Impact of FRBM Act, Monetary policy and Budetary Deficit on Govt Securities n India

20

An Analysis of FRBM framework, Budgetary deficit and Monetary policy

Transcript of Impact of FRBM Act, Monetary policy and Budetary Deficit on Govt Securities n India

An Analysis of FRBM framework, Budgetary deficit and Monetary policy

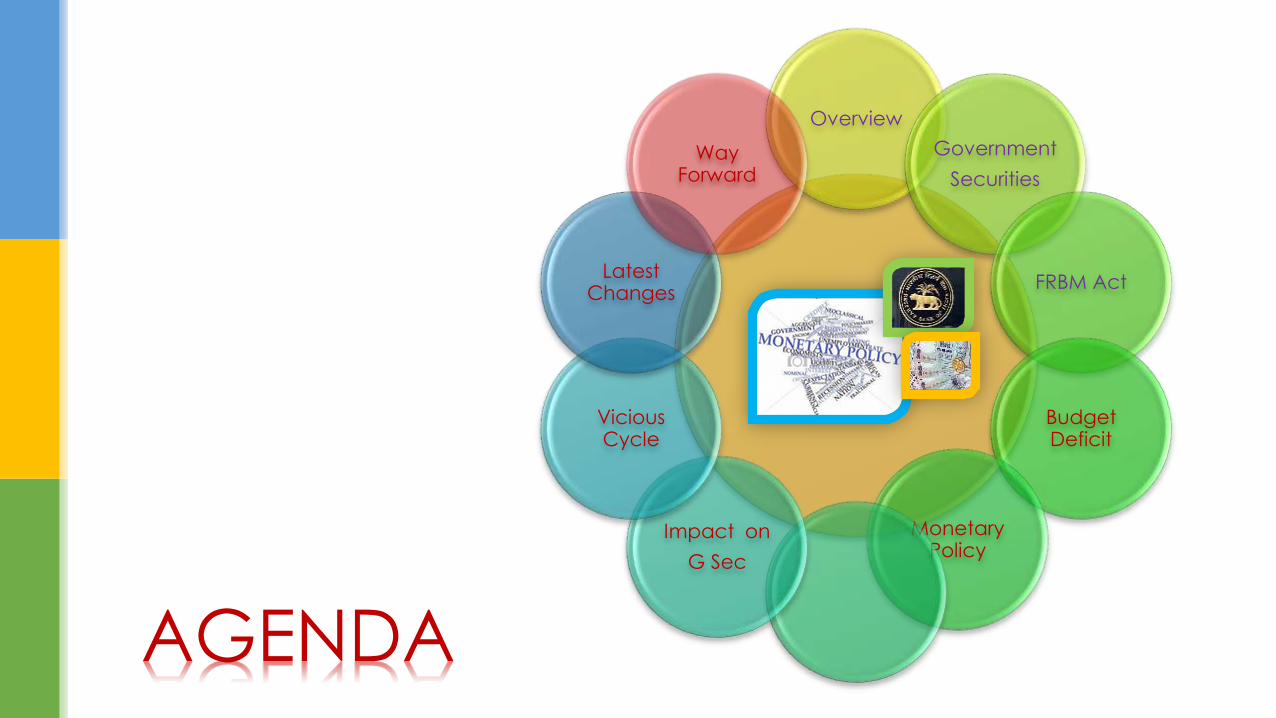

Overview

Government

Securities

FRBM Act

Budget Deficit

Monetary Policy

Impact on

G Sec

Vicious Cycle

Latest Changes

Way Forward

AGENDA

TypeSub

CategoryIssuer

Bonds

Government

Fixed Rate Treasury Bond

Inflation Linked

Treasury Indexed Bond

Corporate

Floating Rate FRN’s

Inflation Linked

Fixed RateCorporate

Bonds

Govt .Securities

-Tradable Sec issues by the Central/State Govt,

-Risk Free Returns

-Govt Debt Obligation

T-Bills

CMB’s

Dated Govt Securitues

State Development Loans (SDL)

