Independent Technical Experts Report on the Mineral Assets of ...

151

Transcript of Independent Technical Experts Report on the Mineral Assets of ...

i

Independent Competent Person’s Report Without Valuations December 2010

COMPETENT PERSON’S REPORT (CPR)

ON THE MINERAL ASSETS

OF SYLVANIA RESOURCES LIMITED

(SYLVANIA) WITHOUT VALUATIONS

BY VENMYN RAND (PTY) LIMITED

(VENMYN)

The Directors Sylvania Resources Limited Constantia View Office Park Block 3, 2 Hogsback Road Quellerina Extn 4 1709 Johannesburg South Africa The Directors Ambrian Partners Limited Old Change House 128 Queen Victoria Street London EC4V4BJ

SYNOPSIS

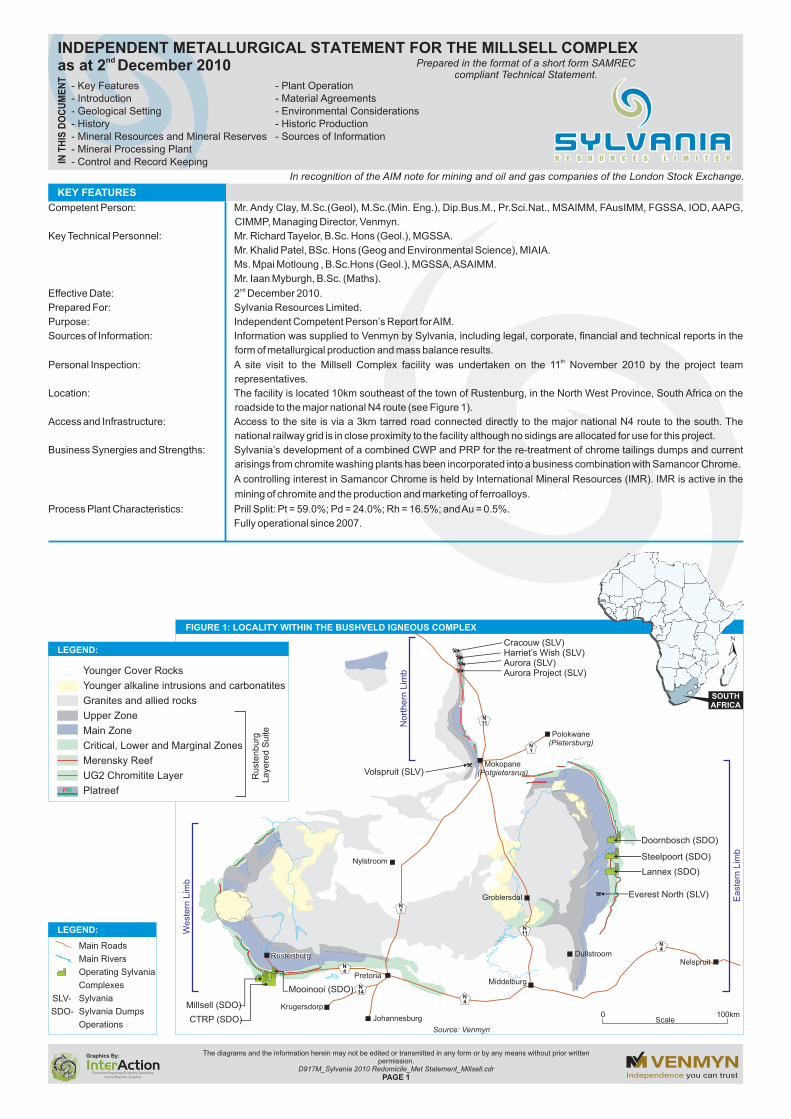

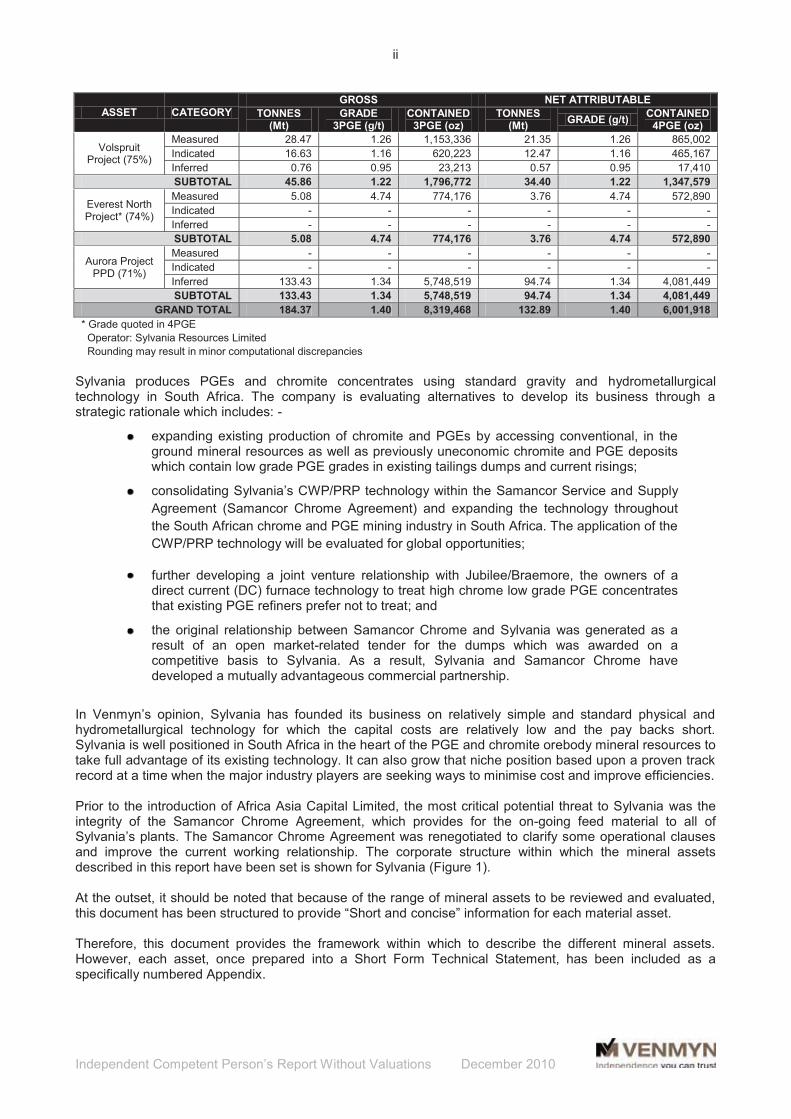

Sylvania has established a chrome recovery and platinum group elements (PGEs) processing and extraction business in South Africa predicated on its ability to build and operate metallurgical concentrators designed and engineered to treat tailings produced by both historical and current mining operations. Sylvania Metals (Pty) Limited (Sylvania Metals), the entity that operates the processing and extraction business in South Africa, is now 100% owned by Sylvania following the recent acquisition by Sylvania of a 26% shareholding in Sylvania Metals that was previously held by its BEE partner, Ehlobo. This 26% shareholding in Sylvania Metals was exchanged for an approximate 19.5% share in Sylvania through the issue of 58,882,551 new Sylvania ordinary shares to a nominee of Africa Asia Capital Limited which is a subsidiary of International Mineral Resources (IMR). IMR owns a controlling interest in Samancor Chrome which owns and operates a number of chrome mines, ferrochrome smelters and tailing dams in South Africa. Sylvania has entered into an agreement with Samancor Chrome to treat its current tailings risings and its existing tailings dams using the Sylvania Chromite Washing Plant (CWP) and PGE Recovery Plant (PRP) technology. The primary purpose of the Sylvania relationship with Samancor Chrome is to enable new technologies to be applied to the chromite miners of the Bushveld Igneous Complex (BIC) so that Samancor Chrome can benefit from increased chromite recovery efficiencies whilst Sylvania can generate revenues from PGE recoveries. The recovery of PGEs from chromite has only been of commercial interest over the past 7 years as previously the PGE grades were considered uneconomic by the chrome miners. In addition, Sylvania has acquired mineral resources in the Northern Limb of the BIC which will be required to realise its smelting and refining initiative. Sylvania has commenced with exploration work to further develop these projects. There are plans to develop the Volspruit Project to a Bankable Feasibility Study by 2011, while carrying out exploration on the farms Harriet’s Wish, Aurora and Cracouw with the aim of defining a mineral resource for the prospect. The AIM Note for mining and oil and gas companies Appendix 3 summary of reserves and resources is presented below:-

ii

Independent Competent Person’s Report Without Valuations December 2010

ASSET CATEGORY GROSS NET ATTRIBUTABLE

TONNES (Mt)

GRADE 3PGE (g/t)

CONTAINED 3PGE (oz)

TONNES (Mt)

GRADE (g/t) CONTAINED

4PGE (oz)

Volspruit Project (75%)

Measured 28.47 1.26 1,153,336 21.35 1.26 865,002

Indicated 16.63 1.16 620,223 12.47 1.16 465,167

Inferred 0.76 0.95 23,213 0.57 0.95 17,410

SUBTOTAL 45.86 1.22 1,796,772 34.40 1.22 1,347,579

Everest North Project* (74%)

Measured 5.08 4.74 774,176 3.76 4.74 572,890

Indicated - - - - - -

Inferred - - - - - -

SUBTOTAL 5.08 4.74 774,176 3.76 4.74 572,890

Aurora Project PPD (71%)

Measured - - - - - -

Indicated - - - - - -

Inferred 133.43 1.34 5,748,519 94.74 1.34 4,081,449

SUBTOTAL 133.43 1.34 5,748,519 94.74 1.34 4,081,449

GRAND TOTAL 184.37 1.40 8,319,468 132.89 1.40 6,001,918

* Grade quoted in 4PGE

Operator: Sylvania Resources Limited

Rounding may result in minor computational discrepancies

Sylvania produces PGEs and chromite concentrates using standard gravity and hydrometallurgical technology in South Africa. The company is evaluating alternatives to develop its business through a strategic rationale which includes: -

expanding existing production of chromite and PGEs by accessing conventional, in the ground mineral resources as well as previously uneconomic chromite and PGE deposits which contain low grade PGE grades in existing tailings dumps and current risings;

consolidating Sylvania’s CWP/PRP technology within the Samancor Service and Supply

Agreement (Samancor Chrome Agreement) and expanding the technology throughout

the South African chrome and PGE mining industry in South Africa. The application of the

CWP/PRP technology will be evaluated for global opportunities;

further developing a joint venture relationship with Jubilee/Braemore, the owners of a direct current (DC) furnace technology to treat high chrome low grade PGE concentrates that existing PGE refiners prefer not to treat; and

the original relationship between Samancor Chrome and Sylvania was generated as a result of an open market-related tender for the dumps which was awarded on a competitive basis to Sylvania. As a result, Sylvania and Samancor Chrome have developed a mutually advantageous commercial partnership.

