india insight 4 - EMPEA › app › uploads › 2017 › 03 › EMPEA...IDG Ventures iCreate...

12

© 2010 Emerging Markets Private Equity Association 1 Insight Country Snapshot* 2010 Population: 1.2 billion 2050 Population: 1.7 billion Population Change (2010–2050): 47% % of Population Under 15 Years-old (2010): 32% 2010 Nominal GDP: US$1.4 trillion 2010 Real GDP Growth: 9.4% 2011 Real GDP Growth: 8.4% 2010 Average Inflation: 13.2% *All data projected. Source: International Monetary Fund, Population Reference Bureau. B oasting one of the most dynamic private equity industries among the emerging markets, India draws an ever-growing number of investors willing to brave the country’s regulatory and infrastructure hurdles in order to gain exposure to some of the most favorable economic growth and demographic trends to be found anywhere in the world. While fundraising and investment activity lagged in 2009 in line with global trends (US$4 billion raised and an additional US$4 billion invested), India has seen a significant uptick in invest- ment pace through the first half of 2010, suggesting renewed confidence in the private equity market as the pricing gap narrows. While fundraising remains challenging with US$1.3 billion raised for India-dedicated vehicles in the first six months of 2010, private equity investments in India have rebounded since the depths of the financial crisis, reaching US$3 billion in the same time period—the highest level of investment experienced since the first half of 2008. A number of strong fundamental drivers set India apart. The IMF recently revised upwards its 2010 GDP growth projections for India to 9.4%, a significant jump from the respectable 5.7% growth rate achieved in 2009. India’s population is additionally projected to overtake China’s by 2050, translating to the rising impor- tance of the Indian consumer. In an August 2010 report, global financial services firm Morgan Stanley predicts that India will become the world’s fastest growing economy by 2013–2015, attributable to India’s largest educated workforce in the world, as well as a cool down of China’s economy. India An Overview of Trends in Select Sectors and Markets August 2010 India Private Equity Fundraising and Investment, 2006–1H 2010, (US$B) Source: EMPEA. Note: Fundraising totals refer to India-dedicated vehicles only. Pan-Asian and global funds that incorporate India in their mandate are not included. 2006 US$ Billions 10 8 6 4 2 0 2007 2008 2009 1H 2010 2.9 5.7 4.6 9.9 7.7 7.5 4.0 4.0 1.3 3.0 Fundraising Investment

Transcript of india insight 4 - EMPEA › app › uploads › 2017 › 03 › EMPEA...IDG Ventures iCreate...

© 2010 Emerging Markets Private Equity Association 1

InsightCountry Snapshot*

2010 Population: 1.2 billion

2050 Population: 1.7 billion

Population Change (2010–2050): 47%

% of Population Under 15 Years-old (2010): 32%

2010 Nominal GDP: US$1.4 trillion

2010 Real GDP Growth: 9.4%

2011 Real GDP Growth: 8.4%

2010 Average Inflation: 13.2%

*All data projected.

Source: International Monetary Fund, Population Reference Bureau.

Boasting one of the most dynamic private equity industries among the

emerging markets, India draws an ever-growing number of investors willing

to brave the country’s regulatory and infrastructure hurdles in order to

gain exposure to some of the most favorable economic growth and demographic

trends to be found anywhere in the world. While fundraising and investment

activity lagged in 2009 in line with global trends (US$4 billion raised and an

additional US$4 billion invested), India has seen a significant uptick in invest-

ment pace through the first half of 2010, suggesting renewed confidence in the

private equity market as the pricing gap narrows. While fundraising remains

challenging with US$1.3 billion raised for India-dedicated vehicles in the first six

months of 2010, private equity investments in India have rebounded since the

depths of the financial crisis, reaching US$3 billion in the same time period—the

highest level of investment experienced since the first half of 2008.

A number of strong fundamental drivers set India apart. The IMF recently revised

upwards its 2010 GDP growth projections for India to 9.4%, a significant jump

from the respectable 5.7% growth rate achieved in 2009. India’s population is

additionally projected to overtake China’s by 2050, translating to the rising impor-

tance of the Indian consumer. In an August 2010 report, global financial services

firm Morgan Stanley predicts that India will become the world’s fastest growing

economy by 2013–2015, attributable to India’s largest educated workforce in the

world, as well as a cool down of China’s economy.

IndiaAn Overview of Trends in Select Sectors and Markets August 2010

India Private Equity Fundraising and Investment, 2006–1H 2010, (US$B)

Source: EMPEA.Note: Fundraising totals refer to India-dedicated vehicles only. Pan-Asian and global funds that incorporate India in their mandate are not included.

2006

US$

Bill

ions

10

8

6

4

2

0

2007 2008 2009 1H 2010

2.9

5.7

4.6

9.9

7.77.5

4.0 4.0

1.3

3.0

Fundraising

Investment

© 2010 Emerging Markets Private Equity Association 2

EMPEA Insight: India August 2010

EMPEA InsightEditorial DirectorJennifer Choi [email protected]

Writing and Research Nadiya Satyamurthy [email protected] Hickey [email protected] Keeler [email protected] Stromquist [email protected]

Executive Editor Carlos Perry [email protected]

Advertising OpportunitiesEach issue of EMPEA Insight provides an opportunity for a single exclusive back page advertisement. For a list of upcoming issues and more information about advertising opportunities and rates, contact EMPEA at [email protected].

About EMPEAThe Emerging Markets Private Equity Association is a non-profit, independent, global industry association that promotes greater understanding of and a more favorable climate for private equity and venture capital investing in the emerging mar-kets of Africa, Asia, Europe, Latin America and the Middle East. For more information, visit us on the web at empea.net.

