IDB Group Forum 2008 “Impact of the Global Financial ... · “Impact of the Global Financial...

20

IDB Group Forum 2008 “Impact of the Global Financial Crisis and Islamic Finance” Iqbal Khan CEO - Fajr Capital Islamic Development Bank, Jeddah 25 October 2008

Transcript of IDB Group Forum 2008 “Impact of the Global Financial ... · “Impact of the Global Financial...

IDB Group Forum 2008“Impact of the Global Financial Crisisand Islamic Finance”

Iqbal KhanCEO - Fajr Capital

Islamic Development Bank, Jeddah25 October 2008

Fajr Capital | 2

“Seven major crises in 20 years ... that is not goodenough.”

(Larry Summers, Former US Secretary of the Treasury)

The global elite is underperforming

Fajr Capital | 3

Latin America n Debt Crisis -Beginning in Mexico (1980s)

1

US Savings and LoansCrisis (1989-1991)

2Collapse of Japanese

Asset Price Bubble(1990s)

3

Speculative Attacks onCurrencies in the EuropeanExchange Rate Mechanism(1992-1993)

4

Mexican Economic Crisis:Speculative Attack andDefault on Mexican Debt(1994-1995)

5Asian Financial Crisis:

Devaluations and BankingCrises across Asia (1997-1998)

6

Russian Financial Crisis:Devaluation of the Ruble andDefault on Russian Debt (1998)

7

Argentine Economic Crisis:Breakdown of Banking System(1999-2002)

8

US and Europe: Spread of theUS Subprime MortgageCrisis (2008)

9

1980 1990 2000 2008

Timeline1 2 3 4 6 75 8 9

Major financial crises since 1980

Fajr Capital | 4

Collapse/rescue ofmajor financial institutions

Unprecedented intervention byglobal regulators

• Direct government capital infusions

• Increased guarantee of bank depositaccounts

• Taxpayers becoming shareholders inbanks

Source: BBCnews.com (6 Oct 2008)

Current crisis is illustrated by milestone events (I)

Fajr Capital | 5

Dow: -37%MSCI: -41%

Volatility in markets Corporate liquidity crisis

Hang Seng: -53%Nikkei 300: -43%

FTSE 100: -39%DJ Eurostoxx 50: -52%

Oil falls from July peak of$147 to around $70 p.b.

Gold fluctuated from$750 to $900 in 30 days

Global equity markets tumble- MSCI World Index -19.60% (3m)

Source: Bloomberg, FT

• Access to credit has shutdown

• Impact on corporate operations

• Impact on earnings starting to show

Current crisis is illustrated by milestone events (II)

1Y performance:

Fajr Capital | 6

I and others who believed that “lending institutionswould do a good job of protecting theirshareholders are in a ‘state of shocked disbelief’. ”

(Alan Greenspan, Former Chairman - U.S. Federal Reserve)

Shocked disbelief

Fajr Capital | 7

• Extremelyoverleveraged banks1:- EU average of 35-1(Deutsche 50-1)- US average of 20-1(Lehman 30-1)

• Consumer attitudes:- “Buy-now-pay-later”- US sub-prime are20% of mortgage write-downs2

• Household debt3:- UK 165% ofdisposable income- US 138%

Excessive lending

A multitude of factors, with long term systemic changes needed

Root causes are unsustainable pattern ofbehaviour

Source: 1: Centre for European Policy Studies; 2: IMF Report Oct 2008; 3: OECD Report 2006; 4: Arabnews.com (23 Oct 2008); 5: Marketwatch.com (22 Jun 2008)

Fajr Capital | 8

• Extremelyoverleveraged banks1:- EU average of 35-1(Deutsche 50-1)- US average of 20-1(Lehman 30-1)

• Consumer attitudes:- “Buy-now-pay-later”- US sub-prime are20% of mortgage write-downs2

• Household debt3:- UK 165% ofdisposable income- US 138%

Excessive lending

• Misleading ratings:AAA ratings on sub-prime MBS which aredifficult to price andvalue

• Derivatives disaster4:- $600 trillion industry- CDS - $55 trillion- (World GDP $66 t)

Opaque financialsecurities

A multitude of factors, with long term systemic changes needed

Root causes are unsustainable pattern ofbehaviour

Source: 1: Centre for European Policy Studies; 2: IMF Report Oct 2008; 3: OECD Report 2006; 4: Arabnews.com (23 Oct 2008); 5: Marketwatch.com (22 Jun 2008)

