Indian fmcg sector

58

INDUSTRY ANALYSIS PROJECT REPORT ON “Indian FMCG Sector” Masters of Business Administration (2013-2015) Submitted By: NITIN PAL SINGH

Transcript of Indian fmcg sector

INDUSTRY ANALYSIS PROJECT REPORT ON “Indian FMCG Sector” Masters of Business Administration (2013-2015)

Submitted By: NITIN PAL SINGH ANIL KUMAR

Department Of Management Faculty of Social Sciences Dayalbagh Educational Institute (Deemed University) DAYALBAGH, AGRA 282005

CONTENTS1. EXECUTIVE SUMMARY2. INTODUCTION3. ECONOMIC ANALYSIS

INDIAN GDP RATE INFLATION RISK FACTOR FOREIGN DIRECT INVESTMENT

4. INDUSTRY ANALYSIS SWOT ANALYSIS PEST ANALYSIS FIVE FORCE MODEL

5. INDUSTRY CATEGORY AND PRODUCTS6. GROWTH PROSPECT7. ADVANTAGE TO THE SECTOR8. MARKET OPPORTUNITIES9. FACTS ABOUT THE FMCG INDUSTRY10.POTENTIAL AND GROWTH OF INDUSTRY11.ROLE OF FMCG SECTOR IN INDIA12.RECENT SCENARIO13.FUTURE OF THE INDUSTRY14.COMPANY ANALYSIS

HUL DABUR INDIA P&G COLGATE PALMOLIVE

EXECUTIVE SUMMARY

Products which have a quick turnover, and relatively low cost are known as Fast Moving Consumer Goods (FMCG). FMCG products are those that get replaced within a year. Examples of FMCG generally include a wide range of frequently purchased consumer products such as toiletries, soap, cosmetics, tooth cleaning products, shaving products and detergents, as well as other non-durables such as glassware, bulbs, batteries, paper products, and plastic goods. FMCG may also include pharmaceuticals, consumer electronics, packaged food products, soft drinks, tissue paper, and chocolate bars. India’s FMCG sector is the fourth largest sector in the economy and creates employment for more than three million people in downstream activities. Its principal constituents are Household Care, Personal Care and Food & Beverages. The total FMCG market is in excess of Rs. 85,000 crores. It is currently growing at double digit growth rate and is expected to maintain a high growth rate. FMCG Industry is characterized by a well established distribution network, low penetration levels, low operating cost, lower per capita consumption and intense competition between the organized and unorganized segments. Market share movements indicate that companies such as Marico Ltd and Nestle India Ltd, with domination in their key categories, have improved their market shares and outperformed peers in the FMCG sector. This has been also aided by the lack of competition in the respective categories. Single product leaders such as Colgate Palmolive India Ltd and Britannia Industries Ltd have also witnessed strength in their respective categories, aided by innovations and strong distribution. Strong players in the economy segment like Godrej Consumer Products Ltd in soaps and Dabur in toothpastes have also posted market share improvement, with revived growth in semi-urban and rural markets.

INTRODUCTION

Products which have a quick turnover, and relatively low cost are known as Fast Moving Consumer Goods (FMCG). FMCG products are those that get replaced within a year. These products are purchased by the customers in small quantity as per the need of individual or family. These items are purchased repeatedly as these are daily use products. The price or value of the products is not very high. These products are having short life also. It may include perishable and non perishable products, durable and non durable goods. Examples of FMCG generally include a wide range of frequently purchased consumer products such as toiletries, soap, cosmetics, tooth cleaning products, shaving products and detergents, as well as other non-durables such as glassware, bulbs, batteries, paper products, and plastic goods. FMCG may also include pharmaceuticals; consumer electronics, packaged food products, soft drinks, tissue paper, and chocolate bars. A subset of FMCGs is Fast Moving Consumer Electronics which include innovative electronic products such as mobile phones, MP3 players, digital cameras, GPS Systems and Laptops. These are replaced more frequently than other electronic products. White goods in FMCG refer to household electronic items such as Refrigerators, T.Vs, Music Systems, etc.

Top 10 Companies in FMCG Sector1. Hindustan Unilever Ltd.2. ITC (Indian Tobacco Company)3. Nestlé India4. GCMMF (AMUL)5. Dabur India6. Asian Paints (India)7. Cadbury India8. Britannia Industries9. Procter & Gamble Hygiene and Health Care10. Marico Industries

ECONOMIC ANALYSIS

ECONOMY ANALYSISEconomic analysis is important in order to understand exact condition of an economy. It aims at determining if the economic climate is conducive and is capable of encouraging the growth of business sector, especially the capital market.

When the economy expands, more industry groups and companies are expected to benefit and grow. When the economy declines, most of the sectors and companies usually face survival problems. Hence, to predict share prices, an investor has to spend time exploring the forces operating in the overall economy

As India’s economy continues to grow at a rapid pace, the automobile industry will be a key beneficiary. This is widely true across automotive markets—from those serving customers with two-wheelers and four-wheelers to those offering commercial vehicles. This Booz & Company Perspective provides an analysis of growth prospects in the Indian automotive industry. The main factors behind such growth are the increasing affluence of the average consumer, overall GDP growth, the arrival of ultra-low-cost cars, and the increasing maturity of Indian original equipment manufacturers (OEMs). However, India’s path to mass motorization will be very different from that of developed countries; it must first develop the new technologies, business models, and government policies that will pave the way to increased automobile penetration. Other challenges—for example, the current global economic crisis and high commodity prices—may slow down the country in the short term, but they will not be able to stop it.

Key Features

Largest Democracy in the world – 1.18 billion people 4th largest GDP (PPP) and 11th largest GDP (Nominal) 2nd fastest growing economy (Estimate 2011-12 – 9%); India’s average

Growth rate 7.3% over past 10 years and expected to outpace China in next 10Years

3rd largest investor base in the World Robust Legal and Banking Infrastructure Demographics of Youth – 50% under 25 years & 65% under 35 years Rural to Urban Migration - 140 million by 2020; 700 million by 2050 2nd largest pool of certified professionals and highest number of qualified