Postponement of the Present Liab –Eg OIL bonds

special securities to entities like Oil Marketing Companies,

Fertilizer Companies, the Food Corporation of India, etc. as

compensation to these companies in lieu of cash

subsidies

To raise funds that pay for the government's

various expenses, including those related

to infrastructure development projects

Investors

-Banks-Commercial/ Cooperative/Rural etc

-Insurance Co’s

-Provident Funds

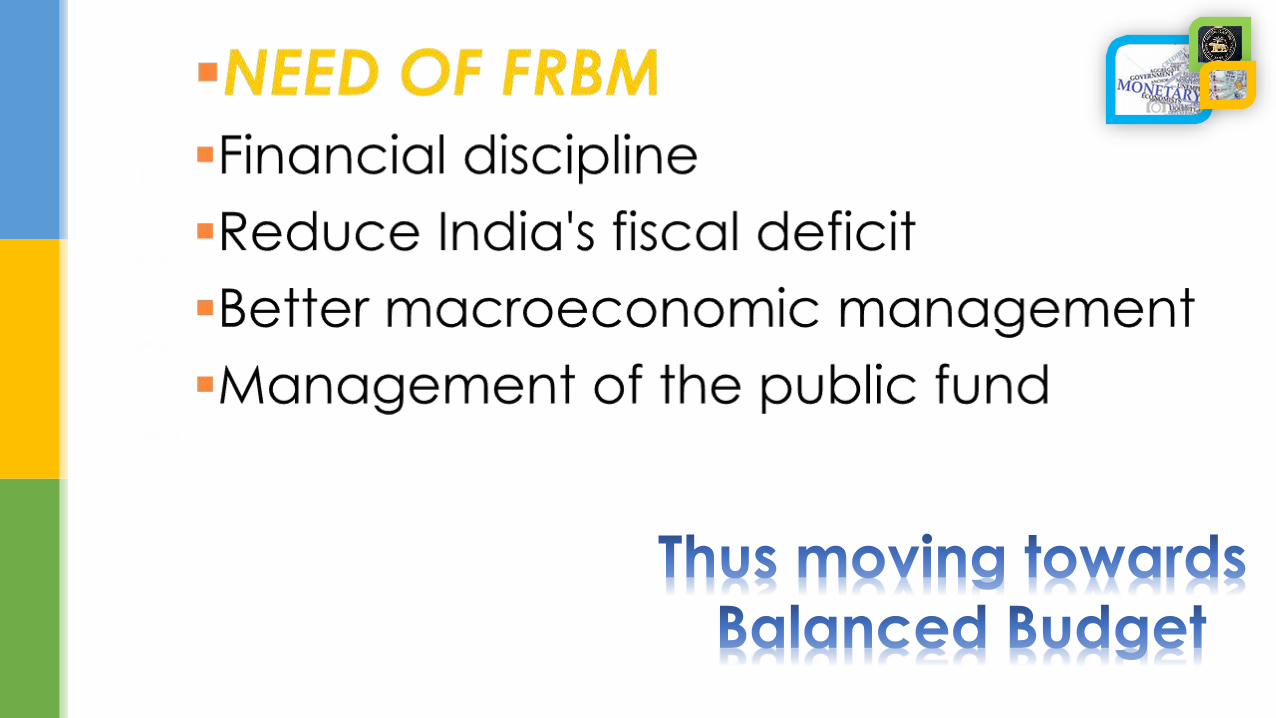

A tool to cater to Fiscal deficit with certain

shortcomings

• Eliminate Revenue Deficit

• Bring Down Fiscal Deficit to 3 % of GDP by March 2008

• International Financial crisis hindered the achievement of the objective

• Target Postponed and suspended in 2009

• In the process of Ongoing recovery (as the other nations are still struggling to emerge)

