IN - Nelsonville City Attorney | Nelsonville Ohio · lll-ll.ll.- .- RECORD QF R LUTIONS ... Shafer...

76

.................. ............. ..... Resolution No ..... 1005 .......................... Passed N.o~ember ..l4 19 67.. -- -- -- A RESOLUTION AUTHORIZING POLICEMEN AND FIREMEN TO TAKE VACATION PAY IN LIEU OF VACATION TIKE AND TO DECLARE AN ENEMERGENCY Whereas it has been difficult for the City of Nelsonville to employ and maintain . , adequate personnel for the Police Department and Fire Depart- ments and the protection and welfare of the citizenry is placed i n jeopardy in the event said personnel i s not available. BE IT RESOLVED BY THE COUNCIL OF THE CITY OF NELSONVILLE SEGTION 1 - That when in the opinion of the Chief of the Police Department and the Chief of the Fire Department it i s necessary that members of their departments remain on duty rather than take their vacation, the Auditor of the City of Nelsonville i s hereby authorized and instructed, upon certifi- cation by the Chiefs of the Department, to pay to said personnel in lieu of vacation time, the money which they would otherwise have been paid i f such vacation had been taken. SECTION 2 - For the reason that it is necessary to maintain a minimum staff of Police and Firemen to protect the lives and property of the citizens of this City, this Resolution i s declared to be an emergency Resolution neces- sary for the public peace, health and safety and shall take effect forth- with upon i t s adoption. Charles G. Shafer /s/ President of Council PASSED t h i s 1 4 t h day of November, 1966 ATTEST: Patricia A. Stockdale /s/ Clerk of Council APPROVED: November 14, 1966 Earl Hilleary /s/ Mayor

Transcript of IN - Nelsonville City Attorney | Nelsonville Ohio · lll-ll.ll.- .- RECORD QF R LUTIONS ... Shafer...

.................. ............. ..... Resolution No ..... 1005 .......................... Passed N.o~ember . . l4 19 67.. -- -- --

A RESOLUTION AUTHORIZING POLICEMEN AND FIREMEN TO TAKE VACATION PAY IN LIEU OF VACATION TIKE AND TO DECLARE AN ENEMERGENCY

Whereas it has been d i f f i c u l t f o r the City of Nelsonville t o employ and maintain . , adequate personnel f o r the Police Department and F i re Depart- ments and the protection and welfare of the c i t i zenry i s placed i n jeopardy i n the event sa id personnel i s not available.

BE I T RESOLVED BY THE COUNCIL OF THE CITY OF NELSONVILLE

SEGTION 1 - That when i n the opinion of the Chief of the Police Department and the Chief of t he F i re Department it i s necessary t h a t members of t h e i r departments remain on duty ra ther than take t h e i r vacation, t he Auditor of the Ci ty of Nelsonville i s hereby authorized and instructed, upon c e r t i f i - cation by the Chiefs of t he Department, t o pay t o said personnel i n l i e u of vacation time, the money which they would otherwise have been paid i f such vacation had been taken.

SECTION 2 - For the reason t h a t it i s necessary t o maintain a minimum s t a f f of Police and Firemen t o protect the l i v e s and property of the c i t i zens of t h i s City, t h i s Resolution i s declared t o be an emergency Resolution neces- sary f o r the public peace, health and safety and s h a l l take e f f ec t for th- with upon i t s adoption.

Charles G. Shafer /s/ President of Council

PASSED t h i s 14th day of November, 1966

ATTEST: Pa t r i c i a A. Stockdale /s/ Clerk of Council

APPROVED: November 14, 1966

Ear l Hilleary /s/ Mayor

..... l.i,.l......" ...... -. ".-,,-..-" ,,l,...l,lll." .... ii~. .--..-..- ....... "."..A ..... ".A ....... ..-.-.'.~-..l.l.......~..-l..-l...l.--..ll. .... lll-ll.ll.- .-

RECORD QF R LUTIONS

1 0 0 6 Resolution .No ........................................... Passed ............................................ bbmnber 2 9 2 ........................ '1 966 19 .......... -,--p.---,,-.--.-.

A RESOLUTION APPROVING THE COMPLETED PLANNING DOCUMENTS PREPARED WITH AN ADVANCE FROM THE UNITED STATES OF AMERICA UNDER THE TEFMS OF PUBLIC LAW 560, 83RD CONGRESS OF THE UNITED STATES, AS AMENDED

iHF,REAS, the City of Nelsonville, Ohio accepted an of fe r from the United State: ;overnment f o r an advance f o r preparation of planning documents pertaining t o E

mblic work described a s f i n a l planning of additions and improvements t o the ?xis t ing water treatment f a c i l i t i e s including a new raw water intake and a new uell; and

JHEREAS, Floyd G. Browne and Associates, Limited, was engaged t o prepare the ~ lanning documents f o r t he aforesaid public work, and said a rch i tec t and/or 'ngineer has completed documents and submitted them f o r approval; and

JHEREAS, the completed planning documents have been carefu l ly studied and are :onsidered t o conprise adequate planning of the public work essen t ia l t o the :omunity and within the f inanc ia l a b i l i t y of the Ci ty of Nelsonville t o con- struct;

iOW THEREFORE, be it resolved by The Council of the City of Nelsonville the governing body of said applicant, t h a t the planning documents submitted by iloyd G. Browne and Associates, Ltd., as the basis f o r detai led planning ,f t h e improvements t o water treatment f a c i l i t i e s dated November 1966, and the ;tatements i n Form CFA-430, Request for Review and Approval of Planning Docu- nents, i n connection with Housing and Home Finance Agency Project No. P-Ohio- 3228 be and the same are hereby approved; and t h a t c e r t i f i e d copies of t h i s "esolution be f i l e d with the Housing and Home Finance Agency.

LTTEST :

' a t r i c ia A. Stockdale Xerk of Council

1PPROVED: November 29, 1967

Charles G. Shafer President of Council

'uoiqdopo s noc'n i lqriqq.roj q o a j j a aye?. TTBYS pun Rqajns pua g q p a q 'aaaac' oyyqnd ayq

x c j .Lwssaaau uoyqn-josaz XouoY~a~ie un oq 03 p'axnTaap sy uoy$nTosax s ~ y q 'r;qy& ~ q ~ o j Xpn1-s a !h . ra~as aqsnbapo 203 a p j ~ o x d 0% X ~ o s s a o o u sy $7 pun X ? . J U ~ U I U I O ~ aqq ?? u.zaouoa qsomqn sqq ;yo sy u m ~ 2 o ~ c I syq: qsq9 uosoa.r sqq JOJ .& N C I ~ ~ ~ S

' U? i aq p w n p o ~ d a x XTTnj q3noyq s.e ;oaJey +xnd s apau pus oqa.say payou+qo sy y33q!~ j o Xdoo n ' a ~ o ~ a ~ a t j $ 9 u ~ p j n o ~ d ~uawaax9u ujuqaao 8:qq.j~ e 3 u v ~ ~ o o o n UJ m v ~ 3 o ~ d

p l s s a a o j s ayq 0% oauaJa jaJ y a p Suy~aauy2ue ~ u u B u ~ u u u ~ d X ~ o s s a a a u nya aqq ; rapun oq ' o ~ u o ' u o y ~ u y ~ ' s x a a u j 4 u ~ 3 u ~ q ~ n s i . 1 0 3 ' .sq1 'saqnyoossy :a uN~oxg

'0 pXo~d Xo~dua & ~ a y saop 7.1 pun 'Xo-~.dua -[Jouno3 syyq ? . n u 'T NOIJ,~S

!uaqsXs a%btAag Xxn$?ua~ s,X?.y3 aqq oq suoyqyvpa ~ u u squamano~dwy p y u s a x o p ayq x o j saqomryJe $SOD 'SUBTCI ~ n ~ a u a 3 ' I C B A J ~ S 2 u ~ ~ a a u r l i u a aqq

a o j s x a a u ~ l ? u a p u o y s s a j o ~ d pa.ra$s~Zax Xo~dwa 0% A x n s s a ~ a u s j qy 'suasaq$.

pus 'yq j ~ h a ~ a y uoyqaauuoo uy uoyqao ~ ' y $ o azyJoq3no 0% pus q3v pyss xapun uor? .noj .~ddu uw

a T j j 02 3Tjauoq s q r oq ~ u a qsazaquj orxqnd ay?. u.r aq 03 qy sdapysuoa ~ y o u n o 3 aqq pue $38 qans paaap.ysuoa X p p pus pauTr;wxa svy Trouno3 ayq ' s n a x a y ~

'pus !&aquypawuy uayoq a q s q ~ o u pyos j o uoTqons:suoo ay?. oq Xaouymyfa~d uoy$ow zuyq A ~ u s s a a a u s y qy

pua 3nqq oq puo qsaaaquy o ~ ~ q n c : ayq uy puu aTqw.rysap s r o l e l ay$ s aousua~xndde Fno maqsXg xa&aS X ~ n q y u s ~ s , X q ~ 3 ayq 0% suojqyppn puw quawano~Zmy s a

paqyaosap X y p ~ a u a 3 ' s y ~ o i ~ a ~ ~ q n d uys?.xaD jo uoy$ona$suoo ay$ xwyq paurujo$aF Aqaxay s t y .el-p aTqnTrr+'lu JO Kpnqs FU" wa~qoxd ax$ JO s?.oadsw sno j son ayq

j o uoyqoJapjsuo3 yl::noxoyl xa:p 'oyqo ' a T T ~ n u o s p N jo A373 or{? ' s s a~ay j i ,

.... ........... .... ..................................... Resolution NO ....... 1113 ........................ Passed Yay 8 ., 19 6.7.. .-

SLTTION 1. That on es t imate duly made, moneys 01' tne c i t y , aggregat ing L maximum amount of One Hundrel and Ten Thousand Dol la rs , s h a l l be awarded as .nac t ive deposi ts .

SECTISN 2 . That t n e a c t i v e and i n a c t i v e moneys or' t h e C i ty s h a l l be .eposi teS i n a bsnk or banks a s provided by law.

SECTION 3 . That t h e bank o r bsnks i n t h e C i ty o f fe r ing the h ighes t .ate of i n e r e s t perannum on inac t ive d e p o s i t s be made t h e depos i tory o r Lepositories of such funds of t h e C i t y f o r a period of two years from tine 1 5 t h lay ol' June 1967- I f , howevar, no bank i n t h e C i t y b ids a s a t i s f a c t o r y r a t e tf i n t e r e s t outs ide of t h e Ci ty bidding the h i ~ h e s t r a t e of i n t e r e s t per innurn on i n a c t i v e depos i t s , s h a l l be made t h e ?epas i tory oi' such funds ol' t h e : i t y ; i n t o r e s t on i n a c t i v e d e o o s i t s t o be ? a i l q u a r t e r l y and conpute? from ;he d a t e of depos i t .

SZCTI311 4,. That b ids be rece ived u n t i l 7 : O O o k l o c k P. M.., on t h e 13th day of June 1967, pnd t h a t no t i ce t o a l l banks i n t h e C i ty and such other ~ a n k s a s may be necessary be given by p i b l i c a ~ i o n a s provided by law. The : i t y r e se rves t h e r i g h t t o r e j e c t any o r a l l b i l s .

SZCTICN 5. That b ids f o r a c t i v e depos i t s be rece ived a t tine same :ism and place as b ids f o r i nac t ive 'deposits an$ ti..: awards made.

SECTION 6. That t h e Council of t h e C i ty s h a l l meet a t i t s r egu la r neetin,: place on tno 1 3 t h d a j of June. 1967, a t 7:00 o 'c lock P. >A. f i r i e s igna t io :~ oi depos i to r i e s .