Data and analysis presented in the EMPEA Insight series is derived from EMPEA’s proprietary industry database, FundLink, made possible with generous support from the following institutions: CDC, DBSA, DEG and FMO. We gratefully acknowledge their contributions.

While possessing robust economic and demographic fundamentals, India poses a number of unique challenges for private equity investors. As one of the most compet- itive markets for investment across the globe, India is characterized by high valuations, driven in part by stiff competition from domestic capital markets as an attractive alternative for capital. India’s rigid bureaucracy and difficult regulatory framework, alongside its dilapi-dated infrastructure, are considerable obstacles to greater market activity. Although the World Economic Forum’s 2009–2010 Global Competitiveness Report ranks India 76 out of 133 nations for its infrastructure, the country is ranked 28th for innovation and business sophistication factors. In spite of its challenges, India Inc.’s vibrant entrepreneurial confidence continues to offer investors significant opportunities in a wide range of sectors from infrastructure and energy to financial services and consumer goods.

Limited Partners (LPs) across the globe, looking in part to diversify away from the West, are increasingly focusing on Emerging Asian funds, with India struggling to rival China as the region’s private equity darling. Despite the buzz on Indian private equity, pan-Asian funds continue to allocate a significantly larger percentage of their capital to China. Nonetheless, according to the 2010 EMPEA/Coller Capital Emerging Markets Private Equity Survey, India continues to rank in the top three among emerging markets in terms of relative attractiveness for private equity investment. Of the 151 institutional investors surveyed, 61% plan to maintain or expand their exposure to the country, while an additional 11% are looking to invest in India for the first time over the next two years.

Fundraising TrendsSecond to China as the largest market of interest in Emerging Asia, India witnessed 26 country-dedicated funds raise US$4 billion in 2009, or 18% of the total for emerging markets, following a peak of US$7.7 billion raised in 2008. In the first half of 2010, India-focused private equity funds raised US$1.3 billion, a sharp decrease (53%) from the US$2.7 billion raised during the same time period one year prior, suggesting that the fundraising environment will remain anemic in India for the remainder of 2010. However, recently closed pan-Asian funds that will likely be active in the market include The Carlyle Group’s Carlyle Asia Partners III Fund, which closed at US$2.6 billion in April 2010 and the JP Morgan Asian Infrastructure & Related Resources Opportunity (AIRRO) Fund, which closed at US$859 mil-lion in February 2010.

Despite a global trend towards smaller fund closes—81% of all emerging market private equity funds reached a final close under US$250 million in 2009—India was home to several of the largest funds raised for the asset class, proving that the opportunity set in the country supports large deal sizes. Outsized funds focused on the Indian market include IDFC Project Equity’s India Infra-structure Fund (IIF), which raised total commitments of US$927 million by June 2009 and India Value Fund Advi-sors’ India Value Fund IV, which held a final close with US$725 million in total commitments in July 2009. Jacob Ballas Capital India’s New York Life Investment Manage-ment India Fund III also ranks among the top 10 largest funds in 2009, holding a final closing on US$440 million in total commitments in January 2009 (after holding a first close at US$278 million in early 2008).

India-dedicated funds closed in the last twelve months have largely been domestic fund managers with established brands and well-built track records. This includes ICICI Venture Funds Management, which

© 2010 Emerging Markets Private Equity Association 3

August 2010

has raised US$400 million as of August 2010 for its India Advantage Fund Series 3 and SME-focused Avigo Capital Partners, which closed their third fund with total commitments of US$240 million in June 2010. Local firms currently in the market launching follow-on funds include BTS Investment Advisors, Everstone Capital, and Milestone Religare Investment Advisors (a private equity joint venture between Milestone Capital and Religare Venture Capital Limited).

While unproven general partners are struggling to launch first-time funds, there are a number of newly formed funds, spearheaded by senior private equity executives who have branched out on their own, that have successfully raised capital. In May 2010, CX Part-ners, led by former Citi Venture Capital International (CVCI) executive Ajay Relan, closed their debut fund at US$515 million, after having reached a first close at US$220 million one year prior. Similarly, former ICICI Venture executive Renuka Ramnath led Multiples Alter-nate Asset Management in achieving a first close at US$250 million in April 2010, and is targeting a final close of US$450 million. In addition to attracting sev-eral domestic investors, the Multiples Alternate Asset Management Fund I drew a commitment of US$100 mil-lion from the Canada Pension Plan Investment Board, representing the LP’s first commitment to an India-focused fund.

According to EMPEA’s database, the number of active fund managers who have launched private equity vehicles targeting India since 2006 stands at over 250 firms. Further crowding the landscape, a number of private equity funds have been launched by Indian

EMPEA Insight: India

corporations and financial institutions. In March 2010, Mumbai-headquartered conglomerate Aditya Birla closed its maiden fund with US$193 million in total commitments. In mid-2009, Reliance Equity Advisors, a subsidiary of the Anil Ambani Group, started fundraising for its debut private equity fund, targeting over US$400 million in total commitments. Other domestic institutions reportedly in the process of launching or evaluating private equity operations are the Tata Group, TVS Group and Mahindra & Mahindra.