Engineers in the world

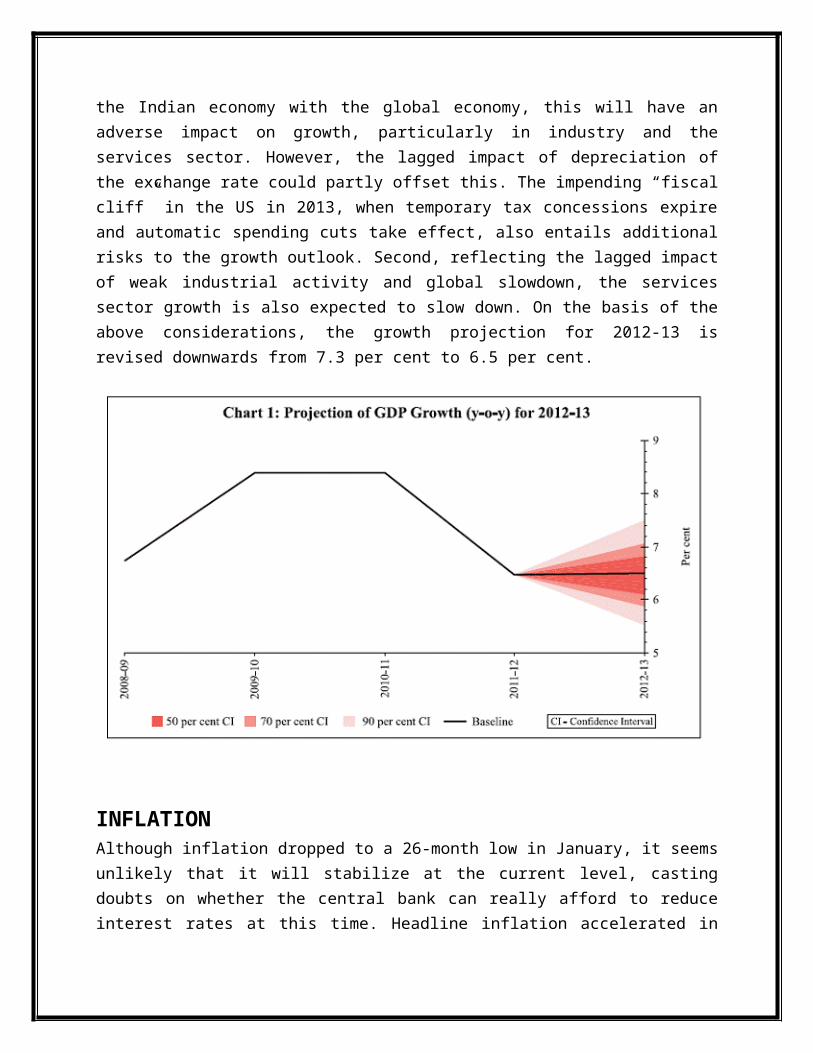

INDIA GDP GROWTH RATEGDP growth in the third quarter of the current fiscal year came in at a woeful 6.1 percent, marking a sharp drop from 7.7 percent growth in the first quarter, and 6.9 percent in the second quarter. Manufacturing growth slipped to 0.4 percent from 7.2 percent and 2.7 percent in the first and second quarters respectively. The seventh successive quarterly slowdown and the slowest growth in three years have triggered fears that the economy slowed down further in the last quarter of the current fiscal (January–March 2012) and that overall growth for the fiscal year could fall short of the downwardly revised target of about 7.0 percent. Furthermore, despite the finance minister’s exhortation that the economy will grow at about 8.0 percent in the next fiscal, it is possible that growth will stagnate at a “new normal” of about 6.0 percent unless significant efforts are made toward improving credit conditions and resurrecting investments in the coming months.In the April Policy, the Reserve Bank had projected GDP growth for 2012-13 at 7.3 per cent on the assumption of a normal monsoon and improvement in industrial activity. Both these assumptions did not hold. The monsoon has been deficient and uneven so far. Also, data on industrial production for April-May suggest that industrial activity, despite some recovery, remains weak. In addition, several risks to domestic growth have intensified. First, global growth and trade volume are now expected to be lower than projected earlier. Given the greater integration of the Indian economy with the global economy, this will have an adverse impact on growth, particularly in industry and the services sector. However, the lagged impact of depreciation of the exchange rate could partly offset this. The impending “fiscal cliff” in the US in 2013, when temporary tax concessions expire and automatic spending cuts take effect, also entails additional risks to the growth outlook. Second, reflecting the lagged impact of weak industrial activity and global slowdown, the services sector growth is also expected to slow down. On the basis of the above considerations, the growth projection for 2012-13 is revised downwards from 7.3 per cent to 6.5 per cent.

INFLATIONAlthough inflation dropped to a 26-month low in January, it seems unlikely that it will stabilize at the current level, casting doubts on whether the central bank can really afford to reduce interest rates at this time. Headline inflation accelerated in February after five months to about 7 percent. Core inflation or inflation minus the effects of food and fuel prices; fell to 5.8 percent in February. While this does mean that demand-driven inflation is falling, it could also imply that demand for manufactured goods is actually on the decline, adding credence to fears that the manufacturing sector is heading toward stagnation.Conversely, the fall in core inflation also implies a rise in food and fuel prices. After hitting near-zero inflation in January, food prices rose about 6 percent in February. Recent announcements by meteorologists predict a below-average rainfall this year, and absent any removal of supply-side bottlenecks in the agriculture sector, food inflation could spiral upward in 2012, taking overall inflation well above the government’s target level of about 7.0 percent for the rest of the year.The fiscal deficit continues to be a cause for concern. Notwithstanding last financial year’s fiscal deficit of 5.9 percent of GDP instead of the planned level of 4.6 percent, the government has set a “realistic” target of 5.1 percent for the current fiscal in the recently unveiled budget. Not only may the target be unsustainably high, the credibility of the target for the current fiscal year has already been called into question by market commentators. A large fiscal deficit surely does not bode well for inflation.

In the April Policy, the Reserve Bank made a baseline projection of WPI inflation for March 2013 of 6.5 per cent. This was based, in part, on an assumption of normal monsoon. The deficient and uneven monsoon performance so far will have an adverse impact on food inflation. Notwithstanding some moderation, international crude oil prices remain elevated. This, coupled with the pass-through of rupee depreciation to import prices, continues to put upward pressure on domestic fuel price inflation. In addition, with the adjustment of domestic prices of petroleum products to international price changes still incomplete, embedded risks of suppressed inflation could also impact fuel prices in India going forward. The decline in non-food manufactured products inflation has not been commensurate with the moderation in growth. Input price pressures on account of exchange rate movements and infrastructural bottlenecks in coal, minerals and power may exert upside pressure on non-food manufactured products inflation.Keeping in view the recent trends in food inflation, trends in global commodity prices and the likely demand scenario, the baseline projection for WPI inflation for March 2013 is now raised from 6.5 per cent, as set out in the April Policy, to 7.0 per cent.

Although inflation has remained persistently high over the past two years, it averaged around 5.5 per cent during the 2000s, both in terms of WPI and CPI, down from its earlier trend rate of about 7.5 per cent. Given this record, the conduct of monetary policy will continue to condition and contain perception of inflation in the range of 4.0-4.5 per cent. This is in line with the medium-term objective of 3.0 per cent inflation consistent with India’s broader integration into the global economy.

RISK FACTORS

The projections of growth and inflation for 2012-13 are subject to a number of risks as indicated below:

External risks to the outlook for the Indian economy are intensifying. Adverse feedback loops between sovereign and financial market stress in the euro area are resulting in increased risk aversion, financial market volatility, and perverse movements in capital flows. With the deteriorating macroeconomic situation in the euro area interacting with a loss of growth momentum in the US and in EDEs, the risks of potentially large negative spillovers have increased. India’s growth prospects too will be hurt by this.

