ICT Indicators Charts End of Q4 2014 - CITC of... · The CITC issues a MVNO licenses ... (MENA) and...

14

- 1 - ICT Indicators Charts End of Q4 2014

Transcript of ICT Indicators Charts End of Q4 2014 - CITC of... · The CITC issues a MVNO licenses ... (MENA) and...

- 1 -

ICT Indicators Charts

End of Q4 2014

- 2 -

in the Kingdom of Saudi Arabia growth The ICT Sector

1. Mobile Telecommunications Market

The total number of mobile subscriptions reached around 53 million by the

end of 2014, with penetration rate of 171.4%. Prepaid subscriptions constitute the

majority (over 87%) of all mobile subscriptions. The CITC issues a MVNO licenses

by the end of 2014 which will help improve services and costumer care plus the

variation of the provided services, in addition the distribution of the ICT market

will increase and more options for the users will be available.

- 3 -

2. Fixed Telephony Market

Fixed telephone lines reached 3.62 million by the end of 2014, of which

around 2.53 million or 70% were residential lines. This represents a household

teledensity of around 45 %, while the population teledensity is about 11.8%, it is

noted that the number of subscribtions is decresed due to the comption of the

mobile services in prices and qualty which make it a subtituon of fixed services

plus the Settlement of some unpaid accounts and cancling the accounts of all

expatriates who are leaving the country for good.

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014

5.5 6.1 6.3 6.6 7.3 6.9 6.8

30.5 38.7 45.3 47.1 45.7 43.9 45.9

138%

167%

186% 188% 181.6%

169.7% 171.4%

36

45

52

54

53

51 53

Sub

scri

pti

on

s (M

illio

ns)

Mobile Service Market Growth-Total Subscriptions

Post-paid Subscriptions Pre-paid Subscriptions Mobile Penetration (%) Total Subscriptions

- 4 -

Note: Population teledensity is calculated by dividing the total number of fixed lines by the total population, and household teledensity is

calculated by dividing the total number of residential fixed lines by the total number of households.

3. Broadband Market:

Recently, demand for broadband services has increased significantly compared to previous years, due to the society's need for broadband services, especially after the government strong support for high tech projects which require good digital infrastructure. In addition, many government services are being accessed through e-government transactions. The widespread use of Internet in society is another factor that led to this growth, where the Internet has become a major source of hundreds of thousands of applications that are downloaded to smart devices such as social networking, business applications, text messaging, security tools, games and more. This has driven service providers to provide many broadband packages targeting different user segments.

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014

3.0 3.0 3.1

3.3 3.4 3.3

2.5

1.1 1.17 1.03

1.3 1.44 1.41

1.1

66.8% 65.1% 66.7%

69.3% 67.6%

64.3%

45.0%

15.8% 15.5% 15.0% 16.2% 16.4% 15.7%

11.8%

Tele

ph

on

e L

ines (

Mil

lio

ns)

Residential Lines Business Lines

Household Teledensity (%) Population Teledensity (%)

- 5 -

4. Fixed Broadband Services:

Fixed broadband subscriptions including DSL, fixed wireless (WiMax), FTTx and

other fixed lines have grown to around 3 million subscriptions at the end 2014.

The Fixed broadband penetration rate stands at about 43.2% of households.

5. Mobile Broadband Services:

The total number of mobile broadband subscriptions continues to increase,

and reached around 29 million by the end 2014, representing a population

penetration rate of 94.5%. The mobile broadband market also continues to gain

momentum in the Kingdom. The key reasons for this growth include strong

competition, the healthy expansion in the use of smart phones, and the offering of

various data packages by mobile operators suitable for different user segments.

These have led to a dramatic rise in the number of users in recent years, and an

increase in the data traffic over these devices, supported by the wide coverage of

the 3G and 4G networks.

0.118 0.258 0.428

1.00

1.30 1.49 1.56 1.87

1.85 1.38

0.2

0.3

0.6

0.8 1.2

1.04

1.44

1.74 1.95

2.54

2.92 3.03

0%

10%

20%

30%

40%

50%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2008 2009 2010 2011 2012 2013 2014

Pen

etr

ati

on

(%

)

Su

bscri

pti

on

s (

Mil

lio

n)

Leased lines + FTTx ADSL Subscriptions

Fixed Wireless Subscriptions Total Fixed Broadband Subscriptions

Households Penetration (%)

- 6 -

6. Internet Services :

The number of Internet users in the Kingdom continues to rise rapidly,

reaching about 19.6 million at the end of 2014, with a population penetration of

63.7%. Increased demand for Internet services and broadband was observed due

to high use of social networking applications, video downloading and gaming.

Customers are seeking higher speeds and larger packages resulting in heavy data

traffic on both mobile and fixed networks.

