Income Computtion and Disclousure Standard

18

ICDS (Income Computation and Disclosure Standard Student of BMU Rohtak By :- NEERAJ SINDHU B.tech, MBA (Finance & Marketing)

-

Upload

neeraj-sindhu -

Category

Economy & Finance

-

view

63 -

download

3

Transcript of Income Computtion and Disclousure Standard

ICDS (Income Computation and

Disclosure Standard

Student of BMU Rohtak

By :-NEERAJ SINDHU

B.tech, MBA (Finance & Marketing)

ICDS

Introduction of ICDS

Ten- Income computation and disclosure standards have been introduced by Central Board of Direct Taxes (CBDT) on 31-March 2015 by Notification No. 33/2015 dated 31/03/2015 under the provisions of section 145(2) 0f the Income Tax, 1961.

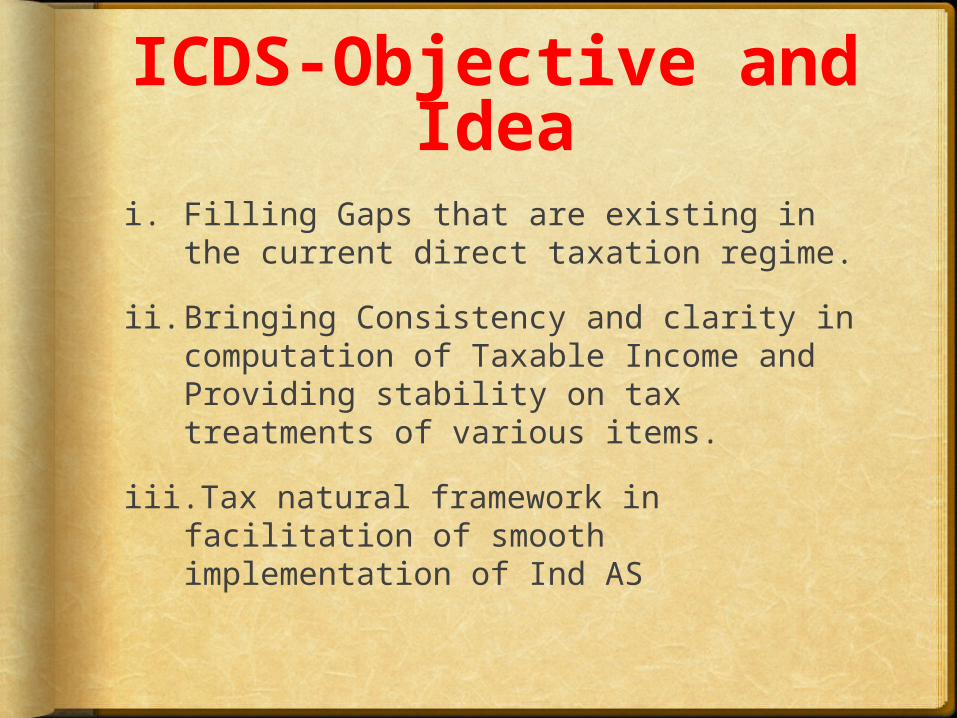

ICDS-Objective and Idea

i. Filling Gaps that are existing in the current direct taxation regime.

ii. Bringing Consistency and clarity in computation of Taxable Income and Providing stability on tax treatments of various items.