Several development finance institutions (DFIs) are struggling with the decision of whether or not to con-tinue supporting the Indian market, given that it already generates significant LP interest. However, DFIs have continued to play a key role throughout the financial downturn, largely investing in funds whose strategies were in line with their developmental mandates. For example, mezzanine-focused BanyanTree Capital Advi-sors held the final closing of its inaugural private equity partnership, BanyanTree Growth Capital Fund, at approximately US$100 million in July 2010 with the support of anchor investors FMO, the international development bank of the Netherlands, and German development finance institution DEG. Meanwhile, U.K.-based government fund of funds CDC Group has made several commitments to India-focused funds, including a US$10 million pledge to Rabo Equity Advisors’ India Agri Business Fund, which is targeting US$100 million in total commitments.

The growing availability of local capital also represents an emerging trend in the Indian market. Aditya Birla’s aforementioned debut fund was reportedly raised entirely

Source: 2010 EMPEA/Coller Capital EM PE Survey.

Limited Partners’ Planned Changes to Their EM PE Investment Strategy Over the Next 1–2 Years

China India Brazil Russia / CIS

% o

f Re

spon

den

ts

100%

80%

60%

40%

20%

0%

No plans to invest

Stop investing

Decrease investing

Stay the same

Begin investing

Expand investment

Sampling of Recent Investments in India

© 2010 Emerging Markets Private Equity Association 4

August 2010

Fund Manager Company SectorTrans. Value

(US$m)Trans. Date

Equity (%)

Actis Integreon Business Services 50 Feb-10 N/A

AIF Capital Famy Care Pharmaceuticals 40 Apr-10 N/A

Bain Capital Lilliput Kidswear Textiles & Apparel 60 Apr-10 31

Baring Private Equity India, Matrix Partners India

Muthoot Finance Financial Services 34 Jul-10 4

The Blackstone Group Jagran Media Network Media & Telecom 51 Apr-10 N/A

The Carlyle Group Tirumala Milk Products Food & Beverage 23 Jun-10 N/A

IDG Ventures iCreate Software Technology 3 Jan-10 N/A

IL&FS Investment Managers The Mobile Store Retail 22 Mar-10 10

India Equity Partners IL&FS Education and Tech. ServicesEd. Services & Training

37 Jan-10 25

Kohlberg Kravis Roberts, New Silk Route Private Equity, Standard Chartered Private Equity

Coffee Day Resorts Food & Beverage 210 Mar-10 20

Quadrangle Capital Partners Tower Vision India Media & Telecom 300 Feb-10 N/A

Warburg Pincus International Metropolis Healthcare Healthcare 85 Jun-10 N/A

Zephyr Peacock India Metro Telworks Media & Telecom 5 Jan-10 19

from domestic institutions and high net worth individuals. Other funds that have successfully sourced domestic capital include ICICI Venture, Multiples Alternate Asset Management and Ascent Capital, to name a few. While the base of domestic investors in India has traditionally been limited, an explosion of wealth has been created in the market over the last five years. According to Forbes Magazine, as of March 2010, India placed fifth of all nations in terms of most billionaires (49) per country, and it is climbing the rankings every year. A growing number of high net worth individuals, as well as family offices and financial institutions, such as the Life Insurance Corporation of India (LIC), have become increasingly educated on and comfortable with the asset class.

Foreign private capital will continue to play the dom-inant role in funding private equity vehicles in India. While domestic LPs are becoming more interested in pri-vate equity, their participation remains relatively small as a percentage of overall fundraising dollars. However, greater encouragement of local participation by the government could create significant traction in terms of further opening up this capital base. This is particu-larly the case for pension funds that hold sizable assets and remain restricted in their ability to invest in the asset class. India’s largest retirement fund, the Employ-ee’s Provident Fund Organization (EPFO), has a corpus estimated between US$40 billion to US$60 billion as of mid-2010. Once domestic private capital is effectively mobilized to make private equity investments, growth in the asset class is poised to increase significantly.

Investment TrendsPrivate equity investments in India have rebounded since the depths of the financial crisis, ascending toward the pre-crisis peak levels seen in 2007. Total investment in the market reached US$3 billion in the first half of 2010, com-pared to US$2.1 billion deployed in the first half of 2009 and US$4 billion invested across the entire year in 2009. The first six months of 2010 have produced the high-est level of investment experienced since the first half of 2008. While India remains characterized by high val-uations, optimistic fund managers on the ground report that the deal pipeline for the remainder of 2010 is steadily building in India, both in terms of number and size of transactions.

In the first half of 2010, the total number of deals reached 126, compared with 71 investments in the same period in 2009. Additionally, for the first time since 2008, inves-tor appetite for larger-sized deals has returned, with a handful of executed transactions already crossing the US$100 million threshold. In fact, in the first half of 2010, several private equity firms completed deals reaching into the several-hundred million dollar range in the infra-structure and energy sectors (for more details on these investments see Spotlight: Energy and Infrastructure).

India remains a growth capital market. Looking broadly at the deal types seen thus far in 2010, growth and expansion transactions in India continue to lead

EMPEA Insight: India

India’s Private Equity Competitive Landscape

Deal activity remains backlogged in India as the competitive density and oversupply of capital causes upward pressure on valuations. Despite the global downturn, there have been few signs of consolida-tion in the market.

According to EMPEA’s database, the number of active fund managers who have launched private equity vehicles specifically targeted at India since 2006 stands at over 250 firms.

However, this figure does not take into account the increasing number of international firms that are investing in India through global or regional funds. Following behind firms such as Blackstone, Car-lyle, KKR and Warburg Pincus, which have already made forays into the Indian market, are a crop of new entrants including Quadrangle Capital, Apollo Management and TA Associates. Bain Capital, which established an office in India in late 2008, has already completed a handful of investments with a local team of 17 investment professionals.

