ on climate changeGOI committed:

- to reduce 26% of GHG emissions from the BaU in 2020- further, to reduce 41% with international support.

The rationale of biofuels development in Indonesia

OIL BALANCE PROJECTION

Production Import

Source: National Energy Blueprint

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Juta

SBM

Produksi-BAU Ekspor-BAU Impor-Skenario Gas & CoalImpor-BAU Impor-Skenario Efisiensi Produksi-Skenario FiskalEkspor-Skenario Fiskal

Export

BAU, exportEfficiency scenario

Gas & Coal scenarioIncentive scenario

BAU, prod

Incentive scenarioBAU, import

MM

BO

E

Biomassa resources in ASEAN Countries

[Sources: Saku Rantanen (Pöyry), 2009]18

Large Potential is still unutilized!.

Source: Saku Rantanen (Pöyry), 2009

W IL M A R G R O U P3 5 0 ,0 0 0 to n /y r

B P P T3 0 0 to n /y r

P T P N 4 & G A N E S H A4 ,0 0 0 to n /y r

R A P1 ,6 5 0 to n /y r E A I

5 0 0 to n /y rS U M IA S IH

4 0 ,0 0 0 to n /y r

E T E R IN D O1 2 0 ,0 0 0 to n /y r

T O T A L 5 2 0 ,0 0 0 k ilo lite rs /y e a r (A p r il 2 0 0 7 )

F e e d s to c k : C P O

F ig u re 2 . In d o n e s ia n B io d ie s e l P ro d u c t io n

P la n 2 0 0 7 -2 0 1 1 : a d d it io n a l 3 .6 m illio n h a (p a lm o il & ja tro p h a )= 4 m illio n k L /y e a r

W IL M A R G R O U P3 5 0 ,0 0 0 to n /y r

B P P T3 0 0 to n /y r

P T P N 4 & G A N E S H A4 ,0 0 0 to n /y r

R A P1 ,6 5 0 to n /y r E A I

5 0 0 to n /y rS U M IA S IH

4 0 ,0 0 0 to n /y r

E T E R IN D O1 2 0 ,0 0 0 to n /y r

T O T A L 5 2 0 ,0 0 0 k ilo lite rs /y e a r (A p r il 2 0 0 7 )

F e e d s to c k : C P O

F ig u re 2 . In d o n e s ia n B io d ie s e l P ro d u c t io n

P la n 2 0 0 7 -2 0 1 1 : a d d it io n a l 3 .6 m illio n h a (p a lm o il & ja tro p h a )= 4 m illio n k L /y e a r

Biodiesel (CPO base) in 2010: 3,1 million ton (~ 3,6 illion kilo liter); withCPO and first generation in 2050: 30 Mton ( 219 MMBOE) in 2050.

Needed: consistant government policy to develop second generation

B P P T L A M P U N G2 5 0 0 k L /y r(c a s s a v a )

S U G A R G R O U P7 0 ,0 0 0 k L /y r(s u g a rc a n e )

M O L IN D O R A Y A1 0 ,0 0 0 k L /y r

T O T A L 8 2 ,5 0 0 k ilo lite rs /ye a r (A p r il 2 0 0 7 )

F ig u re 3 . In d o n e s ia n B io e th a n o l P ro d u c tio n

P la n 2 0 0 7 -2 0 1 0 : a d d itio n a l 1 .1 m illio n h a (c a s s a v a a n d s u g a rc a n e )= 2 – 2 .7 m illio n k L /ye a r

B P P T L A M P U N G2 5 0 0 k L /y r(c a s s a v a )

S U G A R G R O U P7 0 ,0 0 0 k L /y r(s u g a rc a n e )

M O L IN D O R A Y A1 0 ,0 0 0 k L /y r

T O T A L 8 2 ,5 0 0 k ilo lite rs /ye a r (A p r il 2 0 0 7 )

F ig u re 3 . In d o n e s ia n B io e th a n o l P ro d u c tio n

P la n 2 0 0 7 -2 0 1 0 : a d d itio n a l 1 .1 m illio n h a (c a s s a v a a n d s u g a rc a n e )= 2 – 2 .7 m illio n k L /ye a r