SECTIOII 7. That t n i s Resolut ion be dec lared t o be an emergency t e so lu t ion necessary f o r t h e public peace, heul t i i and safety an3 s h a l l take : f fec t f o r t i w i t h u;on i t s adoption,

Charles G. Shafer /s/ P res iden t of Council

PASSZ?: This 8 t h day of )bay, 1967

4TTZST: PaCr ic is A. Stockdale /s/ Clerk of Council

:PFROVED: May 8, 1967

Ear l S i l l e a r y /s/ Xayor

RECORD OF RESOLUTIONS

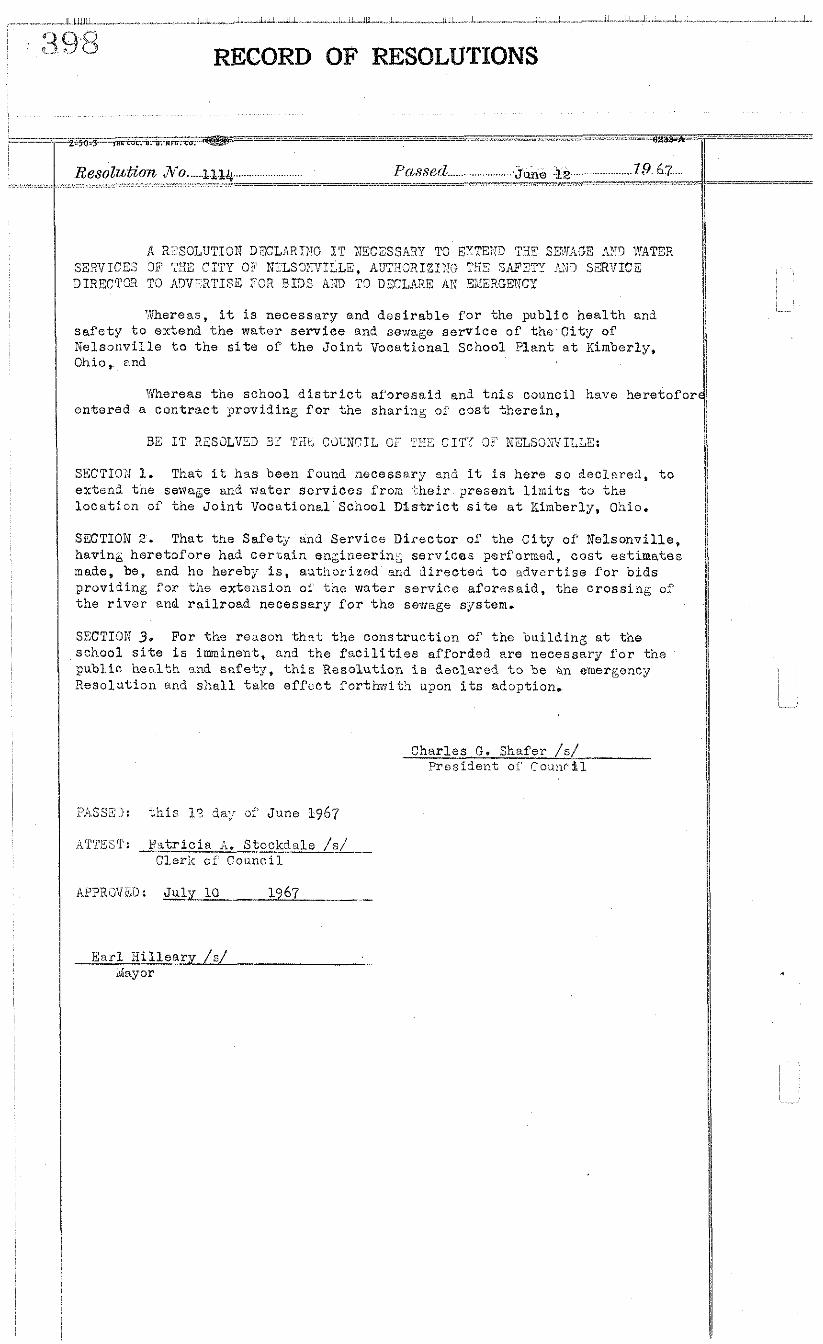

Resolution No ...... 1.1.~ .......................... Passed ........................ . J&& :lp ....,... .............. 19. 67 ... - - -"-"

"ihereat, it is necessary and d e s i r a b l e f o r the publ ic h e a l t h an? s a f e t y t o extend t h e water s e rv ice an? sexage s e r v i c e of the C i ty of Nelsonvil le t o t h e s i t e of t h e J o i n t Vocational School P lant a t Kimberly, Ohio, cnd

Whereas t h e school d i s t r i c t a foresa id an3 t n i s council have heretofox en te red a c o n t r a c t providine f o r the s h a r i n ~ of c o s t t he re in ,

SECTIOJ 1. That it has been found necessary cn3 it i s here s o dec l s r ed , t o extend tho sewage an3 water s e r v i c e s from h e i r ? r e sen t l imits t o t h e l o c a t i o n of t h e J o i n t Vocational Scnool D i s t r i c t s i t e a t Kimberly, Ohio.

SZCTION 2. That t h e Safe ty and Serv ice Di rec to r of the C i t y of Nelsonvil le , having he re to fo re had c e r t a i n engineerin& se rv ices performed, c o s t e s t ima tes made, be, and he hereby is , autborizad and d i r e c t e d t o a d v e r t i s e f o r b ids p rov i l ing :'or t h e ex tens ion 01' t n e water s e rv ice a fo resa id , t h e c ross ing 0;'

t h e r i v e r and r a i l r o a d necessary f o r t h e sewage systom.

SECTION 3. For t h e reason t h a t t h e cons t ruc t ion of t h e bu i ld ing a t the school s i t e i s i m i n e n t , and t h e f a c i l i t i e s afforded are necessary f o r the public h e a l t h and s a f e t y , t'nis Resolut ion i s dec lared t o be i n emergency Resolu t ion and s h a l l take eff::ct for thwi th u2on i t s ad32tion.

Charles 9. Shafer / s j Prosiclent o i Counr $ 1

ATTEST: B3 t r i c i a A. Stockdale /s/ Clerk of Council

Ea r l Sillea- Mayor

LUTIONS

Resolut%on No ................ 3.13.5 .... Passed ........ ~.un.e .... 12 ..... .. ... .......................... 19.67 ....

Whereas t h i s Council has adver t i sed f o r b ids f o r t h e awarding of Cne i n a c t i v e d e l o s i t s of moneJTs oi' t h e C i t y of Belsonvi l le , and

'Vhereas b i d s have been received t h e r e f o r and t h e i n s t i t u t i o n paying t h e g r e a t e s t r a t e oi i n t e r e s t on the s a i d depos i t i s The Peoples Bank of Nelsonvil le , Ohio,

SZCTION 1. That The Peoples aank oi Nelsonvil le , Ohio, be and it hereb-f i s d e s i g n a ~ e d as tho depos i tory f o r t h e i n a c t i v e P.inds f o the Ci ty of Eelsonvi l le f o r t h e period of two years .

SZCTION 2 , For t h e reason t h a t c e r t a i n of' t h e funds of the C i t y a r e p resen t ly on time d e l o s i t s t h e !*uditor and Treasurer a r e i n s t r u c t e d as sa id time depos i t s mature, t o t r a n s f e r t h e inac t ive funds of t h e Ci ty i n hccor5ance witin t h e foregoin; s e c t i o n of t h i s Resolution.

SECTIOX 3. For tho reuson t h a t tho bids have been examlne3, opened and warded. this Resolut ion i s dec lared t o be on emergency Xesolution necessary f o r the publ ic peece, h e a l t h and s a f e t y and s i ia l l take e f f e c t f o r t h v i t h ulon i t s adoption,

Charles G. Shaf e r /s/ P res iden t oi Council

PASSZD: t h i s 12 day of June, 1967

ATTEST: r a t r i c i a A. Stockdale /s/ Clerk of Council

APPXWEi): July 13, 1967

E a r l B i l l e a r g /s/ Mayor

0. --M=*L; . -~w+v&+--mw . ~ .- ~~~~~. ..... . . ~ ~ ~ . ~. . .~ . . ~ ~ ~ ~ ~ . . . ... ...-..~..~-.......~...~.-....a- --

Reso lu t ion .No ...... lrl.z6 ......................... Passed j.uae .... lz ............................ 29. .AT...

RZC,O~JTIO?T DIRSCT1i.K:- T:E C I T Y SDLICITOR AID CITY AUDITOR TO COyFER WTi';{ T:is F'IRI;T NATIOTlAL BA?JK !.:ID TEE PEOPLES 3ANK A N l '10 DzCLAXE ,kN EiwDRGEXCY

Thereas The F i r s t Natior,al. Band t h e The Peoples Bent: of Yo% Ci ty of Nelsonvil le have both submitted b ids looking t o t h e depos it of t h e a c t i v e funds of t h e Ci ty of Melsonville, and

llkereas both banks a r e e l i g i b l e d e p o s i t o r i e s of s a i d funds an3 s a i d b ids a re equal , and

Whereas tne maintenance of two e c t i v e funds viil.1 c r e a t e confusion i n t h e handling of t h e C i ty a f f a i r s ,

3E I T RESOLV33 3 1 Ti!E COUIICIL O! Tli2 CIYI OF M';LSCINVILLE

SECTIOX,T-I. That t h e Ci ty S o k i c i t o r and C i ty AuAitor c o n t a c t both banks s u b r d t t i n g b ids f o r the a c t i v e f'un3s of s a i d Ci ty t o determine whetn o r not a working ai;reement can bc aciiieved i*~ i th3u t n e c e s s i t a t i n g t"e maintenance or two checkin& accounts.

SZCTIOX 2. For t!lo reason t h u t t h e order ly ope ra t i sn of tile f i s c a l ma t t e r s of the C i t y of Nelsonvi l le i s highly d e s i r a b l e , t h i s Resolu t ion i s dec lared t o be an emer gency Resolut ion neocssary f o r t h e publ ic peace, h e a l t h 2nd s a f e t y and shra l l ' t ake e f f e c t f o r t h w i t h upon i t s ado2tion.

Charles 0. Shafer / s / P res iden t of Council

PASSED: t?,is l ? $97 of June, 1967

AT'P~ST: P a t r i c i a A. S tockia le /s/ Clerk OF Council

E a r l H i l l ea ry / S/ .-

May or

SECTION 1. That t h e Auditor be and she hereby i s d i r e c t e d and authorize* t o t r a n s f e r from t h e Po l i ce Radio Expense Fund the sux of' Four Hun3red For ty Dol la rs , Two iiundred and F i f t y Dol la rs of which s h a l l be t r a n s f e r r e d t o t h e Pol ice Uniform Allov!ance and One Hundred and Ninety Do l l a r s t o t h e Po l l ce I n c i d e n t a l Fund.

SECTIO" 2. That t h e s u i of' Two Thousand Eight Hundred and Ninety Do l l a r s be and t h e same hereby i s d i r ec t ed t r a n s f e r r e d from t h e Reeular Po l i ce F'und t o the Ext ra Police Fund.

SETIOIC 3. That t h e su!rL of One Hundred Thirty-One Dol la rs and Thirty-Two Cents b e and t h e same hereby is d i r ec t ed t r a n s f e r r e d f r o 2 t!~e 'Yater U t i l i t y Fund i n tne fol lowing manner; Seventy-Tvio Do l l a r s an* Forty-Eight Cents t o S u ~ e r i n t e n d e n t and Lineman Salary, and Fif ty-Eight Dol la rs an3 Eighty-Your Cents t o t h e Water C le rk ' s sa la ry .

SZTIr3N 4. For t h e reason t h a t s a i d t r a n s f e r s a re necessary fo r thwi th i n order t h a t t h e accounts may be properly r e f l e c t e d , t h i s Resolut ion i s dec lared t o be an emergency Resolut ion necessary f o r t h e public peace, heu1t.b ariii s a f e t y and sno l l take e f f e c t fo r thwi th u2on i t s adoption.

Charles G. Sharer /s/ P r e s i d m t of Council

PASSED: This 10 day of' July , 1967

ATTEST: P a t r i c i a A.. Stockdale /s/ Clerk of Council

S a r l H i l l ea ry /s/ Mayor

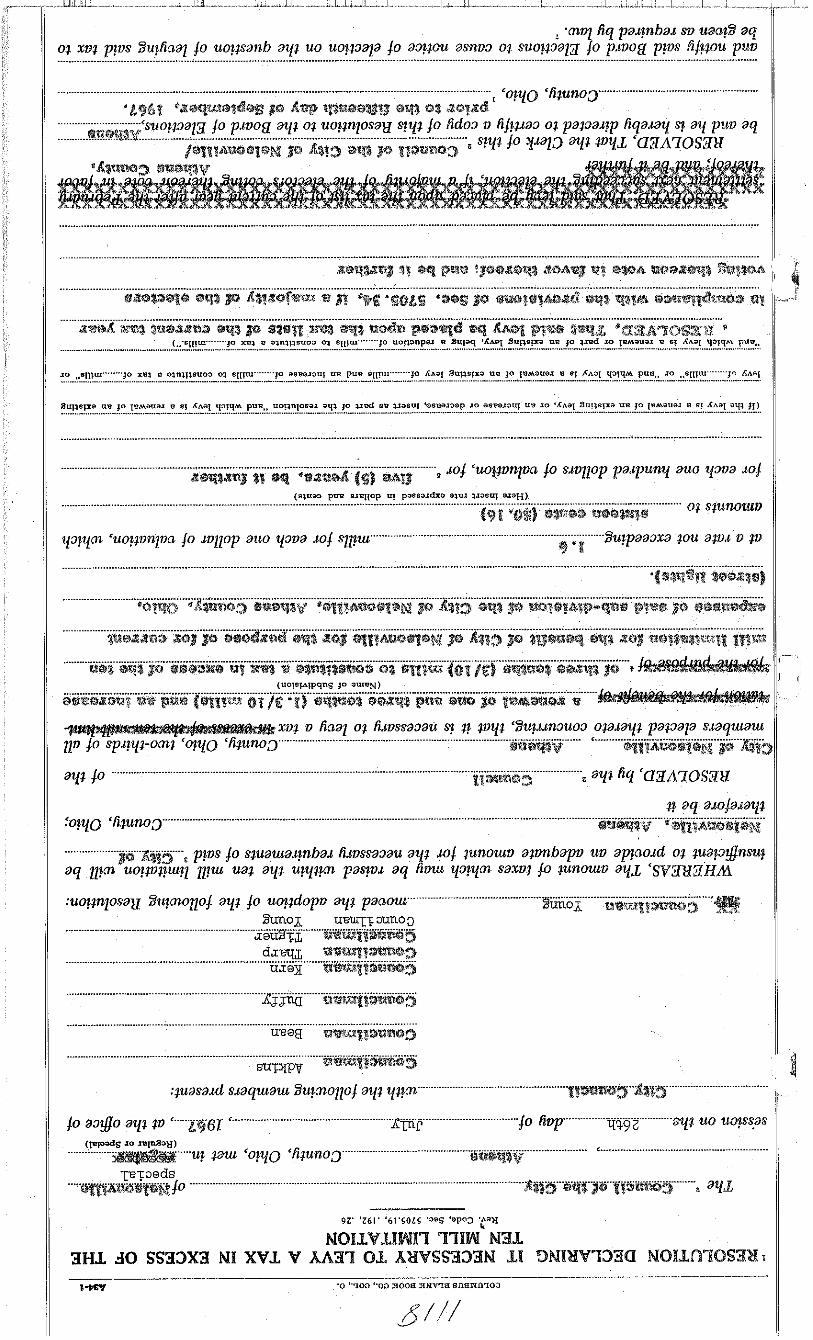

. 'mu1 tiq pas?nbas s?, uan? aq o$ xu$ pp)vs 2uptinal /o uop$sanb ay$ uo uog3ap 40 aqzou amv3 o~ suof&yg lo pmoa p y x fijgou pua ........................................................................................................................................................................................................................................................

