Ignacio Rodríguez Añino, Country Head Spain · Mar-13 6.5% 4.9% Dec-12 5.5% Table shows...

38

Ignacio Rodríguez Añino, Country Head Spain June 2017

Transcript of Ignacio Rodríguez Añino, Country Head Spain · Mar-13 6.5% 4.9% Dec-12 5.5% Table shows...

Ignacio Rodríguez Añino, Country Head Spain

June 2017

2

Fund facts

Source: M&G, 31 May 2017

M&G Dynamic Allocation Fund and M&G Prudent Allocation Fund

M&G DYNAMIC ALLOCATION FUND

Launch December 2009

Co-fund

managers Juan Nevado, Tony Finding

Tenure January 2011

Fund size €4,815 million

Sector Morningstar EUR Flexible Allocation

Currency Euro denominated fund

Best Flexible Allocation fund*

M&G PRUDENT ALLOCATION FUND

Launch April 2015

Co-fund

managers Juan Nevado, Craig Moran

Tenure April 2015

Fund size €1,124 million

Sector Morningstar EUR Cautious Allocation

Currency Euro denominated fund

Juan Nevado Tony Finding Juan Nevado Craig Moran

*Morningstar Awards 2015. Morningstar, Inc. All Rights Reserved. Awarded to M&G Dynamic Allocation Fund, euro A class shares f or Best Flexible Allocation

Fund, Italy

Ratings as at 31.05.17. The Morningstar Overall Rating based on the fund’s Euro Class A shares. Copyright © 2017. Morningstar UK Limited. All Rights

Reserved. Ratings should not be taken as recommendation.

3

• Joined Prudential Portfolio Managers in 1988 and is

a member of the M&G Multi Asset team, with over

20 years of investment experience

• In January 2011, Juan was appointed co-manager of

the M&G Dynamic Allocation Fund and the M&G

Episode Allocation Fund. In April 2015, he was

appointed co-manager of the M&G Prudent

Allocation Fund upon its launch

• He has a BSc in economics from the LSE and an

MA in economics from Warwick University

Juan Nevado Biography

M&G Dynamic Allocation Fund & M&G Prudent Allocation Fund

Juan Nevado, Fund Manager

June 2017

5

Proposition M&G Dynamic Allocation Fund and M&G Prudent Allocation Fund

Source: Morningstar Inc., Pan European database, euro class A shares, net income reinvested, price-to-price, 31 May 2017

7.9%*

Positive

returns 5% - 12% 5% - 10%

Worst: 6%

Best: 40%

Potential to deliver

6.5%

M&G Dynamic Allocation Fund

M&G Prudent Allocation Fund

Positive returns 3% - 7% 3% - 6% Potential to deliver

The fund allows for the extensive use of

derivatives.

The potential return is quoted net of

charges on a total return basis (combination

of income and capital growth) and

calculated over a three- to five-year period. The potential volatility figures are calculated

on a monthly basis over the medium term.

Please note, these figures are not

guaranteed and may be revised in the future.

The fund allows for the extensive use of

derivatives.

There is no guarantee that the fund will achieve a positive return over this or any

other period and investors may not recoup the original amount they invested

*3-year volatility calculated monthly, as at

31 May 2017. **Cumulative 3-year rolling

returns since launch (3 December 2009)

The potential return is quoted net of

charges on a total return basis (combination

of income and capital growth) and

calculated over a three- to five-year period. The potential volatility figures are calculated

on a monthly basis over the medium term.

Please note, these figures are not

guaranteed and may be revised in the future.

6

Agenda

Performance

Investment philosophy

Views and positions

7

M&G Dynamic Allocation Fund

Source: M&G Statistics, Morningstar Inc., Pan European database, euro class A shares, net income reinvested, price -to-price, 31 December 2016.

Aims to deliver positive total returns in any three-year period

There is no guarantee that the fund will achieve a positive return over this or any other period and investors may not recoup the original amount they invested

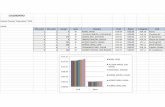

Date of investment Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13

Da

te o

f w

ith

dra

wal

Dec-16 6.2% 5.5% 5.9% 6.3% 5.9% 6.5% 6.8% 8.4% 7.3% 6.4% 7.3% 6.7% 6.7% 5.9% 7.1% 6.5% 6.8%

Sep-16 5.4% 4.6% 5.0% 5.4% 5.0% 5.5% 5.8% 7.4% 6.2% 5.3% 6.1% 5.4% 5.3% 4.4% 5.5% 4.8%