2.70 4.28 4.22 4.59

9.13

7.06 8.07 9.68

19.96

9.7%

39.6% 42.1%

47.6%

94.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

30

35

2010 2011 2012 2013 2014

Pe

ne

tra

tio

n (

%)

Su

bs

cri

pti

on

s (

Mil

lio

n)

Standard Mobile Subscriptions Dedicated Mobile Data Subscriptions

Total Mobile Broadband Subscriptions Mobile BB Telednsity (of populations)

- 7 -

It is expected that the demand for Internet services will continue to

increase significantly over the next few years as a result of the availability of high

speed fiber-optic networks (FTTx), increased Internet content, and the continued

spread.

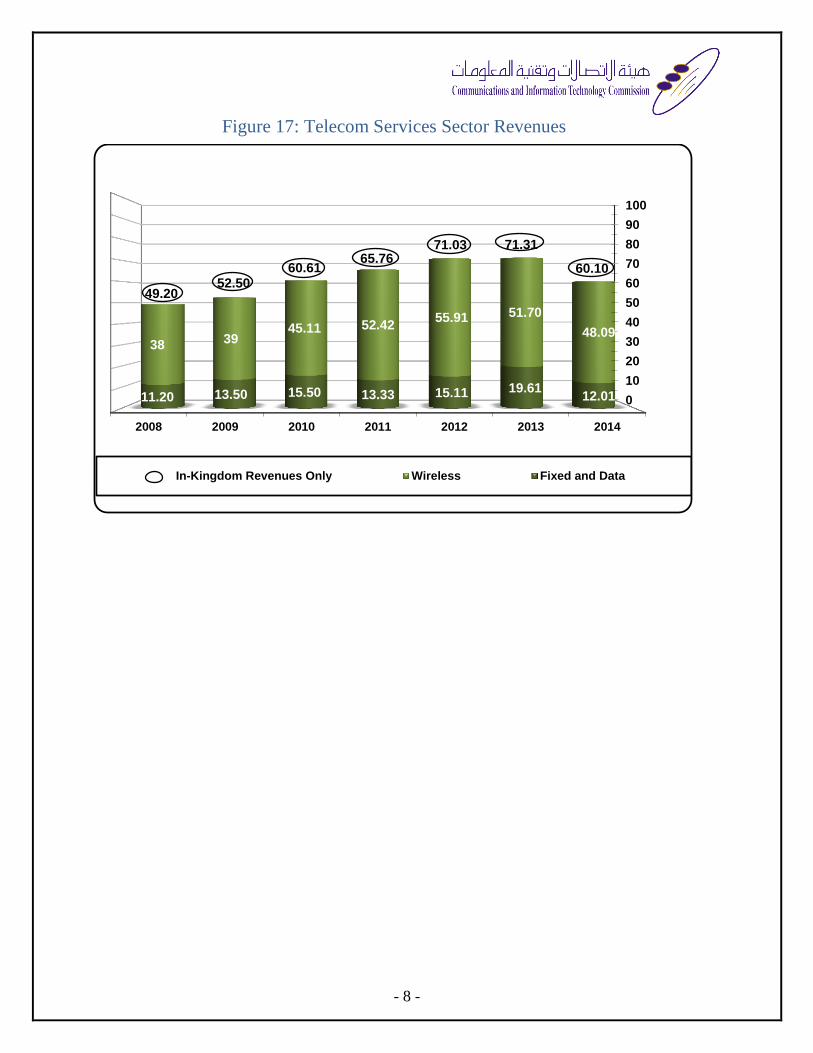

9.5 Telecom Services Sector Revenues:

Telecom services revenues from operations in Saudi Arabia reached about SAR

68.18 billion in 2014. Decreased about 4.3% of 2013 due to the reduction of

services price, plus the CITC role in regulating services prices for non-

competitive markets, Mobile revenues represent 77.8% of all telecom sector

revenues, with fixed and data services accounting for the remaining 22.2%..

0

2

4

6

8

10

12

14

16

18

2008 2009 2010 2011 2012 2013 2014

9.3 10.3

11.4

13.6

15.8

16.5

19.6

36%

38%

41%

47.5%

54.1% 55.1%

63.7%

Internet Penetration (%)

Internet Users (Million)

- 8 -

Figure 17: Telecom Services Sector Revenues

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014

11.20 13.50 15.50 13.33 15.11 19.61 12.01

38 39 45.11 52.42

55.91 51.70

48.09

49.20 52.50

60.61 65.76

71.03 71.31

60.10

In-Kingdom Revenues Only Wireless Fixed and Data

- 9 -

10.7 International Internet Bandwidth

The total capacity for international Internet connectivity in 2014 was about

1321 gigabits per second (Gbits/s) compared to 318 Gbits/s in 2010.

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014

318 440 556 814.2

1321

Gb

ps

International internet bandwidth

- 10 -

9-1 Telecom Service Prices and Inflation:

The liberalization of the telecommunications sector and the opening of its markets

to competition has led to improved coverage and quality of services, increased

choice of suppliers, in addition to lowering of service prices over the past years. It

is worthy to note that while in recent years the Saudi market has seen a remarkable

rise in goods and services prices, the prices of telecommunications services has

been in continual decline.

