Impact of the crisis An OECD Experience IFR - 2010 Elias Masilela September 2010.

60

Impact of the crisis An OECD Experience IFR - 2010 Elias Masilela September 2010

-

Upload

eugene-booth -

Category

Documents

-

view

213 -

download

0

Transcript of Impact of the crisis An OECD Experience IFR - 2010 Elias Masilela September 2010.

Impact of the crisis An OECD Experience

IFR - 2010

Elias MasilelaSeptember 2010

Road map

What we said last year?

What has been the turnout?

What the future has in store?

How should we respond?

Global

Economic backdrop

Crisis chain … a vicious circle

Age of new challenges

"Last year it was banks; this year it is countries."

"Some of today's nervousness comes from policy risk ".

Economist, 13 February 2010, pg 9

Broad recap

Immediate challenge is about restoring

growth

Crisis is increasingly social in nature

i. No longer dual, but multi-crisis

Retirement funds have been a major victim

Silver lining?

Macro stability back on to the agenda

Urgency of proper reforms

Forced rethink on early retirement

Regulatory issues high on agenda

Global

macro conditions

Global overview Slow economic turnaround Impact of uncoordinated interventions

withdrawalsi. Real possibility of a vicious circleii. Double dip

Declining productivity Global trade decline Unemployment becoming deep seated

i. Youth unemployment

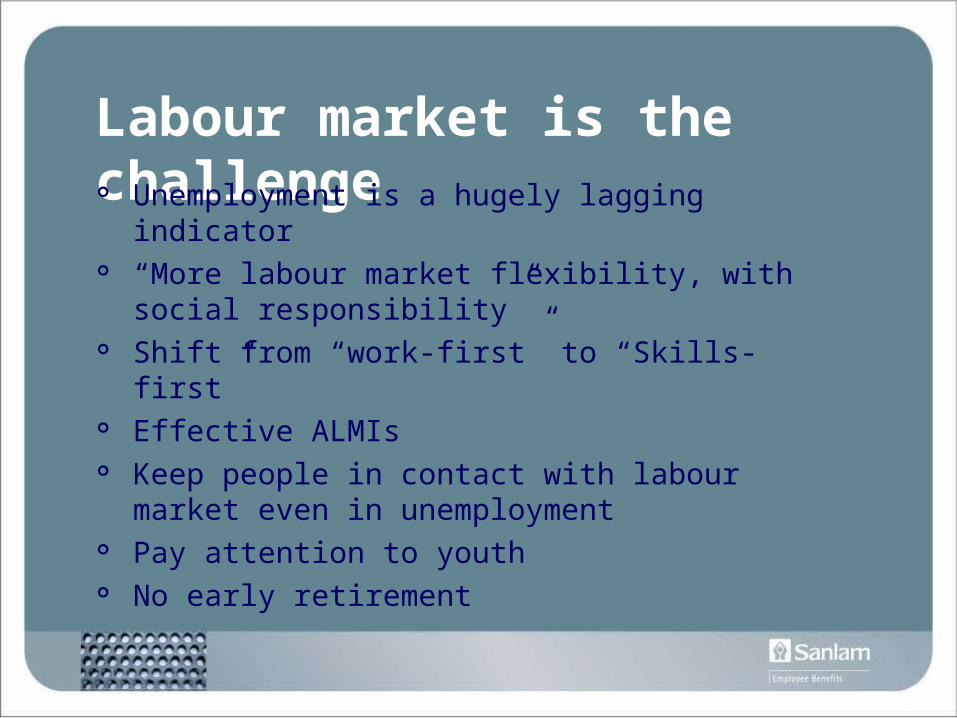

Labour market is the challenge Unemployment is a hugely lagging indicator “More labour market flexibility, with social

responsibility” Shift from “work-first” to “Skills-first” Effective ALMIs Keep people in contact with labour market

even in unemployment Pay attention to youth No early retirement

Global

lessons on

bank crises

Lessons Bank crises have deeper and longer

term impact than non-bank crises

Consistent across all sectors of the economy

Impact on growth

:Source: Haugh David, Ollivaud Patrice and Turner David, 2009

30.5

12.7

-5.4-3.3

5.3 3.3

-10

-5

0

5

10

15

20

25

30

35Duration of downturn (Q's)