Reflecting the setback to the global recovery as also weather-related adversities in several parts of the world, the outlook for food and commodity prices, especially crude oil, has turned uncertain. These developments have adverse implications for domestic growth and inflation.

While inflation in protein items remains elevated due to structural demand supply imbalances, additional risks to food inflation have emerged from the deficient and uneven monsoon. This has the potential of aggravating inflation and inflation expectations.

At current levels of the CAD and the fiscal deficit, the Indian economy faces the “twin deficit” risk. Financing the latter from domestic saving crowds out private investment, thus lowering growth prospects. This, in turn, deters capital inflows, making it more difficult to finance the former. Failure to narrow twin deficits with appropriate policy actions threatens both macroeconomic stability and growth sustainability.

FOREIGN DIRECT INVESTMENT

Foreign Direct Investment (FDI) in India has played an important role in the development of the Indian economy. FDI in India has in a lot of ways enabled India to achieve a certain degree of financial stability, growth and development. This money has allowed India to focus on the areas that needed a boost and economic attention, and address the various problems that continue to challenge the country.

The fast moving consumer goods (FMCG) segment is the fourth largest sector in the Indian economy. The FMCG sector generated revenues worth US$ 27.9 billion in 2010. The industry expanded at a compound annual rate of 15.4 per cent during 2006-10.

Indian and multinational FMCG players can leverage India as a strategic sourcing hub for cost-competitive product development and manufacturing to cater to the international markets. The

emergence of organized retail has boosted the distribution of FMCG sector. A total of 7.8 million retail outlets sell FMCG in India.

Industry has witnessed heavy foreign direct investment (FDI) inflows as they accounted for 2.1 per cent of the country’s total FDI during April 2000 - March 2010. Food processing is the most popular FMCG category; it attracts over 53 per cent of total FDI in the industry.

India currently allows 100 per cent FDI in cash and carry segment and 51 per cent in single-brand retail, which is expected to be further increased to 100 per cent. India is also expected to allow 51 per cent FDI in multi-brand retail, which will boost the nascent organized retail market in the country.

INDUSTRY ANALYSIS

Industrial Analysis of any industry can be done based on the following basis:

1. Five Forces Model2. PEST Analysis3. SWOT Analysis

SWOT ANALYSIS OF FMCG INDUSTRY

PEST ANALYSIS OF FMCG SECTOR

S W O T A N A L Y S I S

Pest analysis of FMCG sector in India is carried out on political, economical, social and technological aspects. It is explained below:Political:

Tax exemption in sales and excise duty for small scale industries. Transportation and infrastructure development in rural areas helps in distribution

network. Restrictions in import policies. Help for agricultural sector.

Economical: The GDP rate of Indian economy is increasing every year. It is expected in future it

would be better only in comparison with other countries. Inflation rate is increasing across the world and India is also no exception. The

government and Reserve Bank of India both are trying to control the inflation rate with the help of different measures.

Increase in disposable income has taken place due to higher GDP rate. The per capita income is increasing so the customers are having more income to spend for various reasons.

Indian FMCG sector recorded 16% sales growth in last fiscal year and it is expected it would further improve in the forthcoming years.

The FMCG sector is a 4th largest sector of Indian economy with market size of more than 60,000 crore. The Indian Territory is very large and number of customers is also very high.

Social: Demographical analysis The Indian culture, social & life styles are changing drastically. The total population is

nearly 115 crores and population includes rich, poor, middle class, male, female, located in rural, urban and sub urban areas, different level of education etc.

Technology: Technology has been simplified and available in the industry. Where technology is not

available then it is brought from foreign countries to meet FMCG sector requirements. Foreign players help in high technological development. With research and

development facilities the new technologies are developed alone or with the help of foreign players.

PORTER'S FIVE FORCES MODELPorter identified five competitive forces that shape every single industry and market. These forces help us to analyze everything from the intensity of competition to the profitability and attractiveness of an industry.

Rivalry among Competing Firms: In the FMCG Industry, rivalry among competitors is very fierce. There are scarce customers because the industry is highly saturated and the competitors try to snatch their share of market. Market Players use all sorts of tactics and activities from intensive advertisement campaigns to promotional stuff and price wars etc. Hence the intensity of rivalry is very high.

Potential Entry of New Competitors: FMCG Industry does not have any measures which can control the entry of new firms. The resistance is very low and the structure of the industry is so complex that new firms can easily enter and also offer tough competition due to cost effectiveness. Hence potential entry of new firms is highly viable.

Potential Development of Substitute Products: There are complex and never ending consumer needs and no firm can satisfy all sorts of needs alone. There are plenty of substitute goods available in the market that can be re-placed if consumers are not satisfied with one. The wide range of choices and needs give a sufficient room for new product development that can replace existing goods. This leads to higher consumers expectation.

Bargaining Power of Suppliers: The bargaining power of suppliers of raw materials and intermediate goods is not very high. There is ample number of substitute suppliers available and the raw materials are also readily available and most of the raw materials are homogeneous. There is no monopoly situation in the supplier side because the suppliers are also competing among themselves.

Bargaining Power of Consumers: Bargaining power of consumers is also very high. This is because in FMCG industry the switching costs of most of the goods is very low and there is no threat of buying one product over other. Customers are never reluctant to buy or try new things off the shelf.

INDUSTRY CATEGORY AND PRODUCTS

HOUSEHOLD CARE1. Personal Wash

The market size of personal wash is estimated to be around Rs. 8,300 Cr. The personal wash can be segregated into three segments: Premium, Economy and Popular. The penetration level of soaps is ~92 per cent. It is available in 5 million retail stores, out of which, 75 per cent are in the rural areas. HUL is the leader with market share of ~53 per cent; Godrej occupies second position with market share of ~10 per cent. With increase in disposable incomes, growth in rural demand is expected to increase because consumers are moving up towards premium products. However, in the recent past there has not been much change in the volume of premium soaps in proportion to economy soaps, because increase in prices has led some consumers to look for cheaper substitutes.

2. DetergentsThe size of the detergent market is estimated to be Rs. 12,000 Cr. Household care segment is characterized by high degree of competition and high level of penetration. With rapid urbanization, emergence of small pack size and sachets, the demand for the household care products is flourishing. The demand for detergents has been growing but the regional and small unorganized players account for a major share of the total volume of the detergent market. In washing powder HUL is the leader with ~38 per cent of market share. Other major players are Nirma, Henkel and Proctor & Gamble.

PERSONAL CARE1. Skin Care

The total skin care market is estimated to be around Rs. 3,400 Cr. The skin care market is at a primary stage in India. The penetration level of this segment in India is around 20 per cent. With changing life styles, increase in disposable incomes, greater product choice and availability, people are becoming aware about personal grooming. The major players in this segment are Hindustan Unilever with a market share of ~54 per cent, followed by Cavin Kare with a market share of ~12 per cent and Godrej with a market share of ~3 per cent.

