Independent Investment Solutions - My Dealer...

32

Transcript of Independent Investment Solutions - My Dealer...

AssureInvest Copyright, Disclaimer, General Advice Warning and Disclosure

Copyright

Copyright AssureInvest Pty Ltd ABN 55 636 036 188 (AssureInvest). All rights reserved. No part of this publication may be reproduced or distributed in any form without

prior consent in writing from AssureInvest.

Disclaimer

AssureInvest has taken all care in preparing this presentation and the data, information and research commentary within it (together referred to as the 'publication')

but to the extent that the publication is based on information received from other parties no liability is accepted by AssureInvest for errors contained in the publication

or omissions from the publication. AssureInvest gives neither guarantee nor warranty nor makes any representation as to the correctness or completeness of the

publication. AssureInvest bases its data, information and research commentary on information disclosed to it by other parties. No information contained in the

publication constitutes the provision of securities advice. AssureInvest warns that: (a) in preparing the publication, AssureInvest did not take into account the

particular goals and objectives, anticipated resources, current situation or attitudes of any particular person; and (b) before making any investment decisions on the

basis of that publication, any investor or prospective investor needs to consider, with or without the assistance of a securities adviser, whether the information

contained within the publication is appropriate in light of the particular goals and objectives, anticipated resources, current situation or attitudes of the investor or

prospective investor. Past performance is no guarantee of future performance.

General Advice Warning

The information contained within this publication is of a general nature only. It does not take your specific needs or circumstances into consideration. You should look

at your own personal situation and requirements before making any financial decisions.

Disclosure

AssureInvest has no debt or equity relationship with any funds management or financial advisory group. AssureInvest may have an interest in the securities referred to

in the publication in that AssureInvest and/or its staff may hold or intend to hold deposits, shares, units or other rights in respect of such products and from time to time

AssureInvest may provide some of the investment product providers mentioned in the publication with research, consulting and other services for a fee.

AssureInvest Pty Ltd

Authorised Representative (number 460115) of Libertas Financial Planning (ABN 27 160 419 134, AFSL number 429718)

2

Agenda

• Our compelling offer to you

• Investment philosophy

• Our approach to asset allocation and equities portfolio management

• Market outlook and portfolio positioning

• Summary, questions and discussion

3

Andrew Doherty

Qualifications

• Master of Business Administration, AGSM, 1999-2004

• Master of Economics, Macquarie University, 1992-1993

• Bachelor of Economics, Macquarie University, 1986-1990

• HSC, Knox Grammar School Sydney, 1980-1985

Career Summary

• Morningstar - Head of Equities, July 2006-December 2013

• Aspect Huntley - Research Manager, 1999-2006

• Deutsche MG, London - Equity Derivatives Risk, 1997-1998

• JP Morgan, London - Fixed Income, 1996-1997

• Credit Suisse AM – Fixed Interest Investment Manager, 1994-1995

AssureInvest Mission

To provide independent, specialist

guidance to advisory firms and high net

worth individuals to help them achieve

their financial goals.

We form alliances with our clients

through objective, customised

investment and business solutions.

4

Equity portfolio outperformance versus market and peers

5

0.7

4.2

7.4

0.6

3.5

6.5

0

1

2

3

4

5

6

7

8

1 month 3 months Since Inception (Feb 14)