.......................................................................................................................................................... 'ozziO 'filunoT.." ............................................... L .

y q g 40 p~vog ayt o$ u f i k ~ a 3 04 pawarp Iiqasay sf ay puo aq ..........................................................................................................

8 SZYl !Q YmZ3 aYJ MYJ 'QEA7OSEbl

....................................................... seconded the Resolution and the roll being called

upon its adoption the vote resulted as follou~:

....... Bean ........... : ............................................................................................. ..... ye.ea-- .............

m>&B ....... mf fs ...................................................................................................... .....yew ............ Councilman Tham T T R 2

.................................................................................... (Name of Subdivision)

....................................... G b r l t

R!!? County, Ohio --

I . This Resolution ie t o he passed end certified to the B W . ~ of ~ k ~ t i o n s prior t o the fifteenth day of September in any year.

2. Board of Countv Commirsionr~s. Council of the City or Village, Board of Education, or Board of Township Trustees 3. Name of Subdivaion. 4. Here inrert any m e of the ~u~~~~~~ listed in Sec. 5705.19 R.C. 5. insert ior all subdivisions indudinn under 5705.19, the life indebtedness or tho number of y r r r s the levy is to run end in the case

,f schools r~nder 5705.19i tho amount of the incrcsse which may he continued for sn indrfinite period of time. 6. schools under 5705.192, shall dso iiri the of ti,! incr.aee in =at., if any, proposed to be levied in ordm to qualify for the +tribu-

tion of school funds under chapter 331 7 R. c., and the portlon of tho increased rate, if any, in enrwss of the amount necessary t o vainly under chapter 331 7 R. C.

smch r e d ~ i t i o n shall n!so providr that the portion of the increased in Excess of that required to allow !he school dietrict to meet the le.ry provisions i,nder chapter 3317 R. C. be in effect ionger than 1 0 years and tha t voted portion of fhe mcreased rate shall b! in eBrrt until such t ime tirr m a y be decreased pursuant to 5705.261 or 'section 5713.11 or such p o r t ~ o n may be an decreased

for a period of not to m d from year to year by a majority vote of the Board of Education. 7. This netice to be eivon by the Board EIestionr be publishad in a of oirculation in tho subdivision once e week

for four consecutive weeks nrior to the election.

The State of Ohio , ............ ...................................................... o u S3.

............................................... that the s m e has been compared by me with the. Resolution on said Record

and that it is a tvue a d colrect copy thereof.

Witness m y signature, this .......... 26th ................. day

.~ -~~~~~ ~~ ~~ ~~ , , , . . .. . , .... ~ ....... -.--.- ~ s33;8.-

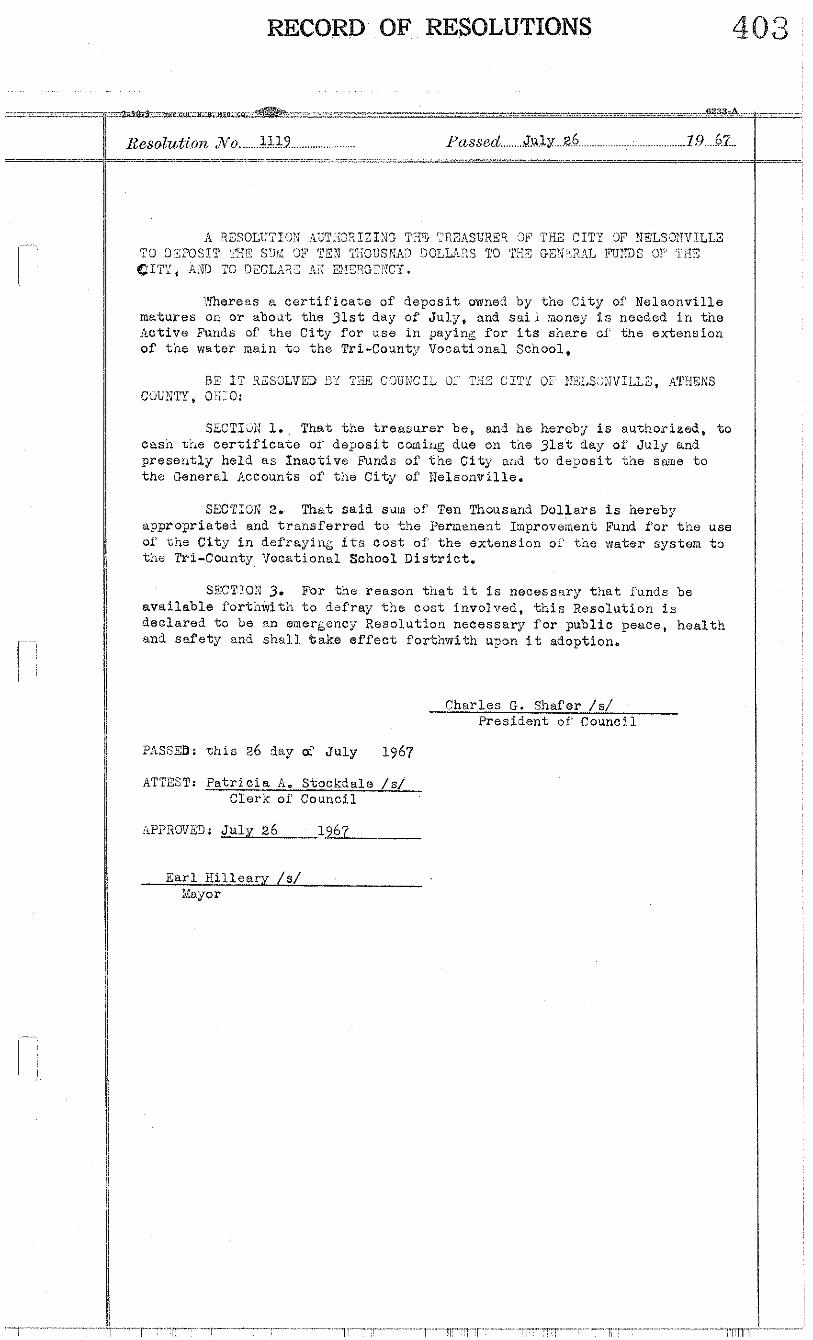

Resolution No ....... LLLS ........................ Passed ......... J.u.1 9....62..

' f i e reas a c e r t i f i c a i . e of depos i t owned by the C i ty of Nelaonvil le matures on or about the 31st day of Ju ly , and s a i l money i s needed i n t n e Active Funds of t h e Ci ty f o r use i n ~ a y i n g f o r i ts share of' t h e extension of t h e water n a i n t o t h e Tri-County Vocatignal School,

SECTIJ~ ; 1. That t n e t r e a s u r e r be, and he hereby i s authorized, t o c a m t n e c e r t i f i c a t e oi de2os i t co:ning due on t n e 31st day of July and preserl t ly held a s Inac t ive Funds of t h e C i ty and t o d e g o s i t m e same t o t h e General Accounts of t h e C i ty of Nelsonvll le .

SECTIOK 2. That s a i d sum of Ten Thousand Dol l a r s i s nereby a2propr ia te5 and t r a n s f e r r e d t o t h e Perlnanerlt Improvement Fund f o r t h e use of che Ci ty i n def raying i t s c o s t o i t h e extension o!' tne water system t o the Tri-County Vocational Sohool D i s t r i c t .

SECTTON 3. For the reason t h a t ir; i s necessnry t h a t funds be avn i l ab le f o r t h w i t h t o def ray tni: cos t involved, Cnis Resolut ion i s dec lared t o be an emergency Resolution necessary f o r publ ic peace, hea l th an5 s a f e t y and sna l l t a k e effecr; fortnwwith u2on i t adoption.

Charles G. Shafer / s / Pres ident of Council

i3'iSSSB: t h i s 26 day of J u l y 1967

ATTEST: P a t r i c i a A. Stockdale /s/ Clerk of Council

E a r l i i i l l e a r y /s/ Mayor

RECORD

Resolution 80 ...................... 1221 ......... Passed ................. Augus t;... lk..... .......... . 9 . 6 . % ...... --- - -- - -

SECTION 1, Tha-t the sum of Six Hundred J o l l a r s ($6>0.00) be and the same hereby i s d i r e c t e d t o ba t r a n s f e r r e * from t h e Parking Meter Fund t o t h e Public Parkway Fund and t h e Auditor i s hereby a u t h o r i ~ e d t o meke such t r a n s f e r .

SECTION 2. The forego in^: Resolution is hereby dec la re3 t o be a emergency Resolution necessary f o r t h e p b l i c peace, h e a l t h and s a f e t y f o r t h e reason t h a t the Public Parkway Fund d o e s n o t have s u f f i c i e n t funds t o meet c u r r e n t expenses and the re fo re s h a l l take e f f e c t f o r t h ~ ~ i t h upon i t s adoption..

Charles G Shafer /s/ P res iden t oi' Council.

PASSED: this 14 day of August 1967

ATTEST: - P G i c i a A Stockdale /s/ Clerk of Council.

APPRQVED: August 14, 1967

Zar l B i l l e a r y /s/ Mayor

RECORD LUTIOMS

..... ........ .... .................................. Resolution No .... 11% ......................... Passed !+!gist &!A 19.67

Whereas, var ious c i t i z e n s have been concerned because of t h e a s s e ion of easements r i g h t s of way across t n e south end l o t s No. 234-235-236- 237 and %38 i n t h e C i t y of ~Te l sonv i l l e , and

T ie reas , t h e Ci ty of Nelsonvil le has no d e s i r e t o wi5en 'Vest Washington S t r e e t a t t h i s p a r t i c u l a r a rea , now, the re fo re ,

SEICTI.JN 1, A l l claiiil an5 r i g h t oi the C i t y . o f Nelsonvi l le i n and t o In-Lots 234 through 238, both numbers inc lus ive , be, and the silme hereby a re , abandoned.

SECT131; 2. That t h e l i n e s of 'Nest Washington S t r e e t be, and they hereby a r e , e s t ab l i shed a t the p a r t i c u l a r po in t s which i t now has oppos i te t h e a fo resa id l o t s .

CCPl T 7 , ~ , . , l ' ~ ~ , , u 3. For t h e reason t h a t grave concern has been expressed by t h e c i t i z e n s , t h i s Resolut ion i s dec larcd t o be an emergency Resolut ion necessary f o r t h e publ ic peace, h e a l t h an(l s a f e t y and s h a l l take e f f e c t for tnwi th upon i t s ado-;ltion.

