IFRS and Deferred Tax Assets - Soliumsolium.com/wp-content/uploads/2012/11/wp_ifrsdta.pdf ·...

6

IFRS and Deferred Tax Assets A Peek into the EU Playbook

Transcript of IFRS and Deferred Tax Assets - Soliumsolium.com/wp-content/uploads/2012/11/wp_ifrsdta.pdf ·...

IFRS and Deferred Tax AssetsA Peek into the EU Playbook

Adoption. Convergence. Endorsement. Oh, and then there is the head-scratcher of the bunch, condorsement. While FASB sorts out what to call its inevitable move toward IFRS or IFRS-like standards, stock plan administrators in the United States are wondering how the transition will affect them. And though much has been said about straight-line versus accelerated amortization methods, the industry has yet to take a closer look at how FASB may decide to handle a few of the not-so-obvious reporting matters that will no doubt be affected by a move toward IFRS-style standards. In this white paper, we take a closer look at how the reporting of deferred tax assets (DTA) might change under an IFRS model.

We sometimes speak of IFRS as if there is one single definitive standard, but jurisdictions that have embraced it generally have made it work for their needs. DTA as a concept doesn’t exist in Canada, as there is no corporate tax benefit of this nature available to issuers. When searching for a useful IFRS DTA model, a good place to start is with the one favored by the European Union (EU).

EU rules

The EU method for handling DTA is a multistep process that differs substantially from the one stipulated by U.S. GAAP. Unlike in the United States, where deferred tax is calculated based exclusively on the expense charge and trued up to the actual tax benefit at the time of transaction, IFRS dictates a company must adjust their expected DTA amount, and therefore the accrual of that DTA, during the life of the award. This method enables companies to get a more accurate projection of their eventual tax impact. The EU’s DTA method bears some resemblance to mark-to-market accounting, so some steps won’t be entirely unfamiliar.

To make these periodic adjustments, companies use the stock price at the end of the reporting period. The expense charge itself is not affected, but for DTA purposes, an intrinsic value is calculated between the end-of-period stock price and issuing price of each award. This value, multiplied by the number of shares outstanding and then by the corporate tax rate, will provide the expected DTA as of that point in time.

This value is then accrued according to the same amortization method as the base award, given that graded amortization is the IFRS standard. Let’s pause here and look at an example that illustrates the first few steps.

How might you handle your deferred tax assets under IFRS?

