India network-and-business-opportunities

33

India Network &Business Opportuni4es India New Delhi Trade Center – Representa5ve Offices Mumbai & Chennai 23.04.2015

Transcript of India network-and-business-opportunities

India Network &Business Opportuni4es India New Delhi Trade Center – Representa5ve Offices Mumbai & Chennai 23.04.2015

Finpron kansainvälinen verkosto

25/09/2014 © Finpro 2

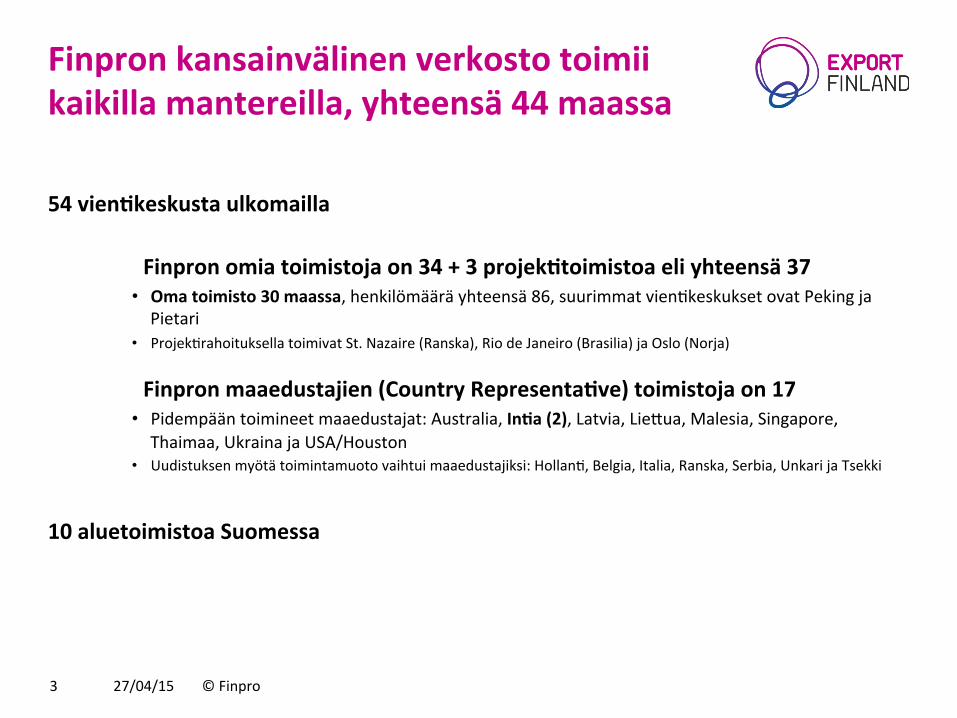

Finpron kansainvälinen verkosto toimii kaikilla mantereilla, yhteensä 44 maassa

54 vien4keskusta ulkomailla

Finpron omia toimistoja on 34 + 3 projek4toimistoa eli yhteensä 37 • Oma toimisto 30 maassa, henkilömäärä yhteensä 86, suurimmat vien5keskukset ovat Peking ja Pietari

• Projek5rahoituksella toimivat St. Nazaire (Ranska), Rio de Janeiro (Brasilia) ja Oslo (Norja)

Finpron maaedustajien (Country Representa4ve) toimistoja on 17 • Pidempään toimineet maaedustajat: Australia, In4a (2), Latvia, Lie^ua, Malesia, Singapore, Thaimaa, Ukraina ja USA/Houston

• Uudistuksen myötä toimintamuoto vaihtui maaedustajiksi: Hollan5, Belgia, Italia, Ranska, Serbia, Unkari ja Tsekki