Jun-16 5.1% 4.3% 4.7% 5.1% 4.7% 5.2% 5.5% 7.1% 5.8% 4.9% 5.7% 4.9% 4.8% 3.8% 4.9%

Mar-16 5.3% 4.5% 5.0% 5.3% 4.9% 5.5% 5.8% 7.5% 6.2% 5.2% 6.1% 5.3% 5.2% 4.1%

Dec-15 5.7% 4.9% 5.4% 5.8% 5.4% 6.0% 6.4% 8.3% 6.9% 5.8% 6.8% 6.1% 6.0%

Sep-15 5.6% 4.8% 5.2% 5.7% 5.2% 5.8% 6.2% 8.3% 6.8% 5.6% 6.7% 5.9%

Jun-15 7.3% 6.4% 7.0% 7.6% 7.2% 8.0% 8.5% 10.9% 9.5% 8.4% 9.8%

Mar-15 7.9% 7.0% 7.6% 8.3% 7.9% 8.8% 9.5% 12.1% 10.6% 9.6%

Dec-14 6.5% 5.5% 6.2% 6.7% 6.2% 7.1% 7.7% 10.3% 8.6%

Sep-14 6.3% 5.3% 5.9% 6.5% 5.9% 6.8% 7.4% 10.3%

Jun-14 6.2% 5.1% 5.7% 6.3% 5.8% 6.7% 7.3%

Mar-14 5.8% 4.6% 5.2% 5.8% 5.2% 6.1%

Dec-13 5.7% 4.5% 5.1% 5.8% 5.1%

Sep-13 5.9% 4.5% 5.2% 6.0%

Jun-13 5.3% 3.8% 4.5%

Mar-13 6.5% 4.9%

Dec-12 5.5%

Table shows annualised product returns over a holding period of at least three years

Track record: 3 December 2009 (inception) to December 2016

8

Performance since launch

Source: Morningstar, Inc., Pan European database, 31 May 2017, euro A class shares, net income reinvested, price to price.

M&G Dynamic Allocation Fund

Performance vs Pan European sector

95

100

105

110

115

120

125

130

135

140

145

150

155

160

165

Rebased t

o 1

00 a

s a

t 4 D

ecem

ber

2009

M&G Dynamic Allocation Fund Morningstar EUR Flexible Allocation sector EURIBOR 3 months

9

Drivers of performance: YTD 2017 Dynamic asset class allocation and selection are the main drivers of performance

M&G Dynamic Allocation Fund*

Source: M&G, Xamin, 31 May 2017. Investment returns (gross of fees) absolute terms, calculated in euros end of day pricing. *Fund launched on 3 December 2009.

**Mainly real estate-related securities and convertibles. ***Fund launched on 23 April 2015.

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%

YTD 2017

Equity Government bonds Corporate bonds

Other** Cash and currencies

M&G Prudent Allocation Fund***

0.0%

0.4%

0.8%

1.2%

1.6%

2.0%

YTD 2017

Equity Government bonds Corporate bonds

Other** Cash and currencies

Strong contribution from our

equity exposure, particularly from

Asia and Europe

Benefited from good performance

in EM bonds

Credit spread compression in

investment grade space

High carry EM currencies

contributed positively

Convertibles and Infrastructure

funds offered diversification and

positive performance

Short duration in UK gilts was

a detractor to the funds’

performance

10

Agenda

Performance

Investment philosophy

Views and positions

11

Building blocks of our investment strategy

Source: M&G

M&G Multi Asset team

A robust, repeatable approach

3

2

1

Strategic assessment

Tactical assessment

Portfolio construction

12

Strategic assessment Valuation framework: the starting point

Source: M&G, Datastream, 1 June 2017. *Real yield for equity is defined as an inflation-adjusted inverted p/e ratio, using forward consensus data

Driver of long-term asset allocation decisions

Sample of assets, showing real yield against an assessment of neutrality

-3%

-1%

1%

3%

5%

7%

9%

11%

13%

Real yi

eld

*

Neutrality Above

neutrality –

Cheap?

Below

neutrality –

Expensive?