Trough in output gap

Recovery half life

bank non-bank

Impact on investment

Source: Haugh David, Ollivaud Patrice and Turner David, 2009

Investment Gap

-34.0

-3.2

-25.1

-7.4

-0.6

3.1

-40

-35

-30

-25

-20

-15

-10

-5

0

5

ResidentialBusinessConsumption

bank non-bank

Impact on fiscus

Source: Haugh David, Ollivaud Patrice and Turner David, 2009

fiscal gap (peak to trough)

ExpenditureRevenue

Fiscal balanceDebt

8.3

3.51.5 2.2

-7.3

-1.3

20.6

8.7

-10

-5

0

5

10

15

20

25

bank non-bank

But it became an economic crisis.

Higher unemployment and pressure on wages cuts revenues from taxes and contributions

Declining output

Rising unemployment

Ballooning budget deficits

-5

-4

-3

-2

-1

0

1

2

3 2007

’08

’09

’10

’112007

’08

’09

’10

’11

0.0

2.5

5.0

7.5

10.0

2007

’08

’09 ’10

’11

-10.0

-7.5

-5.0

-2.5

0.0

OECD experience

Source: Edward Whitehouse and OECD, 2010

Debt overhang… (Finweek, May 2010)

Gross domestic product

E 5

Source: SARB

Household consumption

E 11

Source: SARB

Household debt

E 14

Source: SARB

Gross fixed capital formation

E 13

Source: SARB

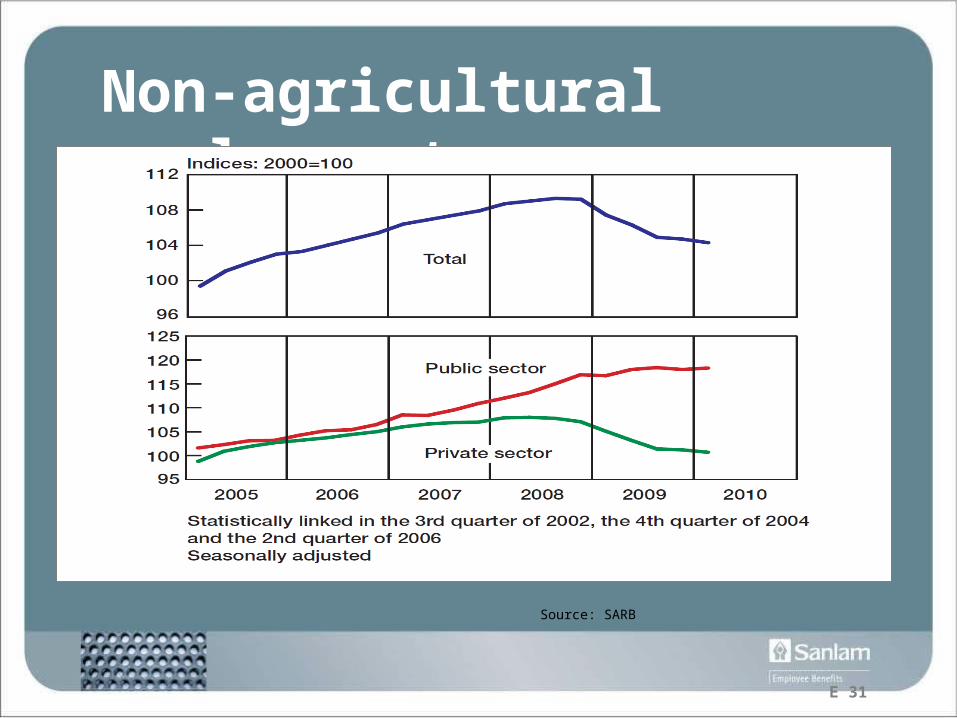

Non-agricultural employment

E 31

Source: SARB

Prospects?

