INDEPENDENT PROFESSIONAL VALUATION BY KHONG & …

36

__________________________________________________________________________________ INDEPENDENT PROFESSIONAL VALUATION BY KHONG & JAAFAR SDN BHD OF M.P. EVANS GROUP PLC’S PROPERTIES

Transcript of INDEPENDENT PROFESSIONAL VALUATION BY KHONG & …

__________________________________________________________________________________

INDEPENDENT

PROFESSIONAL

VALUATION BY KHONG &

JAAFAR SDN BHD OF M.P.

EVANS GROUP PLC’S

PROPERTIES

__________________________________________________________________________________

Khong & Jaafar Sdn Bhd 57-1 Jalan Telawi Tiga

Bangsar Baru 59100 Kuala Lumpur

Malaysia

21 November 2016

The Directors M.P.Evans Group PLC 3 Clanricarde Gardens, Tunbridge Wells Kent TN1 1HQ United Kingdom Dear Sirs, The M.P.Evans Group PLC (“MPE”) appointed Khong & Jaafar Sdn Bhd (Khong & Jaafar) to act as an Independent Professional Valuer to value all the MPE Indonesian Plantations, including the Group’s 36.84% owned PT Agro Muko and its 38% owned PT Kerasaan and the 68.3-hectare Bertam Estate (100% owned) and the Group’s 40% owned share of Bertam Properties Sdn Bhd comprising three development lands and a golf resort in Malaysia. They are hereafter referred to as the “Properties” which in turn refer to the interests in the Properties. In response to this appointment, Khong & Jaafar has prepared the attached Report and Valuation dated 21 November 2016. 1. Professional Qualifications

Khong & Jaafar which was incorporated in Malaysia in 1965 has been involved in the valuation of real estate interests, including oil palm plantations for the past 51 years. Khong & Jaafar is a registered valuation firm under the Valuers, Appraisers and Estate Agents Act 1981, Malaysia. Khong and Jaafar is eminently qualified to undertake the valuation, including the oil palm plantations and has the necessary expertise. The current major shareholder of the company and Managing Director, Elvin Fernandez, is a Fellow of the Royal Institution of Chartered Surveyors, United Kingdom, a Past Chairman of the International Valuation Standards Council, a Past President of the Royal Institution of Surveyors Malaysia and the current Secretary General of the ASEAN Valuers Association among many other professionally related qualifications and affiliations. Elvin Fernandez, who is in fact the signing valuer for this valuation entered the valuation profession in 1979 by passing the Final Examinations set by the Royal Institution of Surveyors Malaysia. Khong & Jaafar has no pecuniary interest, other than to the extent of the professional fees receivable for the preparation of this report, or other interest in the real estate interests valued, that could reasonably be regarded as affecting our ability to give an unbiased view of these real estate assets. Our review was carried out only for the purpose referred to below and may not have relevance in other contexts.

2. Valuation Approach

The Report and Valuation that is prepared by Khong & Jaafar is based on legal, economic and physical facts obtained from our full due diligence and the estimate of market values are derived from suitable approaches to valuation and founded on the said facts. The report is in compliance with the dictates of the RICS Red Book. The Report and Valuation contains all the important aspects of a valuation and we consent to the publication of this report in an initial response document pertaining to the offer for MPE by Kuala Lumpur Kepong Berhad and in any subsequent circular or public document as required including by the London Code on Takeovers and Mergers under, for example, Rule 26 or Rule 29 of the Code.

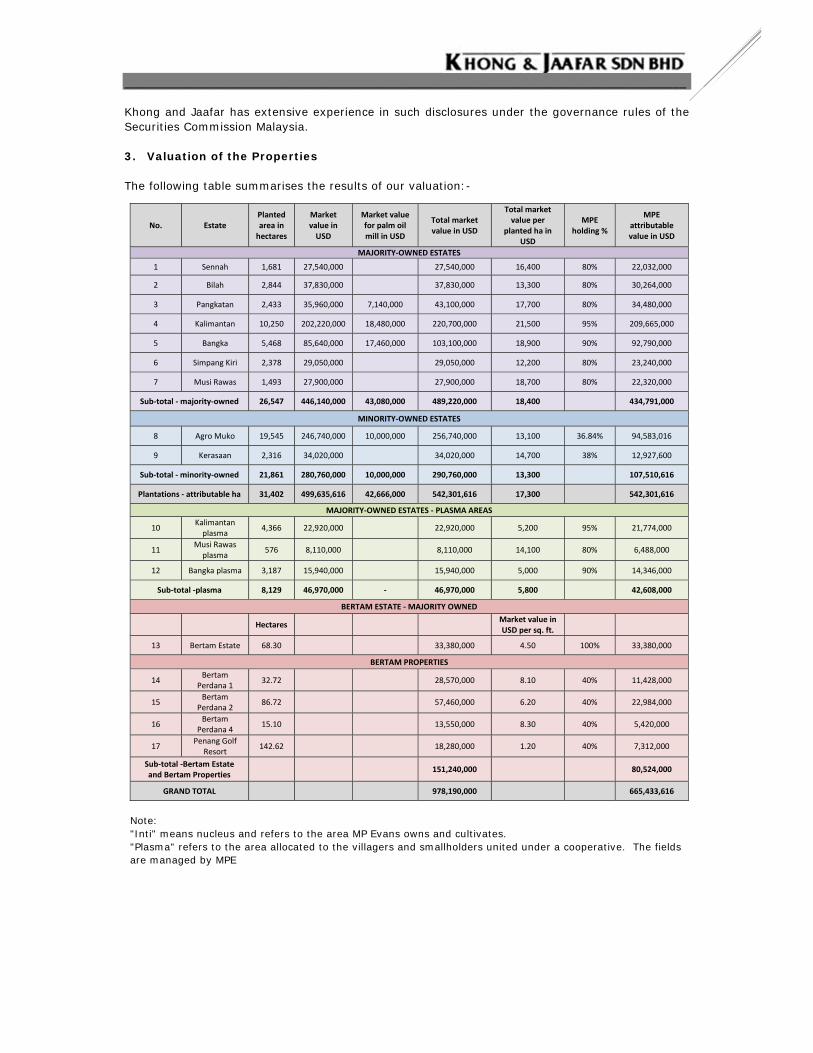

__________________________________________________________________________________ Khong and Jaafar has extensive experience in such disclosures under the governance rules of the Securities Commission Malaysia.

3. Valuation of the Properties

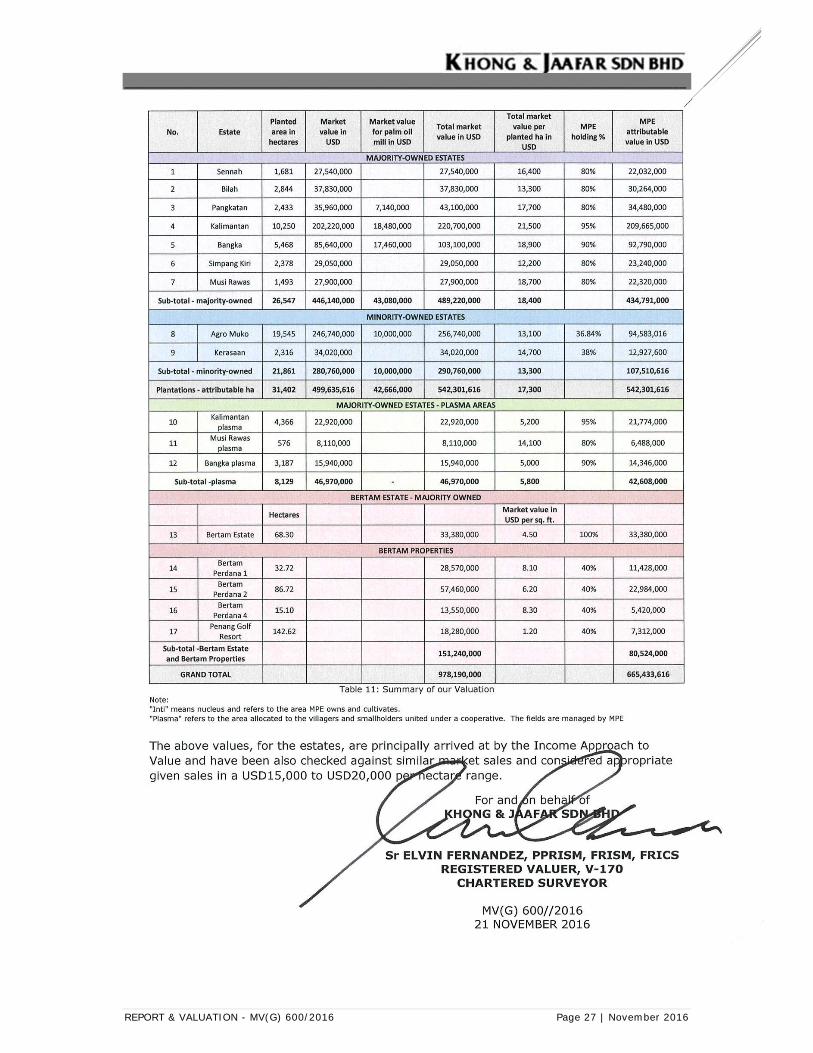

The following table summarises the results of our valuation:-

No. Estate Planted area in hectares

Market value in USD

Market value for palm oil mill in USD

Total market value in USD

Total market value per

planted ha in USD

MPE holding %

MPE attributable value in USD

MAJORITY‐OWNED ESTATES

1 Sennah 1,681 27,540,000 27,540,000 16,400 80% 22,032,000

2 Bilah 2,844 37,830,000 37,830,000 13,300 80% 30,264,000

3 Pangkatan 2,433 35,960,000 7,140,000 43,100,000 17,700 80% 34,480,000

4 Kalimantan 10,250 202,220,000 18,480,000 220,700,000 21,500 95% 209,665,000

5 Bangka 5,468 85,640,000 17,460,000 103,100,000 18,900 90% 92,790,000

6 Simpang Kiri 2,378 29,050,000 29,050,000 12,200 80% 23,240,000

7 Musi Rawas 1,493 27,900,000 27,900,000 18,700 80% 22,320,000

Sub‐total ‐ majority‐owned 26,547 446,140,000 43,080,000 489,220,000 18,400 434,791,000

MINORITY‐OWNED ESTATES

8 Agro Muko 19,545 246,740,000 10,000,000 256,740,000 13,100 36.84% 94,583,016

9 Kerasaan 2,316 34,020,000 34,020,000 14,700 38% 12,927,600

Sub‐total ‐ minority‐owned 21,861 280,760,000 10,000,000 290,760,000 13,300 107,510,616

Plantations ‐ attributable ha 31,402 499,635,616 42,666,000 542,301,616 17,300 542,301,616

MAJORITY‐OWNED ESTATES ‐ PLASMA AREAS

10 Kalimantan plasma

4,366 22,920,000 22,920,000 5,200 95% 21,774,000

11 Musi Rawas plasma

576 8,110,000 8,110,000 14,100 80% 6,488,000

12 Bangka plasma 3,187 15,940,000 15,940,000 5,000 90% 14,346,000

Sub‐total ‐plasma 8,129 46,970,000 ‐ 46,970,000 5,800 42,608,000

BERTAM ESTATE ‐ MAJORITY OWNED

Hectares Market value in USD per sq. ft.

