Ind.chapter 8xx

48

Prentice Hall's Federal Taxation 2013 Individuals, 26e (Pope) Chapter I8 Losses and Bad Debts 1) In order to be recognized and deducted on a tax return, a loss must first be realized. Answer: TRUE Page Ref.: I:8-2 Objective: 1 2) The amount of loss realized on the sale of property is computed by subtracting adjusted basis from amount realized. Answer: TRUE Page Ref.: I:8-2 Objective: 1 3) A loss incurred on the sale or exchange of property is deductible only if the property is used in a trade or business or held for investment. Answer: TRUE Page Ref.: I:8-3 Objective: 1 4) The sale of inventory at a loss results in an ordinary loss. Answer: TRUE Page Ref.: I:8-3 Objective: 1 5) Losses incurred in the sale or exchange of personal-use property are deductible as capital losses. Answer: FALSE Explanation: With limited exceptions, losses on personal assets cannot be recognized. Page Ref.: I:8-3 Objective: 1 6) A loss on business or investment property which is abandoned is deductible as an ordinary loss to the extent of the property's adjusted basis on the date of abandonment. Answer: TRUE Page Ref.: I:8-3 Objective: 1 7) The total worthlessness of a security results in an ordinary loss. Answer: FALSE Explanation: Losses are worthless securities are treated as capital losses. Page Ref.: I:8-4 Objective: 1 1 Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

-

Upload

mbadilishaji-dunia -

Category

Documents

-

view

284 -

download

2

description

xxx

Transcript of Ind.chapter 8xx

Prentice Hall's Federal Taxation 2013 Individuals, 26e (Pope)

Chapter I8 Losses and Bad Debts

1) In order to be recognized and deducted on a tax return, a loss must first be realized.Answer: TRUEPage Ref.: I:8-2Objective: 1

2) The amount of loss realized on the sale of property is computed by subtracting adjusted basis from amount realized.Answer: TRUEPage Ref.: I:8-2Objective: 1

3) A loss incurred on the sale or exchange of property is deductible only if the property is used in a trade or business or held for investment.Answer: TRUEPage Ref.: I:8-3Objective: 1

4) The sale of inventory at a loss results in an ordinary loss.Answer: TRUEPage Ref.: I:8-3Objective: 1

5) Losses incurred in the sale or exchange of personal-use property are deductible as capital losses.Answer: FALSEExplanation: With limited exceptions, losses on personal assets cannot be recognized.Page Ref.: I:8-3Objective: 1

6) A loss on business or investment property which is abandoned is deductible as an ordinary loss to the extent of the property's adjusted basis on the date of abandonment.Answer: TRUEPage Ref.: I:8-3Objective: 1

7) The total worthlessness of a security results in an ordinary loss.Answer: FALSEExplanation: Losses are worthless securities are treated as capital losses.Page Ref.: I:8-4Objective: 1

8) A capital loss may arise from the sale or exchange of a capital asset.Answer: TRUEPage Ref.: I:8-5Objective: 2

9) The destruction of a capital asset by a casualty gives rise to a capital rather than ordinary loss.Answer: FALSEExplanation: A casualty is not a sale or exchange so the loss is treated as ordinary.Page Ref.: I:8-5Objective: 2

1Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

10) One of the requirements which must be met for stock to be considered Section 1244 stock is that the stock must be owned by an individual or a partnership.Answer: TRUEPage Ref.: I:8-5Objective: 2

11) One of the requirements which must be met for stock to be considered Section 1244 stock is that the corporation cannot have more than $10 million of total paid in capital as of the stock issuance.Answer: FALSEExplanation: The paid in capital limitation is $1 million.Page Ref.: I:8-6Objective: 2

12) When applying the limitations of the passive activity rules, a taxpayer's AGI is classified into active income, portfolio income and passive income. For this purpose, portfolio income includes dividends, interest, annuities, and royalties.Answer: TRUEPage Ref.: I:8-7Objective: 3

13) Losses from passive activities that cannot be deducted currently are carried over for up to 5 subsequent years.Answer: FALSEExplanation: Losses may be carried over indefinitely.Page Ref.: I:8-8Objective: 3

14) Individual taxpayers can offset portfolio income with passive losses.Answer: FALSEExplanation: Under the general provisions, passive losses can only offset passive income.Page Ref.: I:8-8Objective: 3

15) If a taxpayer disposes of an interest in a passive activity, unused carryover losses are available to the purchaser of the interest.Answer: FALSEExplanation: The taxpayer will recognize his unused carryover passive losses when his passive activity is disposed of in a taxable manner.Page Ref.: I:8-8Objective: 3

2Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

16) A taxpayer may deduct suspended losses of a passive activity when the taxpayer completely terminates his or her ownership of the activity.Answer: TRUEPage Ref.: I:8-8Objective: 3

17) Once an activity has been classified as passive, it is considered passive with regard to that taxpayer until it is sold.Answer: FALSEExplanation: The taxpayer can become a material participant in an activity at a later time. Status is determined each year.Page Ref.: I:8-9Objective: 3

18) A passive activity includes any rental activity or any trade or business in which the taxpayer does not materially participate.Answer: TRUEPage Ref.: I:8-10Objective: 3

19) Two separate business operations conducted at the same location may be treated as separate activities under the passive activity rules.Answer: TRUEPage Ref.: I:8-10 and I:8-11Objective: 3

20) Partnerships and S corporations must identify their business and rental activities by applying the passive activity rules at the partnership or S corporation level and then must report the results of their operations by activity to the partners or shareholders.Answer: TRUEPage Ref.: I:8-11Objective: 3

21) Material participation by a taxpayer in a passive activity is satisfied if the individual participates in the activity for more than 500 hours during the year.Answer: TRUEPage Ref.: I:8-11Objective: 3

22) For purposes of the application of the passive loss limitations, a closely-held C corporation is a C corporation where more than 50 percent of the stock is owned by five or fewer individuals at any time during the last half of the taxable year.Answer: TRUEPage Ref.: I:8-12Objective: 3

23) A closely-held C Corporation's passive losses may offset its active income.Answer: TRUEPage Ref.: I:8-13Objective: 3

24) Individuals who actively participate in the management of rental real property may deduct up to $25,000 in losses, subject to AGI limitations.Answer: TRUEPage Ref.: I:8-15Objective: 3

3Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

25) For purposes of applying the passive loss limitations for rental real estate, active participation requires a greater time commitment by the taxpayer than does material participation.Answer: FALSEExplanation: Regular, continuous and material involvement is not required for active status so it is a lighter standard of involvement.Page Ref.: I:8-15Objective: 3

26) Taxpayers are allowed to recognize net passive losses from all activies up to a ceiling of $25,000.Answer: FALSEExplanation: The $25,000 loss allowance ceiling only applies to rental real properties in which the taxpayer is an "active" participant. The $25,000 ceiling applies to the total of qualifying losses.Page Ref.: I:8-15Objective: 3

27) A taxpayer may deduct a loss resulting from the theft of business and investment property but not a theft of personal-use property.Answer: FALSEExplanation: A limited deduction is allowed for the loss on personal-use property due to casualty or theft.Page Ref.: I:8-19Objective: 4

28) When business property involved in a casualty is totally destroyed, the amount of the loss is limited to the lesser of the taxpayer's adjusted basis in the property or the reduction in FMV.Answer: FALSEExplanation: The amount of the loss is the taxpayer's adjusted basis in the property.Page Ref.: I:8-19Objective: 4

29) In the case of casualty losses of personal-use property, the losses sustained in each separate casualty are reduced by both $100 and 10 percent of the taxpayer's AGI for the year.Answer: FALSEExplanation: It is the total casualty loss that is reduced by 10 percent of the taxpayer's AGI.Page Ref.: I:8-20Objective: 4

30) A theft loss is deducted in the year in which the theft is discovered.Answer: TRUEPage Ref.: I:8-22Objective: 4

31) When personal-use property is covered by insurance, no deduction is available for a casualty loss of the property unless the taxpayer timely files an insurance claim for the loss.Answer: TRUEPage Ref.: I:8-22Objective: 4

32) When the taxpayer anticipates a full recovery on a casualty loss of personal-use property but receives less than full recovery in a subsequent year, the unrecovered portion may be deducted.

4Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

Answer: TRUEPage Ref.: I:8-22Objective: 4

33) If a taxpayer suffers a loss attributable to a disaster in an area subsequently declared a disaster area, the casualty loss may be deducted in the year preceding the year in which the loss actually occurs.Answer: TRUEPage Ref.: I:8-23Objective: 4

34) For a bad debt to be deductible, the taxpayer must have a basis in the debt.Answer: TRUEPage Ref.: I:8-24Objective: 5

35) A bona fide debtor-creditor relationship can never exist in the case of related parties.Answer: FALSEExplanation: A bona fide debtor-creditor relationship can exist between related parties, but it can be harder to substantiate.Page Ref.: I:8-24Objective: 5

36) A taxpayer guarantees another person's obligation and is forced to pay the debt under the terms of the guarantee. The original debtor does not repay the taxpayer. The taxpayer/guarantor may deduct the loss.Answer: TRUEPage Ref.: I:8-25Objective: 5

37) Lisa loans her friend, Grace, $10,000 to finance a new business. If Grace defaults on the loan, Lisa may take a deduction for a business bad debt in the year of total worthlessness.Answer: FALSEExplanation: In order to be classified as a business bad debt, the debt must be related to the taxpayer's trade or business. See "Typical Misconception."Page Ref.: I:8-26Objective: 5

38) A business bad debt gives rise to an ordinary deduction while a nonbusiness bad debt is treated as a short-term capital loss.Answer: TRUEPage Ref.: I:8-26Objective: 5

39) No deduction is allowed for a partially worthless nonbusiness debt.Answer: TRUEPage Ref.: I:8-27Objective: 5

40) A net operating loss (NOL) occurs when taxable income for any year is negative because itemized deductions and total exemptions exceed business income.Answer: FALSEExplanation: A net operating loss involves only business income and expenses.Page Ref.: I:8-29Objective: 6

41) A net operating loss can be carried back three years or carried forward five years.

5Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

Answer: FALSEExplanation: The relevant period is two year carry back and 20 year carry forward.Page Ref.: I:8-32Objective: 6

42) All of the following losses are deductible exceptA) decline in value of securities.B) total worthlessness of securities.C) sale or exchange of business property.D) destruction of personal use property by fire, storm, or casualty.Answer: AExplanation: A) Securities must be sold or determined to be worthless in order for the loss to be realized and then recognized.Page Ref.: I:8-2; Example I:8-1Objective: 1

43) The amount realized by Matt on the sale of property to Caitlin includes all of the following with the exception ofA) cash received by Matt.B) mortgage on the property that is assumed by Caitlin.C) mortgage on the property paid off by Matt prior to the sale.D) the FMV of any other property received by Matt in the transaction.Answer: CExplanation: C) Cash received, the mortgage assumed by the buyer, and the FMV of property received in the transaction are all part of amount realized.Page Ref.: I:8-2Objective: 1

6Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

44) In 2000, Michael purchased land for $100,000. Over the years, economic conditions deteriorated, and the value of the land declined to $60,000. Michael sells the property in this year, when it is subject to a $30,000 nonrecourse mortgage. The buyer pays Michael $34,000 cash and takes the property subject to the mortgage. Michael incurs $5,000 in real estate commissions. Michael's gain or loss on the sale isA) $4,000 gain.B) $1,000 loss.C) $36,000 loss.D) $41,000 loss.Answer: DExplanation: D) ($30,000 + $34,000 - $5,000) - $100,000 = $41,000 lossPage Ref.: I:8-2; Example I:8-2Objective: 1

45) Jamie sells investment real estate for $80,000, resulting in a $15,000 loss. Jamie's loss isA) an ordinary loss.B) a capital loss.C) a Sec. 1231 loss.D) a Sec. 1244 loss.Answer: BExplanation: B) Real estate held for investment is considered a capital asset, therefore the loss on the sale or exchange is a capital loss.Page Ref.: I:8-5; Example I:8-4Objective: 2

46) Juan has a casualty loss of $32,500 on investment property after receiving an insurance settlement. This is Juan's only casualty transaction this year. Juan's loss isA) an ordinary loss.B) a capital loss.C) a Sec. 1231 loss.D) a Sec. 1244 loss.Answer: AExplanation: A) Although real estate held as an investment is a capital asset, the $32,500 loss is ordinary since a casualty is not a sale or exchange.Page Ref.: I:8-5; Example I:8-4Objective: 2

47) All of the following are true of losses from the sale or worthlessness of small business corporation (Section 1244) stock with the exception ofA) the stock must be owned by an individual or a partnership.B) the stock must have been issued by a domestic corporation.C) the stock must have been issued for cash or property other than stock or securities.D) a single taxpayer may deduct, as ordinary losses, up to a maximum of $100,000 per tax year with the remainder treated as capital losses.Answer: DExplanation: D) Single taxpayers may deduct up to $50,000 per tax year.Page Ref.: I:8-5Objective: 2

7Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

48) Stacy, who is married and sole shareholder of ABC Corporation, sold all of her stock in the corporation for $100,000. Stacy had organized the corporation in 2009 by contributing $225,000 and receiving all of the capital stock of the corporation. ABC Corporation is a domestic corporation engaged in the manufacturing of ski boots. The stock in ABC Corporation qualified as Sec. 1244 stock. The sale results in a(n)A) ordinary loss of $125,000.B) long-term capital loss of $125,000.C) long-term capital loss of $100,000 and ordinary loss of $25,000.D) ordinary loss of $100,000 and long-term capital loss of $25,000.Answer: DExplanation: D) The loss realized is $100,000 - $225,000 = ($125,000). Since the stock is Section 1244 stock and Stacy is an original owner, the first $100,000 (for married individuals) of the loss is treated as ordinary. The remainder of $25,000 ($125,000 - $100,000) is treated as long-term capital gain since Stacy held the stock longer than 12 months.Page Ref.: I:8-5Objective: 2

49) Amy, a single individual and sole shareholder of Brown Corporation, sold all of the Brown stock for $30,000. The stock basis was $150,000. Amy had owned the stock for 3 years. Brown Corporation meets the Section 1244 requirements. Amy hasA) a $50,000 ordinary loss and $70,000 LTCL.B) a $50,000 STCL and a $70,000 LTCL.C) a $100,000 ordinary loss and a $20,000 LTCL.D) a $100,000 LTCL and a $20,000 ordinary loss.Answer: AExplanation: A) The loss realized is $30,000 - $150,000 = ($120,000). Since the stock is Section 1244 stock and Amy is an original owner, the first $50,000 (for single individuals) of the loss is treated as ordinary. The remainder of $70,000 ($120,000 - $50,000) is treated as long-term capital gain since Amy held the stock longer than 12 months.Page Ref.: I:8-5Objective: 2

50) Sarah had a $30,000 loss on Section 1244 stock, a $15,000 loss on sale of a personal use automobile and a $8,000 loss on stock that is not classified as Section 1244. Without regard to net capital loss limitations, Sarah should recognizeA) a ordinary loss of $38,000.B) a capital loss of $53,000.C) an ordinary loss of $30,000 and a capital loss of $8,000.D) an ordinary loss of $30,000 and a capital loss of $23,000.Answer: CExplanation: C) $30,000 Section 1244 ordinary loss + $8,000 capital loss. The loss on the sale of personal use assets, the automobile, is not deductible.Page Ref.: I:8-5Objective: 2

8Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

51) During the year, Mark reports $90,000 of active business income from his law practice. He also owns two passive activities. From Activity A, he earns $20,000 of income, and from Activity B, he incurs a $30,000 loss. As a result, MarkA) reports AGI of $80,000.B) reports AGI of $90,000 with a $10,000 loss carryover.C) reports AGI of $90,000 with a $30,000 loss carryover.D) reports AGI of $110,000 with a $30,000 loss carryover.Answer: BExplanation: B) Mark offsets $20,000 of B's loss against A's income and carries forward the $10,000 loss. His AGI is $90,000 from the active business income.Page Ref.: I:8-8; Example I:8-5Objective: 3

52) Joy reports the following income and loss:

Salary $ 120,000 Income from activity A 60,000 Loss from activity B ( 35,000)Loss from activity C ( 55,000)

Activities A, B, and C are all passive activities.