Returns to August 2014

AssureInvest Australian Equity S&P/ASX 200

%

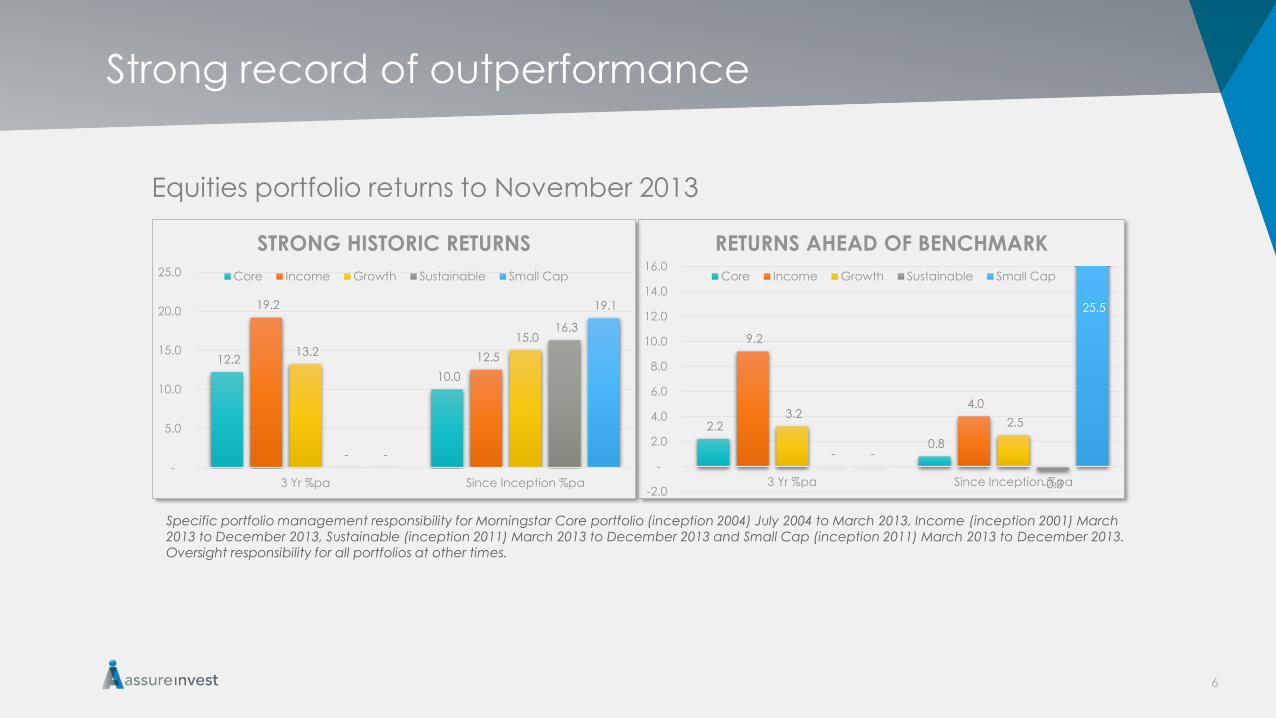

Strong record of outperformance

Equities portfolio returns to November 2013

6

Specific portfolio management responsibility for Morningstar Core portfolio (inception 2004) July 2004 to March 2013, Income (inception 2001) March

2013 to December 2013, Sustainable (inception 2011) March 2013 to December 2013 and Small Cap (inception 2011) March 2013 to December 2013.

Oversight responsibility for all portfolios at other times.

12.2

10.0

19.2

12.5 13.2 15.0

-

16.3

-

19.1

-

5.0

10.0

15.0

20.0

25.0

3 Yr %pa Since Inception %pa

STRONG HISTORIC RETURNS

Core Income Growth Sustainable Small Cap

2.2

0.8

9.2

4.0 3.2

2.5

-

-0.3

-

25.5

-2.0

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

3 Yr %pa Since Inception %pa

RETURNS AHEAD OF BENCHMARK

Core Income Growth Sustainable Small Cap

Our compelling offer to you

• We collaborate with our clients to maximise their

business potential

• Experience, record of outperformance

• Exclusivity – we advise a strictly limited number of

highly valued clients

• Independence - trust, integrity, passion, transparency

• Variety of service options

• Investment consulting (governance, portfolio construction)

• Model portfolios

• Managed account portfolio licensing

• Client portfolio review

7

Investment Philosophy

8

Capital Preservation &

Superior Returns

• Long-term focus on fundamental high-quality and value

• Competitively advantaged firms preferred for investment of capital at high rates of return

• Allowing margin of safety increases potential gains while reducing chance of capital loss

• Suitable diversification across assets and sectors reduces risk

• Macroeconomic overlay helps maximise portfolio returns and reduce risk

• Cost focus through direct securities, low turnover and tax management

• Investment success requires patience and discipline to reduce the risk of permanent capital loss