Charles G. Shafer -- Pres ident oi Council

PASS!D: t h i s lli day of August, 1967

ATTEST: T a t r i c i a A Stock5ale /s/ Clerk of Council

APPR3V?D : August 14, 1967

Ear l B i l l e a r y /s/ - Mayor

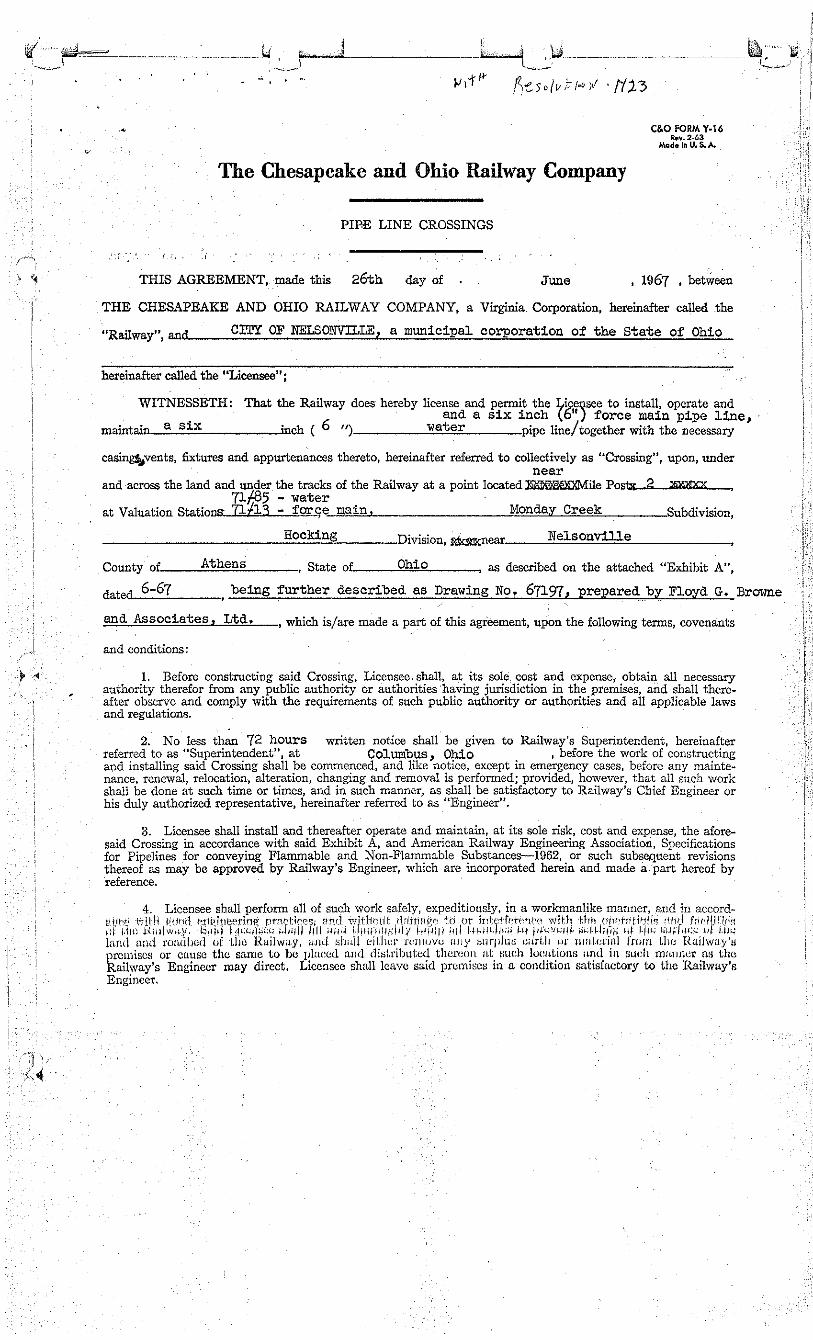

* C&O FORM Y-16 US". 2-63

e, hdeinU.S.*.

The Chesapeake and Ohio ilway Company

PIP33 LINE CROSSINGS

.,, . , .,"-, . , I i . . ., . . .. , . . . , . . . . . . . .

, V THIS AGREEMENT, made this 26th day of . . June , 1967 , between i

I THE CHESAPEAKE AND OHIO RAILWAY COMPANY, a Virginia Corporation, hereinafter called the

i "Railway", and CPrY OF NELSO!JVILLE, a municipal corporation of the State of Ohio

1 hereinafter called the "Licensee"; I

1 WITNESSETH: That the Railway does hereby license and permit the I e see to install, operate and

and a s i x inch y&y force main pipe l ine , 1

& ( 6 ") I

maintain a Water p i p e line/together with the necessary I casinsvents, fixtures and appurtenances thereto, hereinafter referred to collectively as "Crossing", upon, under

i near --. i and across the land and under the tracks of the Railway a t a point located XXE&?CNile Pos- ,I

71i8.5 - water ! I at valuation stations. 7 1 h 3 - f q e main 3 Monday Creek Subdivision, 12 ! ! :

. , , , , , Hocking Division, -near Nelsonville I,,:

,, 1 <

County of Athens , State of Ohio , as described on the attached "Exhibit A",

6-67 dated being further described as Drawing No. 67197, prepared by Floyd G. Brmne '

l and Associa*es 3 Ltd. , which is/are made a part of this agreement, upon the following terms, covenants I I

I _I and conditions:

1. Before constructing said Crossing, Licensee shall, a t its sole, cost and expense, obtain all necessary authority therefor from any public authority or authorities'having jurisdiction in the premises, and shall there- after observe and comply with the requirements of such public authority or authorities and all applicable laws and regulations. -

! ,, . 2. No less than 72 hours written notice shall be given to Railway's Superintendent, hereinafter

referred to as "Superintendent", a t Columbus, Ohio , before the work of constructing and installing said Crossing shall be commenced, and like notice, except in emergency cases, bcfor* any mainte- nance, renewal, relocation, alteration, changing and removal is performed; provided, however, that all such work shall be done at such time or times, and in such manner, as shall be satisfactory to Railway's Chief Engineer or ..

his duly authorized representative, hereinaiter referred to as "Engineer".

3. Licensee shall install and thereafter operate and maintain, at its sole risk, cost and expense, the afore- ! said Crossing in accordance with said Exhibit A, and American Railway Engineering Association, Specifications for Pipelines for conveying Flammable and Non-Flammable Substancesl962, or such subsequent revisions i

thereof as may be approved by Railway's Engineer, which are incorporated herein and made a . part hereof by reference. !

- Enginecr.

SCHEDULE A

r County Auditor's Estimate of T a u

Rate to be l.ev:lul

vi

I Sinking Fund

'' Bond Retirement Fund ii General Fund

ij

/I Library Fund ',

; Rscreafion Fund

' University Fund

I' J Current expense ievy authorized by voters on I;

I! for not to exceed years.

and be it fllrther RESOLVED, That the C k k of thk Council be, and he k hereby directed to certify a copy of

this Resolution to the County Auditor of said County.

Mr ._-_-- l'm i - - - - - e d the Resolution and the ro!l being called

upon its adoption the vote resulted as follows:

yea- _. Mr b&!2&! _--_ ,- . ~. ... . . . .. . -- ~ a ~.

ea Mr .--- @-% -------.- . .- Y . . -. - ea Mr._-&ffs --------- - - 1 ~ - -

RECORD OF RES LUTIONS

Resolution N'o ............... ll26 ............... Passed ...... O.c.t.~.b.~x. ..9, .................................. I$? ........ -- - .-..__I_____..----- --

R RESOLUTION ESTABLISHING AN ALLOWANCE FOR THE SUPERINTENDENT OF THE WATER DEPARTMENT TO REIMBURSE HIM FOR EXPENSES INCURRED I N THE USE OF HIS OWN AUTOMOBILE I N MAKING NECESSARY CHECKS OF THE WATER DISTRIBUTION SYSTEM AND TO DECLARE AN EMERGENCY

Whereas, it has been the custom of the Ci ty of NelsonvSlle t o d i r ec t the Superintendent of Water Department t o rheck the several dead ends of the water system, t ransport samples t o the laboratory f o r analysis and t o check the reservoir and,

Whereas, it appears t h a t approximately three thousand miles per year are involved i n sa id checks and del iver ies . and,

Whereas, the City i s present ly unable t o provide the Water Superinten- dent with a municipally owned vehicle, now, therefore,

BE I T RESOLVED BY THE COUNCIL OF THE CITY OF NELSONVILLE, ATHENS COUNTY, OHIO,

SECTION 1. That so long as t he Water Superintendent of the City of Nelsonville i s required t o use h i s personal automobile t o make t-he necessaq checks of the terminal points of the water system and t o del iver the necessary samples t o the laboratory, t ha t sa id Superintendent be, and he her authorized and directed t o be reimbursed i n the amount of Twenty-Five Doll: per month f o r such use of h i s pr ivate vehicle.

SECTION 2. That the Auditor be, and he hereby i s , authorized and , directed monthly t o draw warrants against the Water Fund i n favor of the Superintendent of the Water Dehartmerit pf the City of Nelsonville i n the amount of Twenty-Five Dollars each t o reimburse the Water Superintendent f o r the use of h i s pr ivate vehicle. I

SECTION 3. For the reason t h a t it i s necessary t h a t sa id checks be made and de l iver ies be accomplished the Resolution i s declared t o be an emergency Resolution effect ive as of the first day of August 1967 and t o take e f f ec t forthwith upon i t s passage f o r t he reason t h a t f a i l u r e t o adopt same forthwith w i l l r e s u l t in necessary samples of the water and checks of the system t o be not made and therefore i s declared necessary f o r t he public peace,':health and safety.

Charles G. ~ h a f er/s/ -,= President of Council

PASSED: t h i s 9 day of October, 1967

ATTEST: Maxine Dixon /s/ Clerk of Council

APPROVED: October 9, 1967

Earl Hilleary /s/ Mayor

I

i s ,

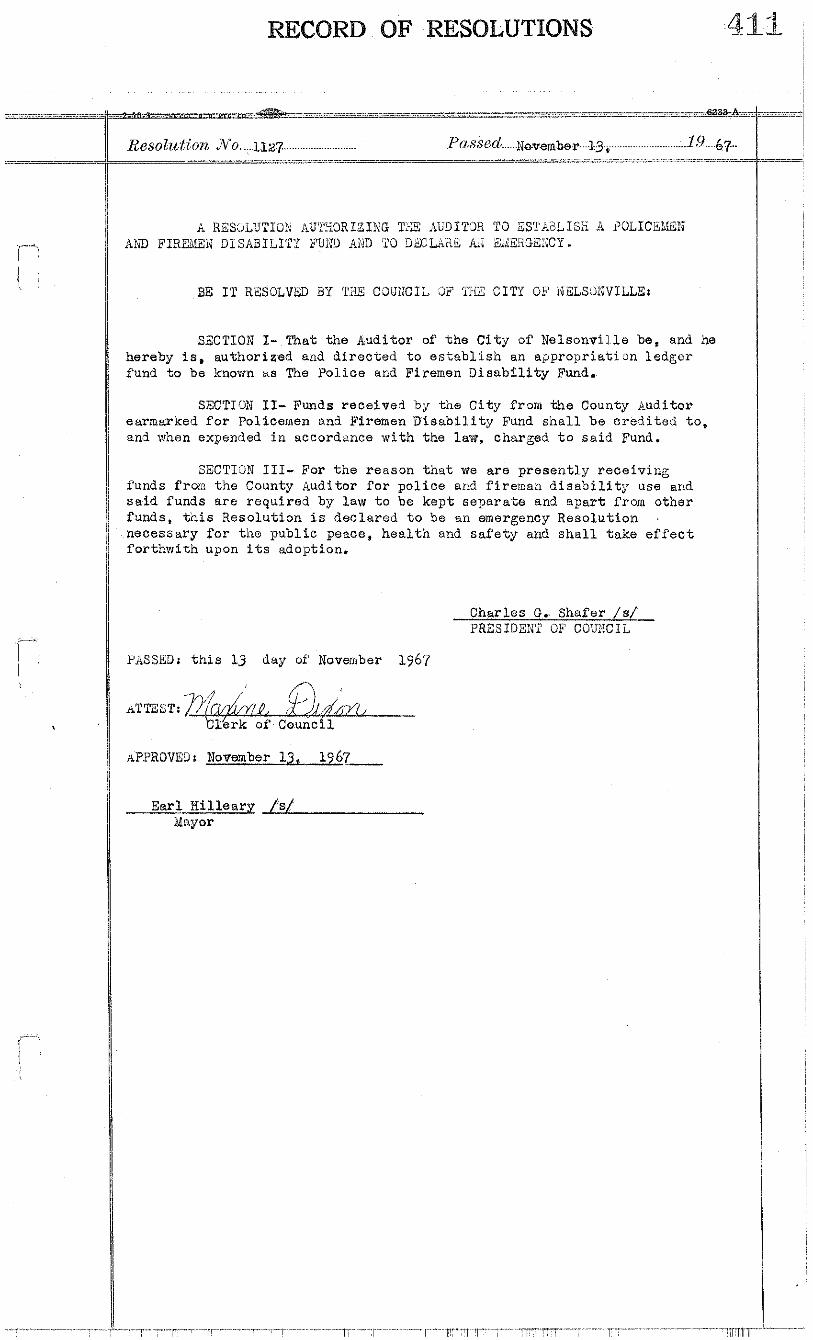

Resolution No ..... ~ ~ 2 3 .... Passed .... N ~ ~ ~ ~ ~ ~ ~ . ~ ~ ~ . ~ ~ ~ ............................... 19 ... b7.. ----- --

BE I T XZSOLVED BY 'RiE C3UNCIL SF 'liiE C I T Y OWNELS9NVILLE:

SZCTION I- That t h e Ruditor of t h e C i t j of Nelsonvi l le be, and he hereby i s , authorized and d i r e c t e d t o e s t a b l i s h an appropr ia t ion ledger fund t o be known as The Po l i ce and Firemen D i s a b i l i t y Fund.

SECTION 11- Funds rece ived Sy the C i ty from 'the County Auditor earmarke? f o r Policemen and Firemen D i s a b i l i t y Fund s h a l l be cre3i to. l t o , and when expended i n accordance w i t % the l a v , charged t o s a i d Fund.

SECTION 111- For t h e reason ths-c we a re p resen t ly r ece iv ing funds from t h e County Auditor f o r po l i ce and fireman d i s a b i l i t y use and s a i d funds a r e requi red by law t o be kept s epa ra t e and a p a r t from other funds, t n i s Resolut ion i s dec lared t o be an emergency Resolut ion necessary f o r t h e publ ic peace, h e a l t h and s a f e t y and s h a l l take e f f e c t fo r thwi th upon i t s adoption.