Future develoment: 300 thousand Kliter (~ 1,8 MMBOE/year) molassesNeeded:1.other bioethanol sources (sugar cane, cassava, nipah, aren, sagu, etc2.second generation (biomasa/selulosic based and micro algae)

Final energy demand projection(BaU, climate 1, and climate 2 scenarios)

INDONESIAN ENERGY OUTLOOK 2010 – 2030

(MEMR, 2009)

Juta SBM

-

500

1,000

1,500

2,000

2,500

3,000

BaU

Iklim

Iklim

BaU

Iklim

Iklim

BaU

Iklim

Iklim

BaU

Iklim

Iklim

BaU

Iklim

Iklim

2010 2015 2020 2025 2030

BiofuelBiomassaListrikLPGGas BumiBatubaraBBM

MMBOE

BiofuelBiomassElectricityLPGNatural GasCoalOil

Primary energy supply projection

Biofuel share in 2030: BaU 1.8% (82 million KL); Climate-14.2% (166 million KL); Climate-2 4.8% (170 miliion KL)

(MEMR, 2009)

INDONESIAN ENERGY OUTLOOK 2010 – 2030

Energy Outlook 2010 – 2050 (National Energy Board, DEN): shows thatthe share of new-renewable energy will be 35% (17% bioenergy)

(MEMR, 2009)

INDONESIAN ENERGY OUTLOOK 2010 – 2030

GHG Emissions of Energy Sector

2020: climate 1 (17.7%) and climate 2 (27.6%)2025: climate 1 (20%) and climate 2 (31.3%)2030: climate 1 (21%) and climate 2 (36%)

Nett emission will increase 1.35 to 2.95 GtCO2e (2000-2020)

0.28 0.371.00

0.040.05

0.06

0.050.05

0.43 0.29

0.130.16 0.17

0.250.39

0.83

1.44

0.06

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5E

mis

sion

(Gt C

O2e

) .

Peat EmissionWasteForestryAgricultureIndustryEnergy

1.35

1.76

2.95

2000 2005 20062020

National Appropriate Mitigation Action (NAMA)

Time

Emission under BAU

Unilateral NAMAs

Supported NAMAs

NAMAs for C-credit

Self financing but some part whichis not interest of the country have tobe supported

Rat

e of

em

issi

ons Implementation need private capital

or high investment – need TT, CB,investment support

Through market mechanism

2020

26%

41%

Non binding commitment

According to the latest development in the country, thetypes of biofuels to be developed in the country includes:-biodiesel to substitute petroleum-based diesel,-bioethanol to substitute petroleum-based gasoline,- biokerosene to substitute petroleum-based kerosene,-pure plant oil (PPO) to substitute diesel in power stations.

Government development target in 2025 for each fuel type:-biodiesel 10.22 million kL (kilo liters),-bioethanol 6.28 million kL,-biokerosene 4.07 million kL,-PPO 1.69 million kL.

National Biofuel Development Plan

Fuel 2005 - 2010 2011 - 2015 2016 - 2025

Biodiesel2.41 4.52 10.22

(10% of diesel) (15% of diesel) (20% of diesel)

Bioethanol1.48 2.78 6.28

(5% of gasoline) (10% of gasoline) (15% of gasoline)

Biokerosene 1.0 1.8 4.07

Pure Plant Oil 0.4 0.74 1.69

Total Biofuel 5.29 9.84 22.26 (*)

Biofuel Development Targets

million kilo liters

+ export : 11 million KL

(*) 5% in national energy mix

Biofuel industry characteristic is different with that of petroleum-based fuel industry (large and efficient system); new regulatoryapproach is needed

Biofuel development require cross sectoral cooperation

The current market rule of biofuel is not supportive to thedevelopment of domestic biofuel market (there is subsidy forbiofuel, but it is notsufficent for biofuel business profitable)

Unlike petroleum refineries, which is usualy large size per unit,biofuel production system in Indonesia will be much smaller insize per unit and distributed throughout the countries.Therefore, regional autonomy policy, regional government isalso expected to play major role in biofuel development

Issues to be addressed

GOI policies were formulated in Presidential Instruction & Decree:1. Presidential Instruction No.1/2006 (January 2006):

Supply and Utilization Biofuels. Instruction ordered relevant ministries& regional government to support biofuel development program.