© 2010 Emerging Markets Private Equity Association 5

August 2010

private equity investment strategies, while venture capital deals, which were popular in the first half of 2009, have diminished in number. Buyout transac-tions remain scarce, largely attributable to regulatory restrictions and the fact that many Indian companies are family-owned and remain reluctant to relinquish controlling stakes in their businesses.

In the last several years, PIPE (private investment in public equities) transactions have become extremely prevalent in the Indian market; however, the strength of this model has been questioned as many PIPE investors racked up significant losses with the tumble in stock markets. Addi-tionally, many LPs argue that “true” private equity firms should not be investing in listed companies because they could gain exposure to these firms on their own at a lower cost and because doing so creates a mismatch in investment horizons. Nonetheless, fund managers in India continue to invest in listed companies, in some cases to make follow-on investments in earlier PIPE deals in order to reduce acquisition costs. PIPEs accounted for 10% of all transactions in 2009, which may grow in light of pending proposals to relax limits on investment ceil-ings for listed companies (for more details see highlight on proposed takeover regulation changes).

From 2009 to the first half of 2010, the media and telecom sector received 25% of total private equity investments by value, with 35 deals accounting for approximately US$1.8 billion. The telecommunications sector offers investors myriad opportunities as the industry expands its services to accommodate India’s rapidly growing consumer class. According to Euromonitor International, India’s consumers spend only 3.3% of their total expenditures on communications, while India’s mobile phone penetration rate of 38.6% remains well below the global average of 67.4%.

The past year has seen a number of deals in the tele-coms space, including Quadrangle Capital Partners’ February 2010 US$300 million investment in Tower Vision India, which provides wireless telecommunications infra-structure, and Zephyr Peacock India’s January 2010 US$5 million investment in Metro Telworks, a company engaged in telecom installations and operations. Addi-tionally, various media and print sources are pushing to expand into India’s smaller cities and more rural areas, creating additional opportunities. In April 2010, The Blackstone Group made a US$50.6 million investment in Jagran Media Network, a leading Indian media and com-munications group.

EMPEA Insight: India

India Private Equity Investment Sector Breakdown by Value of Transactions, 2009–1H 2010 (US$B, No. of Investments)

Source: EMPEA.

Media & Telecom

Energy & Natural Resources

Industrials & Manufacturing

Financial Services

Infrastructure

Technology

Other

(US$1B, 34)

(US$1.2B, 24)

(US$497m, 56)

(US$666m, 32)

(US$730m, 40)

(US$1.2B, 81)

(US$1.8B, 35)

© 2010 Emerging Markets Private Equity Association 6

August 2010

Growth in the consumer and industrials/manufacturing sectors is buoyed by two demographic trends in India: the rising middle class and a young population—one of the youngest in the world with 32% under the age of 15. Both of these factors are key determinants of India’s consumption patterns, particularly in the post-crisis period as levels of disposable income are rising. Private equity investments over the past year reflect the importance of this trend. In April 2010, Bain Capital made a US$86 million investment alongside TPG Capital in Lilliput Kidswear, a leader in the Indian branded apparels market. In March 2010, Kohlberg Kravis Roberts (KKR) led a consortium including Standard Chartered Private Equity and New Silk Route to invest US$210 million in Coffee Day Resorts, which operates coffee chain Cafe Coffee Day as well as a host of resorts and IT parks.

Access to basic services in India is poor and greater investment in India’s soft infrastructure, particularly in the education and healthcare sectors, will play a vital role in helping the country meet the needs of its rapidly expanding population. Several private equity firms have deployed capital in soft infrastructure-related projects, attracted to the non-cyclical nature of the space. In January 2010, India Equity Partners completed a US$37.1 million investment in IL&FS Education and Technology Services (IETS), a subsidiary of IL&FS that offers learning content and training for various educational, corporate sector and government clients. In the healthcare sector, Warburg Pincus made a US$85 million investment in Metropolis Healthcare Limited, a chain of diagnostic laboratories, in June 2010.

Spotlight: Energy and InfrastructureEven with the second largest road and fourth largest rail network in the world, infrastructure in India remains inadequate and unable to keep pace with India’s popula-tion growth and rapidly expanding economy. Considering this infrastructure deficit, it is no surprise that infrastruc-ture and its derivative industries have become popular investment targets for growth and expansion deals. Addi-tionally, a number of privatizations are anticipated for the remainder of 2010 and into 2011—the Indian gov-ernment plans to divest approximately US$10 billion in state-owned assets, including in both the energy and infrastructure sectors, which will create additional oppor-tunities for private equity.

Despite having the fifth largest generation capacity in the world, India’s average per capita electricity consump-tion from 2008–2009 was low at 704kWh compared to China (1,800 kWh) or the world average (2,300 kWh), according to KPMG. Additionally, transmission and dis-tribution losses remain substantially higher than global benchmarks at approximately 33%. Until recently, state-owned companies were the most frequent investors in the power generation space; however, this sector now receives considerable attention from outside sources, including private investors.

While 2009 saw private equity firms invest US$615 million in the energy sector across 16 deals, the first half of 2010 has already witnessed US$610 million worth of investments across 8 deals. In the largest known Indian investment in the first half of 2010, a consortium of investors, including Morgan Stanley Infrastructure Part-ners, Goldman Sachs Investment Managers, Everstone Capital, General Atlantic and Norwest Venture Partners, invested US$425 million in Asian Genco, an infrastructure development company with investments in power gen-eration assets. This sector also witnessed a US$300 million consortium investment in GMR Energy led by Temasek and IDFC Private Equity in April and June 2010.