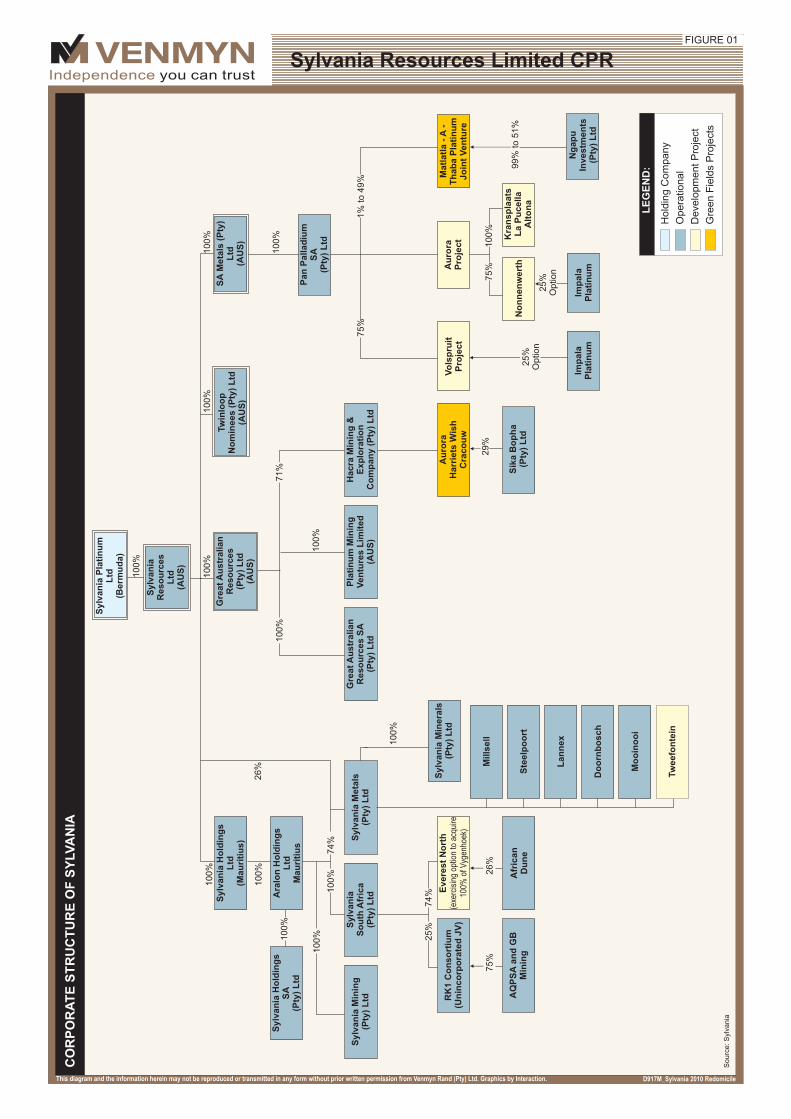

In Venmyn’s opinion, Sylvania has founded its business on relatively simple and standard physical and hydrometallurgical technology for which the capital costs are relatively low and the pay backs short. Sylvania is well positioned in South Africa in the heart of the PGE and chromite orebody mineral resources to take full advantage of its existing technology. It can also grow that niche position based upon a proven track record at a time when the major industry players are seeking ways to minimise cost and improve efficiencies. Prior to the introduction of Africa Asia Capital Limited, the most critical potential threat to Sylvania was the integrity of the Samancor Chrome Agreement, which provides for the on-going feed material to all of Sylvania’s plants. The Samancor Chrome Agreement was renegotiated to clarify some operational clauses and improve the current working relationship. The corporate structure within which the mineral assets described in this report have been set is shown for Sylvania (Figure 1). At the outset, it should be noted that because of the range of mineral assets to be reviewed and evaluated, this document has been structured to provide “Short and concise” information for each material asset. Therefore, this document provides the framework within which to describe the different mineral assets. However, each asset, once prepared into a Short Form Technical Statement, has been included as a specifically numbered Appendix.

iii

Independent Competent Person’s Report Without Valuations December 2010

The report process took into account the principles incorporated in the requirements of the Regulatory Guides Numbers 111 and 112 of the Australian Securities and Investments Commission (ASIC), ASIC consultation Paper 143 (which relates to Regulatory Guides 111 and 112), and the Note for Mining and Oil and Gas Companies – June 2009 of the Alternative Investment Market (AIM). The Technical Statements are intended to incorporate all material issues required by the expert reporting codes and, in particular, JORC and VALMIN, of Australasia, and SAMCODE, of South Africa. The Tweefontein Complex is under review and negotiations are taking place for Sylvania to take over the existing “Green” CWP at the Tweefontein site. A scoping level study will be designed to replicate processes at Mooinooi. Whilst this is conceptual, the experience at Mooinooi should lead to successful implementation. The cost and timing will be defined shortly. In respect of the Volspruit Project, the initial Sylvania feasibility work demonstrates a positive NPV valuation but this will be prepared into a Definitive Feasibility Study over the next year and may demonstrate additional upside potential. The mass balances contained within the Metallurgical Statements were accurate at the time of the release of the document, but are subject to change with future developments. The information in this report (and the appendices) relating to exploration results, mineral resources and ore reserves is based on information compiled by Andrew Neil Clay, who is a Fellow of the Australasian Institute of Mining and Metallurgy, as set out in Appendix 3 (Qualifications, Declarations and Consents), has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person, as defined in the 2004 Edition of the JORC Code. Mr Clay is employed by Venmyn.

iv

Independent Competent Person’s Report Without Valuations December 2010

DISCLAIMER AND RISKS This Competent Person’s Report has been prepared by Venmyn. In the preparation of the report, Venmyn has utilised information relating to operational methods and expectations provided to it by Sylvania. Where possible, Venmyn has verified this information from independent sources after making due enquiry on all material issues that are required in order to comply with the Code for Technical Assessment of Mineral and Petroleum Assets and Securities for Competent Person’s Reports (Valmin Code). Venmyn and its directors accept no liability for any losses arising from reliance upon the information presented in this report.

OPERATIONAL RISKS The businesses of mining and mineral exploration, development and production by their nature contain significant operational risks. The businesses depend upon, amongst other things, successful prospecting programmes and competent management.

POLITICAL AND ECONOMIC RISK Factors such as political and industrial disruption, currency fluctuation and interest rates could have an impact on Sylvania’s future operations. The majority of these factors are, and will be, beyond the control of Sylvania or any other operating entity.

v

Independent Competent Person’s Report Without Valuations December 2010

COMPETENT PERSON’S REPORT (CPR)

ON THE MINERAL ASSETS

OF SYLVANIA RESOURCES LIMITED

(SYLVANIA) BY

VENMYN RAND (PTY) LIMITED (VENMYN)

SYNOPSIS

LIST OF CONTENTS

1. NATURE AND SCOPE OF THE REPORT ................................................................................................. 1

1.1. Nature and Purpose of the Report ................................................................................................. 1

1.2. Basis of the Assessment ................................................................................................................ 1

1.3. Sources of Information ................................................................................................................... 1

1.4. Limitations and Reliance on Information ........................................................................................ 1

2. INDUSTRY OVERVIEW .............................................................................................................................. 3

2.1. Chrome and Ferrochrome Sector .................................................................................................. 3

2.1.1. Geology and Mineralogy ................................................................................................. 3

2.1.2. Geology of the Bushveld ................................................................................................. 4

2.1.3. Occurrence and Mining ................................................................................................... 4

2.1.4. World Production and Global Development ................................................................... 9

2.1.5. Ore Processing ............................................................................................................. 10

2.1.6. Uses and Applications .................................................................................................. 11

2.1.7. Ferroalloys .................................................................................................................... 11

2.1.8. Future Trends ............................................................................................................... 12

2.1.9. The Asian Influence ...................................................................................................... 13

2.1.10. Supply/Demand Dynamics for Chromite ...................................................................... 13

2.2. PGE Sector .................................................................................................................................. 14

2.2.1. Introduction ................................................................................................................... 14

2.2.2. Geology and Mineralogy ............................................................................................... 14

2.2.3. Occurrence and Mining ................................................................................................. 15

2.2.4. World Production and Global Development ................................................................. 16

2.2.5. Ore Processing ............................................................................................................. 20

2.2.6. Concentration ............................................................................................................... 20

2.2.7. Smelting ........................................................................................................................ 21

2.2.8. Base Metal Refining (BMR) .......................................................................................... 22

2.2.9. Precious Metal Refining (PMR) .................................................................................... 23

2.2.10. Low Grade Concentrate Processing ............................................................................. 24

3. South Africa’s Political and Economic Status ............................................................................................ 25

3.1. Political Climate ............................................................................................................................ 25

3.2. Economic Climate and Fiscal Regime ......................................................................................... 25

3.3. Industrial Relations ....................................................................................................................... 26

3.4. South African Infrastructure Capacity .......................................................................................... 26

3.5. Minerals Industry .......................................................................................................................... 27

3.6. South African Mining Law ............................................................................................................ 27

3.6.1. Mineral and Petroleum Resources Development Act (MPRDA) .................................. 27

3.6.2. Broad-Based Socio-Economic Charter for the South African Mining Industry ............. 28

3.6.3. Amendment of the Broad Based Socio-Economic Empowerment Charter .................. 29

3.6.4. Mineral and Petroleum Reserves Royalty Act (MPRRA) ............................................. 29

3.6.5. Chromium Mineral Rights from UG2 Mined for PGEs .................................................. 30

4. PROFILE OF THE SYLVANIA GROUP .................................................................................................... 30

4.1. Overview ...................................................................................................................................... 30

vi

Independent Competent Person’s Report Without Valuations December 2010

4.2. Location ........................................................................................................................................ 30

4.3. Corporate Structure and Management ........................................................................................ 30

4.4. Samancor Chrome Mining and Tailings Operations .................................................................... 32

5. SYLVANIA MINERALS (PTY) LIMITED MINERAL ASSETS ................................................................... 33

5.1. Introduction to the Plant Complex ................................................................................................ 33

5.2. Summary ...................................................................................................................................... 34

6. SYLVANIA SOUTH AFRICA (PTY) LIMITED ........................................................................................... 34

6.1. Introduction ................................................................................................................................... 34

7. GREAT AUSTRALIAN RESOURCES LIMITED ....................................................................................... 35

7.1. Introduction ................................................................................................................................... 35

8. S A METALS LIMITED .............................................................................................................................. 35

8.1. Introduction ................................................................................................................................... 35

9. LEGAL ASPECTS AND TENURE ............................................................................................................. 35

9.1. Material Agreements .................................................................................................................... 38

9.1.1. Samancor Services Supply Agreement ........................................................................ 38

9.1.2. Offtake Agreements ...................................................................................................... 38

9.2. Environmental Considerations ..................................................................................................... 38

LIST OF APPENDICES

Appendix 1: Glossary of Terms ....................................................................................................................... 40

Appendix 2: Abbreviations ............................................................................................................................... 42

Appendix 3: Qualifications, Declarations and Consents .................................................................................. 44

Appendix 4: Metallurgical Statement for Millsell Complex ............................................................................... 59

Appendix 7: Metallurgical Statement for Mooinooi Complex ........................................................................... 60

Appendix 9: Metallurgical Statement for CTRP Complex ................................................................................ 61

Appendix 5: Metallurgical Statement for Lannex Complex .............................................................................. 62

Appendix 6: Metallurgical Statement for Steelpoort Complex ......................................................................... 63

Appendix 8: Metallurgical Statement for Doornbosch Complex ...................................................................... 64

Appendix 10: Technical Statement for Everest North Project ......................................................................... 65

Appendix 11: Technical Statement for Cracouw 391 LR (HACRA Project) .................................................... 66

Appendix 12: Technical Statement for Aurora 397 LR (HACRA Project) ........................................................ 67

Appendix 13: Technical Statement for Harriet’s Wish 393 LR (HACRA Project) ............................................ 68