13 Bertam Estate 68.30 33,380,000 4.50 100% 33,380,000

BERTAM PROPERTIES

14 Bertam

Perdana 1 32.72 28,570,000 8.10 40% 11,428,000

15 Bertam

Perdana 2 86.72 57,460,000 6.20 40% 22,984,000

16 Bertam

Perdana 4 15.10 13,550,000 8.30 40% 5,420,000

17 Penang Golf

Resort 142.62 18,280,000 1.20 40% 7,312,000

Sub‐total ‐Bertam Estate and Bertam Properties

151,240,000 80,524,000

GRAND TOTAL 978,190,000 665,433,616

Note: "Inti" means nucleus and refers to the area MP Evans owns and cultivates. "Plasma" refers to the area allocated to the villagers and smallholders united under a cooperative. The fields are managed by MPE

__________________________________________________________________________________

__________________________________________________________________________________

INDEPENDENT PROFESSIONAL VALUATION BY

KHONG & JAAFAR SDN BHD OF ALL THE

M.P. EVANS GROUP INDONESIAN PLANTATIONS,

INCLUDING THE GROUP’S 36.84% OWNED PT AGRO

MUKO AND ITS 38% OWNED PT KERASAAN AND

THE 68.3-HECTARE BERTAM ESTATE (100% OWNED)

AND THE GROUP’S 40% OWNED BERTAM PROPERTIES

SDN BHD COMPRISING THREE DEVELOPMENT LANDS

AND A GOLF RESORT IN MALAYSIA

MV(G) 600/2016

NOVEMBER 2016

__________________________________________________________________________________

(i)

TABLE OF CONTENTS

1. INTRODUCTION ……………………………………………………….……………………………………....………… 1

2.0 REAL ESTATE INTERESTS/PLANTATION INTERESTS OVERVIEW ………………………………. 1

2.1 INDONESIAN PLANTATIONS OVERVIEW .……………………………………………………… 1

2.1 MALAYSIAN PROPERTIES OVERVIEW ….. .…………………………………………………… 2

3.0 QUALIFICATIONS ……………………………………………………………………………………………………… 3 - 5

4.0 BASIS OF OPINION .…………………………………………………………………..……………………………… 5

5.0 INDEPENDENCE …...…………………………………………………………………………………………………… 5

6.0 DATE OF VALUATION ………………………………………………………………..…………………………….… 6

7.0 EXCHANGE RATE …..………………………………………………………………..…………………………….… 6

8.0 INDONESIA IN GENERAL…………………………………………………………..…………………………….… 6

9.0 INDONESIAN LAND LAW …..………………………………………………………..…………………………… 6 & 7

10.0 MALAYSIA IN GENERAL…………………………………………………………..……..………………………….… 7

11.0 MALAYSIAN LAND LAW …….………………………………………………………..…………………………….… 7

12.0 THE PROPERTIES IN THEIR EXISTING CONDITION .…………………………………..………….… 8

12.1 INDONESIAN PROPERTIES ……...…………………………………………………………………… 8 & 9

12.1 MALAYSIAN PROPERTIES ………………….. .……………………………………………………. 10 - 12

12.2 BERTAM ESTATE ……………………………………………………………………………..…… 10 12.2 BERTAM PROPERTIES SDN BHD …………………………………………………..……11 & 12

__________________________________________________________________________________

(ii)

13.0 TERRAIN AND SOIL……………………..………………………………………………………………………… 14

14.0 RAINFALL ……………………………………..………………………………………………………………………… 13 & 14

15.0 MAINTENANCE AND MANAGEMENT ……………………………………………………………………… 14

16.0 BUILDING AND STRUCTURES, PLANT & MACHINERY AND MOTOR VEHICLES AND OFFICE EQUIPMENT……… …………..…………………………………………………………………… 14

17.0 CRUDE PALM OIL AND KERNEL PRICES..…………………………………………………………….… 15 - 17

18.0 YIELDS …………………………………………………………………………………………………………….…….. 17 - 20

19.0 Oil EXTRACTION RATE …………………………………………………………………………………………… 20 & 21

20.0 PLASMA ……………………..…………………………………………………………………………………………... 22

21.0 VALUATION ……………………..…………………………………………………………………………………… 23

22.0 ROLLING VALUES ……………..…………………………………………………………………………………… 24

23.0 COMPARISON APPROACH TO VALUE .…………………………………………………………………… 24 & 25

24.0 SENSITIVITY ANALYSIS ………………………………………………………………………………………… 26

25.0 VALUATION ………………………………………………………………………………………………………….… 26 & 27

__________________________________________________________________________________

(iii)

LIST OF FIGURES Figure 1: Location Plan ……….……………..…………………………………………………..……..………………… 2

Figure 2: Yield Profile for Pangkatan Estate (Current Planting) ……………………………………… 18 Figure 3: Yield Profile for Kalimantan Estate (Current Planting) ………………………………. 18 Figure 4: Expected Yield Profile for Kalimantan Estate (Replanting) …………………………….. 19 Figure 5: Expected Yield Profile for Pangkatan Estate (Replanting) ………………………………… 19

LIST OF TABLES

Table 1: Terrain & Soil Classification ……………………………………………………………………………….. 13

Table 2: Average Rainfall for the MPE’s Indonesian Plantations – 2011 to 2015 ………… 14

Table 3 - Average selling prices of CPO in the Sumatra Region - Pangkatan Mill ……….. 15

Table 4 - Average selling prices of CPO in the Kalimantan Region – Bumi Permai Mill … 16

Table 5 - Average selling prices of CPO in the Bangka Region– Tengkalat Mill …………… 16

Table 6 – Monthly prices of palm oil products (Source: Malaysian Palm Oil Board) …… 17

Table 7: Historical Oil Extraction Rates used in our valuation model …………………………… 20

Table 8: Projected Oil Extraction Rates used in our valuation model …………………………… 21

Table 9: Rolling Values …………………………………………………………………………………………………. 24

Table 10: Major sales of large Plantations ……………………………………………………………………… 25

Table 11: Summary of our Valuation …………………………………………………………………………….. 27

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 1 | November 2016

1.0 INTRODUCTION: We are to undertake a valuation of the real estate interests or plantation interests of MPE in Malaysia and Indonesia. The real estate interest of MPE in Malaysia is from its ownership of properties that can be identified from their annual report as Bertam Properties Sdn Bhd and Bertam Estates. The plantation interests of MPE in Indonesia can be identified from their annual report in various oil palm plantations and named as Simpang Kiri, Kerasaan, Sennah, Bilah, Pangkatan, Agro Muko, Musi Rawas, Bangka and Kalimantan. The basis of valuation for all the Properties shall be the Market Value of the real estate or plantation interests subsisting in the properties. This will accord with the basis as shown in the Red Book of the Royal Institution of Chartered Surveyors, United Kingdom. 2.0 REAL ESTATE INTERESTS/PLANTATION INTERESTS OVERVIEW: 2.1 INDONESIAN PLANTATIONS OVERVIEW

Oil Palm In accordance with the 2016 interim report of MPE and as subsequently amended from our determination of facts in this exercise, MPE has a majority interest in in 26,547 planted hectares and a substantial minority interest in 21,861 planted hectares of oil-palm plantations in Indonesia. MAJORITY OWNED Sumatra Existing mature plantations As at the date of valuation, MPE had a majority interest in 9,336 hectares of oil palm planted in Sumatra. This consists of some 6,958 planted hectares in three estates which are in close proximity to one another namely the Pangkatan, Bilah and Sennah Estates in the Labuhan Batu District of North Sumatra. A 40-metric tonne-per-hour crude palm-oil processing mill was commissioned in 2005 on the Pangkatan Estate to process the fruit from these three estates. Simpang Kiri Estate (2,371 hectares) is located in the south-east corner of the province of Aceh. MPE also has a majority interest in the 7,000-hectare Musi Rawas Estate to be developed in South Sumatra and a 3,000-hectare smallholders’ cooperative to be developed and managed by MPE. East Kalimantan At as the date of valuation, MPE had developed almost all of its East Kalimantan project, and had planted 14,616 hectares of oil-palm land, of which 4,366 hectares are owned by associated smallholder co-operatives near Samarinda in East Kalimantan. The largely-open land is deemed highly suitable for oil-palm cultivation in terms of soil conditions, terrain and climate. As one of the terms of the license to develop the land, smallholders' co-operatives, comprising 4,366 hectares have been developed on the project and are managed by MPE. The co-operatives' fruit is processed by MPE's mill which was commissioned at the end of 2011. A small amount of further planting is ongoing at the project, and this is expected to be completed within the next 18 months.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 2 | November 2016

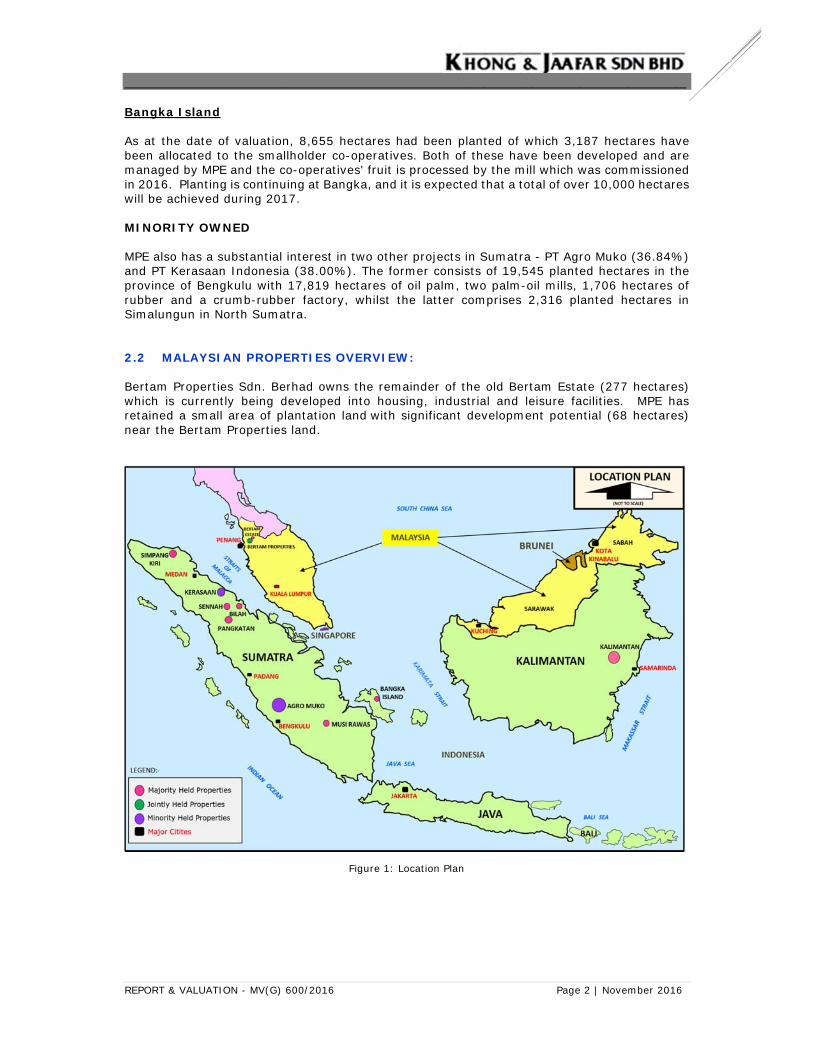

Bangka Island As at the date of valuation, 8,655 hectares had been planted of which 3,187 hectares have been allocated to the smallholder co-operatives. Both of these have been developed and are managed by MPE and the co-operatives' fruit is processed by the mill which was commissioned in 2016. Planting is continuing at Bangka, and it is expected that a total of over 10,000 hectares will be achieved during 2017. MINORITY OWNED MPE also has a substantial interest in two other projects in Sumatra - PT Agro Muko (36.84%) and PT Kerasaan Indonesia (38.00%). The former consists of 19,545 planted hectares in the province of Bengkulu with 17,819 hectares of oil palm, two palm-oil mills, 1,706 hectares of rubber and a crumb-rubber factory, whilst the latter comprises 2,316 planted hectares in Simalungun in North Sumatra. 2.2 MALAYSIAN PROPERTIES OVERVIEW: Bertam Properties Sdn. Berhad owns the remainder of the old Bertam Estate (277 hectares) which is currently being developed into housing, industrial and leisure facilities. MPE has retained a small area of plantation land with significant development potential (68 hectares) near the Bertam Properties land.