2. Hair CareThe hair care market in India is estimated at around Rs. 3,800 Cr. The hair care market can be segmented into hair oils, shampoos, hair colorants & conditioners, and hair gels. Marico is the leader in Hair Oil segment with market share of ~ 33 per cent; Dabur occupies second position at ~17 per cent.

3. Oral CareThe oral care market can be segmented into toothpaste - 60 per cent; toothpowder - 23 per cent; toothbrushes - 17 per cent. The total toothpaste market is estimated to be around Rs. 3,500 Cr. The penetration level of toothpowder/toothpaste in urban areas is three times that of rural areas. This segment is dominated by Colgate-Palmolive with market share of ~49 per cent, while HUL occupies second position with market share of ~30 per cent. In Tooth powders market, Colgate and Dabur are the major players. The oral care market, especially toothpastes, remains under penetrated in India with penetration level ~50 per cent.

4. ShampoosThe Indian shampoo market is estimated to be around Rs. 2,700 Cr. It has the penetration level of only 13 per cent in India. Sachet makes up to 40 per cent of the total shampoo sale. It has low penetration level even in metros. Again the market is dominated by HUL with around ~47 per cent market share; P&G occupies second position with market share of around ~23 per cent. Antidandruff segment constitutes around 15 per cent of the total shampoo market. The market is further expected to increase due to increased marketing by players and availability of shampoos in affordable sachets.

FOOD & BEVERAGES1. Food Segment

The foods category in FMCG is gaining popularity with a swing of launches by HUL, ITC, Godrej, and others. This category has 18 major brands aggregating Rs. 4,600 Cr. Nestle and Amul slug it out in the powders segment. The food category has also seen innovations like softies in ice creams, ready to eat rice by HUL and pizzas by both GCMMF and Godrej Pillsbury.

2. TeaThe major share of tea market is dominated by unorganized players. More than 50 per cent of the market share is capture by unorganized players. Leading branded tea players are HUL and Tata Tea.

3. CoffeeThe Indian beverage industry faces over supply in segments like coffee and tea. However, more than 50 per cent of the market share is in unpacked or loose form. The major players in this segment are Nestlé, HUL and Tata Tea.

GROWTH PROSPECT

Large MarketIndia has a population of more than 1.150 Billions which is just behind China. According to the estimates, by 2030 India population will be around 1.450 Billion and will surpass China to become the World largest in terms of population. FMCG Industry which is directly related to the population is expected to maintain a robust growth rate.

Source: UN Population Division: Medium variant

Spending PatternAn increase is spending pattern has been witnessed in Indian FMCG market. There is an upward trend in urban as well as rural market and also an increase in spending in organ-ized retail sector. An increase in disposable income, of household mainly because of in-crease in nuclear family where both the husband and wife are earning, has leads to growth rate in FMCG goods.

Changing Profile and Mind Set of ConsumerPeople are becoming conscious about health and hygienic. There is a change in the mind set of the Consumer and now looking at “Money for Value” rather than “Value for Money”. We have seen willingness in consumers to move to evolved products/ brands, because of changing lifestyles, rising disposable income etc. Consumers are switching from economy to premium product even we have witnessed a sharp increase in the sales of packaged water and water purifier.Findings according to a recent survey by A. C. Nielsen shows about 71 per cent of Indian take notice of packaged goods labels containing nutritional information compared to two years ago which was only 59 per cent.

ADVANTAGES TO THE SECTOR

Governmental PolicyIndian Government has enacted policies aimed at attaining international competitiveness through lifting of the quantitative restrictions, reducing excise duties, and automatic foreign in-vestment and food laws resulting in an environment that fosters growth. 100 per cent ex-port oriented units can be set up by government approval and use of foreign brand names is now freely permitted.

Central & State InitiativesRecently Government has announced a cut of 4 per cent in excise duty to fight with the slowdown of the Economy. This announcement has a positive impact on the industry.But the benefit from the 4 per cent reduction in excise duty is not likely to be uniform across FMCG categories or players. The changes in excise duty do not impact cigarettes (ITC, Godfrey Phillips), biscuits (Britannia Industries, ITC) or ready-to-eat foods, as these products are either subject to specific duty or are exempt from excise. Even players with manufacturing facilities located mainly in tax-free zones will also not see material excise duty savings. Only large FMCG-makers may be the key ones to bet and gain on excise cut.

Foreign Direct Investment (FDI)Automatic investment approval (including foreign technology agreements within specified norms), up to 100 per cent foreign equity or 100 per cent for NRI and Overseas Corporate Bodies (OCBs) investment, is allowed for most of the food processing sector except malted food, alcoholic beverages and those reserved for small scale industries (SSI).There is a continuous growth in net FDI Inflow. There is an increase of about 165 per cent in Net Inflow for Vegetable Oils & Vanaspati for the year 2010.

MARKET OPPORTUNITIES

Vast Rural MarketRural India accounts for more than 700 Million consumers, or ~70 per cent of the Indian population and accounts for ~50 per cent of the total FMCG market. The working rural population is approximately 400 Millions. And an average citizen in rural India has less than half of the purchasing power as compare to his urban counterpart. Still there is an untapped market and most of the FMCG Companies are taking different steps to capture rural market share. The market for FMCG products in rural India is estimated ~ 52 per cent and is projected to touch ~ 60 per cent within a year. Hindustan Unilever Ltd is the largest player in the industry and has the widest market coverage.

Export - “Leveraging the Cost Advantage”Cheap labor and quality product & services have helped India to represent as a cost ad-vantage over other Countries. Even the Government has offered zero import duty on capital goods and raw material for 100% export oriented units. Multi National Companies out-source its product requirements from its Indian company to have a cost advantage. India is the largest producer of livestock, milk, sugarcane, coconut, spices and cashew apart from being the second largest producer of rice, wheat, fruits & vegetables. It adds a cost advantage as well as easily available raw materials.

Sectoral OpportunitiesMajor Key Sectoral opportunities for Indian FMCG Sector are mentioned below:

Dairy Based ProductsIndia is the largest milk producer in the world, yet only around 15 per cent of the milk is processed. The organized liquid milk business is in its infancy and also has large long-term growth potential. Even investment opportunities exist in value-added products like desserts, puddings etc.

Packaged FoodOnly about 10-12 per cent of output is processed and consumed in packaged form, thus highlighting the huge potential for expansion of this industry.

Oral CareThe oral care industry, especially toothpastes, remains under penetrated in India with penetration rates around 50 per cent. With rise in per capita incomes and awareness of oral hygiene, the growth potential is huge. Lower price and smaller packs are also likely to drive potential up trading.

Beverages

Indian tea market is dominated by unorganized players. More than 50% of the market share is capture by unorganized players highlighting high potential for organized players.

