Impact of Tax Reform on Individuals - Windham Brannon Ta… · • Employer provided education...

58

Impact of Tax Reform on Individuals Barbara Coats, CPA

Transcript of Impact of Tax Reform on Individuals - Windham Brannon Ta… · • Employer provided education...

Impact of Tax Reform

on IndividualsBarbara Coats, CPA

Tax Cuts and Jobs Act of 2017

• House Passage of HR-1• House of Representatives passed bill by vote of 227-205

on November 16• Thirteen Republicans voted against bill• All but one of House Republicans who voted no are from

New York, New Jersey, and California• No Democrat voted for it

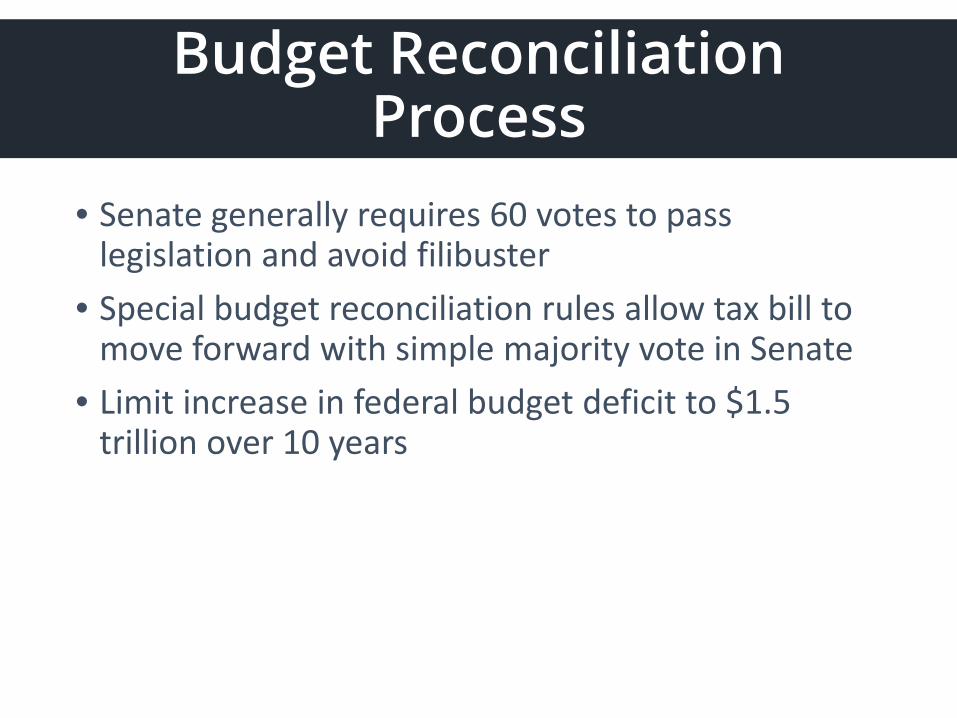

Budget Reconciliation Process

• Senate generally requires 60 votes to pass legislation and avoid filibuster

• Special budget reconciliation rules allow tax bill to move forward with simple majority vote in Senate

• Limit increase in federal budget deficit to $1.5 trillion over 10 years

Chances of Passage in Senate

• Final Senate vote could come as early as November 30• There are 52 Republican Senators• Sen. Ron Johnson (R-Wisconsin) and Steve Daines (R-

Montana) argue that tax rates on pass through entities are too high

• Sen. Susan Collins (R-Maine) opposes repeal of health care mandate

• Sen. Jeff Flake (R-Arizona) and Bob Corker (R-Tennessee) are concerned about budget deficits

• Other possible swing votes: Sen. John McCain (R-Arizona) and Sen. Lisa Murkowski (R-Alaska)