Figure 1: Location Plan

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 3 | November 2016

3.0 QUALIFICATIONS:

The Khong & Jaafar Group was initially established in 1965 by Mr Khong Chia Soon and Encik Jaafar Wazir, both of whom have since retired. The Group comprises three private limited companies namely, Khong & Jaafar Sdn Bhd, Khong & Jaafar (Real Estate) Sdn Bhd and Khong & Jaafar (Corporate Services) Sdn Bhd. Khong & Jaafar Sdn Bhd is the main company and undertakes all property valuations (real estate, businesses, intangibles and plant & machinery), property management, property consultancy, property investment advisory, market and feasibility research and studies, litigation support, tenant representation and dispute resolution (expert determination). Khong & Jaafar is licensed to carry out its property related work throughout Malaysia, which it does and has more than 51 years of experience in valuing all types of properties including specialized properties such as plant & machinery, granite quarries, development rights, land for reclamation purposes, timber concessions, oil palm plantations, oil palm refineries, oil palm mills, steel mills, shopping centres, airport facility, various property interests subsisting within real estate for various purposes including for purposes of submission to the Securities Commission of Malaysia and litigation support for court cases. We have also carried out work in the region for various corporate entities, for example valuations in the United Kingdom, Australia, New Zealand, Indonesia, Papua New Guinea, the Solomon Islands, Vanuatu, Canada, China, India, Pakistan, Kyrgyzstan and Japan. The valuations are to be undertaken on an independent basis and we can assure you that Khong & Jaafar Sdn Bhd which is incorporated in Malaysia has been involved in the valuation of real estate interests, including oil palm plantations for the past 51 years. Khong & Jaafar is a registered valuation firm under the Valuers, Appraisers and Estate Agents Act 1981, Malaysia. Khong and Jaafar is eminently qualified to undertake the valuation, including the oil palm plantations and has the necessary expertise. The current major shareholder of the company and Managing Director, Elvin Fernandez, is a Fellow of the Royal Institution of Chartered Surveyors, United Kingdom, and a Past Chairman of the International Valuation Standards Council, a Past President of the Royal Institution of Surveyors Malaysia and the current Secretary General of the ASEAN Valuers Association among many other professionally related qualifications. Elvin Fernandez, who will in fact be the signing valuer in the valuation entered the valuation profession in 1979 by passing the Final Examinations set by the Royal Institution of Surveyors Malaysia. This valuation assignment was headed by: Elvin Fernandez, PPRISM, FRISM, FRICS Managing Director of the Khong & Jaafar Group of Companies Independent Non-Executive Director of Sunway REIT Management Sdn Bhd Secretary General of the ASEAN Valuers Association Member and Qualified Business Valuation Instructor of the International Association of

Consultants, Valuators & Analysts Vice President of the Business Valuers Association Malaysia Executive Committee Member of the Association of Valuers, Property Managers, Estate

Agents and Property Consultants in the Private Sector Malaysia (PEPS) Past President of the Royal Institution of Surveyors Malaysia (RISM) Past President of the Association of Valuers, Property Managers, Estate Agents and Property

Consultants in the Private Sector Malaysia Past Chairman of the International Valuation Standards Council. Past Member/Exco Member of the Board of Valuers, Appraisers and Estate Agents Malaysia

from 1993 till 2007 Fellow of the Royal Institution of Chartered Surveyors, UK Life Fellow of the Institution of Valuers India

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 4 | November 2016

Member of the Practising Valuers Association (India) Member of the Institute of Philippine Real Estate Appraisers Member of the National Association of Romanian Valuers Member of the Indonesian Society of Appraisers (MAPPI) Member of the China Appraisal Society Awarded “Property Consultant of the Year 2005” by the Board of Valuers in 2006 Conferred with “Professional Excellence” Award in the “Engineering, Construction &

Property” Category by the Malaysian Professional Centre in May 2011 Conferred with “Valuer of the Year 2013” Award by the Valuation Division of RISM in January

2014 Awarded the Million Dollar Roof Top Award by the Malaysian Institute of Estate Agents

(MIEA) on 1 October 2016 Written and presented about 200 papers on property related topics for conferences since

1991 in Malaysia and other countries Featured regularly on property related articles in local newspapers. Elvin Fernandez was assisted by the following persons:- Rozina Shafiei, Director. MSc. Urban Land Appraisal (University of Reading, UK), BSurv.(Hons) Property Management, University of Technology Malaysia, Registered Valuer & Estate Agent Malaysia, Elected Fellow of the Royal Institution of Surveyors, Malaysia (since 23 January 2015). Over 35 years’ experience including 14 years in Khong & Jaafar.

Thilagavathi Ganesan, Executive Assistant to the Managing Director. Graduated with a Diploma in Private Secretaryship from Bedford College, Kuala Lumpur in 1986. Over 30 years’ experience including 27 years in Khong & Jaafar.

Shanti Rani Kolandasamy, Manager. MBA (Finance) (University Malaya), BSurv. (Hons) Property Management and Diploma in Valuation, University of Technology Malaysia. Registered Valuer & Estate Agent Malaysia, Elected Member of the Royal Institution of Surveyors, Malaysia. Over 33 years’ experience including 4 years in Khong & Jaafar.

Rihana Rahim, Senior Valuation Officer. Advance Diploma in Estate Management University of Technology MARA. Over 21 years’ experience in Khong & Jaafar. Terence Rajiv Francis, Valuation Officer. Bachelor (Hons) in Estate Management, University Malaya. Over 9 years’ experience including 5 years with Khong & Jaafar. Rafizah Abdul Rahman, Senior Valuation Officer. Diploma in Estate Management – Institute of Technology MARA, Bachelor of Science (Hons) in Property Management, University of Technology Malaysia. Over 19 years’ experience in Khong & Jaafar.

Zurina Meor Abd Ghani, Senior Valuation Officer. Diploma in Estate Management – Institute of Technology MARA, Bachelor of Science (Hons) in Property Management, University of Technology Malaysia. Over 25 years’ experience in Khong & Jaafar. Lydia Ong Ling Yen, Valuation Officer. Bachelor of Business Management Majoring in Real Estate and Development, University of Queensland, Australia. Over 5 years’ experience in Khong & Jaafar.

Wong Li Mei, Penang Branch Manager. Registered Valuer & Estate Agent Malaysia, Bachelor (Hons) in Estate Management, University Malaya. Over 5 years’ experience including 3 months in Khong & Jaafar. Letchumi Simanchalam, Valuation Executive. Bachelor (Hons) in Land Administration and Development - University of Technology Malaysia. Over 15 years’ experience with 12 years in Khong & Jaafar.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 5 | November 2016

Remy Azrul Mustaffar, Senior Valuation Executive. Diploma in Estate Management from University of Technology MARA, Malaysia. Over 20 years’ experience in Khong & Jaafar. Dhibhan Jayakumaran, Valuation Officer. Bachelor of Science (Property Management) - University Technology Malaysia, 2014. Over 2 years’ experience in Khong & Jaafar.

Rosmini Ismail, Valuation Officer. Bachelor (Hons) in Estate Management. Over 1 year experience in Khong & Jaafar.

Mohamad Ehsan Shafiq Bin Mohamad Sazali, Valuation Officer. Bachelor (Hons) in Estate Management, University Malaya. Over 1 year experience in Khong & Jaafar.

Tengku Nor Hasyimah binti Tengku Azmi, Degree in Estate Management from University Tun Hussein Onn Malaysia. Over 1 year experience in Khong & Jaafar

Alice Ponnazhakan, Valuation Officer. Bachelor (Hons) in Estate Management, University Malaya. Over 7 years’ experience with 4 years in Khong & Jaafar.

Gerald Dass Solomon, Valuation Executive. Over 25 years’ experience in Khong & Jaafar 4.0 BASIS OF OPINION: The basis of valuation for all the Properties is the Market Value of the real estate interests or plantation interests subsisting in the Properties. This will accord with the basis as shown in the Red Book of the Royal Institution of Chartered Surveyors, United Kingdom. In this connection we are to provide an opinion of the Market Value of the Properties in their existing condition with vacant possession and subject to their Titles/HGUs (issued and to be issued) being free from encumbrances good marketable and registrable. “Market Value” is the estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing where the parties had each acted knowledgeably, prudently and without compulsion. 5.0 INDEPENDENCE: Khong & Jaafar makes the following disclosures:- Khong & Jaafar is independent with respect to MPE and confirms that there is no conflict of

interest with any party involved in the assignment.

Under the terms of engagement between Khong & Jaafar and MPE for the provision of this report, Khong & Jaafar will receive a fee, based on time expended at our current standard terms and conditions, payable by MPE. The payment of this fee is not contingent on the outcome of the proposed transaction.

No interests are currently held by Khong & Jaafar Directors or by staff involved in

the preparation of this report.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 6 | November 2016

6.0 DATE OF VALUATION: The Properties were inspected between 10 and 16 November 2016. The date of valuation is taken to be as at the last date of inspection, i.e. 16 November 2016 and we report as follows:- 7.0 EXCHANGE RATE: Throughout this report the currency value is shown in US Dollars. As at 1 November 2016, the exchange rate between the US Dollar and the Malaysian Ringgit was USD1 = RM4.2. As for the Indonesian Rupiah it was 1 USD to 13,041.3297 Indonesian Rupiah (Rp). 8.0 INDONESIA IN GENERAL: The Republic of Indonesia is the world’s longest archipelago stretching 5,000 kilometres in length from the mainland of Asia into the Pacific Ocean. It comprises 17,508 islands, of which 6,000 are inhabited. The largest and main islands are Kalimantan, Sumatra, Sulawesi, Irian Jaya and Java. The total population of Indonesia is estimated at about 261.73 million in 2016, with most living on the islands of Java, Sumatra, Sulawesi and Kalimantan. The capital city of Indonesia is Jakarta and it is located in West Java. The national language is Bahasa Indonesia although nearly 600 other dialects are spoken throughout the archipelago. Indonesia is blessed with a rich variety of natural resources which include deposits of oil, minerals, gemstones, coal, bauxite and tin to name a few. In addition to the minerals in the land, it has a never-ending supply of sunshine, rain and soft volcanic ashes which have thus provided an excellent climate for the cultivation of cash crops in the western islands such as tea plantations in Java, rice fields in Bali and rubber and oil palm estates in Sumatra. 9.0 INDONESIAN LAND LAW: The Government of Indonesia has been looking into ways of attracting foreign investors into Indonesia since the 1990’s. In line with this policy, the government has promulgated a new regulation regarding the rights in land in Indonesia. Based on the Presidential Decree 34/1992 dated 6 July 1992, it introduced a new set of regulations within the context of Foreign Laws No. 11/1970. This decree stipulates that foreign investors are now entitled to the Right to Cultivate in land and the Right to Build. These rights are registrable and may be pledged as collateral to banks. These new rights in land and the registration of the titles may be applied through the Badan Pertanahan Nasional (National Land Board). The basic land laws and “rights in Land” are governed under the Basic Agrarian Law of 1960. Under this law, eleven types of land rights are provided such as:- i) Hak Milik (right of ownership) ii) Hak Guna Usaha (right to cultivate) iii) Hak Milik Bangunan (right to build) iv) Hak Pakai (right of use) v) Hak Sewa Untuk Bangunan (right to lease for building) vi) Hak Sewa Pertanian (right to lease in farmland)

