INDIA AND AUSTRALIA TAX TREATY.

52

INTRODUCTION INDIA In India, income tax was introduced in 1860, abolished in 1873 and reintroduced in 1886. Income tax levels in India were very high between 1950 and 1980. In 1970-71 there were 11 tax slabs with highest tax rate being 93.5% including surcharges. In 1973-74 highest rate was 97.75%. But to reduce tax evasion tax rates were reduced later on, by 1992-93 maximum tax rates were reduced to 40%. The Central Government has been empowered by the Constitution of India to levy tax on all income other than agricultural income. The Income Tax Law comprises The Income Tax Act 1961, Income Tax Rules 1962, Notifications and Circulars issued by Central Board of Direct Taxes (CBDT), Annual Finance Acts and Judicial pronouncements by Supreme Court and High Courts. Levy of tax is separate on each of the persons, including – individuals, Hindu Undivided Families (HUFs), companies, firms, association of persons, body of individuals, local authority and any other artificial judicial person, and is governed by the Indian Income Tax Act, 1961. The Indian Income Tax Department is governed by CBDT and is part of the Department of Revenue under the Ministry of Finance, Govt. of India. Income tax is a key source of funds that the government uses to fund its activities and serve the public. The Income Tax Department is the biggest revenue mobilizer for the Government. The total tax revenues of the Central Government increased from Rs. 1,392.26 billion in 1997-98 to Rs. 5,889.09 billion in 2007-08. AUSTRALIA: Queensland introduced income tax in 1902 by the Income Tax Act of 1902. Federal income tax was first introduced in 1915, in order to help fund

-

Upload

sowjanya-sampathkumar -

Category

Economy & Finance

-

view

485 -

download

1

Transcript of INDIA AND AUSTRALIA TAX TREATY.

INTRODUCTION

INDIA

In India, income tax was introduced in 1860, abolished in 1873 and

reintroduced in 1886. Income tax levels in India were very high between 1950

and 1980. In 1970-71 there were 11 tax slabs with highest tax rate being 93.5%

including surcharges. In 1973-74 highest rate was 97.75%. But to reduce tax

evasion tax rates were reduced later on, by 1992-93 maximum tax rates were

reduced to 40%.

The Central Government has been empowered by the Constitution of India to

levy tax on all income other than agricultural income. The Income Tax Law

comprises The Income Tax Act 1961, Income Tax Rules 1962, Notifications

and Circulars issued by Central Board of Direct Taxes (CBDT), Annual Finance

Acts and Judicial pronouncements by Supreme Court and High Courts.

Levy of tax is separate on each of the persons, including – individuals, Hindu

Undivided Families (HUFs), companies, firms, association of persons, body of

individuals, local authority and any other artificial judicial person, and is

governed by the Indian Income Tax Act, 1961. The Indian Income Tax

Department is governed by CBDT and is part of the Department of Revenue

under the Ministry of Finance, Govt. of India. Income tax is a key source of

funds that the government uses to fund its activities and serve the public.

The Income Tax Department is the biggest revenue mobilizer for the

Government. The total tax revenues of the Central Government increased from

Rs. 1,392.26 billion in 1997-98 to Rs. 5,889.09 billion in 2007-08.

AUSTRALIA:

Queensland introduced income tax in 1902 by the Income Tax Act of 1902.

Federal income tax was first introduced in 1915, in order to help fund

Australia’s war effort in the First World War. Between 1915 and 1942, income

taxes were levied at both the state and federal level.

Income taxin Australia is the most important revenue stream within

the Australian taxation system. Income tax is levied upon three sources of

income for individual taxpayers: personal earnings (such as salary and

wages), business income andcapital gains. Collectively, these three income tax

sources, account for 67% of federal government revenueand 55% of total

revenue.

Income received by individuals is taxed at progressive rates, while income

derived by companies are taxed at a flat rate of 30%. Generally, capital gains

are only subject to tax at the time the gain is realized. The Australian Taxation

office is in charge of collecting the income tax.

In Australia, the financial year runs from 1 July to 30 June of the following

year. Income tax is applied to the income of a taxable entity. Taxable income is

calculated, in a broad sense, by applying allowable deductions against the

assessable income of a taxable entity.

India Australia

Corp. Tax 34.0% 30.0%

Personal Income Tax 45.0% 33.9%

Sales Tax 10.0% 12.4%

On 16 December 2011, the governments of Australia and India signed a

protocol amending the agreement between the two countries for the avoidance

of double taxation and the prevention of fiscal evasion with respect of taxes on

income, which was signed in 1991.The protocol entered into force on 2 April

2013, when both countries completed their domestic arrangements.

THE WAY FORWARD:

The Government of India and the Government of Australia signed a protocol

onDecember 16, 2011, amending the convention entered into between the

twocountries in 1991 for the avoidance of double taxation and the prevention of

fiscalevasion with respect to taxes on income.

The salient features of the Protocol are as follows –

The Protocol has introduced a definition of the term National under

Article 3of the Convention.

The exclusion of services in the nature of royalty has been eliminated,

whichhas enlarged the scope of services that need to be considered to test

the ServicePE (Permanent Establishments), which was a departure from

most of the tax conventions entered into byIndia with other countries.

However, the threshold has been extended to 183days within any 12-

month period from the existing 90 days. Also, thedistinction between

associated enterprises and non-associated enterprises hasbeen removed.

Furthermore, the threshold was to be examined with respect tothe

activities carried on for the same or connected projects only.

A threshold of 90 days in any 12-month period has been prescribed

forconstituting the PE arising out of carrying on of activities in

connection withthe exploration for or exploitation of natural resources.

A threshold of 183 days in any 12-month period has been prescribed

toconstitute a PE arising due to carrying on of activities of operation of

thesubstantial equipment.

The Protocol has also eliminated the Force of Attraction rule under

Article 7 – Business Profits of the Convention. Thus, profits arising on

the sale of goods orother business activities as attributable to the PE may

be subject to tax in thePE state.

A new Article 24A on Non-discrimination has been inserted in line with

theinternational practices and was applicable to all kinds of taxes

notwithstandingArticle 2 – Taxes Covered and persons, whether or not

resident of both oreither of the contracting states. Furthermore, this

Article shall not apply to anydomestic law provisions of the contracting

states, which are enshrined toprevent the avoidance or evasion of taxes, to

address thin capitalization and toensure collection of taxes or to provide

tax incentives to eligible taxpayers inrespect of research and development

expenditure.

Article 26 on Exchange of information in the Convention has been

amended bythe protocol in line with the treaties entered into by India

with countriesincluding Singapore, Norway, the Netherlands and Nepal.

This Article wasapplicable notwithstanding Article 1 and 2 of the

Convention and wouldhelp the Revenue Authorities of two contracting

states to exchange taxpayerinformation on a wider range of taxes.

A new Article 26A on Assistance in Collection of Taxes has been

inserted tolend assistance to the contracting states in the collection of

revenue claims,subject to certain conditions and procedures. This Article

was in line with thetax treaties entered into by India with Norway, Nepal,

Finland, Luxemburg,Ethiopia and Armenia, among others.

The protocol shall be effective as given below:

a) In the case of Articles on General Definitions, Permanent

Establishments,and Business Profits in the Convention, from Financial

Year 2014-15 onwards;

b) In the case of Articles on Non-Discrimination and Exchange

ofInformation in the Convention, from April 2, 2013;

c) In the case of the Article on Assistance in the Collection of Taxes in

theConvention, from July 18, 2013.

The Convention, as amended by this Protocol, provides certainty on some

aspects for taxpayers seeking to claim the benefits under India-Australia tax

treaty. At thesame time, it was facilitating the mutual economic cooperation,

administration andenforcement of the laws of the Contracting States.

AREAS OF TAX TREATY-OBJECTIVES

The Government of the Republic of India and the Government of Australia,

Desiring to conclude an Agreement for the avoidance of double taxation and the

prevention of fiscal evasion with respect to taxes on income.

Have agreed as follows and have the following objectives:

Article 1

PERSONAL SCOPE

This Agreement shall apply to persons who are residents of one or both of the

Contracting States.

Article 2

TAXES COVERED

1. The existing taxes to which this Agreement shall apply are:

a. In Australia:

The income-tax, and the resource rent tax in respect of offshore projects relating

to exploration for or exploitation of petroleum resources, imposed under the

federal law of the Commonwealth of Australia;

b. In India:

i the income-tax including any surcharge thereon; and

ii the surtax imposed on chargeable profits of companies.

