Indian home textile consumers are special: Strategies to meet their expectations.

25

Indian home textile consumers are special: Strategies to meet their expectations.

-

Upload

sibyl-fleming -

Category

Documents

-

view

217 -

download

2

Transcript of Indian home textile consumers are special: Strategies to meet their expectations.

Indian home textile consumers are special:

Strategies to meet their expectations.

Indian Retail R e f l e c t I o n s

(Source: Images – KSA Technopak Study, 2005-06)

2nd Most Attractive Developing market, ahead of China

Ranked 5th amongst the 30 “Emerging Markets” for new retailers to enter

Country with the Largest Youth population in the world- (around 80%) Over 867 million people below 45 years of age!

Indian English Linguals more than the whole of Europe put together

Over 300 million middle class - the Real consumers - is catching the attention of the world

Over 600 million Effective Consumers by 2010

India to emerge as one of the Largest Consumer Markets of the world by 2010

Indian Retail Story

India – One of the Largest Consumer Base with Diverse Charachteristics

Emerging demographic dispersion favors migration to organized retail transactions – across segments

Limited History makes it Dynamic Iterative Evolution

Late participant among the Emerging Market Peer set – to witness a compressed cycle of evolution

Business of making lesser mistakes and correcting the ones made quickly!!!

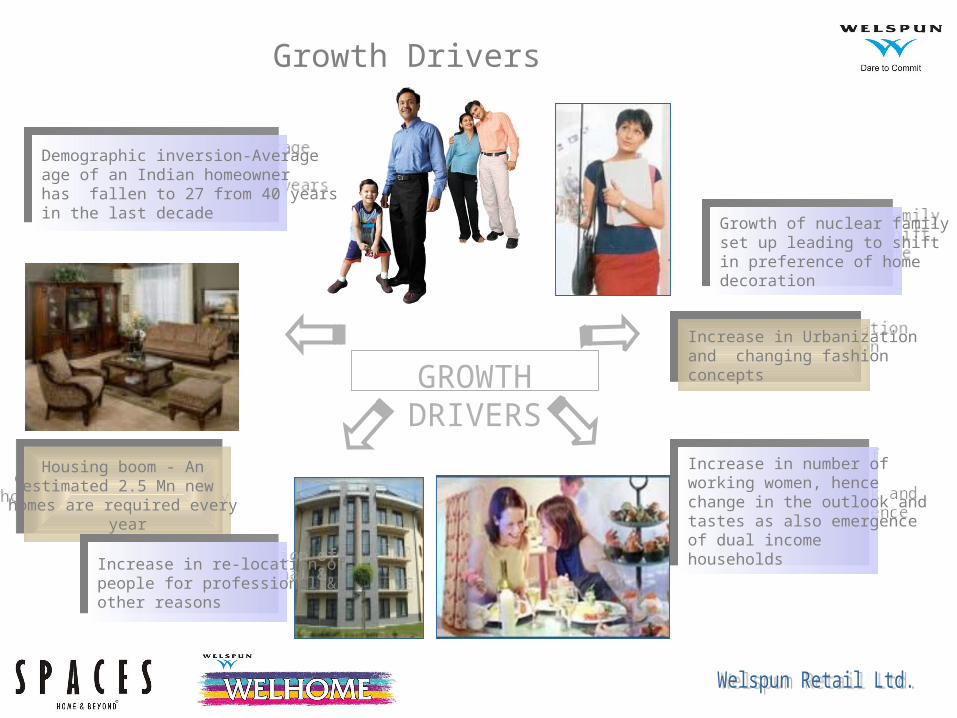

Growth Drivers

Demographic inversion-Average age of an Indian homeowner has fallen to 27 from 40 yearsin the last decade

Demographic inversion-Average age of an Indian homeowner has fallen to 27 from 40 yearsin the last decade Growth of nuclear family

set up leading to shift in preference of home decoration

Growth of nuclear family set up leading to shift in preference of home decoration

Increase in Urbanization and changing fashion concepts

Increase in Urbanization and changing fashion concepts

Increase in number of working women, hence change in the outlook andtastes as also emergence of dual income households

Increase in number of working women, hence change in the outlook andtastes as also emergence of dual income households

Housing boom - An estimated 2.5 Mn new

homes are required every year

Housing boom - An estimated 2.5 Mn new

homes are required every year

Increase in re-location of people for professional & other reasons

Increase in re-location of people for professional & other reasons

GROWTH DRIVERS

804

300

1133

427

1721

637

0

200

400

600

800

1000

1200

1400

1600

1800

GDP Retail Market

2006 2010 2015

All

fig

ure

s i

n U

S$

Bil

lio

ns

Organized retail industry is growing at more than 30% p.a

Source: Technopak Analysis, CSO, BRIC report

All Figures in Current Prices

Indian Retail T h e O p p o r t u n i t y

Organized RetailOrganized Retail

2006 2010

Unorganized Retail Unorganized Retail

Organized retail expected to gain 13% additional share over next five years

Source: Technopak Analysis

97%

3%

16%

84%

Indian Retail O r g a n i z e d

0%

20%

40%

60%

80%

100%

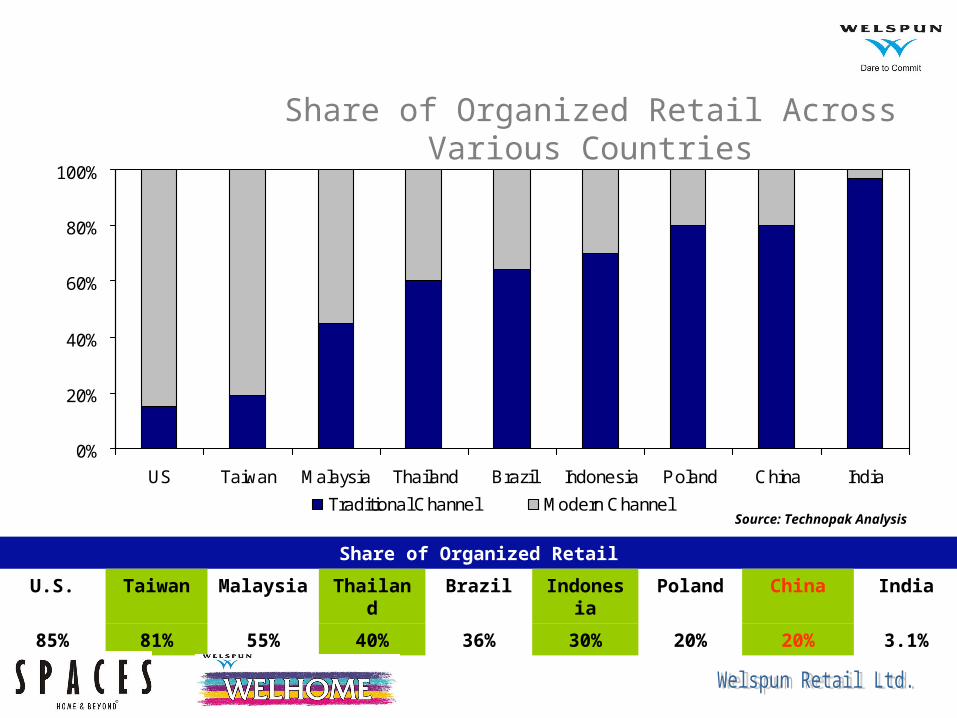

US Taiwan Malaysia Thailand Brazil Indonesia Poland China India

Traditional Channel Modern Channel

Share of Organized Retail Across Various Countries

Share of Organized Retail

U.S. Taiwan Malaysia Thailand

Brazil Indonesia

Poland China India

85% 81% 55% 40% 36% 30% 20% 20% 3.1%

Source: Technopak Analysis

Structural Growth Drivers

Different Stages in Growth of Organized Retail in India

Source: Paper on Indian Urban Retail

Gro

wth

First Gear 1995

Second Gear2004

Third Gear2007

Fourth Gear2012

New Retail Entrants Driving Growth

Consumers demand organised formats

Retailers strengthening

back end system

Retailers going globalLifestyle Retailing

Value Retailing

Create Awareness

Increase Customer Expectation

Strengthening Back-end Management

Consolidation

Indian Retail The Opportunity

Current Indian Retail Industry estimated to be at USD 300 billion

Retail Industry growing @ 5-6% p.a.

Organized Retail is at barely 3 % of the Total Retail Scenario

However it is growing @ over 30 % p.a.

Highest density of Retail Outlets in the world (12 million +)

However majority of these outlets have “shrink size” retail footage

Organized Retail is here to stay – “Key Advantages”Wide spectrum of choices in each category under one roofLocational Suitability (Accessibility & Size)Economies of Size translating into “price cuts” to the end user

Organized Retail is going to rock !! – Expected Investment commitments of over USD 25 billion in the next 5 years speak about its mammoth potential

Source: Technopak Analysis, WRL Analysis & Industry sources)