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 7 | November 2016

vii) Hak Membuka Tanah (right to clear land) viii) Hak Memungut Hasil Hutan (right to harvest forest products) ix) Hak Gadai (right to pawn) x) Hak Usaha Bagi Hasil (right of sharecropping) xi) Hak Menumpang (right of lodging) The most common rights in land are Hak Milik, Hak Guna Bangunan and Hak Guna Pakai/Usaha. The “Hak Milik” category is the strongest right in land which can only be held by natural persons who are Indonesian by nationality. Therefore, no legal entities such as limited liability companies both operating within or outside the domestic and foreign investment laws are permitted to hold such lands under this category of rights. The right conferred shall be a grant-in-perpetuity. The Indonesian Properties fall under the Hak Guna Usaha (HGU) category i.e. the rights to cultivate the land (which may be either issued to individual companies or natural persons) for farming, agricultural and fishing purposes. Foreign entities or limited liability companies with foreign participation established under Law 1, Year 1976 on Foreign Investment may also obtain and hold this right. The HGU rights conferred to any persons may have a validity period of 25-35 years with a further extension of an additional 25 years upon application. 10.0 MALAYSIA IN GENERAL: Malaysia, a country of 30.98 million, is a parliamentary democracy. It is a Federation of 14 States and 2 Federal Territories one of which is the capital city of Kuala Lumpur. The country can be broadly divided into Peninsular Malaysia which is attached to the Asian mainland and the East Malaysian States of Sabah and Sarawak which occupy the northern part of an island which was formerly known as Borneo. Malaysia has a 100-year plus operating free market in property. Generally there are no restrictions to entrants to the market to develop and supply properties in accordance with the dictates of the market. There is security of tenure in property in a codified land law. Foreign ownership of substantial Malaysian property is generally restricted to 30 per cent which is a target tenet of the national plan. For smaller properties foreign ownership is generally allowed except the purchase of low-end residential property. 11.0 MALAYSIAN LAND LAW: Prior to the independence in 1957, Malaysia was part of the British Empire and being so it has a Common Law framework quite similar to the United Kingdom. The predominant Land Law is the Malaysian National Land Code which is based on the Torrens System of Registration. The Town and Country Planning Act has its source from the British Town and Country Planning laws as well. So do other land legislations such as the Land Acquisition Act.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 8 | November 2016

12.0 THE PROPERTIES IN THEIR EXISTING CONDITION: 12.1 INDONESIAN PROPERTIES There are 9 oil palm plantations in all, namely, Simpang Kiri, Kerasaan, Sennah, Bilah, Pangkatan, Agro Muko, Musi Rawas, Bangka and Kalimantan. The first seven mentioned above are in Sumatra, Bangka is in Bangka Island and Kalimantan is in East Kalimantan. The older and majority held estates i.e. Simpang Kiri, Bilah, Sennah and Pangkatan.are in North Sumatra. Three of the newer estates namely Kalimantan, Bangka and Musi Rawas have plasma areas or KKPA and these are explained later in the report. Of the two minority held, Kerasaan is in North Sumatra and Agro Muko is in South Sumatra. There is a 40-tonne oil palm processing mill in Pangkatan, a 60-metric tonne in Kalimantan, a 45-metric tonne mill in Bangka and two mills in Agro Muko which are 30 and 60 metric tonnes. There is a proposed mill in Musi Rawas which is to be a 45-metric tonne and due for construction in about three years’ time. There is also another proposed 45-metric tonne mill in Kalimantan and this is due for construction in mid-2017. There is also a bulking station for storage of crude palm oil in Kalimantan and a crumb rubber factory in Agro Muko.

Kahoi Estate, Kalimantan

Air Bikuk Estate, Agro Muko

Harvesting, Kahoi Estate

A general view of the Kahoi Estate in Kalimantan

A general view of the Air Buluh Estate in Agro Muko A general view of the Kerasaan Estate

__________________________________________________________________________________

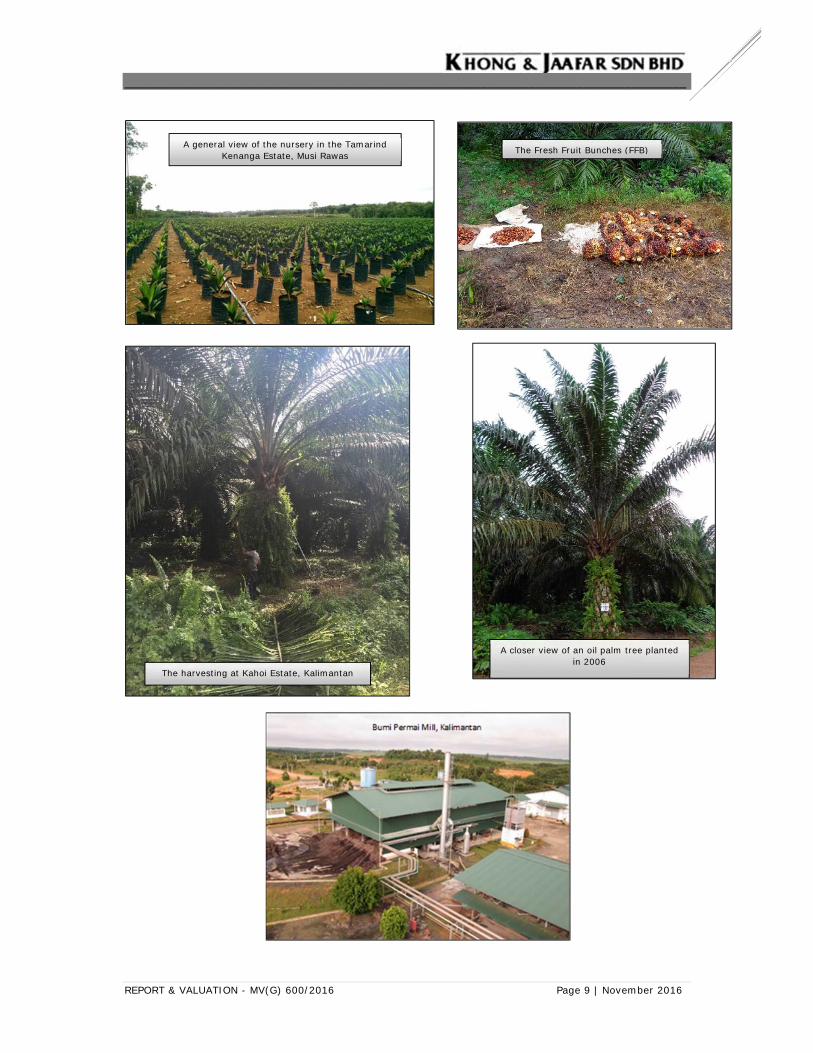

REPORT & VALUATION - MV(G) 600/2016 Page 9 | November 2016

A general view of the nursery in the Tamarind Kenanga Estate, Musi Rawas The Fresh Fruit Bunches (FFB)

The harvesting at Kahoi Estate, Kalimantan

A closer view of an oil palm tree planted in 2006

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 10 | November 2016

12.2 MALAYSIAN PROPERTIES 12.2.1 Bertam Estate Bertam Estate, which is located in the Mukim 3, District of Seberang Perai Utara, Penang, Malaysia, comprises 19 lots held under grants-in-perpetuity with category of land use ‘Nil’ and has a total land area of 68.3 hectares. 9 lots are held under First Grade Grants and the remaining lots are held under Mukim Grants/Grants.

The lots are located scattered along and off Jalan Paya Keladi, Bertam, about 7 kilometres and 23 kilometres northeast of the towns of Kepala Batas and Butterworth respectively. 9 of the lots are zoned residential and the remaining 10 lots are zoned agriculture. Generally, its terrain is flat and lies at the same level with the frontage road. During the course of our inspection, we noted that the land was encumbered with about 10 squatters and usually there is an element of compensation that must be made prior to development for the removal of these squatters. We have taken this fact into account in arriving at our opinion of value. Bertam Estate is an agriculture land built upon with a warehouse and workers’ quarters. It has significant development potential due to its location. 12.2.2 Bertam Properties Sdn Bhd The real estate interest in Bertam Properties comprises the Penang Golf Resort and the ongoing Bertam Perdana township development comprising commercial, residential and institutional developments. The Penang Golf Resort is held under 3 freehold titles and fronting Jalan Tun Hamdan Sheik Tahir, and comprises three contiguous parcels of land with a combined title land area of 142.62 hectares developed with a 36-hole golf course complete with a clubhouse and a driving range.

The entrance to Penang Golf Resort A closer view of the golf course

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 11 | November 2016

The Bertam Perdana development made up of Bertam Perdana 1, 2 and 4 is located in Mukim 6, District of Seberang Perai Utara, Penang, Malaysia and lies to the immediate east of the Bertam Interchange of the North-South Expressway along the northern side of Jalan Tun Hamdan Sheik Tahir at about a kilometre east and 17 kilometres north-east of the towns of Kepala Batas and Butterworth respectively. Bertam Perdana 1 is a 32.72-hectare parcel of land located near to the Tesco site of Bertam Perdana. It is made up of 7 individual lots, out of which 1 is zoned for residential use and the remaining 6 are zoned for commercial use. All these 7 lots are presently vacant and there are no buildings on it.

A general view of Bertam Perdana 1 fronting Persiaran Dagangan

A closer view of part of Bertam Perdana 1

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 12 | November 2016

Bertam Perdana 2 is an 86.724-hectare parcel of land collectively held under 6 individual lots. One of the lots with an area of 69.21 hectares is approved for 81 single-storey detached houses, 61 2-storey detached houses, 91 single-storey semi-detached houses, 58 2-storey semi-detached houses, 140 single-storey terrace houses, 140 2-storey low-cost cluster houses and 20 2-storey shop offices. Although approved for this development, the land is vacant and there are no buildings on it. The remaining 5 lots are held under lands which are zoned for mixed development and for residential development. They are also vacant. Bertam Perdana 4 is a 15.10-hectare parcel of land held under 10 Parent Titles that have been surrendered for purposes of subdivision into 249 individual lots. It has been approved for development of 67 single-storey detached houses, 26 2-storey detached houses, 44 2-storey semi-detached houses and 112 2-storey terrace houses.

A general view of part of Bertam Perdana 2 fronting Jalan Tun Hamdan Sheik Tahir A general view of part of Bertam Perdana 2

(indicated by a red arrow) taken from lakeside.