Appendix 14: Technical Statement for Volspruit Project ................................................................................. 69

Appendix 15: Technical Statement for Aurora Project .................................................................................... 70

LIST OF FIGURES Figure 1: Corporate Structure of Sylvania ......................................................................................................... 2

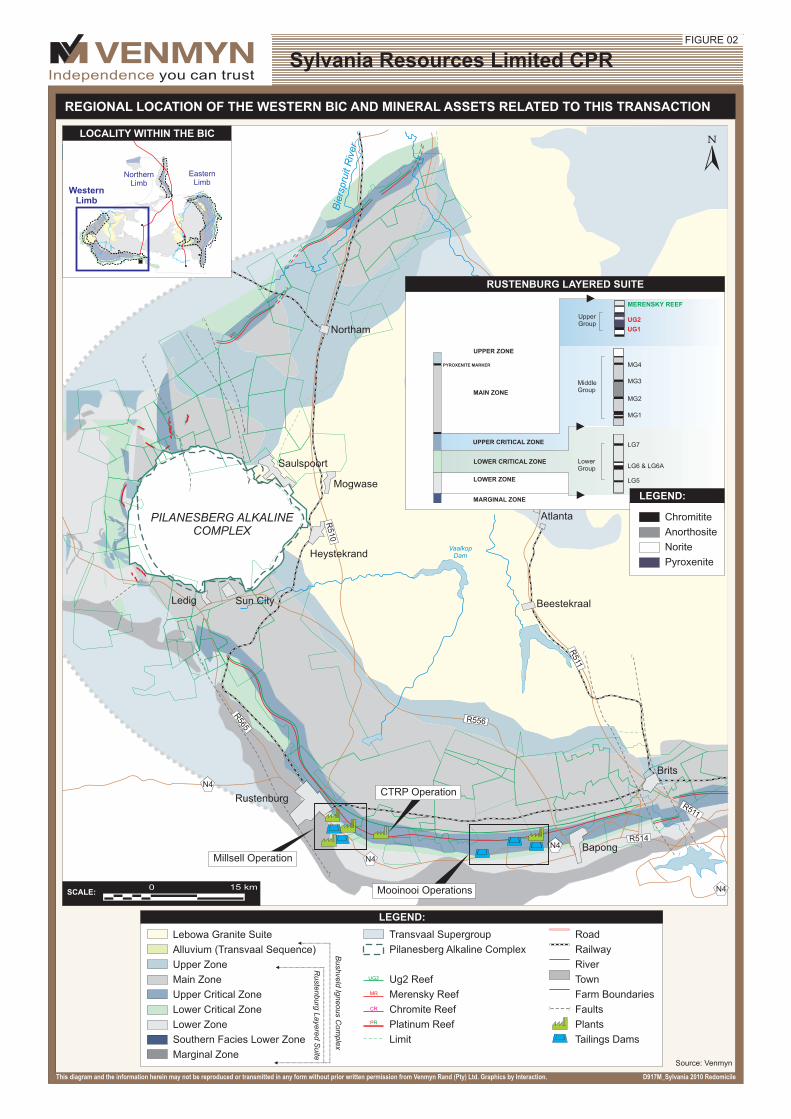

Figure 2: Regional Location of the Western BIC and Related Mineral Assets to this Transaction ................... 5

Figure 3: Regional Location of the Eastern Bushveld and Mineral Assets Related to this Transaction ........... 6

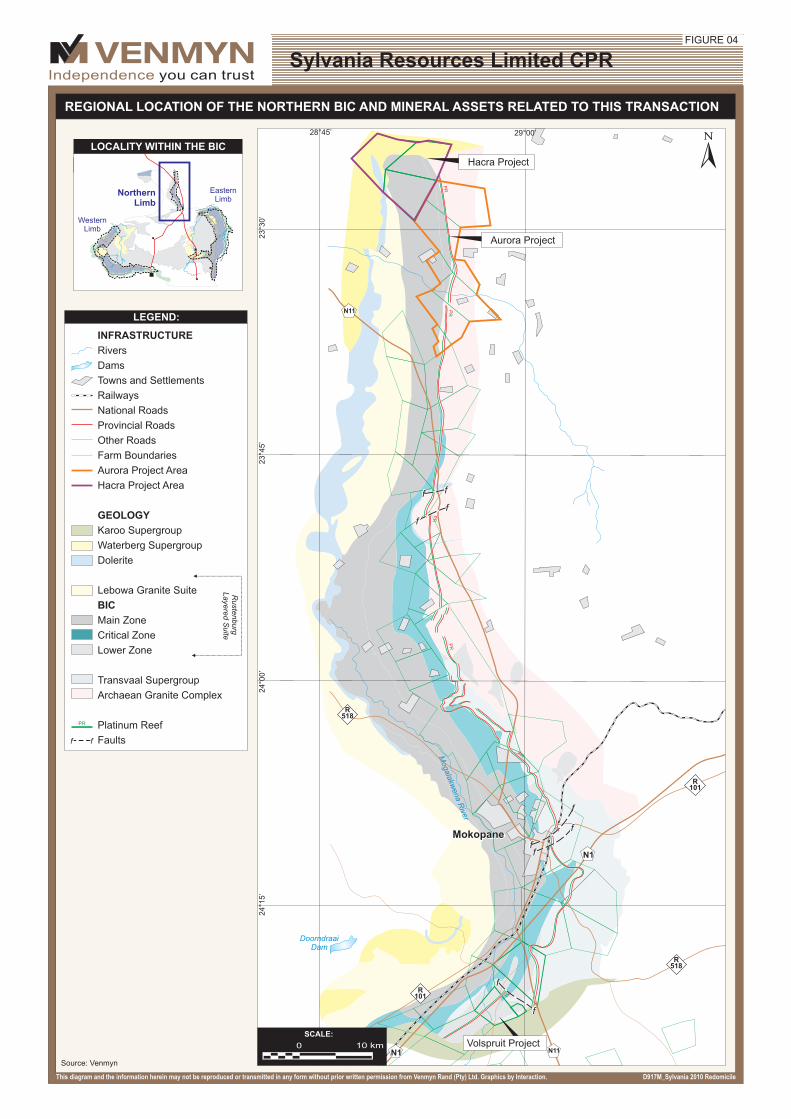

Figure 4: Regional Location of the Northern Bushveld and Mineral Assets Related to this Transaction .......... 7

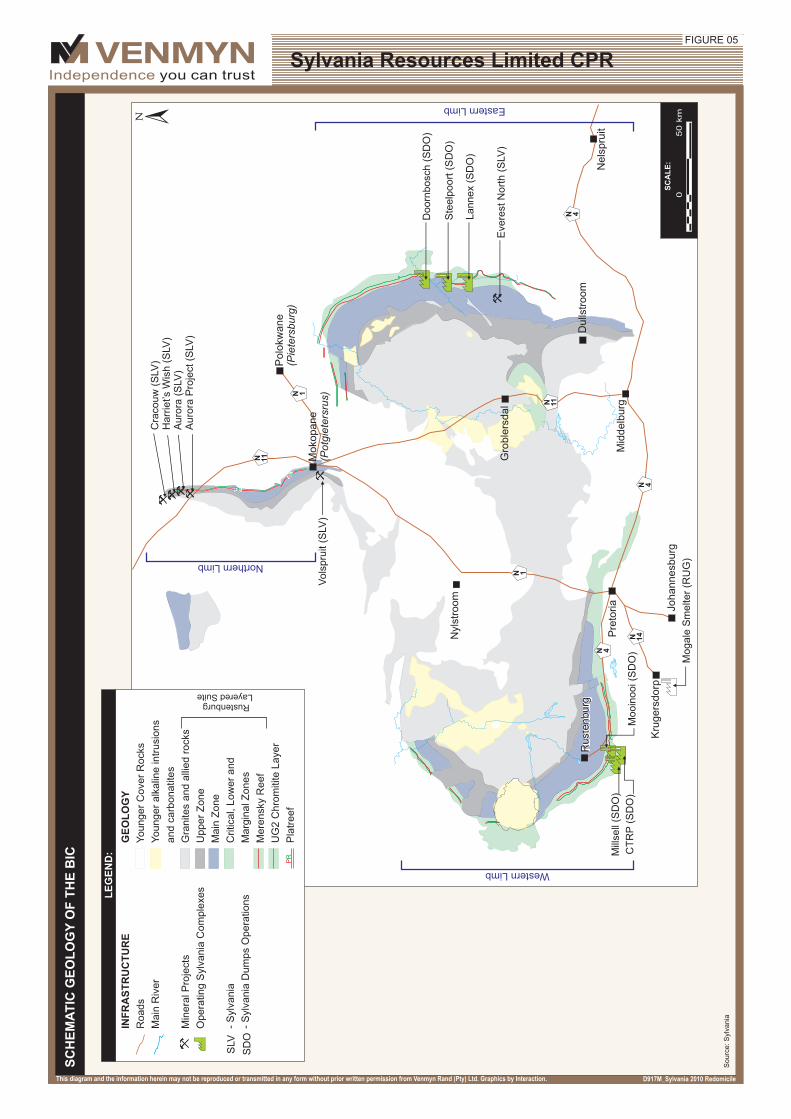

Figure 5: Schematic Geology of the BIC ........................................................................................................... 8

LIST OF TABLES

Table 1: Global Chromite Mineral Resources and Mineral Reserves ............................................................... 9

Table 2: Global Chromite Production 2007 ....................................................................................................... 9

Table 3: Global Chromite Production 2008 ....................................................................................................... 9

Table 4 : Global Chromite Production 2009 ...................................................................................................... 9

Table 5: High Carbon Ferrochrome Production in 2007 .................................................................................. 11

Table 6 : High Carbon Ferrochrome Production in 2009 ................................................................................. 11

vii

Independent Competent Person’s Report Without Valuations December 2010

Table 7: Low and Medium Carbon Ferrochrome Production 2007 ................................................................. 12

Table 8 : Low and Medium Carbon Ferrochrome Production 2009 ................................................................ 12

Table 9: Typical Compositions of Various Grades of Chromite....................................................................... 12

Table 10: Global Platinum and Palladium Mineral Resources as at 2009 ...................................................... 15

Table 11: Platinum and Palladium Production in 2008 .................................................................................... 16

Table 12: Key Features of the PGE Extraction Business ................................................................................ 23

Table 13: Characteristics of BIC PGE Ore Types ........................................................................................... 24

Table 14: Types of Rights Applicable to Mining in South Africa ...................................................................... 28

Table 15: Attributable Equity of Sylvania South Africa .................................................................................... 35

Table 16: Attributable Equity of GAU ............................................................................................................... 35

Table 17: Attributable Equity of SA Metals ...................................................................................................... 35

Table 18: Summary of the Legal Tenement for Sylvania’s Mineral Properties ............................................... 36

1

Independent Competent Person’s Report Without Valuations December 2010

1. NATURE AND SCOPE OF THE REPORT

1.1. Nature and Purpose of the Report

This Competent Person’s Report has been prepared for Sylvania to describe and define the technical issues relevant to specific mineral assets within the Sylvania corporate structure. Sylvania intends changing its domicile from Australia to Bermuda by way of it becoming held by a newly incorporated Bermudan entity called Sylvania Platinum Limited that will be listed on the ASX and AIM. The existing reporting jurisdiction of Sylvania has led to this document being prepared in accordance with the Code for Technical Assessment of Mineral and Petroleum Assets and Securities for Competent Person’s Reports (Valmin Code). The principal author of this report is a fellow of the Australasian Institute of Mining and Metallurgy (AusIMM) as well as the South African regulatory bodies in the minerals industry. Venmyn was not required to comment on the fairness of any vendor or promoter considerations in relation to any of the properties which are the subject of this report and no opinion in that regard has been offered. However, the reasonableness of the underlying assumptions and the proposed business plan for each individual mineral asset has been assessed.