Based on this information, Joy hasA) adjusted gross income of $90,000.B) salary of $120,000 and deductible net losses of $30,000.C) salary of $120,000 and net passive losses of $30,000 that will be carried over.D) salary of $120,000, passive income of $60,000, and passive loss carryovers of $90,000.Answer: CExplanation: C) The losses from passive activities B and C may offset and eliminate the income from passive activity A resulting in a net passive loss of $30,000 ($60,000 income less $90,000 loss). The passive loss of $30,000 may not offset the salary and must be carried over to the next tax year.Page Ref.: I:8-8; Example I:8-6Objective: 3

53) Jeff owned one passive activity. Jeff sold the activity and realized a $2,000 gain on the sale. Prior to the sale, he realized a current year loss from the activity of $6,000. In addition, he has suspended losses from prior years of $7,000. What is the net impact on Jeff's AGI this year due to the passive activity?A) Increase of $2,000.B) No net change.C) Decrease of $4,000.D) Decrease of $11,000.Answer: DExplanation: D) Due to the sale, the current year loss and the suspended loss will be recognized. $2,000 gain - $$6,000 current loss - $7,000 suspended loss = $11,000 loss.Page Ref.: I:8-8Objective: 3

9Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

54) Nancy reports the following income and loss in the current year.

Salary $ 60,000 Income from activity A 18,000 Loss from activity B ( 9,000)Loss from activity C ( 13,000)

All three activities are passive activities with respect to Nancy. Nancy also has $21,000 of suspended losses attributable to activity C carried over from prior years. During the year, Nancy sells activity C and realizes a $15,000 taxable gain. What is Nancy's AGI as a result of these transactions?A) $50,000B) $55,000C) $64,000D) $71,000Answer: AExplanation: A) Loss from C for the year ($ 13,000)Gain on sale of C 15,000 Suspended loss from C ( 21,000)Total loss from C ($19,000)Income from A $ 18,000 Loss from B ( 9,000) 9,000 Nancy's deduction against salary income ($ 10,000)

$60,000 - $10,000 = $50,000Page Ref.: I:8-8; Example I:8-7Objective: 3

55) Lewis died during the current year. Lewis owned passive activity property with a FMV of $61,000 and a basis of $48,000. Suspended losses of $15,000 were attributable to the property. How much of the suspended loss is deductible on Lewis's final income tax return?A) $0B) $2,000C) $13,000D) $15,000Answer: BExplanation: B) ($61,000 - $48,000) is increase in basis; $13,000 of suspended losses is lost. $15,000 - $13,000 = $2,000.Page Ref.: I:8-9; Example I:8-8Objective: 3

10Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

56) Mara owns an activity with suspended passive losses from prior years of $13,000. In the current year, Mara becomes a material participant in the activity. This year the activity generates $6,000 of income. The net effect of this activity on Mara's current year AGI is a(n)A) increase of $6,000.B) decrease of $13,000.C) -0-.D) decrease of $7,000.Answer: CExplanation: C) The suspended passive loss will be allowed to offset this year's non-passive income from the activity, but the excess suspended passive loss of $7,000 will carryforward.Page Ref.: I:8-9; Example I:8-9Objective: 3

57) Charlie owns activity B which was considered a passive activity and generated a $17,000 suspended loss. Charlie increases his involvement with activity B so that this year activity B is not considered passive for Charlie. During this year, activity B produces a $9,000 loss. In addition, Charlie acquires an investment in activity X, a passive activity, this year. Charlie's share of activity X's income is $13,000. Charlie's salary this year is $70,000. As a result, this year Charlie mustA) offset B's loss carryover against X's current income and carry over $9,000 loss from activity B to next year.B) offset B's carryover loss and current loss against X's income first and then offset any remaining loss against salary.C) offset B's $9,000 loss against X's $13,000 income and offset B's loss carryover against the remaining $4,000 of X's income.D) offset B's current $9,000 loss against his salary and offset B's loss carryover against X's income and carry over $4,000 of loss to next year.Answer: DExplanation: D) Charlie may deduct Activity B's current $9,000 loss since it is not a passive activity; may offset passive activity X's income of $13,000 with the $17,000 carryover from Activity B resulting in a $4,000 carryover.Page Ref.: I:8-9; Example I:8-9Objective: 3

58) Jorge owns activity X which produced a $20,000 passive loss last year. Jorge's only income last year was wages of $30,000. Jorge is a material participant in activity X this year when it produces a $14,000 loss. This year, Jorge's wages are $40,000. This year, Jorge also has passive activity income from activity Y of $16,000. What is the total passive activity loss carryover to next year?A) $-0-B) $3,000C) $4,000D) $18,000Answer: CExplanation: C) $20,000 carryover from prior year - $16,000 current passive income offset = $4,000 carryover to next year. This year's $14,000 active business loss from Activity X may offset Jorge's wages.Page Ref.: I:8-9; Example I:8-9Objective: 3

11Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

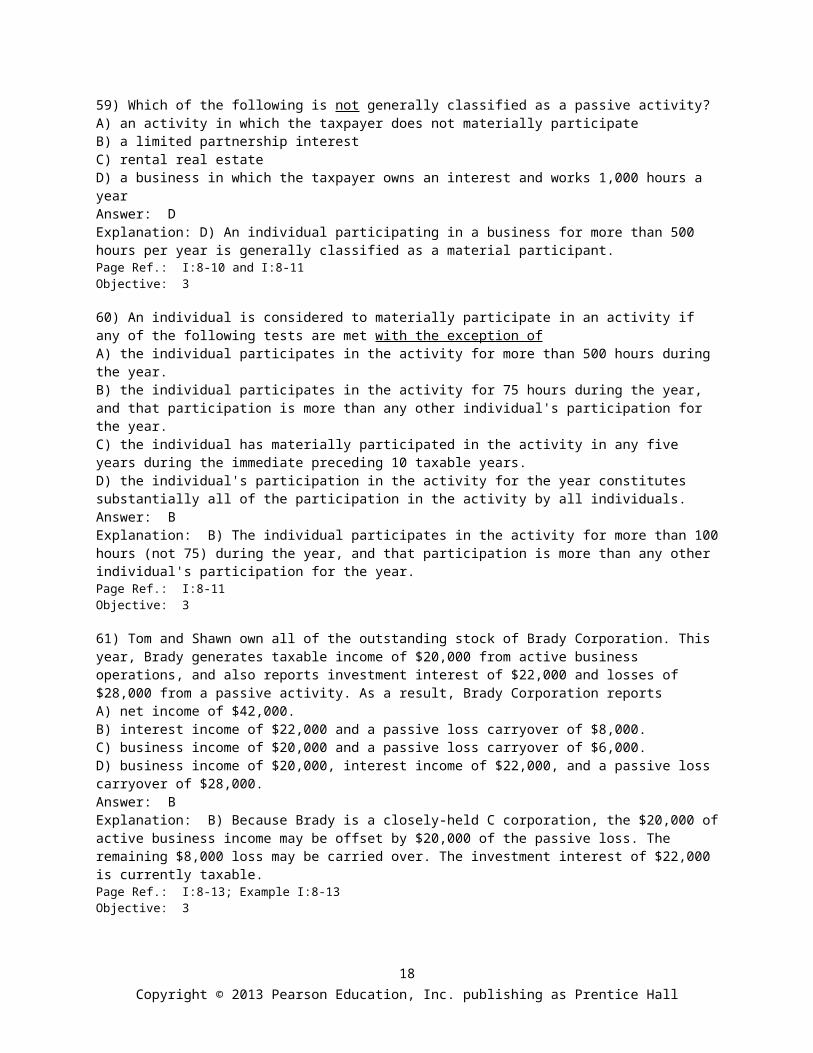

59) Which of the following is not generally classified as a passive activity?A) an activity in which the taxpayer does not materially participateB) a limited partnership interestC) rental real estateD) a business in which the taxpayer owns an interest and works 1,000 hours a yearAnswer: DExplanation: D) An individual participating in a business for more than 500 hours per year is generally classified as a material participant.Page Ref.: I:8-10 and I:8-11Objective: 3