Article 3

GENERAL DEFINITIONS

1. For the purposes of this Agreement, unless the context otherwise requires:

a. the term "Australia", when used in a geographical sense, excludes all

external territories other than:

i. the Territory of Norfolk Island;

ii. the Territory of Christmas Island;

iii. the Territory of Cocos (Keeling) Islands;

iv. the Territory of Ashmore and Cartier Islands;

v. the Territory of Heard Island and McDonald

Islands; and

vi. the Coral Sea Islands Territory,

and includes any area adjacent to the territorial limits of Australia (including the

Territories specified in sub-paragraphs (i) to (vi) inclusive) in respect of which

there is for the time being in force, consistently with international law, a law of

Australia dealing with the exploitation of any of the natural resources of the sea-

bed and sub-soil of the continental shelf;

b. the term "India" means the territory of India and includes the territorial sea

and the air space above it, as well as any other maritime zone in which India has

sovereign rights, other rights and jurisdictions, according to the Indian law and

in accordance with international law;

Article 4

RESIDENCE

1. For the purposes of this Agreement, a person is a resident of one of the

Contracting States if the person is a resident of that Contracting State for the

purposes of its tax. However, a person is not a resident of a Contracting State

for the purposes of this Agreement if the person is liable to tax in that State in

respect only of income from sources in that State.

2. Where in an individual is a resident of both Contracting States, then the status

of that person shall be determined in accordance with the following rules:

a. the person shall be deemed to be a resident solely of the Contracting State in

which a permanent home is available to the person;

b. if a permanent home is available to the person in both Contracting States, or

in neither of them, the person shall be deemed to be a resident solely of the

Contracting State with which the person's personal and economic relations are

closer..

For the purposes of this paragraph, an individual's citizenship of a Contracting

State as well as that person's habitual abode shall be factors in determining the

degree of the person's personal and economic relations with that Contracting

State.'

Article 5

PERMANENT ESTABLISHMENT

1. For the purposes of this Agreement, the term "permanent establishment"

means a fixed place of business through which the business of an enterprise is

wholly or partly carried on.

2. The term "permanent establishment" shall include especially:

a. a place of management;

b. a branch;

c. an office;

d. a factory;

e. a workshop;

f. a mine, an oil or gas well, a quarry or any other place of extraction of

natural resources;

g. a warehouse in relation to a person providing storage facilities for others;

h. a farm, plantation or other place where agricultural, pastoral, forestry or

plantation activities are carried on;

i. premises used as a sales outlet or for receiving or soliciting orders;

j. an installation or structure, or plant or equipment, used for the exploration

for or exploitation of natural resources;

k. a building site or construction, installation or assembly project, or

supervisory activities in connection with such a site or project, where that site or

project exists or those activities are carried on (whether separately or together

with other sites, projects or activities) for more than six months.

3. An enterprise shall be deemed to have a permanent establishment in one of

the Contracting States And to carry on business through that permanent

establishment if:

a. substantial equipment is being used in that State by, for or under a contract

with the enterprise;

b.it carries on activities in that State in connection with the exploration for or

exploitation of natural resources in that State; or

Article 6

INCOME FROM REAL PROPERTY (IMMOVABLE PROPERTY)

1. Income from real property may be taxed in the Contracting State in which

that property is situated.

2. For the purposes of this Article, the term "real property":

a. in the case of Australia, has the meaning which it has under the laws of

Australia and shall include:

i. a lease of land and any other interest in or over land, whether improved or

not; and

ii. a right to receive variable or fixed payments either as consideration for the

working of or the right to work or explore for, or in respect of the exploitation

of, mineral or other deposits, oil or gas wells, quarries or other places of

extraction or exploitation of natural resources; and

b. in the case of India, means such property which, according to the laws of

India, is immovable property and shall include

i. property accessory to immovable property;

ii. rights to which the provisions of the general law respecting landed property

apply;

Article 7

BUSINESS PROFITS

1. The profits of an enterprise of one of the Contracting States shall be taxable

only in that State unless the enterprise carries on business in the other

Contracting State through a permanent establishment situated therein. If the

enterprise carries on business as aforesaid, the profits of the enterprise may be

taxed in the other State but only so much of them as is attributable to:

a. that permanent establishment; or

b. sales within that other Contracting State of goods or merchandise of the

same or a similar kind as those sold, or other business activities of the same or a

similar kind as those carried on, through that permanent establishment.

Article 8

SHIPS AND AIRCRAFT

1. Profits from the operation of ships or aircraft, including interest on funds

connected with that operation, derived by a resident of one of the Contracting

States shall be taxable only in that State

Article 9

ASSOCIATED ENTERPRISES

1. Where:- a. an enterprise of one of the Contracting States participates directly

or indirectly in the management, control or capital of an enterprise of the other

Contracting State; or

b. the same persons participate directly or indirectly in the management, control

or capital of an enterprise of one of the Contracting States and an enterprise of

the other Contracting State,

Article 10

DIVIDENDS

1. Dividends paid by a company which is a resident of one of the Contracting

States for the purposes of its tax, being dividends to which a resident of the

other Contracting State is beneficially entitled, may be taxed in that other State.

2. Such dividends may also be taxed in the Contracting State of which the

company paying the dividends is a resident for the purposes of its tax, and

according to the law of that State, but the tax so charged shall not exceed 15 per

cent. of the gross amount of the dividends.

3. The term "dividends" in this Article means income from shares and other

income which is subjected to the same taxation treatment as income from shares

by the laws of the Contracting State of which the company making the

distribution is a resident for the purposes of its tax.

Article 11

INTEREST

1. Interest arising in one of the Contracting States, being interest to which a

resident of the other Contracting State is beneficially entitled, may be taxed in

that other State.

2. Such interest may also be taxed in the Contracting State in which it arises,

and according to the law of that State, but the tax so charged shall not exceed 15

per cent. of the gross amount of the interest.

3. The term "interest" in this article includes interest from Government

securities or from bonds or debentures, whether or not secured by mortgage and

whether or not carrying a right to participate in profits, and interest from any

other form of indebtedness as well as all other income assimilated to income

from money lent by the law, relating to tax, of the Contracting State in which

the income arises, but does not include interest referred to in paragraph (1) of

Article 8.

Article 12

ROYALTIES

1. Royalties arising in one of the Contracting States, being royalties to which a

resident of the other Contracting State is beneficially entitled, may be taxed in

that other State.

2. Such royalties may also be taxed in the Contracting State in which they arise,

and according to the law of that State, but the tax so charged shall not exceed a

particular range.

Article 13

ALIENATION OF PROPERTY

1. Income or gains derived by a resident of one of the Contracting States from

the alienation of real property referred to in Article 6 and, as provided in that

article, situated in the other Contracting State may be taxed in that other State.

2. Income or gain derived from the alienation of property, other than real

property referred to in Article 6, that forms part of the business property of a

permanent establishment which an enterprise of one of the Contracting States

has in the other Contracting State or pertains to a fixed base available to a

resident of the first-mentioned State in that other State for the purpose of

performing independent personal services, including income or gains from the

alienation of such a permanent establishment (alone or with the whole

enterprise) or of such a fixed base, may be taxed in that other State.

Article 14

INDEPENDENT PERSONAL SERVICES

1. Income derived by an individual or a firm of individuals (other than a

company) who is a resident of one of the Contracting States in respect of

professional services or other independent activities of a similar character shall

be taxable only in that State unless:

a. the individual or firm has a fixed base regularly available to the individual or

firm in the other Contracting State for the purpose of performing the

individual's or the firm's activities, in which case the income may be taxed in

that other State but only so much of it as is attributable to activities exercised

from that fixed base; or

2.The term "professional services" includes services performed in the exercise

of independent scientific, literary, artistic, educational or teaching activities as

well as in the exercise of the independent activities of physicians, surgeons,

lawyers, engineers, architects, dentists and accountants.

Article 15

DEPENDENT PERSONAL SERVICES

1. Subject to the provisions of Articles 16, 17, 18, 19 and 20, salaries, wages

and other similar remuneration derived by an individual who is a resident of one

of the Contracting States in respect of an employment shall be taxable only in

that State unless the employment is exercised in the other Contracting State.

2. Notwithstanding the provisions of paragraph (1), remuneration derived by an

individual who is a resident of one of the Contracting States in respect of an

employment exercised In the other Contracting State shall be taxable only in the

first-mentioned State if:

a. the recipient is present in that other State for a period or periods not

exceeding in the aggregate 183 days in a year of income of that other State;

b. the remuneration is paid by, or on behalf of, an employer who is not a

resident of that other State;

c. the remuneration is not deductible in determining taxable profits of a

permanent establishment or a fixed base which the employer has in that other

State.

Article 16

DIRECTORS' FEES

Directors' fees and similar payments derived by a resident of one of the

Contracting States as a member of the board of directors of a company which is

a resident of the other Contracting State may be taxed in that other State.

Article 17

ENTERTAINERS

1. Notwithstanding the provisions of Articles 14 and 15, income derived by

residents of one of the Contracting States as entertainers, such as theatre, motion

picture, radio or television artistes, musicians and athletes, from their personal

activities as such exercised in the other Contracting State, may be taxed in that

other State.