2. Presidential Decree No.10/2006 (July 2006): Establishment ofNational Team for Acceleration of Biofuel Development forPoverty Alleviation and Creation of Employment.

GOI issued strategic policies concerning biofuel development(January 2006).

The objective of these policies:•to reduce dependency on fossil fuels•to strengthen national energy security.

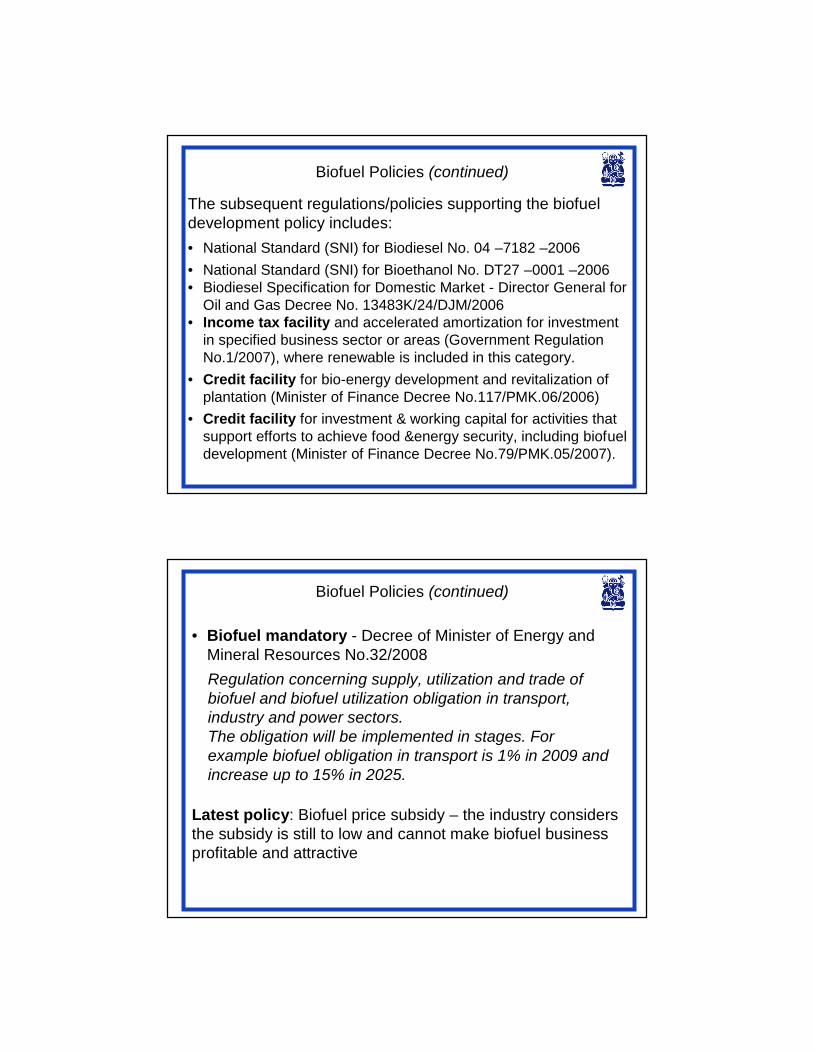

Biofuel Policies

• National Standard (SNI) for Biodiesel No. 04 –7182 –2006• National Standard (SNI) for Bioethanol No. DT27 –0001 –2006• Biodiesel Specification for Domestic Market - Director General for

Oil and Gas Decree No. 13483K/24/DJM/2006• Income tax facility and accelerated amortization for investment

in specified business sector or areas (Government RegulationNo.1/2007), where renewable is included in this category.

• Credit facility for bio-energy development and revitalization ofplantation (Minister of Finance Decree No.117/PMK.06/2006)

• Credit facility for investment & working capital for activities thatsupport efforts to achieve food &energy security, including biofueldevelopment (Minister of Finance Decree No.79/PMK.05/2007).

Biofuel Policies (continued)

The subsequent regulations/policies supporting the biofueldevelopment policy includes:

• Biofuel mandatory - Decree of Minister of Energy andMineral Resources No.32/2008

Biofuel Policies (continued)

Regulation concerning supply, utilization and trade ofbiofuel and biofuel utilization obligation in transport,industry and power sectors.The obligation will be implemented in stages. Forexample biofuel obligation in transport is 1% in 2009 andincrease up to 15% in 2025.