Within the power sector, private equity investments in clean energy and renewable assets have also gained traction. Coal, which remains the foundation of power production in India, accounts for 40% of India’s total greenhouse gas emissions. Power companies are pushing to meet India’s energy demands, while simultaneously addressing climate change concerns. In order to combat pollution, India has set a voluntary target to cut carbon emissions by as much as 25% from 2005 levels by the

EMPEA Insight: India

© 2010 Emerging Markets Private Equity Association 7

August 2010 EMPEA Insight: India

year 2020. In January 2010, TPG Capital invested approxi-mately US$35 million for a 10% stake in the clean energy power producer Greenko Group, which has assets in hydro and biomass-fired plants. The investment was part of a larger round of funding for the Greenko Group led by TPG for a total consideration of US$116 million. The Global Environment Fund (GEF) also made a prior invest-ment in Greenko for US$46 million in November 2009.

Weak infrastructure is arguably India’s greatest hindrance to growth. India’s 11th Five Year Plan estimates that India will require nearly US$500 billion in infrastructure investment from 2007–2011, inclusive of large-scale improvements in power, ports, airports, roads and railway infrastructure. This represents an increase in spending on infrastructure from 4.7% of GDP to approximately 8% of GDP. To fund investments in infrastructure projects needed to keep pace with skyrocketing urban population growth, urban India will need to spend the equivalent of US$134 per capita annually through 2030, according to the McKinsey Global Institute. This is eight times the current level of investment.

In addition to ramping up public sector investment in infrastructure, the Indian government has been engag-ing with the private sector to complement these efforts by allowing private actors greater access to those infra-structure projects in which they find the risk-return profile acceptable, including roads, ports, airports and other construction projects. In April 2010, Actis invested US$77.5 million in TRIL Roads, a 100% subsidiary of India’s Tata Realty and Infrastructure. Other notable invest-ments in this sector include IDFC Project Equity’s March

2010 US$33.3 million investment into Karaikal Port, a port company and subsidiary of the real estate company MARG, and a January 2010 US$54.9 million consortium investment by Baring Private Equity Asia, Sequoia Capital, Fidelity and Deutsche Bank in Coastal Projects, a tunnel engineering company.

Exit TrendsWhile the pace of exit activity slowed in 2009, private equity fund managers see the revival of India’s stock markets as a positive sign and are optimistic about the industry’s ability to capitalize on an improving economic environment. According to Deloitte’s most recent India Private Equity Confidence Survey, 97% of respondents believe that overall exit activity will increase in the near term, while 94% expect IPOs to remain the primary exit route, largely as a result of renewed faith in the public markets. As of mid-August 2010, the Bombay Stock Exchange’s benchmark Sensex Index hit a 52-week high, returning to levels last reached in early February 2008.

India’s large and robust capital markets provide the country with a distinct advantage over other emerging economies in terms of offering a viable exit path with a track record of activity. There are 23 stock exchanges in India, of which the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) account for the majority of traded shares in the country. Most IPOs by India issuers are dual-listed on both. As of July 2010, the BSE had approximately 5,000 listed companies, while the NSE was home to just under 1,500. In 2009, the BSE ranked in the

Sampling of Recent Energy and Infrastructure Investments in India

Fund Manager Company SectorTrans. Value

(US$m) Trans. Date

Actis TRIL Roads Roads, Highways 78 Apr-10

Baring Private Equity Asia, Sequoia Capital India Coastal Projects Engineering & Const. 55 Jan-10

Blackstone Group Moser Baer Projects Power Gen. & Distr. 300 Aug-10

General Atlantic, Everstone Capital, Goldman Sachs Private Equity, Morgan Stanley Private Equity, Norwest Venture Partners