1.2. Basis of the Assessment

An information gathering process and investigation into the mineral assets held by Sylvania was undertaken during November 2010. This process and the information so gathered were supported by discussions with the various company management and employee representatives, together with site visits where possible. This information was used to substantially update a comprehensive review carried out by Venmyn in October 2009. The relevant details pertaining to the assessment of prospectivity, operating performance and the combination of technical issues for each mineral asset were then consolidated into compliant Short Form Technical Statements. These represent stand alone reports for each mineral asset and have been incorporated into this document as duly marked Appendices. Venmyn has, to the best of its abilities, applied its mind to the reasonableness of the information and parameters pertaining to each mineral asset.

1.3. Sources of Information

Sylvania management provided full and open access to its records and information on its mineral assets. This included corporate, legal, financial and operating information for existing plants, proposed plants and mineral projects. At the same time, the commercial and technical arrangements between Sylvania and Samancor Chrome were also provided since Samancor Chrome is the owner of the source materials for the majority of the existing CWP and PRP operations. Additional sources included the press releases and other public domain information available electronically via the Internet.

1.4. Limitations and Reliance on Information

Venmyn considers that its expert work must be prepared and considered within the context of Sylvania’s business plan to appreciate the status of the mineral assets. Venmyn’s view is also based upon technical, financial and other conditions and expectations prevailing at the date of this report. These conditions and expectations could change over relatively short periods of time. To the extent that there are legal issues relating to the mineral assets or issues relating to compliance by Sylvania with applicable laws, regulations and policies, Venmyn assumes no responsibility and offers no legal opinion or interpretation on these issues.

3

Independent Competent Person’s Report Without Valuations December 2010

2. INDUSTRY OVERVIEW

2.1. Chrome and Ferrochrome Sector

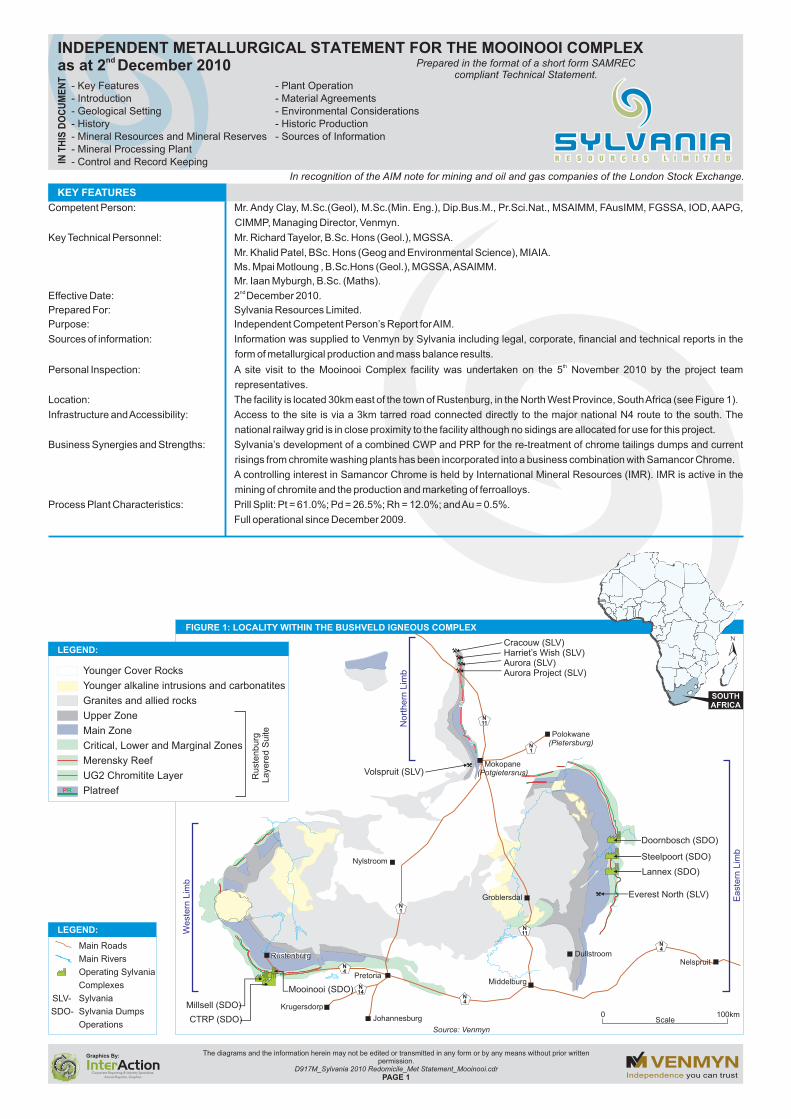

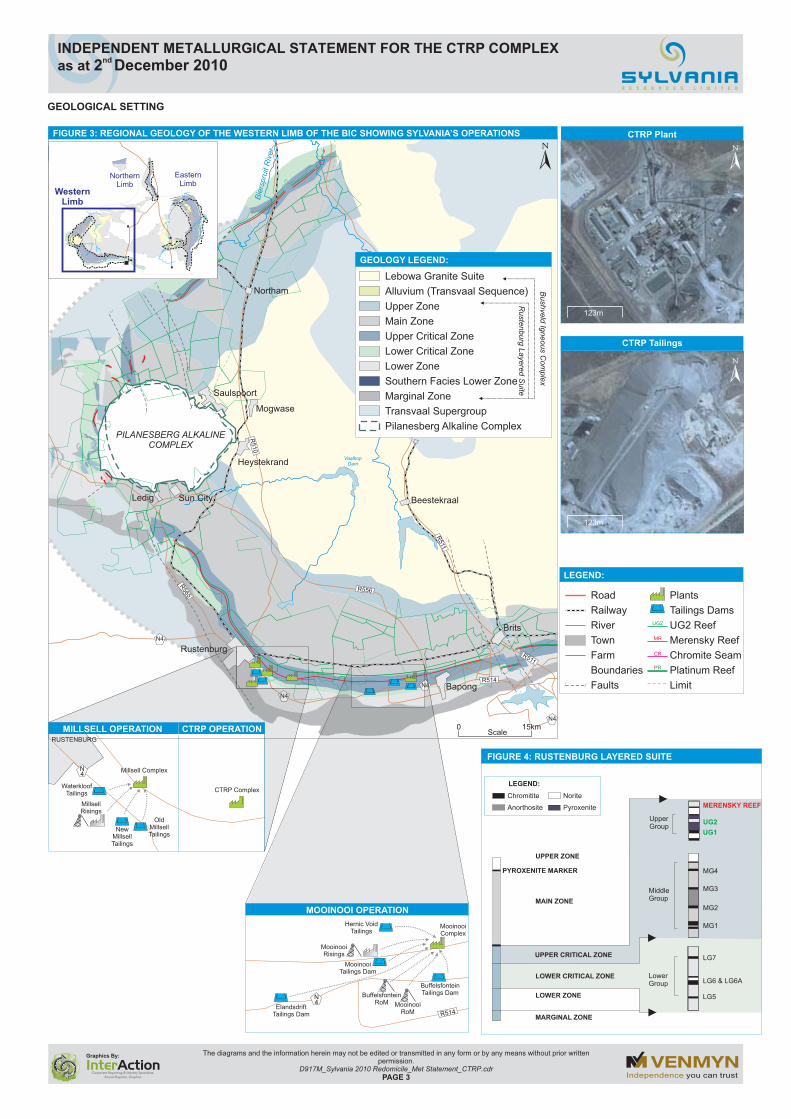

A short review of the global chromite production, supply and demand, and pricing has been prepared to set the context for the South African industry within which Sylvania’s technology is presently applied. The regional location of the Western, Eastern and Northern limbs of the BIC is shown in Figure 2, Figure 3 and Figure 4. Firstly, chromium is the most abundant of the Group VIA family of metallic elements, consisting of chromium, molybdenum and tungsten. At a concentration of nearly 400ppm in the earth's crust, it is the 13

th most common element. The only

commercial ore of chromium is chromite. 2.1.1. Geology and Mineralogy

Chromium ore, or chromite, occurs exclusively in rocks formed by the intrusion and solidification of molten lava or magma which is rich in the heavy, iron containing minerals such as pyroxenes and olivines. Within these rocks, often referred to as ultramafic igneous rocks, chromium occurs as a chromium spinel, a highly complex mineral made up, in its form, of magnesium as MgO and aluminium as Al2O3. However, the magnesium can be substituted in varying proportions by divalent iron, and the aluminium can be substituted, also in varying proportions, by trivalent chromium and trivalent iron. This actually improves the Cr:Fe ratio. For this reason, the chromium spinel may be represented as (Fe,Mg)O(Cr,Fe,Al)2O3. Large variations in the total and relative amounts of Cr and Fe in the lattice occur in different deposits. These affect the ore grade not only in terms of the Cr2O3 content but also in the Cr:Fe ratio which determines the chromium content of the ferrochromium produced. This is a very important ratio. The variations in this ratio also affect the reducibility of the ore. For example, increasing amounts of magnesium compared with iron in the divalent site will make the spinel more difficult to reduce. Conversely, increasing amounts of iron in the trivalent site, replacing aluminium, will increase the reducibility of the spinel. The greater the refractory index, the more refractory, or less reducible, the ore is. Chromium spinel is a heavy mineral and it concentrates through gravity separation from most of the other molten material in the magma during crystallisation from the cooling magma. Commercial chromite deposits are found mainly in two forms which are:-

stratiform seams in basin-like intrusions, often multiple seams through repeated igneous injections; and

the more irregular podiform or lenticular deposits.

The best known example of a stratiform deposit is the BIC of South Africa. This complex contains approximately 72% of the world's chromite reserves. The Great Dyke of Zimbabwe, traversing nearly the length of the country (NNE to SSW), is very similar and has been linked to the BIC in geological history. These two features are well-known also for their important and very large commercial deposits of PGEs. Other stratiform deposits occur in Madagascar and in the Orissa district of India. Stratiform deposits are generally very large complexes. They can be more than 5km thick and cover thousands of square kilometres. The podiform deposits are relatively small in comparison and may be shaped as pods, lenses, slabs or other irregular shapes. Many have been extensively altered to serpentine and they are often faulted. They are generally richer in chromium than the stratiform deposits and have higher Cr:Fe ratios. Mineral resources in Kazakhstan are of the podiform type. Podiform ores were originally sought after as the best source of metallurgical grade chromite for high-carbon ferrochromium. These ores also tend to be massive (hard lumpy) ores, as opposed to the softer, more friable ores from the stratiform deposits, and this makes for better electric smelting operation. There is a third type of chromite deposit but of very limited commercial significance. These are the eluvial and alluvial deposits that have been formed by weathering of chromite-bearing rock and release of the chromite spinels with subsequent gravity concentration by flowing water.

