Income Computation & Disclosure Standards PPT dtd 19.08.2017.pdf · Methodology of MAT Computation...

43

Income Computation & Disclosure Standards CA Gaurav Makhijani

-

Upload

nguyendung -

Category

Documents

-

view

215 -

download

1

Transcript of Income Computation & Disclosure Standards PPT dtd 19.08.2017.pdf · Methodology of MAT Computation...

Income Computation & Disclosure Standards

CA Gaurav Makhijani

Agenda

ICDS – A brief overview

Critical analysis of ICDS

• ICDS V (Tangible Fixed Assets)

• ICDS VI (Effects of changes in foreign exchange rates)

• ICDS VIII (Government Grants)

• ICDS X (Provisions, Contingent liabilities and Contingent assets

ICDS - A Brief Overview

ICDS – A Brief Overview

10 ICDS have been notified by CBDT - effective from April 1, 2016 (i.e. FY 2016-17)

Applicable to all tax payer(s)1 following mercantile system of accounting with respect to PGBP and IOS

For applicability of ICDS - no minimum threshold or exemption granted

Objective of ICDS - To provide consistency in accounting procedures while computing taxable income and to reduce tax litigation

No separate books of accounts are required to be prepared by a Taxpayer

Methodology of MAT Computation continues to be same - based on ‘book profits’

Reporting required in TAR

1 Except Individuals and HUFs not liable for tax audit u/s 44AB

Section 145 a computation mechanism and not a charging section – held by SC in

− A krishnaswai Mudaliar & others (53 ITR 122)

− Standard Triumph (67 Taxman 160)

Under Section 145, the Assessee’s regular method of accounting determines the mode of computing the taxable income but it does not determine or even affect the range of taxable income or the ambit of taxation - SC in the case of State Bank of Travancore (158 ITR 102)

ICDS has been notified u/s 145 - Is Section 145 a “Charging Section” ?

Whether ICDS is only a computation provision and not a charging provision ?

Does ICDS override the Act ?

Held by Various courts Remarks

Rules can be resorted to for the purpose of construing the provisions of a statute only where the provisions are ambiguous / doubtful and a particular construction has been put upon the statute by the rules -Delhi HC in the case of All India Lakshmi (150 ITR 1)

In case of existing differing views regarding provisions of the Act, ICDS may have persuasive value with regard to transactions on or after April 1, 2016

Rules made under the Act must be treated as if they are in the Act and have the same force as the Sections in the Act – SC in the case of Ajanta Elec (215 ITR 114, 119)

Although ICDS must be treated as a part of the Act, it remains a delegated legislation

No exercise of rule-making power can affect, control, enlarge or detract full operative effect of provisions of the Schedules / Sections; any rule that purports to do so would be ultra vires and void even though the Statute provides that it shall have the effect as if enacted in that Statute –SC in the cases of Chenniappa (74 ITR 41), Ajanta Elec (215 ITR 114) and Bombay HC in the case of K. T. Udeshi (114 ITR 542)

ICDS cannot affect, control, enlarge or detract full operative effect of provisions of the Act

Does ICDS override the Act?

Held by Various courts Remarks

A notification that has the effect of curtailing the scope of a deduction granted under the Act or imposing a tax without authority of law will be invalid – SC in the case of Sirpur Paper (237 ITR 41)

ICDS cannot curtail a deduction or impose tax

As far as possible the Act should be construed in such a way as to reconcile various provisions and unravel apparent conflict into harmony, bearing in mind that a general provision cannot derogate from a special provision regarding a certain class of cases – various HC cases