13

60

80

100

120

140

160

180

The environment has been forgiving of ‘set and forget’

asset allocation…

Source: Datastream, 28 April 2017. *Rebased as at 31 December 2006

Tota

l re

turn

, re

based (

US

D)*

50/50

(5.6% pa)

70% equity/ 30% bond

(5.6% pa)

70% bond/ 30% equity

(5.5% pa)

MSCI AC World and Citigroup World Government Bond Index (10Y+), US dollar terms

… but the environment might have changed

14

80

100

120

140

160

180

200

May-12 Nov-12 May-13 Nov-13 May-14 Nov-14 May-15 Nov-15 May-16 Nov-16

US equity and bond returns over the last 5 years

Source: M&G, DataStream, 31 May 2017. *Rebased as at 30 May 2017

Real returns on S&P 500 and US 10-year Treasuries, rebased* To

tal

Retu

rns,

rebased*

S&P 500

US 10 Year

Treasury

15

Why do we like volatility? Equities generally rally in the year after volatility peaks

Source: Bloomberg, 9 June 2017

0

10

20

30

40

50

60

70

80

90

Index

Volatility Index (VIX) X% Performance of the S&P 500 one year forward

28.4%

34.5%

15.1%

23.1%

37.1% -15.3%

23.1%

33.6%

33.2%

25.3%

-37.8%

47.0%

24.4% 25.3%

11.7%

28.6% 9.2%

14.9%

24.9%

16

Volatility is not risk The volatility phase at the beginning of 2016 was partly behavioural

Source: M&G, Datastream, 30 August 2016. *Bloomberg, February 2016. **As at 30 March 2016. ***Rebased to 100 as at 28 April 2007

Justified market reaction or overreaction?

Focus on a single event* Rapid price movement** Inconsistent responses

75

80

85

90

95

100

105

Tota

l re

turn

s,

rebased t

o 1

00 a

s a

t 31 D

ecem

ber

2015

S&P 500

DAX

0

20

40

60

80

100

120

140

160

12

-mo

nth

fo

rwa

rd e

arn

ings p

er

sh

are

*** MSCI Germany

S&P 500

Topix

Topix

Oil

Oil

Oil

Oil

Oil

Oil

Oil

Oil

Oil Oil

17

Tactical Assessment

Source: M&G, Datastream, Bloomberg, 7 June 2017. *As at 30 April 2017

Dynamic asset allocation in practice

Equity allocation Fixed income allocation*

Total net equity allocation in

M&G Dynamic Allocation Fund

-3

-2

-1

0

1

2

3

4

5

6

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

Fund d

ura

tion (ye

ars

)

Yie

ld t

o m

atu

rity

Duration of M&G Dynamic Allocation Fund (RHS)

BofA ML All Maturity G7 Govt Index (LHS)

Average duration

Active asset allocation to take advantage of market opportunities

55%

6.0%

6.2%

6.4%

6.6%

6.8%

7.0%

7.2%

7.4%

7.6%

World e

arn

ings y

ield

46.5%

45%

40%

50%

40% 40%

47%

40% 35%

40%

18

Agenda

Performance

Investment philosophy

Views and positions

19

4. What is the biggest risk

for markets in 2017?

3. EM- what are the

opportunities ?

1. Fixed income: a turning

point?

2. Is there still value in

equities?

Four burning questions for investors

Source: M&G

What is the market worrying about?

20

2.0%

2.2%

2.4%

2.6%

2.8%

3.0%

3.2%

3.4%

3.6%

3.8%

Real G

DP

exp

ecta

tions

World 2011 World 2012 World 2013 World 2014

World 2015 World 2016 World 2017 World 2018

Global: Real GDP expectations

Source: Consensus Economics, June 2017

Real GDP expectations

21

Current market context

Unemployment rates

Corporate earnings trends* Inflation – Consumer Price Index

Source: M&G, Bloomberg, Datastream, 31 May 2017. *As at 4 April 2017

3%

5%

7%

9%

11%

13%

Jan-08 Jan-10 Jan-12 Jan-14 Jan-16

Japan Eurozone USA

-4%

-2%

0%

2%

4%

6%

Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

Eurozone USA Japan

-15

-10

-5

0

5

10

15

20

Apr-15 Oct-15 Apr-16 Oct-16 Apr-17

USA Japan Eurozone

Purchasing Managers’ Indices

45

50

55

60

65

Jan-15 Jun-15 Nov-15 Apr-16 Sep-16 Feb-17

Index

Japan Eurozone USA

22

Opportunities in fixed income Selectivity, flexibility and dynamic asset allocation is key

-2%

-1%

0%

1%

2%

3%

4%

Yie

ld

US UK Japan Germany

Source: Bloomberg, Datastream, 9 June 2017

On the short side: 10-year real bond yields On the long side: spreads vs US Treasuries

0%

2%

4%

6%

8%

10%

12%

14%

16%

Sp

rea

d

Mexico Brazil Colombia US BBB

Importance of flexibility to implement negative view on bonds

23

Current fixed interest exposures: targets

Source: M&G, 26 June 2017. *Fund duration as at 23 June 2017. **Treasury Inflation-Protected Securities. †These positions are a combination of outright

short positions and hedging duration strategies.