A general view of part of Bertam Perdana 4 (indicated by a red arrow) fronting Persiaran

Perindustrian Bertam Perdana

A closer view of part of Bertam Perdana 4

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 13 | November 2016

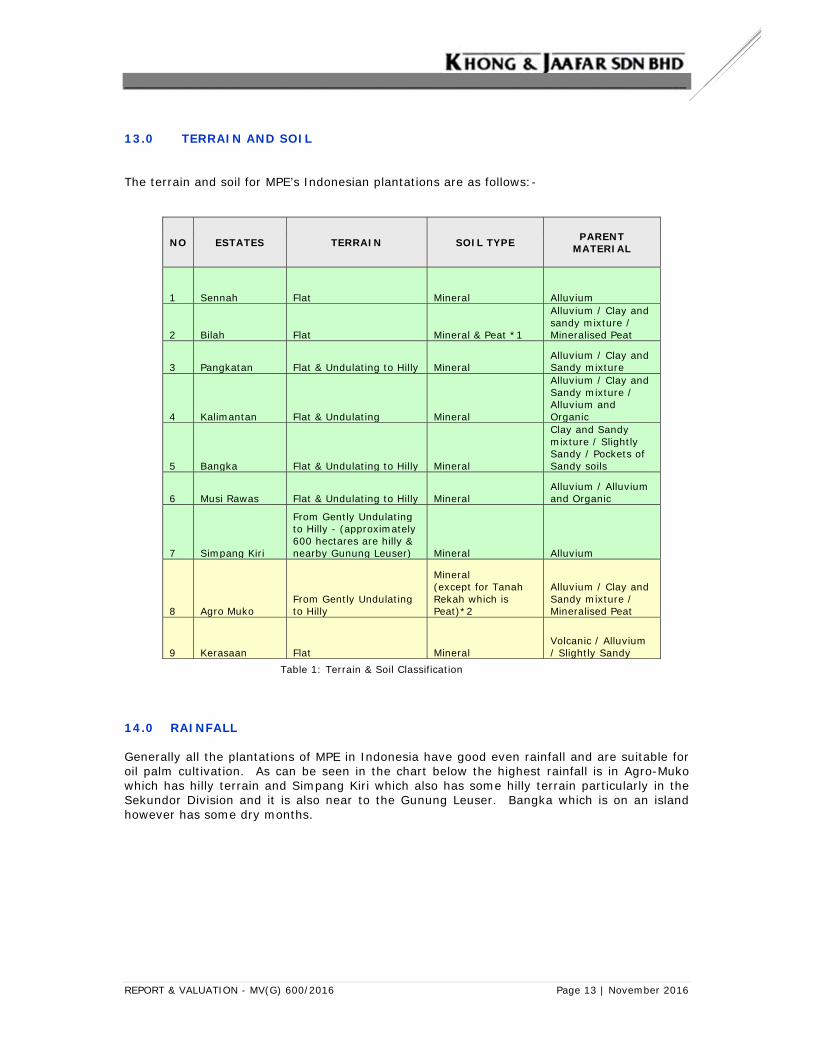

13.0 TERRAIN AND SOIL The terrain and soil for MPE’s Indonesian plantations are as follows:-

NO ESTATES TERRAIN SOIL TYPE PARENT MATERIAL

1 Sennah Flat Mineral Alluvium

2 Bilah Flat Mineral & Peat *1

Alluvium / Clay and sandy mixture / Mineralised Peat

3 Pangkatan Flat & Undulating to Hilly Mineral Alluvium / Clay and Sandy mixture

4 Kalimantan Flat & Undulating Mineral

Alluvium / Clay and Sandy mixture / Alluvium and Organic

5 Bangka Flat & Undulating to Hilly Mineral

Clay and Sandy mixture / Slightly Sandy / Pockets of Sandy soils

6 Musi Rawas Flat & Undulating to Hilly Mineral Alluvium / Alluvium and Organic

7 Simpang Kiri

From Gently Undulating to Hilly - (approximately 600 hectares are hilly & nearby Gunung Leuser) Mineral Alluvium

8 Agro Muko From Gently Undulating to Hilly

Mineral (except for Tanah Rekah which is Peat)*2

Alluvium / Clay and Sandy mixture / Mineralised Peat

9 Kerasaan Flat Mineral Volcanic / Alluvium / Slightly Sandy

Table 1: Terrain & Soil Classification

14.0 RAINFALL Generally all the plantations of MPE in Indonesia have good even rainfall and are suitable for oil palm cultivation. As can be seen in the chart below the highest rainfall is in Agro-Muko which has hilly terrain and Simpang Kiri which also has some hilly terrain particularly in the Sekundor Division and it is also near to the Gunung Leuser. Bangka which is on an island however has some dry months.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 14 | November 2016

15.0 MANAGEMENT AND MAINTENANCE The Management is headed by Mr Chandra Sekaran who has four persons who work directly under him i.e. the Head of Finance, Head of Procurement and Marketing, Head of Agronomy and Head of Engineering. There are about 300 staff in total who make up the Management team.

The estates are well maintained. We have been informed and we have observed that there is a Zero Burning Policy for the development of the plantations. In a vast area such as these plantations, there is inevitably some pockets of peat but we believe that these smallish pockets of peat are easily managed and can be mineralised over time. We also understand that MPE does not do any development in areas considered virgin forest but confines itself only to areas which are previously logged over. MPE also has a Zero Waste Program where mill waste is turned into compost and this compost is used as fertiliser. MPE adheres to the Round Table on Sustainable Palm Oil (RSPO), Indonesian Sustainable Palm Oil (ISPO) and International Sustainability and Carbon Certification (ISCC), all of which ensures that they get premium prices. 16.0 BUILDINGS AND STRUCTURES, PLANT & MACHINERY AND MOTOR

VEHICLES AND OFFICE EQUIPMENT

We have perused copies of the schedules of buildings and structures and plant and machinery (including in the mills), motor vehicles, and office equipment provided by the Jakarta Office of MPE and generally we consider these items to be in good repairing condition. In our valuation model, they are taken to be ancillary items required for the operations of the Estate and their values are reflected within the Estate Values we have arrived at.

0

500

1000

1500

2000

2500

3000

3500

4000

Sennah Bilah Pangkatan Kalimantan Bangka MusiRawas

SimpangKiri

Agro Muko Kerasaan

Average Rainfall (in mm) 2156 2138 2237 2051 1702 2305 3873 3482 2026

Average

Rainfall (in m

m)

Average Rainfall for the MPE's Indonesian Plantations ‐ 2011 to 2015

Table 2: Average Rainfall for the MPE’s Indonesian Plantations – 2011 to 2015

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 15 | November 2016

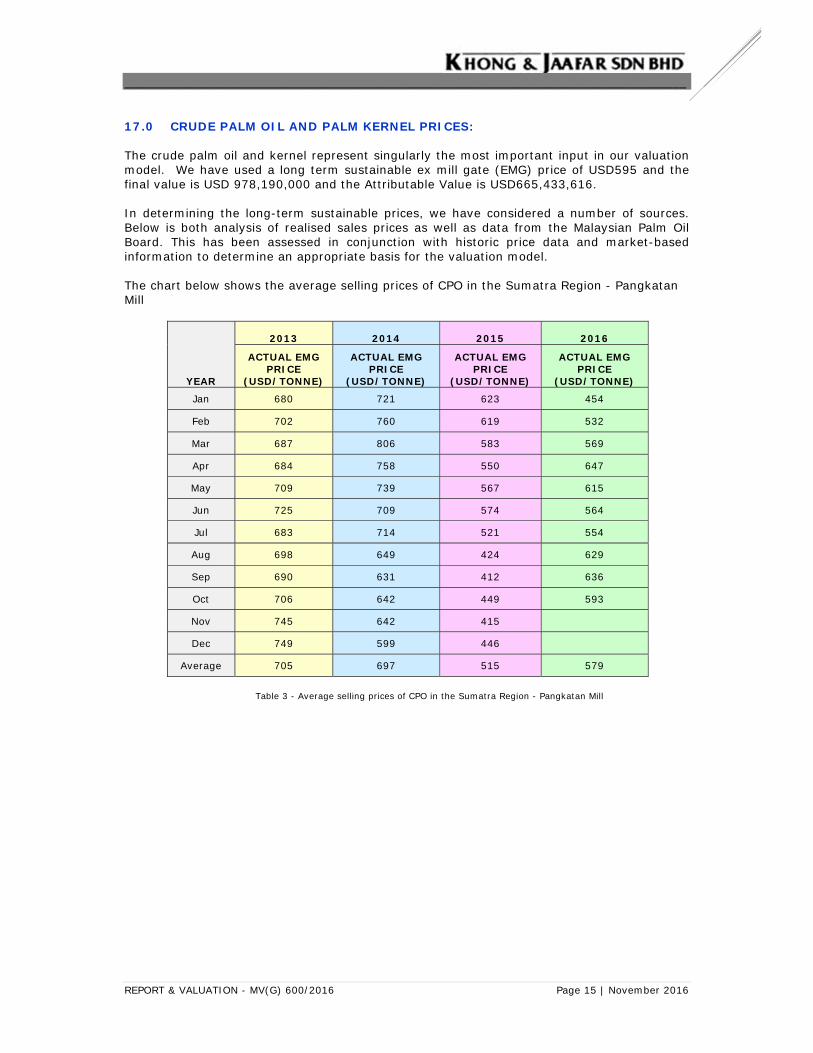

17.0 CRUDE PALM OIL AND PALM KERNEL PRICES:

The crude palm oil and kernel represent singularly the most important input in our valuation model. We have used a long term sustainable ex mill gate (EMG) price of USD595 and the final value is USD 978,190,000 and the Attributable Value is USD665,433,616.

In determining the long-term sustainable prices, we have considered a number of sources. Below is both analysis of realised sales prices as well as data from the Malaysian Palm Oil Board. This has been assessed in conjunction with historic price data and market-based information to determine an appropriate basis for the valuation model. The chart below shows the average selling prices of CPO in the Sumatra Region - Pangkatan Mill

YEAR

2013 2014 2015 2016

ACTUAL EMG PRICE

(USD/TONNE)

ACTUAL EMG PRICE

(USD/TONNE)

ACTUAL EMG PRICE

(USD/TONNE)

ACTUAL EMG PRICE

(USD/TONNE)

Jan 680 721 623 454

Feb 702 760 619 532

Mar 687 806 583 569

Apr 684 758 550 647

May 709 739 567 615

Jun 725 709 574 564

Jul 683 714 521 554

Aug 698 649 424 629

Sep 690 631 412 636

Oct 706 642 449 593

Nov 745 642 415

Dec 749 599 446

Average 705 697 515 579

Table 3 - Average selling prices of CPO in the Sumatra Region - Pangkatan Mill

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 16 | November 2016

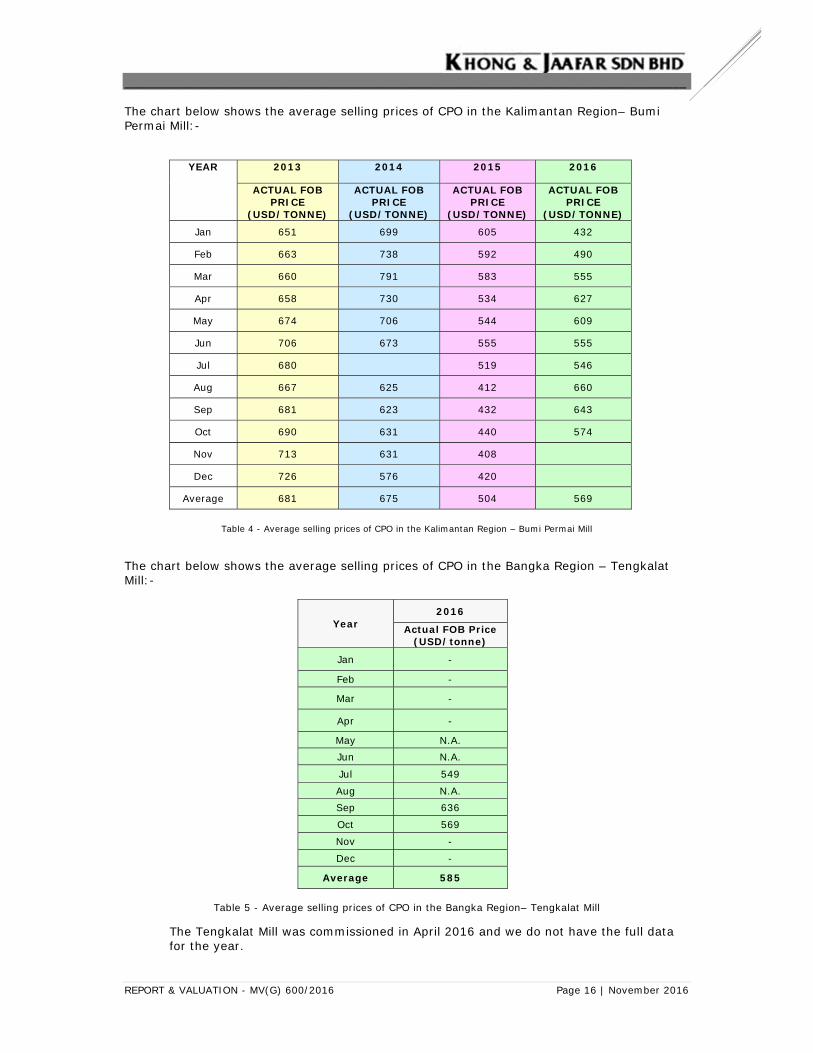

The chart below shows the average selling prices of CPO in the Kalimantan Region– Bumi Permai Mill:-

YEAR 2013 2014 2015 2016

ACTUAL FOB PRICE

(USD/TONNE)

ACTUAL FOB PRICE

(USD/TONNE)

ACTUAL FOB PRICE

(USD/TONNE)

ACTUAL FOB PRICE

(USD/TONNE)

Jan 651 699 605 432

Feb 663 738 592 490

Mar 660 791 583 555

Apr 658 730 534 627

May 674 706 544 609

Jun 706 673 555 555

Jul 680 519 546

Aug 667 625 412 660

Sep 681 623 432 643

Oct 690 631 440 574

Nov 713 631 408

Dec 726 576 420

Average 681 675 504 569

Table 4 - Average selling prices of CPO in the Kalimantan Region – Bumi Permai Mill

The chart below shows the average selling prices of CPO in the Bangka Region – Tengkalat Mill:-

Year 2016

Actual FOB Price (USD/tonne)

Jan -

Feb -

Mar -

Apr -

May N.A. Jun N.A.