10 aluetoimistoa Suomessa

27/04/15 © Finpro 3

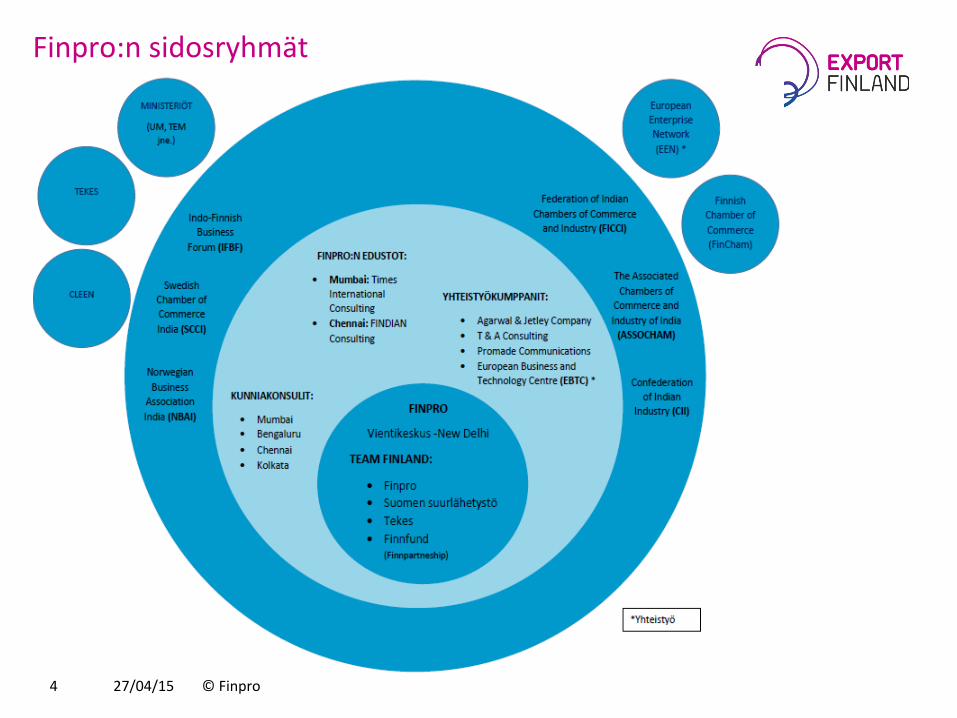

Finpro:n sidosryhmät

27/04/15 © Finpro 4

Finpro Country Representa4ves and Partners

Finpro country representa5ves

Finpro partners

27/04/15 © Finpro 5

Praveen Agarwal Agarwal Jetley & Company

Silva Paananen Promade Communica5ons

Tarun Gupta T&A Consul5ng

Ashish Koltewar Times Interna5onal Consul5ng

Dinkar Krishnan Rekha Salvi FINDIAN Colsul5ng

Team Finland key persons in India

27/04/15 © Finpro 6

Aapo Pölhö Suurlähedläs

Ritva Haukijärvi Lähetystöneuvos

Leena Österberg Finpro:n In5an johtaja

Anand K. Sethi Neuvonantaja (Finnfund)

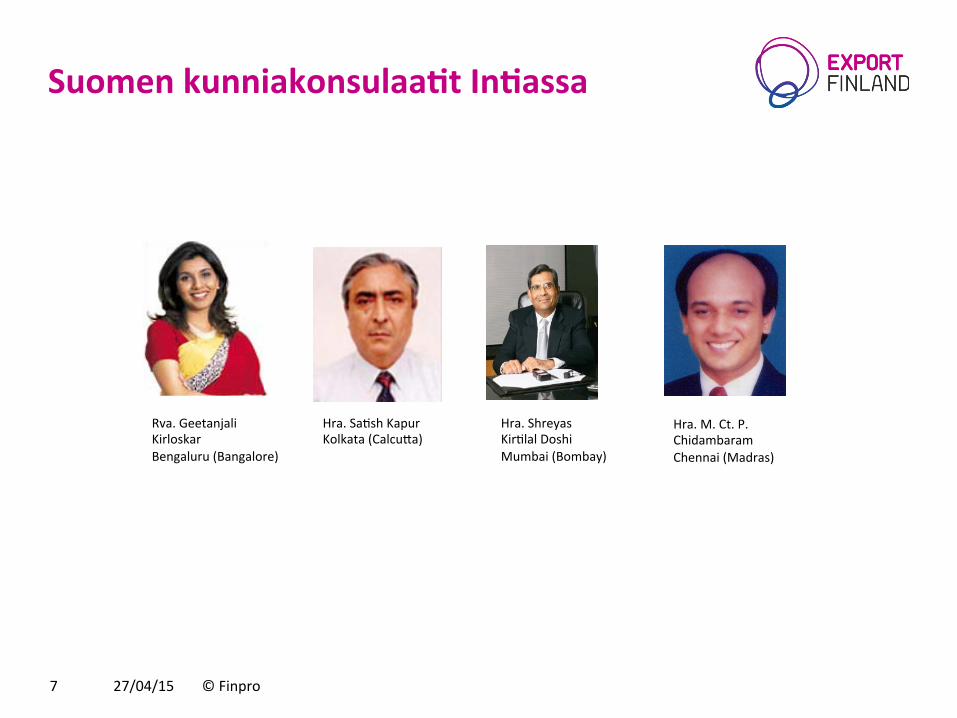

Suomen kunniakonsulaa4t In4assa

27/04/15 © Finpro 7

Rva. Geetanjali Kirloskar Bengaluru (Bangalore)

Hra. Sa5sh Kapur Kolkata (Calcu^a)

Hra. Shreyas Kir5lal Doshi Mumbai (Bombay)

Hra. M. Ct. P. Chidambaram Chennai (Madras)

India Network &Business Opportuni4es India New Delhi Trade Center – Representa5ve Offices Mumbai & Chennai 23.04.2015