#WBInsights17

Tax Brackets for Married Couple Filing Jointly

$- $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 $900,000

$1,000,000 $1,100,000

2017 House

10% 12% 15% 25% 28% 33% 35% 39.6%

Taxa

ble

Inco

me

Tax Brackets for Single Individual

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

2017 House

10% 12% 15% 25% 28% 33% 35% 39.6%

Taxa

ble

Inco

me

Tax Bracket for Trusts & Estates

$- $2,000 $4,000 $6,000 $8,000

$10,000 $12,000 $14,000 $16,000 $18,000 $20,000

2017 House

12% 15% 25% 28% 33% 35% 39.6%

Taxa

ble

Inco

me

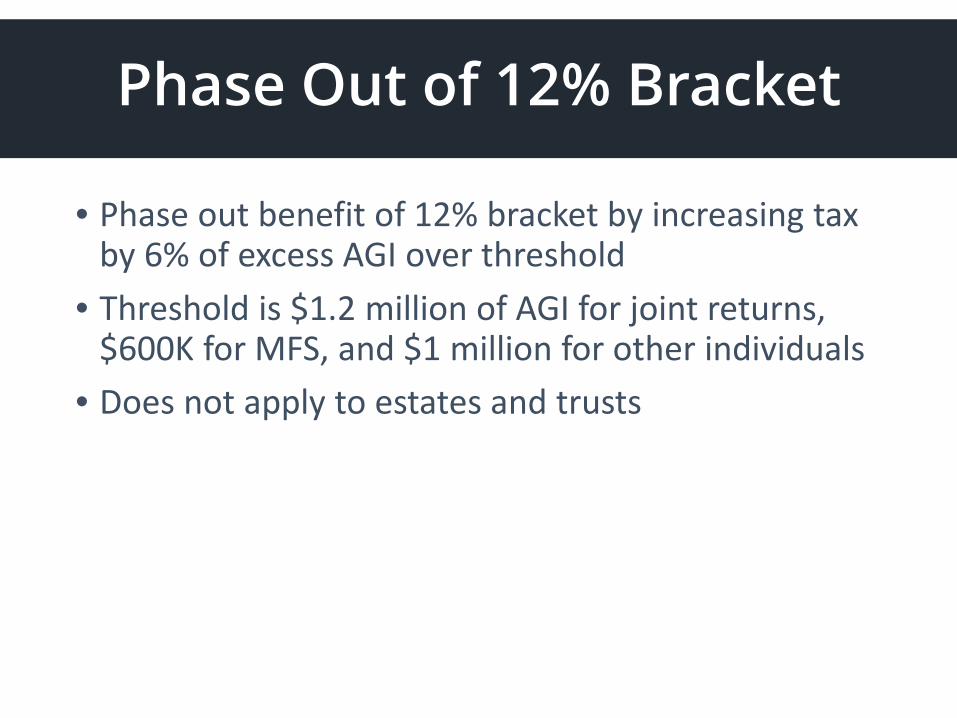

Phase Out of 12% Bracket

• Phase out benefit of 12% bracket by increasing tax by 6% of excess AGI over threshold

• Threshold is $1.2 million of AGI for joint returns, $600K for MFS, and $1 million for other individuals

• Does not apply to estates and trusts

Capital Gains Tax Rates

• 0% capital gains tax rate for taxpayers in 12% bracket

• 15% capital gain tax for 25% and 35% brackets• 20% tax rate for 39.6% bracket taxpayers

Change in Inflation Indexing

• Current tax brackets and exemptions adjust for Consumer Price Index (CPI)

• House bill ties inflation indexing to Chained CPI• Chained CPI assumes that consumers will choose

less expensive substitutes in inflationary times. • Consumers’ reduction of quality of consumed

goods reduces inflation

Divorced Taxpayers

• Currently, alimony is taxable to recipient and deductible to payor

• House bill provides that alimony will not be taxable or recipient nor deductible by payor

• Effective for agreements executed after 2017• No provision in Senate bill

Repeal of Tax Free Fringe Benefits After 2017

• Dependent care assistance programs – current exclusion is maximum of $5,000 per employee per year

• Qualified tuition reduction – attention Emory University Courtesy Scholarship families!

• Employer provided education assistance – $5,250 per employee is currently tax free

• Employer provided housing• Adoption assistance programs – currently $13,570 per

adoption; phases out for higher income taxpayers• Employee achievement awards – currently tax-free up

to $400 per employee for nonqualified awards and $1,600 for qualified awards

Capital Gains – Cost Basis Choices

• Current law provides choice of methods to use for cost basis when selling securities. Choices are average cost, first in, first out (FIFO) and specific identification

• House bill does not change current law• Senate bill requires that cost basis of securities sold

after January 1, 2018 use FIFO except to extent that average cost is otherwise allowed

Sale of Principal Residence: Gain Exclusion

• Gain exclusion limited to $500K for joint filers and $250K for singles; does not change

• Currently available if live in home for 2 out of past 5 years

• House bill provides gain exclusion only if live in home for 5 out of past 8 years

• House bill provides exclusion can only be claimed once every 5 years

• House bill phases out exclusion by $1 for every dollar of AGI over $500K for joint returns and $250K for singles; average of income for year of sale and 2 immediate prior years