Latest policy: Biofuel price subsidy – the industry considersthe subsidy is still to low and cannot make biofuel businessprofitable and attractive

Consequences:

Economy (jobs, export/import)

Food vs. Fuel

Environment (GHG, local, biodiversity)

Social

Sustainability

Biofuel development Reduce oil depencence(but it is not the only outcome)

Pro-con of biofuels development in Indonesia

Land Use Competion(Bioenergy Develompent vs Food and Forestry)

G ro w in gV e g O il

L a n dV e g O ilE x p a n s io n

F o o d c ro pla n d

P ro d u c t iv eV e g O il

L a n dt o p ro d u c t iv ela n d

e x p t im e O

F o o d c ro pe x p a n s io n

E x p e c t e d la n d e x p a n s io n

S e e dp ro d u c t io n

V e g o il la n dp ro d u c t iv it y

t im e t o m a t u reF o re s t

R e f in e r ie sC a p a c it y

re n d e m e n t

re m o v in gc o n s t ru c t io n

n o rm o ile x p t im e

b io d ie s e lp ro d u c t io n

~c a p a c it yu t ilis a t io n

c o n v e r t io nc o n s t a n t

re m a in e d

f e e d s t o c ka v a ila b le V e g O il

d e m a n d

V e g e t a b leO il

S t o c k

p ro d u c t io n c o n s u m p t io n

N o rm a lS t o c k

V e g O ilL a n d

e x p e c t e df e e d s t o c k

To t a l f e e d s t o c ka v a ila ib le

p ro d u c t io nt a rg e t

f e e d s t o c kc o n s u m p t io n

To t a ls h a re

S k e n a r io

V e g O ild e m a n d

P e rc e iv e dS h a re

f e e d s t o c ks u f f ic ie n c y

u m u r e k o n o m is

S k e n a r io

a d j o f s h a re

D e s ire ds h a re

a c t u a ls h a re

a d ju s t m e n tt im e

c o n v e rt io nc o n s t a n t

~

p ro d u c t io nt a rg e t b a s e

d e s ire dc a p a c it y

p la n n e dc a p a c it y e x p a n s io n

c o n s t ru c t io n t im e

t a rg e tg ro w t h

I d leL a n d

f o re s tc o n v e r t io n

la n d c o n v e rs io n

F o o dp ro d u c t iv it y

F o o dD e m a n d

F o o dP ro d u c t io n

f o o ds u f f ic ie n c y

e x p e c t e df o o d c ro p e x p

P o p u la t io np o p g ro w t h

g ro w t h

f o o de x p t im e

f o o dp e r c a p it a

n a t u ra lp ro d u c t iv it y

t e c h n o lo g ic a le f f e c t

c o n v ra t e

S u it a b le la n df o r V e g O il

la n d f o r f o o d

F ix e d f o re s t ~e f f la n ds c a rc it y

la n d f o r o il

la n d in d e xf o o d o il

e x p e c t e do il la n d e x p

~la n d a v

e f f t o f o o d

n o rm f o o de x p t im e

~la n d a ve f f t o o

n o rm o ile x p t im e

c o n v t im e

n o rmc o n v t

~

b io e t h a n o lp ro d t a rg e t

f o o dt o b io t h a n o l

b io e t a n o lt o r ic e ra t

d e s ire da ra b le

d u ra t io no f s u f f

in it f o re s t

F o o d S u p p ly

F O O D

L A N D

B I O D I E S E L I N D U S TR Y

System Dynamics Model of Indonesian Biofuel Development

Seedproduction

Veg oil landproductiv ity

Ref ineriesCapacity

rendement

remov ingconstruction

biodieselproduction

~capacityutilisationconv ertion

constant

f eedstockav ailable Veg Oil

demand

VegetableOil

Stock

productionconsumption

NormalStock

Productiv eVeg Oil

Land

expectedf eedstock

Total f eedstockav ailaible

productiontarget

f eedstockconsumption

Totalshare

Skenario

Veg Oildemand

Perceiv edShare

f eedstocksuf f iciency

umur ekonomis

adj of share

Desiredshare

actualshare

adjustmenttime

conv ertionconstant

~

productiontarget base

desiredcapacity

plannedcapacity expansion

construction time

targetgrowth

BIODIESEL INDUSTRY

Biodiesel Industry Model

Skenario

Food cropland

Foodproductiv ity

FoodDemand

FoodProduction

f oodsuf f iciency

expectedf ood crop exp

Populationpop growth

growthf ood

per capita

naturalproductiv ity

technologicalef f ect

norm f oodexp time

~

bioethanolprod target

f oodto biothanol

bioetanolto rice rat

Food Supply

FOOD

Food sector model

GrowingVeg Oil

LandVeg Oil

Expansion

Food cropland

Productiv eVeg Oil

Landto productiv e

land

exp time O