FACTS ABOUT THE FMCG INDUSTRY

FMCG, otherwise known as CPG, is one of the biggest industries in the world and there are a lot of facts that stand the FMCG industry apart as a career choice:

FMCG companies are behind the biggest brands in the world. FMCG is all about names, the products which everyone recognizes from trips to the supermarket or from ads on television. The brands that make up this sector are the high profile ones, the ones everybody knows and loves. Think Coca-Cola, Dettol and Dove. This is an industry that puts you in living rooms, kitchens and bathrooms across the globe.

The FMCG industry changes fast and is constantly evolving. It's fair to say there is never a dull moment in FMCG. From the pace at which goods leave the shelves to the rate of product innovation and career progression, things move quickly. And it doesn't end there. The brands themselves are changing just as quickly. 40% of brands on the top 100 list twenty years ago have already been replaced by new names today.

FMCG firms thrive on employee and customer retention. Employee investment is a big part of the ethos of the FMCG world. Perhaps it's because we understand the importance of loyalty. Customer loyalty can make or break a brand. Take Twinings, for example – a century after they entered the top 100 brand list, they are still there and going strong. So it makes sense for FMCG companies to encourage the loyalty of their employees too.

FMCG companies can beat the recession. This is an industry that has proved itself very resilient to recession – with the majority of companies in the sector weathering the financial storm in a way that very few others have managed. Why? Well, consumers will always need to buy the products created by FMCG companies. They may not buy big items like refrigerators or cars in a recession, but floors still need to be cleaned, clothes need to be laundered and aches and pains still need to be soothed.

The FMCG industry thinks bigger – and better. This is an industry that offers things on a whole new scale. Where else could you find yourself handling $150 million accounts? Working in FMCG gives you the chance to be a part of some global success stories and influence the way consumers shop for products. FMCG firms are always thinking of the next great discovery or

innovation – always developing and ever-changing to meet consumer's needs.

FMCG has a history of delivering what consumers want. Some FMCG companies' roots are over two centuries old – driving the industry to a value of $570.1 billion. In short, to quote Sam Walton, founder of Wal-Mart: "High expectations are the key to everything".

POTENTIAL AND GROWTH OF INDUSTRYWith the presence of 12.2% of the world population in the villages of India, the Indian rural FMCG market is something no one can overlook. Increased focus on farm sector will boost rural incomes, hence providing better growth prospects to the FMCG companies. Better infrastructure facilities will improve their supply chain. FMCG sector is also likely to benefit from growing demand in the market. Because of the low per capita consumption for almost all the products in the country, FMCG companies have immense possibilities for growth. And if the companies are able to change the mindset of the consumers, i.e. if they are able to take the consumers to branded products and offer new generation products, they would be able to generate higher growth in the near future. It is expected that the rural income will rise in 2007, boosting purchasing power in the countryside. However, the demand in urban areas would be the key growth driver over the long term. Also, increase in the urban population, along with increase in income levels and the availability of new categories, would help the urban areas maintain their position in terms of consumption. At present, urban India accounts for 66% of total FMCG consumption, with rural India accounting for the remaining 34%. However, rural India accounts for more than 40% consumption in major FMCG categories such as personal care, fabric care, and hot beverages. In urban areas, home and personal care category, including skin care, household care and feminine hygiene, will keep growing at relatively attractive rates. Within the foods segment, it is estimated that processed foods, bakery, and dairy are long-term growth categories in both rural and urban areas.

ROLE OF FMCG SECTOR IN INDIAThe Indian FMCG sector is the fourth largest sector in the economy with a total market size in excess of US$ 13.1 billion. It has a strong MNC presence and is characterized by a well established distribution network, intense competition between the organized and unorganized segments and low operational cost. Availability of key raw materials, cheaper labor costs and presence across the entire value chain gives India a competitive advantage. The FMCG market is set to treble from US$ 11.6 billion in 2003 to US$ 33.4 billion in 2015. Penetration level as well as per capita consumption in most product categories like jams, toothpaste, skin care, hair wash etc in India is low indicating the untapped market potential. Burgeoning Indian population, particularly the middle class and the rural segments, presents an opportunity to makers of branded products to convert consumers to branded products. Growth is also likely to come from consumer 'upgrading' in the matured product categories. With 200 million people

expected to shift to processed and packaged food by 2010, India needs around US$ 28 billion of investment in the food-processing industry. The FMCG sector witnessed robust year-on-year growth of approximately 11 per cent in the last decade, almost tripling in size from Rs 47,000 crore in 2000-01 to Rs 130,000 crore now (it accounts for 2.2 per cent of the country’s GDP). Growth was even faster in the past five years — almost 17 per cent annually since 2005. It identifies robust GDP growth, opening up of rural markets, increased income in rural areas, growing urbanization along with evolving consumer lifestyles and buying behaviors as the key drivers of this growth.

RECENT SCENARIOThe Indian FMCG sector with a market size of US$13.1 billion is the fourth largest sector in the economy. A well-established distribution network, intense competition between the organized and unorganized segments characterizes the sector. FMCG Sector is expected to grow by over 60% by 2010. That will translate into an annual growth of 10% over a 5-year period. It has been estimated that FMCG sector will rise from around Rs 56,500 crores in 2005 to Rs 92,100 crores in 2010.

FUTURE OF THE INDUSTRYFast moving consumer goods will become Rs 400,000-crore industry by 2020. Consumption patterns have evolved rapidly in the last five to ten years. The consumer is trading up to experience the new or what he hasn’t. He’s looking for products with better functionality, quality, value, and so on. What he ‘needs’ is fast getting replaced with what he ‘wants’? A new report by Booz & Company for the Confederation of Indian Industry (CII), called FMCG Roadmap to 2020: The Game Changers, spells out the key growth drivers for the Indian fast moving consumer goods (FMCG) industry in the past ten years and identifies the big trends and factors that will impact its future.

COMPANY ANALYSIS

COMPANIES IN INDIAN FMCG SECTOR

Indian market is a big market and its population is nearly 115 croers. The markets are of different types and can be segmented as urban, sub- urban and rural markets. The rural market is very wide and still it is difficult to cover. Nearly 70 percent of Indian population is living in rural areas. There is a great opportunity for FMCG companies in Indian markets. Further due to liberalization a good number of MNCs have entered in India market and mainly in FMCG sector also. They have entered in skin care, toothpaste, toiletries, fast-food, chocolates, cosmetics and many other products. The FMCG sector is flooded by companies from India and abroad. In future the level of competition would increase further. The situation in Indian economy is very favorable for foreign companies. The major factors attractive them are availability of raw materials, low labor cost, market potential for consumption and more disposable income of Indian customers. More over the GDP in Indian economy is increasing every year so per capita income increasing and there is scope for further development. At present large and small companies are operating in Indian FMCG sector. Some of the major players in FMCG sector are explained below:

HINDUSTAN UNILEVER LIMITED

Hindustan Unilever Limited (HUL), earlier called Hindustan Lever Limited (HLL) was established in 1933 as Lever Brothers India Limited. Hindustan Lever Limited (HLL) is India's largest Fast Moving Consumer Goods Company, with a customer base of 2 out of every 3 Indian in the category of Home & Personal Care Products and Foods & Beverages. The company has combined volumes of about 4 million tonnes and sales of Rs.10, 000 crores. HLL is also one of the country's largest exporters; the Government of India has recognized HLL as a Golden Super Star Trading House.