Charles G. Shafer /s/ PRESIDENT OY COUXCIL

P-'XSS&D: t n i s 13 day of November 1967

API~ROVEI): November 13, 1967-

E w l H i l l e a r y /s/ Mayor

TITLZ: A Resolut ion levying a t a x t o nrovidr: funds f o r t';e purpose of ;enera1 municipal o se ra t ions , maintenance of equipment, new e q u i p e n t , ex tens io :nlargement and improvement of municipal s e r v i c e s and f a c i l i t i e s and c a p i t a l .rnprovements, on a l l s a l a r i e s , wages, cornmissions and o the r compensation earned ,y r e s i d e n t s of t h e C i t y of Xelsonvi l le ; on a l l s a l a r i e s , wages, commissions ind o ther compensation earned by non-residents of the C i ty of Xelsonvi l le f o r vork done or s e r v i c e s performed or rendereri i n the C i t y of ?Jelsonvi!le; on t h e l e t p r o f i t s earned on a l l bus inesses , p o f e s s i o n s o r o the r a c t i v i t i e s conducted ,y r e s i d e n t s of t h e Ci ty of Xel8onvil le; on t h e n e t p r o f i t s earned, on a l l p r o f i 3arned on a l l bus inesses , p o f e s s i o n s o r o the r a c t i v i t i o s conducted i n the Ci ty .n t h e Ci ty of Nelsonvi l le by:non-residents , and on t h e n e t p r o f i t s , earned by r l l corpora t ions doing business i n t h e Ci ty of Nelsonvi l le , as the r e s u l t of vork done o r s e r v i c e s performed or rendered i n t h e C i ty of Nelsonvil le; re- ju i r ing t h e f i l i n g of r e t u r n s and fu rn i sh ing ci' information by employers and 3 1 1 those s u b j e c t t o s a i d tax ; imposing on employers t h e duty of c o l l e c t i n g ihe t a x a t the source and payini; t h e same t o tile Ci ty of Nelsonvi l le ; providing ?or the a d m i n i s t ~ a t i a n , c o l l e c t i o n and enforcement of s a i d tax ; dec la r ing r io la t ior l thereof t o be a misdemeanor and imposing p e n a l t i e s t h e r e f o r ; and i e c l a r i n g an emergency..

ARTICLE 1 - 1

DFFINI TIONS

For t h e j?urpose of these Regulations ?he fol lowing terms s h a l l have the l e f i n i t i o n s h e r e a f t e r given;

(A) *TkX?XZP--A person, whether an ind iv idua l , par tnersn ip , l i m i t e d p a r t - nership, corpora t ion , a s s o c i a t i o n o r o ther e n t i t y , requi red hereunder t o f i l e e r e tu rn or t o pqy 3 t a x hereunder.

(B) *'ACEGCI:,'TI!)N'~-- :i pa r tne r sh ip , 1 i : d t o d par tnersh ip , or any o ther form c unincorporated e n t e r p r i s e , owned by two o r more persons.

(C) y'DUSIfVESS"- .An e n t e r p r i s e , a c t i v i t y , proi'ession or undertaking of any nature conducted f o r p r o f i t o r o r d i n a r i l y conducted f o r p r o f i t , whether by a n ind iv idua l , pa r tne r sh ip , l imi t e% pa r tne r sh ip , co rpora t ion , , a s soc ia t ion o r any o the r e n t i t y ,

(9) WCOitPOR.kTIilN"- A corpora t i an or j o i n t s tock a s soc ia t ion organized under t.le laws of t h e United S t a t e s , the S t a t e of Ohio, or any o t h e r s t a t e , t e r r i t o r y , o r fo re ign country o r dependency,

(E) *r31dPLOYEE*-- fffl i nd iv idua l 1whose earn ings a re sub jec t t o the with-, holding of Federal Income Tax o r Soc ia l S e c u r i t y Tax,

(F) *E<i3L'3YER#-- An ind iv idua l , pa r tne r sn ip , l imi t ed pa r tne r sh ip , associa- t i o n , corporat ion, gave rn~menta l body, u n i t o r agency, o r any o t h e r e n t i t y wno o r t h a t employs one o r more persons on a s a l a r y , wage, commissfon, o r ohher compensation basis .

(G) 'NET ?ROYITS*--Tne n e t ga in f r o n t!le opera t iw of a business , professioz o r e n t e r p r i s e a f t e r grovis ion f o r a l l c o s t s and expenses i n c u r r e i i n t h e con- duct tinereof, inc luding reasonable allowance f o r dep rec ia t ion , dep le t ion , amor t iza t ion , and reasonable add i t ions t o r e se rves f o r bad Aebts, e i t h e r paid o r accrued i n accordance w i t h recognized 3 r i n c i p a l s o r accounting app l i cab le t c t h e method of accounting r e g u l a r l y employed, and without deduct ion of Fe3eral Taxes based on income, and witnout deduct ing taxes imposed by t h e Ordinance.

(a) n?:9R-KES13EI'3T"-- An ind iv idua l , par tnersh ip , l imi t ed p n r t m . ~ s l ~ % p ; , cor- porat ion, a s soc ia t ion o r o t h e r e n t i t y domiciled outs i?e the Ci ty of iJelsonville

( I ) "E'ZRS2IT*-- Every n a t u r a l person. pa r tne r sh ip , l i m i t e d par tnersh ip , corpora t ion , f i d u c i a r y o r a s soc ia t ion . Whenever used i n an3 c lause p r e s c r i b i n ~ und imposing a penal ty, t h e t e r m #personw as applied t o a s soc ia t ion , s h a l l meal t h e pa r tne r s or members thereof , and a s appl ied t o corpora t ion , t h e o f f i c e r s thereof .

(J) %SIDEtJTh- An ind iv idua l , par tnersh ip , l i m i t e d pa r tne r sh ip , corpora- t i a n , a s soc ia t ion , o r o the r e n t i t i domiciled i n the C i ty of Nelsonville.

(8) 1'OTiiC;:c EXTI'W-- ' b e term #,other entity! ' means any person or unincor- pora ted body not previous ly nmied o r def ined and included i n t e r a l i a , f i d u c i a r i e k loca ted wi tn in t h e C i ty of Nelsonvil le .

(L) Tne term 'PLAC.CE 0:- BUSIWSS* means any bone f i d e o f f i c e , ( o t h e r than a

mere s t a t u t o r y o f f i c e ) f a c t o r y , warehouse, or o the r space vvhich is occupied a,,>,' ;i used by t h e taxpayer i n c ,arrying on any bus iness a c t i v i t y ind iv idua l ly o r 11 through one o r more of h i s r egu la r employees r egu la r ly i n atten3ance. j!;

2, taxpayer does n o t have a r e g u l a r p lace of business outs ide n 'e lsonvil le s o l e l y by consigning goods t o an independent f a c t o r o r con t r ac to r o u t s i d e t h e C i ty f o r s a l e .

(X) 'The term "'BUS:!'IZSS .4L,LOCU!::r!l ,?iG?CZX':'XZ*, a s used i n these Regulations, means t h a t average percentage a r r ived a t by applying t h e f o r a u l a s e t f o r t h i n Sec t ion 2 , subsectioniYof t n e Ordinance. The "Business Al loca t ion ?ercentageR i s t h e percentage which may be agpl ied t o determine Che por t ion of t h e e n t i r e n e t p r o f i t s of a tax-payer t o be a l l o c a t e d as having been made w i t h i n t h e C i t y oi' Nelsonvi l le w i th in t h e meaning of the provis ions o f s a i d Sec t ion 2.

( N ) The term *T)iE (IHDINANCG~neans Ordinance No. 17-67 enacted by the Counci o f the C i ty of Nelsonvi l le on 1 L December, 1,967, and any amendments o r supple- ments there to .

The s ingu la r s h a l l include t h e p l u r a l and t h e masculine s h a l l inc lude t h e $ ,I feminine and t h e neut;er. 3 I! ARTICLE 1 - %

$ 1 The t a x imposed by t h e Ordinance is e f f e c t i v e a s t o income and p r o f i t s earne

o r accru i n g on and a f t e r 1 January, 1968, and payro l l deductions must be made II \ I a g a i n s t a l l s a l a r i e s , wages, commissions, bonuses and o the r compensation earned 3 o r accruing on and a f t e r t h a t date . I,

The Ordinance continues e f f e c t i v e i n s o f a r a s t h e levy of t axes i s coicerned u n t i l 31 December, 1973. !i

b~ ARTICLE I1 - 1 Ji

I n t h e case of t h e r e s i d e n t s of t h e Ci ty of Relsonvi i le an annual t a x of one percent i s imposed on a l l s a l a r i e s , wages, corrm.issions and o the r compensation earned or accrue& on and a f t e r 1 January, 3.968, For t h e purpose of determining t h e t a x on t h e earn ings of t h e r e s i d e n t taxpayers , taxed under subsec t ion A o'f Sec t ion 2 of t h e Ordinance, t h e source o f ' the earn ings and t h e p lace o r p laces i n o r a t wnich t h e s e r v i c e s were rendered a r e inmaterial . A l l such earnings, wherever er;rned o r pa id* a re taxable..

The following a r e items which a r e sub jec t t o t h e Tax: Vj ! I

(A) S a l a r i e s , bonuses or i ncen t ive paymerits received by an ind iv idua l , whether d i r e c t l y o r t h r o u ~ h an agent and whether i n cash o r i n proper ty , f o r s e rv ices rendered on and a f t e r 1 January, 1968.

(1) A s an o f f i c e r o r employee, or both, of a corpora t ion ( inc luding charita 'r and o ther non-profi t co rpora t ions ) , j o i n t s tock a s soc ia t inn o r j o i n t s tock company;

( 2 ) A s an employee ( a s d i s t ingu i shed from a pa r tne r o r member) of a par tner . sh ip , l i m i t e d pa r tne r sh ip , o r any o the r form of' unincorporated e n t e r p r i s e wmed by one or more persons;

;1

j (3) :ts an empl.oyee ( a s d i s t ingu i shed from the p r w r i e t o r ) of a bus iness , I;! t r a d e o r profess ion ccrnducted by a n ind iv idua l owner; 1

(4) As an d f f i c e r o r employee (whether e l e c t e d , appointed or coi.missioned) :' of a governmental adminis t ra t ion , agency, arm, a u t h o r i t y , board, body, branch,

bureau, department, d i c i s i o n , subdiv is ion , s e c t i o n or u n i t of t h e SBate of Ohic 8 o r any of' t h e p o l i t i c a l subdiv is ions thereof ; 1:

I '8 (5) A s an o f f i c e r or employee (whether e l ec t ed , appointed, o r commissioned) _I af a governmental adminis t ra t ion , agency, arm, a u t h o r i t y , board, body, branch, : I bureau,department, d iv i s ion , subdiv is ion , s e c t i o n or u n i t of t h e United S t a t e s i< i$ Government or of' a co rpora t i an c rea t ed and owned, o r con t ro l l ed by t n e United

S t a t e s Goverrment o r any oi. i t s agencies; 4, I:!, I J ( 6 ) ks an ernployee o: any o t h e r e n t i t y or person, ,I ,: (B:) Wages, bonuses, or i ncen t ive payments received by an ind iv idua l , whethe] # d i r e c t l y o r through an agent and whether i n cash o r i n property, f o r s e rv ices !l rendered on and a f t e r 1 January, 1968. ii

( I ) based upon hourly, d a i l y , weekly, semi-monthly, monthly, annual, 11 [k Page 2

,lunis; of' production of piece-work raqes ; and $

(2) 'ðer paid by an ind iv idua l , l imi t ed par tnersh ip , pa r tne r sh ip , associe c o r p o r a t i o n . ( inc luding c h a r i t a b l e and o the r non-profit corpora t ions) , govern- !!mental adminis t ra t ion , agency, ann, au thor i ty , board, body, branch, department, ; d iv i s ion , subdiv is ion , s e c t i o n o r u n i t , o r any o t h e r e n t i t y .

(C) Commissions reoeived by a taxpayer whether d i r e c t l y o r through an agent whether i n cash o r i n proper+$, f o r s e r v i c e s rendered on and ~ f t e r 1 Januarg 8, r ega rd le s s of how computed, by whom o r wheresoever paid.

If arl~ounts rece ived as a drawing account am&d t h e commissions earned, the x i s payable on t n e gross amounts received..

,mounts rece ived frori, an employer by majr of expenses and n o t '0.1 way oi' ompensation, and used a s such bjr t h e indiv idual r ece iv ing them, a re not dee~ncd o bs compensation i f t h e employer deducts such expense advances a s such from i s g ross income f o r t j le purpose of' de t e rn in ing h i s n e t p r o f i t s t axab le under he Ordinance.