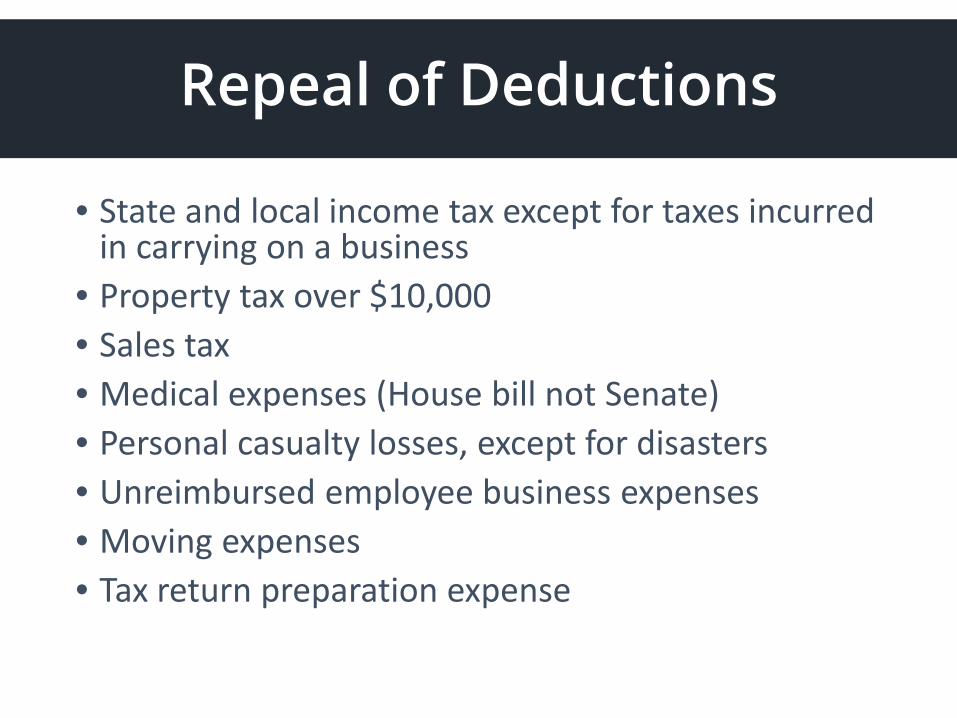

Repeal of Deductions

• State and local income tax except for taxes incurred in carrying on a business

• Property tax over $10,000• Sales tax• Medical expenses (House bill not Senate)• Personal casualty losses, except for disasters• Unreimbursed employee business expenses• Moving expenses• Tax return preparation expense

Mortgage Interest Deduction

• Current interest deduction• $1 million of acquisition debt ($500K for MFS) and

$100,000 of home equity debt ($50K for MFS)• Principal residence and one other residence

• House bill• Grandfathers existing debt, including refinancing• Limits deduction to interest on $500K of debt incurred

after November 2, 2017• Can only deduct interest on a principal residence• Interest on home equity debt is non-deductible

Charitable Contributions

• Cash contributions currently limited to 50% of adjusted gross income (AGI)

• Change cash contribution limit to 60% of AGI after 2017• Repeals 80% charitable deduction for contributions to

university athletic seating rights• New standard mileage rate for charitable use of an auto• Repeals the exception that allows charities to file a

return with required documentation rather than delivering information to donor directly

“Pease” Limitation on Itemized Deductions

• Requires higher-income individuals to reduce itemized deductions

• Lesser of 3% of AGI above a threshold or 80% of itemized deductions

• Threshold is AGI over $313,180 for joint filers and $261,500 for singles

• House bill repeals Pease limit

Education Funding Accounts

• Coverdell Education Savings Accounts• Prohibit contributions after 2017• Provides tax-free rollover into Section 529 plans