Deriving value from relative value positions

M&G DYNAMIC ALLOCATION FUND Net fixed income exposure, excluding hedging instruments: 15.5% Fund duration, -1.77 years*

Periphery:

9.5% Emerging markets: 10.3% Credit: 8.5% Mainstream govt bonds: -40.5%

M&G PRUDENT ALLOCATION FUND Net fixed income exposure, excluding hedging instruments: 21.5% Fund duration, -1.51 years*

4.0%

-2.0% -5.0%

-7.5% -7.5%

-22.5%

7.5% 2.0%

6.0% 1.5% 1.0% 1.0% 0.5% 0.3%

5.0% 2.5% 1.0%

-25%

-15%

-5%

5%

15%

% o

f fu

nd

exp

osu

re

4.0%

-2.0% -3.0% -5.5% -7.0%

-26.0%

8.0% 2.0%

6.0% 2.0% 1.5% 1.0% 1.0% 0.5% 0.5%

7.0% 2.0% 1.0%

-30%

-20%

-10%

0%

10%

% o

f fu

nd

exp

osu

re

Mainstream govt bonds: -39.5% Periphery:

10.0% Emerging markets: 12.5% Credit: 10.0%

24

4. What is the biggest risk

for markets in 2017?

3. EM- what are the

opportunities ?

1. Fixed income: a turning

point?

2. Is there still value in

equities?

Four burning questions for investors

Source: M&G

What is the market worrying about?

25

Valuation signals are clear

Source: Datastream, 31 May 2017. Equity proxy is MSCI Germany; cash proxy is EURIBOR 3 months. All data is inflation-adjusted.

Equities offer compelling earnings yield relatively to fixed income

Safer assets have yield well below normal

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Real yi

eld

s

German real yields

Cash

Equity

10-year German

govt bond

Equity risk premium

26

-10

-5

0

5

10

15

20

25

30

35

8 10 12 14 16 18 20 22 24 26

-15

-10

-5

0

5

10

15

20

25

6 8 10 12 14 16 18 20 22 24 26 28

Why is valuation our starting point?

Source: Datastream, 31 December 2016

Valuation is a good indicator of future returns

Forward PE

5Y

annualis

ed r

etu

rn

Forward PE

5Y

annualis

ed r

etu

rn

27

Current equity exposures: targets Deriving value from relative value positions

Source: M&G, 26 June 2017

M&G DYNAMIC ALLOCATION FUND Equity exposure, 40.0% versus 40% neutrality

M&G PRUDENT ALLOCATION FUND Equity exposure, 23.0% versus 20% neutrality

EM: 3.5% Global equities: 34.5% Relative value trade: 2%

EM: 3.3% Global equities: 18.8% Relative value trade: 1%

14.5%

8.5% 7.5% 4.0%

7.3%

2.8% 2.0% 1.0%

-11.0%

2.0% 1.5%

-15%

-10%

-5%

0%

5%

10%

15%

% of t

ota

l fund e

xposure

7.3% 5.0% 4.5%

2.0%

6.5%

2.0% 1.5% 1.0%

-10.0%

2.0% 1.3%

-12%-10%-8%-6%-4%-2%0%2%4%6%8%

10%

% of t

ota

l fund e

xposure

28

1. Fixed income: a turning

point?

4. What is the biggest risk

for markets in 2017?

Four burning questions for investors

Source: M&G

What is the market worrying about?

2. Is there still value in

equities?

3. EM- what are the

opportunities?