The Hindustan Lever Research Center (HLRC) was established in 1958, and now has facilities in Mumbai & Bangalore. HLRC has 200 highly qualified scientists and technologists, many of them with post-doctoral experience. HLL also runs various ambitious programmes like Shakti. Shakti's aim is to create opportunities for rural women thereby improving their livelihood and standard of living in rural sector. Shakti also includes health and hygiene education through the Shakti Vani Programme.

The programme covers about 50,000 villages in 12 states. HLL's motive is to take this programme to 100,000 villages influencing the lives of over a 100 million rural Indians. HLL is also involved in running a rural health programme - Lifebuoy Swasthya Chetana. The programme aims to inculcate the hygienic practices among rural Indians to bring down the figure of diarrhea patients. It has already covered 70 million people in approximately 15000 villages of 8 states.

PRODCUTS

Some of HUL brands are:

Kwality Walls Ice Cream Hamam Lifebuoy Rexona Lux Liril Moti Soaps Breeze Lipton Tea Brooke Bond Tea Bru Coffee

Pepsodent Close Up Surf Rin Wheel Laundry Detergent Kissan Annapurna Pond's Vaseline Fair & Lovely Lakmé Clinic Plus Clinic All Clear Sunsilk and Lux Shampoos Vim Ala Bleach Domex Pureit Water Purifie

SWOT ANALYSISSWOT analysis of HUL is carried as follows:Strengths:

HUL has presence across the world and coverage is very wide. It has its established distribution network in urban, suburban and rural areas in India.

Financial position of the company is very strong. Enjoying very high reputation in markets with popular brands in the FMCG sector. Low cost operations in India due to favorable factors.

Weaknesses: Export of its products is low because it has its units across the world.

Opportunities: Indian market is very large and still it is uncovered. Export potential is there and can be utilized. Opportunity for boosting sales and revenue is very good.

Threats: Imports from China at lower cost creating difficulty. Tax and regulatory structure of Indian government are to be followed Slowdown in demand due to local factors in India economy.

Tough competition is being faced from local and international players in markets.

Dabur India Limited

HistoryDabur India Limited is a leading Indian consumer goods company with interests in Hair Care, Oral Care, Health Care, Skin Care, Home Care and Foods. From its humble beginnings in the by lanes of Calcutta way back in 1884 as an Ayurvedic medicines company, Dabur India Ltd has come a long way today to become a leading consumer products manufacturer in India. For the past 125 years, we have been dedicated to providing nature-based solutions for a healthy and holistic lifestyle. Through our comprehensive range of products, we touch the lives of all consumers, in all age groups, across all social boundaries. And this legacy has helped us develop a bond of trust with our consumers. That guarantees you the best in all products carrying the Dabur name. With a basket including personal care, health care and food products, Dabur India Limited has set up subsidiary Group Companies across the world that can manage its businesses more efficiently. Given the vast range of products, sourcing, production and marketing have been divested to the group companies that conduct their operations independently. Dabur's mission of popularizing a natural lifestyle transcends national boundaries. Today, there is growing global awareness on alternative medicine, nature-based and holistic lifestyles and an interest in herbal products. Dabur has been in the forefront of popularizing this alternative way of life, marketing its products in more than 60 countries all over the world. Over the years, Dabur's overseas business has successfully transformed from being a small operation into a multi-location business spreading through the Middle East, North Africa, West Africa and South Asia. Dabur has spread itself wide and deep to be close to our overseas consumers. Overseas product portfolio is tailor-made to suit the needs and aspirations of our growing consumer base in the international markets. Strategic partnerships with leading multinational food and health care companies to introduce innovations in products and services. Six modern manufacturing facilities spread across South Asia, Middle East and Africa to optimize production by utilizing local resources and the most modern technology available. The journey of the company stated in 1884 and it was founded by Doctor Burman and after his name the name Dabur derived. Dr. Burman was a young and qualified person took venture to start this company. It started humbly and developed to a leading manufacturer of consumer healthcare, personal care and food products. At present it has over 125 years of proven track record of business. Under one brand name Dabur it has marketed a variety of products, ranging from hair care to honey, oil, chyawanprash, Amla, Vatika, Hajmola and Real. The company is taking care of young and old generation demands into mid for development of products. It is having its manufacturing plants mainly in hilly areas where it can get the raw materials of herbs for production of ayurvedic medicines and other products. In 1936 Dr. Burman established Dabur India Limited. From its beginning it has launched many products and these are doing successful business in Indian as well as foreign markets on the basis of trust and loyalty. The products are consumer friendly with almost no side effects on human body. This company has development its own research laboratory for development and testing of the products. The future of the company is very bright at least in Indian markets.

Products of Dabur

Dabur India Limited is a leading Indian consumer goods manufacturer of Hair Care, Oral Care, Health Care, Skin Care, Home Care and Foods. The company is committed to provide natural solution healthy and holistic lifestyle. The products are herbal based and very friendly to the health without any adverse effects. The company is manufacturing a variety of products and marketing with trust and on the basis of loyalty of customers in India and abroad. Through research and development facilities the products are developed as per the emerging demands of the customers. Dabur is manufacturing products and medicines related to ayurvedic area. It is having a long list of its products for customers to use. The list of the products is appended below;

Hair care products: Dabur amla hair oil, Dabur hair oil sikakai, Dabur vatika hair oil, Dabur amla hair oil lite, Dabur special hair oil, Dabur jasmine hair oil, Dabur jasmine hair oil, Parachute coconut oil, Cocoraj coconut oil , Dabur anmol coconut oil

Soaps: Dabur neem soap, Dabur sandalwood soap, Dabur sandalwood soap, Dabur aloe vera soap

Ayurvedic medicines: Dabur hajmola tablets, Dabur shilajit health tonic, Dabur hingwastak churan, Dabur nature care triphla. Dabur hajmola candy, Dabur herbal toothpaste, Basil,Sat isabgol, Dabur nature care triphla, Dabur hingwastak churan, Dabur lavan bhaskar churan,Dabur honey, Dabur sitopaladi churan, Dabur pudin hara pearls

Dabur healthcare products: Dabur chyawanprakash - sugar free, Dabur chyawanshakti - energy food, Dabur chyawanprash, , Dabur chyawan junior, Chocolate flavoured health drinkfor kids.

SWOT Analysis of Dabur India

SWOT is the process and it stands for Strengths, Weaknesses, Opportunities and Threats, and is an important tool often used to highlight where a business or organization is, and on the basis of this the company can take the strategic decisions for the business in the future. It looks at internal factors, the strengths and weaknesses of a business, and external factors, the opportunities and threats facing the business. This process highlights strength, weakness, opportunities in the markets and threats to the business of the company.