Equities Investment Process

9

Portfolio

Fundamental Data Screens

External Research Checks

Proprietary Research

Macro Overlay

Mandates & Best Practice

Fundamental Data Screens

Return on equity

Return on Invested Capital

Free cash flow

Reliable earnings growth

Responsible Leverage

Net Debt/Equity

EBIT/Interest Cover

EV/EBITDA

Operating Leverage

Valuation Methods

Price/Book

Price/Earnings

Price/Earnings Growth

Free Cash Flow Yield

Dividend Yield

EBIT/Enterprise Value

(EPS Growth + Yield)/PE

Margin of Safety

Measure Mandate

Objective Outperform

S&P/ASX 200

Accumulation

Index over long

term

Investment

Universe

S&P/ASX 200

Strategy Best S&P/ASX

200 high quality

opportunities,

concentrated

Number

stocks held

15 – 30

Maximum

position

weight

20%

Maximum

cash

weight

10%

Derivatives Not used

The importance of sustainable competitive advantage

• Companies able to invest capital at high

rates of return will create value over time

• Firms with sustainable competitive advantages

have unique assets or skills

• They will have strong industry positions in relation to

barriers to entry, rivalry, strength of consumers,

power of suppliers and degree of substitution

• Predictability of cash flows affects the ability

to reliably assess value

• Business risk is determined by revenue cyclicality,

operating leverage, balance sheet strength and

risk of unforeseen events

10

Sources of competitive advantage

11

Cost Advantage

Differentiation Advantage

Switching Costs

Network Effect

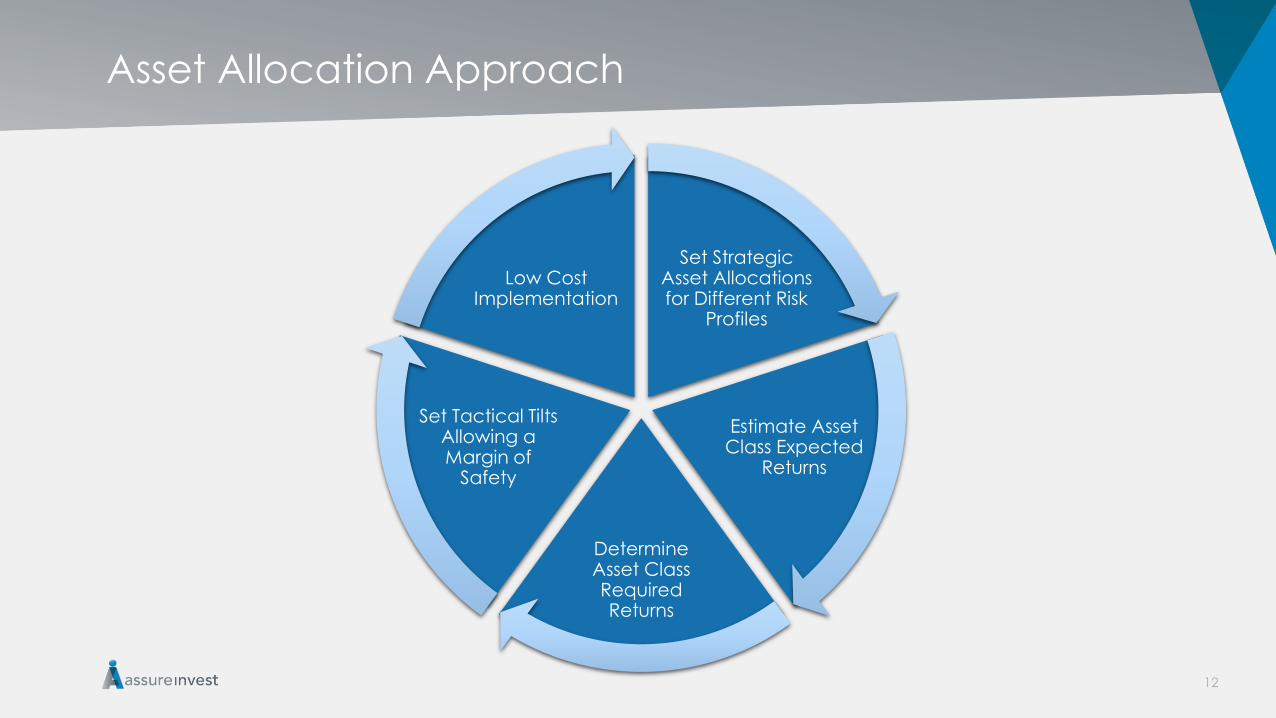

Asset Allocation Approach

Set Strategic Asset Allocations for Different Risk

Profiles

Estimate Asset Class Expected

Returns

Determine Asset Class Required Returns

Set Tactical TiltsAllowing a Margin of

Safety

Low Cost Implementation

12

15%

30%

50%

70%

85%

85%

70%

50%

30%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Defensive Moderately Defensive Balanced Moderate Growth High Growth

Strategic Asset Allocation - Asset Style by Portfolio

Growth Income

Various strategic asset allocations according to investor goals

13

10%

20%

30%

40%

55%

0%

5%

10%

10%

5%

3%

3%

6%

13%

16%

1.4%

1.4%

2.9%

5.7%

7.2%

0%

0%

1%

2%

2%

55%

45%

30%

15%

5%30%

25%20%

15%10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Defensive Moderately Defensive Balanced Moderate Growth High Growth

Australian Equities Australian REITs US Equities Europe Equities Japan Equities Australian Bonds Australian Cash

Strategic Asset Allocation - Assets Weights by Portfolio

14

Tactical Tilts away from European Equities and Bonds

15

0% 0% 0%

-1%

0%

-6%

7%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Australian Equities Australian REITs US Equities Europe Equities Japan Equities Australian Bonds Australian Cash