29

Opportunities in EM – equities and bonds

Source: M&G, 25 April 2017

Russia – Equities • Attractive valuation

• Improving fundamentals, oil play • Basket of companies that focus

on shareholder value

Mexico, Brazil, Colombia,

Argentina – Bonds • Attractive yield

• Positive trend

Korea, Taiwan – Equities • Attractive valuation

• Improvement in earnings growth not priced in

• Improvement in corporate governance

Turkey – Equities • Attractive valuations

• Strong earnings growth

30

Opportunities in currencies Some EM currencies now look attractive

Source: Bloomberg, 9 June 2017

Exchange rates versus the USD 3-month implied carry versus the USD

30

40

50

60

70

80

90

100

110

Rebased t

o 1

00 a

s a

t 31 D

ecem

ber

2012

Russian ruble Mexican peso

Turkish lira Brazilian real

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

Russianruble

Turkish lira Brazilianreal

Mexicanpeso

31 Source: Bloomberg, 31 May 2017

Valuation is one metric that drives FX positioning…

60

70

80

90

100

110

120

130

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17

Real E

ffectiv

e E

xchange R

ate

rebased t

o

100 a

t 31 J

anuary

2012

… but carry and ‘episodic’ behaviour also play key roles

US dollar

Chinese

renminbi

Euro

Mexican

peso

Japanese

yen

British

pound

32

5.0%

-1.5%

3.5% 2.0% 2.0% 1.5% 1.0% 1.0% 1.0% 0.5%

2.0%

-2.0% -2.0% -3.0% -4.0%

-6.0% -7%

-4%

-1%

2%

5%

8%

Currency exposure: targets Additional source of performance

M&G DYNAMIC ALLOCATION FUND Currency exposure targets

M&G PRUDENT ALLOCATION FUND Currency exposure targets

99.5%

70%

100%

≈

% o

f fu

nd e

xposure

99.0%

70%

100%

≈

% o

f fu

nd e

xposure

3.3%

-1.0%

2.5% 2.0% 2.0%

1.0% 1.3% 1.0% 1.0% 0.5% 2.0%

-1.0% -2.0%

-3.0% -3.0%

-6.0% -7%

-4%

-1%

2%

5%

8%

Long high-carry currencies: 12.5%

Short low-yielding Asian currencies: -17.0%

Long high carry currencies: 11.3%

Short low-yielding Asian currencies: -15.0%

Source: M&G, 26 June 2017

33

4. What is the biggest risk

for markets in 2017?

3. EM- what are the

opportunities?

1. Fixed income: a turning

point?

2. Is there still value in

equities?

Four burning questions for investors

Source: M&G

What is the market worrying about?

34

What is the biggest risk for markets in 2017?

Mario Draghi World Economic Forum 2013 crop" by World Economic Forum - Cropped from File:Mario Draghi World Economic Forum 2013.jpg, original source Flickr: Special Address: Mario Draghi. Licensed under CC BY-SA 2.0 via Commons - https://commons.wikimedia.org/wiki/File:Mario_Draghi_World_Economic_Forum_2013_crop.jpg#/media/File:Mario_Draghi_World_Economic_Forum_2013_crop.jpg – Bank of England via commons - https://commons.wikimedia.org/wiki/File%3ALondon.bankofengland.arp.jpg

Mario Draghi continuing QE?

China: hard or soft landing? Is global growth going to

pick up?

What’s next in commodities?

Will Fed continue to raise

rates?

Volatility is not risk – being flexible and dynamic is key

What does Brexit really mean?

Will populism continue to rise?

35

Summary

Source: M&G, April 2017

2016 has shown the folly of forecasting; what matters are valuations and the

economic environment

Equity risk premium is still the biggest valuation anomaly

Importance of being dynamic, selective and flexible in today’s markets

36

Appendix

37

Episode blog

Our bloggers

Information

www.allocationblog.com

@allocation_en

Allocation blog

“We think being aware of market inefficiencies and behavioural

biases is an essential element to being a good investor”

Bringing you Multi Asset views, straight from the fund management floor

Source: M&G, October 2015

The Multi-Asset “Allocation” blog is

available in 5 languages

38

The value of investments will fluctuate, which will cause fund prices to fall as well as rise and investors may not get back the original amount invested.

For Inv estment Professionals and Institutional Inv estors only. Not for onward distribution. No other persons should rely on any information

contained within. For Switzerland: Distribution of this document in or from Switzerland is not permissible with the exception of the distribution to

Qualified Investors according to the Swiss Collectiv e Inv estment Schemes Act, the Swiss Collective Inv estment Schemes Ordinance and the

respectiv e Circular issued by the Swiss supervisory authority ("Qualified Investors"). Supplied for the use by the initial recipient (prov ided it is a

Qualified Investor) only. In Spain the M&G Investment Funds are registered for public distribution under Art. 15 of Act 35/2003 on Collective Investment