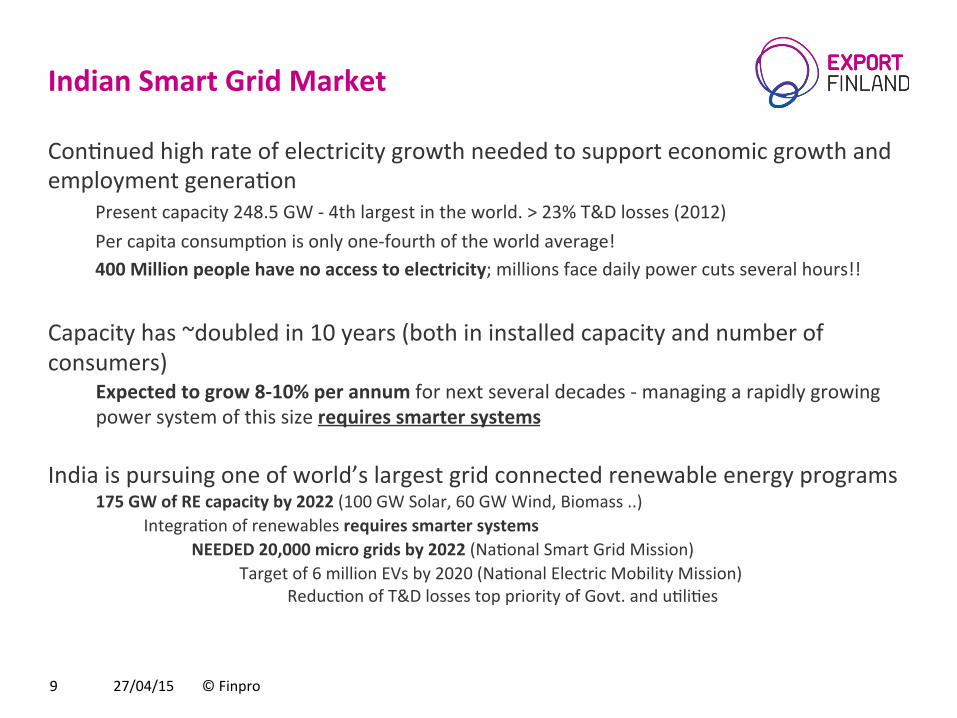

Indian Smart Grid Market

Con5nued high rate of electricity growth needed to support economic growth and employment genera5on

Present capacity 248.5 GW -‐ 4th largest in the world. > 23% T&D losses (2012) Per capita consump5on is only one-‐fourth of the world average! 400 Million people have no access to electricity; millions face daily power cuts several hours!!

Capacity has ~doubled in 10 years (both in installed capacity and number of consumers)

Expected to grow 8-‐10% per annum for next several decades -‐ managing a rapidly growing power system of this size requires smarter systems

India is pursuing one of world’s largest grid connected renewable energy programs 175 GW of RE capacity by 2022 (100 GW Solar, 60 GW Wind, Biomass ..)

Integra5on of renewables requires smarter systems NEEDED 20,000 micro grids by 2022 (Na5onal Smart Grid Mission) Target of 6 million EVs by 2020 (Na5onal Electric Mobility Mission) Reduc5on of T&D losses top priority of Govt. and u5li5es