• Section 529 Plans• Distributions of up to $10,000 per year may be used for

qualified expenses for elementary school and high school

• Qualified expenses include expenses associated with apprenticeship programs

• Unborn child (in utero) may be named as a designated beneficiary

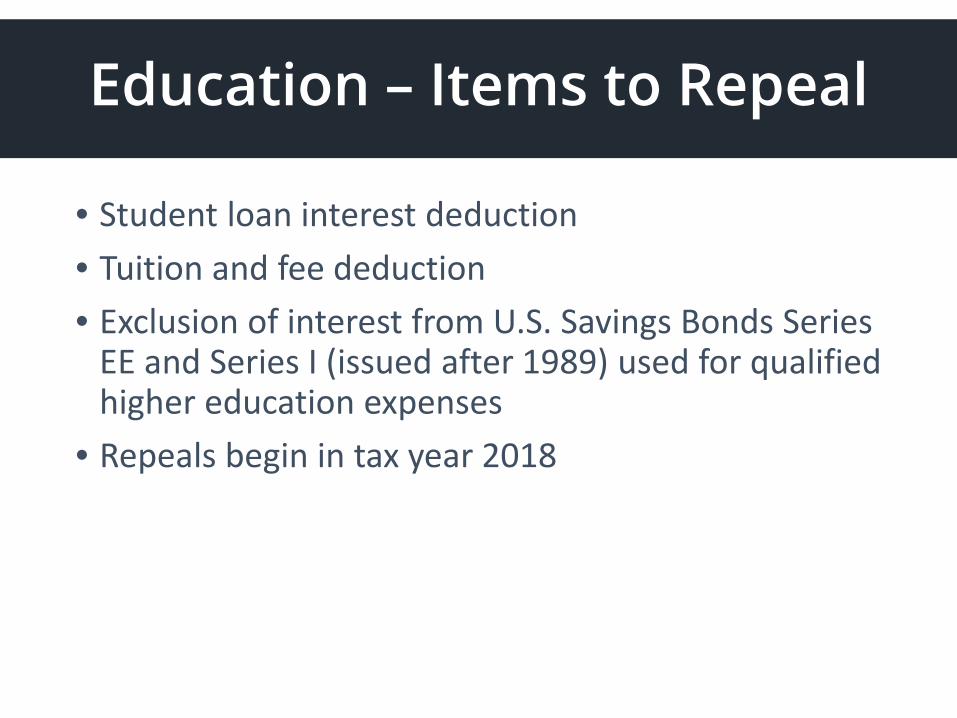

Education – Items to Repeal

• Student loan interest deduction• Tuition and fee deduction• Exclusion of interest from U.S. Savings Bonds Series

EE and Series I (issued after 1989) used for qualified higher education expenses

• Repeals begin in tax year 2018

Standard Deduction

Personal Exemptions

• Currently $4,050 per person• Phases out for married couples beginning with AGI

of $313,800 and $261,500 for singles• House bill repeals at end of 2017 & consolidates

into standard deduction

Alternative Minimum Tax

• House bill repeals for 2018 tax year• Currently, taxpayers receive a tax credit for all or

some of AMT paid in prior years• House bill allows refund claims for 50% of

remaining AMT credits in 2019, 2020, and 2021• Taxpayers can claim refund for 100% of remaining

credit in 2022

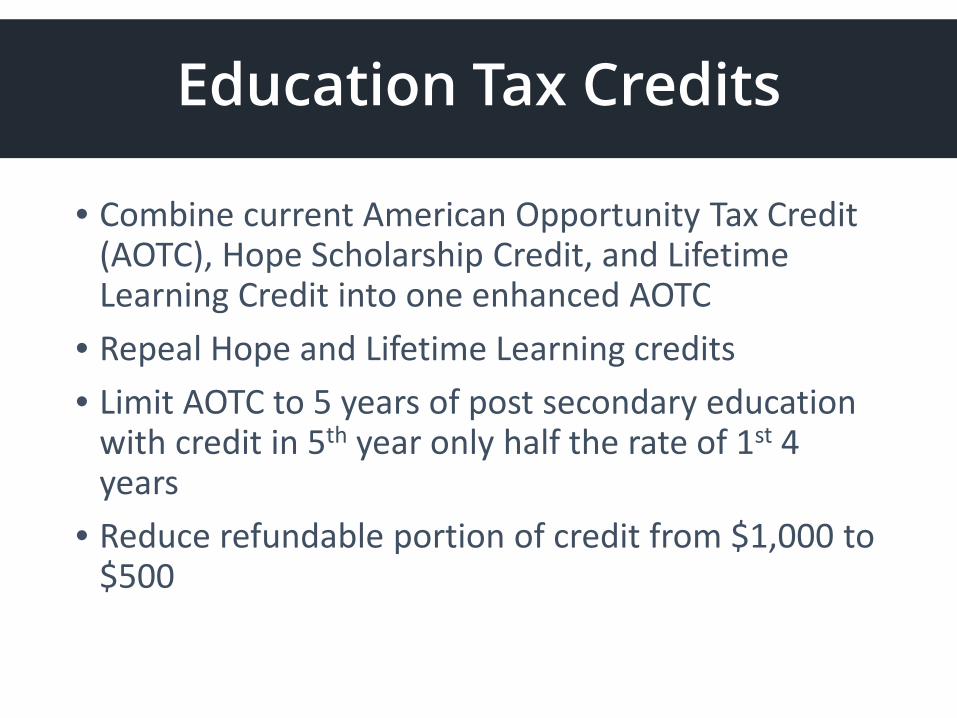

Education Tax Credits

• Combine current American Opportunity Tax Credit (AOTC), Hope Scholarship Credit, and Lifetime Learning Credit into one enhanced AOTC

• Repeal Hope and Lifetime Learning credits• Limit AOTC to 5 years of post secondary education

with credit in 5th year only half the rate of 1st 4 years

• Reduce refundable portion of credit from $1,000 to $500

Child Tax Credit

• Current Law• Credit is $1,000 per child under age 17• Credit begins to phase out when MAGI exceeds $110K

for joint filers and $75K for singles• Credit is refundable for some taxpayers

Child & Family Tax Credits

• Changes• Credit increases to $1,600 per child • Additional $300 non-refundable credit for non-child

dependents• New family flexibility credit of $300 • $300 credits phase out in 2022• Phase out begins when MAGI exceeds $230K for joint

returns and $115K for singles• Portion of credit is refundable for some taxpayers