Jul 549

Aug N.A. Sep 636

Oct 569

Nov -

Dec -

Average 585

Table 5 - Average selling prices of CPO in the Bangka Region– Tengkalat Mill

The Tengkalat Mill was commissioned in April 2016 and we do not have the full data for the year.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 17 | November 2016

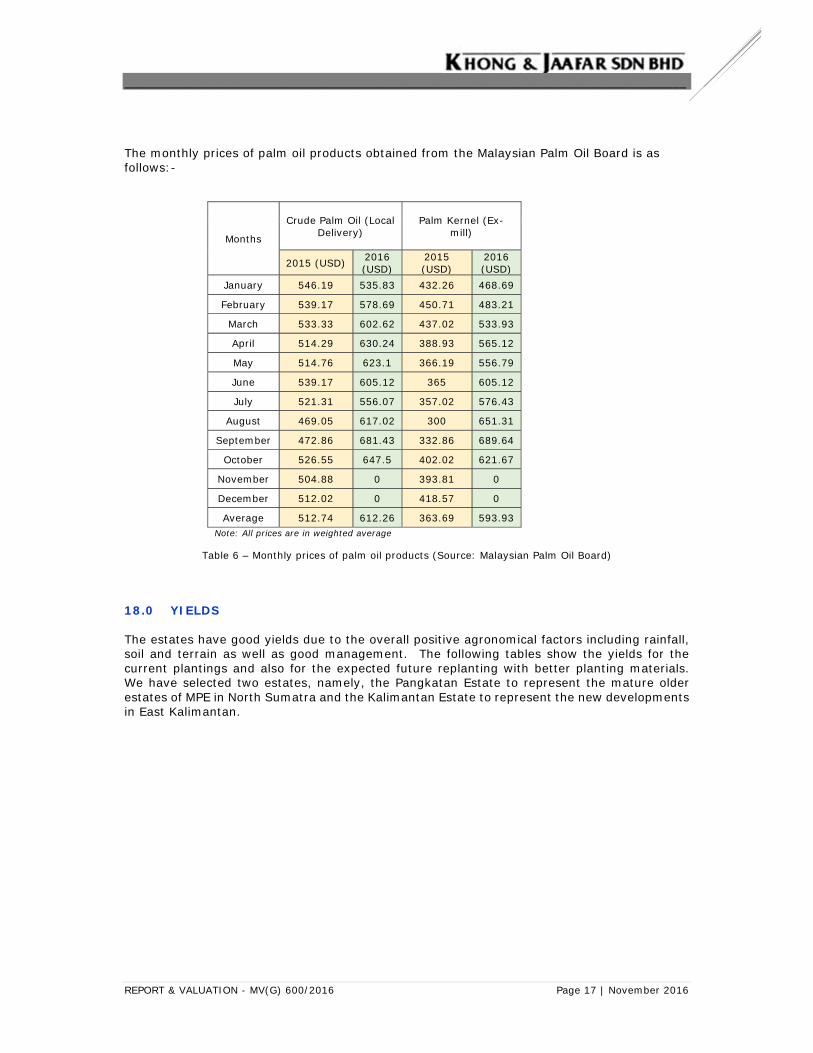

The monthly prices of palm oil products obtained from the Malaysian Palm Oil Board is as follows:-

Months

Crude Palm Oil (Local Delivery)

Palm Kernel (Ex-mill)

2015 (USD) 2016 (USD)

2015 (USD)

2016 (USD)

January 546.19 535.83 432.26 468.69

February 539.17 578.69 450.71 483.21

March 533.33 602.62 437.02 533.93

April 514.29 630.24 388.93 565.12

May 514.76 623.1 366.19 556.79

June 539.17 605.12 365 605.12

July 521.31 556.07 357.02 576.43

August 469.05 617.02 300 651.31

September 472.86 681.43 332.86 689.64

October 526.55 647.5 402.02 621.67

November 504.88 0 393.81 0

December 512.02 0 418.57 0

Average 512.74 612.26 363.69 593.93 Note: All prices are in weighted average

Table 6 – Monthly prices of palm oil products (Source: Malaysian Palm Oil Board)

18.0 YIELDS

The estates have good yields due to the overall positive agronomical factors including rainfall, soil and terrain as well as good management. The following tables show the yields for the current plantings and also for the expected future replanting with better planting materials. We have selected two estates, namely, the Pangkatan Estate to represent the mature older estates of MPE in North Sumatra and the Kalimantan Estate to represent the new developments in East Kalimantan.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 18 | November 2016

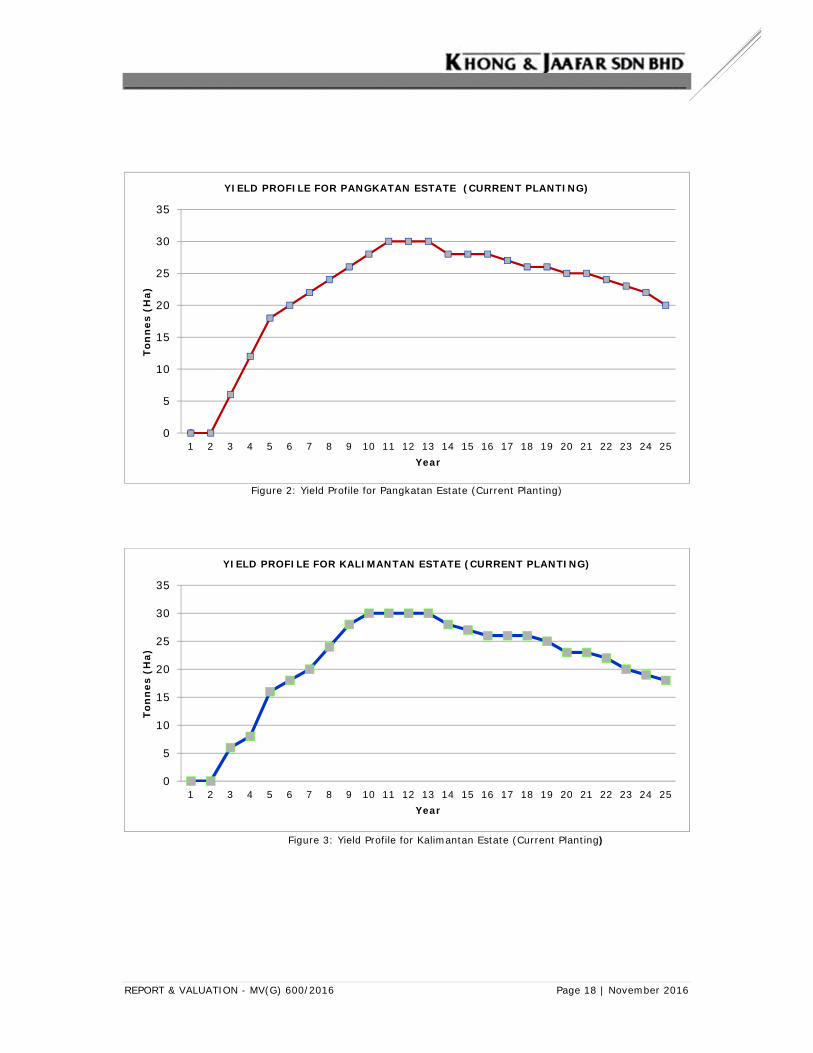

Figure 2: Yield Profile for Pangkatan Estate (Current Planting)

Figure 3: Yield Profile for Kalimantan Estate (Current Planting)

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Ton

nes

(H

a)

Year

YIELD PROFILE FOR KALIMANTAN ESTATE (CURRENT PLANTING)

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Ton

nes

(H

a)

Year

YIELD PROFILE FOR PANGKATAN ESTATE (CURRENT PLANTING)

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 19 | November 2016

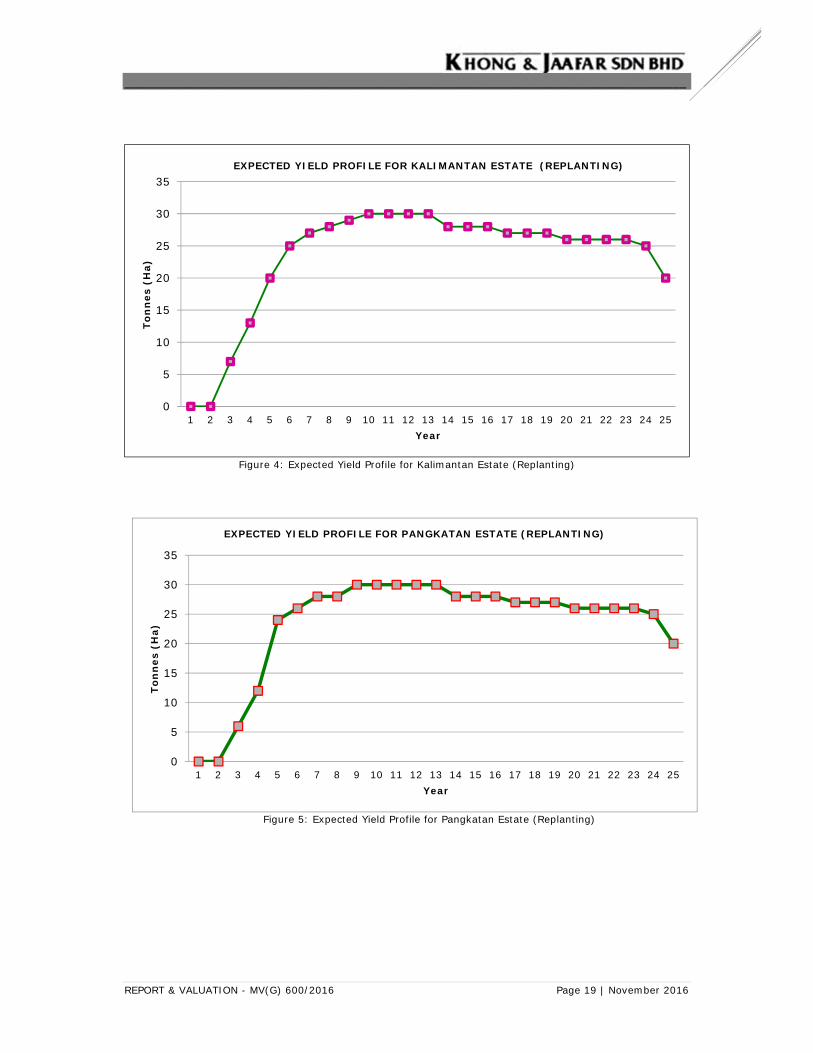

Figure 4: Expected Yield Profile for Kalimantan Estate (Replanting)

Figure 5: Expected Yield Profile for Pangkatan Estate (Replanting)

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Ton

nes

(H

a)

Year

EXPECTED YIELD PROFILE FOR KALIMANTAN ESTATE (REPLANTING)

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Ton

nes

(H

a)

Year

EXPECTED YIELD PROFILE FOR PANGKATAN ESTATE (REPLANTING)

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 20 | November 2016

The yields in the estates of MPE do reflect higher and consistent yields than normally encountered and we do attribute this to the fact that management is exceptionally at a high level and we have also noted during our inspections that operating costs are kept as low as possible. This results in a higher cash flow for the estates which in turn has an impact on values.