The cost of living index in KSA increased by 2.7 percent in 2014 compared to

2013. This is due to the rise in the major expenditure groups of the consumer price

index except for the telecommunications services group which decreased by about

0.1 percent in 2014.

Figure (14) shows that the general cost of living index increased by around 30.1

percent cumulatively over the period 2007-2014, while the prices of telecom

services decreased by around 6.3%. This decline is mainly because of the

accelerating pace of competition in the telecommunications market and the

diversity of promotions offered, which reflected positively on the prices of services.

- 11 -

9-2 ICT Contribution to the National Economy

The ICT sector plays an important role in the national economy, and can be

measured the extent of its effect on several indicators, including: contributing to the

gross domestic product of the economy, investment in the activity of

Communications and Information Technology, and the size of spending on ICT

services.

9-2-1 Contribution to the National GDP

The growth of capital investment, and the development and expansion and of ICT

networks have significantly contributed to the national gross domestic product

(GDP). This growth has been the result of liberalizing the telecommunications

sector and opening the markets to competition, The deployment of modern

technology and availability of applications have the positive effect of raising the

efficiency of other economic sectors as well. According to CITC estimates, the

contribution of the ICT sector represents around 2.78% of total GDP and has been

rising over the past three years. If, however, the oil and mining sector components

of the GDP are excluded, it is estimated that the ICT contribution to the national

GDP is up to 8%. In addition, the huge investments in infrastructure and networks

currently underway, particularly broadband services, will further enhance the

contribution of telecommunication services in GDP. Studies also show that there is

a direct correlation between the availability of broadband services and the rate of

growth to GDP. It is estimated that a 10% increase in the availability of broadband

services could result in growth in GDP of 1.3%.

The published data indicates that the communications and transport sector is the

fastest growing economic sectors. This sector has achieved a growth of about 6% in

2014, and the average annual growth rate during the past five years (2010-2014) is

about 8.7%.

- 12 -

8.72%

5.8%

0% 2% 4% 6% 8% 10%

Communication & Transport

Agriculture , Forestry & Fishing

Mining & Quarrying

Manufacturing

Electricity , Gas and Water

Construction

Wholesale & Retail Trade, Restaurants& hotels

Finance , Insurance , Real Estate ' &Business Services

Community , Social & Personal Services

Imputed Bank Services Charge

Producers of Government Services

Total GDP

Source: Central Department of Statistics & Information

- 13 -

9-2-2 Investments in ICT

The investment environment in the Kingdom is distinguished by the continuous

evolution and high profitability returns to investors with light of the growing

investments taking place in the government and private sector, and with the

recovery of consumer confidence, as well as the growing focus by companies to

enhance their efficiency and support capabilities. The aim of the Kingdom is to

shift to an information society and to become a leader in the field of ICT. The

Kingdom is also looking forward to achieve this by attracting investments that

enhance competitiveness, and help to create quality jobs, and contribute to the

diversification of income sources and technology transfer. The Kingdom is the

largest ICT market by far in (MENA) and this lead Saudi Arabia to

Succeed in its endeavors to become one of the top-ranking economies of the world.

The estimated current capital investment in the ICT sector in the kingdom is

currently more than 30 billion riyals ($ 8 billion), mostly concentrated in

infrastructure projects, particularly fixed and mobile broadband networks, and in

solutions for information security, managed services, and 3rd Platform solutions.

CITC expects that the investments in the sector to increase in the next few years

with the growing demand in the market for telecommunications services and

information technology for broadband services, and data services, and applications

of the 3rd Platform, as well as with the entry of mobile virtual network operators

(MVNOs) to the market. This will undoubtedly lead to enhanced market efficiency

and improve the level of services, and contribute to lowering of prices.

- 14 -

9-2-3 Spending on ICT Services:

CITC estimates that spending on ICT services was up to SAR 111 billion in 2014,

with a growth rate of about 9% compared to 2013. The telecommunications sector

accounts for the lion's share of spending by 64%, while the proportion of spending

on IT services is about 36%. This scale of expenditure is due to the investment in

infrastructure for the Next generation Networks, and 4G mobile networks, and the

adoption of electronic services (e-government,e-health, e-education, e-commerce,

etc.) as well as spending on information security. It is expected that the

telecommunications market and information technology will continue to grow on a

regular basis, to exceed the size of spending by about 120 billion riyals in 2015.

4.5 5.2 5.8 7 9 14.4

18 21 21.9 22.5 24.8 33

37.29 39.96

13.5 15.7 17.6

21

27

33.6

42

49 51.1 52.5

57.8

61

65.27

71.04

18 21 23.4

28

36

48

60

70 73

75

82.5

94

102.5

111

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Spending on Telecommunications Services and Information Technology

IT Telecom Total Spending Annual Growth