iii. Tax natural framework in facilitation of smooth implementation of Ind AS

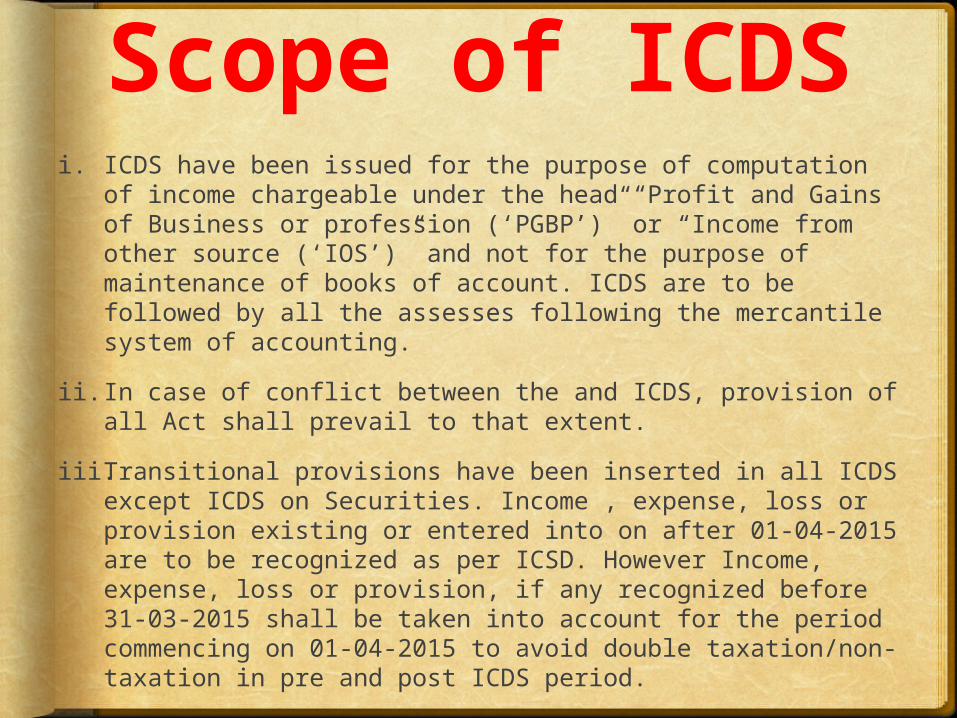

Scope of ICDSi. ICDS have been issued for the purpose of computation of

income chargeable under the head “Profit and Gains of Business or profession (‘PGBP’)” or “Income from other source (‘IOS’)” and not for the purpose of maintenance of books of account. ICDS are to be followed by all the assesses following the mercantile system of accounting.

ii. In case of conflict between the and ICDS, provision of all Act shall prevail to that extent.

iii. Transitional provisions have been inserted in all ICDS except ICDS on Securities. Income , expense, loss or provision existing or entered into on after 01-04-2015 are to be recognized as per ICSD. However Income, expense, loss or provision, if any recognized before 31-03-2015 shall be taken into account for the period commencing on 01-04-2015 to avoid double taxation/non-taxation in pre and post ICDS period.

List of ICDSsICDS I•Accounting polices (AS-1)

ICDS II•Valuation of

Inventories

(AS-2)

ICDS

III•Constr

uction

Contra

cts

(AS-7)

ICDS IV •Revenue Recognition (AS-9)IC

DS

V•Ta

ngi

ble

Fixed

Asset

s (A

S-

10)

ICDS VI•The effects of Changes in Foreign Exchange Rates (AS-11)

ICDS VII•Gover

nment

Grants (AS-

12)

ICDS VIII

•Secu

rities

(AS-

13)

ICDS IX

•Borrowing Costs

(AS-16)

ICDS X

• Provisi

on,

Contin

gent

Liabili

t

ies

and

Contin

gent

Assets

(AS-

29)

ICSD I Relating to Accounting Policies

Marked to Market Loss or an expected loss shall not be recognised unless the recognitions of such loss is in accordance with the provision of any other ICDS.

Accounting polices shall not be changed without reasonable case.

ICSD II relating to Valuation of Inventories

Unlike AS-2, Standard costing method has not been prescribe to measure cost.

ICDA provide for valuation of inventories in the case of service provide are materials or surplus to be consumed in rendering of service .

Method of valuation of inventory once adopted cannot be changed , unless there is a reasonable cause for doing .

In case of dissolution of a partnership firm or association of person (AOP) or Body of individual value of inventories shall be the net realizable value on the date of dissolution.

ICDS III relating to construction contract

Contract revenue is to be recognized when there is reasonable certainty of its ultimate collection.

Contract revenue shall comprise of (a) initial amount of revenue agreed in the contract including retention and (b) variation in the work , claims and incentive payments if it can be measure reliably.

Contract revenue already recognized as income is to be written off as bad debt (and not as an adjustment of the amount of contract revenue)if the collection of that revenue later becomes uncollectible.

Contract costs shall not be reduced by any incidental income being in the nature of interest, dividend and capital gains. The same shall be separately chargeable to tax.

ICDS IV relating to Revenue Recognition

Revenue service contract only to be recognized on percentage completion method as against AS9 revenue recognition where both completed service contract method and percentage completion method is permitted for recognition of revenue from service contract.

Disclosure requirements similar to construction have been prescribed from services contract.

ICDS V relating to tangible fixed assets

In case of acquisition of a tangible fixed asset in exchange for another asset , shares, or other securities the fair value of the tangible fixed asset so required shall be its actual cost .

There is not concept of revaluation of asset in the ICDS . The same is in conformity with the provision of the act wherein also the concept of revaluation of assets is not recognised.

ICDS prescribes disclosure requirement similar to requirement of tax audit report . Even the person not subject to tax audit have to company with such disclosure requirement.