4

Independent Competent Person’s Report Without Valuations December 2010

2.1.2. Geology of the Bushveld

The Kaapvaal and Zimbabwe cratons in Southern Africa are characterised by the presence of large mafic to ultramafic layered complexes. By far the most important and economically viable of these is the BIC, which was intruded 2.06bn years ago into the rocks of the Transvaal Supergroup along the unconformity between the Magaliesburg quartzites and the overlying Rooiberg felsites. The total estimated area of the BIC is 66,000km

2, about 55% of which is covered by younger formations. The mafic rocks of the

BIC can be divided into a number of units according to their representative gravity anomalies. These include the northwestern and southwestern lobes, separated by the Pilanesberg Alkaline Complex, and the north eastern and south eastern lobes that are separated by the Steelpoort fault. The geology and stratigraphy of the BIC is presented in Figure 2, Figure 3 and Figure 4. The mafic rocks (collectively known as the Rustenburg Layered Suite - RLS) can be divided into five zones known (from the top downwards, as shown in Figure 2, Figure 3 and Figure 4) as:-

Upper Zone (UZ);

Main Zone (MZ);

Critical Zone (CZ);

Lower Zone (LZ); and

Marginal Zone.

At the base, the Marginal Zone consists of generally finer-grained rocks than those of the interior of the complex and contains an abundance of xenoliths. It is highly variable in thickness, may be completely absent in some areas and contains no economic mineralisation. The chromite layers are confined to the Critical Zone and are subdivided into Lower, Middle, and Upper Groups. All the layers of the Lower Group (LG) occur within the pyroxenites of the Lower Critical Zone. The Middle Group (MG) of layers occur at the transition from the Lower to the Upper Critical Zone, at a level where plagioclase first becomes persistently cumulus within the whole BIC sequence. The MG chromitite layers are either hosted by pyroxenites or by plagioclase-rich norites and anorthosites. The Upper Group (UG) of layers occur within the Upper Critical Zone below the Merensky Reef. The LG contains seven layers, the MG four, and the UG two layers in the western BIC and three layers in the eastern BIC. The most productive layers for chromite have been the LG6, MG4 and MG2 horizons.

2.1.3. Occurrence and Mining

The International Chromium Development Association (ICDA) estimates that world chromite reserves total 3.6Bt, with resources (exclusive of reserves) totalling 7.5Bt (Table 1). The most intensive mining occurs in the BIC, in South Africa. South Africa’s reserves and resources are the largest in the world, and consist of 3.1Bt and 5.5Bt, respectively. Zimbabwe’s resources are also substantial, and it ranks second in global chromite resources, with 1Bt. Zimbabwe exploits both stratiform deposits in the Great Dyke and podiform deposits in the Selukwe and Belingwe areas. Kazakhstan, meanwhile, ranks second in global chromite mineral reserves and third in global resources. It has podiform deposits in the Southern Ural Mountain region, with greatly varying chromium content and in Cr:Fe ratios. Finland and India each have 1% of the world’s reserves, but Finland has 2% of the world’s resources, compared with 1% in India. India's podiform bodies lie on the east coast of the state of Orissa while Finland’s are located near Kemi in northern Finland. Finland’s Cr2O3 content in its deposits is low, but the ore is successfully mined, concentrated and smelted to ferrochrome, and converted to stainless steel thereafter. Various other countries are home to the remaining 1% of global reserves and 7% of global resources. The potential reserves and resources that can be found in China have yet to be quantified, although the country is known to have podiform and stratiform deposits.

9

Independent Competent Person’s Report Without Valuations December 2010

Historically, there was sufficient high-grade metallurgical ore to meet demand. However, rapid growth in the stainless and other alloy steel industries have led to much larger reserves with lower Cr grade and higher iron content having to be exploited. Table 1: Global Chromite Mineral Resources and Mineral Reserves

RESERVES RANK RESOURCES1 RANK

COUNTRY Mt % Mt %

South Africa 3,100 85% 1 5,500 73% 1

Kazakhstan 320 9% 2 320 4% 3

Zimbabwe 140 4% 3 1,000 13% 2

Finland 41 1% 4 120 2% 4

India 27 1% 4 67 1% 5

Others 38 1% 555 7%

TOTAL 3,666 100% 7,562 100 1 Reported exclusively of reserves

2.1.4. World Production and Global Development

The years 2007, 2008 and 2009 have shown a steady drop in chromite production, as can be seen in Table 2, Table 3 and Table 4. Table 2: Global Chromite Production 2007

COUNTRY 2007 CHROMITE PRODUCTION

Mt %

South Africa 8.58 39

Kazakhstan 3.74 17

India 3.30 15

Brazil, Finland, Russia, Turkey, Zimbabwe 4.18 19

Others 2.20 10

TOTAL 22.00 100

Table 3: Global Chromite Production 2008

COUNTRY 2008 CHROMITE PRODUCTION

Mt %

South Africa 9.6 45%

Kazakstan 3.7 17%

India 3.3 15%

Others 4.9 23%

TOTAL 21.5 100%

Table 4 : Global Chromite Production 2009

COUNTRY 2009 CHROMITE PRODUCTION1

Mt %

South Africa 6.27 33%

India 3.8 20%

Kazakstan 3.23 17%

Brazil, Finland, Oman, Russia, Turkey 3.99 21%

Others 1.71 9%

TOTAL 19 100% 1 Estimate

This can largely be attributed to the global economic slowdown which had resulted in chromite producers reducing production, and is seen as uncharacteristic for an industry with has seen:-

demand for chromium alloys expanding by some 5% annually over the past decade; and

the output of chromite ore following alloy demand increases closely, with an average growth rate of 4.6% per annum over this period.

10

Independent Competent Person’s Report Without Valuations December 2010

2.1.5. Ore Processing

Initial processing of chromite ores is generally by hand sorting of lumpy ores followed by heavy media or gravity separation of finer ores, to remove gangue or waste materials and produce upgraded ores or concentrates. Magnetic separation and flotation techniques may also be applied. Over 94% of the world's production of chromite is converted into various ferrochromium alloys for use in the stainless steel and other alloy industries. Chromite is generally smelted in submerged arc furnaces, together with carbonaceous reductants and fluxes, although other technologies such as DC arc furnace smelting are also in use. Importantly, agglomeration of ore fines, especially those produced from South Africa's friable chromites, is an important aspect of processing prior to smelting. Pelletising of the fines is currently the preferred route. A wide range of possible technologies for smelting chromite to ferrochromium has been investigated. Stainless steel is produced from the ferrochromium alloys by melting the alloys in electric arc furnaces together with varying amounts of carbon steel and stainless steel scrap, and then adding nickel and other minor elements for the grade of stainless steel required. In the early days of high-carbon ferrochromium production, the furnaces were supplied with high-grade, lumpy chromite from countries such as Zimbabwe, but with the increasing demand from the 1970s, most countries, and in particular South Africa, began production from lower-grade ores. The alloy produced from these ores became known as charge chrome because the chromium content was lower and the carbon content, and, in particular, the ratio of C:Cr, was very much greater than in high-carbon ferrochromium. This did not suit the stainless steelmakers who required as little carbon as possible entering their melts for each chromium unit and they had compensated for this by using larger quantities of the more costly low-carbon ferrochromium. However, the situation changed significantly with the introduction of the argon-oxygen decarburising (AOD) and vacuum-oxygen decarburising (VOD) processes. These processes enabled the steelmakers to remove carbon from the stainless melts without excessive oxidation and losses of chromium. A more advanced attempt to overcome the problem of ore fines was the introduction of DC arc, or plasma, furnace technology. Some of the advantages of DC arc furnace operation are as follows:-

application use of fine ores without agglomeration;

application of lower-cost reductants and greater choice of reductants;

better chromium recoveries;

specific changes in the charge composition as reflected in slag or metal; and

the introduction of the closed furnace enabling off-gas energy to be used for power co-generation.

Pelletising technology was introduced for friable chromite ores by binding, adding a reductant and fluxes and then passage through a rotary kiln for hardening by sintering. This also enables a degree of pre-heating and pre-reduction of the chromite feed before charging to a submerged arc furnace to produce ferrochrome. A more recent approach, and one which is being incorporated by more plants, is pelletising. Pellets are produced with coke and these are sintered and partly pre-reduced on a steel belt sintering system. From there, the pellets are delivered to pre-heating shaft kilns that are located above submerged arc furnaces and which operate as direct feed bins, making use of the off-gas heat from the furnaces. Lump ore, coke and fluxes are also directed to the feed bins. Chromite in various sizes is typically charged into a submerged AC electric arc furnace with the addition of reductants (coke, coal and quartzite). The smelting process is energy intensive, requiring up to 4MWh/t of material. Slag is separated from the liquid ferrochrome and tapped into ladles for further processing. Liquid ferrochrome is then poured into moulds and after cooling crushed into sizes as required by the customers. Crushed ferrochrome is railed to final customers or harbours for shipment.

11

Independent Competent Person’s Report Without Valuations December 2010

2.1.6. Uses and Applications

Chromium is an extremely versatile element and finds a wide variety of uses in applications in the steel and alloy, chemical and refractory industries. Approximately 91% of global chromite production is smelted into ferrochromium alloys. These are used in the stainless steel, steel and other alloy industries. Chromium metal, composed of nearly 100% chromium, is produced by the aluminothermic or electrolytic process. It is mainly used for specialty alloys. Only 2% of the world's production of chromite was used in 2007 for chromium chemicals. The primary product from the chromite is sodium chromate. From this, a variety of other chemical products are made and used, for example, for tanning leather, as coloured pigments in paints, plastics and ceramics, and metal finishing such as chromium plating. Production of chromite for refractory use and foundry sands is about 4% of global chromite production. Refractory chromite is used in sectors of ferrous and non-ferrous metallurgy, in cement kilns and in the glass industry.

2.1.7. Ferroalloys

The main alloys that are produced are:-

high-carbon ferrochrome (HCFeCr), produced from ores with Cr:Fe ratios of 2.0-3.6, and with a chromium content of more than 60% and carbon content of 4-6%,

and charge chrome produced from lower grade ores, mainly from South Africa, with Cr:Fe ranging from 1.3-2.0, and containing 50-55% Cr and 6-8% carbon.