Variance from benchmark asset allocations for Moderate Growth Portfolio

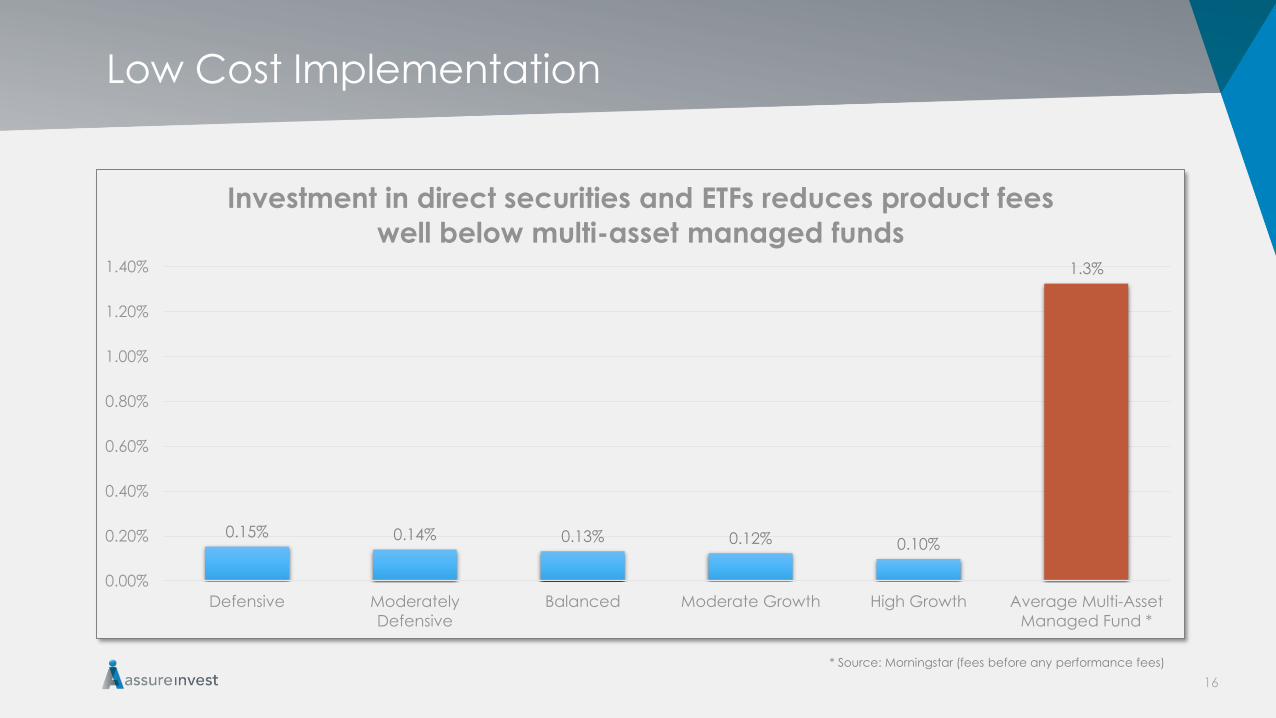

Low Cost Implementation

16

0.15% 0.14% 0.13% 0.12% 0.10%

1.3%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

Defensive Moderately

Defensive

Balanced Moderate Growth High Growth Average Multi-Asset

Managed Fund *

Investment in direct securities and ETFs reduces product fees

well below multi-asset managed funds

* Source: Morningstar (fees before any performance fees)

Moderate Growth Portfolio - Implementation Example

17

10%

5%

4%

13%

5%

2%

22%

40%

Vanguard Australian Prop Secs Index ETF (VAP) iShares UBS Composite Bond ETF

AGB 2.75% 21/4/2024 iShares Core S&P 500

iShares Europe ETF iShares MSCI Japan ETF

BetaShares Aus High Interest Cash ETF (AAA) AssureInvest Australian Equities Portfolio

Investment outlook

18

US Fed Balance Sheet has Expanded by USD 3.3 Tr Since 2008Fed Funds Rate at Historic Lows

19

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2002 -12 - 1 8 2004 -12 - 1 8 2006 -12 - 1 8 2008 -12 - 1 8 2010 -12 - 1 8 2012 -12 - 1 8

US FED BALANCE SHEET (USD TR)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2002 -07 - 0 1 2004 -08 - 0 1 2006 -09 - 0 1 2008 -10 - 0 1 2010 -11 - 0 1 2012 -12 - 0 1

%

US FED FUNDS RATE

Source: FRED

US Economy No Longer Weak…Supporting Fed Funds Rise Mid-2015

20

Avg Since Jan

1993= 4.6 %

-15.0

-10.0

-5.0

-

5.0

10.0

15.0

Ja

n-1

99

3

Se

p-1

99

3

Ma

y-1

99

4

Ja

n-1

99

5

Se

p-1

99

5

Ma

y-1

99

6

Ja

n-1

99

7

Se

p-1

99

7

Ma

y-1

99

8

Ja

n-1

99

9

Se

p-1

99

9

Ma

y-2

00

0

Ja

n-2

00

1

Se

p-2

00

1

Ma

y-2

00

2

Ja

n-2

00

3

Se

p-2

00

3

Ma

y-2

00

4

Ja

n-2

00

5

Se

p-2

00

5

Ma

y-2

00

6

Ja

n-2

00

7

Se

p-2

00

7

Ma

y-2

00

8

Ja

n-2

00

9

Se

p-2

00

9

Ma

y-2

01

0

Ja

n-2

01

1

Se

p-2

01

1

Ma

y-2

01

2

Ja

n-2

01

3

Se

p-2

01

3

Ma

y-2

01

4

US Retail Sales Growth Near Long Term Average

Long Term Avg:

85.1

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0

197

8-0

1-0

1

197

9-0

5-0

1

198

0-0

9-0

1

198

2-0

1-0

1

198

3-0

5-0

1

198

4-0

9-0

1

198

6-0

1-0

1

198

7-0

5-0

1

198

8-0

9-0

1

199

0-0

1-0

1

199

1-0

5-0

1

199

2-0

9-0

1

199

4-0

1-0

1

199

5-0

5-0

1

199

6-0

9-0

1

199

8-0

1-0

1

199

9-0

5-0

1

200

0-0

9-0

1

200

2-0

1-0

1

200

3-0

5-0

1

200

4-0

9-0

1

200

6-0

1-0

1

200

7-0

5-0

1

200

8-0

9-0

1

201

0-0

1-0

1

201

1-0

5-0

1

201

2-0

9-0

1

University Michigan Consumer Confidence Now

Around Long Term Average

Average since

1967: 80.6

65.0

70.0

75.0

80.0

85.0

90.0

196

7-0

1-0

1

196

8-1

0-0

1

197

0-0

7-0

1

197

2-0

4-0

1

197

4-0

1-0

1

197

5-1

0-0

1

197

7-0

7-0

1

197

9-0

4-0

1

198

1-0

1-0

1

198

2-1

0-0

1

198

4-0

7-0

1

198

6-0

4-0

1

198

8-0

1-0

1

198

9-1

0-0

1

199

1-0

7-0

1

199

3-0

4-0

1

199

5-0

1-0

1

199

6-1

0-0

1

199

8-0

7-0

1

200

0-0

4-0

1

200

2-0

1-0

1

200

3-1

0-0

1

200

5-0

7-0

1

200

7-0

4-0

1

200

9-0

1-0

1

201

0-1

0-0

1

201

2-0

7-0

1

201

4-0

4-0

1

US Capacity Utilisation @ LT average

LT Avg 2.9%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

195

7-0

1-0

1

195

9-0

2-0

1

196

1-0

3-0

1

196

3-0

4-0

1

196

5-0

5-0

1

196

7-0

6-0

1

196

9-0

7-0

1

197

1-0

8-0

1

197

3-0

9-0

1

197

5-1

0-0

1

197

7-1

1-0

1

197

9-1

2-0

1

198

2-0

1-0

1

198

4-0

2-0

1

198

6-0

3-0

1

198

8-0

4-0

1

199

0-0

5-0

1

199

2-0

6-0

1

199

4-0

7-0

1

199

6-0

8-0

1

199

8-0

9-0

1

200

0-1

0-0

1

200

2-1

1-0

1

200

4-1

2-0

1

200

7-0

1-0

1

200

9-0

2-0

1

201

1-0

3-0

1

201

3-0

4-0

1

US Industrial Prod’n (YoY Chg%) modest, steady and near LT Avg

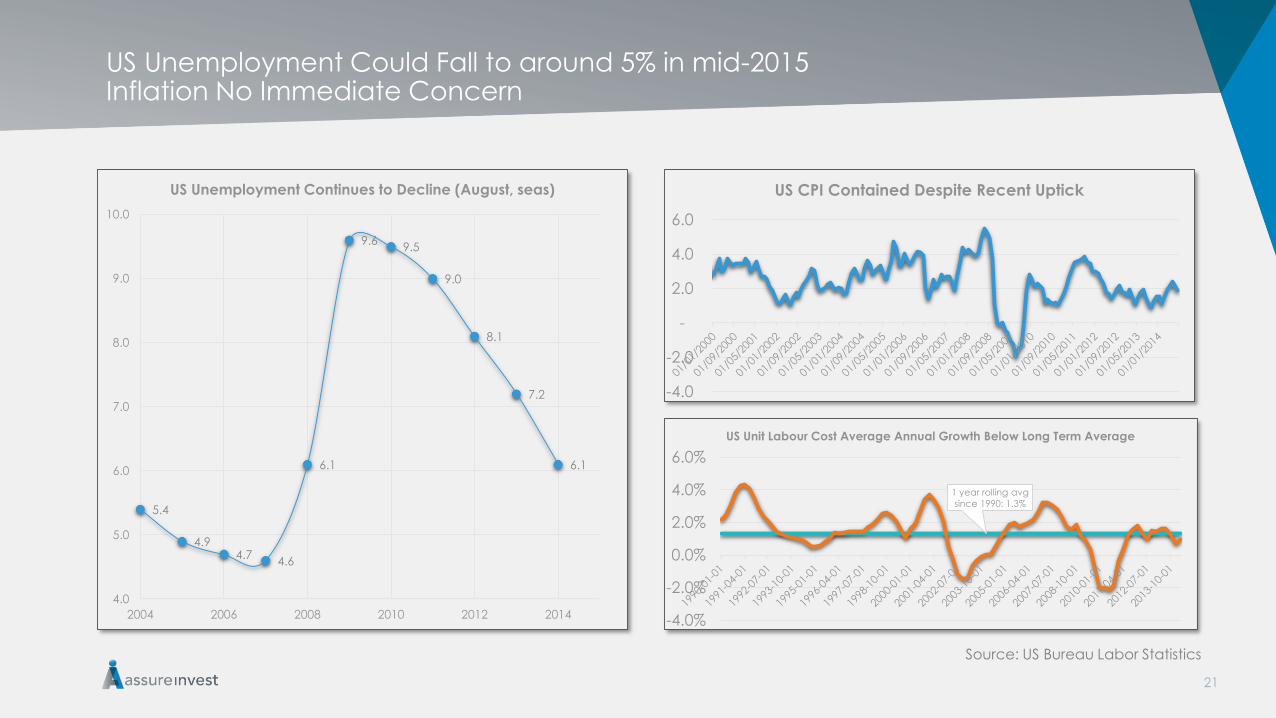

US Unemployment Could Fall to around 5% in mid-2015Inflation No Immediate Concern

21

1 year rolling avg

since 1990: 1.3%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

US Unit Labour Cost Average Annual Growth Below Long Term Average

5.4

4.94.7

4.6

6.1

9.69.5

9.0

8.1

7.2

6.1

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2004 2006 2008 2010 2012 2014

US Unemployment Continues to Decline (August, seas)