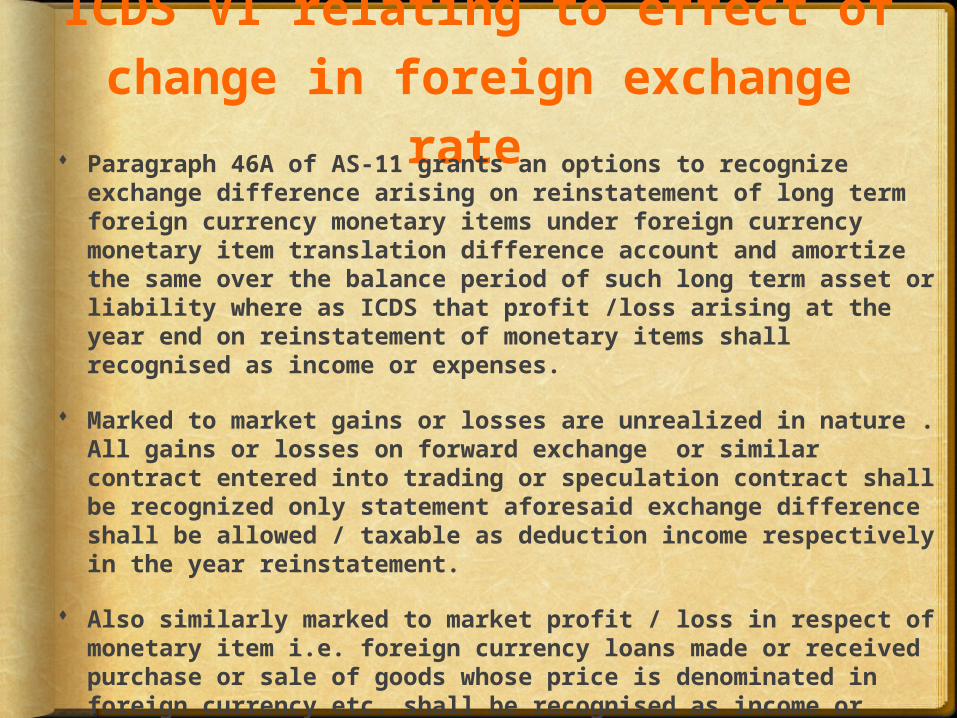

ICDS VI relating to effect of change in foreign exchange

rate Paragraph 46A of AS-11 grants an options to recognize exchange difference arising on reinstatement of long term foreign currency monetary items under foreign currency monetary item translation difference account and amortize the same over the balance period of such long term asset or liability where as ICDS that profit /loss arising at the year end on reinstatement of monetary items shall recognised as income or expenses.

Marked to market gains or losses are unrealized in nature . All gains or losses on forward exchange or similar contract entered into trading or speculation contract shall be recognized only statement aforesaid exchange difference shall be allowed / taxable as deduction income respectively in the year reinstatement.

Also similarly marked to market profit / loss in respect of monetary item i.e. foreign currency loans made or received purchase or sale of goods whose price is denominated in foreign currency etc. shall be recognised as income or expenses.

Premium or discount on forward exchange contracts shall be recognised as income or expenses on amortisation basis over the life of the contract.

ICDS VII relating to government grants

Grants in respect of depreciable fixed asset is to be reduced from actual cost of such assets. This treatment is similar to explanation 10 to sec 43(1). How ever AS 12 prescribes that the same may either be adjusted with the value of assets or recognized as income on reasonable basis over a period of time.

Additional disclosure are required to be made for each pervious year which inter-alia includes nature & extent of grants reduces from the block of asset, grants not reduce from the block of assets with reasons & grants not recognized as income with reasons.

ICDS VIII relating to securities

This ICDS deals with securities held as stock in trade and not for securities held as investment .

Where a securities is required in exchange for another security , cost shall be fair value of the security acquired.

Securities listed on a recognized stock exchange shall be actual cost initially recognized or net realizable value, whichever is lower.

Securities not listed on a recognized stock exchange shall be valued at actual cost as initially recognized.

ICDA XI relating to Borrowing cost

This ICDS deals with borrowing cost other than relating to exchange differences arising from foreign currency borrowings. The same will be treated in terms of ICDS on The effect of changes in foreign exchange rate.

Borrowing coat is respect of borrowing partly used for acquisition of the qualifying asset to be capitalized in accordance with the following formula:

(A)*(B)/(C)

(A) borrowing cost except directly relatable to specific purpose .

(B) average cost of qualifying asset at the first day of the pervious years and

(C)average cost of asset at the first day and the last day of the pervious year.

Unlike AS 16 , suspension of capitalization of borrowing cost is not covered in the ICDS.

ICDS X relating to provision,

contingent liabilities &contingent

assets AS 29 requires the recognition of a provision

when it is probable that there will be outflow of resource. However , under ICDS provision is to be recognized when there is reasonable certainty (more likely than not ) for the out flow of resources.

Comparison of ICDS, IndianGAAP and Ind AS

ICDS Income Computation and Disclosure Standards issued by the CBDT on 31 March 2015

Ind AS Indian Accounting Standards notified by the MCA on 16 February 2015

AS Indian Accounting Standard(s) Notified under the Companies (Accounting Standards) Rules, 2006

![DRAFT INCOME COMPUTATION AND DISCLOSURE ... Releases...2015/01/08 · Income Computation and Disclosure Standard [ICDS] Accounting Policies Preamble This Income Computation and Disclosure](https://static.fdocuments.us/doc/165x107/6083f1186324d247d57da594/draft-income-computation-and-disclosure-releases-20150108-income-computation.jpg)

![DRAFT INCOME COMPUTATION AND DISCLOSURE …2).pdfIncome Computation and Disclosure Standard [ICDS] Accounting Policies Preamble This Income Computation and Disclosure Standard is applicable](https://static.fdocuments.us/doc/165x107/5f93ba5c79d5986f47034079/draft-income-computation-and-disclosure-2pdf-income-computation-and-disclosure.jpg)