ICDS and other provisions of the Act must be read harmoniously

Act and ICDS must be read harmoniously

Preamble to ICDS

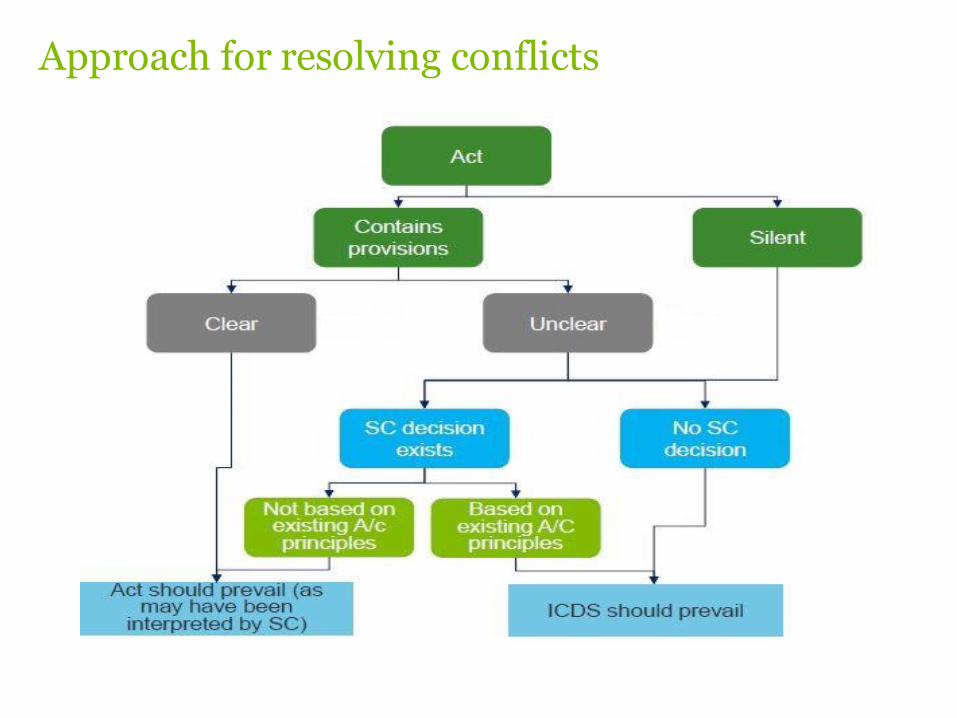

“In case of conflict between the provisions of Act and ICDS, the provisions of the Act shall prevail to that extent”

If Act contains a provision and the same is clear, Act shall prevail over ICDS. What if Act is silent or unclear ?

Supreme Court judgement – Law of Land

Supreme Court is the law of the land since Article 141 of the Constitution provides that the Law declared by the Supreme Court is binding on all Courts within the territory of India

Following SC cases lay down this principle:

U.P. Pollution Control Board vs Kanoria Industrial Ltd. (259 ITR 321)

Shenoy And Co. vs The Commercial Tax Officer (1985 SCR (3) 659)

Assistant Collector Of Central vs Dunlop India Ltd. And Ors (1985 SCR (2) 190 SC)

Based on above, Supreme court’s judgments' declares the Act as it always stood

Approach for resolving conflicts

Critical analysis of ICDS

ICDS V: Tangible Fixed Assets

Covers assets (such as land, building, machinery, plant, furniture) held with an intention of being used for producing goods / providing services.

Not applicable to assets held for sale in normal course of business. Expenditure on software – revenue vs. capital ?

Tangible fixed asset to be recorded at actual cost including purchase price, taxes (excluding those that are recoverable) and any other direct cost for making the asset ready for its intended use

Stand-by equipment and service equipment to be capitalized

Spares / consumables need to be expensed-off

If connected with a particular fixed asset and used irregularly - to be capitalized

In case of assets exchanged, fair value of cost of asset “acquired” needs to be considered

Consolidated price for acquiring group of assets shall be apportioned on fair basis

ICDS V: Tangible Fixed AssetsHighlights

MasterMaster

Cost of improvement (which increases the previously assessed level of performance) to be capitalized, otherwise to be expensed-off

What about minor improvement or repairs (such as, replacement of computer RAM or hard disk) ?

What about major inspection costs (such as, aircraft interiors) ? Under Ind-AS such inspection costs to be capitalized if recognition criteria is met.

Depreciation and capital gain on transfer of asset will be as per the Act

Only deals with tangible fixed assets. Unlike AS-10, it does not provide for ‘Goodwill’

Revaluation of assets not permitted under ICDS

Silent on decommissioning, restoration and similar liabilities. Under Ind-AS such costs to be capitalized.

ICDS V: Tangible Fixed AssetsHighlights

Actual cost defined u/s 43(1); depreciation to be computed u/s 32; and capital gains to be computed u/s 45. Limited purpose is served by ICDS V (Tangible Fixed Assets).

Expenditure on start-up and commissioning of a project to be capitalized [Para 8 ICDS V- refer Appendix]

Expenditure post commencement of commercial production to be expensed-off

Treatment of costs for time period between trial run and commencement of commercial production is unclear

1 Also held by Gujarat HC in the case of Saurashtra Cement (127 ITR 47), Delhi HC in the case of Food Specialities (136 ITR

203), Bombay HC in the case of G T Industries (203 ITR 538)

2 On a combined reading of ICDS, a view emerges that expense incurred during the period between trial run and commercial production may have to be capitalized. Also, stands clarified vide Ques No. 15 of the FAQs issued by CBDT on 23.03.2017