2. Where income in respect of the personal activities of an entertainer as such

accrues not to that entertainer but to another person, that income may,

notwithstanding the provisions of Articles 7, 14 and 15, be taxed in the

Contracting State in which the activities of the entertainer are exercised.

Article 18

PENSIONS AND ANNUITIES

1. Pensions (not including pensions referred to in Article 19) and annuities

paid to a resident of one of the Contracting States shall be taxable only in that

State.

2. The term "annuity" means a stated sum payable periodically at stated times

during life or during a specified or ascertainable period of time under an

obligation to make the payments in return for adequate and full consideration in

money or money's worth.Article 19

GOVERNMENT SERVICE

1. Remuneration, other than a pension or annuity paid by one of the

Contracting States or a political sub-division or local authority of that State to

any individual in respect of services rendered in the discharge of Governmental

functions, shall be taxable only in that State. However, such remuneration shall

be taxable only in the other Contracting State if the services are rendered in that

other State and the recipient is, a resident of that other State who:

a. is a citizen of that State; or

b. did not become a resident of that State solely for the purpose of performing

the services.

Article 20

PROFESSORS AND TEACHERS

1. Where a professor or teacher who is a resident of one of the Contracting

States visits the other Contracting State for a period not exceeding two years for

the purpose of teaching or carrying out advanced study or research at a

university, college, school or other educational institution, any remuneration

that person receives for such teaching, advanced study or research shall be

exempt from tax in that other State to the extent to which such remuneration is,

or upon the application of this article will be, subject to tax in the first-

mentioned State.

2. This article shall not apply to remuneration which a professor of teacher

receives for conducting research if the research is undertaken primarily for the

private benefit of a specific person or persons.

Article 21

STUDENTS AND TRAINEES

Where a student or trainee, who is a resident of one of the Contracting States or

who was a resident of that State immediately before visiting the other

Contracting State and who is temporarily present in that other State solely for

the purpose of the student's or trainee's education or training, receives payments

from sources outside that other State for the purpose of the student's or trainee's

maintenance, education or training, those payments shall be exempt from tax in

that other State.

Article 22

INCOME NOT EXPRESSLY MENTIONED

1. Items of income of a resident of one of the Contracting States which are not

expressly mentioned in the foregoing articles of this Agreement shall be taxable

only in that State.

2. However, any such income derived by a resident of one of the Contracting

States from sources in the other Contracting State may also be taxed in that

other State.

Article 23

SOURCE OF INCOME

1. Income, profits or gains derived by a resident of one of the Contracting

States which, under any one or more of Articles 6 to 8, Articles 10 to 20 and

Article 22 may be taxed in the other Contracting State, shall for the purposes of

the law of that other State relating to its tax be deemed to be income from

sources in that other State.

2. Income, profits or gains derived by a resident of one of the Contracting

States which, under any one or more of Articles 6 to 8, Articles 10 to 20 and

Article 22 may be taxed in the other Contracting State, shall for the purposes of

Article 24 and of the law of the first-mentioned State relating to its tax be

deemed to be income from sources in that other State.

Article 24

METHODS OF ELIMINATION OF DOUBLE TAXATION

a. Subject to the provisions of the law of Australia from time to time in force

which relate to the allowance of a credit against Australian tax of tax paid in a

country outside Australia (which shall not affect the general principle hereof),

Indian tax paid under the law of India and in accordance with this Agreement,

whether directly or by deduction, in respect of income derived by a person who

is a resident of Australia from sources in India shall be allowed as a credit

against Australian tax payable in respect of that income.

b. Where a company which is a resident of India and is not a resident of

Australia for the purposes of Australian tax pays a dividend to a company which

is a resident of Australia and which controls directly or indirectly not less than

10 per cent. of the voting power of the first-mentioned company, the credit

referred to in sub-paragraph (a) shall include the Indian tax paid by that first-

mentioned company in respect of that portion of its profits out of which the

dividend is paid.

In paragraph (1), Indian tax paid shall include:

a. subject to sub-paragraph

b. an amount equivalent to the amount of any Indian tax forgone which, under

the law of India relating to Indian tax and in accordance with this Agreement,

would have been payable as Indian tax on income but for an exemption from, or

reduction of, Indian tax on that income in accordance with:

i. section 10(4), 10(15)(iv), 10A, 10B, 80HHC, 80HHD or 80-I of the

Income-tax Act, 1961, insofar as those provisions were in force on, and have

not been modified since, the date of signature of this Agreement, or have been

modified only in minor respects so as not to affect their general character; or

ii. any other provision which may subsequently be made granting an

exemption from or reduction of Indian tax which the Treasurer of Australia and

the Ministry of Finance of India agree from time to time in letters exchanged for

this purpose to be of a substantially similar character, if that provision has not

been modified thereafter or has been modified only in minor respects so as not

to affect its general character; and

c. in the case of interest derived by a resident of Australia which is exempted

from Indian tax under the provisions referred to in sub-paragraph (a), the

amount which would have been payable as Indian tax if the interest had not

been so exempt and if the tax referred to in paragraph (2) of Article 11 did not

exceed 10 per cent. of the gross amount of the interest.

3. Paragraph (2) shall apply only in relation to income derived in any of the

first ten years of income in relation to which this Agreement has effect under

sub-paragraph (1)(a)(ii) of Article 28 or in any later year of income that may be

agreed by the Contracting States in letters exchanged for this purpose.

4. In the case of India, double taxation shall be avoided as follows:

a. the amount of Australian tax paid under the laws of Australia and in

accordance with the provisions of this Agreement, whether directly or by

deduction, by a resident of India in respect of income from sources within

Australia which has been subjected to tax both in India and Australia shall be

allowed as a credit against the Indian tax payable in respect of such income but

in an amount not exceeding that proportion of Indian tax which such income

bears to the entire income chargeable to Indian tax; and

b. for the purposes of the credit referred to in sub-paragraph (a) above, where

the resident of India is a company by which surtax is payable, the credit to be

allowed against Indian tax shall be allowed in the first instance against the

income-tax payable by the company in India and, as to the balance, if any,

against the surtax payable by it in India.

5. Where a resident of one of the Contracting States derives income which, in

accordance with the provisions of this Agreement, shall be taxable only in the

other Contracting States, the first-mentioned State may take that income into

account in calculating the amount of its tax payable on the remaining income of

that resident.

Article 25

MUTUAL AGREEMENT PROCEDURE

1. Where a person who is a resident of one of the Contracting States

considers that the actions of the taxation authority of one or both of the

Contracting States result or will result for the person in taxation not in

accordance with this Agreement, the person may, notwithstanding the remedies

provided by the national laws of those States, present a case to the competent

authority of the Contracting State of which the person is a resident. The case

must be presented within three years from the first notification of the action

giving rise to taxation not in accordance with this Agreement.

Article 26

EXCHANGE OF INFORMATION

1. The competent authorities of the Contracting States shall exchange such

information as is necessary for the carrying out of this Agreement or of the

domestic laws of the Contracting States concerning the taxes to which this

Agreement applies insofar as the taxation there under is not contrary to this

Agreement, or for the prevention of evasion or avoidance of, or fraud in relation

to, such taxes. The exchange of information is not restricted by Article 1. Any

information received by the competent authority of a Contracting State shall be

treated as secret in the same manner as information obtained under the domestic

laws of that State and shall be disclosed only to persons or authorities (including

courts and administrative bodies) concerned with the assessment or collection

of, enforcement or prosecution in respect of, or the determination of appeals in

relation to, the taxes to which this Agreement applies and shall be used only for

such purposes. They may disclose the information in public court proceedings

or in judicial decisions.

Article 27

DIPLOMATIC AND CONSULAR OFFICIALS

Nothing in this Agreement shall affect the fiscal privileges of diplomatic or

consular officials under the general rules of international law or under the

provisions of special international Agreements.

Article 28

ENTRY INTO FORCE

1. This Agreement shall enter into force on the date on which the Contracting

States exchange notes through the diplomatic channel notifying each other that

the last of such things has been done as is necessary to give this Agreement the

force of law in Australia and in India, as the case may be, and thereupon this

Agreement shall have effect:

a. In Australia:

i. in respect of withholding tax on income that is derived by a non-resident, in

relation to income derived on or after 1st July in the calendar year following

that in which the Agreement enters into force;

ii. in respect of other Australian tax, in relation to income, profits or gains of

any year of income beginning on or after 1st July, in the calendar year next

following that in which the Agreement enters into force;

b. In India:

in respect of income, profits or gains arising in any year of income beginning on

or after 1st April, in the calendar year next following that in which the

Agreement enters into force.