, If such cor~i~nissions aze included i n t h e n e t earn ings of a t r a d e , business , ~ p r o f e s s i o n s , e n t e r p r i s e o r a c t i v i t y r e g u l a r l y c a r r i e d on by such ind iv idua l and ,I , , t he re fo re s u b j e c t t o t a x under subsec t ion C of 8ectic;n 2 of t h e Ordinance, they , s h a l l no t again be s e p a r a t e l y t axed . , I n such case , such n e t earnings s h a l l be '%taxed a s provided i n A r t i c l e 11 - 9 of these Regulations. :,'Il I ; !! ( 3 ) m e r e c e i p t of' f e e s and o the r compensation f o r personal s e r v i c e s render: ( A : s h a l l be deemed t o be sub jed t t o t a x a t i o n under the ordinance. g r:: ( E ) Domestic s e rvan t s a r e s u b j e c t t o Nelsonvil le t a x under t h i s Ordiriance bu I:,&

:are not s u b j e c t o t withholding provis ions . That i s t o say, t h e domestic w i l l !report earnings and pay the t a x d i r e c t l y t o t h e Nelsonvi l le Income Tax Deparbnen ' I

I,! The Frovisions of t h i s Ordinance s h a l l n o t be construed a s levying a t a x {hpon the f o l l o w i ~ :

1. Funds reoeived from l o c a l , s t a t e o r TZlderal governments because of e rv i ca i n the Armed Forces of t i e United S t a t e s by t!?e person rendering such e r v i c e , o r a s a r e s u l t OE another person render ing such service.

,.

, , i,!. 2 Poor r e l i e f , pensions, Soc ia l Secur i ty , unemployment compensation, and , I d i s a b i l i t y b e n e f i t s rece ived fro!:: p r iva t e indus t ry o r l o c a l , s t . i t e o r fe!ertd k o v o r ~ n e n t s , o r from c h a r i t a b l e , r e l i g i o u s or educilt ional organizat ions.

3. nuas , cc;ntr ibut ion and s i m i l a r payments rooeived by c h a r i t a b l e , r e l i g i o u s u c a t i ~ > n a l or l i t e r a r y organiza t ions o r l abor unions, lodges and s i m i l a r organ-

4. Receipts from casual en ter ta inment , amusements, s p o r t s even t s an? h e a l t h nd v ~ e l f a r e a c t i v i t i e s conducted by bona f i ? e c h a r i t a b l e , r e l i g i o u s and educat iu rgan iza t ions and a s soc ia t ions .

1/ 5. imy as soc ia t ion , organiza t ion , corpora t ion , c lub o r t r u s t , which is exem

ljfrom feder r , l t axes on inco!ne by reason o i i ts c h a r i t a b l e , r e l i g i o u s , educations: hi t e r a r y , s c i e n t i f i c , e t c . purposes. j! <.!

6. Gains from involuntary conversion, c a n c e l l a t i o n of indebtedness, i n t e re s . n Federal a b l i g a t i o n s , i tems of income a l r eady taxed by the S t a t e of Ohio, and ncome of a dece '3entrs e s t a t e during the period of' administration (except such ncome from t h e opera t ion of a business)..

! 7.. Earnings and income of a l l persons under 18 yea r s of age whether residon. &r non-residents. . :; (1

ARTICLE I1 - 2

IEIF3SITIOR OF TAX -- ?JON-REO,TD!TJTS

Tn %he case of i nd iv idua l s who a r e non-residents of ?k lsonvi l le , t h e r e i n is. $osed under t h e Ordinance an annual t a x of one percent on a l l s a l i i r i e s , wa;;es, $ommissions an? o ther compensation, earned o r accruing on arid a f t e r 1 January, $968, f o r work done o r s e rv ices performed or rendered w i t h t h e C i ty of Nelsonvil 4he ther such compensation or remuneration is received o r e a r n e l d i r e c t l y o r $hrough a s agent and whether paid i n cash ox i n property. : j

The i tems sub jec t ho t a x urder t iAs s e c t i o n a r e t h e same a s those l i s t e d and f fned i n A r t i c l e TI - 1. For methods of coinputing t h e e x t s n t of such work or

e rv i r .es performed witit in t h e C i ty of Nelsonvi l le , arid cases involving compensr Ion personal s e r v i c e s p a r t l y w i t h i n and p a r t l y ou t s ide the ciiy of Nelsonr

Art2c1,e IV -. I. Page. 3

2. The provis ions of !%ragraph Z of A r t i c l e I1 - 14 of -che Regulations a r e q l i c a b l e t o such corpora t ions .

3. :i corporaciori doing bus iness both wi th in and outs ide tne C i t y o i n'elson- i l l e may, i n determining t h e p a r t of the net p r o f i t s which a r e t axab le under thl rdir~ance, a t i t s opt ion:

(a) Use the usual accounting system of t h e taxpayer oorgorat ion, s o long as r i d usual accounting system s h a l l be one acceptable t o t h e U. 8- I n t e r n a l Revenl apartment as evidenced by acce l tance and approval of inco~ne t a x r e t u r n s f i l e d ne r in ; o r

(b) Use trie Business R l l o c a ~ i o n b r c e n t a g e F'~r1nula s e z fo rzh i n S e c t i w 2, subsect i ,n K of t h e Ordinance.

ARTICLE 11 - 6

j 1. A t the opt ion 01' a corpora te taxpayer o r of a non-resident business

n t i t y , such taxpayers may, but a re not obl iged t o , use t h e f o r m l a s e t f o r t h i n , e c t i o n 2 of t h e Orfiinance t o compute t h e percentage of t h e i r e n t i r e n e t p r o f i t s der ived from a c t i v i t i e s bo th w i t h i n and ou t s ide t h e C i ty of Xelsonvi l le ) whZoh. : s taxable under t h e Ordinance, and t o de te rn ine t h e t a x payable t o tile Ci ty

8

f Nelsonvi l le thereunder .

If t h e taxpayer d i d n o t have a place of bus iness ou t s ide Nelsonvil le dur ing ;he period covere? by m y d e c l a r a t i o n and/or r e t u r n requi red under t h e Ordinance . ts business a l l o c a t i o n percent&ge i s 100 percent; , i n o ther words t h e taxpayer .s requi red t o pay a t a x of one percent on t h e e n t i r e n e t ; j r o f i t oi' t h e vusiness

I f t h e taxpayer ha1 a p lace o r p laces of bus iness ou t s ide Xelsonvi l le , and !as doing bus iness i n Nelsonvil le dur ing such period, t h e business a l l o c a t i o n )ercerithge s l ~ a l l be computed on t h e fo l lowing b a s i s (Sec t fon '718.08 Revised Code .- S t a t e oi Ohio):

(A) In the t a x a t i o n of Incoue which i s sub jec t t o t axa t ion by t h e provis ion >f tile Ordinance, if t h e books arid records of a taxpayer c o n d ~ c t i n g a business ,r profess ion both w i t h i n and without the boundaries of t h e C i t y oi' Ne1si;nviLle s h a l l d i s c l o s e wi th reasonable accuracy what po r t ion of i t s n e t p r o f i t i s

s t t r i b u t a b l u t o t h a t p a r t of t h a t business or p ro fes s ion conducted. wi th in the 3oundaries of :bhe C i t y of Nelsonvil le , then only such por t ion s h a l l be considere is having a taxable siJcus i n t h e C i t y of Nelsonvi l le f o r purposes o f municipal income taxa t ion . I n t h e absence of such records , n e t p r o f i t from y bus iness o r profession conducted wi th in and without t h e boundaries of t h e C i t y of Nelsonvil l % h a l l be considered a s having a taxable 8 i . b i n t h e C i t y of Nelsonvi l le fo r Pmposes of municipal income t a x a t i o n i n t l e s m e propor t ion as t h e average r a t $ 3f:

(1) average n e t book va lue 01' t h e r e a l and t ang ib le porsonal property Jwned or used by the taxpayer i n t h e bus iness o r profess ion i n tino C i t y of Nelsc v i l l e durin: t h e taxable p r i o d t o tne average n e t bwak value ol a l l of the r e a l %rid t ang ib le personal proper ty o w e d or used by t h e taxpayer i n t h e business o r profession dur ing t h e sameperiod, wherever s i t ua t ed .

( 2 ) Wages, s a l a r i e s , and o t h e r conpensat icm paid during t!le taxable period t o persons employed i n the business orprofess ion f o r s e r v i c e s performed i n the :itj of I~Jelsonvil le t o wages, s a l a r i e s , and o t h e r co:::pensaiion pa id during t h e same period t o persons employed in the business o r profession, wherever t h e i r perv ices a r e performed..

( 3 ) Gross r e c e i p t s of t h e bus iness mr profess ion f r o a s a l e s made and se rv ices performed dur ing the t a x a b l e period i n t h e C i ty of Nelsonvil le t o grosz r e c e i p t s 01' t n e business o r profess ion dur ind t h e same period from s a l e s and se rv ices , wherever made or gerfonned.

I n toe event t h a t tile foregoitig al locat ior! formula does not produce an *qu i t ab le r e s u l t , another b a s i s may, under uniform regu la t ions be s u b s t i t u t e d s c as t o produce such r e s u l t .

(ii) As use2 i n d i v i s i o n ( A ) 01 t n i s subsac'cion, * s a l e s made i i r tile C i ty of tJelsonvil lea~ means8

(1) A l l s a l e s of t a n g i b l e personal propert:! which i s d e l t w r e d v ~ i t n i n t h e Oity of Xelsonvi l le r ega rd le s s 3f where t i t l e passes i f shipped or d e l i w r e d f r o 2 a s tock of goods within such municipal corpora t ion;

(2) A 1 1 s a l e s $ t ang ib le persorial proper ty which i s del.iverred w i t h i n t h e

C i ty Of Nelsonvil le r ega rd le s s of where t i t l e passes even thouj j l transported fr,

po in t outsido such C i ty i f the taxpayer i s re.gu1arly engaged through i t s own nployees i n t h e s o l i c i t a t i o n or promotion of s a l e s wi th in such ::ity and the lies r e s u l t f r o a such s o l i c i t a t i o n ,or promotion;

(3) A11 s a l e s of t ang ib le personal property vvlnich i s shippe3 from a place l t n i n t h e C i t y of Nelsonvi l le t o purchasers ou t s ide such C i t y regai ,dless of 3re t i t l e passes i f t h e taxpayer i s not , through i t s own enlployees, r e g u l a r l y ngaged i n t h e s o l i c i t a t i o n o r promotion oi' s a l e s a t t n e p lace where d e l i v e r y i; sde .

The business a l l o c ~ t i o ~ l perce:itb&e i s computed by deterinitrir~g ' he percentage. $) which Nelsoriville r e a l and t ang ib le personal property bears t o a l l r e a l and angible personal proper ty ( inc ludiny t h a t s i t u a t e d i n N e l s o n v i l l e ~ of' taxpayer !heresoever s i t u a t e d ; (B) which I 'Jelsonville bus iness s a l e s bear t o taxpuyer 's n t i r e bus iness s a l e s wheresoever der ived ( i n c l u d i n ~ : tnose derived from Helson- - i l l e ) ; and ( G ) which payro l l s paid by taxpayer wi th in Xelsonvi l le bear t o tax- : a y e r r s e n t i r e pay ro l l wheresoever paid ( inc luding Nelsonvil le p a y r o l l s ) ; add- :; rig together the t h r e e percentages s o a r r ived a t and d iv id ing the t o t a l by tkveet

1

e : IIwpever, i f one of t h e fa (property, s a l e s o r pay ro l l s ) i s missing, t h e

t h e r tyro peroenta$es a r e added and t h e sum i s d iv ided by two, and il' two of th a c t o r s a re missing the r e m i n i n g percentage i s the business a l l o c a t i o n percent ge . y 1:

Corporation have places of bus iness i n Nelsonvil le , Athens and Logan.

Nelsonvi l le r e a l and t ang ib le personal proper ty $10,000.00. A l l r e a l and e r sona l property(Tdelsonvil.le, Athens and Logan) $100,000.00. Percentage; 10.5

Nelsonvil le s a l e s $15,000.00. -111 s a l e s $75,000.03. Percentage 20%

1?elsonvil le pay ro l l $6.0~10.00, pay ro l l $20,030.00. Fercentage 3%

Business a l l o c u t i o n percentage:

equa l s --

Same corpora t ion owning no r e a l or t a n g i b l e personal property anywhere.. Vels i l l e s a l e s $15,000.00. r r l l s a l e s $75,000.00.. Perce!?tager 2056

Nelsonvil le pay ro l l $6,000.00. A l l pay ro l l $;?0.000.00. Percentage;-

Business a l l o c a t i o n percentages

p lus 30:5

- - equals* i!

Same corpora t ion owning r e a l and t ang ib le personal proper$$ i n Nelsonvil le a lued a t $10,000.00 and owning no r e a l or t a n g i b l e personal property ou t s ide -- e l s o n v i l l e . Other f a c t o r s same as i n exauiplos 1 arid 2.

Business a l l o c a t i o n p e r c e n t a ~ e :

Af ter de ter t~ l ia ing such 'busiriess a l l o c a t i o u percentage, t h e rax s l ia l l be de te ined by alply'ing t h a t Tercontage t o the e n t i r e n e t p r o f i t s of' tihe taxpayer , herever der ive$ ( tnus a r r i v i n g a t the t axab le n e t g o f i t ), and computing one e r c e n t oi' t h e r e s u l t a n t . t axable n e t p r o f i t .