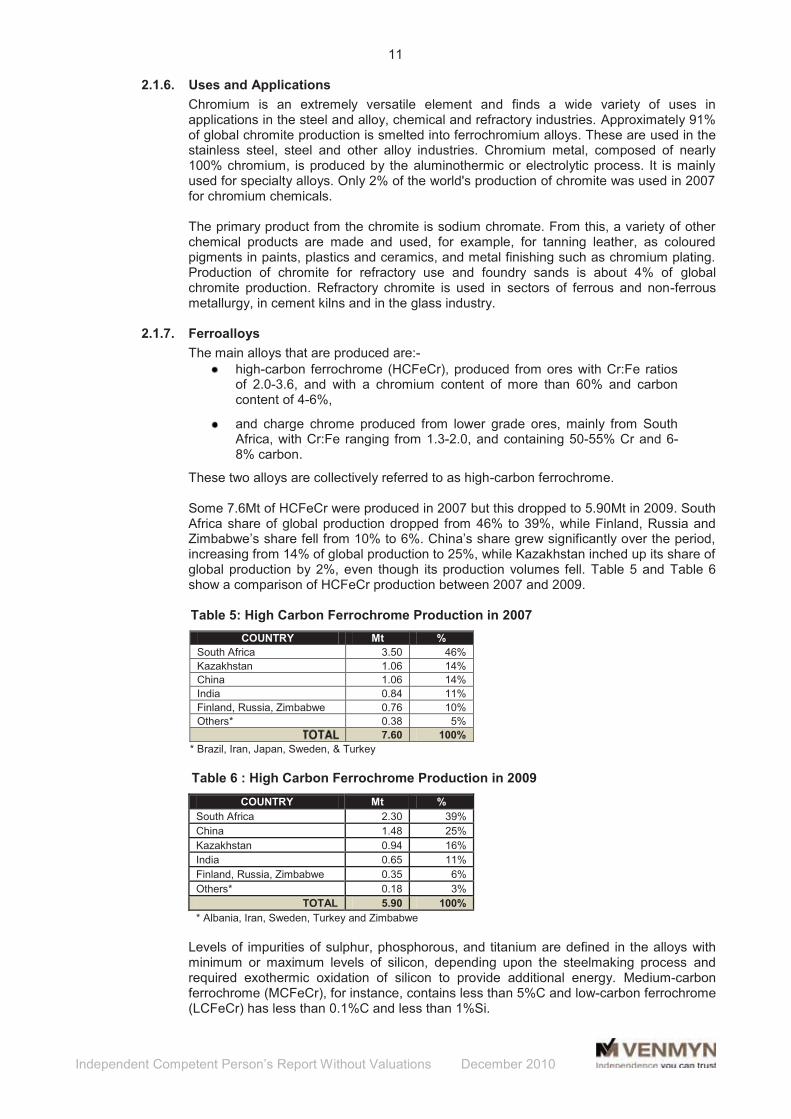

These two alloys are collectively referred to as high-carbon ferrochrome. Some 7.6Mt of HCFeCr were produced in 2007 but this dropped to 5.90Mt in 2009. South Africa share of global production dropped from 46% to 39%, while Finland, Russia and Zimbabwe’s share fell from 10% to 6%. China’s share grew significantly over the period, increasing from 14% of global production to 25%, while Kazakhstan inched up its share of global production by 2%, even though its production volumes fell. Table 5 and Table 6 show a comparison of HCFeCr production between 2007 and 2009. Table 5: High Carbon Ferrochrome Production in 2007

COUNTRY Mt %

South Africa 3.50 46%

Kazakhstan 1.06 14%

China 1.06 14%

India 0.84 11%

Finland, Russia, Zimbabwe 0.76 10%

Others* 0.38 5%

7.60 100%

* Brazil, Iran, Japan, Sweden, & Turkey

Table 6 : High Carbon Ferrochrome Production in 2009

COUNTRY Mt %

South Africa 2.30 39%

China 1.48 25%

Kazakhstan 0.94 16%

India 0.65 11%

Finland, Russia, Zimbabwe 0.35 6%

Others* 0.18 3%

TOTAL 5.90 100%

* Albania, Iran, Sweden, Turkey and Zimbabwe

Levels of impurities of sulphur, phosphorous, and titanium are defined in the alloys with minimum or maximum levels of silicon, depending upon the steelmaking process and required exothermic oxidation of silicon to provide additional energy. Medium-carbon ferrochrome (MCFeCr), for instance, contains less than 5%C and low-carbon ferrochrome (LCFeCr) has less than 0.1%C and less than 1%Si.

12

Independent Competent Person’s Report Without Valuations December 2010

MCFeCr and LCFeCr, like HCFeCr, were produced in lower volumes in 2009 as compared with 2007, with 500kt being produced as compared with 681kt in 2007. China, Russia, South Africa, and Kazakhstan remained the main producers in 2009, but China’s share of world production has grown significantly. This is shown in Table 7 and Table 8:-

Table 7: Low and Medium Carbon Ferrochrome Production 2007

COUNTRY kt %

China 245 36%

Russia 218 32%

South Africa 89 13%

Kazakhstan 75 11%

Others 54 8%

681 100%

Table 8 : Low and Medium Carbon Ferrochrome Production 2009

COUNTRY kt %

China 300 60%

Russia 100 20%

Kazakhstan 40 8%

South Africa 25 5%

Others 35 7%

TOTAL 500 100%

Chromium provides stainless steel with its corrosion resistant properties. Nickel and, in the top grades of stainless steel, titanium and molybdenum can also be added to improve technical performance in specific environments. For the purpose of this transaction, further details concerning chrome metal, chemicals and refractories are not relevant. However, Table 9 is a summary of the typical compositions of the chromite required for various types of end-uses: - Table 9: Typical Compositions of Various Grades of Chromite

USE %Cr2O3 %C Cr:Fe %SiO2

HCFeCr >60 4 - 6 2.0 - 3.6 2 - 4

Charge Chrome 50 - 55 6 - 8 1.3 - 2.0

MCFeCr <5

LCFeCr <0.1 <1.0

Chemical 40 - 46 <2.1

Refractory >60 (plus Al2O3) 0.7

2.1.8. Future Trends

Specifications of chromite for metallurgical uses are becoming less rigid. For the manufacture of ferrochrome, the Cr2O3 has decreased from 48% to 46% (minimum) and the Cr:Fe ratio from 2.8:1 to 2:1. This has resulted in the broadening of the base of metallurgical-grade chromite. However, the specification of the ores for charge chrome is far more rigid. A similar trend is also noted in the grade of the refractory grade ore. Also, the use of technologies such as pelletisation, agglomeration, plasma arc technology and direct reduction have meant the ores that were previously considered uneconomic can be used to economically produce ferrochrome. Cutting edge technology, such as Outokumpu Technology, has greatly changed the landscape of the chromite mining industry by making the process more efficient. The advantages of the new technology are:-

lower total production cost;

high chrome recovery;

environmentally friendly process;

clean and safe plant to operate; and

higher production unit capacity available.

13

Independent Competent Person’s Report Without Valuations December 2010

Importantly, the retreatment of tailings dams and future risings at existing operations has been a development that has spawned businesses like Sylvania, although Sylvania has been the leader in this regard. Part of the reason for this trend was the recognition that many of the chrome seams, traditionally mined for chromite, contain low grade PGEs which, at high metal prices, could be economically liberated. This was however, really developed from the PGE industry’s Aquarius Platinum Limited (AQP).starting to mine UG2 ore at Kroondal mine in the late 1990s.

2.1.9. The Asian Influence

As the world is experiencing a dramatic economic downturn, with many major economies in a recession, China has continued to post positive growth rate figures. However, the growth of the Chinese economy has slowed from the rate of the past decade. It remains an important driver of many commodity markets, fuelled by strong materials-intensive growth over the last 20 years. Citigroup notes that the Chinese contributions to global economic growth and commodities consumption have been dramatic and, currently, China accounts for:-

5% of global GDP on an exchange rate basis;

11% of world GDP on a purchasing power parity basis, up from 9% in 1995; and

8% of world industrial production, up from 6% in 1995.

The intensity of use of metals and minerals in China lags behind those of the developed economies of the world and especially those of the newly-industralised economies of South Korea and Taiwan. It is, therefore, possible that strong growth in the commodity consumption could be sustained, albeit at rates lower than experienced during the last few years. South Africa has sufficient chromite Mineral Resources (5.5bn tonnes) to sustain an estimated 200 years of mining at current production rates.

2.1.10. Supply/Demand Dynamics for Chromite

The world market for chromite is driven primarily by the world’s demand for ferrochrome used in stainless steels. The largest growth market for chromites has been in ferrochrome production for stainless steels. The secondary markets are all either stable or declining slightly. Especially in the secondary markets, there are environmental concerns related to hexavalent chromium (Cr

6+). In the refractory market, several large international

producers have dropped chromite-bearing refractory from their product range, and in the wood preservatives market, chromated copper arsenate (CCA). It was almost banned in the United States but was allowed to be used provided mitigation measures were submitted. However, it is likely that other chemicals will not be so fortunate. The mining of chromite has shifted from the one based on high-grade ores to one based on lower-grade deposits that are extensive in size. Because of the economies-of-scale, this makes the mining operations competitive in terms of costs to the smaller high-grade ones. Traditionally, mined deposits were sourced from thick chromite seams (preferably 2m) to reduce the unit mining costs. In addition, a high Cr:Fe ratio in the basic chromitite mineral (three at the highest) was sought in order to reduce the unit cost of producing chrome metal as ferrochrome. South Africa’s BIC chromite seams are relatively low grade with Cr:Fe ratios of typically 1.7 or less. Early producers exploited reserves with Cr:Fe ratios of greater than three, but following the advent of the AOD process that permitted charge chrome alloy grades (typically 50 to 52% Cr) to be converted to stainless steel, by the 1980s reserves of Cr:Fe ratios of less than two became the norm. Currently, the typical smelter feeds have a Cr:Fe ratio of approximately 1.5 but ratio requirements are dropping as alloy grades of less than 50%Cr (with concomitantly increased Fe credits) have started to become accepted by some customers.

14

Independent Competent Person’s Report Without Valuations December 2010

During the past two decades this has led to the increasing dominance of South Africa as the geographical source of chromites and ferrochrome, so much so that South Africa is the world’s leading supplier of ferrochrome. The factors affecting the global supply of chromite are:-

growth in supply of raw ore for export will be limited by South Africa’s power and water issues;

ore export tariffs were introduced in India (USD40/t), and the Kazakhstan government may follow with similar tariffs;

ferrochrome production costs are rising due to increasing power costs, under utilization of capacity and aggressive inflation in baseline costs;

infrastructure solutions, including rail and port facilities, are likely to be long-term;

deferral of capacity expansion in South Africa limits response to rising demand, creating expected supply shortages for an extended period;

global contract for ferrochrome price at USD1.30/lb which probably is marginally above production costs; and

volatile 2010 contract prices as a result of current global economic issues.

The following factors influence global demand of ferrochrome:-

world consumption of ferrochrome increased from 6.1Mt in 2006 to 7.3Mt in 2007 (19%);

90% of ferrochrome is used in stainless steel and alloy steel production;

there are no substitutes for ferrochrome in the production of stainless steel;

ferrochrome production tracks at 25% of stainless steel volume (28Mt in 2007);

ferrochrome’s growth is expected to be greater than 7% per annum due to shift from austenitic to ferritic stainless steel production (BRIC countries);

China stainless steel production growth was 500% from 1996 to 2006;

Asia now accounts for 60% of global stainless steel production; and

North America imports 400 to 500kt of ferrochrome annually.

2.2. PGE Sector

A short review of the global PGE production, supply and demand, and pricing has been prepared to set the context for the South African industry. 2.2.1. Introduction

PGEs include six closely related elements: platinum (Pt), palladium (Pd), rhodium (Rh), iridium (Ir), ruthenium (Ru), and osmium (Os). Gold (Au) is normally quoted as part of the prill split and included as, for example, 3PGEs plus gold. Each metal has slightly different characteristics and uses. Platinum and palladium are by far the most abundant in all deposits, and the other four are always minor byproducts from exploitation of platinum-palladium deposits, except in alluvial occurrences (which are now relatively minor producers), where osmium and iridium may be abundant. All world resource estimates recognise the importance of the BIC in such global figures.

2.2.2. Geology and Mineralogy

The pattern of values in different ore samples can vary widely. The precious metals occur in a variety of forms. One or more of the metals may be present in combination with sulphur, arsenic, selenium, or tellurium metallic particles of PGEs, or PGEs alloyed with base metals are also found. Additional PGEs are found in solid solution in base-metal sulphide particles.