Fajr Capital | 9

• Extremelyoverleveraged banks1:- EU average of 35-1(Deutsche 50-1)- US average of 20-1(Lehman 30-1)

• Consumer attitudes:- “Buy-now-pay-later”- US sub-prime are20% of mortgage write-downs2

• Household debt3:- UK 165% ofdisposable income- US 138%

Excessive lending

• Misleading ratings:AAA ratings on sub-prime MBS which aredifficult to price andvalue

• Derivatives disaster4:- $600 trillion industry- CDS - $55 trillion- (World GDP $66 t)

Opaque financialsecurities

• Misalignedincentives:Generous bonuseswhile shareholderssuffer

• Sleepy supervision:Fractured set-up withpiecemeal regulation

• Regulatory lapses:Buildup of $10 trillion5

shadow bankingindustry; low creditapproval screens,leverage ratio

Failings ingovernance

A multitude of factors, with long term systemic changes needed

Root causes are unsustainable pattern ofbehaviour

Source: 1: Centre for European Policy Studies; 2: IMF Report Oct 2008; 3: OECD Report 2006; 4: Arabnews.com (23 Oct 2008); 5: Marketwatch.com (22 Jun 2008)

Fajr Capital | 10

FinancialInstitutions

Impact of current crisis is sweeping

Systemic impact Global Markets

Real Economy

PolicyImplications

1

2

3

4

Fajr Capital | 11

FinancialInstitutions

Financial institutions hardest hit 1

Largest banking writedowns and capital raisingto date (USD billion – 13 October 2008)

• Cause of writedowns:Banking exposure to mortgagebacked debt and derivativeproducts

• Capital shortfall:- Small capital bases andreliance on short-term fundinghave led to solvency fears andliquidity crunch- Capital raising has not offsetwritedowns to date

Fajr Capital | 12

Global banks too large forhome regulators to save

• Credit driven:Loan books grewinflating assets

• As big as countries:11 banks are biggerthan their country

• Systematic risk:Size of banks increasescost of collapse – and acase for separation ofpayments system