. The Agreement made between the Government of Australia and the

Government of the Republic of India for the avoidance of double taxation of

income derived from International air transport signed at Canberra on 31st May,

1983 (in this article called "1983 Agreement") shall cease to have effect with

respect to taxes to which this Agreement applies when the provisions of this

Agreement become effective in accordance with paragraph (1).

4. The 1983 Agreement shall terminate on the expiration of the last date on

which it has effect in accordance with the foregoing provisions of this Article.

Impact of FDI & Liberalization on Tax Treaties

The current wave of globalization and liberalization sweeping across the world has

activated the governments in developing countries to compete for foreign direct

investment (FDI).

Encouragement of FDI is an integral part of the economic reforms process of these

countries because it is seen as an instrument of technology transfer, managerial skills,

augmentation of foreign exchange reserves and globalization of the economy.

With a view to provide a conducive environment to foreign investment, many countries,

including India, are redesigning their tax systems to make them internationally

competitive.

Bilateral tax treaties are a part of this exercise to alleviate the problem of international

double taxation.

Bilateral tax treaties are signed, to facilitate the inflow of FDI. Such treaties restrict the

taxation of corporate income of foreign investors and hence affect their profits

positively.

It is generally assumed that having a smaller share of revenues as a result of tax

concessions would, in the long-run, be compensated for by increased inflows of FDI

and other benefits that are part of the FDI package.

In India, the Central Government, under Section 90 of the Income Tax Act, has entered

into Double Taxation Avoidance Agreements or bilateral tax treaties with other

countries.

These tax treaties serve the purpose of providing protection to taxpayers against double

taxation and thus preventing any discouragement which double taxation may otherwise

cause in the free flow of international investment and international transfer of

technology.Section 90 of the Act provides that a treaty may be entered into (a) for

grant of relief in respect of income which is taxed in both the countries, (b) for the

avoidance of double taxation on income, (c) for exchange of information for the

prevention of evasion or avoidance of income tax and (d) for the recovery of

income tax.

Broadly speaking, in India’s tax treaties, double taxation relief is provided by a

combination of the exemption method and tax credit method. Further, Section 91

of the Act provides for the grant of unilateral relief in the case of resident

taxpayers on income which has suffered in India as well as in the country with

which there is no Double Taxation Avoidance Agreement.

A comparison of patterns of change in FDI flows in the pre-treaty period and the

post-treaty period is possible only in case of such countries where the treaty was

entered into a few years after 1991. This is because where the treaty was entered

into prior to 1991; it was not of much significance in terms of FDI flows as the

Indian economy was opened up to foreign investment only after 1991.

Thus, it was only after foreign investment started coming to the economy that the

question of treaty provisions became relevant. Mauritius is a case in point.

The tax treaty with Mauritius was signed in August 1982. Giving special

consideration to business entities of Mauritius, the treaty specified that capital

gains made on the sale of shares of Indian companies by investors resident in

Mauritius would be taxed only in Mauritius and not in India. For almost 10 years,

the treaty existed only on paper since foreign institutional investors (FIIs) were

not allowed to invest in Indian stock markets. This changed in 1992 when FIIs

were allowed into India. Coinciding with this liberalization of the Indian

economy, the Government of Mauritius promulgated the Mauritius Offshore

Business Activities Act, 1992 to regulate the offshore business in that country.

This Act allowed foreign companies to register in Mauritius for investing abroad.

A body corporate registered under the laws in Mauritius would be a resident in

Mauritius and thus ‘subject to taxation’ as a resident. Income Tax Act of

Mauritius provided that offshore companies were liable to pay ‘zero percent’ tax.

Thus, by bringing an offshore company within the definition of resident, not only

was the benefit of offshore company extended to it but also the benefits of

residency allowable under the DTAA bestowed on it.

This led to establishment of conduit companies in Mauritius through which

investors of third countries routed their investment to India. By doing so, they

avoided paying capital gains tax altogether and also enjoyed low rates of dividend

and income taxes in Mauritius.

This, in fact, is one of the reasons why Mauritius is the single largest investing

country in India since 1993 despite its small size.

In case of countries where the treaty was entered into in 1991 or a year after that

(such as in the case US, Japan and Netherlands), the increase in FDI observable

after the signing of the treaty could be largely due to the liberalization of the

Indian economy, although treaty provisions may also have a role to play.

While in some countries (US and France) FDI flows have seen a consistent rise

since the signing of treaty, in some others no particular trend is discernible (such

as UK and Switzerland). In certain cases, we do not see an immediate rise in FDI

activity once the treaty has been signed. This could be due to the fact in the short-

run, new treaties may increase investor uncertainty. Since a new treaty is yet to be

tested in both the Contracting States and may have unresolved legal issues, it

could actually increase the perceived risk of investment between treaty partners

until unsettled issues are resolved.

Thus, in the short-run, the treaty may lead to a reduction in FDI activity. Over the

long run, however, this uncertainty will be resolved, clearing the way for the

treaty to promote investment.

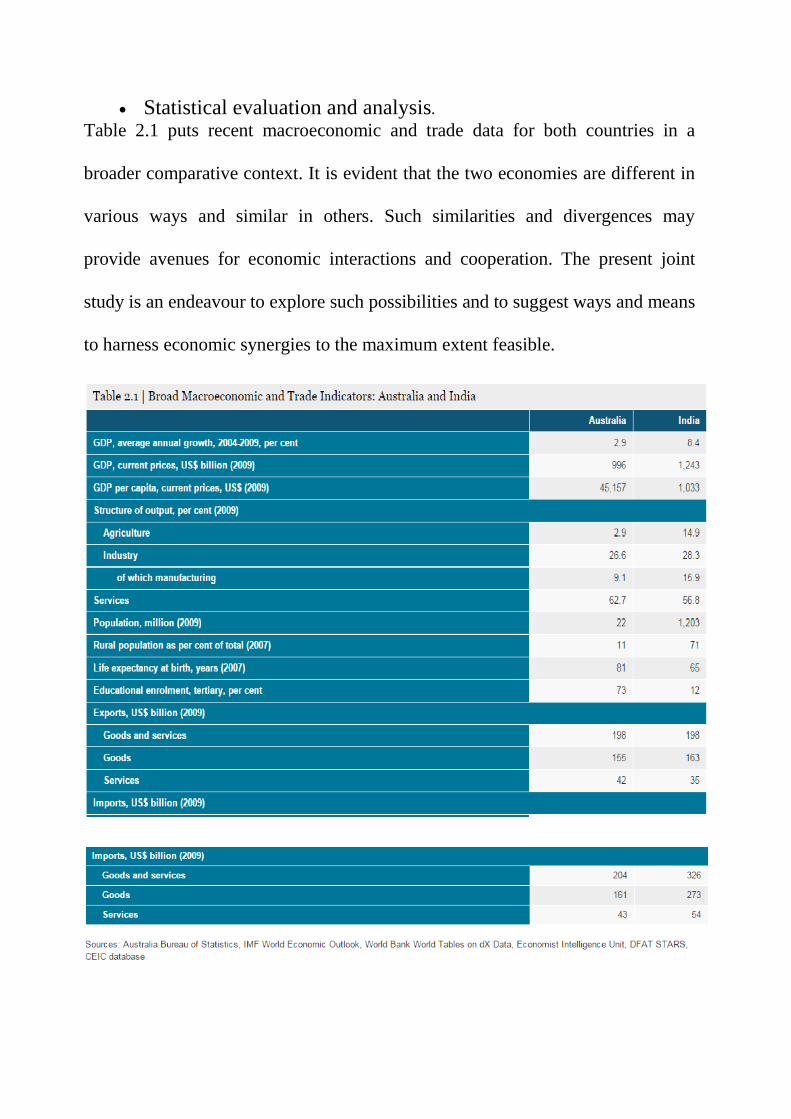

Statistical evaluation and analysis.

Table 2.1 puts recent macroeconomic and trade data for both countries in a

broader comparative context. It is evident that the two economies are different in

various ways and similar in others. Such similarities and divergences may

provide avenues for economic interactions and cooperation. The present joint

study is an endeavour to explore such possibilities and to suggest ways and means

to harness economic synergies to the maximum extent feasible.

Table 2.2 India's developmental trajectory, therefore, owes much to the broad-

based growth in the services sector of the economy. Services have contributed

around 69 per cent of the overall average growth of GDP in the period 2002-03 to

2006–07. Interestingly, services falling under the rubric of trade, hotels, transport

and communications have clocked double digit growth (Table 2.2) since 2003-04

except in 2008–09 (period of global slowdown). Services exports increased

threefold during the last three years. Preliminary estimates indicate that an annual

growth of 26 per cent was achieved during 2008–09. Growth has been

particularly rapid in exports of software services, business services, financial

services and communication services.