60) An individual is considered to materially participate in an activity if any of the following tests are met with the exception ofA) the individual participates in the activity for more than 500 hours during the year.B) the individual participates in the activity for 75 hours during the year, and that participation is more than any other individual's participation for the year.C) the individual has materially participated in the activity in any five years during the immediate preceding 10 taxable years.D) the individual's participation in the activity for the year constitutes substantially all of the participation in the activity by all individuals.Answer: BExplanation: B) The individual participates in the activity for more than 100 hours (not 75) during the year, and that participation is more than any other individual's participation for the year.Page Ref.: I:8-11Objective: 3

61) Tom and Shawn own all of the outstanding stock of Brady Corporation. This year, Brady generates taxable income of $20,000 from active business operations, and also reports investment interest of $22,000 and losses of $28,000 from a passive activity. As a result, Brady Corporation reportsA) net income of $42,000.B) interest income of $22,000 and a passive loss carryover of $8,000.C) business income of $20,000 and a passive loss carryover of $6,000.D) business income of $20,000, interest income of $22,000, and a passive loss carryover of $28,000.Answer: BExplanation: B) Because Brady is a closely-held C corporation, the $20,000 of active business income may be offset by $20,000 of the passive loss. The remaining $8,000 loss may be carried over. The investment interest of $22,000 is currently taxable.Page Ref.: I:8-13; Example I:8-13Objective: 3

12Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

62) Justin has AGI of $110,000 before considering his $30,000 loss from rental property, which he actively manages. How much of the rental loss can Justin deduct this year?A) $10,000B) $20,000C) $25,000D) $30,000Answer: BExplanation: B) Justin must reduce the $25,000 rental loss allowance by 50% of his AGI over $100,000, resulting in a deductible loss of $20,000 [$25,000 - .5($110,000 - $100,000)].Page Ref.: I:8-14 and I:8-15; Example I:8-16Objective: 3

63) Joseph has AGI of $170,000 before considering the $20,000 rental loss for property which he actively manages. How much of the rental loss can he deduct?A) $0B) $10,000C) $20,000D) $25,000Answer: AExplanation: A) His AGI exceeds $150,000, so no portion of the rental loss is deductible.Page Ref.: I:8-15Objective: 3

64) Shaunda has AGI of $90,000 and owns rental property generating a $27,000 loss. She actively manages the property. Her deductible loss isA) $0.B) $13,500.C) $25,000.D) $27,000.Answer: CExplanation: C) Since her AGI is less than $100,000, she is allowed a $25,000 rental loss. She has a $2,000 suspended loss.Page Ref.: I:8-15Objective: 3

13Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

65) Brandon, a single taxpayer, had a loss of $48,000 from a rental real estate activity in which he actively participated. He also had $27,000 of income from another rental real estate activity in which he actively participated. He acquired both investments in 2008. If Brandon has no other passive income or losses and has adjusted gross income of $84,000 before considering passive activities, how much loss from rental activities can he use to offset his nonpassive income?A) $21,000B) $24,000C) $25,000D) $45,000Answer: AExplanation: A) $27,000 of the loss offsets $27,000 income from the other passive activity, leaving a net.$21,000 loss. The $21,000 net rental loss may offset nonpassive income using the special allowance of up to $25,000.Page Ref.: I:8-15Objective: 3

66) Which of the following is most likely not considered a casualty?A) fire lossB) water damage caused by a busted water heaterC) death of a pine tree due to a two-day infestation of pine beetlesD) water damage to the walls and ceiling of a taxpayer's personal residence as the result of gradual deterioration of the roofAnswer: DExplanation: D) Water damage due to the gradual deterioration of a roof is not a casualty.Page Ref.: I:8-17Objective: 4

67) Nicole has a weekend home on Pecan Island that she purchased in 2005 for $250,000. Recently, the home was appraised at $260,000. After the appraisal, a hurricane hit Pecan Island, severely damaging Nicole's home. An appraisal placed the value of the home at $140,000 after the hurricane. Because of its prohibitive cost, Nicole had no hurricane insurance. Before any reductions or limitations, Nicole's casualty loss amount isA) $0.B) $10,000.C) $120,000.D) $140,000.Answer: CExplanation: C) Lesser of: Basis $250,000

or Reduction in FMV: FMV Before casualty $260,000 Minus: FMV After casualty ( 140,000)Reduction in FMV $120,000

Page Ref.: I:8-19; Example I:8-21Objective: 4

68) A fire totally destroyed office equipment and furniture which Monica uses in her business. The equipment had an adjusted basis of $15,000 and a FMV of $10,000 before the fire. The furniture's adjusted basis was $5,000 and its FMV was $2,000 before the fire. Monica's AGI for the year is $60,000. Monica does not have insurance on the destroyed assets. How much is Monica's deductible casualty loss?A) $5,900B) $12,000

14Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

C) $13,900D) $20,000Answer: DExplanation: D) For business property totally destroyed, the amount of the loss is the property's adjusted basis. There is no reduction for the $100 floor and 10% of AGI for business property. The loss equals the $20,000 adjusted bases of the property destroyed ($15,000 + $5,000).Page Ref.: I:8-19 and I:8-20; Example I:8-22Objective: 4

69) Lena owns a restaurant which was damaged by a tornado. The following assets were partially destroyed:

Basis Reduction in FMV Insurance PaymentBuilding $150,000 $200,000 $100,000Equipment $30,000 $20,000 $10,000

Lena has AGI of $50,000. What is the amount of Lena's deductible casualty loss?A) $54,900B) $60,000C) $70,000D) $180,000Answer: BExplanation: B) (150,000 - 100,000) + (20,000 - 10,000) = $60,000. The amount of the loss is the lower of the property's adjusted basis or the decline in FMV, reduced by the insurance proceeds. Since the property was used in Lena's business, there is no 10% of AGI and $100 floor.Page Ref.: I:8-19 and I:8-20Objective: 4

70) Leonard owns a hotel which was damaged by a hurricane. The hotel had an adjusted basis of $1,000,000 before the hurricane. A recent appraisal determined that the hotel's FMV was $1,500,000 before the hurricane and $700,000 afterwards. Leonard received insurance proceeds of $500,000. His AGI is $60,000. What is the amount of his deductible casualty loss?A) $293,900B) $300,000C) $793,900D) $800,000Answer: BExplanation: B) For business property partially destroyed, the amount of the loss is the lower of the decline in FMV or adjusted basis. The decline in FMV is $800,000. Leonard received insurance proceeds of $500,000, resulting in a deductible casualty loss of $300,000.Page Ref.: I:8-20Objective: 4

15Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

71) Jarrett owns a mountain chalet that he purchased in 2008 for $175,000. This year, the home appraised at $300,000. Shortly after the appraisal, a blizzard hit the area in spring of the current year, destroying trees and severely damaging several homes, including Jarrett's chalet. Its value was reduced to $135,000. Jarrett does not have insurance. Jarrett's AGI is $200,000. Jarrett's deductible loss after limitations isA) $135,000.B) $144,900.C) $164,900.D) $165,000.Answer: BExplanation: B) Lesser of: Basis $ 175,000

or Reduction in FMV: FMV Before casualty $300,000 Minus: FMV After casualty ( 135,000)Reduction in value $ 165,000

Loss $ 165,000 Minus: $100 floor ( 100)

$ 164,900 Minus: 10% of AGI ( 20,000)Deductible loss $ 144,900 Page Ref.: I:8-20; Example I:8-23 and I:8-24Objective: 4

72) Hope sustained a $3,600 casualty loss due to a severe storm. She also incurred a $800 loss from a theft in the same year. Both the casualty and theft involved personal-use property. Hope's AGI for the year is $25,000 and she does not have insurance coverage. Hope's deductible casualty loss isA) $1,700.B) $1,800.C) $4,200.D) $4,300.Answer: AExplanation: A)

Storm Theft TotalLoss before limits $3,600 $ 800 $4,400Minus: $100 floor ( 100) ( 100) ( 200)

$3,500 $ 700 $4,200Minus: 10% of AGI ( 2,500)Deductible loss $ 1,700

Page Ref.: I:8-20; Example I:8-24Objective: 4

16Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

73) In the current year, Marcus reports the following casualty gains and losses on personal-use property. Assets X and Y are destroyed in the first casualty while Z is destroyed in a second casualty.