-4.0

-2.0

-

2.0

4.0

6.0

US CPI Contained Despite Recent Uptick

Source: US Bureau Labor Statistics

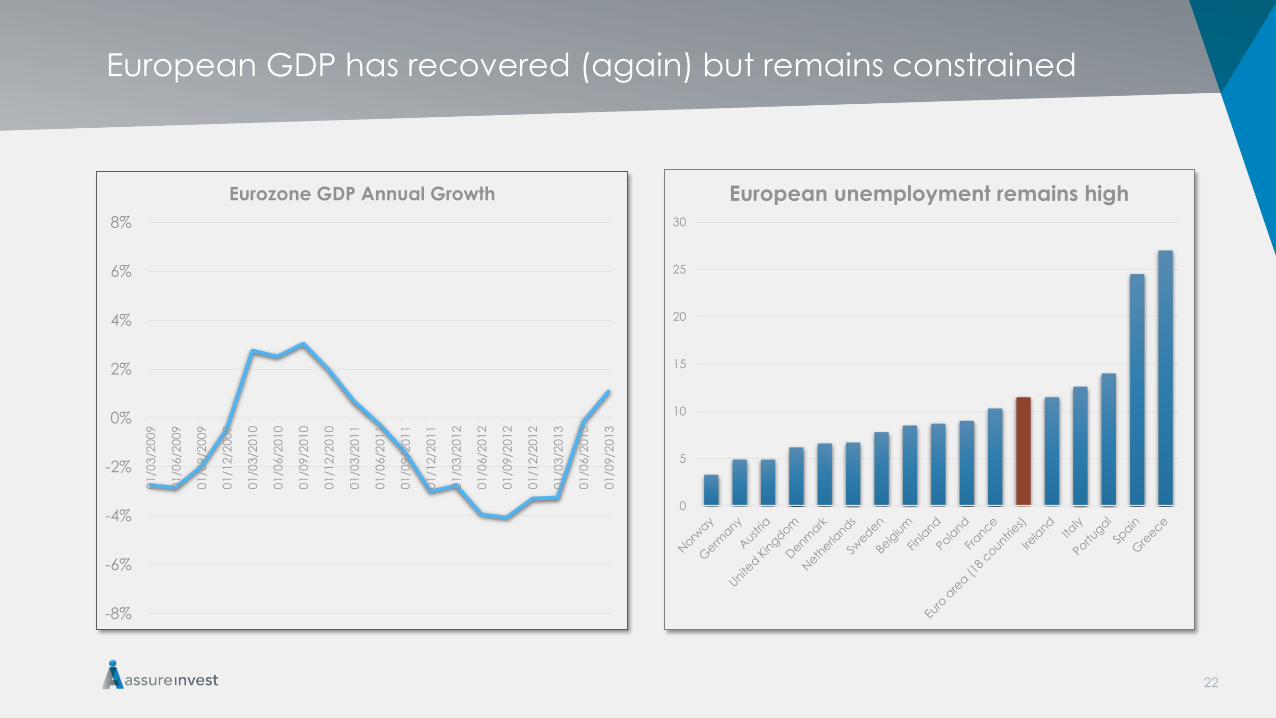

European GDP has recovered (again) but remains constrained

22

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01/0

3/2

00

9

01/0

6/2

00

9

01/0

9/2

00

9

01/1

2/2

00

9

01/0

3/2

01

0

01/0

6/2

01

0

01/0

9/2

01

0

01/1

2/2

01

0

01/0

3/2

01

1

01/0

6/2

01

1

01/0

9/2

01

1

01/1

2/2

01

1

01/0

3/2

01

2

01/0

6/2

01

2

01/0

9/2

01

2

01/1

2/2

01

2

01/0

3/2

01

3

01/0

6/2

01

3

01/0

9/2

01

3

Eurozone GDP Annual Growth

0

5

10

15

20

25

30

European unemployment remains high

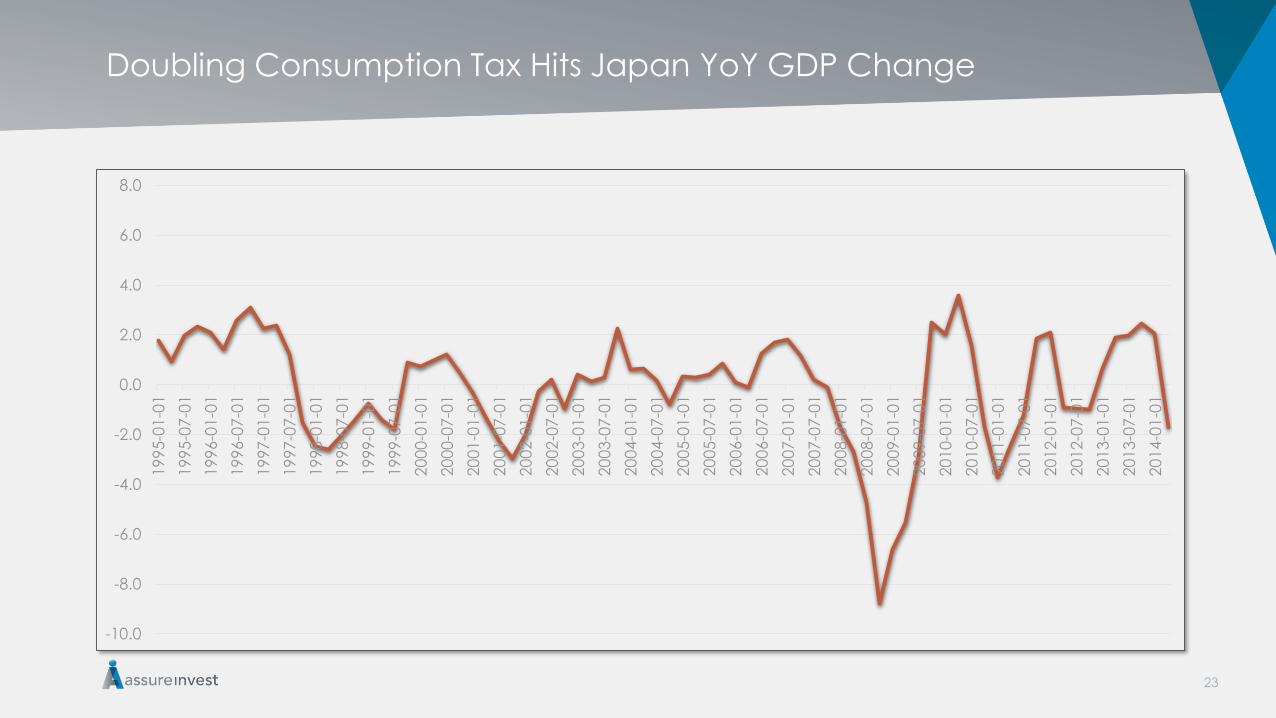

Doubling Consumption Tax Hits Japan YoY GDP Change

23

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

19

95-0

1-0

1

19

95-0

7-0

1

19

96-0

1-0

1

19

96-0

7-0

1

19

97-0

1-0

1

19

97-0

7-0

1

19

98-0

1-0

1

19

98-0

7-0

1

19

99-0

1-0

1

19

99-0

7-0

1

20

00-0

1-0

1

20

00-0

7-0

1

20

01-0

1-0

1

20

01-0

7-0

1

20

02-0

1-0

1

20

02-0

7-0

1

20

03-0

1-0

1

20

03-0

7-0

1

20

04-0

1-0

1

20

04-0

7-0

1

20

05-0

1-0

1

20

05-0

7-0

1

20

06-0

1-0

1

20

06-0

7-0

1

20

07-0

1-0

1

20

07-0

7-0

1

20

08-0

1-0

1

20

08-0

7-0

1

20

09-0

1-0

1

20

09-0

7-0

1

20

10-0

1-0

1

20

10-0

7-0

1

20

11-0

1-0

1

20

11-0

7-0

1

20

12-0

1-0

1

20

12-0

7-0

1

20

13-0

1-0

1

20

13-0

7-0

1

20

14-0

1-0

1

Australian growth modest while driver shifts from resources

24

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Ma

r-20

05

Ju

n-2

00

5

Se

p-2

00

5

De

c-2

00

5

Ma

r-20

06

Ju

n-2

00

6

Se

p-2

00

6

De

c-2

00

6

Ma

r-20

07

Ju

n-2

00

7

Se

p-2

00

7

De

c-2

00

7

Ma

r-20

08

Ju

n-2

00

8

Se

p-2

00

8

De

c-2

00

8

Ma

r-20

09

Ju

n-2

00

9

Se

p-2

00

9

De

c-2

00

9

Ma

r-20

10

Ju

n-2