27/04/15 © Finpro 9

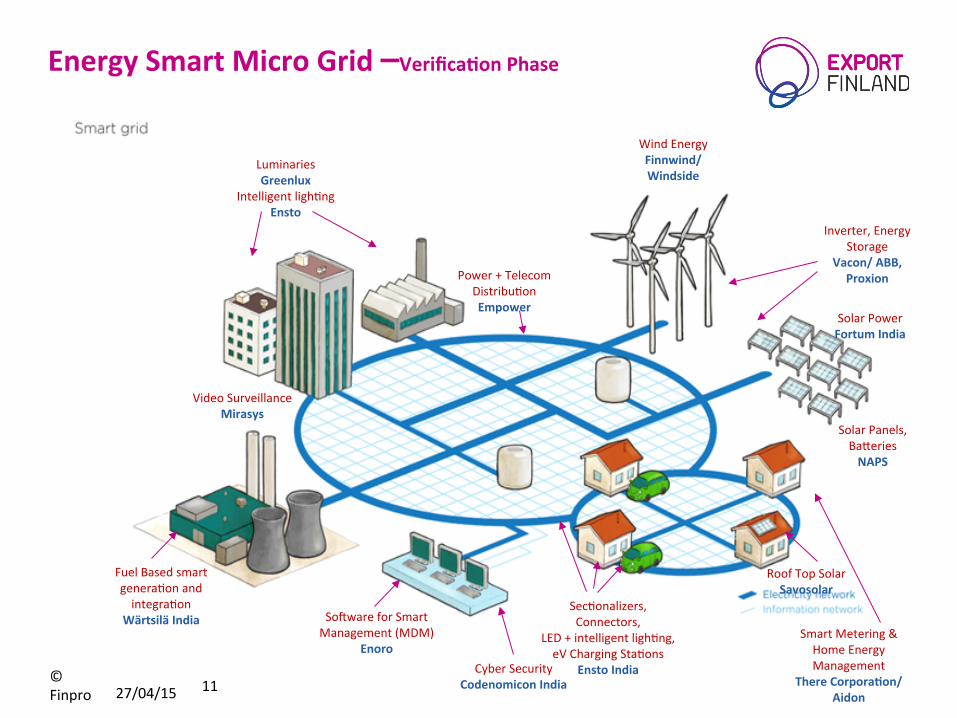

Energy Smart Micro Grid – Verifica4on Phase

• Target: • Energy Smart Micro Grid Pilot

(SpecialEconomicZone/ Port/ Industrial Cluster) for demonstra5on and scaling up in India and Other Markets (Africa). Consor5um: 7 Finnish Cos so far + Finnfund, CLEEN, Embassy of Finland Value Network: Tata Power, ISGF, EBTC, World Bank, IL&FS Pilot campus: Sri City SEZ, NIT-‐Delhi

• Highlights: – Sri City SEZ – India Smart Grid Week (March 3-‐7, Bangalore) – CLEEN visit March 2015. FLEXe – CII Finland visit

27/04/15 © Finpro 10

Energy Smart Micro Grid –Verifica4on Phase

27/04/15 11 © Finpro

Luminaries Greenlux

Intelligent ligh5ng Ensto

Power + Telecom Distribu5on Empower

Wind Energy Finnwind/ Windside

Inverter, Energy Storage

Vacon/ ABB, Proxion

Solar Power Fortum India

Roof Top Solar Savosolar

Fuel Based smart genera5on and integra5on

Wärtsilä India

Souware for Smart Management (MDM)

Enoro Cyber Security

Codenomicon India

Smart Metering & Home Energy Management

There Corpora4on/ Aidon

Sec5onalizers, Connectors,

LED + intelligent ligh5ng, eV Charging Sta5ons

Ensto India

Solar Panels, Ba^eries NAPS

Video Surveillance Mirasys

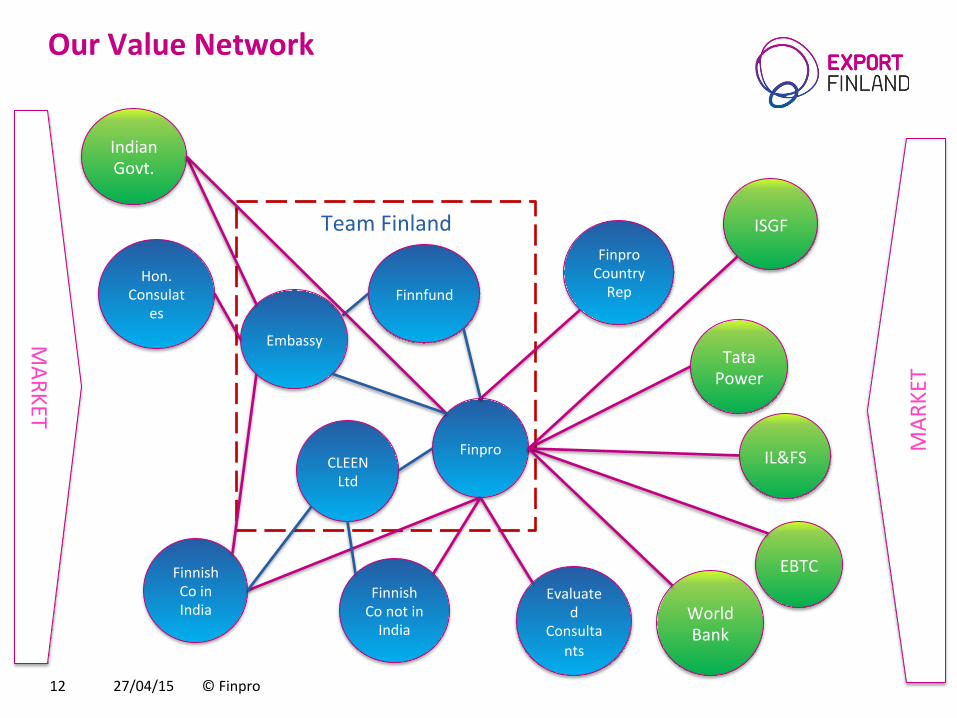

Our Value Network

27/04/15 © Finpro 12

Finpro CLEEN Ltd

Embassy

Finnfund

Team Finland

Finnish Co in India

Hon. Consulat

es

Finpro Country Rep

Evaluated

Consultants

ISGF

Tata Power

EBTC Finnish Co not in India

Indian Govt.

MARKET

MAR

KET

IL&FS

World Bank

Opportunities in the Indian Healthcare Sector

27/04/15 © Finpro 13

Opportunities in the Indian Healthcare Sector Healthcare es5mated to be USD 100 billion business – CARG. 18% Per capita healthcare expenditure: US$ 61 (2012)

• Drivers: Hospital services covers more than 70%of the en5re healthcare market. • Private healthcare accounts for almost 70% of the country's total healthcare expenditure.