Source: Citi Research

FinancialInstitutions

1

Iceland

Switzerland

Belgium

Switzerland

Denmark

LuxembourgSweden

BelgiumSweden

NorwaySweden

SpainGreece

Italy

Fajr Capital | 13

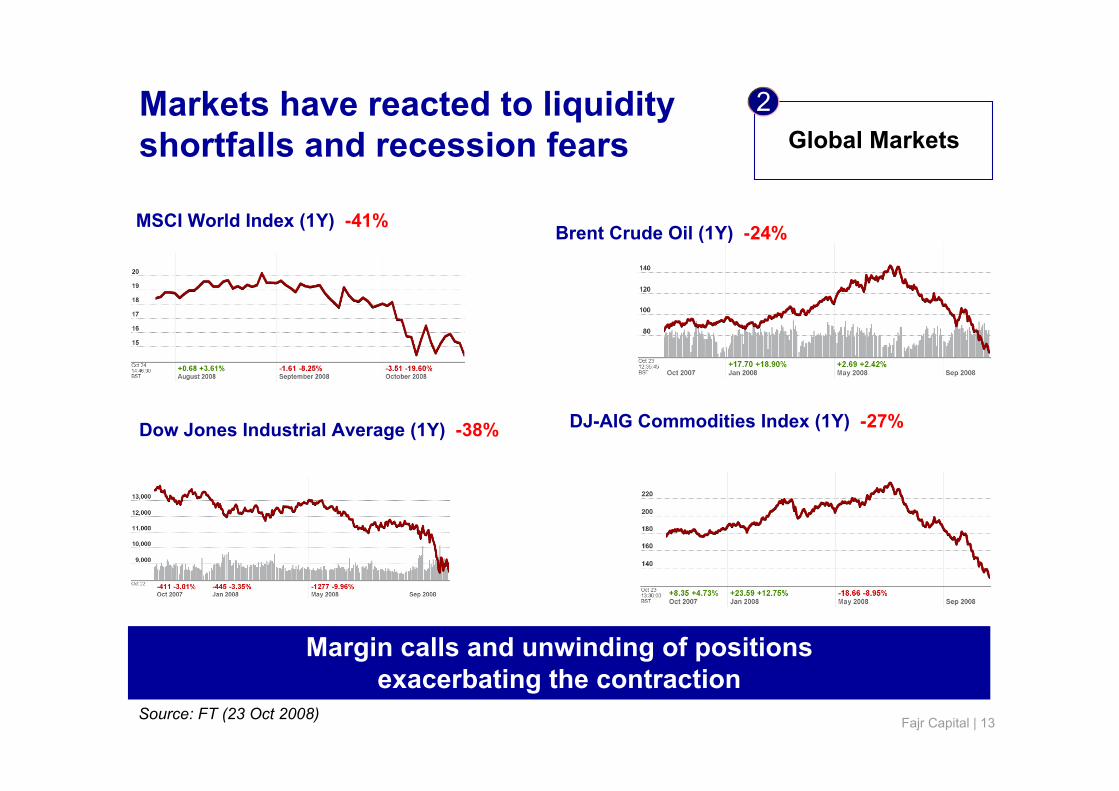

Global MarketsMarkets have reacted to liquidityshortfalls and recession fears

2

MSCI World Index (1Y) -41% Brent Crude Oil (1Y) -24%

DJ-AIG Commodities Index (1Y) -27%Dow Jones Industrial Average (1Y) -38%

Source: FT (23 Oct 2008)

Margin calls and unwinding of positionsexacerbating the contraction

Fajr Capital | 14

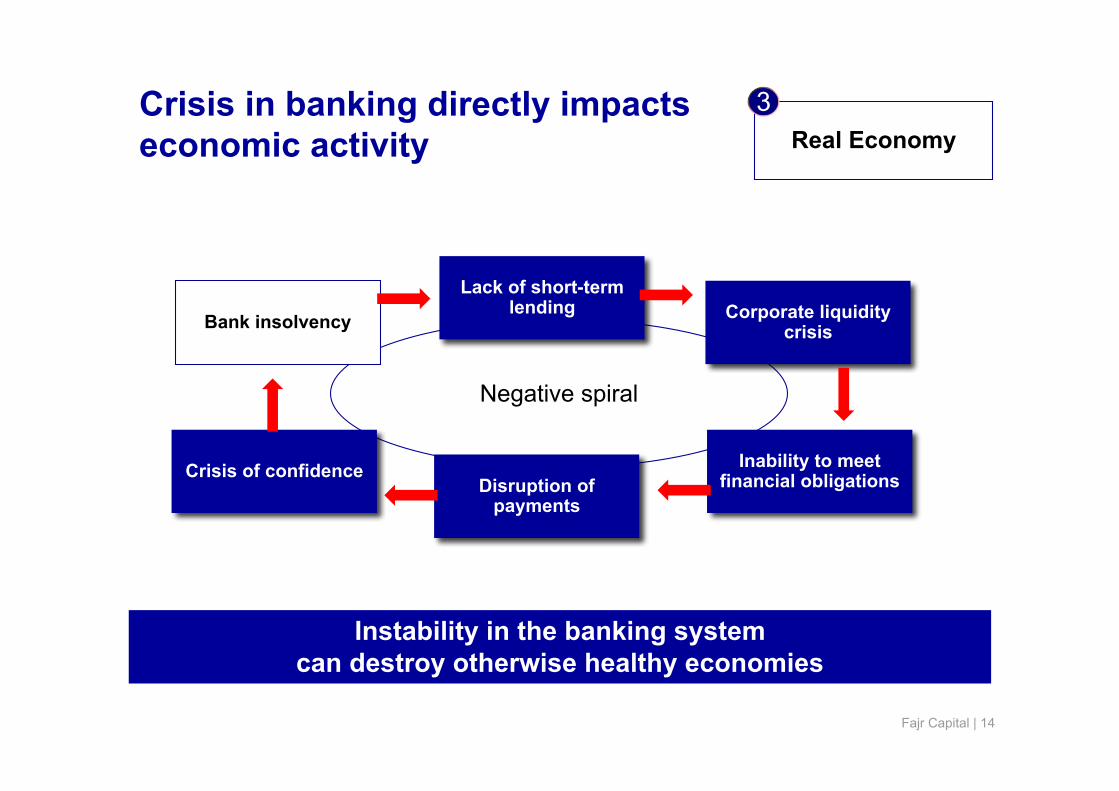

Real EconomyCrisis in banking directly impactseconomic activity

3

Negative spiral

Bank insolvency

Lack of short-termlending Corporate liquidity

crisis

Inability to meetfinancial obligationsDisruption of

payments

Crisis of confidence

Instability in the banking systemcan destroy otherwise healthy economies

Fajr Capital | 15

Real EconomyEconomic crisis puts mostvulnerable stakeholders as risk

3

Small and Medium-sized Enterprises

(SME)