• The Economic Advisory Council publicly advised the GOI to Reconsider FRBMA

History for Broad Objectives

FY 2003-

04

Same as 1991

crisisStructure of

Exp

Unproductive Exp

Poorly designed subsidies

Fiscal Deficit -10%

of GDP

Revenue Receipts Rs2.63 Trn

GovtDebt Rs3.91 Trn-Leading to Debt

Trap

F

R

B

M

Revenue Deficit

Monetised Deficit

Fiscal Deficit

Capital Deficit

GovtRevenue

Govt Exp

Def

• Monetary Authority (Central Bank) controls the money supply in economy

• through Interest rates

Objective

• Control Over Interest Rate

• Price Stability

• Stable Exchange Rate

Objectives

• Healthy Balance of Payments

• Controlling Inflation

Tools

• OMO

• CRR,SLR,Repo rates, Bank Rates, Credit Ceiling etc

Corporates

Source=Develop

ment

Liability=CSR and

Taxes

Source=Income

Liability= Taxes

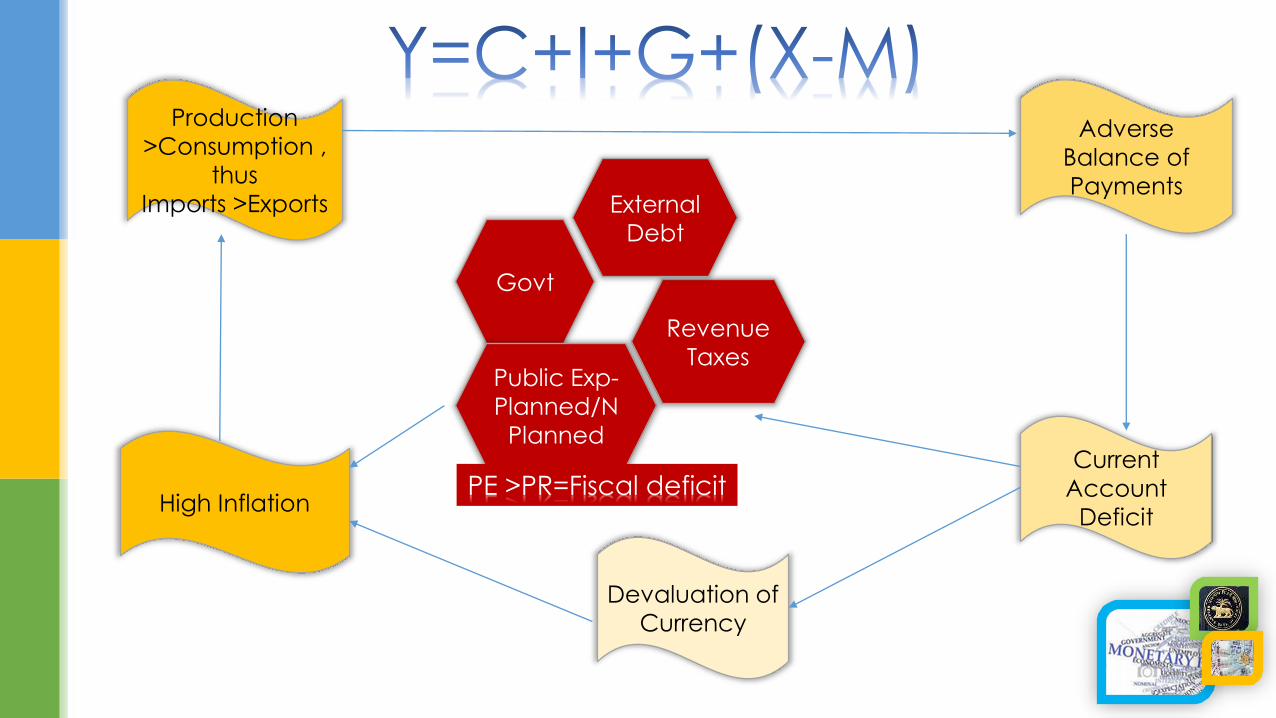

HouseholdGovt

Public Exp-

Planned/N

Planned

Revenue

Taxes

Investment

in Govt sec

Banking/

Institutions

Mobilisatio

n of

Savings

Borrowing from Public/Printing of Currency

Markets

Gilt

Edged

Market

Primary

/Secon

dary

Adverse

Balance of

Payments

Current

Account

Deficit

Devaluation of

Currency

High Inflation

Production

>Consumption ,

thus

Imports >Exports

Govt

Public Exp-

Planned/N

Planned

Revenue

Taxes

PE >PR=Fiscal deficit

External

Debt

Well developed Govt Securities Market –Provides Flexibility to Debt Management

Authorities to optimise interest cost to govt , minimise govt debt Operations and facilitate