The SWOT analysis of Dabur would make the position of the company clear and it can assess the capacity of the company and the market positions for the business. The SWOT process for Dabur is carried out as follows:

Strengths: It highlights the plus points of the company internally. It shows the position of the company relating to its resources, management approach etc. On the basis of this management can dare to take further steps. The strengths of the company are:

Support from leading businesses houses from abroad. Financial position of the company is sound. Research and development facilities are adequate for further development of the

products. Market position is well maintained Niche marketing strategy is doing well.

Weaknesses: The impact of Dabur products is slow and of low quality and that is to be improved; Production and operating costs are higher and these reduce the profits of the company. Dabur India’s R&D facilities are comparatively inadequate and needs improvements. In experienced staff sometimes creating problems and giving weak performance. Old and outdated technologies not helping in production of more production of higher

quality. Lack of innovative approach in the company exists.

Opportunities Indian market is very wide and having great potential for further development. The knowledge of the company regarding customers and there profile is good. The availability of raw materials and low labour cost is another opportunity. Less level of competition is herbal based products

Threats Export expansion chances are very less. Competition is slowly increasing and for further it would be threat. Higher inflation increasing the total costs

Recent Performance

Dabur India limited is one of the leading companies in India producing herbal products mainly. Its progress is very attractive and hopes it would maintain in future also. It has a large number of products in its portfolio and developing further also. It has its business in India as well as in other countries outside of India. In recent past worldwide economies were facing recession so the demands of the products of MNCs were down whereas the demand, sales, revenue and profit of this company did not fall. Sincere efforts of the management are there to sustain its growth rate further also.

PROCTER & GAMBLE Hygiene and Health Care

HISTORYThe Procter & Gamble Company (P&G) is a giant in the area of consumer goods. The leading maker of household products in the United States, P&G has operations in nearly 80 countries around the world and markets its nearly 300 brands in more than 160 countries; more than half of the company's revenues are derived overseas. Among its products, which fall into the main categories of fabric care, home care, beauty care, baby care, family care, health care, snacks, and beverages, are 16 that generate more than $1 billion in annual revenues: Actonel (osteoporosis treatment); Always (feminine protection); Ariel, Downy, and Tide (laundry care); Bounty (paper towels); Charmin (bathroom tissue); Crest (toothpaste); Folgers (coffee); Head & Shoulders, Pantene, and Wella (hair care); Iams (pet food); Olay (skin care); Pampers (diapers); and Pringles (snacks). Committed to remaining the leader in its markets, P&G is one of the most aggressive marketers and is the largest advertiser in the world. Many innovations that are now common practices in corporate America--including extensive market research, the brand-management system, and employee profit-sharing programs--were first developed at Procter & Gamble.

PRODUCTSSince its founding in 1837, Procter & Gamble has become the world's largest consumer product manufacturer, with a lineup of famous brands. The brands are sold through three global business units and include Tide laundry detergent, Charmin toilet paper, Pantene shampoo, Cover Girl cosmetics, Folgers coffee, and Iams pet food. P&G completed its acquisition of Gillette in October 2005 and since 2001 it has doubled the sales it derives from developing markets Ad brands coverage of Procter & Gamble is split across several different pages. As of July 2006, the group operates three main global business units: P&G Beauty, P&G Household Care and P&G Global Health & Well Being. In addition, Ad brands tracks several geographic units: Procter & Gamble Latin America and Procter & Gamble Europe, as well as Procter & Gamble UK, Procter & Gamble Germany, Procter & Gamble France; Procter & Gamble India and Procter & Gamble Japan. Individual brands covered include Pampers, Gillette, Charmin, Crest, Iams, Clairol, Always, Tampax, Olay, Pantene, Wella, P&G Prestige Products, Tide / Ariel, Folgers and Pringles. The list of products of the company is given below:Fabric care

Ariel Front-O-Mat Ariel 2 Fragrances Tide Detergent Tide Bar

Hair care Pantene Pro V Head & Shoulders Rejoice

Baby care Pampers

Health care Vicks Tablets Vicks cough syrup Vicks vaporub Vicks Formula 44 Vicks Inhaler

SWOT ANALYSISSWOT analysis of the company is as follows:Strengths:

In India the distribution network is strong upto suburban areas. Products and brands of the company are more preferred by the customers. Low cost operations due to better technology and well managed workforce. Competent employees at all levels to handle the competitive situation in markets.

Weaknesses: Export of the company is limited. Difficult to develop image of the products in the beginning in Indian markets. No major weakness of the company has been noticed so far.

Opportunities: Large increasing domestic market with future potential to grow. Export potential can be utilized by the company. Cost competitive advantage to the company due to favorable factors in economy. Opportunity to increase sales, revenue, profits and image of the company.

Threats: Imports from low cost producing countries like China giving tough competition. Tax exemption is not available much. Slowdown in demand due to inflation, draughts and recession in economy. Poor transportation and infrastructure in rural markets.

PROCTER & GAMBLE COMPANY

HISTORYThe Procter & Gamble Company (P&G) is a giant in the area of consumer goods. The leading maker of household products in the United States, P&G has operations in nearly 80 countries around the world and markets its nearly 300 brands in more than 160 countries; more than half of the company's revenues are derived overseas. Among its products, which fall into the main categories of fabric care, home care, beauty care, baby care, family care, health care, snacks, and beverages, are 16 that generate more than $1 billion in annual revenues: Actonel (osteoporosis treatment); Always (feminine protection); Ariel, Downy, and Tide (laundry care); Bounty (paper towels); Charmin (bathroom tissue); Crest (toothpaste); Folgers (coffee); Head & Shoulders, Pantene, and Wella (hair care); Iams (pet food); Olay (skin care); Pampers (diapers); and Pringles (snacks). Committed to remaining the leader in its markets, P&G is one of the most aggressive marketers and is the largest advertiser in the world. Many innovations that are now common practices in corporate America--including extensive market research, the brand-management system, and employee profit-sharing programs--were first developed at Procter & Gamble.

PRODUCTSSince its founding in 1837, Procter & Gamble has become the world's largest consumer product manufacturer, with a lineup of famous brands. The brands are sold through three global business units and include Tide laundry detergent, Charmin toilet paper, Pantene shampoo, Cover Girl cosmetics, Folgers coffee, and Iams pet food. P&G completed its acquisition of Gillette in October 2005 and since 2001 it has doubled the sales it derives from developing markets Ad brands coverage of Procter & Gamble is split across several different pages. As of July 2006, the group operates three main global business units: P&G Beauty, P&G Household Care and P&G Global Health & Well Being. In addition, Ad brands tracks several geographic units: Procter & Gamble Latin America and Procter & Gamble Europe, as well as Procter & Gamble UK, Procter & Gamble Germany, Procter & Gamble France; Procter & Gamble India and Procter & Gamble Japan. Individual brands covered include Pampers, Gillette, Charmin, Crest, Iams, Clairol, Always, Tampax, Olay, Pantene, Wella, P&G Prestige Products, Tide / Ariel, Folgers and Pringles. The list of products of the company is given below:Fabric care

Ariel Front-O-Mat Ariel 2 Fragrances Tide Detergent Tide Bar

Hair care Pantene Pro V Head & Shoulders Rejoice

Baby care Pampers

Health care Vicks Tablets Vicks cough syrup Vicks vaporub Vicks Formula 44 Vicks Inhaler

SWOT ANALYSISSWOT analysis of the company is as follows:Strengths:

In India the distribution network is strong upto suburban areas. Products and brands of the company are more preferred by the customers. Low cost operations due to better technology and well managed workforce. Competent employees at all levels to handle the competitive situation in markets.