ICDS V: Tangible Fixed Assets

Construction / acquisition of asset

Trial run – ready to use

Commercial

production

Capitalize as per ICDS 1 Revenue as per ICDS

Capitalize or revenue expense? 2

Initial Cost of starting the project

ICDS VI: Changes in Foreign Exchange Rates

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Scope

Enterprise carrying activities involving foreign exchange

Treatment of transactions in foreign

currencies

Translating financial statements of foreign

operation

Treatment of foreign currency transactions

in the nature of forward exchange

contracts

Like other ICDS - applicable only for computation of income chargeable under the head ‘PGBP’ or ‘Other Sources’

Foreign currency translation

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Some important terms

Foreign currency transaction

A transaction which is denominated in or requires settlement in a foreign currency, including transactions arising when a person :-

(i) Buys or sell goods or services whose price is denominated in a foreign currency; or

(ii) Borrows or lends funds when the amount payable or receivable are denominated in a foreign currency; or

(iii) Becomes party to an unperformed forward exchange contracts; or

(iv) Otherwise acquires or disposes of assets, or incurs or settles liabilities, denominated in a foreign currency.

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Some important terms

Monetary Items

• Means the money held and assets to be received or liabilities to be paid in fixed or determinable amount of money.

• Eg. Cash, receivables, payables, etc.

Non-monetary Items

• Assets & liabilities other than monetary items

• Eg. Fixed assets, inventories, investments in equity shares, etc.

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Initial recognition

Foreign currency amount

Exchange rate at the

date of transaction

Amount in reporting currency

Initial recognition - exchange rate at the “date of transaction”

An average rate for a week or a month might be used for all transactions during that period

o However, if exchange rates fluctuate significantly, the use of exchange rate for a period is unreliable

No key deviation from AS – No change in tax positions

MasterMaster

Monetary items – to be converted by applying “the closing rate”

o Where closing rate does not reflect with reasonable accuracy or is unrealistic – relevantmonetary item shall be converted at the “amount” which is likely to be realized from or requiredto disburse such item at the last date of previous year.

ICDS VI: Changes in Foreign Exchange Rates

Conversion at last date of each previous year

Foreign currency amount

Closing rate Amount in reporting currency

Monetary Items

No key deviation from AS – No change in tax positions

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Conversion at last date of each previous year

Non-monetary Items

Inventory carried at NRV denominated in

foreign currency

Others

Rates that existed when such value was

determined

Rates at the date of transaction

No key deviation from AS – No change in tax positions

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Recognition of exchange difference

Particular On last day of

previous year

On settlement

Monetary items Yes Yes

Non-Monetary items No Yes

Above provisions are subject to section 43A of Act

Financial statements of Financial operations

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Translation

• Translation to be done using the principles and procedures laid down for foreign currency transactions

• Revised ICDS VI has done away with the distinction between Integral and Non-Integral Foreign Operations