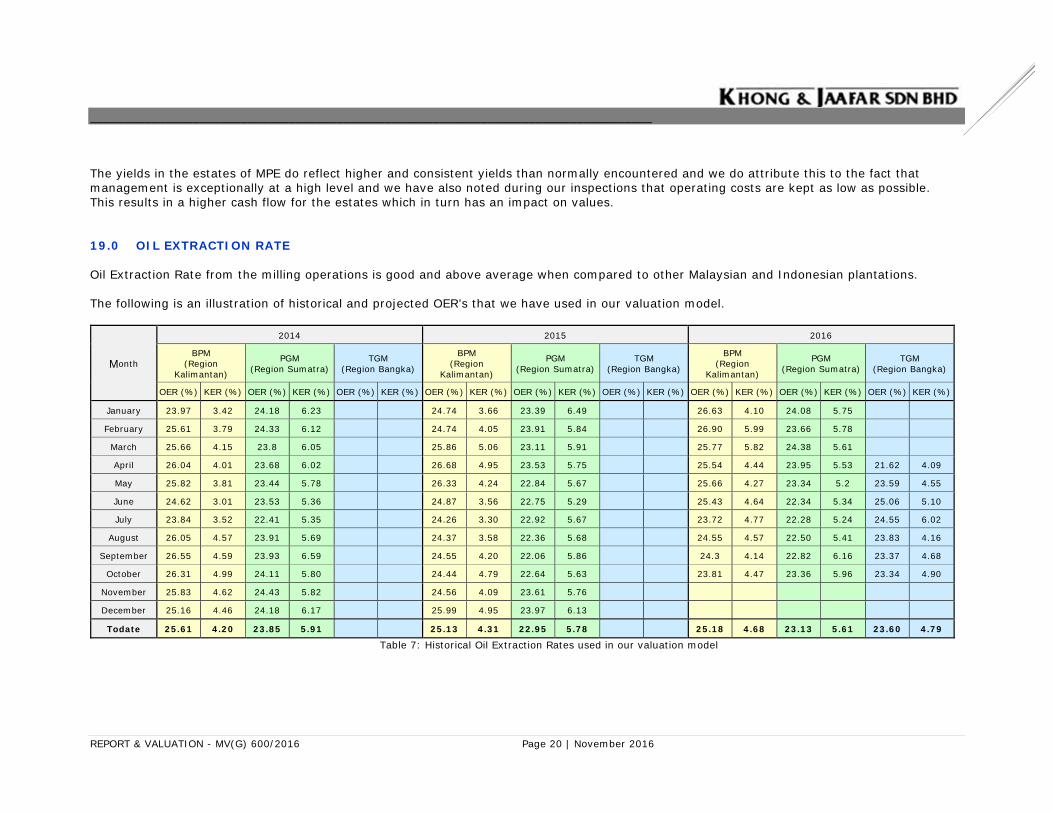

19.0 OIL EXTRACTION RATE Oil Extraction Rate from the milling operations is good and above average when compared to other Malaysian and Indonesian plantations. The following is an illustration of historical and projected OER’s that we have used in our valuation model.

Month

2014 2015 2016

BPM (Region

Kalimantan) PGM

(Region Sumatra)TGM

(Region Bangka)

BPM (Region

Kalimantan)

PGM (Region Sumatra)

TGM (Region Bangka)

BPM (Region

Kalimantan)

PGM (Region Sumatra)

TGM (Region Bangka)

OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%) OER (%) KER (%)

January 23.97 3.42 24.18 6.23 24.74 3.66 23.39 6.49 26.63 4.10 24.08 5.75

February 25.61 3.79 24.33 6.12 24.74 4.05 23.91 5.84 26.90 5.99 23.66 5.78

March 25.66 4.15 23.8 6.05 25.86 5.06 23.11 5.91 25.77 5.82 24.38 5.61

April 26.04 4.01 23.68 6.02 26.68 4.95 23.53 5.75 25.54 4.44 23.95 5.53 21.62 4.09

May 25.82 3.81 23.44 5.78 26.33 4.24 22.84 5.67 25.66 4.27 23.34 5.2 23.59 4.55

June 24.62 3.01 23.53 5.36 24.87 3.56 22.75 5.29 25.43 4.64 22.34 5.34 25.06 5.10

July 23.84 3.52 22.41 5.35 24.26 3.30 22.92 5.67 23.72 4.77 22.28 5.24 24.55 6.02

August 26.05 4.57 23.91 5.69 24.37 3.58 22.36 5.68 24.55 4.57 22.50 5.41 23.83 4.16

September 26.55 4.59 23.93 6.59 24.55 4.20 22.06 5.86 24.3 4.14 22.82 6.16 23.37 4.68

October 26.31 4.99 24.11 5.80 24.44 4.79 22.64 5.63 23.81 4.47 23.36 5.96 23.34 4.90

November 25.83 4.62 24.43 5.82 24.56 4.09 23.61 5.76

December 25.16 4.46 24.18 6.17 25.99 4.95 23.97 6.13

Todate 25.61 4.20 23.85 5.91 25.13 4.31 22.95 5.78 25.18 4.68 23.13 5.61 23.60 4.79

Table 7: Historical Oil Extraction Rates used in our valuation model

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 21 | November 2016

YEAR 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

PANGKATAN MILL (SUMATRA)

OER

(%) 0 0 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8 23.8

KER

(%) 0 0 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6 6

BUMI PERMAI MILL (KALIMANTAN)

OER

(%) 0 0 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25 25

KER

(%) 0 0 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5 5

TENGKALAT MILL (BANGKA)

OER

(%) 0 0 24 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5 24.5

KER

(%) 0 0 5.5 5.5 5.5 5.6 5.7 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8 5.8

Table 8: Projected Oil Extraction Rates used in our valuation model

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 22 | November 2016

20.0 PLASMA

The Government of Indonesia remains committed to increase the income of farmers and to ensure that the villagers whose lands are to be used by the plantation companies are not deprived of their livelihood and can take part in the progress of the development of plantations. The Indonesian Ministry of Agriculture Regulation, has made it mandatory from 2007 for new plantation developments to set aside at least 20% of its net cultivated area for plasma plantations. Generally known as the Nucleus-Plasma Scheme, this scheme is essentially made up of the plantation companies known as the “Inti” (nucleus) and a cooperative representing the smallholders/villagers known as the “Plasma”. Principally, in the Nucleus-Plasma Scheme, the Inti assists the plasma farmers to a predetermined physical condition, at which time, the plasma plantation is ready to be transferred to the plasma farmers.

Presently, in the main, the plasma scheme widely implemented is the Koperasi Kredit Primer Anggota or Primary Credit for Cooperative Members (KKPA) because the productivity of the plasma plantations can be maintained.

Under the KKPA, the villagers/smallholders are united under cooperatives and the Inti will assist the plasma farmers by undertaking the task of managing and cultivating the plasma areas on behalf of the cooperative. The Inti will also bear the initial planting cost (which will be reimbursed by the cooperatives) and secure the funding from banks for the cooperatives to cover the operating cost.

In return, the cooperatives generally agree to sell all their produce (the FFB) to the mills within the plantation companies. The selling price of the FFB is based on a specific formula known as the “K” Index which is set by the Government and varies from province to province. The “K” Index uses a fixed oil extraction rate and palm kernel extraction rate to arrive at the selling price of the FFB. The plantation companies can derive a profit as their mills are more efficient and can extract at a higher extraction rate and when the plantation companies themselves ensure that the quality of the fruits are high on account of their management, the plantation companies also secure a benefit of higher throughputs to the mills which helps to lower their overall mill cost.

Plasma areas can either be well managed by the plantation companies and be of substantial benefit to the plantation or on the other hand if they are not well managed, it may cause problems when the villagers do not derive benefits as a result of the scheme.

From our observation, in our site visits of all the estates, MPE has managed the plasma areas extraordinarily well and this brings added financial benefits which we have computed using a similar income approach i.e. the discounted cash flow methodology for the net incomes from the plasma areas. However on account on what we judge to be a higher risk, to the operations in the plasma areas, we have used a pre-tax discount rate of 19% as against the 16% we used for the Inti areas of the plantation. For the MPE there are only three areas, areas post to 2007 where these plasma areas exist and they are in the Kalimantan Estate, the Bangka Estate and the Musi Rawas Estate.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 23 | November 2016

21.0 VALUATION All the plantation assets of MPE are valued principally by the Income Approach to Value (Discounted Cash Flow Methodology). This approach to value recognises the ongoing nature of the plantation and is carried out on a field by field basis for each of the estates. Khong & Jaafar has, over the years, developed, internally, a valuation model specifically designed to value oil palm plantations. This model is used not just to value plantations but it is also used to analyse oil palm market transactions as they happen. The use of the model for valuations and analyses of market sales makes the model a market calibrated model. Significantly it enables Khong & Jaafar, when undertaking market value estimates to adhere to the overaching principle in the RICS Red Book and the International Valuation Standards that market values (as opposed to investment value estimates) can only be derived from market derived inputs, in a valuation model. The Khong & Jaafar model adheres to this tenet strictly. The model is a 30-year model (exhausting fully the present value of future cash flows), and accommodates incomes for the current plantings up to the oil palms reaching 25 years of age, replanting with better yielding clones in the following three years, a market derived yield profile, a sustainable long term crude oil palm price of USD595, production, milling and replanting costs based on current market costs and a pre-tax discount rate of 16 percent per annum to reflect risks. The model does not incorporate inflation or growth in the input or output values and is based on current prices and costs to give current values. The market derived pre-tax discount rate can be obtained from analysis of market sales in the past where the actual market sale is matched against estimated or actual net incomes from the plantation. Generally Malaysian plantations in the past have had market derived pre-tax discount rates of 14 to 15 percent but this has now compressed in recent times to between 12 to 13 percent. Indonesian plantations, because of the higher risks principally in land ownership have always been benchmarked between 3 to 5 percent more than the Malaysian rate. Again in recent times, the range has narrowed and based upon analysis of valuations and sales that we have generally analyse we believe that a proper pre-tax discount rate for Indonesian plantations is in the order of 16 percent as used in our valuation model. For the valuation of the Malaysian real estate interests, because all the various parcels are essentially development lands with inherent development potentials values obtainable in the market over and above any pure agricultural values, and because there are sufficient, recent market sales, the Comparison Approach to Value is preferred and is adequately reliable. For the mills within the oil palm plantations, as well as the bulking installation and the crumb rubber factory we have used the Cost Method of Valuation, where firstly the current estimated replacement cost new of the facility is estimated and from that the observed physical deterioration and functional and economic obsolescence is deducted. Physical deterioration results from wear and tear over time and the lack of necessary maintenance. Functional (or technological) obsolescence results from advances in technology that creates new plant/machinery capable of more efficient delivery of goods and services. Economic (or external) obsolescence results from external influences such as demand, shrinkage in supply of raw material and labour, legislation affecting tax and duties, environmental or zoning controls that affect the value of the plant and machinery.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 24 | November 2016

22.0 ROLLING VALUES On account of the fact that the Indonesian estates of MPE are in different stages of development, with for example the estates in Northern Sumatra being second and third generation estates while those in Kalimantan and South Sumatra and Bangka being first generation plantation in their early stage of development, we consider it appropriate to have rolling values of the estates on the supposition that the facts are the same but the dates of the values are advanced one to five years from 2016. This will allow the values of the estates to better reflect their potentials in the next five years. The figures are as follows:-

Property Current Value (USD)

Value One Year From

2016 (USD)

Value Two Years From 2016 (USD)

Value Three Years From 2016 (USD)

Value Four Years From 2016 (USD)

Value Five Years From 2016 (USD)

Value Of Estates (including mills & etc.) 826,950,000 832,020,000 906,020,000 946,200,000 979,710,000 1,019,900,000

Value Of Estates + Bertam 978,190,000 983,260,000 1,057,260,000 1,097,440,000 1,130,950,000 1,171,140,000

MPE Attributable Value 665,433,616 677,980,876 738,558,992 768,736,904 792,845,844 823,560,220

Table 9: Rolling Values

23.0 COMPARISON APPROACH TO VALUE We have counterchecked our valuation by the Income Approach to Value discussed above, with the Comparison Approach to Value, which entails making comparisons between market sales of other known sizable, oil palm plantations in the region with the subject plantation.