better coordination between monetary policy and debt management

Monetised deficit indicates the level of support extended by the Reserve Bank of India to

the government’s borrowing programme-Phased out in 2006

If Revenue deficit is eliminated and Fiscal deficit is reduced, the use of RBI policies to

mange the money supply shall be substantially reduced

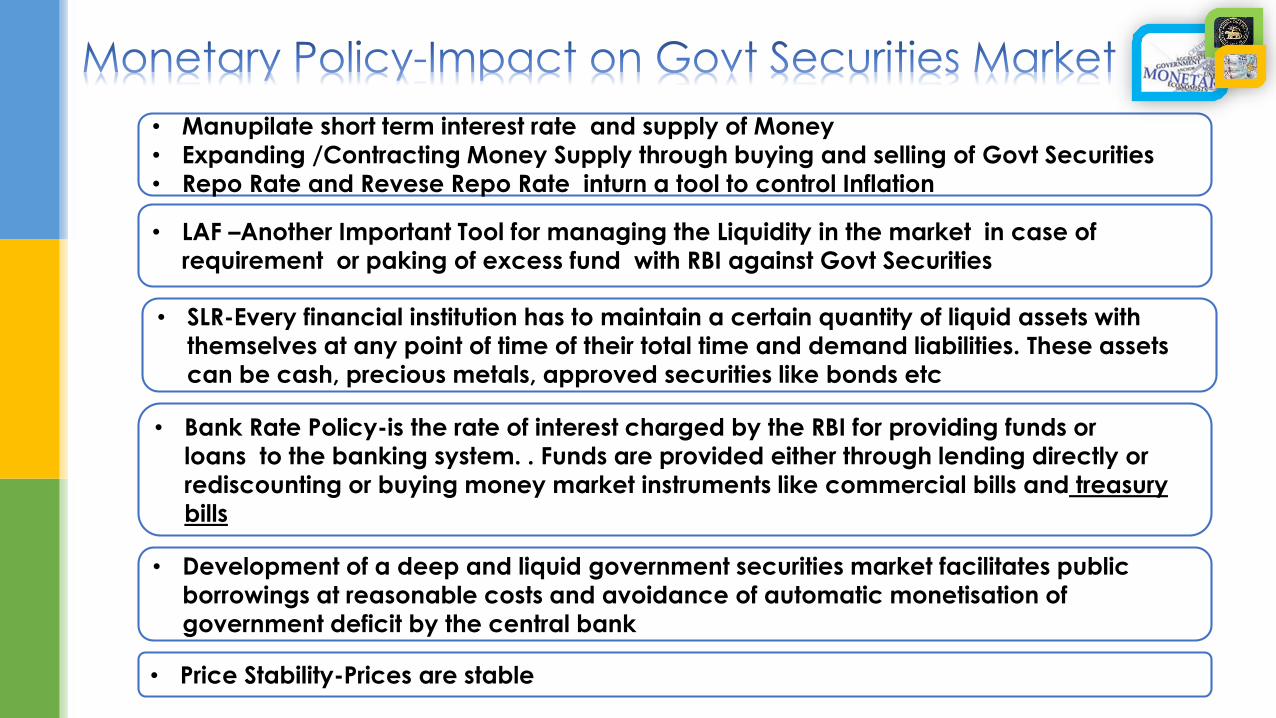

• Manupilate short term interest rate and supply of Money

• Expanding /Contracting Money Supply through buying and selling of Govt Securities

• Repo Rate and Revese Repo Rate inturn a tool to control Inflation

• LAF –Another Important Tool for managing the Liquidity in the market in case of

requirement or paking of excess fund with RBI against Govt Securities

• SLR-Every financial institution has to maintain a certain quantity of liquid assets with

themselves at any point of time of their total time and demand liabilities. These assets

can be cash, precious metals, approved securities like bonds etc

• Bank Rate Policy-is the rate of interest charged by the RBI for providing funds or

loans to the banking system. . Funds are provided either through lending directly or

rediscounting or buying money market instruments like commercial bills and treasury

bills

• Development of a deep and liquid government securities market facilitates public