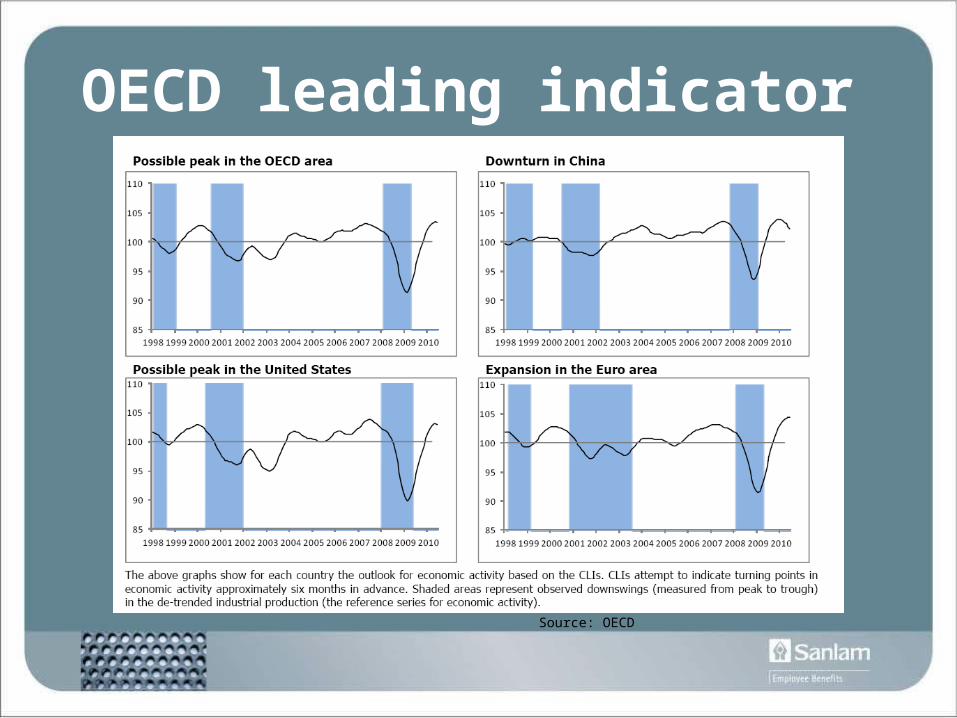

OECD leading indicator

Source: OECD

SA composite leading indicator

Manufacturing production

E 22

Source: SARB

Mining production

E 23

Source: SARB

Turnaround will be hampered Debt overhang

Fiscal constraints

Inflexibility in markets

i. Labour market in particular

Capital constraints

Poor savings base

Impact on

OECD

retirement

Investment returns

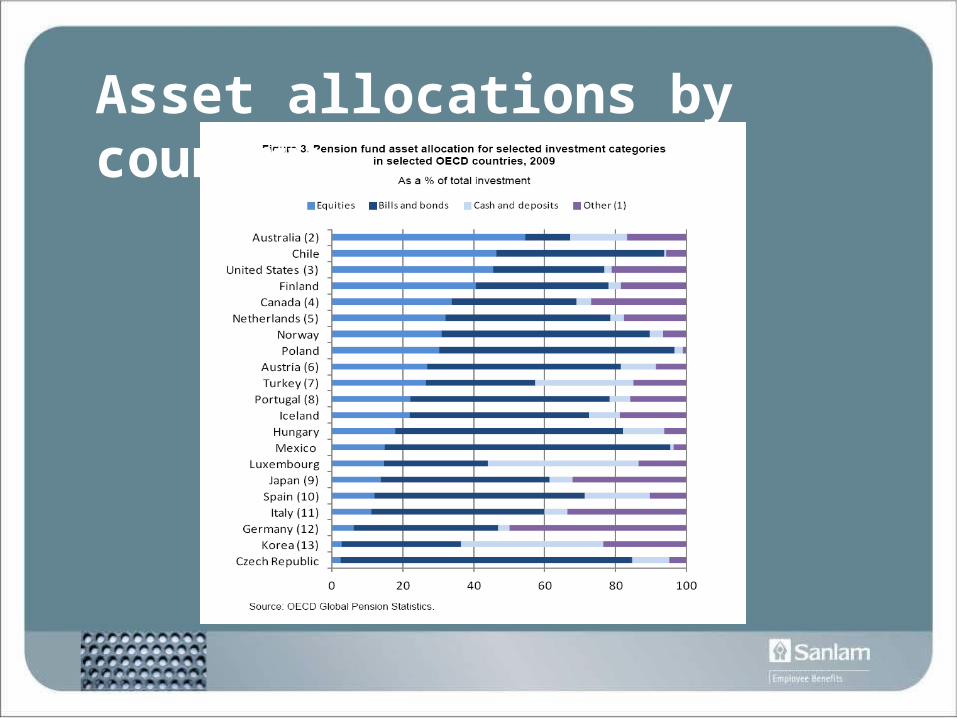

Asset allocations by country

“Pension fund assets struggle to return to pre-crisis levels” (OECD, July 2010)