Whilst the Income Approach to Value, and by way of the market calibrated model we have adopted is explicit in nature, the Comparison Approach can also be reduced to a model but that model will have to identify all the dissimilarities between each of the market sales of the comparable plantations and make adjustments for each of those dissimilarities. When you compare plantations, this is not an easy task because of the vast legal, economic and physical factual differences from one plantation and another. Thus, the Comparison Approach when used for large sized plantations has to be done on the basis of broad ranges of value.

The comparables that have been selected are considered to be a reasonable basis for comparison to MPE due to their similarities in size, location, management and operations.

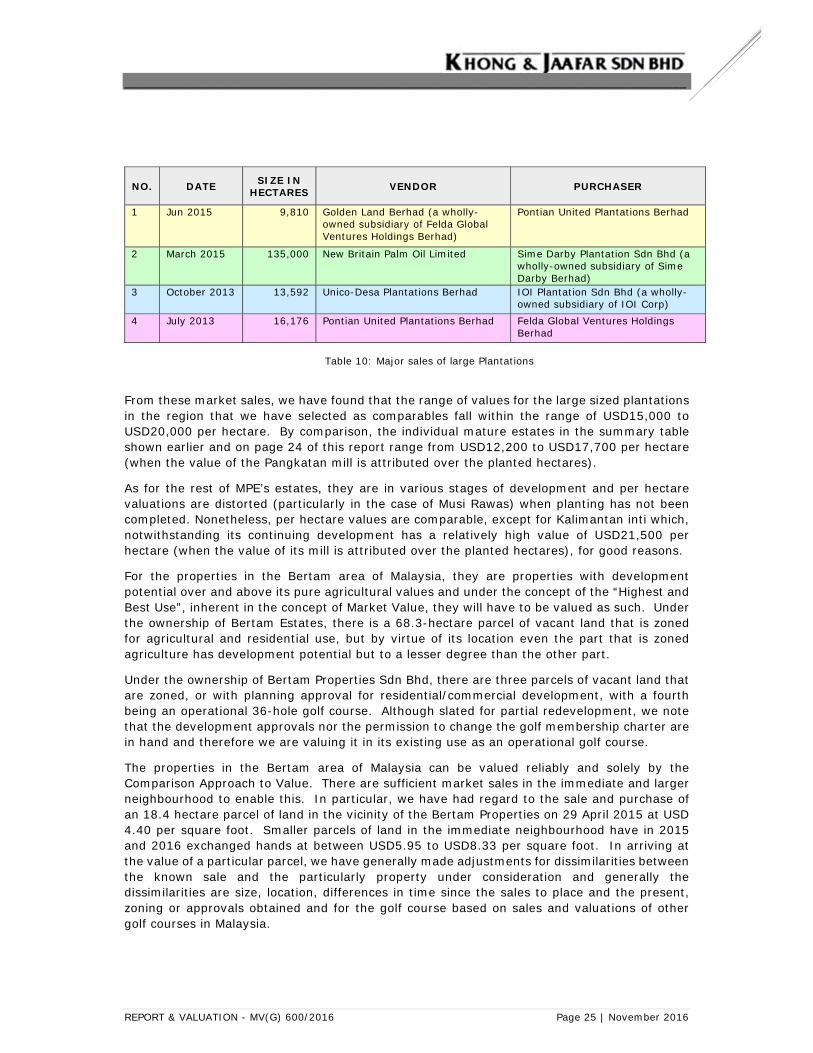

The major sales of large plantations that we have considered and in particular studied include the following:-

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 25 | November 2016

NO. DATE SIZE IN HECTARES VENDOR PURCHASER

1 Jun 2015 9,810 Golden Land Berhad (a wholly-owned subsidiary of Felda Global Ventures Holdings Berhad)

Pontian United Plantations Berhad

2 March 2015 135,000 New Britain Palm Oil Limited Sime Darby Plantation Sdn Bhd (a wholly-owned subsidiary of Sime Darby Berhad)

3 October 2013 13,592 Unico-Desa Plantations Berhad IOI Plantation Sdn Bhd (a wholly-owned subsidiary of IOI Corp)

4 July 2013 16,176 Pontian United Plantations Berhad Felda Global Ventures Holdings Berhad

Table 10: Major sales of large Plantations

From these market sales, we have found that the range of values for the large sized plantations in the region that we have selected as comparables fall within the range of USD15,000 to USD20,000 per hectare. By comparison, the individual mature estates in the summary table shown earlier and on page 24 of this report range from USD12,200 to USD17,700 per hectare (when the value of the Pangkatan mill is attributed over the planted hectares).

As for the rest of MPE’s estates, they are in various stages of development and per hectare valuations are distorted (particularly in the case of Musi Rawas) when planting has not been completed. Nonetheless, per hectare values are comparable, except for Kalimantan inti which, notwithstanding its continuing development has a relatively high value of USD21,500 per hectare (when the value of its mill is attributed over the planted hectares), for good reasons.

For the properties in the Bertam area of Malaysia, they are properties with development potential over and above its pure agricultural values and under the concept of the “Highest and Best Use”, inherent in the concept of Market Value, they will have to be valued as such. Under the ownership of Bertam Estates, there is a 68.3-hectare parcel of vacant land that is zoned for agricultural and residential use, but by virtue of its location even the part that is zoned agriculture has development potential but to a lesser degree than the other part.

Under the ownership of Bertam Properties Sdn Bhd, there are three parcels of vacant land that are zoned, or with planning approval for residential/commercial development, with a fourth being an operational 36-hole golf course. Although slated for partial redevelopment, we note that the development approvals nor the permission to change the golf membership charter are in hand and therefore we are valuing it in its existing use as an operational golf course.

The properties in the Bertam area of Malaysia can be valued reliably and solely by the Comparison Approach to Value. There are sufficient market sales in the immediate and larger neighbourhood to enable this. In particular, we have had regard to the sale and purchase of an 18.4 hectare parcel of land in the vicinity of the Bertam Properties on 29 April 2015 at USD 4.40 per square foot. Smaller parcels of land in the immediate neighbourhood have in 2015 and 2016 exchanged hands at between USD5.95 to USD8.33 per square foot. In arriving at the value of a particular parcel, we have generally made adjustments for dissimilarities between the known sale and the particularly property under consideration and generally the dissimilarities are size, location, differences in time since the sales to place and the present, zoning or approvals obtained and for the golf course based on sales and valuations of other golf courses in Malaysia.

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 26 | November 2016

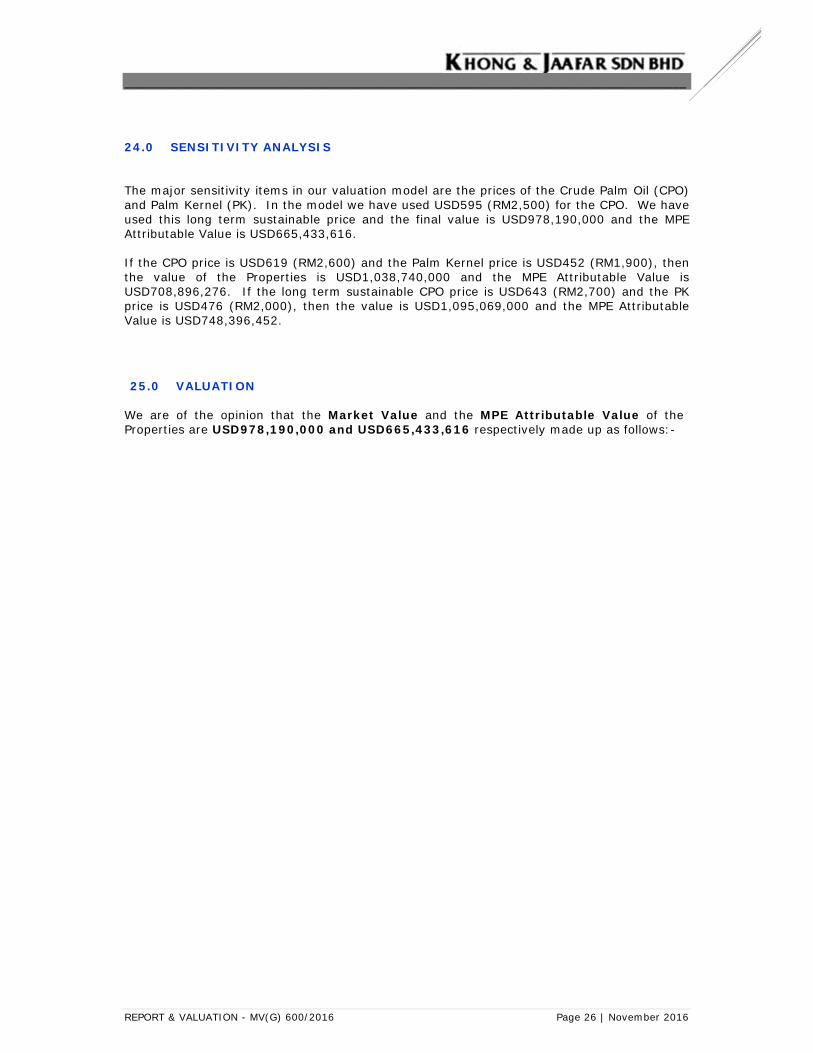

24.0 SENSITIVITY ANALYSIS

The major sensitivity items in our valuation model are the prices of the Crude Palm Oil (CPO) and Palm Kernel (PK). In the model we have used USD595 (RM2,500) for the CPO. We have used this long term sustainable price and the final value is USD978,190,000 and the MPE Attributable Value is USD665,433,616. If the CPO price is USD619 (RM2,600) and the Palm Kernel price is USD452 (RM1,900), then the value of the Properties is USD1,038,740,000 and the MPE Attributable Value is USD708,896,276. If the long term sustainable CPO price is USD643 (RM2,700) and the PK price is USD476 (RM2,000), then the value is USD1,095,069,000 and the MPE Attributable Value is USD748,396,452.

25.0 VALUATION We are of the opinion that the Market Value and the MPE Attributable Value of the Properties are USD978,190,000 and USD665,433,616 respectively made up as follows:-

__________________________________________________________________________________

REPORT & VALUATION - MV(G) 600/2016 Page 27 | November 2016

__________________________________________________________________________________

This page has been left intentionally blank