Table 2.3 In 2008, while India's share and ranking in world merchandise exports

were 1 per cent and 26th, respectively, its share and ranking in world commercial

services exports was 2.7 per cent and 10th, respectively. Services exports grew

much faster than merchandise exports and constituted almost 60 per cent of

merchandise exports in 2005–06. The composition of India's services exports and

growth in specific sectors is represented in Table 2.3.

Table 2.4 While it is well known that Indian software services have been

growing for some time, other services such as management and consultancy,

advertising and trade fairs, financial services, architectural and engineering

services are emerging as major foreign exchange earners (see Table 2.4).

Business services, which also include legal, accounting and auditing services and

environmental services, achieved exports of US$12.9 billion in 2005–06 as

against US$23.6 billion from software services. This has been made possible

because of the widespread expansion of the telecommunications sector and the

increasing digitisation of various services, making it possible to supply services

remotely. This is also referred to as Cross Border Supply (Mode 1).

Table 2.5 An emerging feature of India's economy is the growing importation of

services (see Table 2.5). India's import of services grew more than ten-fold during

the period 1990-91 to 2005–06. The rapid growth in the import of services is

being fuelled by sustained 8 per cent plus economic growth and increased

engagement by India with the world economy. The growth in services imports is

spread across most sectors.

Imports of commercial services have become important in recent years reaching

US$44 billion in 2006–07 with annual growth of 29 per cent. Business services

are the most important category of services imports, followed by transportation

and travel. Business services grew by 121 per cent in 2006–07.

Temporary movement of people to deliver services is an area of great importance

for India given the growing work-age population and increasing potential to

supply services through movement of skilled persons. India identifies several

domestic laws and regulations that apply to free movement of natural persons to

Australia, including in relation to the ability of Indian service providers to visit

Australia for providing different types of services.

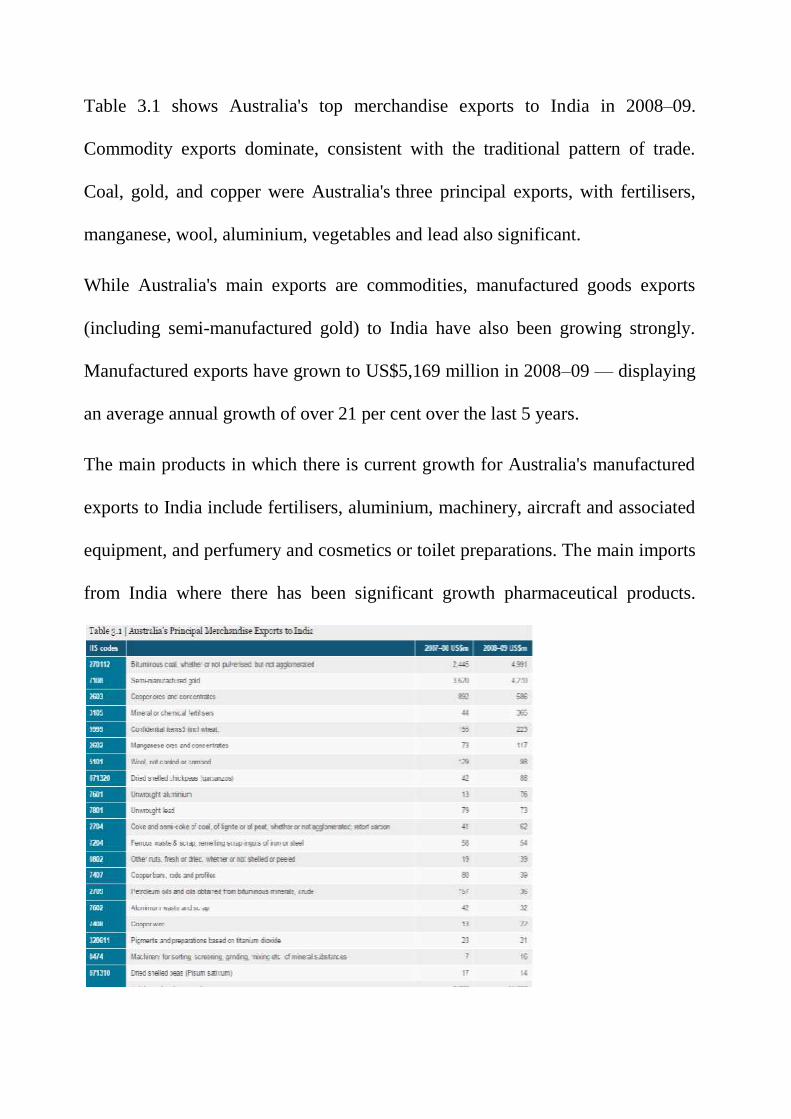

Table 3.1 shows Australia's top merchandise exports to India in 2008–09.

Commodity exports dominate, consistent with the traditional pattern of trade.

Coal, gold, and copper were Australia's three principal exports, with fertilisers,

manganese, wool, aluminium, vegetables and lead also significant.

While Australia's main exports are commodities, manufactured goods exports

(including semi-manufactured gold) to India have also been growing strongly.

Manufactured exports have grown to US$5,169 million in 2008–09 — displaying

an average annual growth of over 21 per cent over the last 5 years.

The main products in which there is current growth for Australia's manufactured

exports to India include fertilisers, aluminium, machinery, aircraft and associated

equipment, and perfumery and cosmetics or toilet preparations. The main imports

from India where there has been significant growth pharmaceutical products.

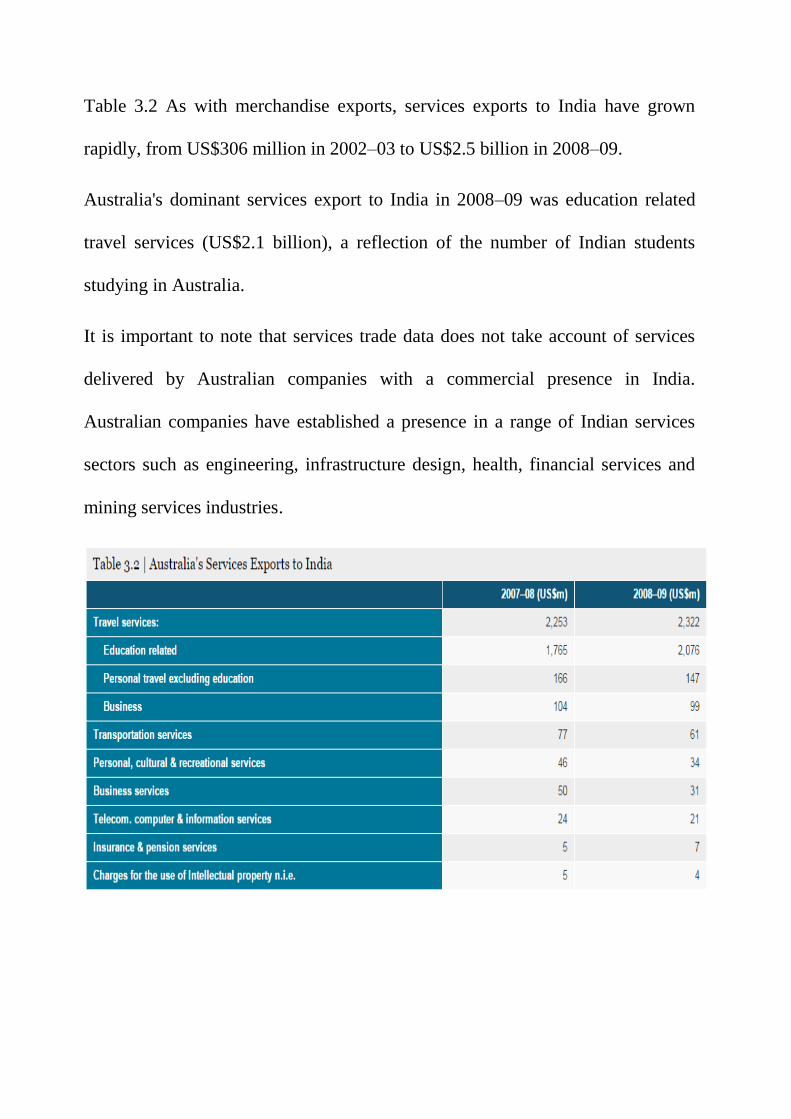

Table 3.2 As with merchandise exports, services exports to India have grown

rapidly, from US$306 million in 2002–03 to US$2.5 billion in 2008–09.

Australia's dominant services export to India in 2008–09 was education related

travel services (US$2.1 billion), a reflection of the number of Indian students

studying in Australia.

It is important to note that services trade data does not take account of services

delivered by Australian companies with a commercial presence in India.

Australian companies have established a presence in a range of Indian services

sectors such as engineering, infrastructure design, health, financial services and

mining services industries.