MasterMaster

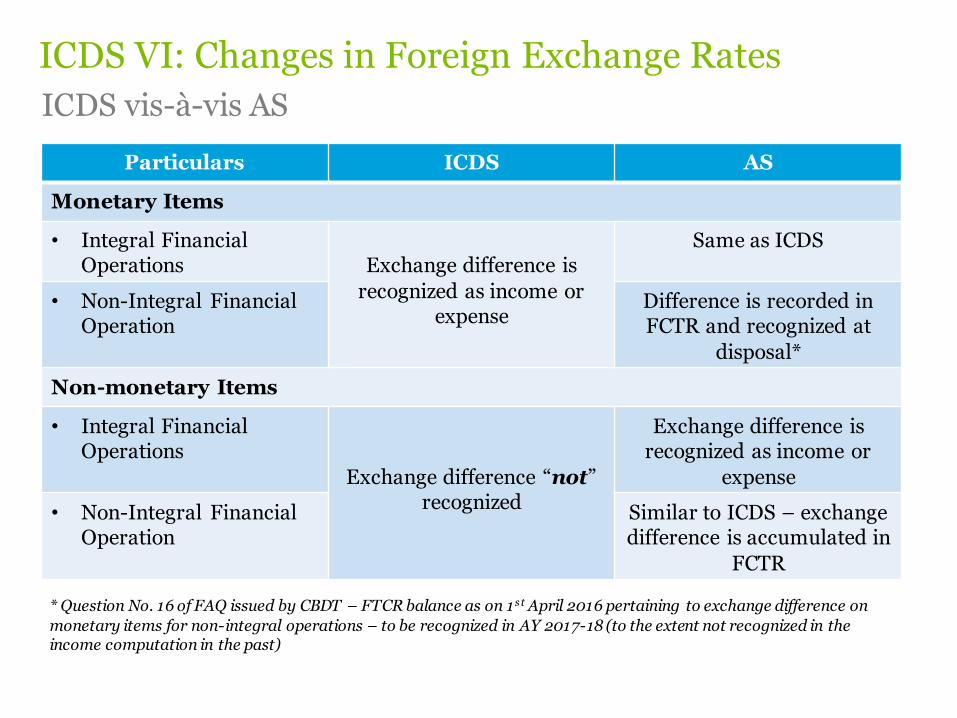

ICDS VI: Changes in Foreign Exchange Rates

ICDS vis-à-vis AS

Particulars ICDS AS

Monetary Items

• Integral Financial Operations Exchange difference is

recognized as income or expense

Same as ICDS

• Non-Integral Financial Operation

Difference is recorded in FCTR and recognized at

disposal*

Non-monetary Items

• Integral Financial Operations

Exchange difference “not” recognized

Exchange difference is recognized as income or

expense

• Non-Integral Financial Operation

Similar to ICDS – exchange difference is accumulated in

FCTR

* Question No. 16 of FAQ issued by CBDT – FTCR balance as on 1st April 2016 pertaining to exchange difference on

monetary items for non-integral operations – to be recognized in AY 2017-18 (to the extent not recognized in the income computation in the past)

Forward exchange contracts

MasterMaster

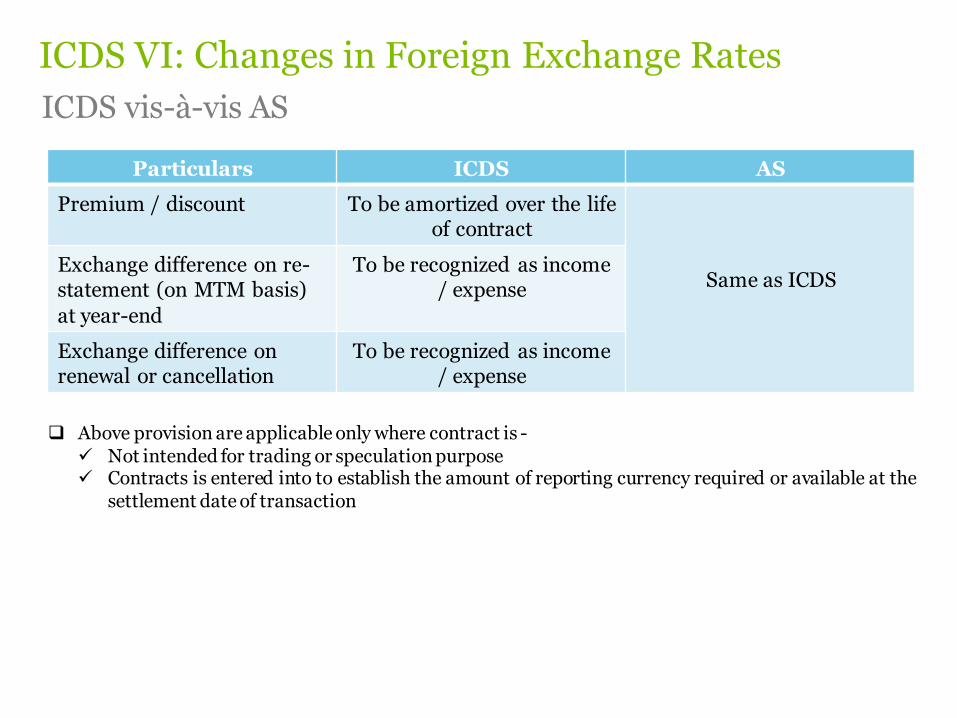

Above provision are applicable only where contract is - Not intended for trading or speculation purpose Contracts is entered into to establish the amount of reporting currency required or available at the

settlement date of transaction

ICDS VI: Changes in Foreign Exchange Rates

ICDS vis-à-vis AS

Particulars ICDS AS

Premium / discount To be amortized over the life of contract

Same as ICDSExchange difference on re-statement (on MTM basis)

at year-end

To be recognized as income / expense

Exchange difference on renewal or cancellation

To be recognized as income / expense

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

ICDS vis-à-vis AS

Forward contract entered

ICDS AS

For trading or speculation purposes

Premium / discount / exchange difference

accounted for on settlement basis

Premium / discount is ignored

MTM gain / losses is

recognized

To hedge firm commitments or a highly probable

transaction

MTM losses are recognized.MTM gains are ignored*

* Under Ind-AS –MTM gain / losses to be recognized as income / expense in OCI

Open issues

MasterMaster

Critical Analysis

ICDS VI: Changes in Foreign Exchange Rates

Open issues

Income / loss needs to be recognized in case of revaluation of loan / payables related to fixed assets(except as covered under Sec 43A)

Whether in case of Indian asset purchased with foreign loan, gain / loss onrevaluation thereof may be recognized in the tax computation ???