15

Independent Competent Person’s Report Without Valuations December 2010

In the BIC, the PGEs occur in the Merensky Reef, UG2 Reef, and Platreef. Chromite crystals form a large part of the volume of UG2 PGE ore and other chrome ores. Base-metal sulphides are much more prevalent in Merensky and Platreef ores than in the UG2 or chrome ores. The grain size of mineral particles varies widely but is coarsest in Merensky Reef ores. The difficulty in recovering PGEs from any particular ore is determined by the ore's mineralogy. Although Merensky ores are often easier to treat, it is not easy to generalise. Ore from different areas of the same mine can have quite different characteristics.

2.2.3. Occurrence and Mining

The PGE resources of the BIC were discovered by Hans Merensky and Andries Lombaard in 1924. Within the complex, three horizons occur. The Merensky Reef, UG2 Chromitite, and the Platreef are mined for PGEs and make the BIC the largest PGE source in the world. Platinum and palladium production from the BIC represents 72% and 34% of annual global production, respectively. The location of the reefs is shown in Figure 2, Figure 3 and Figure 4. The Merensky Reef is the source of over 80% of the platinum mined in South Africa and this has been successfully exploited since the late 1920s. More PGEs are found in the chromitite reefs of the BIC. The highest PGE values are associated with the UG2 Reef which lies about 200m below the Merensky. Since the mid 1970s increasing tonnages of UG2 ore have been mined and treated by the established producers. Smaller quantities of PGEs are found in the middle and lower group chrome seams which are mined for their chrome content. Recently, some of these PGEs have been recovered by re-treatment of chrome mine tailings in Chrome Washing Plants (CWP). Other similar schemes are planned, though the quantities of precious metals from this source will not be large relative to the mines. In the case of Sylvania, it operates the CWP and PRP plants in tandem.

The PGE-bearing Platreef occurs in the northern portion of the BIC. Mining of this reef was discontinued in the early 1930s owing to treatment difficulties and patchy values. Exploration and test-work have continued and currently, only Anglo Platinum is mining on this reef for PGEs. The global platinum and palladium mineral resources for different countries are shown in Table 10:-

Table 10: Global Platinum and Palladium Mineral Resources as at 2009

PLATINUM PALLADIUM

COUNTRY CONTENT RANK CONTENT RANK

Moz kt % Moz kt %

South Africa 1,142.00 35.53 74.69 1 827.10 25.73 50.06 1

Zimbabwe 143.00 4.45 9.35 2 87.00 2.71 5.27 4

Russia 89.00 2.77 5.82 3 314.00 9.77 19.01 2

United States 45.00 1.40 2.94 4 162.00 5.04 9.81 3

Canada 11.00 0.34 0.72 5 13.00 0.40 0.79 5

Others 99.00 3.08 6.47 249.00 7.75 15.07

TOTAL 1,529.00 47.57 100.00 1,652.10 51.40 100.00 Source: South African Journal of Science

The mining of PGE ores is similar to Witwatersrand gold mining inasmuch as the BIC orebodies are normally thin, tabular reefs covering an extensive area. This enables a progressive method of mining – the reef is drilled and blasted to advance the face, with support being installed for local control of the hanging wall. As in the Witwatersrand gold mines, PGE mining is incorporating the increased use of mechanisation and trackless-mining methods in stopes little more than 1m high. PGE mining, however, differs from gold mining in several ways. Unlike gold reefs, which are sedimentary deposits resulting from the settling of granular particles on the bed of an inland lake and subjected to great pressure, PGE reefs are igneous rocks.

16

Independent Competent Person’s Report Without Valuations December 2010

They were intruded into the BIC as molten volcanic magma rising from below the earth's crust, and later cooling and solidifying. This phenomenon created a strata control environment differing markedly from that of the gold mines. The Merensky and UG2 reefs are narrow (typically less than 1m thick). Traditionally, both reefs were mined using narrow reef methods, and many operations continue to use these methods today. Miners use hand-held pneumatic drills to drill holes that are then filled with explosives. After blasting, the ore is removed from the stope using scrapers attached to winches. It is then transported through a series of ore passes to the bottom of the shaft, and hauled to the surface. Mechanical and hybrid methods are increasingly being adopted by both new and existing mines. Drilling may be carried out either using conventional hand-held pneumatic drills, or via low-profile machines equipped with specialised drilling equipment. Ore is subsequently cleaned from the stopes using low-profile load-haul-dump (LHD) vehicles. The mining width, typically around 1.8m, must allow the use of machinery although some mines are experimenting with ultra-low profile equipment which can operate in stopes little more than a metre high. Open-pit methods are used to mine the Platreef, which is much wider than the other reefs, varying between 5m and 90m in thickness. Open casting is also used on a smaller scale to exploit the UG2 and Merensky Reef where it outcrops. Mill-head grades of the BIC ore (a measure of the ore's PGE content as it enters the first stage of processing) are typically between 3 and 6g/t. Allowing for losses which occur during refining, and the varying platinum contents of the different BIC ores, this means that between 10 and 25t of ore must be processed to obtain a single ounce of platinum.

2.2.4. World Production and Global Development

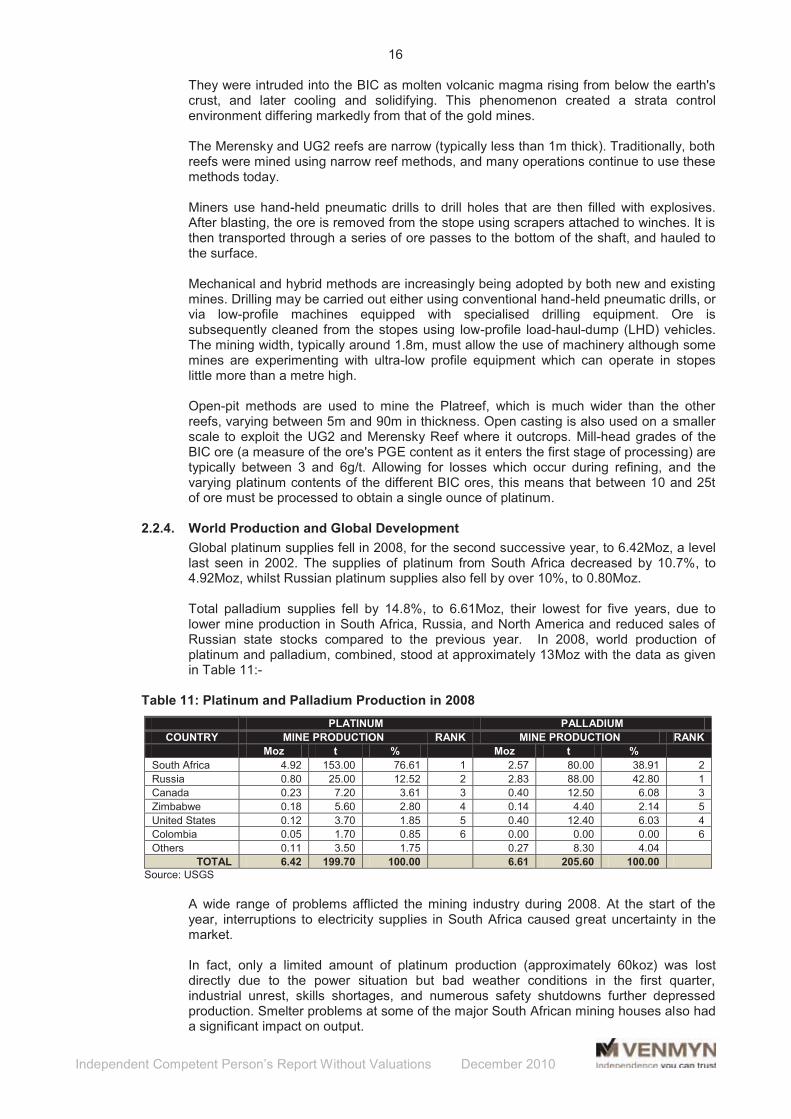

Global platinum supplies fell in 2008, for the second successive year, to 6.42Moz, a level last seen in 2002. The supplies of platinum from South Africa decreased by 10.7%, to 4.92Moz, whilst Russian platinum supplies also fell by over 10%, to 0.80Moz. Total palladium supplies fell by 14.8%, to 6.61Moz, their lowest for five years, due to lower mine production in South Africa, Russia, and North America and reduced sales of Russian state stocks compared to the previous year. In 2008, world production of platinum and palladium, combined, stood at approximately 13Moz with the data as given in Table 11:-

Table 11: Platinum and Palladium Production in 2008

PLATINUM PALLADIUM

COUNTRY MINE PRODUCTION RANK MINE PRODUCTION RANK

Moz t % Moz t %

South Africa 4.92 153.00 76.61 1 2.57 80.00 38.91 2

Russia 0.80 25.00 12.52 2 2.83 88.00 42.80 1

Canada 0.23 7.20 3.61 3 0.40 12.50 6.08 3

Zimbabwe 0.18 5.60 2.80 4 0.14 4.40 2.14 5

United States 0.12 3.70 1.85 5 0.40 12.40 6.03 4

Colombia 0.05 1.70 0.85 6 0.00 0.00 0.00 6

Others 0.11 3.50 1.75 0.27 8.30 4.04

TOTAL 6.42 199.70 100.00 6.61 205.60 100.00 Source: USGS

A wide range of problems afflicted the mining industry during 2008. At the start of the year, interruptions to electricity supplies in South Africa caused great uncertainty in the market. In fact, only a limited amount of platinum production (approximately 60koz) was lost directly due to the power situation but bad weather conditions in the first quarter, industrial unrest, skills shortages, and numerous safety shutdowns further depressed production. Smelter problems at some of the major South African mining houses also had a significant impact on output.

17

Independent Competent Person’s Report Without Valuations December 2010

Later in the year, the mining industry was forced to react to sharp falls in metal prices. In North America, some PGE and nickel mines were placed under care and maintenance and other operations have been reorganised with the aim of ensuring their economic sustainability, with an associated cut in production capacity. In South Africa, planned capital expenditure had been cut heavily at most mines. In contrast to North America, however, relatively little current production capacity had been closed with only a limited number of shafts, pits or smaller operations affected. Difficult economic conditions negatively affected demand for platinum in many sectors during 2009, driving gross demand 11.9% lower to 7.04Moz. Supplies fell by only 20,000oz to 5.92Moz despite the closure of some uneconomic mine production in South Africa. Although the weight of platinum recovered from open loop recycling also fell, to 1.41Moz, the platinum market was in oversupply by 285,000oz during 2009. The short term outlook for platinum production in South Africa is quietly positive. The three newest mines, Blue Ridge, Pilanesberg and Smokey Hills, should continue to ramp up to full production. Other mines, such as Two Rivers, should produce more platinum in the near term. Continuing progress in developing new shafts at Lonmin should boost underlying production marginally, although refined sales will be dependent on smelter availability. Production at Impala is set to remain relatively flat but there is some scope for additional sales of refined metal. At Anglo Platinum, the company has acknowledged that it may elect to increase production by up to 200,000oz of platinum above its planned guidance for 2010, if the market demands it, suggesting that underlying production should rise above 2009 levels. Palladium demand also suffered due to the weak state of the world’s economy. Gross automotive demand fell by 9.3% and gross electrical sector demand decreased by 7.3% as companies and individuals restrained their spending in the first half of 2009, in particular. Although the economic picture started to improve later in 2009, total gross demand fell to 7.77Moz. Supplies of palladium fell to 7.10Moz, including the sale of 960,000oz from Russian state stocks, with mine output decreasing in North America, Russia and South Africa, but rising in Zimbabwe. The weight of metal recovered from scrapped autocatalysts, electronics and jewellery declined to 1.43Moz. The palladium market was therefore in oversupply during 2009 by 760,000oz, a slightly larger surplus than in the previous year. Supplies of palladium from current Russian mining are expected to increase marginally, in line with higher nickel output from Norilsk Nickel’s Polar and Kola operations. Sales are also expected of the remainder of the palladium originally shipped from Russian state stocks in 2007 and 2008, equating to roughly 1Moz. Little if any clarity exists in the longer term about the size and likely fate of remaining palladium stocks. However, over ten tonnes of palladium were shipped into Switzerland in early 2010, apparently also from Russian State stocks, which are not expected to be sold during 2010, although such sales remain possible and, if they were to occur, would boost supplies further. A summary of the world’s platinum market during 2010 as presented by the Johnson Matthey report is as follows:-

the platinum market was in surplus by 290,000oz. Gross demand is set to rise by 11% to 7.56 Moz

supplies are expected to remain flat at 6.01 Moz, while recovery from recycling is forecast to increase to 1.84Moz.