Energy Tax Credits

• Current credit extended through 2022• Credit rate of 26% for property placed in service

during 2020• Credit rate of 21% for property placed during 2021

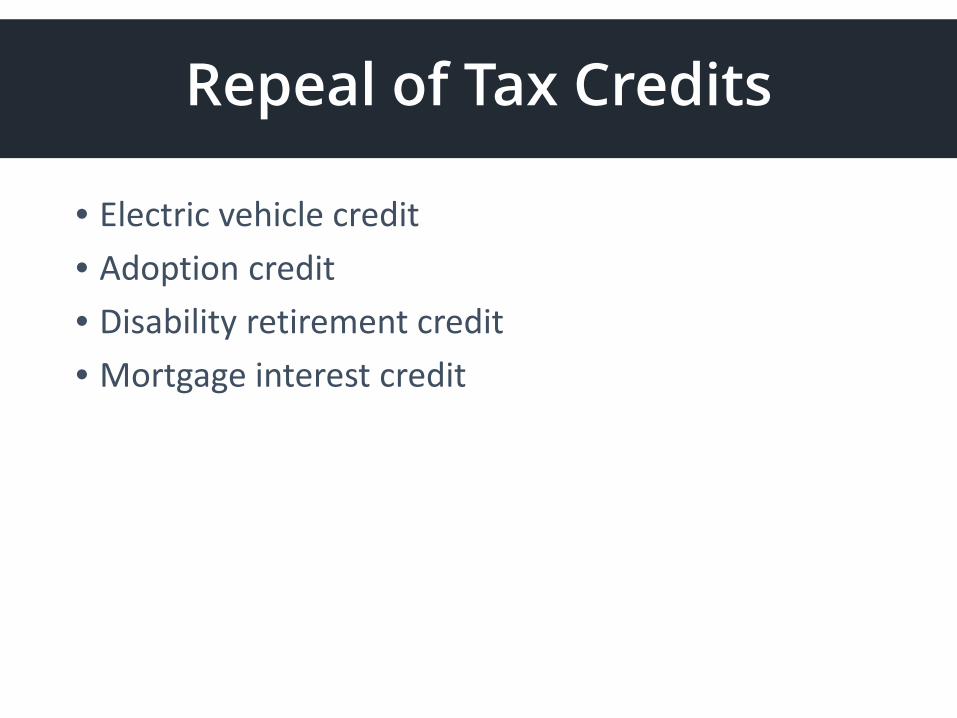

Repeal of Tax Credits

• Electric vehicle credit• Adoption credit• Disability retirement credit• Mortgage interest credit

Estate Tax

• 2018 exemption is currently is $5.6 million per person

• House bill doubles estate tax exemption and GST exemption to $11.2 million per person; continue adjustment for inflation

• Estate tax remains at 40%• House bill repeals estate tax and GST after 2023• Basis step-up is preserved• No portability beginning in 2024

Estate Tax Timeline

• 2018-2023 double current exemption • 2024-2027 estate tax is repealed• 2028 reverts to existing law

Gift Tax

• Current gift tax exemption and rate are same as estate tax

• House bill does not repeal gift tax• House bill lowers gift tax rate to 35% for transfers

