Incapacity Planning in Your South Carolina Estate Plan

25

IN YOUR SOUTH CAROLINA ESTATE PLAN

Transcript of Incapacity Planning in Your South Carolina Estate Plan

IN YOUR SOUTH CAROLINA ESTATE PLAN

If you are 20 years old right now you stand a 1 in 4 chance of suffering a period of disability before you reach retirement age

About 12% of the population is considered disabled

Half of all disabled individuals are under retirement age

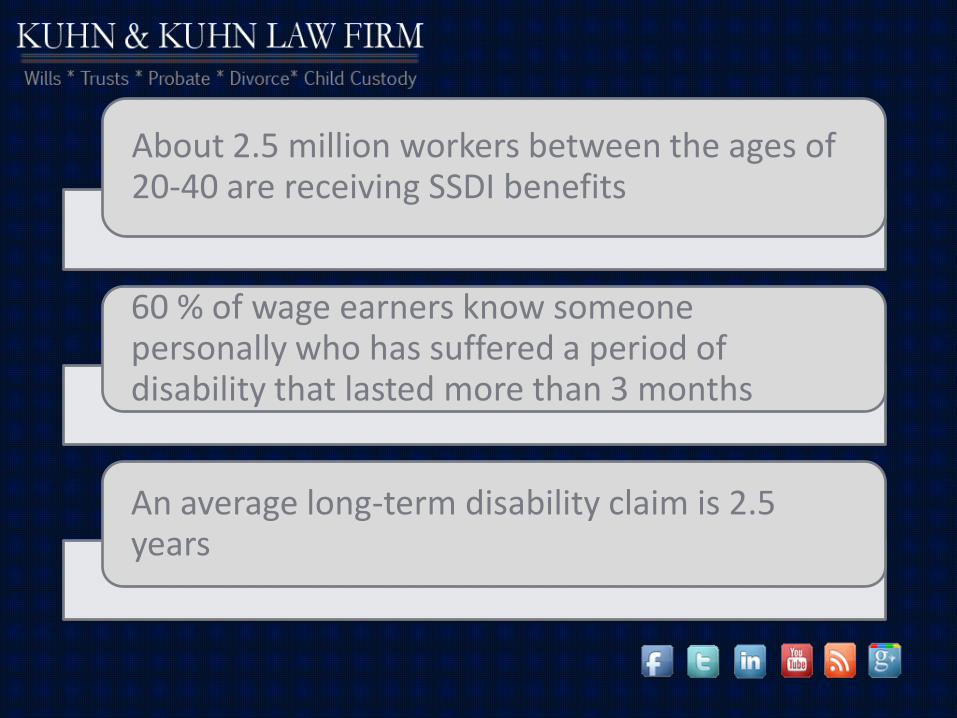

About 2.5 million workers between the ages of 20-40 are receiving SSDI benefits

60 % of wage earners know someone personally who has suffered a period of disability that lasted more than 3 months

An average long-term disability claim is 2.5 years

1 out of every 8 workers will be disabled for 5 years or longer during their working years

1 in 3 seniors dies with Alzheimer’s or another dementia disease

Alzheimer’s is the 6th leading cause of death in the United States

Someone will have to make medical decisions for you. Absent a choice made by you prior to your incapacity a court may have to decide who to appoint. Moreover, your wishes with regard to treatment, including end of life care, may not be honored because they are not known.

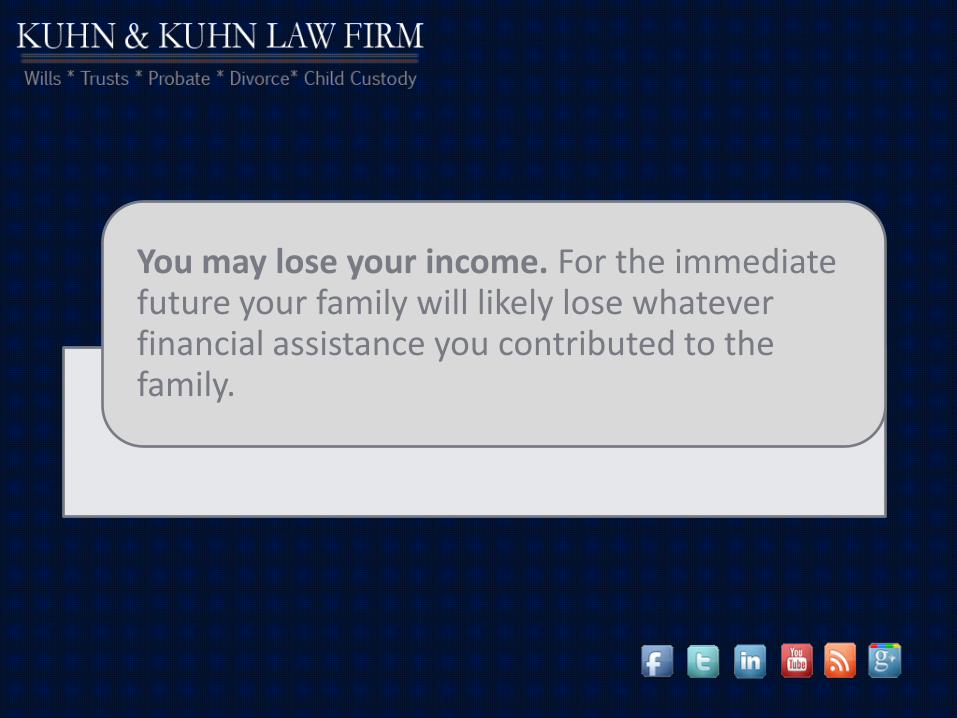

You may lose your income. For the immediate future your family will likely lose whatever financial assistance you contributed to the family.

Someone must take control of your assets and pay your bills. If you failed to legally give someone authority ahead of time a court may have to make the decision. Worse still, your loved ones could end up in a lengthy, and costly legal battle over the right to control your assets during your incapacity.

Everyday decisions must be made for you by someone. Decisions, such as where you will live and what doctor will treat you must be made by someone. Absent a plan the matter may end up before a judge.

o You create the trust and name yourself as the Trustee

o You appoint a spouse/parent/adult child as the successor Trustee.

o You then transfer all of your major assets into the trust.

o You control and manage all trust assets as long as you are capable

o If you become incapacitated control automatically shifts to the successor Trustee

Works like this

Most common strategy

Advanced directives – these allow you to appoint an Agent to make healthcare decisions for you should and to make important treatment decisions for yourself now.

Power of attorney – if a POA is a durable POA it will survive your incapacity.

Joint ownership – holding assets jointly means the co-owner will have control over the asset if you are incapacitated.

Disability insurance – short-term disability insurance is often a wise addition to your estate plan as it can cover your family’s immediate cash flow problems until long-term disability benefits kick in.

Kuhn & Kuhn Law Firm