18

Independent Competent Person’s Report Without Valuations December 2010

gross autotmotive demand for platinum is forecast to increase by 800,000 oz to 2.99 Moz.

gross demand from the jewellery sector is set to decline by 14% in 2010 to 2.42 Moz as consumers feel the effect of higher prices;

industrial demand is expected to rise by 51% to 1.72 Moz, back to the 2008 level; and

identifiable physical investment demand is forecast to decrease by 34% to 435,000 oz.

A summary of the world’s palladium market during 2010 as presented by the Johnson Matthey report is as follows:-

palladium was in surplus by 45,000oz in 2010. Gross demand is expected to rise by 15% to 8.94 Moz. Supplies of palladium are flat at 7.14 Moz.. Palladium recovery from recycling is set to increase by 29% to 1.85 Moz;gross automotive demand for palladium is set to rise by 27% to 5.15 Moz with purchases of palladium higher in all regions;

gross palladium jewellery is expected to fall by 8% to 630,000oz due to weaker Chinese demand;

gross industrial demand for palladium (is expected to increase by 8% to 2.49 Moz; net annual identifiable physical investment demand for palladium is anticipated to rise to 670,000 oz, an increase of 7%.

PGEs: Looking Back and Forward

A power crisis in January 2008 in South Africa, the world’s largest producer of PGEs, resulted in the closure of all PGE mines for five days. This had the effect of causing production losses leading to supply fears and record-high prices in the first half of 2008. As such, prices of platinum reached an all-time high of USD2,275/oz and that of rhodium also reaching an all-time high of USD10,100/oz. Palladium reached a 7-year high of USD585/oz in 2008, although this price level has since been exceeded, with palladium reaching USD720/oz in November 2010. The global economic downturn has resulted in lower automobile demand, which in turn resulted in the decline of consumption, and therefore, prices of PGEs in the second half of 2008. The desire for an alternative fuel, both for automobiles and homes, has led to a large global public and private effort to develop fuel cell technology. Platinum is the catalyst used in these cells. A decrease in car sales in Europe and North America caused a decrease in the consumption of platinum and palladium in 2009. 2010 however saw a recovery in the automotive sector which caused an increase in demand for PGE’s. The tightening of emissions standards in China, Europe, Japan, and other parts of the world is expected to lead to higher average platinum loadings on catalysts, particularly in light-duty diesel vehicles, as particulate matter emissions become more tightly controlled. Thrifting is continuing at most manufacturers and is likely to lead to the reduction of use of platinum and palladium in auto-catalysts. The large price difference between platinum and palladium has led to the assumption that car manufacturers will continue to change PGEs ratio in petrol-engine vehicles in favour of palladium, as well as continue efforts to increase the proportion of palladium used in diesel vehicles. The sale of platinum jewellery is expected to drop globally as the price continues to be high and white gold and palladium are substituted for platinum. In May 2008, new investment vehicles for PGEs, ETNs (Exchange Traded Notes), were launched for platinum and palladium and are the first such PGE-trading product available to US investors. Unlike exchange-traded funds (ETFs), ETNs are based on futures contracts, and the physical metal is not held. For most other end-uses, certain PGEs can be substituted for other PGEs, with some losses in efficiency. In addition, electronic parts manufacturers are reducing the average palladium content of the conductive pastes used to form the electrodes of multi-layer ceramic capacitors by substituting base-metals or silver-palladium pastes that contain significantly less palladium.

19

Independent Competent Person’s Report Without Valuations December 2010

The outlook for rhodium demand in 2009/2010 is poor. Demand for this metal is highly dependent on vehicle output which is currently very weak. Also, car makers are reducing average rhodium loadings in catalysts (the result of thrift programmes carried out at higher metal prices). Although vehicle production is expected to rise from the very low levels of early 2009, gross rhodium auto-catalyst demand is expected to fall sharply this year. The effects of the high rhodium price were also seen in the glass sector last year. Rhodium/platinum alloys are used to prolong the working life of components which are in contact with molten glass. At the highest rhodium prices, the cost savings made by de-alloying drove the greater use of lower-rhodium alloys and demand for rhodium fell substantially. However, the glass industry is able to vary its use of PGEs quite rapidly. The rhodium market moved from a surplus of 25,000oz in 2008 into a much larger surplus of 241,000oz in 2009. Supplies rose from 695,000oz to 770,000oz. Demand was hit by a poor performance by its largest sector, the automotive market, where gross demand fell 19.4% lower to 619,000oz, the lowest figure since 2004. Demand fell in most other applications too, although some of this weakness was offset by lower rhodium recovery from scrapped autocatalysts. It is expected that rhodium will be in another large fundamental surplus in 2010. Supplies of rhodium are unlikely to change significantly from 2009. Production of refined rhodium was hit by a build-up in pipeline stocks in 2008 and some of this metal was refined and sold in 2009, boosting supplies strongly. With the pipeline now less full, sales of rhodium should revert to closer to the level of mine output. So, although increasing production from rhodium-rich UG2 ore on the BC should boost underlying output, supplies will rise by less this year. Rhodium supplies from other producing nations should remain flat. The fate of the ruthenium market is closely tied to that of the electronics sector. With consumer and business purchasing of electronic goods currently weak, gross ruthenium demand is expected to soften. Additionally, the sector is likely to be able to meet most of its ruthenium requirements for the production of hard disks by using metal recycled from its own manufacturing processes. At current price levels, it remains attractive to recycle much of the scrap produced in the manufacture of hard disks. However, at prices significantly below this, recycling becomes less attractive than purchasing new metal. If the price falls further, therefore, net demand could rise strongly, providing some support for the metal price. Ruthenium demand decreased from 699,000oz to 574,000oz in 2009, continuing its slide from the elevated levels of 2006. Demand in the electrical sector fell once again, to 336,000oz, and chemical industry demand softened too. Ruthenium use in the electrochemical sector and in a number of other small applications was steady compared to previous year levels. Supplies were adequate to meet demand. Demand for Ruthenium grew in 2010, largely due to increased demand from the hard disk industry. Perpendicular magnetic recording (PMR) is now the dominant hard disk technology and this market should start to grow rapidly once more as computer sales recover, driving ruthenium usage higher. As importantly, the hard disk makers have reduced their working stocks of ruthenium and are no longer able to source the majority of their requirements from material they had previously bought. Purchases of ruthenium by the industry, equivalent to demand, are therefore rising strongly. The outlook for iridium demand in 2009/2010 was weak. Demand for iridium crucibles for the growth of high quality crystals started to decrease in 2008 and declined further in 2009. Use of this metal in spark plugs and aero-engine igniters is also likely to soften. However, newer technology used in the chlor-alkali process will continue to replace older mercury-based cells, leading to steady iridium demand from the electrochemical industry. Iridium demand dropped in 2009, slipping from 102,000oz to 91,000oz. In the electrochemical sector, demand rose from 25,000oz to 33,000oz, reflecting the move to upgrade the Chinese chlor-alkali industry to membrane technology.

20

Independent Competent Person’s Report Without Valuations December 2010

Chemical demand remained flat at 21,000oz. Temporary falls in demand for iridium crucibles and for new vehicles drove demand in the electrical sector and other applications, principally spark plugs, lower to 7,000oz and 30,000oz, respectively. Supplies of iridium, mainly from South Africa, remained sufficient to meet demand and the price moved little throughout the year, remaining at USD425 for most of 2009. Iridium demand is also forecast to perform well this year. Increasing car production will boost iridium demand for use in high-specification spark plugs. Demand for iridium crucibles for growing high-quality metal oxide single crystals is also set to rebound. Electrochemical demand should strengthen again, reflecting the continuing conversion of mercury cell chlor-alkali technology to more environmentally-friendly membrane cells in Asia and in other regions.

2.2.5. Ore Processing

The processing of BIC PGE ores poses a number of challenges due to the nature of the mineralogy and the subsequent smelting requirements. Merensky Reef ores are the easiest to treat, followed by Platreef ores, and then the UG2 Reef ores. The characteristics of the PGE ores from the Western Limb are well known, as compared to those from the other regions. The PGE mineralogy changes significantly on the Eastern Limb, where the PGE minerals are not only finer, but have a greater association with bismuth and antimony, resulting in more difficult flotation metallurgy. Similarly, on the Northern Limb, although superficially similar to Merensky Reef ores, Platreef ores have a different PGE mineralogy which results in a poorer process response. The Merensky Reef is characterised by high PGE grades and a high ratio of platinum to the other PGEs. Although the grade and the PGE proportions are relatively constant, the PGE mineralogy varies considerably. In general, the Pt-Pd sulphides are dominant (60%), followed by the PGE tellurides (11%) and arsenides (6%), with the balance of mostly PGE alloys and Ag/Au phases. There are three PGE associations which are:-

enclosed in or attached to base-metal sulphides (BMS);

enclosed in silicates; and

enclosed in or attached to chromite.

The first association is the most dominant in Merensky Reef ores. The BMS content is around 1% by weight, and consists of mainly pyrrhotite, pentlandite, and chalcopyrite. The PGEs are coarse (20 to 150microns) and are well liberated after comminution. They generally float quickly, reporting with the chalcopyrite to the first rougher cell concentrates. Most composites are with the BMS and also float well. The remainder of the ore consists of mostly silicate minerals such as pyroxene and plagioclase, with some talc and chromite. Although neither pyroxene nor feldspar show any natural flotation tendencies, they can become activated by base-metal ions and subsequently float after interaction with collectors. Talc, a naturally floating mineral, can also rim the pyroxene particles, resulting in flotation.

2.2.6. Concentration

During the processing of Merensky Reef ores, the BMSs and PGEs are recovered using conventional sulphide ore flotation practice to produce a bulk concentrate. A standard rougher-scavenging operation is followed by several cleaning stages. The treatment strategy employs the Mill-Float-Mill-Float or MF2 approach, where the ore is coarsely milled and floated and the flotation tailings further milled to a finer size and re-floated. Comminution is undertaken in low aspect ratio semi-autogenous (SAG) mills using high-chrome grinding media with typical sequential grind sizes of 60% and 75% passing 74microns.

21

Independent Competent Person’s Report Without Valuations December 2010