Table 3.3 India's key merchandise exports to Australia by broad product groups

are shown in Table 3.3. The major product group in 2008–09 among India's

merchandise exports to Australia was machinery and equipment, constituting a

share of around 29 per cent. The other major items in India's exports to Australia

included textiles and garments (14 per cent), gems and jewellery (8 per cent),

base metals (10 per cent), chemicals (12 per cent), vegetables products[7] (7 per

cent), plastics and rubber (4 per cent) and leather and leather products (4 per

cent). Over recent years the percentage of textiles and garments from India as a

proportion of Australia's total merchandise imports has fallen.

Table 3.4 India exports a range of services to Australia, including ITeS, software

and BPO — see Table 3.4. India's exports to Australia have grown over the last

decade. The balance of services trade is in Australia's favour. The major Indian

exports to Australia, by sector, are: travel services, IT and IT enabled services

and other business services.

The growth in travel services indicates increasing interest in India towards

Australia as a tourist destination, as well as travel from India to visit Indian origin

residents in Australia or students from India studying in Australia.

Table 4.1 Total FDI into India since the onset of the Indian liberalisation

process has reached US$133.6 billion up to June 2009.

India's FDI policy has been liberalised in recent years as a result of a

comprehensive review of policy in 2006, including liberalisation of a number of

sectors in 2008 and the revision of norms for calculation of total foreign

investment and for transfer of ownership and control from resident Indian citizens

to non-resident entities in 2009. The result has been a marked upswing in FDI

inflows, from US$2.22 billion in 2003–04 to US$24.58 billion in 2008–09.

An analysis of FDI flows into India from Australia reveals that investment from

Australia has risen off a low base (Table 4.1) since the announcement of India's

new industrial policy in August 1991. Australia's FDI in India as a percentage of

total Indian FDI has remained low and relatively constant.

Table 4.2 it shows the principal Indian sectors receiving Australian FDI inflows.

Australian investment has benefited India's metallurgical industries, services,

telecoms, consultancy and hotel and tourism sectors.

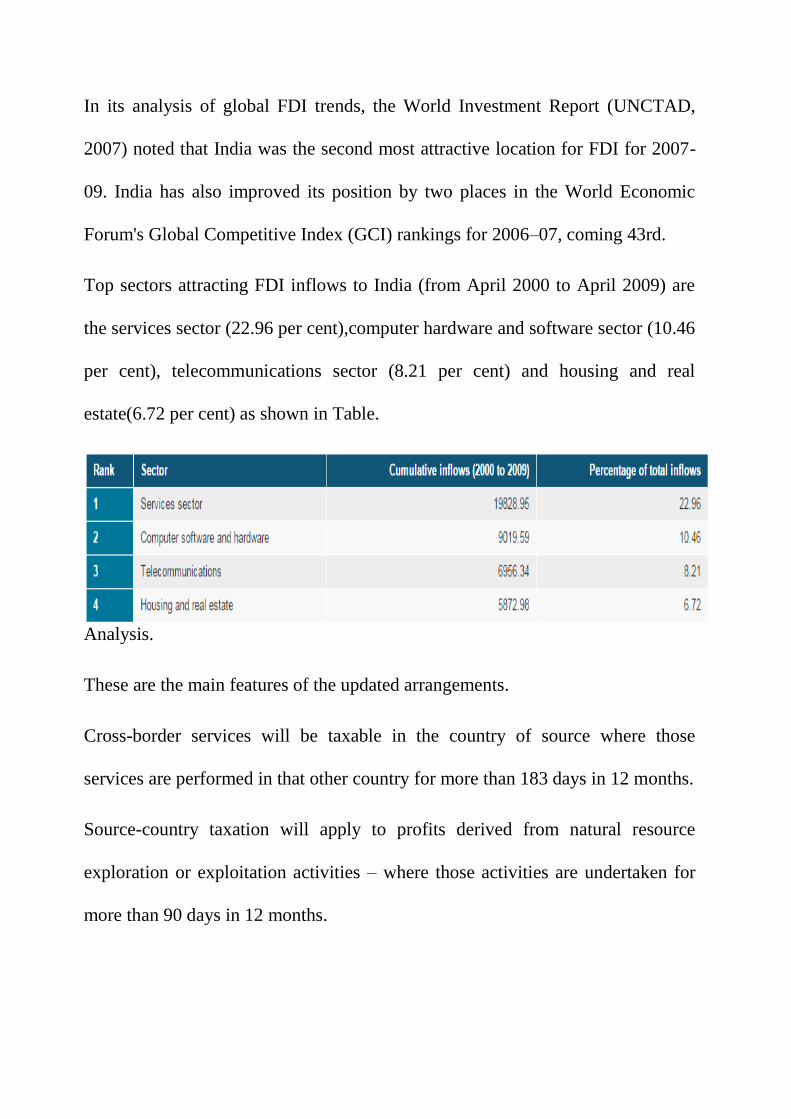

In its analysis of global FDI trends, the World Investment Report (UNCTAD,

2007) noted that India was the second most attractive location for FDI for 2007-

09. India has also improved its position by two places in the World Economic

Forum's Global Competitive Index (GCI) rankings for 2006–07, coming 43rd.

Top sectors attracting FDI inflows to India (from April 2000 to April 2009) are

the services sector (22.96 per cent),computer hardware and software sector (10.46

per cent), telecommunications sector (8.21 per cent) and housing and real

estate(6.72 per cent) as shown in Table.

Analysis.

These are the main features of the updated arrangements.

Cross-border services will be taxable in the country of source where those

services are performed in that other country for more than 183 days in 12 months.

Source-country taxation will apply to profits derived from natural resource

exploration or exploitation activities – where those activities are undertaken for

more than 90 days in 12 months.

Source-country taxation will apply to profits derived from the operation of

substantial equipment – where such operation continues for more than 183 days

in 12 months.

Only the profits attributable to an enterprise's permanent establishment (branch)

in Australia or India may be taxed in that country. This will remove the force-of-

attraction rule in the existing treaty which allows for the taxation of indirect

profits connected with a permanent establishment.

A new non-discrimination article will protect nationals and businesses of one

country from tax discrimination in the other country.

The exchange-of-information article has been updated to the current international

standard and will also allow the revenue authorities of Australia and India to

exchange taxpayer information on a wider range of taxes.

A new article regarding assistance in the collection of taxes will allow the

revenue authorities of Australia and India to assist each other in the collection of

outstanding tax debts.

Withholding tax rates on dividends, interest and royalties, and withholding tax

rates on managed investment trust distributions, remain unchanged and apply as

set out in the original (1991) agreement.

Conclusion

Both countries can make gains through further services liberalisation and with

this in mind could undertake to make substantive, high-quality commitments. To

maximise the potential gains India and Australia should aim for:

liberalisation which delivers meaningful commercial outcomes in services;

substantial sectoral coverage measured in terms of number of sectors, volume of

trade and modes of supply;

basing rules and disciplines on trade in services on GATS provisions and

improving them further wherever possible including, potentially, domestic

regulations;

giving priority to areas with greater potential and complementarities between

both the counties, such as computer-related services, financial services, tourism

services , professional services and educational services;

maximising trade through Movement of Natural Persons;

committing to work towards a mutual recognition of professional qualifications

by authorities and professional registration bodies in Australia and India; and

maximise trade in services to the benefit of the economies of the parties.

Taxation System in India

India has a well-developed tax structure with clearly demarcated authority

between Central and State Governments and local bodies.

Central Government levies taxes on income (except tax on agricultural income,

which the State Governments can levy), customs duties, central excise and

service tax.

Value Added Tax (VAT), stamp duty, state excise, land revenue and profession

tax are levied by the State Governments.

Local bodies are empowered to levy tax on properties, octroi and for utilities

like water supply, drainage etc.

Indian taxation system has undergone tremendous reforms during the last

decade. The tax rates have been rationalized and tax laws have been simplified

resulting in better compliance, ease of tax payment and better enforcement. The

process of rationalization of tax administration is ongoing in India.

Direct Taxes

In case of direct taxes (income tax, wealth tax, etc.), the burden directly falls on

the taxpayer.

Income tax

According to Income Tax Act 1961, every person, who is an assessee and

whose total income exceeds the maximum exemption limit, shall be chargeable

to the income tax at the rate or rates prescribed in the Finance Act. Such income

tax shall be paid on the total income of the previous year in the relevant

assessment year.

Assessee means a person by whom (any tax) or any other sum of money is

payable under the Income Tax Act, and includes -

(a) Every person in respect of whom any proceeding under the Income Tax Act

has been taken for the assessment of his income (or assessment of fringe

benefits) or of the income of any other person in respect of which he is

assessable, or of the loss sustained by him or by such other person, or of the

amount of refund due to him or to such other person;

(b) Every person who is deemed to be an assessee under any provisions of the

Income Tax Act;

(c) Every person who is deemed to be an assessee in default under any provision

of the Income Tax Act.