01

0

Se

p-2

01

0

De

c-2

01

0

Ma

r-20

11

Ju

n-2

01

1

Se

p-2

01

1

De

c-2

01

1

Ma

r-20

12

Ju

n-2

01

2

Se

p-2

01

2

De

c-2

01

2

Ma

r-20

13

Ju

n-2

01

3

Se

p-2

01

3

De

c-2

01

3

Ma

r-20

14

Australian Annual GDP and CPI Changes

CPI GDPSource: ABS

Bond yields to normalise over a multi-year timeframe

25

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Au

g-1

99

0

Ma

r-19

91

Oc

t-19

91

Ma

y-1

992

De

c-1

99

2

Ju

l-199

3

Fe

b-1

994

Se

p-1

99

4

Ap

r-19

95

No

v-1

995

Ju

n-1

99

6

Ja

n-1

997

Au

g-1

99

7

Ma

r-19

98

Oc

t-19

98

Ma

y-1

999

De

c-1

99

9

Ju

l-200

0

Fe

b-2

001

Se

p-2

00

1

Ap

r-20

02

No

v-2

002

Ju

n-2

00

3

Ja

n-2

004

Au

g-2

00

4

Ma

r-20

05

Oc

t-20

05

Ma

y-2

006

De

c-2

00

6

Ju

l-200

7

Fe

b-2

008

Se

p-2

00

8

Ap

r-20

09

No

v-2

009

Ju

n-2

01

0

Ja

n-2

011

Au

g-2

01

1

Ma

r-20

12

Oc

t-20

12

Ma

y-2

013

De

c-2

01

3

Ju

l-201

4

Australian interest rates

RBA Cash Rate Australian 10YB

AssureInvest Australian Equities Portfolio

26

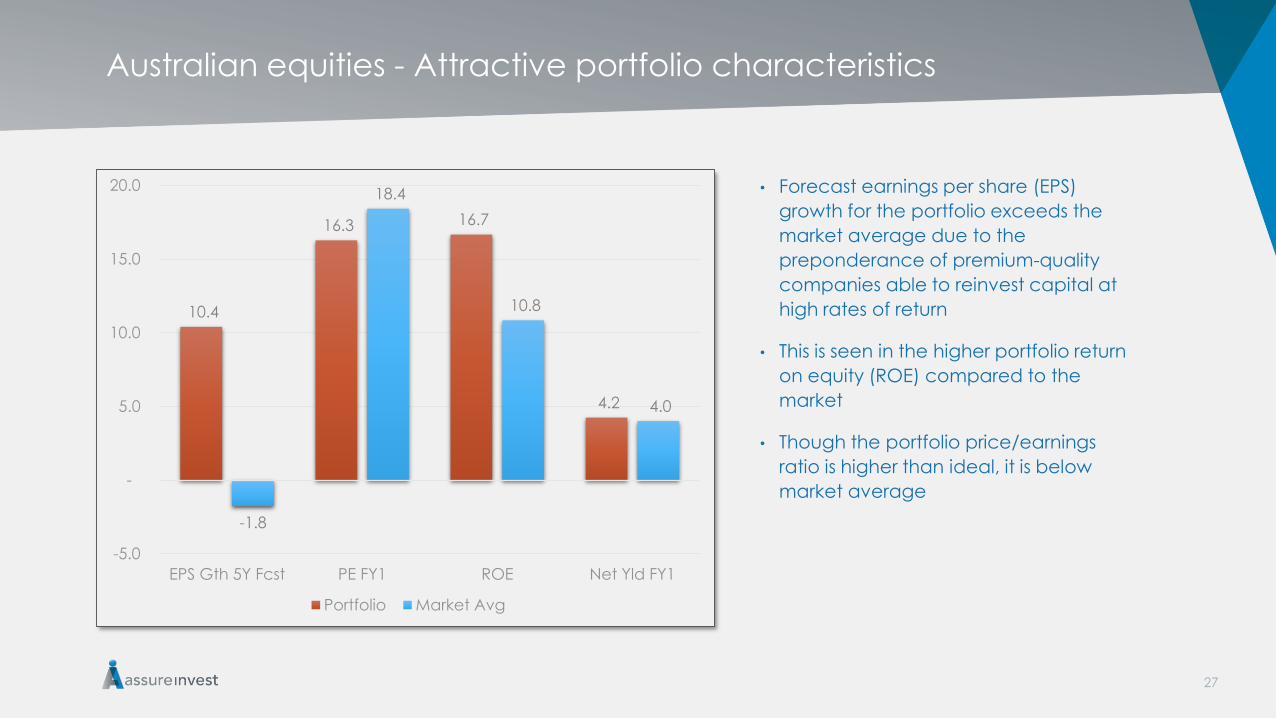

Australian equities - Attractive portfolio characteristics

• Forecast earnings per share (EPS)

growth for the portfolio exceeds the

market average due to the

preponderance of premium-quality

companies able to reinvest capital at

high rates of return

• This is seen in the higher portfolio return

on equity (ROE) compared to the

market

• Though the portfolio price/earnings

ratio is higher than ideal, it is below

market average

27

10.4

16.3 16.7

4.2

-1.8

18.4

10.8

4.0

-5.0

-

5.0

10.0

15.0

20.0

EPS Gth 5Y Fcst PE FY1 ROE Net Yld FY1

Portfolio Market Avg

Australian equities portfolio weighted to conviction sector opportunities

4%

8%6%

45%

5%7%

1%

16%

5%

2%0%

4%

8%

36%

12%

4% 3%

18%

6%

3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Sector Relative Weights

Index Wt Portfolio Wt