Beneficiaries ofpublic aid

Beneficiaries ofinternational aid

Food insecure

• Employment impact: SMEs are the economy’semployment generation base

• Public welfare project strains: Government capitalinjections will draw from other budget items

• Humanitarian relief impact: Benevolent aid packageswill be effected as low priority budget allocations

• Economic downturn: Bottom-of-the-pyramid will be themost socially vulnerable group as disposable income isthreatened

Shari’a-compliant solutions needed to ensure the flow of aid

Fajr Capital | 16

PolicyImplications

Crisis is recastingbasic regulatory model

4

Lending practices

Financial securitiesmarket

Accountability

The case for“narrow banking”

• How did sub-prime mortgages reach 20% of U.S.mortgage market?

• Reform of derivatives market regulation(in particular CDS and CDO) is required

• Need for global co-ordination in supervision activities, withlender-of-last-resort empowered with greater authority

• Fundamental distinction between guaranteed deposit-takers (bank payment system) and investment managers(risk-bearing accounts) is increasingly essential

Fajr Capital | 17

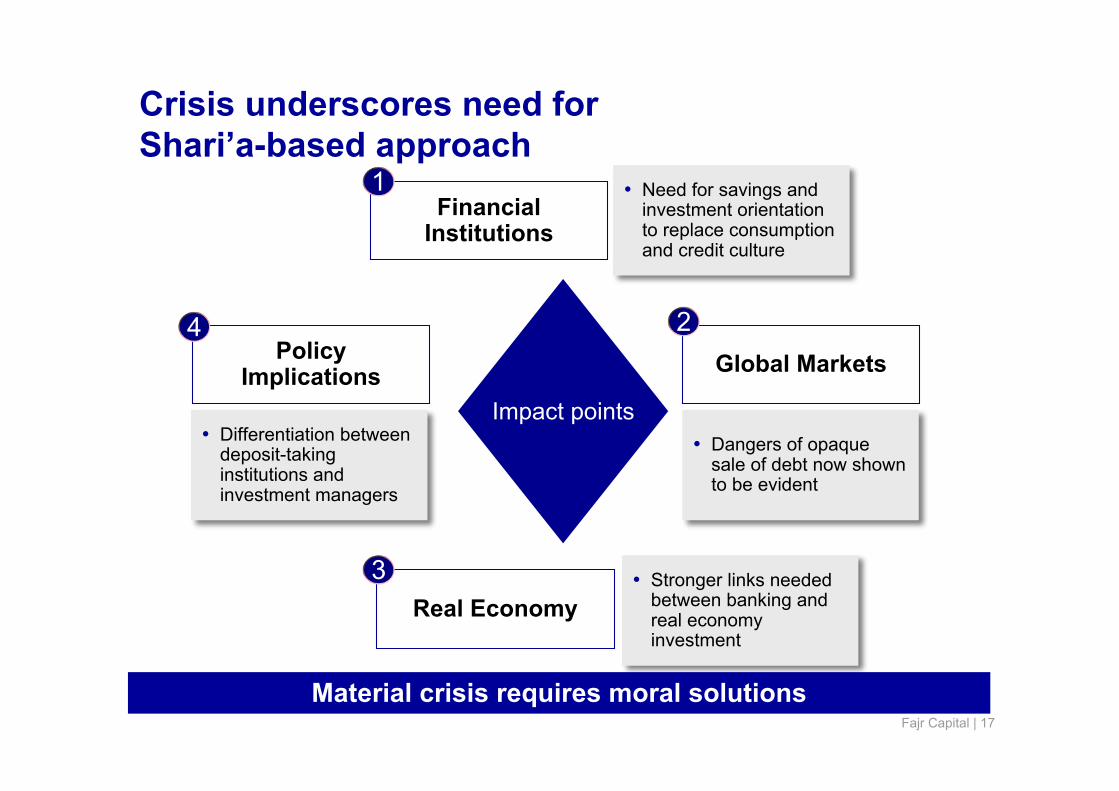

FinancialInstitutions

Crisis underscores need forShari’a-based approach

Impact points

Global Markets

Real Economy

PolicyImplications

1

2

3

4

• Need for savings andinvestment orientationto replace consumptionand credit culture

• Dangers of opaquesale of debt now shownto be evident

• Differentiation betweendeposit-takinginstitutions andinvestment managers

• Stronger links neededbetween banking andreal economyinvestment

Material crisis requires moral solutions

Fajr Capital | 18

Is Islamic finance the key to solving the current crisis?