I n case i t s h a l l appear t o the C i t y Auditor t h a t any agreement, unde r s tmdin tr arrangement e x i s t s between t h e taxpayer and any o the r person, f i m o r oorpor .ion, whereby t h e a c t i v i t y , bus iness , incone o r c a p i t a l of t h e t a x p y e r i s mproperly o r ~ i n a c c u r a t e i y r e f l e c t e d , the C i t ' j Auditor may a d j u s t i tems of incorn educt ions and c a p i t a l , am2 d is regard a s s e t s i n computing any a l l o c a t i o n percen ,ge, provided any income d i r e c t l y t r a c e a b l e t h e r e t o i s a l s o excludeci from e n t i r n e t income, s o a s equ i t ab ly t o determine the tax.

'pasn aq aousqsuj 3sa ny vmu xo& amoou1 TEJapad eya .lo asodana' at17 x o j pasn 2uyayad j o s ~ s s q aq,T,

'pasn oq i s n u sayxoquaAuJ *awoouy qoaxjax R.~xedoxd 0% X ~ ~ s s a o a u aaavj, (E)

'xaL amoo3u1: Tvaapa,~I jo esodrnd ayq xo.7 ancIobaU ysuao.iuI ,jo xoqaaxr@ nq$ Xq y m s 3 paz~d3ooa.z aq Lam ao uaaq suy 11: JJ Xruo pazyuaooax aq t j - f~ ~ e a A p o s y j tl

*$561 xequraoea TE Zuypn~out. pus 0% pus ;961 Rasnusp 3 a a q j s pus uo peuxna suo~qssued~ :~ : , xayqo xo/pus s a a j 'sucJssy~rniroa

'squamifsd aay$uaouy 'sosnuoq 'sa%n&i 'saJxs1ns aqq 0% qaadsex yqyn p p d pus k o e ~ p o ' p q a q aq qsxy j ~ p q s 2-11 PIXU 1-11 B T ~ J ~ J B UJ 0% paaxajax ~ 8 % ay&

jll (6) If t h e r e tu rn i s made on an "accrual basis ' , Oross h 0 f i . t s h a l l inc lude I ?

' / (I) coiiuaissions, f e e s and i n t e r e s t earned, p lus ( 2 ) t h e g ross p r o f i t or l o s s of merciian:iise, c h a t t e l s , goods, wares, s e c u r i t i e s , no tes , choses-in-

and s e r v i c e s , . . except a s h e r e i n a f t e r provided.

' j j (e ) F r m Cross P r o f i t Lhere shall . be s u b s t r a c t e l a l lowable expenses t o a r r i v , jl :,,at t h e n e t p r o f i t s s u b j e c t t o tax . 44

( f ) A l l ordiriery and necessary expenses of doin& bus iness , inc luding reason- jj jrablecoinpun~ation paid employees, s h a l l be allowed (bu t no deduct ion may be !claimed f o r * s a l a r y or withdrawals or a p ropr i e to r o r of t h e pa r tne r s , members 0

jother 00-owners of an unincorporated bus iness o r en te rp r i se . ) ill

(g) If n o t claimed a s p a r t of the Cost oi* Goods Sold 9 r elsewhere i n tine r e - urn f i l e d , there inay be claiiued and allowed a reasonable deduct ion f o r deprec ia ion . . dep le t ion . . obsolescence. l o s s e s r e s u l t i n g from t h e f t o r c a s u a l t y not ompensated f o r by insurance or otherwise, of property used i n the t;ril,ie or bus- ness , bu t the moun t may n o t exceed t h a t recognized t'or Ohe purpose of t h e Fed- r a l Income Tax. Provided, however, t h a t l o s s on t h e s a l e , exch@,eor o t h e r i s p o s i t i o n of deprec iable property md r e a l e s t a t e used i n business, sha l i riot b

lowed a s a deduc t ib l e expense.

, (h) Bad debts i n a reasonable amount inay be allowed i n t h e a sce r t a ined worth ;!less and charged o f f , o r ( i f the Reserve method i s used), a reasonable add i t iun , t o t h e Reserve may be claimed, b u t i n no event shn l l t h e moun t allowed excedd t $amount recognized as a deduct ian f o r the purpose of the Federal Income Tax.

( , ( i ) Tuxes. Only t axes d i r e c t l y connected wi th t h e taxpayer ' s bus iness may be 1 !:claimed as a d$duction. If f o r any reason t h e incorne from property i s not sub- !, jlject t o t ax , then tho t a x on sa id $ropertjj i s not deduct ib le . I n any event , the 44 fo l lowing t axes . . . a r e not deduc t ib l e from income: :I, I '

i! j I # # ( I ) The t a x ullder the Ordinance;

f r (2) Any Federal t axes based upon incoiiie; .)

:I :! (3) Gi:rts, estaLe o r inherLtance taxes, wid 1;

(4) Taxes f o r l o c a l b e n e f i t s or improvements t o proper ty whicli tend t o apprec ia te t h e va lue thereof .

L?,

( j ) Cap i t a l ga ins and l o s s e s (iilcludini; p i n s or l o s s e s from the s a l e , ex- il :change, o r ot i ler d i s p o s i t i o n of deprec iable business property, and r e a l propert) :used i n tine taxpayer ' s t r a d e o r Business) s h a l l no t be taken i n t o cons ide ra t ion j:in a r r i v i n g a t "Net P r o f i t s Earned#.. j

(k) If t h e taxpayer i s a n ~ n - r e s i d e n t , only t h e aziounr: of n e t p r o f i t s agplic t h e a c t i v i t i e s of t h e '.usiness i n Belsonvil.le branch, o f f i ce , s t o r e , o r a c t -

itq sepa ra t e ly , then t h e b a s i s of a l l o c a t i o n s h a l l be d i sc iosed i n the r e t u r n , such b a s i s of a l l o c a t i o n is n o t deemed c o r r e c t , i n view oi' a l l t h e known c i r .

mstances, +,he C i t y Auditor wi1.l make a r e a l l o c a t i o n based upon g ross r e c e i p t s any o ther b a s i s which s h a l l , under the circumstances o i t h e case, more accurr

f l ee t ; the n e t p r o f i t s .

(1) I n general , ail . bus iness expense recognized and t o t h e ex ten t allowed a1 uch f o r %he purpose 01: determining Federal Income Tax w i l l be recognized and ilowed f o r . . . d e t e m i ~ ~ ~ B e l . s o n v i l l e Income Tax u&er provis ions of Chis rdinance . . . Rowever, a i i expenses connected wi th a c q u i s i t i o n or ca r ry ing of e c u r l t i e s , th,e incorne from which i s not recognized a s t axab le under t h i s Ordint ay not be deducted i n a e t e n i n i n g taxable n e t p r o f i t s hereunder.

(m) I n genera l , unearned income i s n o t t o be included i n computing t h e t a x v i ed hereunder. Gain o r l o s s from the s a l e , exchange o r o t h e r d i spos f t ion of p i t a i a s se t s . including deprec iable property md r e a l e s t a t e used in bus iness ,

in11 not be inchuded i n determining n e t proi'itel, Income from in t ang ib le . . . y of dividends, i n t e r e s t and t h e l i k e , should not be included if t h e proper ty om which such income i s der ived i s s u b j e c t t o t axa t ion under t h e Intangib1.e r sonal Property Tax Laws of t h e S t a t e of Ohio, or i s s p e c i f i c a l l y exempted f r ~ xa t ion under s a i d laws.

(n) Rentals received by t h e taxpayer a r e t o be included only if and t o t h e t e n t t h a t t h e r e n t a l , ov~nership, management o r ope ra t ion of t h e r e a l esta.Le om which such r e n t a l s a r e derived (whether so ren ted , managed o r operated by xpayer ind iv idua l ly or through agents o r o the r r ep resen ta t ives ) cor i s t i tu tues I . . bus iness a c t i v i t y ok' t h e taxpayer i n whole or i n p a r t .

F'ollonir~g a r e circumstances under b ~ i c h . i n any ins tance , the rental. of any vea l proper ty s h a l l o r s h a l l no t be deemed t o be a "Business [I/ i;

(1) Where t h e gross monthly r e n t a l of any and a l l r e a l p rope r t i e s , r ega rd le .umber arid va lue , nggragates i n excess of $100.00 permonth , i t s h a l l be .a f a c i e evirience thut t h e r e n t a l , owner:ihip, management. o r opera t ion of auC ~ e r t i e s i s a bus iness a c t i v i t y of such taxpayer , and t h e n e t income of such ; a l property s h a l l be sub~ec5. t o tax ; provided t h a t i n Case of commercial ~ e r t y , t h e owner s h a l l be considered engaged i n a bus iness a c t i v i t y when t h e ; a l i s based on a f i x e d o r f l u c t u a t i n g percentage of gross o r n e t s a l e s . I ip ts o r p r o f i t s of t h e l e s s e e , whether o r not such r e n t a l exoeeds $luO.uu pe ;h; provided f u r t h e r t h a t i n t h e case of farin proper ty t h e ormer s h a l l be ; idered engaged i n u bus iness a c t i v i t y when be sha res i n t n e crops o r when t h ;a1 i s bused on a percentage of t h e gross o r n e t r e c e i p t s der ived from the is. whether or n o t .the gross income exceeds $1.00.00 pe r month; and providdd - ;her t h a t t h e person who opera tes a rooming house s h a l i be considered i n .ness whether o r not t h e gross income exceeds $I.u0.00 per month.

(a) I n d e t e m i n i n g t h e smognt of gross monthly r e n t a l of any r ea l property, ioda du r ine which (by reason of vacancy o r any o t h e r cause) r e n t a l s a r e not , ived shall . no t be taken i n t o cons ide ra t ion by t h e taxpayer.

(3) Rentals received by a taxpayer eneaged i n t h e bus iness or buying and Ling r e a l e s t a t e s h a l l be considered s s g a r t of bus iness income.

(4) Real property, a s t h e term i s used i n the Regulation, s h a l l inc lude nerBial property, res ident ia l . p roper ty , fann property. and any and a l l t y p e s Peal property.

(5) In determining t n e taxable net; income from r e n t a l s , t h e deduc t ib l e m s e s s h a l l be of' t h e same nature, ex tun t and amount a s a re ailowed by t h e srtment of I n t e r n a l Revenue f o r Federal Income Tax purposese

( 6 ) Residents of Nelsonvi l le a r e s u b j e c t t o t a x a t i o n upon t h e n e t incorne n ren ' ta i s ( t o t h e e x t e n t above spec i f i ed ) r e&%rd les s of t h e l o c a t i o n of' t h e 1 proper ty owned:

Ron-residents of Nelsonvi l le a r e sub jec t t o such t axa t ion only i i t h e perty i s siLuated wi th in tile C i t y of Nalsonvil le . Non-residents, i n da t e r - ing whether gross nontn ly r e n t a l s exceed $100.00 s h a l l take i n t o cons idera t ior q r e a l e s t a t e s i t u a t e d wi t , i l r~ l je isonvil le .

(0) Income. . . froin r o y a l t i e s o r copyrig!lts i s not 'ao be included.

ARTICLE 11 - 10

RECOMCILU&TION W E PEDEBBL RETURN

In a form s a t i s f a c t o r y t o t h e C i t y Auditor, t h e r e s h a l l be s u b a i t t e d wi th ch r e t u r n f i l e d by a taxpayer s u b j e c t t o the Federal Income Tax, a r econc i l i a . on between t h e amount shown i n t h e r e t u r n f i l e d w i t h the Ci ty Auditor and t h e s i n e s s income repor ted t o t h e Federal Bureau of I n t e r n a l Revenue.

If, a s a r e s u l t of a ohange made i n business income by the Federal. Bureau o, t e r n a l Revenue, o r by a ; ludicla1 dec is ion , an add i t iona l amount w i l l r e s u l t a ; ing t o t h e C i ty of Welsonvill,e, a r epor t of such change from the fad era^ t h o r i t i e s o r a f h r Final dec i s ion of a Court ad jud ica t ing any such Federal come Tax l i a b l i i t y . .

ARTICLE 111

1. On or before 15 Apr i l 1968, every taxpayer engaked i n nny bus iness , t h e t p r o f i t s of which a r e s u b j e c t i n whole or i n p a r t t o the t a x imposed by this dinance, s h a l l make and f i l e wi th the C i t y Auditor a f i n a l r e t u r n on a form rnished 'by or obta inable froiri t h e C i t y Auditor, Thereaster , each such tax- yer s h a l l , on o r be fo re lj Apr i l of' each subsequanb yea r , make and f i l e a fir11 t u r n with t h e C i Q Auditor. Like r&urns s h a l l be f i l e d a t the sarne Lime an(

t h e same manner by a l l persons whose wages, s a l a r i e s , bonuses, i ncen t ive yments, cobunissi ons, f eos and o the r compensation rece ived during t h e 2recedf nl xable yea r a r e s u b j e c t t o t h e t a x imposed by t h e Ordinance. However, where

eri~ployee's e n t i r e ea rn ings f o r t h e yea r a r e paid by an employer and t h e one rcemt t a x thereon has i n each ins tance been withheld and deducted by the ployer from t h e gross amount of t h e e n t i r e earn ings of such employee-taxpayer .i where t h e employer o r such employee has f i l e d a r e p o r t o r r e t u r n i n which ch employee's e n t i r e and only earnings a r e repor ted t o t h e C i ty Auditor, and e r e such employee. has no t axab ie income o ther than such earnings, it s h a l l 'no

necessary f o r such employee t o f i l e a r e t u r n f o r any taxable year i n which oh condi t ions have prevai led.