Home Retail In Focus

Home Retail is currently estimated to be at INR 9300 crore

Organized market accounts for around 6 % of the Total Home Retail

This translates into a meagre INR 550 crore + Organized Home Retail presence

However our analysis shows that the Potential for Organized Home Retail in India is over INR 8,000 crore by 2011-12

Thus a ‘Huge Potential’ of over USD 1.5 bn !!

And thus a “Great Opportunity” to foray into given thatUnorganized Local Players dominate the market - Major focus on FurnishingsNational Department Stores though present are weak in the Home category; their product profile ignores furnishings though it is a prime category with the exception of Atmosphere which caters only to Furnishings

i n f o c u s

Bath Rs 1200 Cr 13%

Curtains Rs 1000 Cr

11%

Upholstery Rs 1000 Cr, 11%

Kitchen Rs 300Cr

3%

Bed Rs 5000Cr

53%

Others, Rs 800Cr.

9%

Home Furnishings Market Size And Growth

• Urban home textiles market is estimated to be Rs 9,300 Crores

and expected to grow to Rs 20,000 Crores by 2011. Only 6% of

the market is organized.

• Bed and Bath constitute about two thirds of the market.Home Furnishing Market Size Breakup

Source: Technopak Analysis

Home Furnishings Retail Market

Structure Home Furnishing Market

Organized Market Un-organized Market

General Retailers Category SpecificRetailers

Small Niche Players(2,000-3,000 Sqft)

AUOR(5,000-10,000 Sqft)

Hypermarkets

Department Stores

Others

Small Niche Players(2,000-3,000 Sqft)

Street Markets

94%

share of market

Home Furnishings Retail Market Structure

• Retailers like Maspar, Bombay Dyeing, Welspun, Atmosphere etc. are slowly organizing the home textiles retail business especially in the metro and mini metro cities.

Unorganized• Targeted towards mass market

• Crammed and clumsy store frontage

• More emphasis on price than towards quality of merchandise

Organized• Targeted towards medium and high

end

• Emphasis on visual merchandising, branding and retail imagery and quality of merchandise on offer.

Home Furnishings Retail Market Structure

• Unorganized players are mostly in small size stores (<1000 sq ft.) selling unbranded products or export surplus. These stores are typically in high streets or furniture markets but lack any “quality retail” positioning or imagery.

Unorganized• Cluttered product display

• Dependence on store staff for showing products

Organized• In-store Visual Merchandising and

Ambience

• Emphasis on product display and customer service

Fluid Landscape

(Home Retail)Market Evolution

Retailer EvolutionBuyer Evolution

200 Mn + Households

% Spend on Home – insignificant currently –

Home is dominant high-ticket segment and hence needs special attention

Categories of preference are yet to get fully defined – making it an Iterative process

How does one buy?