Where a person includes:

IndividualHindu Undivided Family (HUF)Association of persons (AOP)Body

of individuals (BOI)CompanyFirmA local authority and,Every artificial judicial

person not falling within any of the preceding categories.

Income tax is an annual tax imposed separately for each assessment year (also

called the tax year). Assessment year commences from 1st April and ends on

the next 31st March.

The total income of an individual is determined on the basis of his residential

status in India. For tax purposes, an individual may be resident, nonresident or

not ordinarily resident.

Resident

An individual is treated as resident in a year if present in India:

1. For 182 days during the year or

2. For 60 days during the year and 365 days during the preceding four years.

Individuals fulfilling neither of these conditions are nonresidents. (The rules are

slightly more liberal for Indian citizens residing abroad or leaving India for

employment abroad.)

Resident but not Ordinarily Resident

A resident who was not present in India for 730 days during the preceding seven

years or who was nonresident in nine out of ten preceding years is treated as not

ordinarily resident.

Non-Residents

Non-residents are taxed only on income that is received in India or arises or is

deemed to arise in India. A person not ordinarily resident is taxed like a non-

resident but is also liable to tax on income accruing abroad if it is from a

business controlled in or a profession set up in India.

Non-resident Indians (NRIs) are not required to file a tax return if their income

consists of only interest and dividends, provided taxes due on such income are

deducted at source. It is possible for non-resident Indians to avail of these

special provisions even after becoming residents by following certain

procedures laid down by the Income Tax act.

StatusIndian IncomeForeign IncomeResident and ordinarily

residentTaxableTaxableResident but not ordinary residentTaxableNot

taxableNon-ResidentTaxableNot taxable

Personal Income Tax

Personal income tax is levied by Central Government and is administered by

Central Board of Direct taxes under Ministry of Finance in accordance with the

provisions of the Income Tax Act.

Rates of Withholding Tax

To view tax rates applicable in India under Avoidance of Double Taxation

(ADT) agreement Click here

Tax upon Capital Gains

Corporate tax

Definition of a company

A company has been defined as a juristic person having an independent and

separate legal entity from its shareholders. Income of the company is computed

and assessed separately in the hands of the company. However the income of

the company, which is distributed to its shareholders as dividend, is assessed in

their individual hands. Such distribution of income is not treated as expenditure

in the hands of company; the income so distributed is an appropriation of the

profits of the company.

Residence of a company

A company is said to be a resident in India during the relevant previous year

if:It is an Indian companyIf it is not an Indian company but, the control and the

management of its affairs is situated wholly in IndiaA company is said to be

non-resident in India if it is not an Indian company and some part of the control

and management of its affairs is situated outside India.

Corporate sector tax

The taxability of a company's income depends on its domicile. Indian

companies are taxable in India on their worldwide income. Foreign companies

are taxable on income that arises out of their Indian operations, or, in certain

cases, income that is deemed to arise in India. Royalty, interest, gains from sale

of capital assets located in India (including gains from sale of shares in an

Indian company), dividends from Indian companies and fees for technical

services are all treated as income arising in India. Current rates of corporate tax.

Different kinds of taxes relating to a company

Minimum Alternative Tax (MAT)

Normally, a company is liable to pay tax on the income computed in accordance

with the provisions of the income tax Act, but the profit and loss account of the

company is prepared as per provisions of the Companies Act. There were large

number of companies who had book profits as per their profit and loss account

but were not paying any tax because income computed as per provisions of the

income tax act was either nil or negative or insignificant. In such case, although

the companies were showing book profits and declaring dividends to the

shareholders, they were not paying any income tax. These companies are

popularly known as Zero Tax companies. In order to bring such companies

under the income tax act net, section 115JA was introduced w.e.f assessment

year 1997-98.

A new tax credit scheme is introduced by which MAT paid can be carried

forward for set-off against regular tax payable during the subsequent five year

period subject to certain conditions, as under:-

When a company pays tax under MAT, the tax credit earned by it shall be an

amount, which is the difference between the amount payable under MAT and

the regular tax. Regular tax in this case means the tax payable on the basis of

normal computation of total income of the company.MAT credit will be

allowed carry forward facility for a period of five assessment years immediately

succeeding the assessment year in which MAT is paid. Unabsorbed MAT credit

will be allowed to be accumulated subject to the five-year carry forward limit.In

the assessment year when regular tax becomes payable, the difference between

the regular tax and the tax computed under MAT for that year will be set off

against the MAT credit available.The credit allowed will not bear any interest

Fringe Benefit Tax (FBT)

The Finance Act, 2005 introduced a new levy, namely Fringe Benefit Tax

(FBT) contained in Chapter XIIH (Sections 115W to 115WL) of the Income

Tax Act, 1961.

Fringe Benefit Tax (FBT) is an additional income tax payable by the employers

on value of fringe benefits provided or deemed to have been provided to the

employees. The FBT is payable by an employer who is a company; a firm; an

association of persons excluding trusts/a body of individuals; a local authority; a

sole trader, or an artificial juridical person. This tax is payable even where

employer does not otherwise have taxable income. Fringe Benefits are defined

as any privilege, service, facility or amenity directly or indirectly provided by

an employer to his employees (including former employees) by reason of their

employment and includes expenses or payments on certain specified heads.

The benefit does not have to be provided directly in order to attract FBT. It may

still be applied if the benefit is provided by a third party or an associate of

employer or by under an agreement with the employer.

The value of fringe benefits is computed as per provisions under Section

115WC. FBT is payable at prescribed percentage on the taxable value of fringe

benefits. Besides, surcharge in case of both domestic and foreign companies

shall be leviable on the amount of FBT. On these amounts, education cess shall

also be payable.

Every company shall file return of fringe benefits to the Assessing Officer in the

prescribed form by 31st October of the assessment year as per provisions of

Section 115WD. If the employer fails to file return within specified time limit

specified under the said section, he will have to bear penalty as per Section

271FB.

The scope of Fringe Benefit Tax is being widened by including the employees

stock option as fringe benefit liable for tax. The fair market value of the share

on the date of the vesting of the option by the employee as reduced by the

amount actually paid by him or recovered from him shall be considered to be

the fringe benefit. The fair market value shall be determined in accordance with

the method to be prescribed by the CBDT.

Dividend Distribution Tax (DDT)

Under Section 115-O of the Income Tax Act, any amount declared, distributed

or paid by a domestic company by way of dividend shall be chargeable to

dividend tax. Only a domestic company (not a foreign company) is liable for the

tax. Tax on distributed profit is in addition to income tax chargeable in respect

of total income. It is applicable whether the dividend is interim or otherwise.

Also, it is applicable whether such dividend is paid out of current profits or

accumulated profits.

The tax shall be deposited within 14 days from the date of declaration,

distribution or payment of dividend, whichever is earliest. Failing to this

deposition will require payment of stipulated interest for every month of delay

under Section115-P of the Act.

Rate of dividend distribution tax to be raised from 12.5 per cent to 15 per cent

on dividends distributed by companies; and to 25 per cent on dividends paid by

money market mutual funds and liquid mutual funds to all investors.

Banking Cash Transaction Tax (BCTT)

The Finance Act 2005 introduced the Banking Cash Transaction Tax (BCTT)

w.e.f. June 1, 2005 and applies to the whole of India except in the state of

Jammu and Kashmir.BCTT continues to be an extremely useful tool to track

unaccounted monies and trace their source and destination. It has led the

Income Tax Department to many money laundering and hawala transactions.

BCTT is levied at the rate of 0.1 per cent of the value of following "taxable

banking transactions" entered with any scheduled bank on any single day:

Withdrawal of cash from any bank account other than a saving bank account;

andReceipt of cash on encashment of term deposit(s).

However,Banking Cash Transaction Tax (BCTT) has been withdrawn with

effect from April 1, 2009.

Securities Transaction Tax (STT)

Securities Transaction Tax or turnover tax, as is generally known, is a tax that is

leviable on taxable securities transaction. STT is leviable on the taxable

securities transactions with effect from 1st October, 2004 as per the notification

issued by the Central Government. The surcharge is not leviable on the STT.

Wealth Tax

Wealth tax, in India, is levied under Wealth-tax Act, 1957. Wealth tax is a tax

on the benefits derived from property ownership. The tax is to be paid year after

year on the same property on its market value, whether or not such property

yields any income.

Under the Act, the tax is charged in respect of the wealth held during the

assessment year by the following persons: -

IndividualHindu Undivided Family (HUF)Company

Chargeability to tax also depends upon the residential status of the assessee

same as the residential status for the purpose of the Income Tax Act.

Wealth tax is not levied on productive assets, hence investments in shares,

debentures, UTI, mutual funds, etc are exempt from it. The assets chargeable to

wealth tax are Guest house, residential house, commercial building, Motor car,

Jewellery, bullion, utensils of gold, silver, Yachts, boats and aircrafts, Urban

land and Cash in hand (in excess of Rs 50,000 for Individual & HUF only).