AssetReduction

in FMVAdjusted Basis Insurance

Holding Period

X $8,000 $2,000 $7,000 2 yearsY 3,000 5,000 2,000 10 monthsZ 2,500 1,300 1,000 8 months

As a result of these losses and insurance recoveries, Marcus must reportA) a net gain of $3,700.B) a long-term gain of $4,900 on asset X; a short-term capital loss of $900 on asset Y; and a short-term capital loss of $200 on asset Z.C) a long-term capital gain of $5,000 on asset X; a short-term capital loss of $900 on asset Y; and a short-term capital loss of $200 on asset Z.D) a long-term capital gain of $5,000 on asset X; a short-term capital loss of $900 on asset Y; and a short-term capital loss of $300 on asset Z.Answer: CExplanation: C) Gain on X: $7,000 - $2,000 $5,000 Minus: Loss on Y: $2,000 - $3,000 - 100 ( 900) Net gain on first casualty $4,100Loss on Z: $1,000 - $1,300 300 Minus: $100 floor ( 100) ( 200)Net casualty gain $3,900

If the netting process results in a net gain, each item is treated as a separate capital gain and loss. Thus, there is a $5,000 LTCG on Asset X; the $1,000 STCL on Asset Y is reduced by the $100 floor; the $300 STCL on Asset Z is reduced by the $100 floor.Page Ref.: I:8-21; Example I:8-25Objective: 4

74) Wesley completely demolished his personal automobile in a car accident. Damage to the auto was estimated at $35,000. Wesley had purchased the car a few years ago for $60,000. He received an insurance reimbursement of $28,000. His adjusted gross income this year was $55,000 and he incurred no other losses during the year. What amount can he deduct as a casualty loss on his income tax return after limitations?A) $1,400B) $1,500C) $6,900D) $7,000Answer: AExplanation: A) ($35,000 - $28,000 - $100 - $5,500) = $1,400Page Ref.: I:8-22Objective: 4

17Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

75) A flood damaged an auto owned by Mr. and Mrs. South on June 15 of this year. The car was only used for personal purposes.

Fair market value before the flood $18,500Fair market value after the flood 2,000Cost basis 20,000Insurance proceeds 13,000Adjusted gross income for this year 25,000Business use of auto -0-

Based on these facts, what is the amount of the South's casualty loss deduction after limitations for this year?A) $900B) $1,000C) $4,400D) $4,500Answer: AExplanation: A) Fair market value before the flood $18,500 Fair market value after the flood ( 2,000)Decline in FMV $16,500 Cost basis 20,000 Lesser of basis or decline in FMV $16,500 Minus: Insurance proceeds ( 13,000)Net loss $3,500 Minus: $100 Floor ( 100)10% of AGI ( 2,500)Deductible Loss $ 900

Page Ref.: I:8-22Objective: 4

18Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

76) In February 2012, Amelia's home, which originally cost $150,000, is damaged by a windstorm. Amelia had refinanced the home shortly before the storm, and it was appraised at $200,000. After the storm, the home appraised at $120,000. Amelia has received no insurance reimbursement by December 31, but expects to recover 90 percent of the loss. In the subsequent year, the insurance company pays Amelia $50,000. Amelia's AGI is $85,000 in 2012, and her 2013 AGI is $80,000. Amelia suffers no other casualty losses in either year. Amelia may deductA) $7,900 in 2012.B) $22,000 in 2013.C) $13,900 in 2013.D) $14,000 in 2013.Answer: DExplanation: D) Loss deducted 2012:Decrease in FMV (200,000 -120,000) $80,000 Minus: Floor ( 100)Subtotal $79,900 Minus: Anticipated recovery ( 72,000)Tentative loss $ 7,900 Minus: 10% of AGI ( 8,500)Deductible loss -0- Loss in 2013, additional loss due to smaller recovery ($72,000 - 50,000) $22,000 10% of AGI ( 8,000)Deductible in subsequent year $14,000

Page Ref.: I:8-22 and I:8-23; Example I:8-29Objective: 4

77) This summer, Rick's home (which has a basis of $80,000) is damaged by a tornado. An appraisal by a realtor placed the FMV of the home at $120,000 before the tornado and at $85,000 after the tornado. Rick estimates that the insurance company will reimburse him for 60% of the loss. Next year, the insurance company pays Rick $20,000. Rick's current year's AGI is $50,000 and his next year's AGI is $55,000. Rick suffers no other casualty losses in either year. After limitations, Rick may deduct a casualty loss this year ofA) $ 8,900.B) $ 9,900.C) $15,000.D) $35,000.Answer: AExplanation: A) Where partial recovery is expected in a subsequent year, the loss may be deducted in the year of the casualty for the estimated unrecovered amount. Lesser of adjusted basis or loss in value [($120,000 - $85,000) - $21,000 insurance recovery - $100 floor - $5,000 AGI =$8,900]. Anticipated recovery is 60% × $35,000 = $21,000.Page Ref.: I:8-23; Example I:8-29Objective: 4

19Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

78) Juanita, who is single, is in an automobile accident in 2012 and her car sustains $6,200 in damages. Because both drivers received tickets in the accident, Juanita does not expect to recover any of the loss from her insurance company. Juanita's 2012 AGI is $31,000, and she deducts a $3,000 loss on her 2012 tax return. Her other itemized deductions in 2012 exceed $12,000. In 2013, Juanita's insurance company reimburses her $2,800. Juanita's 2012 AGI is $28,000. As a result, Juanita mustA) amend 2012 to show a $200 loss.B) do nothing and simply keep the $2,800.C) do nothing to the 2012 return but report $2,800 of income on her 2013 return.D) amend the 2012 return to show $0 loss and file her 2013 return to show a $200 loss.Answer: CExplanation: C) Loss deducted in 2012: $6,200 Minus: Floor ( 100)

$6,100 Minus: 10% of AGI (3,100)Loss deducted in 2012 $3,000 Tax benefit received $3,000 Reimbursement received in 2013 $2,800 Report lesser amount in 2013 income $2,800