after 12/31/2023• Retains annual gift tax exclusion; $15K per person

in 2018, up from $14K per person in 2017

#WBInsights17

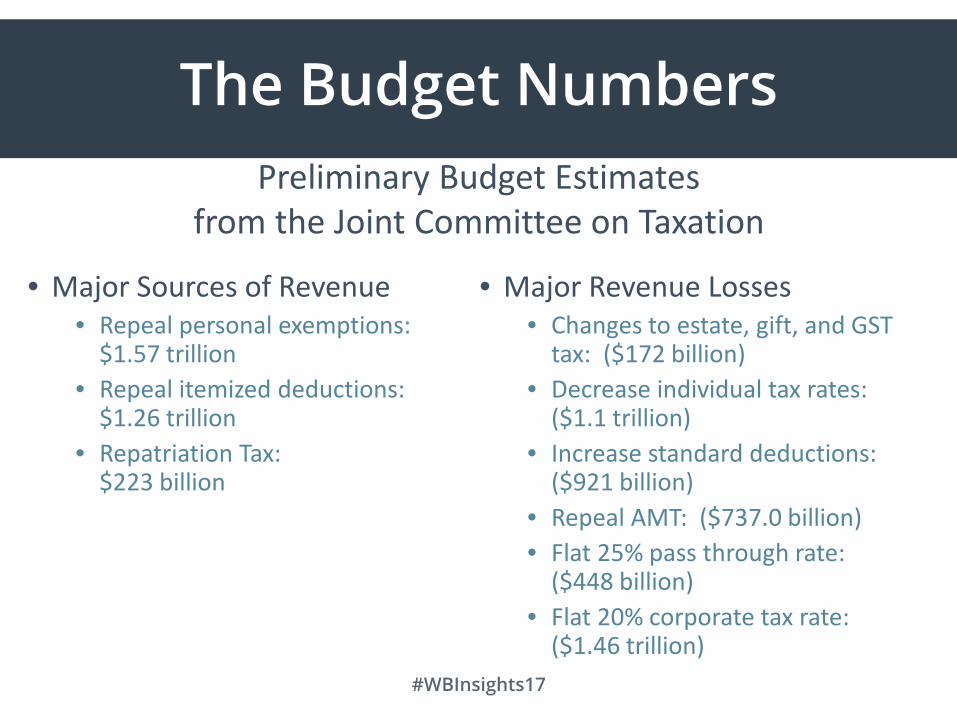

The Budget Numbers

• Major Sources of Revenue• Repeal personal exemptions:

$1.57 trillion• Repeal itemized deductions:

$1.26 trillion• Repatriation Tax:

$223 billion

• Major Revenue Losses• Changes to estate, gift, and GST

tax: ($172 billion)• Decrease individual tax rates:

($1.1 trillion)• Increase standard deductions:

($921 billion)• Repeal AMT: ($737.0 billion)• Flat 25% pass through rate:

($448 billion)• Flat 20% corporate tax rate:

($1.46 trillion)

Preliminary Budget Estimatesfrom the Joint Committee on Taxation

#WBInsights17

Example Taxpayers:Impact of Senate Version of Tax

Changes

James Jason Amber Kayla & Nick Sophie & Chad

Ordinary Income $30,000 $52,000 $75,000 $85,000 $165,000

Pass Through Income $- $- $- $- $-

Marital Status Single Single Single Married Married

Earners 1 1 1 1 2

Children - 2 - 2 2

Tax Def. Retirement Contrib.

$2,600 $4,000 $5,500 $5,500 $20,000

Deductions Standard Standard Standard Standard Itemize

Current Law $4,331 $5,198 $16,104 $11,035 $29,345

Proposed Law $3,953 $3,306 $14,327 $8,782 $27,122

Change in Tax $(378) $(1,892) $(1,777) $(2,253) $(2,223)

% Change in Tax -9% -36% -11% -20% -8%

% Change After Tax Income

1.3% 3.6% 2.4% 2.7% 1.3%

Source: Tax Foundation

Example Taxpayers:Impact of Senate Version of Tax

Changes

Soren & Linnea Laura & Seth Olivia & Richard Joe & Ethan

Ordinary Income $325,000 $2,000,000 $800,000 $48,000

Pass Through Income $- $- $- $-

Marital Status Married Married Married Married

Earners 2 1 1 Retired

Children 3 2 2 -

Tax Def. Retirement Contrib.

$37,000 $18,500 $18,500 $-

Deductions Itemize Itemize Itemize Standard

Current Law $71,629 $713,234 $318,315 $3,497

Proposed Law $64,456 $703,749 $292,478 $3,227

Change in Tax $(7,173) $(9,485) $(25,837) $(270)