The following will not be included in Assets: -

Assets held as Stock in trade.A house held for business or profession.Any

property in nature of commercial complex.A house let out for more than 300

days in a year.Gold deposit bond.A residential house allotted by a Company to

an employee, or an Officer, or a Whole

Time Director (Gross salary i.e. excluding perquisites and before Standard

Deduction of such Employee, Officer, Director should be less than Rs

5,00,000).

The assets exempt from Wealth tax are "Property held under a trust", Interest of

the assessee in the coparcenary property of a HUF of which he is a member,

"Residential building of a former ruler", "Assets belonging to Indian

repatriates", one house or a part of house or a plot of land not exceeding

500sq.mts(for individual & HUF assessee)

Wealth tax is chargeable in respect of Net wealth corresponding to Valuation

date where Net wealth is all assets less loans taken to acquire those assets and

valuation date is 31st March of immediately preceding the assessment year. In

other words, the value of the taxable assets on the valuation date is clubbed

together and is reduced by the amount of debt owed by the assessee. The net

wealth so arrived at is charged to tax at the specified rates. Wealth tax is

charged @ 1 per cent of the amount by which the net wealth exceeds Rs 15

Lakhs.

Tax Rebates for Corporate Tax

The classical system of corporate taxation is followed in India

Domestic companies are permitted to deduct dividends received from other

domestic companies in certain cases.Inter Company transactions are honored if

negotiated at arm's length.Special provisions apply to venture funds and venture

capital companies.Long-term capital gains have lower tax incidence.There is no

concept of thin capitalization.Liberal deductions are allowed for exports and the

setting up on new industrial undertakings under certain circumstances.There are

liberal deductions for setting up enterprises engaged in developing, maintaining

and operating new infrastructure facilities and power-generating units.Business

losses can be carried forward for eight years, and unabsorbed depreciation can

be carried indefinitely. No carry back is allowed.Dividends, interest and long-

term capital gain income earned by an infrastructure fund or company from

investments in shares or long-term finance in enterprises carrying on the

business of developing, monitoring and operating specified infrastructure

facilities or in units of mutual funds involved with the infrastructure of power

sector is proposed to be tax exempt.

Capital Gains Tax

A capital gain is income derived from the sale of an investment. A capital

investment can be a home, a farm, a ranch, a family business, work of art etc. In

most years slightly less than half of taxable capital gains are realized on the sale

of corporate stock. The capital gain is the difference between the money

received from selling the asset and the price paid for it.

Capital gain also includes gain that arises on "transfer" (includes sale,

exchange) of a capital asset and is categorized into short-term gains and long-

term gains.

The capital gains tax is different from almost all other forms of taxation in that

it is a voluntary tax. Since the tax is paid only when an asset is sold, taxpayers

can legally avoid payment by holding on to their assets--a phenomenon known

as the "lock-in effect."

The scope of capital asset is being widened by including certain items held as

personal effects such as archaeological collections, drawings, paintings,

sculptures or any work of art. Presently no capital gain tax is payable in respect

of transfer of personal effects as it does not fall in the definition of the capital

asset. To restrict the misuse of this provision, the definition of capital asset is

being widened to include those personal effects such as archaeological

collections, drawings, paintings, sculptures or any work of art. Transfer of

above items shall now attract capital gain tax the way jewellery attracts despite

being personal effect as on date.

Short Term and Long Term capital Gains

Gains arising on transfer of a capital asset held for not more than 36 months (12

months in the case of a share held in a company or other security listed on

recognised stock exchange in India or a unit of a mutual fund) prior to its

transfer are "short-term". Capital gains arising on transfer of capital asset held

for a period exceeding the aforesaid period are "long-term".

Section 112 of the Income-Tax Act, provides for the tax on long-term capital

gains, at 20 per cent of the gain computed with the benefit of indexation and 10

per cent of the gain computed (in case of listed securities or units) without the

benefit of indexation.

Double Taxation Relief

Double Taxation means taxation of the same income of a person in more than

one country. This results due to countries following different rules for income

taxation. There are two main rules of income taxation i.e. (a) Source of income

rule and (b) residence rule.

As per source of income rule, the income may be subject to tax in the country

where the source of such income exists (i.e. where the business establishment is

situated or where the asset / property is located) whether the income earner is a

resident in that country or not.

On the other hand, the income earner may be taxed on the basis of the

residential status in that country. For example, if a person is resident of a

country, he may have to pay tax on any income earned outside that country as

well.

Further,some countries may follow a mixture of the above two rules. Thus,

problem of double taxation arises if a person is taxed in respect of any income

on the basis of source of income rule in one country and on the basis of

residence in another country or on the basis of mixture of above two rules.

In India, the liability under the Income Tax Act arises on the basis of the

residential status of the assessee during the previous year. In case the assessee is

resident in India, he also has to pay tax on the income, which accrues or arises

outside India, and also received outside India. The position in many other

countries being also broadly similar, it frequently happens that a person may be

found to be a resident in more than one country or that the same item of his

income may be treated as accruing, arising or received in more than one country

with the result that the same item becomes liable to tax in more than one

country.

Relief against such hardship can be provided mainly in two ways: (a) Bilateral

relief, (b) Unilateral relief.

Bilateral Relief

The Governments of two countries can enter into Double Taxation Avoidance

Agreement (DTAA) to provide relief against such Double Taxation, worked out

on the basis of mutual agreement between the two concerned sovereign states.

This may be called a scheme of 'bilateral relief' as both concerned powers agree

as to the basis of the relief to be granted by either of them.

Unilateral relief

The above procedure for granting relief will not be sufficient to meet all cases.

No country will be in a position to arrive at such agreement with all the

countries of the world for all time. The hardship of the taxpayer however is a

crippling one in all such cases. Some relief can be provided even in such cases

by home country irrespective of whether the other country concerned has any

agreement with India or has otherwise provided for any relief at all in respect of

such double taxation. This relief is known as unilateral relief.

Double Taxation Avoidance Agreement (DTAA)

List of countries with which India has signed Double Taxation Avoidance

Agreement :

DTAA Comprehensive Agreements - (With respect to taxes on income)DTAA

Limited Agreements – With respect to income of airlines/ merchant

shippingLimited Multilateral AgreementDTAA Other Agreements/Double

Taxation Relief RulesSpecified Associations AgreementTax Information

Exchange Agreement (TIEA)

Indirect Taxation

Sales tax

Central Sales Tax (CST)

Central Sales tax is generally payable on the sale of all goods by a dealer in the

course of inter-state trade or commerce or, outside a state or, in the course of

import into or, export from India.

The ceiling rate on central sales tax (CST), a tax on inter-state sale of goods, has

been reduced from 4 per cent to 3 per cent in the current year.

Value Added Tax (VAT)

VAT is a multi-stage tax on goods that is levied across various stages of

production and supply with credit given for tax paid at each stage of Value

addition. Introduction of state level VAT is the most significant tax reform

measure at state level. The state level VAT has replaced the existing State Sales

Tax. The decision to implement State level VAT was taken in the meeting of

the Empowered Committee (EC) of State Finance Ministers held on June 18,

2004, where a broad consensus was arrived at to introduce VAT from April 1,

2005. Accordingly, all states/UTs have implemented VAT.

The Empowered Committee, through its deliberations over the years, finalized a

design of VAT to be adopted by the States, which seeks to retain the essential

features of VAT, while at the same time, providing a measure of flexibility to

the States, to enable them to meet their local requirements. Some salient

features of the VAT design finalized by the Empowered Committee are as

follows:

The rates of VAT on various commodities shall be uniform for all the

States/UTs. There are 2 basic rates of 4 per cent and 12.5 per cent, besides an

exempt category and a special rate of 1 per cent for a few selected items. The

items of basic necessities have been put in the zero rate bracket or the exempted

schedule. Gold, silver and precious stones have been put in the 1 per cent

schedule. There is also a category with 20 per cent floor rate of tax, but the

commodities listed in this schedule are not eligible for input tax rebate/set off.

This category covers items like motor spirit (petrol), diesel, aviation turbine

fuel, and liquor.There is provision for eliminating the multiplicity of taxes. In

fact, all the State taxes on purchase or sale of goods (excluding Entry Tax in

lieu of Octroi) are required to be subsumed in VAT or made VATable.Provision

has been made for allowing "Input Tax Credit (ITC)", which is the basic feature

of VAT. However, since the VAT being implemented is intra-State VAT only

and does not cover inter-State sale transactions, ITC will not be available on

inter-State purchases.Exports will be zero-rated, with credit given for all taxes

on inputs/ purchases related to such exports.There are provisions to make the

system more business-friendly. For instance, there is provision for self-

assessment by the dealers. Similarly, there is provision of a threshold limit for