Schemes as follows: M&G Investment Funds (1) reg. no 390, M&G Investment Funds (2) reg. no 601, M&G Investment Funds (3) reg. no 391, M&G

Investment Funds (5) reg. no 972, M&G Investment Funds (7) reg. no 541, M&G Investment Funds (9) reg. no 930, M&G Investment Funds (12) reg. no 1415,

M&G Investment Funds (14) reg. no 1243, M&G Global Dividend Fund reg. no 713, M&G Dynamic Allocation Fund reg. no 843, M&G Global Macro Bond Fund

reg. no 1056 and M&G Optimal Income Fund reg. no 522, M&G (Lux) Investment Funds 1 reg. no 1551. The collective investment schemes referred to in this

document (the "Schemes") are open-ended investment companies with variable capital, incorporated in England and Wales in respect of M&G Investment

Funds and in Luxembourg in respect of M&G (Lux) Investment Funds. In the Netherlands, all funds referred to, are registered with the Dutch regulator, the

AFM. This information is not an offer or solicitation of an offer for the purchase of investment shares in one of the Funds referred to herein. Purchases of a

Fund should be based on the current Prospectus. The Instrument of Incorporation, Prospectus, Key Investor Information Document, annual or interim

Investment Report and Financial Statements, are available free of charge, in paper form, from the ACD: M&G Securities Limited, Laurence Pountney Hill,

London, EC4R 0HH, GB; or one of the following - M&G International Investments Limited, German branch, mainBuilding, Taunusanlage 19, 60325 Frankfurt

am Main; the Austrian paying agent: Société Générale Vienna Branch, Zweigniederlassung Wien Prinz Eugen-Strasse, 8-10/5/Top 11 A-1040 Wien, Austria;

the Luxembourg paying agent Société Générale Bank & Trust SA, Centre operational 28-32, place de la Gare L-1616 Luxembourg; the Danish paying agent:

Nordea Bank Danmark A/S Issuer Services, Securities Services, Hermes Hus, Helgeshøj Allé 33, Postbox 850, DK-0900, Copenhagen C, Denmark; Allfunds

Bank, Calle Estafeta, No 6 Complejo Plaza de la Fuente, La Moraleja, 28109, Alcobendas, Madrid, Spain; M&G International Investments Limited, the French

branch; from the French centralising agent of the Fund: RBC Investors Services Bank France; or from the Swedish paying agent: Nordea Bank AB (publ),

Smålandsgatan 17, 105 71 Stockholm, Sweden. For Switzerland, please refer to M&G International Investments Switzerland AG, Talstrasse 66, 8001 Zurich or

Société Générale, Paris, Zurich Branch, Talacker 50, P.O. Box 5070, 8021 Zurich, which acts as the Swiss representative of the Schemes (the "Swiss

Representative") and acts as their Swiss paying agent. For Italy, they can also be obtained on the website: www.mandgitalia.it. For Germany and Austria,

copies of the Instrument of incorporation, annual or interim Investment Report, Financial Statements and Prospectus are available in English and the

Prospectus and Key Investor Information Documents/s are available in German. Before subscribing inv estors should read the Prospectus, which includes

investment risks relating to these funds. The information contained herein is not a substitute for independent advice. In Switzerland, this financial promotion is

issued by M&G International Investments Switzerland AG, authorised and regulated by the Swiss Federal Financial Market Supervisory Authority. Elsewhere, it

is issued by M&G International Investments Ltd. Registered Office: Laurence Pountney Hill, London EC4R 0HH, authorised and regulated by the Financial

Conduct Authority in the UK. Registered in England No. 4134655 and has a branch located in France, 6 rue Lamennais 34, Paris 75008, registered on the

Trade Register of Paris, No. 499 832 400 and a branch in Spain, with corporate domicile at Plaza de Colón 2, Torre II, Planta 14, 28046, Madrid, registered

with the Commercial Registry of Madrid under Volume 32.573, sheet 30, page M-586297, inscription 1, CIF W8264591B and registered with the CNMV under

the number 79. The Portuguese Securities Market Commission (Comissão do Mercado de Valores Mobiliários, the “CMVM”) has received a passporting

notification under Directive 2009/65/EC of the European Parliament and of the Council and the Commission Regulation (EU) 584/2010 enabling the fund to be

distributed to the public in Portugal. M&G International Limited is duly passported into Portugal to provide certain investment services in such jurisdiction on a

cross-border basis and is registered for such purposes with the CMVM and is therefore authorised to conduct the marketing (comercialização) of funds in

Portugal.