Earlier, few courts have held that the same is capital loss / gain and hence, not tax deductible /chargeable to tax.

Treatment of derivatives contract like cross currency swaps, futures, interest rate swaps etc. ???

Under AS - Forward exchange contract means an agreement to exchange different currenciesat a forward rate.

Under ICDS - An agreement to exchange different currencies at a forward rate, and includes aforeign currency option contract or another financial instrument of a similar nature.

Reconciliation of ICDS vis-à-vis AS

MasterMaster

ICDS VI: Changes in Foreign Exchange Rates

Reconciliation of ICDS vis-à-vis AS

Effect of foreign exchange difference on purchase of indigenous assets (not covered under Section 43A)

Transitional provision w.r.t. FCTR balance as on 1 April 2016 and effect of exchange difference on monetary items in case of Non Integral financial operations

Effect of exchange difference on non-monetary items – Integral Financial Operations

Premium / discount / exchange difference on forward contract entered for trading / speculation or for hedging of firm commitments or a highly probable transaction

ICDS VII: Government Grants

MasterMaster

Deals with the treatment of Government grants - does not cover government assistance

Government grants not to be recognized until there is a reasonable assurance that :-

The person shall comply with the related conditions attached; and The grants shall be received

All government grants related to depreciable fixed assets needs to be reduced from cost of the asset

Grants received for a group of assets needs to be apportioned

Grants for compensation of expense / loss or for giving immediate financial support with no furtherrelated costs - to be recognized as income in the year in which it is receivable

In all other cases (including non-depreciable assets) to be recognized as income :-

on upfront basis - if there is no condition attached;or on proportionate basis - over the period of time over which cost of meeting condition is incurred

ICDS VII: Government Grants

Highlights

MasterMaster

ICDS VII: Government Grants

Key deviations from AS

ICDS does not permit the capital approach for recording of government grants as was allowed underIndian GAAP – in line with the amended definition of “income” under section 2(24) of the Act.

Recording grants in the nature of promoter’s contribution or grants related to non-depreciableassets, directly in shareholder’s fund as a capital reserve not permitted

Initial recognition of grant cannot be postponed beyond the date of actual receipt.

ICDS X: Provisions, Contingent liabilities and Contingent assets

MasterMaster

Provision is to be recognized only if there is a ‘reasonable certainty’ that an outflow of resourcesembodying economic benefits will be required to settle the obligation:

obligations should arise out of past event (existing independently of future actions); and in case of a new law yet to be finalized, an obligation arises only when the legislation is enacted.

Contingent liability should not be recognized.

Contingent assets are to be assessed continuously and any assets / related income is to be recognized ifit is “reasonably certain” that an inflow of economic benefits will arise.

Indian GAAP provides for the test of “virtual certainty” for recognition of contingent assets.

Intention appears to bring tax treatment of losses and gains at par.

Provision and contingent assets are to be reviewed at each year end and reversed if they do not meetrecognition criteria.

ICDS X: Provisions, Contingent liabilities and

Contingent assets

Highlights

MasterMaster

Unlike Indian GAAP, ICDS-X does not cover provisions for onerous contracts.

Accordingly, no upfront provision of onerous contract may be allowed in tax computation

Recognition criteria of provision / assets and related income in the ICDS is based on “reasonablecertainty”

Indian GAAP requires “probable certainty” for provision and “virtual certainty” for assets /related income.

The term “reasonable certainty” is neither defined in the ICDS nor in the Act - may become difficult toclaim such provision created for an expenditure which was otherwise allowable as per earlier judicialprecedents.

ICDS X: Provisions, Contingent liabilities and

Contingent assets

Key deviations from AS

Certainty Pre ICDS Post ICDS

Income Expense Income Expense

Probable Certainty - Recognize N.A. N.A.

Reasonable Certainty N.A. N.A. Recognize Recognize

Virtual Certainty Recognize - N.A. N.A.

Questions……

Appendix

Para 8 of ICDS V

Para 8 - The expenditure incurred on start‐up and commissioning of the project, including the expenditure incurred on test runs and experimental production, shall be capitalized.

The expenditure incurred after the plant has begun commercial production, that is, production intended for sale or captive consumption, shall be treated as revenue expenditure.