In theory, Islamic principleswould avoid the crisis...

• Riba-based and creditarylending

• The unrestricted sale of debt

• Gharar and lack oftransparency in financialsecurities

Fajr Capital | 19

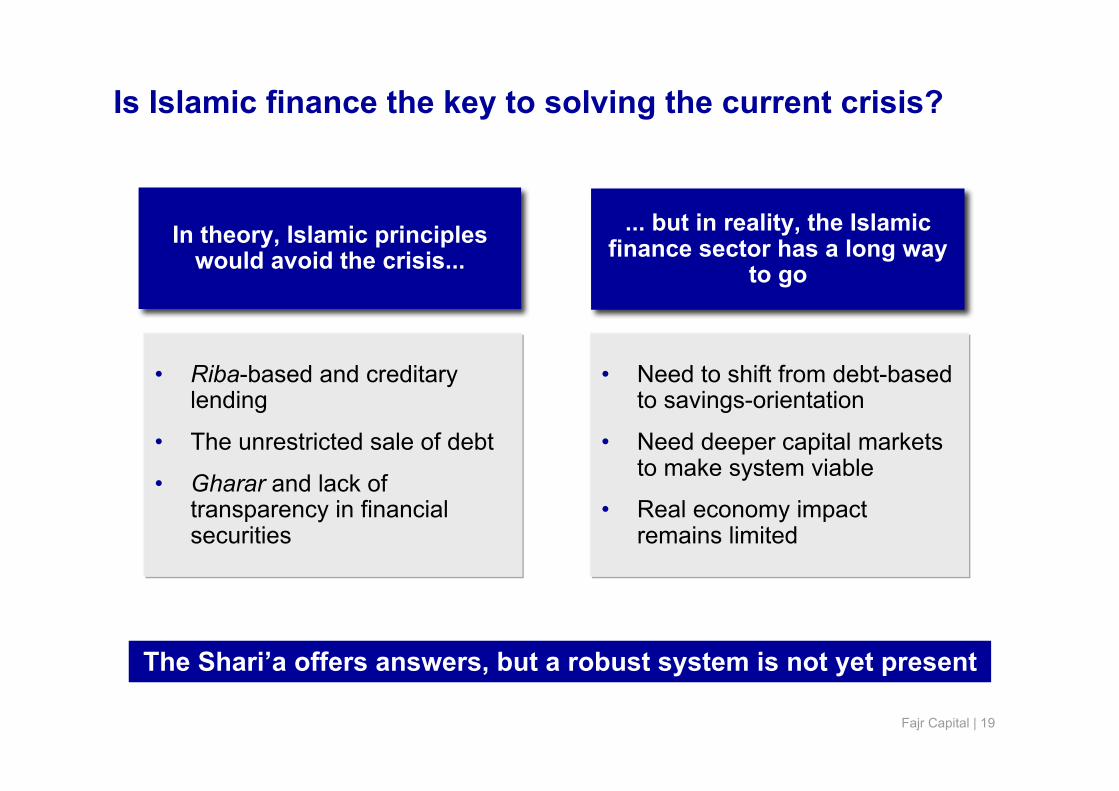

Is Islamic finance the key to solving the current crisis?

In theory, Islamic principleswould avoid the crisis...

... but in reality, the Islamicfinance sector has a long way

to go

• Riba-based and creditarylending

• The unrestricted sale of debt

• Gharar and lack oftransparency in financialsecurities

• Need to shift from debt-basedto savings-orientation

• Need deeper capital marketsto make system viable

• Real economy impactremains limited

The Shari’a offers answers, but a robust system is not yet present

Fajr Capital | 20

Crisis brings opportunity for fundamental re-thinking

Holistic, multi-disciplinary approach is required

Diverse stakeholders must be involved

Pivotal time for Shari’a-based thought leadership

Corporate Social Responsibility (CSR) needed as urgently as ever,in innovative and creative ways

Closing thoughts

Today’s IDB Forum is a landmark opportunity