Weaknesses: Export of the company is limited. Difficult to develop image of the products in the beginning in Indian markets. No major weakness of the company has been noticed so far.

Opportunities: Large increasing domestic market with future potential to grow. Export potential can be utilized by the company. Cost competitive advantage to the company due to favorable factors in economy. Opportunity to increase sales, revenue, profits and image of the company.

Threats: Imports from low cost producing countries like China giving tough competition. Tax exemption is not available much. Slowdown in demand due to inflation, draughts and recession in economy. Poor transportation and infrastructure in rural markets.

COLGATE PALMOLIVE (India) LIMITED

HISTORYIn 1806, William Colgate, himself a soap and candle maker, opened up a starch, soap and candle factory on Dutch Street in New York City under the name of "William Colgate & Company". In the 1840s, the firm began selling individual cakes of soap in uniform weights. In 1857, William Colgate died and the company was reorganized as "Colgate & Company" under the management of Samuel Colgate, his son. In 1872, Colgate introduced Cashmere Bouquet, a perfumed soap. In 1873, the firm introduced its first toothpaste, aromatic toothpaste sold in jars. His company sold the first toothpaste in a tube, Colgate Ribbon Dental Cream, in 1896. By 1908 they initiated mass selling of toothpaste in tubes. In Milwaukee, Wisconsin, the "B.J. Johnson Company" was making a soap entirely of palm and olive oil, the formula of which was developed by B.J. Johnson in 1898. The soap was popular enough to rename their company after it - "Palmolive".Colgate-Palmolive has long been in fierce competition with Procter & Gamble, the world's largest soap and detergent maker. P&G introduced its Tide laundry detergent shortly after World War II and thousands of consumers turned from Colgate's soaps to the new product. Colgate lost its number one place in the toothpaste market when P&G started putting fluoride in its toothpaste. In the beginning of television, "Colgate-Palmolive" wished to compete with Procter & Gamble as a sponsor of soap operations.From a modest start in 1937, when hand-carts were used to distribute Colgate Dental Cream, Colgate-Palmolive (India) Ltd. today has one of the widest distribution networks in India – a logistical marvel that spans around 3.5 million retail outlets across the country, of which the Company services 9.40,000 outlets directly. The Company has grown to Rs. 1475 crores plus with an outstanding record of enhancing value for its strong shareholder base. Colgate's strong focus on Oral Care in India while building its Personal Care business coupled with a simple, but sound worldwide financial strategy, has helped deliver consistent shareholder value. Colgate consistently increases gross margin while at the same time reducing overhead expenses. The increase in gross margin and the reduction in overhead expenses provide the money to invest in advertising to support the launch of new brands.

PRODUCTSThe Company is manufacture different types of products taking care of most of the segment of the population. The list of products includes toothpastes, toothbrushes. Toothpowders, whitening products, kids products, mouth wash products, body wash, hand wash , hair care, skin care, shaving creams, professional oral care and many other products. The list is given below:Toothpastes:

Colgate Dental Cream

Colgate Max Fresh Colgate Active Salt Colgate Total 12 Colgate Sensitive Colgate Kids Colgate Advanced Whitening Colgate Herbal Colgate Cibaca Colgate Fresh Energy Gel Colgate Max white

Toothbrushes: Colgate Massager Colgate Navigator Plus Colgate Extra Clean Gum Care Colgate Sensitive Toothbrush Colgate 360 Toothbrush Colgate Zig Zag

Body wash: Palmolive Aroma Body wash Relaxing Palmolive Thermal Spa Body wash Firming Palmolive Aroma Body wash Vitality Palmolive Thermal Spa Body wash Massage Palmolive Naturals Moisturizing Body wash Milk & Almond Palmolive Naturals Moisturizing Body wash Milk & Honey

Liquid hand wash: Palmolive Naturals Milk and Honey Hand Wash Palmolive Aroma Liquid Hand Wash Relaxing Palmolive Naturals Liquid Hand Wash Family Health

Other products:The list of other products includes;

Hair Care-Palmolive Halo Shampoo Skin Care -Palmolive Charmis Cream Saving Cream -Shave Cream Home Care-Axion - Dish Washing Paste Sensitivity Treatment -Colgate Sensitive, Colgate Gel Kam Tooth Whitening-Colgate Visible White Fluoride Therapy -Phos Flur Mouth Ulcer Treatment -Oragard-B

Specialty Cleaning-Specialty Cleaning Toothpowder-Colgate Super Rakshak Whitening Products-Colgate Advanced Whitening

SWOT ANALYSISA name synonymous with the Indian oral care industry is the undisputed market leader in toothpastes with over 45% share in the Rs 21 bn (90,000 TPA) oral care segment. The company's parent has a presence in over 200 countries worldwide:Strengths:

Well-established distribution network extending to urban, sub urban and rural areas. The products of the company are reaching to the customers even in rural areas.

Strong brands in the FMCG sector especially of toothpaste, tooth brush and creams. The brands are taken as products in the market.

Low cost operations due to availability of raw materials and workers for their factories.Weaknesses:

Low export levels because facing tough competition in international markets from other leading competitors.

Small scale sector reservations limit ability to invest in technology and achieve economies of scale.

Some of the products are not familiar in the market so lots of advertising efforts are needed.

Opportunities: Indian market is a very large market. The major parts of rural markets are not yet

covered. There is good potential for its products in market. Export potential can be increased with special focus on niche markets. Increasing income levels will result in faster revenue growth.

Threats: Imports creating a threat for the company because the cheaper products are being

dumped. Tax and regulatory structure increases the liability of the company and give impact on

profitabilitySlowdown in rural demand due to recession but there are chances of revival further

REFERENCES

http://www.hul.co.in/

http://www.colgate.co.in/app/Colgate/IN/HomePage.cvsp

www. moneycontrol .com/

www.economywatch.com › World Industry Directory

http://www.business-standard.com/india/news/the-fmcg-

market-in-india/333156/

www. investopedia .com/

in.finance.yahoo.com/

![FMCG Sector Report[1]](https://static.fdocuments.us/doc/165x107/54fed95e4a7959b8508b4bac/fmcg-sector-report1.jpg)