% Change in Tax -10% -1% -8% -8%

% Change After Tax Income

2.2% 0.5% 2.6% 0.6%

Source: Tax Foundation

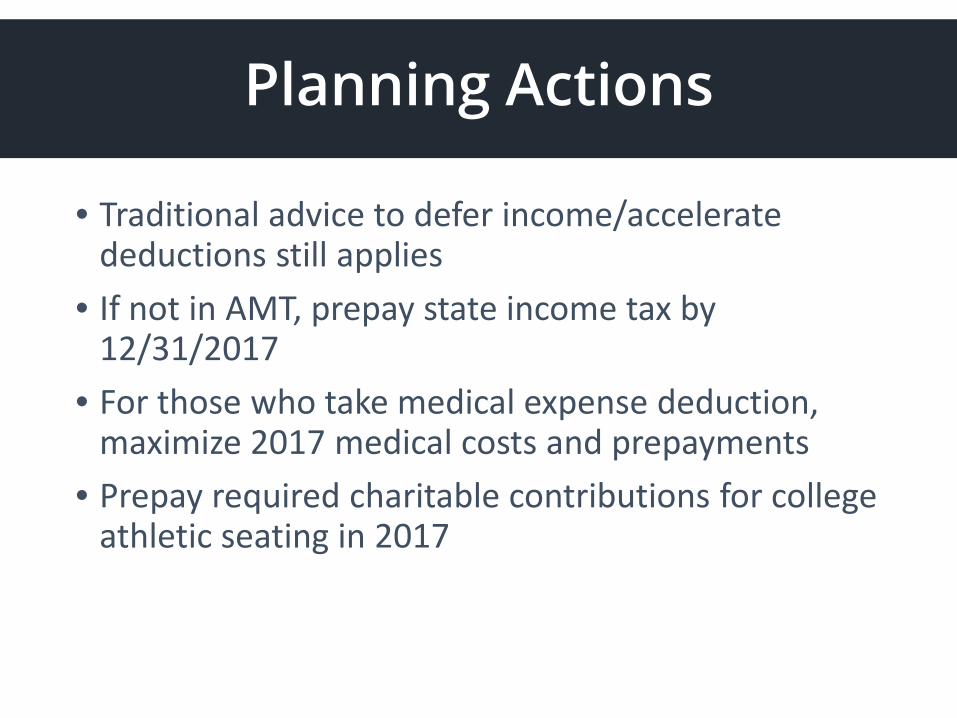

Planning Actions

• Traditional advice to defer income/accelerate deductions still applies

• If not in AMT, prepay state income tax by 12/31/2017

• For those who take medical expense deduction, maximize 2017 medical costs and prepayments

• Prepay required charitable contributions for college athletic seating in 2017

Planning Actions

• If not in 2017 AMT, avoid purchase of GA film credits and low income housing credits

• Accelerate closing date into 2017 for high income taxpayers selling a principal residence

• Make 2018 reservation for GA education expense credit by 12/15/2017

• Do not make a 2017 gift for which gift tax is owed• Purchase fixed assets used in business by

12/31/2017

#WBInsights17

#WBInsights17

Tax Planning with Georgia Tax Credits

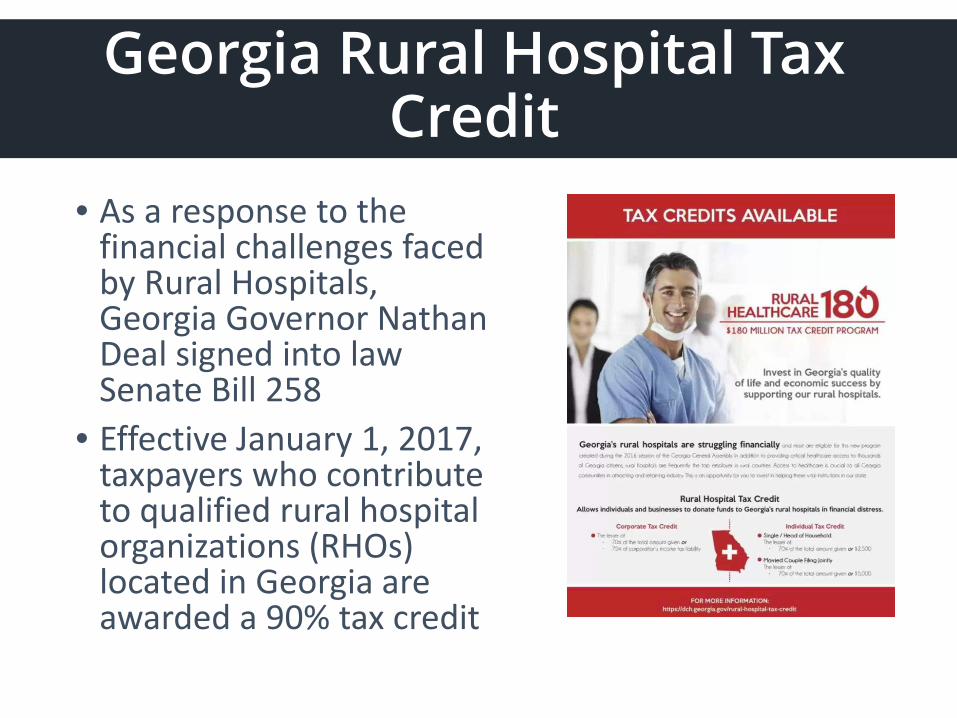

Georgia Rural Hospital Tax Credit

• As a response to the financial challenges faced by Rural Hospitals, Georgia Governor Nathan Deal signed into law Senate Bill 258

• Effective January 1, 2017, taxpayers who contribute to qualified rural hospital organizations (RHOs) located in Georgia are awarded a 90% tax credit

Qualifying Rural Hospitals

• County population of 50,000 or less• Acceptance of Medicare and Medicaid• Minimum annual provision for indigent care• File 5-year plan with GA Department of Community