28

Australian equities portfolio - Top 10 holdings

ASX

code Name GICS Sector Price Weight

Mkt Cap

($, 000)

EPS Gth

5Y Fcst

PE

FY1

Net Yld

FY1 P/Book

(EPS Gth

+ Yld) /

PE Equity Style ROE

Int

Cover PEG

WBC Westpac Financials 35.22 7.80% 109,501 5.3 14.3 5.30% 2.3 0.9 Growth 15.2 na 1.9

ANZ ANZ Bank Financials 33.67 6.40% 92,815 5.3 13.3 5.30% 2.1 0.9 Growth 15 na 2.3

TLS Telstra Telecom 5.72 6.30% 71,174 3.8 17.8 5.20% 5.5 0.5 Growth 33.7 7.5 20.1

CBA Commonwealth Financials 81.70 6.00% 132,462 4.8 14.5 5.20% 2.9 0.7 Growth 18.5 na 2.2

SHL

Sonic

Healthcare Health Care 17.71 5.90% 7,098 5.9 17.2 4.10% 2.4 0.8 Income 12.8 10 1.6

BHP BHP Materials 36.20 5.40% 116,263 9.1 14.3 3.80% 2.5 0.8 Growth 19.4 18.3 1.3

NAB National Financials 35.31 5.20% 83,535 4.3 13.2 5.70% 2 0.9 Growth 13.1 na 1.7

Cash Cash 5.00%

WPL Woodside Energy 43.31 4.90% 35,684 7 13.5 5.90% 2.1 1.5 Income 11.9 16.9 0.8

WES Wesfarmers Cons Stap 43.80 4.40% 50,075 6.8 17.9 5.00% 1.9 1.2 Income 10.3 7.2 2.1

Total Portfolio

100.00

% 10.2 16.7 4.10% 2.7 1.2 16.8 2.7

29

Summary

• Investors should acclimatise to lower returns than in the recent past due to full

valuations and modest growth outlook

• Focus on higher-quality companies particularly vital given lack of value in the

market as these will be less affected by unforeseen shocks

• Competitively advantaged firms will rise in value over time due their ability to

invest capital at greater return than the costs

• Additional cash is valuable given likely rise in volatility which may create

opportunity for investment

30

Questions and Discussion

31

Contact Information

Andrew Doherty

Director

AssureInvest

Level 1, 50 Yeo Street

PO Box 612, Neutral Bay NSW 2089

m + 61 400 456 132

p + 612 8094 8410

32

![TERMS AND CONDITIONS zt{ / aGb]h · TERMS AND CONDITIONS zt{ / aGb]h ... 8](https://static.fdocuments.us/doc/165x107/5ecb9c6360da650bc655f7ac/terms-and-conditions-zt-agbh-terms-and-conditions-zt-agbh-8.jpg)