Page Ref.: I:8-23; Example I:8-30Objective: 4

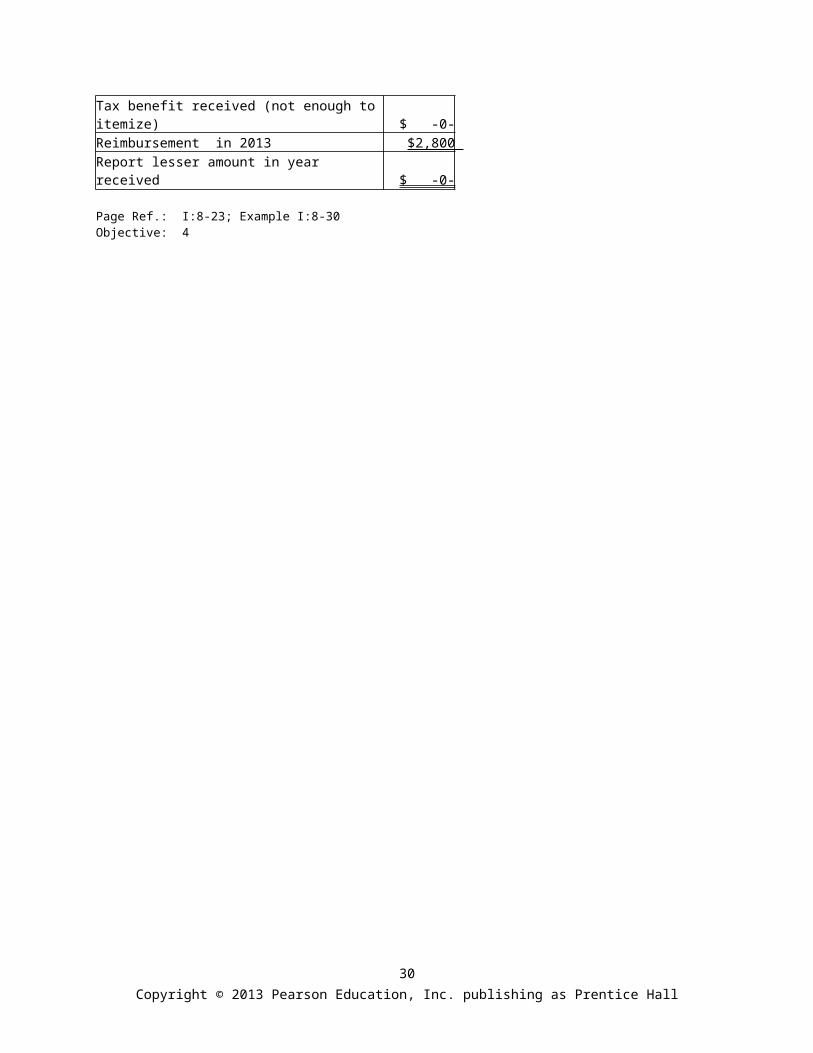

79) Constance, who is single, is in an automobile accident in 2012, and her car sustains $6,200 in damages. Because both drivers received tickets in the accident, Constance does not expect to recover any of the loss from her insurance company. Constance's 2012 AGI is $31,000. Her casualty loss is $3,000; she has other itemized deductions of $1,200. In 2013, Constance's insurance company reimburses her $2,800. Constance's 2013 AGI is $28,000. As a result, Constance mustA) amend the 2012 return to show the $200 loss.B) do nothing and simply keep the $2,800.C) amend the 2012 return to show $0 loss and file her 2013 return to show $200 loss.D) do nothing to the 2012 return but report $2,800 of income on her 2013 return.Answer: BExplanation: B) Loss deducted in 2012: $6,200 Minus: Floor ( 100)

$6,100 Minus: 10% of AGI (3,100)Loss $3,000 Tax benefit received (not enough to itemize) $ -0- Reimbursement in 2013 $2,800 Report lesser amount in year received $ -0-

Page Ref.: I:8-23; Example I:8-30Objective: 4

20Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

80) Last year, Abby loaned Pat $10,000 as a gesture of their friendship. Although Pat had signed a note payable that contained interest payments and a maturity date, the loan had not been repaid this year when Pat died insolvent. For this year, assuming that the loan was bona fide, Abby should account for nonpayment of the loan as a(n)A) itemized deduction.B) ordinary loss.C) long-term capital loss.D) short-term capital loss.Answer: DExplanation: D) Because the debt is not related to Abby's trade or business, it is a nonbusiness bad debt. All nonbusiness bad debts are deductible as short-term capital losses.Page Ref.: I:8-26Objective: 5

81) In October 2012, Jonathon Remodeling Co., an accrual-method taxpayer, remodels and renovates an office building for Dale and bills him $30,000. Dale signs a note for the debt. Dale keeps delaying payment and files bankruptcy in 2013. Creditors are informed that no assets are available for payment. Jonathon Remodeling Co. will reportA) $0 income in both years.B) $30,000 income in 2012 and a bad debt deduction of $30,000 in 2013.C) $30,000 income in 2012 and a STCL of $30,000 in 2013 limited to $3,000 after netting.D) $30,000 income in 2012 and then must amend last year's return to show $0 income when advised of the bankruptcy.Answer: BExplanation: B) Since Jonathon Remodeling Co. is an accrual-basis taxpayer, the $30,000 is recognized in income when billed in 2012. The debt is a business bad debt since it is related to a trade or business. The nonpayment in 2013 results in a business bad debt which is an ordinary loss deductible in 2013.Page Ref.: I:8-26Objective: 5

82) Martha, an accrual-method taxpayer, has an accounting practice. In 2011, she performs tax analyses for Arnold and sends him an invoice for $10,000. In 2012, Martha sells her practice and all accounts to David. Arnold's debt becomes worthless that year. The result isA) Martha deducts a nonbusiness bad debt in 2012.B) Martha deducts a business bad debt in 2012C) David deducts a business bad debt in 2012.D) David deducts a nonbusiness bad debt in 2012.Answer: CExplanation: C) Since David acquired the account upon acquiring the business, he is entitled to a business bad debt deduction because the debt was incurred in the trade or business in which David is currently engaged.Page Ref.: I:8-27; Example I:8-34Objective: 5

21Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

83) Vera has a key supplier for her business who was facing cash flow problems which would impair Vera's ability to get shipments of key components for her production. Vera made a $10,000 to the supplier. Unfortunately the supplier filed for bankruptcy and has gone out of business without repaying Vera. Vera will be able to recognize a loss ofA) $10,000.B) $3,000.C) $7,000.D) -0-Answer: AExplanation: A) The motivation for the loan is to assist the functioning of Vera's business so it will be considered a business bad debt. An ordinary loss of the full amount will be allowed.Page Ref.: I:8-27; Example I:8-35Objective: 5

84) In 2011 Grace loaned her friend Paula $12,000 to invest in various stocks. Paula signed a note to repay the principal with interest. Unfortunately the market for that industry sector plunged, and Paula incurred large losses. In 2012 Paula declared personal bankruptcy and Grace was unable to collect any of her loan. Grace had no other gains or losses last year or this year. The result isA) Grace deducts a business bad debt of $12,000 in 2012.B) Grace deducts a $12,000 nonbusiness bad debt as a short-term capital loss in 2012.C) Grace deducts a $3,000 nonbusiness bad debt as a short-term capital loss in 2012 and carries $9,000 over to subsequent years.D) Grace deducts a business bad debt of $3,000 in 2012 and carries $9,000 over to subsequent years.Answer: CExplanation: C) The debt is a nonbusiness bad debt since it is not related to Grace's trade or business. Therefore, the $12,000 loss is treated as a short-term capital loss, $3,000 of which is deductible this year and $9,000 of which may be carried over to next year.Page Ref.: I:8-27; Example I:8-36Objective: 5

85) Which of the following expenses or losses could create a net operating loss for an individual taxpayer?A) large losses on sales of investment assetsB) an operating loss from a sole proprietorshipC) large charitable contributionsD) all of the aboveAnswer: BExplanation: B) Generally only business losses will allow the creation of an NOL.Page Ref.: I:8-29Objective: 6

22Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

86) An individual taxpayer has negative taxable income for the year. In calculating the net operating loss created, which of the following expenses or losses will be added back to the negative taxable income?A) capital lossesB) personal and dependency exemptionsC) nonbusiness deductions in excess of nonbusiness incomeD) all of the aboveAnswer: DExplanation: D) The NOL is due to business losses so all of the above will be added back in the computation of the NOL.Page Ref.: I:8-30 and I:8-31Objective: 6

87) A taxpayer incurs a net operating loss in the current year. With respect to the application of the NOL, A) the taxpayer will carry back the NOL three years first, then carry forward any balance for five years.B) the taxpayer must carry forward the loss and has up to 20 years to use it.C) the taxpayer can carry forward the loss indefinitely until there is sufficient taxable income to use it up.D) the taxpayer will first carry back the NOL for two years, then carryforward the balance for a period of 20 years, or the taxpayer can elect to only carry forward the loss for the 20-year allowable period.Answer: DExplanation: D) The normal application period for utilizing the NOL is carry back two years and then carry forward for up to 20 years, but the taxpayer does have the option to forego the carryback period.Page Ref.: I:8-32 and I:8-33Objective: 6