What Matters to him/her!!!

What drives the Purchase – Utility/ Value/ Fashion

The Right Price Points!!!

Buying Habits and Merchandise preference are still to evolve – an iterative process

How to be consistent? Positioning/ Experience/ Delivery

How To be Relevant? Location/ Formats / Channels

How To Churn MONEY? Cash/ Profits/ ROI

Early stage of rollout-makes it an iterative process across all key variables.

Revolution~ Rapid Simultaneous Iterations Towards Change

Market Evolution

Fragmented,

Unorganized,

Limited Categories…

Consolidation,

Organization,

Wider Categories…

Forward & Backward Integration,

Strategic Complementary Initiatives

Matured Categories…

Pote

nti

al S

ale

s

Local Tier IRegional National Trade Blocs

Global

Tier I--III

WRL

Buyer Evolution

WRL

Suspect Prospect First Timer Repeat Loyal Advocate

Comes by Chance…

Comes by Choice…

Comes by Compulsion…

Right Location

Right Positioning

Right Merchandise Mix- Depth- Width

Right-Priced Merchandise

Differentiated Service/ Experience

Continuous Innovation

Avera

ge T

icket

Siz

e

(ATS

)

Retailer Evolution

WRL

Retu

rn o

n I

nvestm

en

t (R

OI)

COMPETE

COMPLEMENT

COMPLETE

No Defined Formats Format Refinement Defined Formats

Erratic Delivery Mechanism

Evolved Supply Chain Management

Product Focus & Awareness

Build Positioning & Merchandise to fit that Positioning

Take-Off with Refined Positioning & Continuous Innovation

Refined Supply Chain Management

Informal Organization

Learning Organization

Knowledge Organization

Welspun Retail Ltd…The Story so far

Novice… Reactive Participant…

Adaptive Player…

Proactive Veteran…

No Prior History

Presence of a few Established Home Brands

Different Untested Proposition

Format Refinements

Intuitive Site Selection

Merchandise Experiments

Scientific Revisit of –

• Formats

• Locations

• Brands

Segmentation

- Value

• WELHOME

- Lifestyle

• SPACES

Defined Source-code for

• Site Selection

• Merchandise

• Formats

• Pricing

Modular approach to build scale

Who is your TARGET?The one who BUYS

it ?The one who DECIDES to buy it ?

The one who USES it ?

BUYER DECISION

MAKER END USER

Challenge is to aim 3 Birds with 1 Arrow !

Sensory Appeal

Mind Share

Wallet Share

There is a fabric for every space and a space for every fabric. There is a reason to decorate, or perhaps spontaneity. For all of this, simple, elaborate, beautiful, functional and a vivid sense of

style, there is

Spaces, Home and Beyond celebrates the joie- de vivre of a young

professional, home maker and entertainer...

fulfilling the aspirations of a decorator as an Individual or Family. The brand targets

the middle and upper middle class of India’s Metros.

We retail through 2 flagship stores, MBO’s and Shop in Shops: Lifestyle, Shoppers

Stop and @ Home

The brand dwells on the many manifestations of our heritage, craftsmanship, ever evolving pioneers, maverick and bohemian tempraments. Indian perhaps, always Modern though and certainly International.

Welspun Retail Ltd…Our thoughts

SPACES – 3 %

WELHOME –22 %

A Booming Opportunity !!

SPACES – 6 mn Households

WELHOME – 46mn Households

200 mn + Households

A Multi-Dimensional Boom

Talent Boom

Real EstateBoom

Process Boom

Capital Boom

Retail Boom

FinallyHow we define a Home is evolving each day…

How we define a Home Maker is evolving each day…

How we define Home Products is evolving each day…

Home Retailers who are poised to deal with this evolving phase will strike a

Home-Run

thank you