borrowings at reasonable costs and avoidance of automatic monetisation of

government deficit by the central bank

• Price Stability-Prices are stable

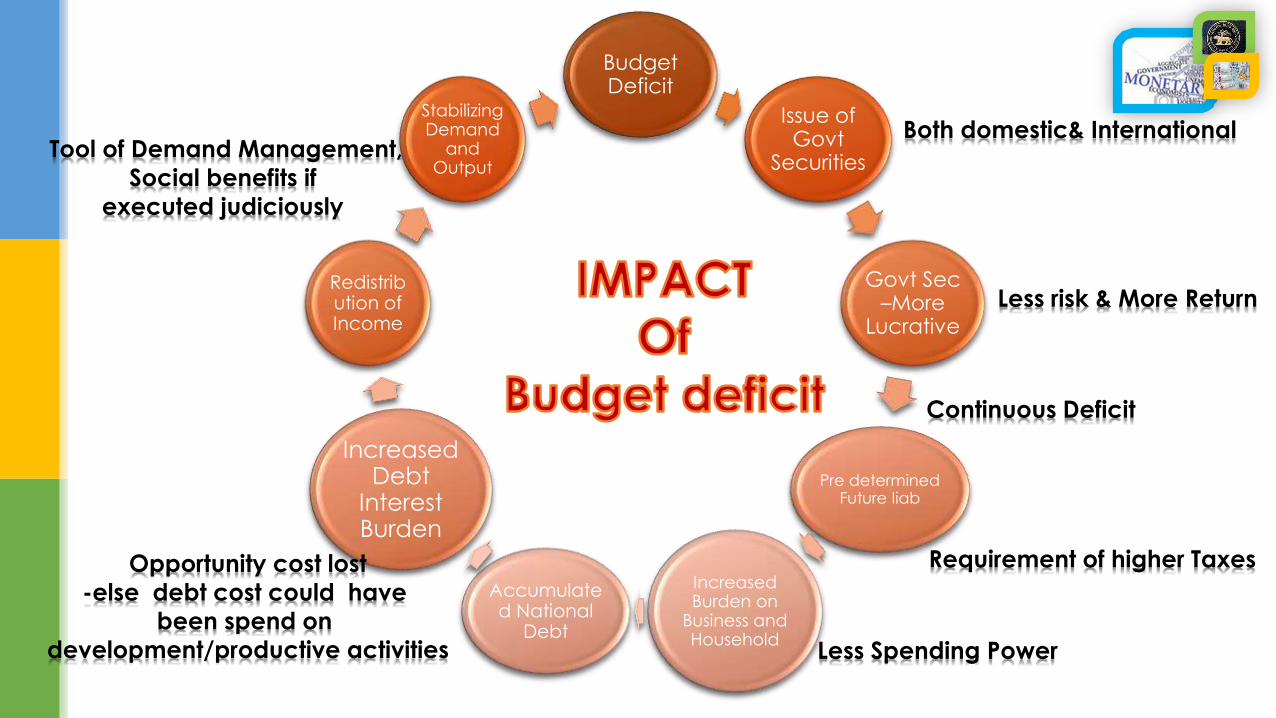

Budget Deficit

Issue of Govt

Securities

Govt Sec –More

Lucrative

Pre determined Future liab

Increased Burden on

Business and Household

Accumulated National

Debt

Increased Debt

Interest Burden

Redistribution of Income

Stabilizing Demand

and Output

Both domestic& International

Less risk & More Return

Continuous Deficit

Requirement of higher Taxes

Less Spending Power

Opportunity cost lost

-else debt cost could have

been spend on

development/productive activities

Tool of Demand Management,

Social benefits if

executed judiciously

• New FRBM Act with Teeth- Economic Survey 2014

• Improved Budgetary Management

• Better Accounting practices

• High quality fiscal adjustment based on improvements in both tax and expenditure

• With fiscal deficit still at a high of 4.5 per cent in FY14 as against the target of three per cent by FY17, the finance ministry is mulling a revised roadmap for fiscal consolidation that will be more realistic

• Shifting subsidy programmes to income support, a change in focus of government spending towards provision of public goods and a focus on outcomes through an improvement in systems of accountability

Way forward

0

1

2

3

4

5

Year

2014-15

Year

2015-16

Year

2016-17

4.13.6

3

Fiscal Deficit

Expectations