Asian Genco (AGPL) Power Gen. & Distr. 425 Mar-10

Global Environment Fund (GEF) Greenko Group Clean Technology 46 Nov-09

Temasek, IDFC Private Equity, Argonaut Ventures, UTI Ventures Funds Management

GMR Energy Power Gen. & Distr. 300Apr-10, Jun-10

IDFC Project Equity Karaikal Port (Subsidiary of MARG)Ports, Waterways, Shipping

33 Mar-10

Templeton Asset Management Shiv-Vani Oil & Gas 21 Mar-10

August 2010EMPEA Insight: India

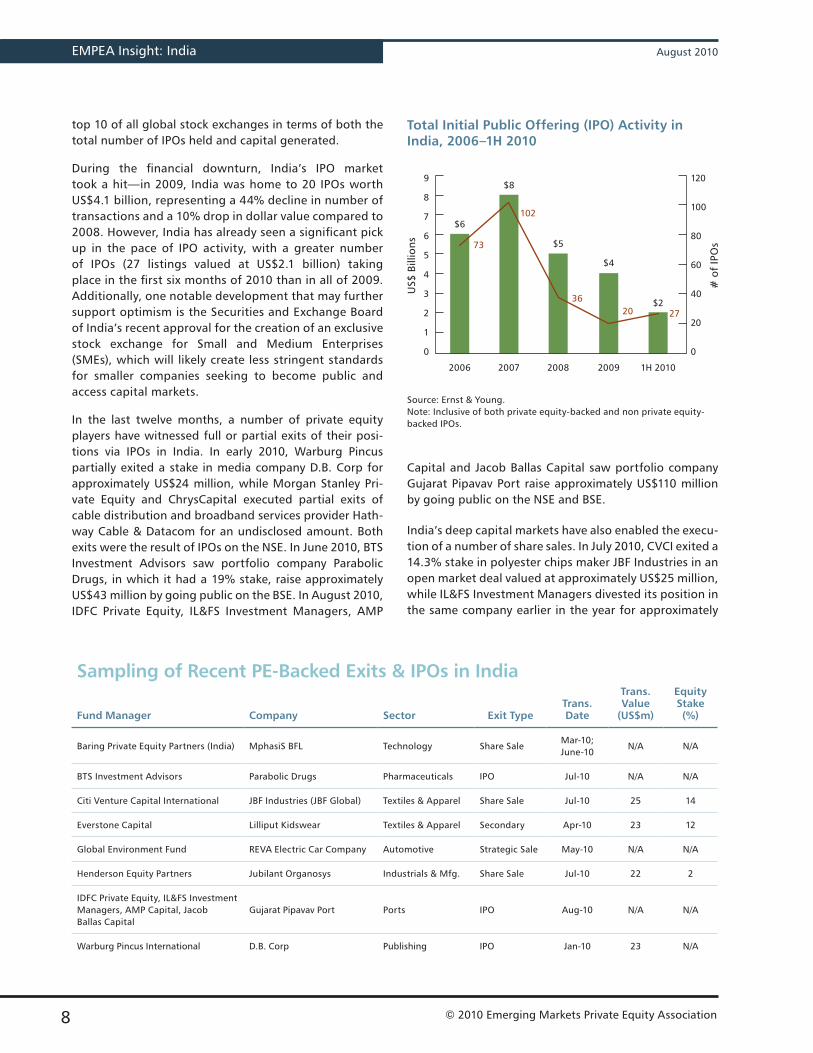

top 10 of all global stock exchanges in terms of both the total number of IPOs held and capital generated.

During the financial downturn, India’s IPO market took a hit—in 2009, India was home to 20 IPOs worth US$4.1 billion, representing a 44% decline in number of transactions and a 10% drop in dollar value compared to 2008. However, India has already seen a significant pick up in the pace of IPO activity, with a greater number of IPOs (27 listings valued at US$2.1 billion) taking place in the first six months of 2010 than in all of 2009. Additionally, one notable development that may further support optimism is the Securities and Exchange Board of India’s recent approval for the creation of an exclusive stock exchange for Small and Medium Enterprises (SMEs), which will likely create less stringent standards for smaller companies seeking to become public and access capital markets.

In the last twelve months, a number of private equity players have witnessed full or partial exits of their posi-tions via IPOs in India. In early 2010, Warburg Pincus partially exited a stake in media company D.B. Corp for approximately US$24 million, while Morgan Stanley Pri-vate Equity and ChrysCapital executed partial exits of cable distribution and broadband services provider Hath-way Cable & Datacom for an undisclosed amount. Both exits were the result of IPOs on the NSE. In June 2010, BTS Investment Advisors saw portfolio company Parabolic Drugs, in which it had a 19% stake, raise approximately US$43 million by going public on the BSE. In August 2010, IDFC Private Equity, IL&FS Investment Managers, AMP

© 2010 Emerging Markets Private Equity Association 8

Capital and Jacob Ballas Capital saw portfolio company Gujarat Pipavav Port raise approximately US$110 million by going public on the NSE and BSE.

India’s deep capital markets have also enabled the execu-tion of a number of share sales. In July 2010, CVCI exited a 14.3% stake in polyester chips maker JBF Industries in an open market deal valued at approximately US$25 million, while IL&FS Investment Managers divested its position in the same company earlier in the year for approximately

Sampling of Recent PE-Backed Exits & IPOs in India

Fund Manager Company Sector Exit TypeTrans. Date

Trans. Value

(US$m)

Equity Stake (%)

Baring Private Equity Partners (India) MphasiS BFL Technology Share SaleMar-10; June-10

N/A N/A

BTS Investment Advisors Parabolic Drugs Pharmaceuticals IPO Jul-10 N/A N/A

Citi Venture Capital International JBF Industries (JBF Global) Textiles & Apparel Share Sale Jul-10 25 14

Everstone Capital Lilliput Kidswear Textiles & Apparel Secondary Apr-10 23 12

Global Environment Fund REVA Electric Car Company Automotive Strategic Sale May-10 N/A N/A

Henderson Equity Partners Jubilant Organosys Industrials & Mfg. Share Sale Jul-10 22 2

IDFC Private Equity, IL&FS Investment Managers, AMP Capital, Jacob Ballas Capital

Gujarat Pipavav Port Ports IPO Aug-10 N/A N/A

Warburg Pincus International D.B. Corp Publishing IPO Jan-10 23 N/A

Total Initial Public Offering (IPO) Activity in India, 2006–1H 2010

Source: Ernst & Young.Note: Inclusive of both private equity-backed and non private equity-backed IPOs.

US$

Bill

ions

# o

f IP

Os

120

100

80

60

40

20

0

9

8

7

6

5

4

3

2

1

0

2006 2007 2008 2009 1H 2010

$6

$8

$5

$4

$2

73

102

3620 27

August 2010 EMPEA Insight: India

© 2010 Emerging Markets Private Equity Association 9

US$7.4 million. Additionally, Baring Private Equity Part-ners India has sold portions of its stake in IT solutions firm MphasiS in several tranches since the beginning of 2010.

Diversification in exit strategies is slowly becoming a reality. A handful of strategic sales have recently taken place in India. An example of a recent domestic acquisition is GEF’s exit of its stake in REVA Electric Car to Mahindra & Mahindra in May 2010. Internationally, ICICI Venture sold its investment in Vetnex Animal Health to Pfizer Animal Health in mid-2009. While many of the larger multinational corporations already have a presence in the country, there are several mid-tier and small global firms that are interested in acquiring Indian assets in order to obtain access to the fast-growing market. Private equity firms in the region report that inbound strategic acquirers are often willing to pay a premium to purchase a portfolio company that has implemented governance and accounting practices in line with global standards.