Growth drivers: private hospitals, clinics (300 000) and government hospitals

• Increasing life expectancy • New innova5ons and research • High-‐disposable income • Greater penetra5on of insurance (currently 15%) • Growing lifestyles diseases • Growth in medical tourism (27% in last 3 years)

• Healthcare Informa4on Technology (HIT) Services • Electronic Health Records • mHealth • Hospitals & Infrastructure • Medical Devices • Contract Research • Travel -‐ educa4on

27/04/15 © Finpro 14

Opportuni4es in Indian Healthcare Sector

The Indian medical devices market 4th largest in Asia auer Japan, China and South Korea.

Most of the country’s medical technology needs are fulfilled by imports -‐ represent around 70% of the Indian medical devices market.

Medical device market is es5mated at around US$ 4 Billion and is likely to grow at a CAGR of 15% 5ll 2020. Indian hospital services market is es5mated at US$ 65 Billion, growing at 20%. 100% Foreign Direct Investment (FDI) in medical devices manufacturing

Untapped rural market which cons5tutes about 70% of Indian popula5on

Key markets for Finnish companies:

(1) Private Hospitals in big ci5es, (2) Import of high tech medical devices, (3) Digitaliza5on and machine-‐to-‐machine communica5on, (4) Educa4on (further training of healthcare staff).

27/04/15 © Finpro 15

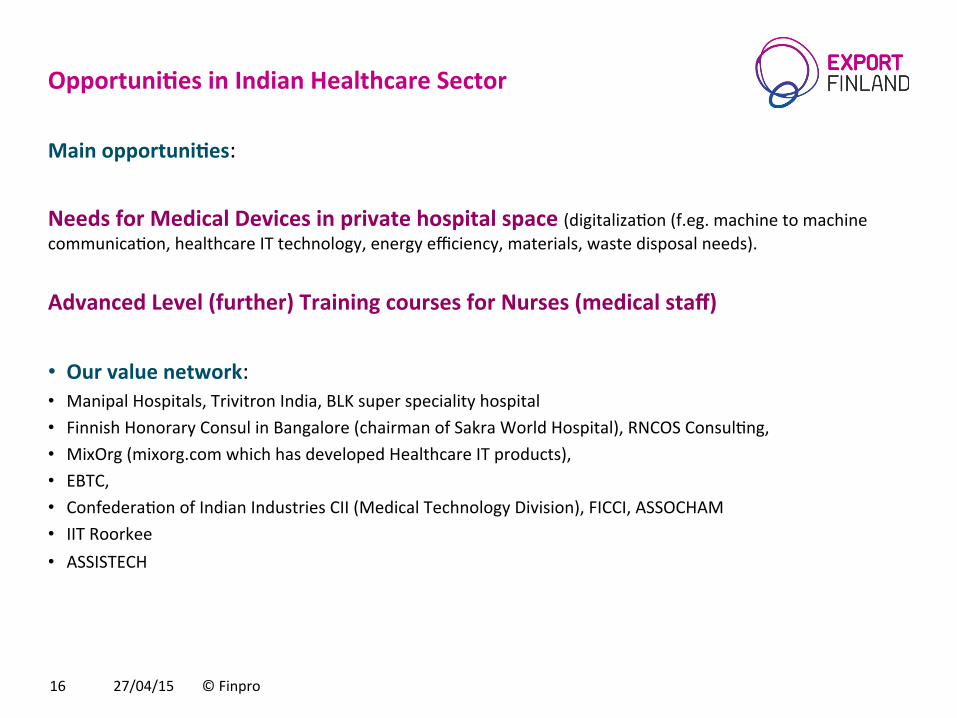

Opportuni4es in Indian Healthcare Sector

27/04/15 © Finpro 16

Main opportuni4es: Needs for Medical Devices in private hospital space (digitaliza5on (f.eg. machine to machine communica5on, healthcare IT technology, energy efficiency, materials, waste disposal needs).

Advanced Level (further) Training courses for Nurses (medical staff)

• Our value network: • Manipal Hospitals, Trivitron India, BLK super speciality hospital • Finnish Honorary Consul in Bangalore (chairman of Sakra World Hospital), RNCOS Consul5ng, • MixOrg (mixorg.com which has developed Healthcare IT products), • EBTC, • Confedera5on of Indian Industries CII (Medical Technology Division), FICCI, ASSOCHAM • IIT Roorkee • ASSISTECH

Cyber Security for India

27/04/15 © Finpro 17

Cyber Security for India

• Increased Cyber a^acks-‐ Cybercrime cost India $8 billion in last 12 months: Norton (2012)

• Digital India project (integra5ng all municipali5es and villages through digital network).

• Unique Iden5fica5on Authority: AADHAAR link to govt program

• Na5onal Policy on Cyber Security (2013) – budgeted $ 200 million with $ 100 million for training itself.

• Infrastructure and energy sector projects (a) smart grid projects, (b) 100 smart ci4es.