?my person who rece ives both compensation f o r s e r v i c e s performed f o r an ployer i n whatsoever form and i n a d d i t i o n r ece ives income from any h u ~ i n e s s

Page 10

a c t i v i t y of occupation not sub jec t t o wi t~ ihold ing under the Ordinance, must f i l e a d e c l a r a t i o n and a f i n a l re turn .

P,. I n a l l r e t u r n s f i l e d hereunder t h e r e s h a l l be s e t f o r t h t h e aggregate amount of s a l a r i e s , wages, bonuses, i ncen t ive payments, commissions, f e e s and other compensaGion rece ived and/or n e t p r o f i t s earned ( a l l a s here inbefore defxned) by an3 during t h e preceding year arid s u b j e c t t o s a i d tax, toge ther witn such p e r t i n e n t information as che C i ty Auditor may require .

;j id

3. If' t h e r e t u r n i s made !'or a f i s c a l year or f o r any period o t h e r than a 3 ca lendar year , the s a i d r e t u r n sha l l , be made wi th in one hundred f i v e (103) days 'j from t h e end of s a id f i s c a l year o r o t h e r period. Cl $!,

4. The r e tu rn s h a l l a l s o show t h e amount of t h e t a x imposed by the Ordinance : j ,:r on such earnings, or n e t p r o f i t s , o r bo.th. 9

5. The taxpayer making t h e r e t u r n s h a l l a t t h e t h e of f i l i n g thoreof , pay t o t h e C i ty Treasurer t h e amount of t a x shown t o be due and unpaid by tho ro tur r If, pursuant t o t h e provis ions of' A r t i c l e V - 2, t h e taxpayer has a t t ho t i a e Of

making such f i n s 1 r e t u r n overpai3 h i s t ax , such taxpayer s h u l l skiow the ,m~oun't of overpayment and may i n s a i d r e t u r n e i t h e r (a ) reques t a refund the re fo r , o r ( 5 ) r eques t t h h t Cie amount tilsreof be c r e d i t e d s g a i n s t t h e mount w'nich will be requi red t o be paid by taxpayer on the next succeeding ins t a l lmen t of t a x which mag beco!m due.

For p a p a n t s i n in s t a l lmen t s , see A r t i c l e V - 3,. 6. Where any p o r t i m oY t h e t a x otherwise due s h u l l have been deducted a t

t h e source and shal.1 have been paid 'to the C i ty Treasurer by the person making t h e s a i d deduction, a c r e d i t equal t o t h e amount s o paid s h a l l be deducted from t h e amount shown .to be due and only t h e 'balance, i f any, s h a l l be due and pay- ab le a t the time of tile f i l i n g of' t h e s a i d re turn .

7. Upon w r i t t e n reques t of t h e taxpayer , t h e C i ty Auditor may extend b e t i a e f o r f i l i n g t h e annual r e t u r n f o r a period of n o t roore than s i x inontas or n more than t i i i r t y days beyond my e x t e ~ ~ s i d n requested ol and granted by t h e Bureau of I n t e r n a l Revenue f o r 1 i l i n ~ of t h e Federal Income Tax Return.

E., 1% is the duty of each employer ( a s here inbefore defined) who employs on' o r more porsons on a sal.ary, wage, comu~ission, o r o t h e r compensation b a s i s , t o deduct from compensation paid t o any employee sub jec t t o tho Ordinance t h e t a x of one percent of such sa l a ry , wage, bonus, i ncen t ive payment, comnission or o ther compensation due b;r s a i d employer t o s a i d employee. The t a x s h a l l be deducted by t h e employer from:

j (a ) A l l compensation paid t o employees who a re non-residents of tho C i ty of ; Nelsonvi l le f o r s e rv ices rendered, work performed, or o t h e r a c t i v i t i e s engaged 1; t o ea rn such co!npensation, w i th in t h e C i ty of i ie l sonvi l le ; tlnd ,;,

h i (b) Froir! t h e g ross amount of a l l s a l a r i e s , wages, bonusos, i ncen t ive pay- ments, co:missions o r o ther form of compensation paid t o employees who a r e

11 11: r e s i d e n t s of t h e C i t y of Nelsonvil le , r ega rd le s s of t h e place where t h e se rv ioe a r e rendered. I!

2.. A 1 1 employers who or which maintain an o f f i c e o r o t h e r p lace of business i n Nelsonvil le a r e requi red t o make t h e col.lec.tions and deductions i n t h i s A r t i c l e spec i f i ed , r ega rd le s s of t h e f a c t t h a t t h e s e r v i c e s on account of which any p a r t i c u l a r deduct ion i s r equ i red a s t o r e s i d e n t s of t h e Ci ty of Nelsonvil le were performed a t a p l ace of bus iness of' any such employer s i t u a t e d ou t s ide tile C i t y of Melsonville.

(:I 3.The mere f a c t t h a t the t a x i s not witilheld w i l l no t r e l i e v e .the e!nployee ?'; of t h e r e s p o n s i b i l i t y of f i l i n g a r e t u r n and paying t h e t a x on the compensation I . ,#; k:! received. i l l

4. Cornmissions and foes paid t o profess ional men, brokers , wid o t h e r s who a r e independent c o n t r a c t o r s and n o t employees of the payor, a r e mot sui i ject t o withholding o r c o l l e c t i o n of t h e wax a t t h e source. Such taxpayers must i n a l l i n s t ances f i l e r e t u r n s and pay the t a x pursuant t o t h e provisions of Sect ion 2 o r of Sec t ion 3 of t h e Ordinance. (See A r t i c l e 11 - 3 arid I1 - 4)

" /I 5.111 t h e case oP employees who a re r e s i d e n t s of Nelsonvil le t h e moun t t o b 'I !I deducted is one percent of the compensation paid wi th r e s p e c t t o personal fi j s e r v i c e s rendered i n Nelsonvil le . !Y 1 Pwge 11 4

For adjustment of e r r o r s i n r e t u r n s of t a x withheld by employers see ~ r t i c l c I - 3 of' t h e s r egu la t ions .

The f a i l u r e of' any employer, r e s idng e i t h e r w i t h i n o r outs ide t h e C i ty of l s a n v i l . l e , t o col lec 'k the t a x and t o nuke any r e t u r n prescr ibed here in , sha1.1 ~t r e l i e v e t h e ernployce from t h e payment of such t a x i n compliance with t h e s e ~ g u l n t i o n s r e spec t ing the making of r e t u r n s and thepayment QB taxes.

Every employer is deemed t o be a t ru scee of t h e C i ty of Welsonville i n , I l ec t in t ; and holdink tho t a x requi red under the Ordinance t o be 'vithheld, and ie funds s o c o l l e c t e d by such ivitkiholding a r e deomed t o be t r u s t funds.

Every such employer requi red t o deduct and withhold t h e t a x a t t h e source i s .ab le d i r e c t l y t o tho C i t y of Nelsonvi l le f o r the payment of such t ax , whether ; t u a l l y c o l l e c t e d by such employer o r not&

1. An employee whose e n t i r e wages, s a l a r i e s , o r o t h e r cornpensation f o r any ixnble year w i l l be subjec ted t o t h e withholding provis ions under A r t i c l e IV of i e se 13egulations, whose t a x v i l l accordingly be withhe1.d a s t o h i s e n t i r e earn- igs f o r such year by h i s employer, and who during such taxab1.e year expects t o w i v e no o the r coruponsation o r o the r incosue which i s sub jec t &@ t a x under the rdinance, need not f i l e a d e c l a r a t i o n a s provided i n t h i s ~ r t f o i e .

2. A l l o t h e r taxpayer ( a s :iefined i n t h e Ordinance and i n these Regulat ions) ~ b j e c t t o the taxes imposed i n Sec t ion 2 of t h o Ordinance,and every taxpayer wh i t i c i p a t e s any income o r n e t p r o f i t s not s u b j e c t t o t o t n l withholding as pro- ided i n t h e n e t preceding paragraph, s h a l l f i l e with t h e C i t y Auditor u. dec la ra Lon of h i s estirnated t a x as follows:

3. On or before 15 Apr i l , 1960, every such taxpayer s h a l l r i l e a dec la ra t ion t' h i s e s t i u a t e d t a x f o r t h e taxable period beginning 1 January, 1968, and iding 31 December, 1968.

4.. A s imi l a r d e c l a r a t i o n s h a l l be f i l e d by each such taxpayer on or before no 15 day of Apri l of each subsequent year dur ing t h e l i f e of t h i s Ordinance, ad each such d e c l a r a t i o n s h a l l con ta in a statemerrt of t h e t&xpayer4s e s t i n ~ a t e d ax f o r the f u l l t axab le yea r i n which such deolarmtion i s f i l e d .

5,Taxpayers who o r which a re permit ted, pursuant ba t h e provis ions of ,%rticl I - 8 t o r e t u r n and pay t h e i r t a x upon a f i s c a l year b a s i s , s h a l l f i l e t h e i r irst d e c l a r a t i o n wi th in lu5 days a f t e r t h e beginning of t h e f i r s t f i s c a l year eginning a f t e r 1 January, 1968 and t h e subsequent d e c l a r a t i o n f o r each year he rea f t e r on o r before t h e 15 day of t h e f o u r t h month fol lowing t h e bogimning c ach such f i s c a l year.

6. The est imated t a x inay be paid i n f u l l wi th t h e d e c l a r a t i o n o r i n equal nstallrnents on o r before 15 Apr i l , 30 June, 30 September, and 31 Decembar, t h e irst f i l i n g being as of 15 Apri l , 1966. Those taxpayers on a f i s c a l year b a s i ~ h a l l make q u a r t e r l . ~ payments on or before the 15 day of t h e fou r th month-land on r before t h e l a s t day of t h e s i x t h , n in th , and twe l f th month fol lowing t h e eginrning of' such f i s c a l year . The f i r s t ins ' ta l lment , equal t o a t l e a s t one- ou r th o f t h e estisnated tax , m u s t accompany t h e dec la ra t ion .

7- The d e c i a r a t i o n s o requi red s h a l l be f i l e d upon a form furnishad by or btltixiable from t h e C i t y Auditor. ilny taxpayer who has f i l e d an estirnate f o r ede ra l Incorne Tax purposes may, i n making t h e dec la ra t ion , requi red hereunder, imp1.y s t a t e t h e r e i n t h a t t h e f i g u r e s t h e r e i n contained a r e t h e same f i i jurus use y tha taxpayer i n making t h e dec iu ra t ion of' h i s e s t i n a t e f o r the Federal Tncorne ax. However, i n a d d i t i o n t o such stratemen't, aqy such taxpayer may, i n such e c l a r a t i o n , modify and a d j u s t such dec lared income so as t o exclude tl ierefrol:~ ncome which i s not sub jec t t o t a x under t h e Ordinance.

8. Any est ixlate f i l . ed heroundor may be amended by tho r i l i n g oi' an wriended st i rnate a t the time prescr ibed f o r the payment of any ins ta l l rneni oi' t a x paid i ccordance wi th A r t i c l e V - 2 of these Regula t ions . .

ARTICLE V - 2

Page 13

PAYMENT OF 'TAX INSTILLLIEENTS

Z.. A t t h e time of f i l i n g each d e c l a r a t i o n ( requi red by A r t i c l e V - 1 ) each ;axpayer s h a l l pay t o t h e C i t y Treasurer one-fourth (2) af t h e amount of h i s rstimated annual tax. Thereafter , on o r before t h e 30 day of gune, September, ~ n d December 31 of each year during t h e l i f e of t h e Ordinance, such taxpayer rha l l pay a t l e a s t a s i m i l a r amount. Bowever. if any such taxpayer s h a l l , on o ,efore any such payment d a t e , f i l e an amended d e c l a r a t i o n showing an inc rease o lecrease of t h e estima.t;ed t ax , t h e in s t a l lmen t s then and t h e r e a f t e r due s h a l l b increased o r dimisished ( a s t h e case may be) i n such manner t h a t t h e b&lance of the es t imated t a x s h a l l be f u l l y paid on o r before Becember 31 of t h e t axab l s rear involved through t h e payment of q u a r t e r l y in s t a l lmen t s i n equal amounts iur ing the q u a r t e r l y periods remaining from and a l 0 e r t h e f i l i n g of any such mended dec la ra t ion .

2. Taxpayers who o r mhic!l a r e permit ted t o make r e t u r n s and pay t h e i r t a x o i f i s c a l year b a s i s ( see A r t i c l e I1 - 8). may make t h e q u a r t e r l y payments on t h e i r d o c l a r a t i o n of est imated t r x pursuant t o A r t i c l e V - 1 6 ) ( 6 ) of these iegual t ions .

3. For f i n a l r e t u r n s and f i n a l adjustr:ierrt of t a x due, s ee A r t i c l e 111.