Another interesting development has been a rise in private equity firms exiting portfolio companies by selling their stakes to the majority shareholder. This primarily occurs when plans to go public are deferred. IDFC Private Equity has executed three exits this year via this process in L&T Infrastructure Development Projects, Chalet Hotels and Manipal Health Systems.

Finally, a market is beginning to develop for secondary sales, particularly as many firms are reaching the end of their investment horizons with portfolio companies not yet ready for IPOs. In February 2010, Citigroup Mauritius Strategic Holdings reportedly sold its 5% stake in Multi Commodity Exchange of India to U.K.-based private equity firm Ashmore Group for approximately US$40 million. In late 2009, The Carlyle Group exited its investment in Financial Software & Systems, an electronic payments processing firm, via a sale to Jacob Ballas Capital and New Enterprise Associates for an undisclosed sum.

OutlookAlthough the private equity industry has rapidly matured in India in response to high levels of global investor inter-est, the asset class remains relatively nascent at only 0.6% of GDP compared to 1.4% in the U.S. India has encour-aged deregulation over the last decade and is continuing to relax restrictions on FDI in a number of sectors, includ-ing financial services, insurance and retail. In fact, most sectors are now open to 100% FDI. Additionally, the Indian Venture Capital Association (IVCA) is working with regulators to further open the private equity market in India. However, a significant amount of work remains to be done on the legal and regulatory front in India to make the country more attractive for private equity gen-erally, and for private equity investment in particular.

A number of initiatives are underway with the potential to impact private equity activity. The government has published proposals for a series of tax reforms to come online in 2011, which include reducing the corporation tax from 35% to 25% and also introducing a flat rate capital gains tax. Additionally, the Securities and Exchange Board of India’s Achuthan Committee on Takeover Regulations has submitted a proposal to overhaul current takeover regulations, with a proposition to adjust the current 15% threshold for open offers of listed companies up to 25%.

SectorFDI

Permitted? Investment Cap

Atomic Energy No -

Gambling and Betting No -

Lottery Business No -

Non-Banking Financial Services Yes MIR

Real Estate Construction & Development Projects

Yes MIR

Insurance Yes 26%

Civil Aviation Yes 49%

Retail Trade of Single Brands Yes 51%

Banking Yes 74%

Telecom Services Yes 74%

Most Other Sectors Yes 100%

MIR=Minimum investment requirement.

Source: Nishith Desai Associates. Note: Some investments in certain sectors may require prior government approval.

Caps on Foreign Direct Investment in India, as of August 2010

As of August 2010, these proposals remain in draft stage and private equity stakeholders are waiting to see how these developments will unfold.

In summary, all signs point to strong fundamentals driving continued robust investor demand and the further development of the domestic private equity industry in India. Despite a recent decline in fundraising, India’s private equity market houses some of the largest funds in the asset class, and LPs consistently identify India as one of the most favored emerging markets destinations for new private equity commitments. As of mid-year, the investment climate was markedly rosier, with total investment through June nearly equal to the full year 2009 total. A number of sizeable transactions in late 2009 and 2010 offer encouraging signs of potential for deal activity in a number of key sectors including telecoms, energy and infrastructure. Finally, private equity-backed exits are expected to increase in line with India’s rebounding stock market. The aggregate of these recent developments in India’s private equity space suggests continued expansion of the opportunity for all private equity participants.

Resources for Reference

Emerging Markets Private Equity Association: Insight India, August 2009www.empea.net

Nishith Desai Associates: Doing Business in India, 2009www.nishithdesai.com

KPMG: Insight India: India’s Private Equity Market after the Financial Crisis, December 2009www.kpmg.com

Deloitte: India Private Equity Confidence Survey, April 2010www.deloitte.com

August 2010EMPEA Insight: India

© 2010 Emerging Markets Private Equity Association 10

Proposed Takeover Regulation Changes

In a potentially promising development for the future of private equity in India, the Securities and Exchange Board of India’s Achuthan Committee on Takeover Regulations has submitted a proposal to overhaul current takeover regulations. The sug-gested new code includes a proposition to adjust the current 15% threshold for open offers of listed companies up to 25%. If ratified, such a change could offer investors significantly more flexibility to increase their investment amount and share size. At the current 15% threshold, high-growth listed Indian companies are blocked from accepting substantial capital injections by global private equity funds.

If the proposed changes are implemented, the private equity industry could be impacted in a number of ways. One likely result would be an expansion in the number of PIPE deals since companies would be able to accept significantly larger capital infusions without crossing the new 25% threshold. Given the peculiarities of the Indian market, a sizable number of early stage companies are listed, thus enlarging the opportunity set. By expanding the range of pos-sible investment opportunities for private equity players, the proposed change could also help to ease the extremely dense and highly competitive investment environment that currently defines the asset class in India.

A potential challenge posed by the new code for private equity investors concerns those investors looking to acquire stakes over 25% in a target com-pany. Under the new code, these investors would be required to make a mandatory bid to purchase up to 100% of the remaining shares of the target company, up from an additional 20% at present. The pro-posed change would significantly increase the cost of acquisition for investors. If the proposed changes result in an acquirer holding more than the permis-sible maximum level for non-public shareholding, the acquirer may either have to delist or lower its holding to meet India’s listing requirements. In the future, a 100% mandatory offer requirement could increase instances of hostile takeovers, which have been rare in India up until this point.