.com 2IFRS and Deferred Tax Assets

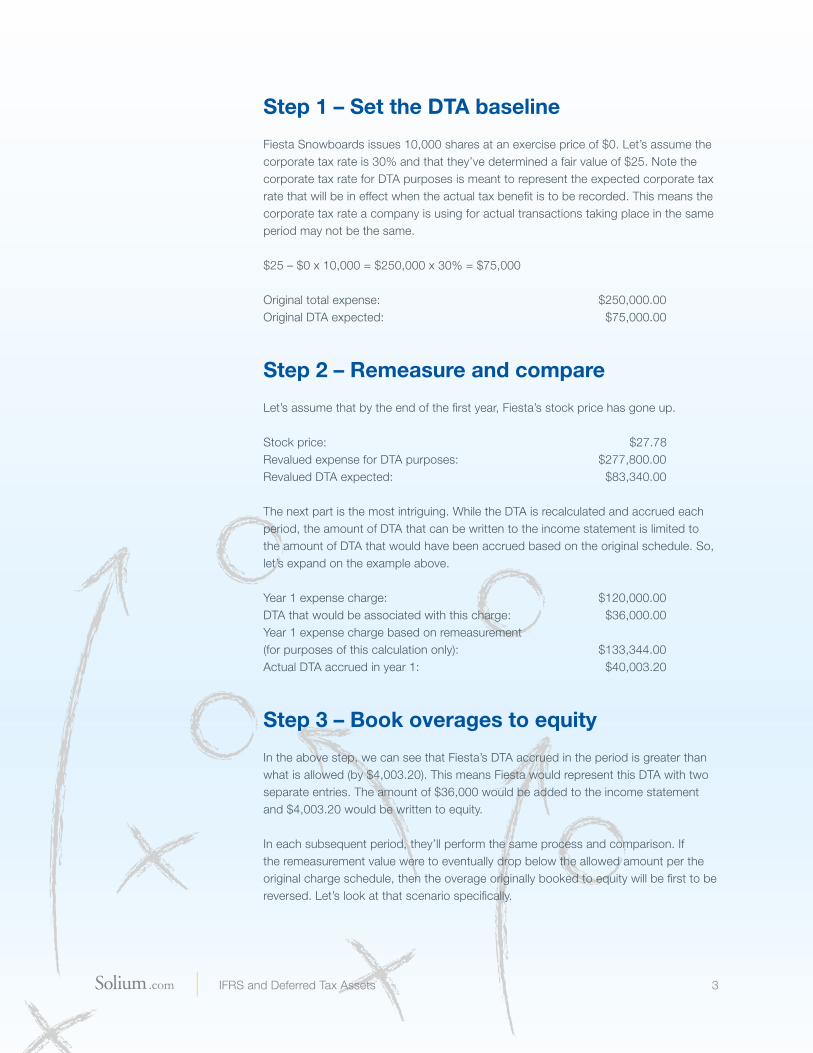

Step 1 – Set the DTA baseline

Fiesta Snowboards issues 10,000 shares at an exercise price of $0. Let’s assume the corporate tax rate is 30% and that they’ve determined a fair value of $25. Note the corporate tax rate for DTA purposes is meant to represent the expected corporate tax rate that will be in effect when the actual tax benefit is to be recorded. This means the corporate tax rate a company is using for actual transactions taking place in the same period may not be the same.

$25 – $0 x 10,000 = $250,000 x 30% = $75,000

Original total expense: $250,000.00 Original DTA expected: $75,000.00

Step 2 – Remeasure and compare

Let’s assume that by the end of the first year, Fiesta’s stock price has gone up.

Stock price: $27.78 Revalued expense for DTA purposes: $277,800.00 Revalued DTA expected: $83,340.00

The next part is the most intriguing. While the DTA is recalculated and accrued each period, the amount of DTA that can be written to the income statement is limited to the amount of DTA that would have been accrued based on the original schedule. So, let’s expand on the example above.

Year 1 expense charge: $120,000.00 DTA that would be associated with this charge: $36,000.00Year 1 expense charge based on remeasurement (for purposes of this calculation only): $133,344.00 Actual DTA accrued in year 1: $40,003.20

Step 3 – Book overages to equity

In the above step, we can see that Fiesta’s DTA accrued in the period is greater than what is allowed (by $4,003.20). This means Fiesta would represent this DTA with two separate entries. The amount of $36,000 would be added to the income statement and $4,003.20 would be written to equity.

In each subsequent period, they’ll perform the same process and comparison. If the remeasurement value were to eventually drop below the allowed amount per the original charge schedule, then the overage originally booked to equity will be first to be reversed. Let’s look at that scenario specifically.