Food cropexpansion

Expectedland expansion

time to matureForest

norm oilexp time

remained

Veg OilLand

~capacityutilisation

targetgrowth

expectedf ood crop exp

norm f oodexp time

IdleLand

f orestconv ertion

landconv ersion

f oodexp time

conv rate

Suitable landf or Veg Oil

land f or f ood

Fixed f orest ~ef f landscarcity

land f or oil

land indexf ood oil

expectedoil land exp

~land av

ef f to f ood

~land avef f to o

norm oilexp time

conv time

normconv t

desiredarable

durationof suf f

init f orest

LAND

Land utilization model

• Government’s biofuel production target in 2025 could beachieved, but with a consequence that there will be competitionbetween land use for food and for fuel production; foodproduction sector has to sacrifice (food demand has to be metwith import).

• To minimize food vs fuel competition, Indonesia has to enhanceR&D activities for improving the productivity of food productionand biofuel production technologies

• To decrease demand in land use for biofuel productionIndonesia has to begin developing technologies that is not land-demanding (second generation biofuel technology, from wastes).In addition, Indonesia has to begin consider the development ofbiofuel feedstock that is planted in water (micro algae)

Finding of the system dynamic model

Indonesia Biofuel Development Strategy

1. Develop investment and financing scheme for biofuel supplybusiness

2. Develop pricing policy/mechanism (for feedstock to biofuelproducts) that is supportive to biofuel development.

3. Increase local content/component for biofuel development.4. Improve feedstock supply system & production infrastructure5. Establish biofuel market rule6. Accelerate land acquirement for biofuel feedstock production7. Increase the participation of regional government and

community in biofuel development8. Prioritize national biofuel supply security

• To prioritize investment for biofuel plant to parties that is readywith biofuel feedstock

• To encourage private sector to invest in biofuels (domestic orabroad)

• To establish special financing for biofuel feedstock development

1. Develop investment/financing scheme for biofuel supply business

2. Develop pricing policy/mechanism (for feedstock to biofuelproducts) that is supportive to biofuel development

Indonesia Biofuel Development Strategy

3. Increase local content/component for biofuel dev.• Capacity building to master biofuel technology• To encourage the use of domestic product in biofuel businesses

4. Improve feedstock supply system and production infrastructure

• Assign jatropha curcas, sugarcane, cassava, coconut andpalm oil as the main plants for feedstock of biofuel and in themean time search and develop other potential biofuel plants

• Ensure the availability of support systems of biofuelproduction including quality seeds, fertilizers and methanol

Indonesia Biofuel Development Strategy (continued)

• Establish quality standards of biofuel as “special fuel”• Establish simple procedures for biofuel quality testing• Establish simple regulation to include biofuel as part of existing

petrofuel market system• Assign standby buyer (off taker) for biofuel feedstock& product

5. Establish biofuel market rule

6. Accelerate land acquirement for biofuel feedstock production• To use idle land, critical land, and convertible production

forest (11 million ha).• To use inactive (idle) plantation land

Indonesia Biofuel Development Strategy (continued)

7. Increase the participation of regional government and communityin biofuel development

• Facilitate the establishment of Nucleus-Plasma plantationscheme for biofuel plantation

• Develop business scheme that maximize added value to thecommunity

• Include biofuel development in regional development budget

• Impose domestic market obligation or export tax for securingdomestic biofuel supply while maintaining national andbusiness interest considerations