88) Kendal reports the following income and loss:

Salary $120,000 Income from activity A 36,000 Loss from activity B ( 30,000)Loss from activity C ( 60,000)

Activities A, B, and C are all passive activities, but none are rental properties. What is the amount of the suspended loss attributable to each activity?Answer: Kendal has a net passive loss for the year of $54,000 ($90,000 losses - 36,000 income) which must be carried over to subsequent years. The carryover is allocated as follows:

Activity B: $54,000 × = $18,000

Activity C: $54,000 × = $36,000

Page Ref.: I:8-8; Example I:8-6Objective: 3

23Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

89) During the year, Patricia realized $10,000 of taxable income from activity A, $4,000 loss from activity B, and $6,000 of taxable income from activity C. All three activities are passive activities with regard to Patricia. In addition, $32,000 of passive losses from activity C is carried over from prior years. During the current year, Patricia sells activity C for an $18,000 taxable gain. Patricia's salary for the year is $100,000. What is the amount of Patricia's deduction against salary income?Answer: Income for the year from C $6,000 Gain from the sale of C 18,000 Suspended losses from C (32,000)Total loss from C ($8,000)Income for the year from A $10,000 Loss for the year from B ( 4,000) 6,000 Patricia's deduction against salary income ($2,000)Page Ref.: I:8-8 and I:8-9; Example I:8-7Objective: 3

90) Hersh realized the following income and loss this year:

Net taxable income from chocolate shop $50,000Interest income 10,000Loss from passive activity (not a rental property) (58,000)

a. Assume Hersh is an individual taxpayer and the chocolate shop is his sole proprietorship. Determine Hersh's AGI and any carryovers.b. Assume the taxpayer is Hersh Inc., a C corporation, owned 100% by the Hersh family. Determine Hersh Inc.'s taxable income and any carryovers.Answer:

a. Individualb. C corporation

Active trade or business income $50,000 $50,000Portfolio (interest) income 10,000 10,000Allowed passive loss 0 (50,000)AGI/Taxable income $60,000 $10,000

Passive loss carryover $58,000 $8,000

Hersh Inc. is a closely held C corporation and can recognize passive losses up to the level of its active trade and business income, but it cannot offset portfolio income.Page Ref.: I:8-12 and I:8-13; Example I:8-13Objective: 3

91) Adam owns interests in partnerships A and B, both of which are Publicly Traded Partnerships. During the current year, Adam's share of the income from A is $12,000. Adam's share of B's loss is $3,500. B also generates portfolio income of which Adam's share is $2,000. What are the tax consequences of these income and loss items?Answer: The $12,000 income from A and the $2,000 from B are portfolio income. Thus, Adam reports $14,000 of portfolio income. He also has a suspended loss of $3,500 from partnership B.Page Ref.: I:8-13 and I:8-14; Example I:8-14Objective: 3

92) Parveen is married and files a joint return. He reports the following items of income and loss for the year:

24Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

Salary $ 135,000 Activity A (passive) 13,000 Activity B (nonbusiness rental real estate) ( 45,000)

If Parveen actively participates in the management of Activity B, what is his AGI for the year and what is the passive loss carryover to next year?Answer: Salary $135,000 Passive Activity A Income $13,000 Less: Portion of Activity B Loss ( 13,000) -0-

Less: Special AllowanceMaximum rental real estate lossAllowed for Activity B $25,000 Reduced by Phase-out:

($135,000 - 100,000) × .50 (17,500) ( 7,500)AGI $127,500

The carryover is $45,000 - 13,000 - 7,500 = $24,500.Page Ref.: I:8-14 and I:8-15; Example I:8-16Objective: 3

25Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

93) Aretha has AGI of less than $100,000 and a 25% marginal tax rate. During the year, she reports a $36,000 loss from Activity A and a $24,000 loss from Activity B. Additionally, Activity A generates $8,000 of tax credits. Both activities A and B are passive real estate rental activities in which Anita actively participates and owns over 10% of each activity. a. How much loss can be recognized from each activity?b. What is the amount of Aretha's suspended loss from each activity?c. How much of the tax credits can be applied this year?Answer: a. There are losses from each activity, totalling $60,000. Because AGI is less than $100,000, the special rental loss provision will allow the deduction of losses up to $25,000. The $25,000 deduction is first allocated to the losses. Because the sum of the losses ($60,000) exceeds the limit, the deductible loss must be allocated ratably between the activities as follows:

Activity A: $25,000 × $36,000 = $15,000$60,000

Activity B: $25,000 × $24,000 = $10,000$60,000

b. Activity A has a suspended loss of $21,000 (36,000 - $15,000), and Activity B has a suspended loss of $14,000 ($24,000 - $10,000). c. Because the activities are utilizing the full $25,000 loss ceiling, the credits cannot be applied this year. Activity A has $8,000 of suspended tax credits.Page Ref.: I:8-14 through I:8-16; Example I:8-18Objective: 3

94) Wes owned a business which was destroyed by fire in May 2012. Details of his losses follow:

Adj. FMV FMV Insurance Asset Basis Before After Reimbursement

A $1,000 $2,000 $ 0 $2,000B 15,000 10,000 3,000 2,000C 2,400 5,000 2,500 1,000

His AGI without consideration of the casualty is $45,000.

What is Wes's net casualty loss deduction for 2012?Answer: Asset A: $1,000 basis - $2,000 insurance = $ 1,000 gainAsset B: $7,000 loss in value - $2,000 insurance = ( 5,000) lossAsset C: $2,400 basis - $1,000 insurance = ( 1,400) lossFor AGI deduction ($5,400) lossPage Ref.: I:8-19 and I:8-20Objective: 4

26Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

95) Determine the net deductible casualty loss on the Schedule A for Alan Michael when his adjusted gross income was $40,000 in 2012 and the following occurred:

Adj. FMV FMV Insurance Asset Basis Before After Reimbursement

A $1,200 $2,000 $ 500 $ 100B 14,000 12,000 5,000 1,100C 600 3,000 2,775 125

A and B were destroyed in the same casualty in March. C was destroyed in a separate casualty in July.

All casualty losses were nonbusiness personal use property losses and none occurred in a federally declared disaster area.

What is the amount of the net deductible casualty loss?Answer: March casualty: A: Loss is lesser of basis or loss in value $ 1,200

Less: Insurance reimbursement ( 100) $1,100

B: Loss is lesser of basis or loss in value$7,000 Less: Insurance reimbursement ( 1,100) $5,900

Loss before $100 floor $7,000 Less: $100 floor 100 Casualty loss from March casualty $6,900

July casualty: C: Loss is lesser of basis or loss in value $ 225 Less: Insurance reimbursement ( 125) $ 100 Less: $100 floor ( 100)Casualty loss from July casualty $ 0

Total loss before 10% AGI $6,900 10% AGI 4,000 Net deductible casualty loss $2,900 Page Ref.: I:8-21Objective: 4

27Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

96) Frank loaned Emma $5,000 in 2010 with the agreement that the loan would be repaid in three years. In 2011, Emma filed for bankruptcy and based on available information from the bankruptcy court, it was estimated that Frank could expect to receive $.65 on the dollar. In 2012, final settlement was made and Frank received $600.a. Assuming the loan is a business bad debt, what is the amount of and the nature of Frank's deduction in 2011?b. Assuming the loan is a business bad debt, what is the amount of and the nature of Frank's deduction in 2012?c. Assuming instead that the loan is a nonbusiness bad debt, what is the amount of and the nature of Frank's deduction in 2011? 2012?Answer: a. 2011 deduction--$1,750 ordinary loss ((1.00 - .65 = .35 expected loss rate) × $5,000 loan))b. 2012 loss--$2,650 ordinary loss ($5,000 loan - $1,750 prior year deduction - $600 recovery)c. In 2011, the loss is partially worthless, so no deduction is allowed until settlement has occurred. In 2012, the $4,400 short-term capital loss ($5,000 loan - $600 recovery) will be netted against other capital gains and losses. If there are no other capital gains and losses, the loss is limited to the $3,000 current deduction.Page Ref.: I:8-26 through I:8-28Objective: 5

28Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

97) Becky, a single individual, reports the following taxable items in 2012:

Gross income from business $ 93,000 Minus: Business expenses ( 105,000)

($ 12,000)Interest income 1,500 AGI ($ 10,500)Greater of:Itemized deductions:Interest expense $ 3,000State Income Taxes 2,000Casualty 3,000Total itemized deductions ( 8,000)Minus: Personal exemption ( 3,800)Taxable income ($22,300)

What is Barbara's NOL for the year?Answer: Taxable income ($22,300)Plus: Nonbusiness deductions:Itemized deductions $ 8,000 Minus: Casualty loss ( 3,000)

$ 5,000 Minus: Nonbusiness income:

Interest income (1,500)Plus: Excess of nonbusiness deductions

over nonbusiness income 3,500 Plus: Personal exemption 3,800 Net operating loss ($15,000)Page Ref.: I:8-31; Example I:8-41Objective: 6

29Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

98) Harley, a single individual, provided you with the following information for this year:

Income:Salary from part-time employment $ 16,000 Interest income from savings 1,000Net long-term capital gain from investment property 3,000

Deductions:Net business loss(sales of $100,000 less expenses of $130,000) ($30,000)Personal exemption ( 3,800)Standard deduction ( 5,950)Net-operating loss carryover from last year ( 3,000)

What is the amount of Harley's net operating loss for this year?Answer: Salary from part-time employment $ 16,000 Interest income from savings 1,000 Net long-term capital gain from inv. property 3,000 Subtotal 20,000 Net business loss (30,000)Personal exemption ( 3,800)Standard deduction ( 5,950)Net-operating loss carryover from last year ( 3,000) ( 42,750)Taxable Income (22,750)NOL Deduction + 3,000 Excess of non-business deductions over non-business income ($5,950-4,000) 1,950 Exemption 3,800 Net Operating Loss ($14,000)

Page Ref.: I:8-30 through I:8-33; Example I:8-42Objective: 6

99) Businesses can recognize a loss on abandoned property. What types of factors would indicate that property had been abandoned?Answer: 1. Worthlessness of the property2. The property is not worth placing into a serviceable condition3. If it is depreciable property, taxpayer must physically abandon property.Page Ref.: I:8-3Objective: 1

30Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

100) What must an individual taxpayer prove to receive a worthless security deduction?Answer: 1. Security is completely worthless2. Security became worthless during the current tax yearPage Ref.: I:8-3 and I:8-4Objective: 1

101) Erin, a single taxpayer, has 1,000 shares of 1244 stock she purchased directly from AAA Corporation for $120,000 five years ago. The stock has a FMV of $30,000, and Erin is thinking of selling the stock. She has no other capital gains or losses for the year. Discuss the tax consequences and planning opportunities relating to selling the stock?Answer: A single taxpayer may deduct up to $50,000 as an ordinary loss when Section 1244 stock is sold at a loss. To maximize the benefit, Erin should consider selling part of the stock this year (enough to generate a $50,000 loss) and selling the remainder next year. By splitting the sale, she will be able to convert all of the $90,000 loss to an ordinary loss and maximize the tax benefits. Ordinary loss treatment is preferable to capital loss treatment since Erin has no other capital gains and losses and the net capital loss deduction is limited to $3,000 per year. Non-tax considerations include Erin's need for the sale proceeds currently as well as the time value of money and the risk of further losses on the stock.Page Ref.: I:8-5Objective: 2

102) Why was Section 1244 enacted by Congress? Specifically, consider and discuss some of the individual qualifying requirements of Sec. 1244.Answer: Sec. 1244 was enacted in order to encourage investment in small business enterprises. By allowing an ordinary (instead of a capital) deduction a tax break is given to individuals and partnerships when they sell stock in small new enterprises that suffer reductions in stock equity. In order for stock to qualify under Sec. 1244:-The stock must be owned by an individual or partnership.-The stock must have been originally issued by the corporation to the shareholder.-The corporation must be a domestic corporation.-The stock must have been issued for cash or property other than stock or securities.-More than 50% of the gross receipts must be from sources other than passive income during the five preceding years.-Paid in capital did not excess $1 million at the time of stock issuance.Page Ref.: I:8-5 and I:8-6Objective: 2

103) Why did Congress enact restrictions and limitations on losses from passive activities?Answer: If there were no restrictions or limitations on passive losses many taxpayers would engage in passive activities for a tax shelter. These tax shelters would create deductions and credits from passive activities to offset and sometimes eliminate income from active business activities, which is what Congress is trying to prevent.Page Ref.: I:8-7Objective: 3

31Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

104) What is required for an individual to be considered as actively participating in a real estate activity for purposes of utilizing the $25,000 ceiling on rental real estate losses?Answer: The taxpayer must participate in making management decisions or arrange for others to provide services in a significant and bona fide sense. Some of these management decisions include approving new tenants, deciding on rental terms, and approving expenditures. This is a lower level of participation than material participation.Page Ref.: I:8-15Objective: 3

105) What is or are the standards that must be present to warrant a casualty loss deduction?Answer: 1. The loss must arise in an identifiable event2. The event is sudden or unexpected or unusualPage Ref.: I:8-17Objective: 4

106) A taxpayer suffers a casualty loss on personal-use property for which he has insurance coverage. However, to avoid a premium adjustment, the taxpayer fails to make a timely claim. In this situation is the full deduction for the casualty, after the normal floors, available to the taxpayer? Why or why not?Answer: No deduction is allowed. Sec. 165(h)(4)(E) states that a timely insurance claim is required for a casualty loss on personal-use property to be deductible.Page Ref.: I:8-22Objective: 4

107) If a loan has been made to a related party, what are some considerations for determining whether the loan is a bona fide debt or is, in fact, merely a gift?Answer: Consider whether there is a written instrument to indicate evidence of an obligation to repay. Is there a definite schedule of repayment? Consider whether a reasonable rate of interest has been imposed. Also, determine whether an unrelated party would make a similar loan.Page Ref.: I:8-24 and I:8-25Objective: 5

108) Distinguish between the accrual-method taxpayer and the cash-method taxpayer with regard to basis in a receivable.Answer: An accrual-method taxpayer reports income in the year services are performed or property is provided. Thus the accrual-method taxpayer has a basis in a receivable equal to the amount included in gross income.

A cash-method taxpayer reports income only in the year in which payment is received. Thus, if a receivable is an open account item, a cash-method taxpayer reports no income until the receivable is collected. Because no income is reported until the receivable is collected, there is no basis in the receivable.Page Ref.: I:8-26Objective: 5

32Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall

109) What are some factors which indicate that a debt may be worthless?Answer: 1. Bankruptcy of the debtor.2. Death or disappearance of the debtor.3. Repeated unsuccessful attempts at collection.Page Ref.: I:8-26Objective: 5

110) If an NOL is incurred, when would a taxpayer elect to forgo the carryback period and only carry the loss deduction forward?Answer: The taxpayer should elect to forgo carryback if the marginal tax rate in future years is expected to be higher than the marginal tax rate in carryback years.

General business and other tax credits may be reduced by an NOL carryback because these credits must be recomputed based upon the adjusted tax liability after the NOL carryback.Page Ref.: I:8-34Objective: 7

111) How is a claim for refund of taxes filed by an individual who carries an NOL deduction back to a prior year?Answer: A claim for refund of taxes is filed by either filing an amended return on Form 1040X or filing for a quick refund on Form 1045. If Form 1045 is used, the IRS must act on the application for refund within 90 days from the later of (1) the date of the application or (2) the last day of the month in which the return of the loss year must be filed. Form 1045 must be filed within a year after the end of the year in which the NOL arose.Page Ref.: I:8-35Objective: 8

33Copyright © 2013 Pearson Education, Inc. publishing as Prentice Hall