Health

Eligible Rural Hospitals for 2017

Eligible Rural Hospitals for 2017

Size & Duration of Program

• Annual limit on credits is $60 million per year• Each rural hospital cannot access more than $4

million of credits• Applies for 2017, 2018, and 2019 tax years• Unless renewed, automatically repealed on

December 31, 2019

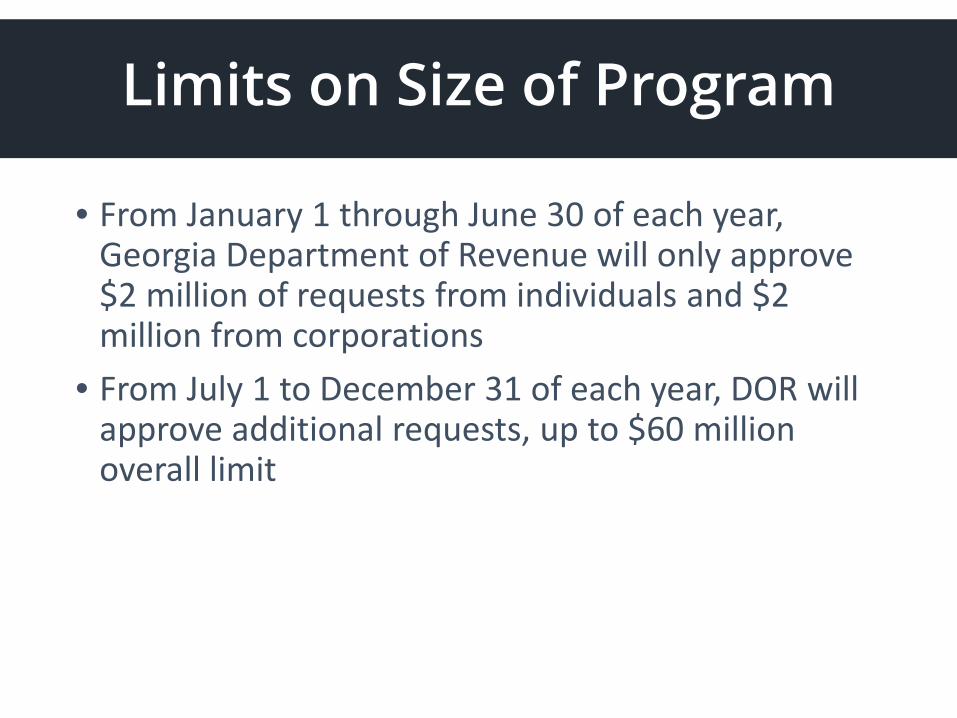

Limits on Size of Program

• From January 1 through June 30 of each year, Georgia Department of Revenue will only approve $2 million of requests from individuals and $2 million from corporations

• From July 1 to December 31 of each year, DOR will approve additional requests, up to $60 million overall limit

Making a Donation

• Complete Georgia Heart tax credit form https://www.georgiaheart.org/my_georgia_heart/tax_contribution

• Georgia Heart submits application to GA Department of Revenue

• Within 30 days, DOR notifies its approval

Making a Donation

• Within 60 days of DOR approval, contribute to hospital by making check payable to hospital and send to Georgia HEART

• Within 30 days of confirmation of contribution, Georgia HEART provides instructions for required confirmation done on GA Tax Center on-line account

• GA HEART confirms completion

Deadline

• Must complete all required steps by December 31 to claim credit in that year

• Georgia HEART will begin accepting applications for 2018 credits on January 2, 2018

Income Tax Treatment

• Federal deduction – charitable contribution for 100% of contribution

• Georgia credit – 90% of contribution• Georgia deduction – none

Maximum Credit Limits

• Single individual – $5,000• Married couple – $10,000• Trust – 75% of GA tax• C Corporations – 75% of GA tax• No increased limits for owners of pass-through

entities

Maximum Contributions

• Single – $5,555 contribution * 90% = $5,000 credit• Married couple – $11,111 contribution * 90% =

$10,000 credit

Carryover of Unused Credits

• Excess credit carry forward for 5 years• No carry back is available

Planning: Know If You Owe AMT

Tax Credits: Rates of Return

Credit AMT No AMT Maximum Purchase

Education expense 127% 96% $10K but oversold (got 50% in 2017)

Rural hospital 119% 91% $10,000Film at $0.92 105% 107% UnlimitedLow income housing at $0.90 107% 109% Unlimited

A Word of Caution!

• Each taxpayer is unique; need to run the numbers to calculate rate of return

Contact Information

Barbara M. Coats, CPAPrincipal

Windham Brannon

3630 Peachtree Road NE, Suite 600

Atlanta, GA 30326

Main: 404.898.2000

Direct: 678.510.2724

Fax: 404.898.2010

Email: [email protected]