• Finnish companies F-‐Secure, Codenomicon, Mirasys are already successful in the Indian market. Codenomicon’s market segmets/ opportuni5es : (i) Telecom, (ii) U5li5es, (iii) Government & Defence, (iv) Banking & Finance, (v) Educa5on/ Capacity Building

• Delhi government has floated the Phase I of their WiFi and CCTV TV network tender for 6000 cameras and WiFi hot spots. In three phases it is expected to establish a network of 100 000 cameras and WiFi hot spots.

27/04/15 © Finpro 18

Cyber Security for India

What we plan to achieve: Informa4on security project for group of Finnish Cos (2) A need based cyber security training program module

Finnish Cos: Codenomicon India, F-‐Secure India, Mirasys India, Triba Learning CLEEN ltd (informa5on security for smart grid) Value network: IL&FS (security for Gurgaon Metro Rail), Delhi Government (WiFi Delhi,

CCTV network for Delhi), Indian Ins5tute of Public Admin IIPA (educa5on and training), Sector experts

• Main opportuni4es: Banking & Finance, Power U5li5es (linked to Smart Grid), Defence & Security, Telecom, Educa5on (Alto University, Triba Learning)

• Highlights: – Interna5onal Cyber Security Conference in Gujarat – Aalto University – Gujarat Forensic Science Univ GFSU – Triba Learning

27/04/15 © Finpro 19

Business Opportunity for Finnish Cos

27/04/15 © Finpro 20

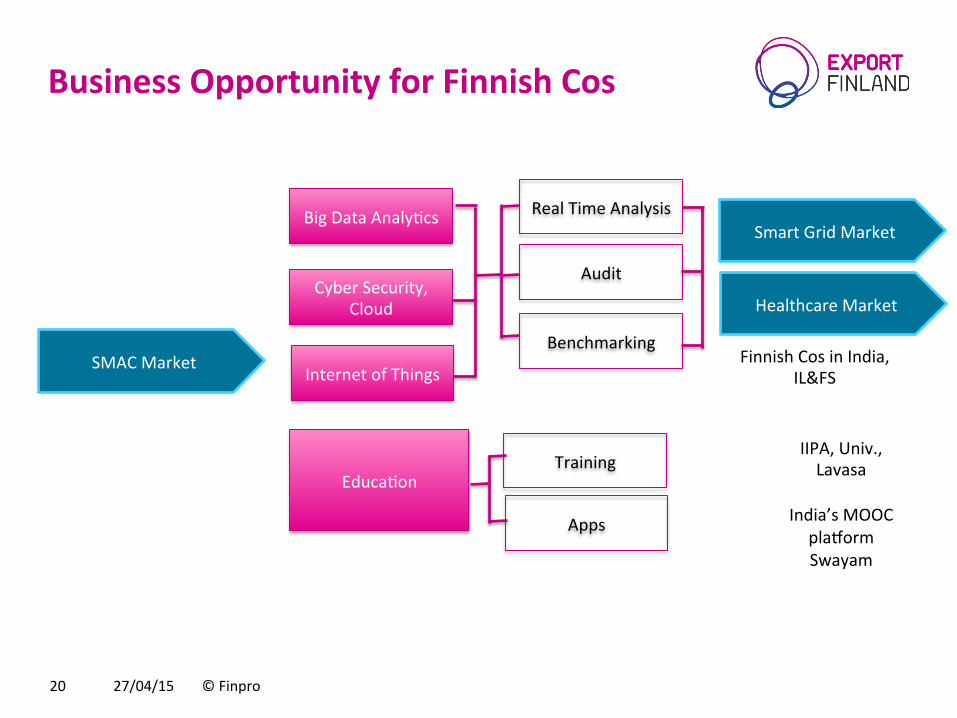

SMAC Market

Cyber Security, Cloud

Internet of Things

Educa5on

IIPA, Univ., Lavasa

India’s MOOC

pla{orm Swayam

Finnish Cos in India, IL&FS

Big Data Analy5cs

Apps

Training

Real Time Analysis

Audit

Benchmarking

Smart Grid Market

Healthcare Market

Immediate Opportuni4es: Cyber Security for India

q Social, Mobility, Analy5cs and Cloud: SMAC are key drivers q The IPv4..IPv6 CGNAT solu5ons complements dual stack IPv4..IPv6 Network with possibility of seemless interconne5vity with IPV6 backend as well as Customer Premises equipment.

q 4G/Lte : Broadband connec5vity to the end users via Smartphone/handsets, either solu5ons including OSS, Radio, test suites, Core/Switch tes5ng, KPI/KRA for Monitoring the Lte/3G/2.5G Networks.

q Network Security/NOC/SOC /Cyber Security tes5ng/standardiza5on & benchmarking for cri5cal infrastructure networks to define the Cyber Policy framework in India.

q Cloud Compu5ng/ SaaS/DAAS tes5ng cum Services shall be deployed by leading System Integrators/ data Centres for sharing the Infrastructure/ bandwidth and ensuring the revenue growth.

q Power distribu5on companies in India are migra5ng from SDH4 technology to next level called MPLSTP.

q Cyber security: Cryptanalysis, Network & Systems Security, Security Architectures, Vulnerability & Assurance, Monitoring Surveillance and Forensic.

q MOOC Massive Online Open Courses Swayam, Digital Locker (Digilocker), Adhar

27/04/15 © Finpro 21

Finland for Cyber Security Educa4on

What we can do: – Certificate course: Distance

learning/ e-Learning/ Visiting faculty

– Developing course content – Developing Apps

27/04/15 © Finpro 22

Indian Ins5tute of Public Administra5on IIPA

1. Gujarat Foreinsic Science University GFSU 2. Raksha Shak5 University (Police science

and internal security)

Lavasa City (Pune): Upcoming Cyber Security training for banking and financial sectors

Puhdas In4a (Clean India) Mission

• The opportunity pertains to Indian market, industry sector being Waste management

• The current Indian government has started the Swachh Bharat Abhiyaan (Clean India Mission). While the campaign is intended to increase the awareness among the general public about cleanliness and sanita5on issues, it has helped garner na5onal a^en5on on Clean and Green ini5a5ves

– The specific Business Opportunity for Finland is to pitch for a package of Waste

management offerings that covers the following areas,

• Municipal Solid Waste (MSW)

• Water and Waste Water Treatment

• E-‐Waste and Management

Puhdas In4a (Clean India) Mission, key aspects

• The key aspects of this Business Opportunity are as follows, – To be pitched as package offering (Puhdas In5a – Clean India) of Team Finland to the PM’s vision of Swachh

Bharat Mission

– Puhdas In5a to cover the following broad topics and related sub topics • Municipal Solid Waste (MSW)

• Waste collec5on and segrega5on tools and solu5ons, awareness and best prac5ces

• Monitoring and control systems

• Waste shredders and compactors

• Water and Waste Water Treatment

• Water treatment and processing technology

• Water quality and monitoring systems

• Water recycling and recovery

• E-‐Waste and Management

• Electronic waste recovery technologies (VTT research and such)

• E-‐waste processing plants

Puhdas In4a (Clean India) Mission

– Points to be noted

• Puhdas In5a (Swachh Bharat) project not directly correlated to SBM, but a complimentary

effort from Finland to India

• Packaging ma^ers (something similar to Beau5ful Beijing)

• Cluster of companies reduces the overall costs for individual companies

• A pilot project to be submi^ed to Prime Minister’s Office (PMO) or Ministry of Urban

Development, through the Embassy in New Delhi

• Proposal to adopt a municipality, panchayath or village each from a Metro, Tier I and Tier II

ci5es each

• Team Finland (Embassy Finpro, FinnFund, TEKES etc.) to coordinate with interested

companies in the Puhdas In5a work

Business Opportunity & Finnish Companies – The following is a sample of prospec5ve Finnish companies that could be enlisted for a cluster-‐based

approach for this project

Company Core Area of Ac4vity Contribu4on Scope

BMH Technology Waste to Energy, Power Plants Municipal and Industrial Waste Management

Tana Oy Waste Shredders and Waste Compactors Municipal Waste Management

Ecosir Vacuum transfer systems for Biowaste Municipal/Solid Waste Management

Marima5c Municipal waste and waste sor5ng solu5ons Municipal/Solid Waste Management

Dora Nova Water and Waste Treatment Contaminated Sites

Municipal/Solid Waste Management, Water and Waste Water Treatment

Aquamec Shallow water dredging Water and Waste Water Treatment

BioLan Organic fer5lizers, equipment for waste treatment, etc. Municipal/Solid Waste Management

Aqua Clean Industrial cleaning, Oil separa5on and filtering Water and Waste Water Treatment

Ecosible Electronic waste procurement and processing E-‐Waste

Stage of Business Opportunity Work: • The BO is s5ll in the concept stage. • Need to be verified/clarified with various stakeholders and prospec5ve target audience in India