Sampling of Firms Investing in IndiaFund Fund Name Sector Focus

3i Group 3i India Infrastructure Fund (2007, US$1.2B) Infrastructure

Actis Actis Emerging Markets Fund 3 (2007, US$2.9B) Generalist

Aditya Birla Capital Advisors Aditya Birla Private Equity Fund I (2010, US$193m) Generalist

AIF Capital AIF Capital Asia III, L.P. (2006, US$435m) Generalist

Avigo Capital Partners Avigo SME Fund III (2009, US$240m) Generalist

Bain Capital Bain Capital Fund X (2007, US$12.5B) Generalist

BanyanTree Growth Advisors BanyanTree Growth Capital Fund (2008, US$100m) Generalist

Baring Private Equity Partners (India) Baring India Private Equity Fund III (2008, US$550m) Generalist

Blue River Capital Blue River Capital LLC (2006, US$135m) Generalist

BTS Investment Advisors BTS India Clean Energy Fund (Raising, US$120m) Renewable Energy

The Carlyle Group Carlyle Asia Growth Partners IV (2008, US$1B) Generalist

Catamaran Venture Fund Catamaran Venture Fund (2009, US$128m) Generalist

ChrysCapital ChrysCapital Fund V (2007, US$1.25B) Generalist

CLSA Capital Partners Aria Investment Partners III L.P. (2006, US$333m) Generalist

CX Partners CX Partners Fund Alpha (2009, US$515m) Consumer

Everstone Capital Indivision India Partners (2006, US$425m) Infrastructure

Evolvence India Life Science Fund Evolvence India Life Science Fund (2007, US$90m) Life Sciences

Global Environment Fund Global Environment Emerging Markets Fund III (GEEMF III) (2006, US$350m)

Cleantech

HDFC Property Ventures HDFC India Real Estate Fund (US$250m) Real Estate

ICICI Venture Funds Management India Advantage Fund Series 3 (2009, US$400m) Generalist

IDFC Private Equity IDFC Private Equity Fund III (2008, US$700m) Infrastructure

IDFC Project Equity Indian Infrastructure Fund (IIF) (2008, US$928m) Infrastructure

IDG Ventures IDG Ventures India I (2006, US$150m) Technology

IL&FS Investment Managers IL&FS India Realty Fund II (2007, $895m); Tara India Fund III (2007, US$225m)

Real Estate; Generalist

India Equity Partners India Equity Partners Fund I (2006, US$353m) Generalist

Jacob Ballas Capital India New York Life Investment Management (NYLIM) India Fund III (2008, US$440m)

Generalist

Kohlberg Kravis Roberts & Co. (KKR) KKR Asian Fund (2007, US$4B) Generalist

Kotak Private Equity Group Kotak India Growth Fund II (2008, US$440m) Generalist

Lighthouse Funds India 2020, Ltd (2008, US$100m) Generalist

Macquarie Group, State Bank of India (SBI), International Finance Corporation

Macquarie-SBI Infrastructure Fund (MSIF) (US$1B) Infrastructure

Mayfield India Mayfield India Fund I (2008, US$111m) Generalist

New Silk Route Private Equity New Silk Route PE Asia Fund LP (2007, US$1.4B) Generalist

Rabo Equity Advisors India Agri Business Fund (Raising, US$100m) Agribusiness

Reliance Equity Advisors Reliance Alternative Investments Fund - Private Equity Scheme I (Raising)

Generalist

Religare Global Asset Management Religare Private Equity (US$50m) Fund of Funds

Sequoia Capital (India) Sequoia India Growth Fund II (2008, US$725m) Generalist

Small Enterprise Assistance Funds (SEAF) SEAF India Agribusiness Fund (Raising, US$75m) Agribusiness

Templeton Asset Management Templeton Strategic Emerging Markets Fund III (2008, US$180m) Generalist

UTI Ventures Funds Mgmt UTI Ventures Ascent India Fund III (2009, US$350m) Generalist

Warburg Pincus Warburg Pincus Private Equity X, L.P. (2007, US$15B) Generalist

Zephyr Peacock India Zephyr Peacock India Fund II (Raising, US$75m) Generalist

August 2010 EMPEA Insight: India

© 2010 Emerging Markets Private Equity Association 11

Committed to the highest financial and non-

financial returns, we partner closely with our

investors and the companies in which we

invest. As a long-term business partner Actis

adopts an approach defined by corporate

governance, rigorous environmental and social

standards, and decency in all that we do.

With a growing portfolio of investments in

Asia, Africa and Latin America; Actis currently

has US$4.8bn funds under management and

is proud to actively and positively grow the

value of those companies in which we invest.

In 2010, Actis won African Private Equity

Firm of the Year for the third consecutive

year and African Infrastructure Fund Manager

of the Year, both awarded by Private Equity

International.

KS Distribution: Invested US$104m to

develop what aims to be Asia’s largest oil &

gas and marine products distribution business.

Tata Realty and Infrastructure Limited:

Invested US$78m in a joint venture to invest

in Indian roads and highways.

Integreon: Invested US$50m for a minority

stake in a leading provider of research and

legal professional services to law firms and

multinationals.

CIB: Invested US$200m to become the largest

single shareholder in Egypt’s Commercial

International Bank.

7 Days Inn Group: Led investment of

US$65m in the fastest-growing player in

China’s budget hotel industry.

Actom SA: Invested US$138m as part

of a consortium to acquire an electrical

engineering business in South Africa.

www.act.is

Actis is a leading private equity investor that

invests exclusively in the emerging markets

Actis Ad [8.5"x 11"].indd 1 13/08/2010 11:39