.com 3IFRS and Deferred Tax Assets

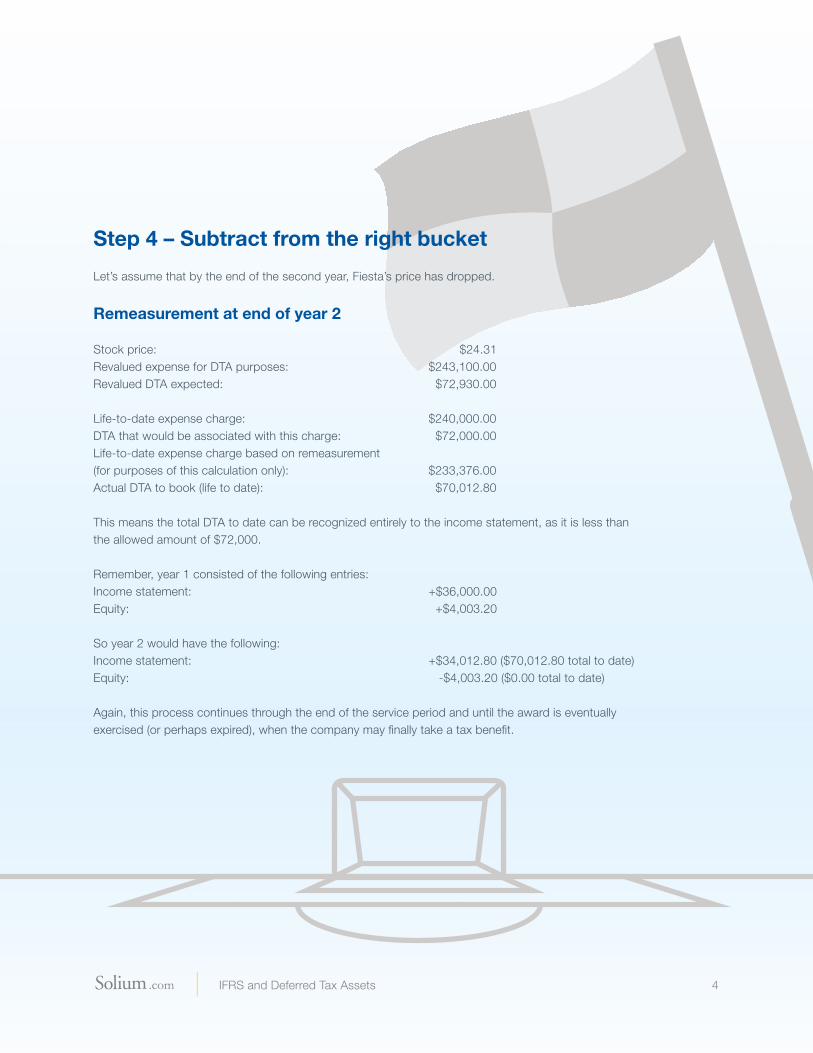

Step 4 – Subtract from the right bucket

Let’s assume that by the end of the second year, Fiesta’s price has dropped.

Remeasurement at end of year 2

Stock price: $24.31 Revalued expense for DTA purposes: $243,100.00 Revalued DTA expected: $72,930.00

Life-to-date expense charge: $240,000.00 DTA that would be associated with this charge: $72,000.00Life-to-date expense charge based on remeasurement (for purposes of this calculation only): $233,376.00 Actual DTA to book (life to date): $70,012.80

This means the total DTA to date can be recognized entirely to the income statement, as it is less than the allowed amount of $72,000.

Remember, year 1 consisted of the following entries:Income statement: +$36,000.00Equity: +$4,003.20

So year 2 would have the following: Income statement: +$34,012.80 ($70,012.80 total to date) Equity: -$4,003.20 ($0.00 total to date)

Again, this process continues through the end of the service period and until the award is eventually exercised (or perhaps expired), when the company may finally take a tax benefit.

.com 4IFRS and Deferred Tax Assets

Step 5 – Calculate the actual tax benefit

When calculating the actual tax benefit, Fiesta will perform a similar comparison of estimated value to actual value, which may isolate portions of the benefit to the income statement and equity. In this case, we assumed the actual corporate tax rate at the end of the service period would have increased to 35%.

Corporate tax rate: 35% Taxable compensation realized by participant: $340,000.00 Actual tax benefit for company: $119,000.00

This $119,000 is compared to the tax benefit that would be associated with the IFRS charge for the same shares. The resulting comparison will dictate if they can write all or part of the tax benefit to the income statement.

IFRS charge for shares exercised: $306,000.00 Actual tax benefit allowed to income statement: $107,100.00 ($306,000.00 * 35%) Remaining tax benefit pushed to equity: $11,900.00 (($340,000.00 – $306,000.00) * 35%)

The last piece of the puzzle is the alternate entry when an actual tax benefit is booked (that is, the reversal of the DTA previously set aside for those shares). It’s important to reverse the DTA from the right bucket, either the income statement or equity. Let’s continue with our example.

IFRS charge for shares exercised: $306,000.00 Most recent revalued expense for DTA purposes: $323,000.00 Total DTA to be reversed: $96,900.00 ($323,000.00 * 30%) DTA to reverse from income statement: $91,800.00 ($306,000.00 * 30%) DTA to reverse from equity: $5,100.00 (($323,000.00 – 306,000.00) * 30%)

This same reversal of DTA, and the analysis thereof to see what bucket it’s reversed from, also takes place if shares expire or for some reason are cancelled in a vested state.

Final thoughts

The EU’s DTA method is a comparatively intricate process that requires more frequent calculations than U.S. issuers may be accustomed to, but it ultimately results in a more accurate expectation. While it’s by no means certain if FASB will choose to handle DTA in a manner similar to the EU, it does seem relatively certain that significant change is around the corner.

As a global provider of stock plan administration software and services, Solium Capital has experience with different instances of IFRS. We’ve gone through hundreds of conversions and, when the time comes, we can help you navigate the complex road to compliance. When you choose Solium, you choose the experts.

.com 5IFRS and Deferred Tax Assets

About Solium

Solium is a leading global provider of web-based stock plan administration technology and services. Shareworks®, our industry-leading software, provides unrivaled, comprehensive regulatory and financial reporting capabilities, helping companies automate and manage their stock option and purchase plans.

Since our inception in 1999, we have been known as industry pioneers, always striving to change the status quo and challenge conventional methods. We take great pride in being leaders of change and delivering the most innovative stock plan administration experience possible for finance and HR professionals, plan administrators and participants. Solium has offices in Canada, the United States and the UK.

Contact Solium

© 2012 Solium Capital Inc. All rights reserved. The Solium logo and Shareworks are trademarks or registered trademarks of Solium Capital in the U.S. and/or other countries.

Calgary, ABLondon, UK

Shelton, CT

Montréal, QC

Toronto, ON

Phoenix, AZ

San Francisco, CA