8. Prioritize national biofuel supply security

Total area: 49 million hectares

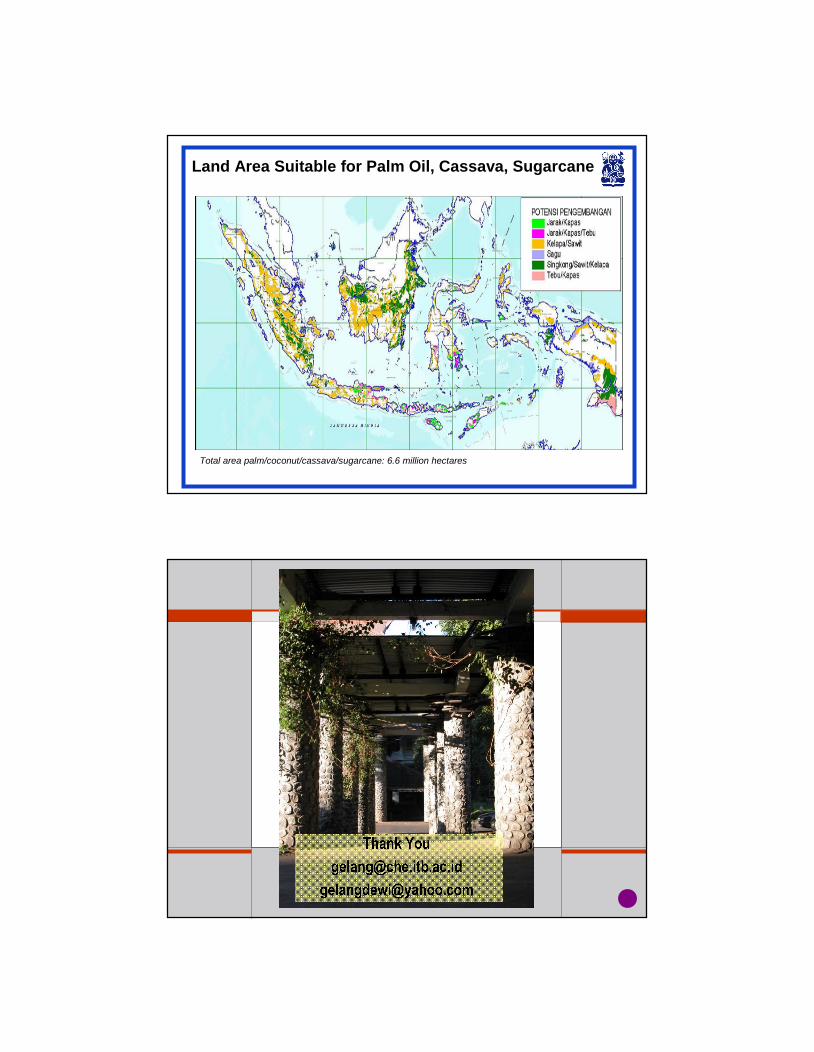

Area Suitable For Jatropha Curcas Plantation

Total area palm/coconut/cassava/sugarcane: 6.6 million hectares

Land Area Suitable for Palm Oil, Cassava, Sugarcane

Thank [email protected]

8:15 AM Tue, Nov 20, 2007

BIODIESEL

Page 12007.00 2011.50 2016.00 2020.50 2025.00

Years

1:

1:

1:

2:

2:

2:

3:

3:

3:

4:

4:

4:

0

20

401: production target base 2: biodiesel production 3: production[Palm] 4: production[Jatropha]

1

1

1

1

2

2

2

2

3

3

33

4

4

44

Biodiesel development projection

8:15 AM Tue, Nov 20, 2007

LAND

Page 22007.00 2011.50 2016.00 2020.50 2025.00

Years

1:

1:

1:

2:

2:

2:

3:

3:

3:

4:

4:

4:

0

18

361: Food crop land 2: V Oil Land 3: Idle Land 4: Convertible

1

1

1

1

2

2

2 2

3

3

33

4

44 4

Impact of biodiesel development on land use and availability

8:15 AM Tue, Nov 20, 2007

FOOD

Page 12007.00 2011.50 2016.00 2020.50 2025.00

Years

1:

1:

1:

2:

2:

2:

3:

3:

3:

0

50

1001: Food Supply 2: Food Demand 3: food to bioethanol

11

112

22

2

33

33

Impact of biofuel development on food supply