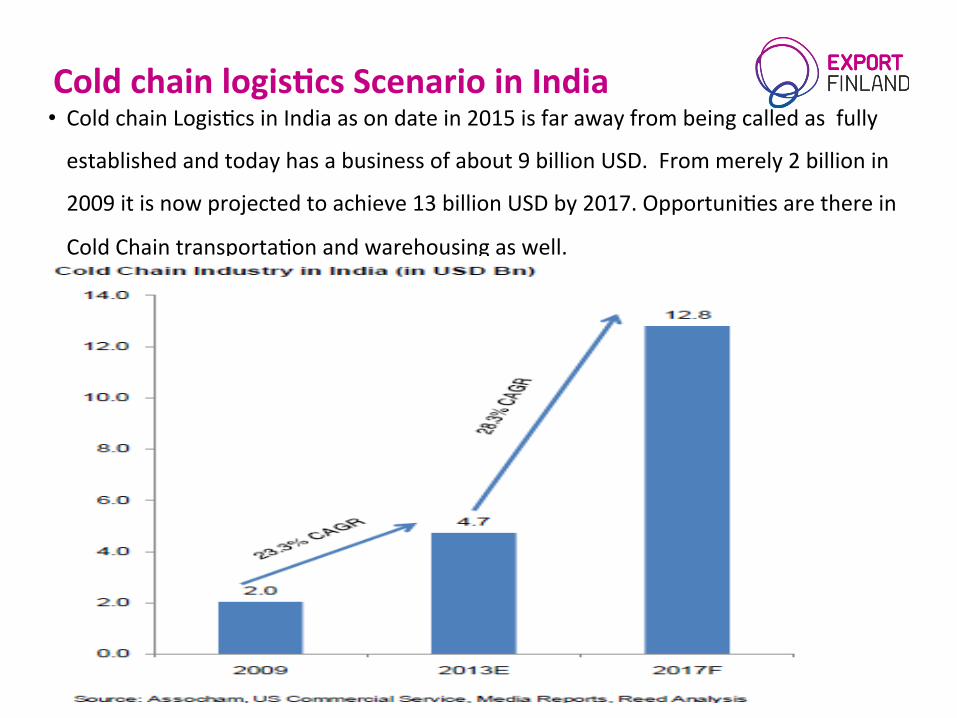

Cold chain logis4cs Scenario in India • Cold chain Logis5cs in India as on date in 2015 is far away from being called as fully

established and today has a business of about 9 billion USD. From merely 2 billion in

2009 it is now projected to achieve 13 billion USD by 2017. Opportuni5es are there in

Cold Chain transporta5on and warehousing as well.

27/04/15 © Finpro 27

Cold Chain Iogis4cs (CCL) – Scenario in India Drivers to the CC (Cold chain) • Organised retail increasing s5ll under 800 bn or under 15% of total retail but increasing every year and increasing working women prefer packed food

• Shiu towards Hor5culture crops • Growth in Bio Pharma sector • Growth in processed food sector • Government ini5a5ves promo5ng the sector

• Change in habits – acceptance to cold storage food in ea5ng habits

• Clear cut demand supply gap

Challenges to CC • Lack of logis5cs support • Uneven distribu5on of Cold chains • Human resources needs to be trained • Cost structure • Lack of Consistent power supply all over India

Compe44on § Very few players in this Industry compared to the current & growing need of India § Few state owned and Private players in CCL § Surface storage comprising of both organised and unorganised § Cap5ve establishments and New entrants

Cold Chain warehousing (Today most cold chains gedng towards mul4 purpose cold storage from tradi4onally Potato storage)

Opportunity Genera4on – Direct opportuni4es Market Demand

• This current opportunity is related to India market and industry sector is Cold chain

logis4cs . The Indian company Kolkata East India

based Balmer & Lawrie will invest about 50

million Euros this year. North East India is the

area that will agract most.

• Driver : Infrastructure spend cons4tutes the major spending for Govt for next 5 to 10 years,

about 30 developing cold chain logis4c parks.

• Growing organised retail ( will con4nue to grow today only under 15% of total retailing)

• The above PPT explains the demand, growth and

future of Cold Chain industry in India in double

digit for a decade atleast year on year.

27/04/15 © Finpro 30

Opportunity in Railways, Mass Transit Sectors

• Railways, Metro Rail, Monorail, Tram. • Railways moderniza5on • 40 Metro Rail projects • Mass transit solu5ons for Smart Ci5es • Private sector

27/04/15 © Finpro 31

Indian Railways

• 64 015 route kilometers, opera5ng 14 244 trains daily that includes 10 673 passengers trains

• 1,4 million employees, the largest rail passenger carrier, the 4th largest rail freight carrier globally.

• over 6 900 million passengers and over 833 million tonnes of of freight per annum

27/04/15 © Finpro 32

Manufacturing: Indian Railways, Metro Rail, Monorail

27/04/15 © Finpro 33

• Par4cipants from Finland so far: Mirasys, Outokumpu, EKE Electronics, Blastman Robo5cs, Kone Elevators

• Main opportuni4es: Freight Traffic | Passenger Traffic | Parcel Traffic | Signalling & Telecom | Safety | Moderniza5on | Rolling Stock | Dedicated Freight Corridor | High Speed Rail Corridor | Interiors of coaches | Sta5ons | Energy | Vacuum Toilets.

• Our value network: Finnish Cos, Associated Container Terminals Ltd ACTL, IL&FS, Bharat Forge, Chambers of Commerce

• Highlights: – Mirasys surveillance systems for railway sta5ons (CCTV based video analy5cs, Security System

Integra5on, Design and Installa5on). – IL&FS is supplying Vacuum Toilets for the railways. – ISGF for smart grid for railway sta5ons (Smart Distributed Energy Genera5on for 8000 railway sta5ons)