Only made up USD 1.5 trillion of the 3.5 trillion 2008i. 6% real returns in 2009

Funding rates average 75% Outside the OECD area, pension funds

suffered less in 2008 and have also recovered quicker in 2009

What the

Europeans say?

Retirement optimism

Source: AON Consulting, July 2010

EU Retirement gap

Source: AON Consulting, July 2010

EU Retirement gap

Source: AON Consulting, July 2010

Source: AON Consulting, July 2010

Key concerns

Source: AON Consulting, July 2010

Delaying retirement

Policy

Responses

Macro policy responses Restoration of trust/confidence Keep fiscal and monetary policies

expansionary for longer Avoid protectionism Align short term social protection with longer

term structural goals Stronger labour force participation Step up education and financial literacy Implementable withdrawal strategies

Financial sector responses Reform financial regulation and new

instruments Focused interventions:

i. Guarantees

ii. Remove toxic assets

iii.Recapitalise

iv.Get out

Impacting retirement funding Grow incomes Retirement ages continue to increase Unsustainable public systems

i. Promises growing faster than national incomes

ii. Promises being reviewediii. Replacement ratios declining

Difficult balance between financial and social sustainability

Response to collapsing savings Encouraging voluntary savings Incentivising switching to private

schemes

Responses to social pressures Stronger social safety nets

Once off payments as part of stimulus

packages

Early access to savings

Encourage workers to move to less

risky assets

Challenges for individuals Live longer, work longer

Avoid early retirement and/or disability

Restoring confidence

Cultural and behavioural changes

Education

Policy reversal risk

“… governments may …

backtrack on earlier

reforms as labour market

conditions worsen.” Pensions at a

Glance, 24 June 2009

Outlier

“Australia”

Macro-economy Healthy macroeconomy

i. Strong reinvestments Never went into recession Whilst the ROW was cutting they were

tightening in H2 2009 Strong fiscal position Strong investment trajectory

i. Build Australia fund, 2008-09 Strong China links

Labour market Rising productivity

i. Labour prod (3,3% 1993-1999) Rising employment Labour market flexibility

i. Decentralised wage bargaining Deep technological application

i. Despite importing 98% of it

Regulatory environment

Sound retirement regime

Sound regulation in fin sectori. Wary of sub-prime lending

- Increased capital req for risky loans in 2004 (Low-doc)

ii. Prudential regulation is taken seriously

iii. Continuous improvement in regulation quality

- Good lesson for BEE in SA

Institutions are key

Emphasis on institutional capacities

Department of Finance and deregulationi. Effective communication with private sector

Serious on RIAi. Preserve competition and productivity

ii. Reduce costs and complexity

Response to crisis

Only strategic and targetted fiscal stimuli

Ambitious reg programme

Responsible fiscal and mon pol responses

Manage future pension liabilities

What we learn

Long term planning

Decisiveness

Strong and predictable institutions

Effective communication

Beyond

the crisis

Global retirement reforms Shift from DB to DC continues

Enhanced governance

Risk management is being escalated

Education is deepened

Jobs

OECD-wide interventions Job subsidies Reduction in non-wage labour costs Public sector job creation Short-time week Job search assistance Training programmes Work experience Business start-up assistance Support for apprentices Unemployment benefits Social assistance Other support for job losses

Thoughts

to take away

How committed are we…? Are we serious in creating and

preserving sustainable jobs? Are we moving fast enough to

establish requisite institutions to deal with retirement?

Have we exerted sufficient effort to preserve trust and certainty in the industry?

Is it not time for a social compact?

SIYATHOKOZASIYABONGASIYABULELAROLIVHUWA

HI NKHENSILETHANK YOU

DANKIEMERCIContacts: