Icici Life Insurance - Copy

146

PART-I 1

-

Upload

ranaindia2011 -

Category

Documents

-

view

232 -

download

2

Transcript of Icici Life Insurance - Copy

PART-I

1

EXECUTIVE SUMMARY

2

EXECUTIVE SUMMARY

Overall, the life insurance and pension sector is set for rapid changes and growth in

the years ahead. Delivering service, building trust and being innovative are key areas

in which any company will have to excel in order to do well in the long road ahead.

Different companies will take different approaches and it would be myriad of

solutions that will be found to delight the Indian customer.

During the first part, I was given complete classroom training about the various unit

linked as well as the traditional plans and solutions which the company offers.

Later, Market Research was done through various activities and tele-calling which are

discussed further in the report. Activities led to practical exposure and taught me the

aspects of customer dealing.

Finally, interesting conclusions were drawn out of the data collected regarding the

Awareness of Financial Planning among the people in today’s environment.

It was great experience because selling an insurance product demands a great deal of

confidence and product knowledge.

3

INDUSTRY PROFILE

4

INDUSTRY PROFILE

The business of life insurance in India in its existing form started in India in the year

1818 with the establishment of the Oriental Life Insurance Company in Calcutta.

The story of insurance is probably as old as the story of mankind. The same instinct

that prompts modern businessmen today to secure themselves against loss and disaster

existed in primitive men also. They too sought to avert the evil consequences of fire

and flood and loss of life and were willing to make some sort of sacrifice in order to

achieve security. Though the concept of insurance is largely a development of the

recent past, particularly after the industrial era – past few centuries – yet its

beginnings date back almost 6000 years.

Life Insurance in its modern form came to India from England in the year 1818.

Oriental Life Insurance Company started by Europeans in Calcutta was the first life

insurance company on Indian Soil. All the insurance companies established during

that period were brought up with the purpose of looking after the needs of European

community and these companies were not insuring Indian natives.

Bombay Mutual Life Assurance Society heralded the birth of first Indian life

insurance company in the year 1870, and covered Indian lives at normal rates.

Bharat Insurance Company (1896) was also one of such companies inspired

by nationalism. The Swadeshi movement of 1905-1907 gave rise to more

insurance companies.

The United India in Madras, National Indian and National Insurance in

Calcutta and the Co-operative Assurance at Lahore were established in 1906.

5

In 1907, Hindustan Co-operative Insurance Company took its birth in one of

the rooms of the Jorasanko, house of the great poet Rabindranath Tagore, in

Calcutta.

The Indian Mercantile, General Assurance and Swadeshi Life (later Bombay

Life) were some of the companies established during the same period.

The Parliament of India passed the Life Insurance Corporation Act on the 19th of

June 1956, and the Life Insurance Corporation of India was created on 1st September,

1956, with the objective of spreading life insurance much more widely and in

particular to the rural areas with a view to reach all insurable persons in the country,

providing them adequate financial cover at a reasonable cost.

Some of the important milestones in the life insurance business in India are:

1850: Non life insurance debuts with triton insurance company.

1870: Bombay mutual life assurance society is the first Indian owned life insurer.

1912: The Indian Life Assurance Companies Act enacted as the first statute to

regulate the life insurance business.

1928: The Indian Insurance Companies Act enacted to enable the government to

collect statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the

objective of protecting the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies taken over by the

central government and nationalized. LIC formed by an Act of Parliament, viz. LIC

6

Act, 1956, with a capital contribution of Rs. 5 Crore from the Government of India.

Insurance sector reforms

In 1993, Malhotra Committee, headed by former Finance Secretary and RBI

Governor R. N. Malhotra, was formed to evaluate the Indian insurance industry and

recommend its future direction.

The Malhotra committee was set up with the objective of complementing the reforms

initiated in the financial sector.

The reforms were aimed at “creating a more efficient and competitive financial

system suitable for the requirements of the economy keeping in mind the structural

changes currently underway and recognizing that insurance is an important part of the

overall financial system where it was necessary to address the need for similar

reforms…”.

The Insurance Regulatory and Development Authority (IRDA)

The Insurance Act, 1938 had provided for setting up of the Controller of Insurance to

act as a strong and powerful supervisory and regulatory authority for insurance. Post

nationalization, the role of Controller of Insurance diminished considerably in

significance since the Government owned the insurance companies.

But the scenario changed with the private and foreign companies foraying in to the

insurance sector. This necessitated the need for a strong, independent and autonomous

Insurance Regulatory Authority was felt. As the enacting of legislation would have

taken time, the then Government constituted through a Government resolution an

Interim Insurance Regulatory Authority pending the enactment of a comprehensive

legislation.

7

The Insurance Regulatory and Development Authority Act, 1999 is an act to provide

for the establishment of an Authority to protect the interests of holders of insurance

policies, to regulate, promote and ensure orderly growth of the insurance industry and

for matters connected therewith or incidental thereto and further to amend the

Insurance Act, 1938, the Life Insurance Corporation Act, 1956 and the General

insurance Business (Nationalization) Act, 1972 to end the monopoly of the Life

Insurance Corporation of India (for life insurance business) and General Insurance

Corporation and its subsidiaries (for general insurance business).

Insurance Sector Reforms

Prior to liberalization of Insurance industry, Life insurance was monopoly of LIC.

In 1993, Malhotra Committee- headed by former Finance Secretary and RBI

Governor R.N. Malhotra- was formed to evaluate the Indian insurance industry and

recommend its future direction. The Malhotra committee was set up with the

objective of complementing the reforms initiated in the financial sector. The reforms

were aimed at creating a more efficient and competitive financial system suitable for

the requirements of the economy keeping in mind the structural changes currently

underway and recognizing that insurance is an important part of the overall financial

system where it was necessary to address the need for similar reforms. In 1994, the

committee submitted the report and some of the key recommendations included:

Structure

Government stake in the insurance Companies to be brought down to 50%.

Government should take over the holdings of GIC and its subsidiaries so that these

subsidiaries can act as independent corporations.

8

Competition

Private Companies with a minimum paid up capital of Rs.1 billion should be allowed

to enter the sector. No Company should deal in both Life and General Insurance

through a single entity. Foreign companies may be allowed to enter the industry in

collaboration with the domestic companies.

Regulatory Body

The Insurance Act should be changed. An Insurance Regulatory body should be set

up. Controller of Insurance- a part of the Finance Ministry- should be made

independent

Investments

Mandatory Investments of LIC Life Fund in government securities to be reduced from

75% to 50%. GIC and its subsidiaries are not to hold more than 5% in any company

(there current holdings to be brought down to this level over a period of time)

STATISTICS (INDIAN & GLOBAL)

This section gives the users important and detailed statistics of the Indian as well as

the Global insurance industry. These statistics would give important insights of where

the respective markets are headed for.

The global life insurance market stands at $1,521.2 billion while the non-life

insurance market is placed at $922.4 billion.

The United States itself accounts for about one-third of the $2443.6 billion

global insurance market and Japan stands next with a 20.62% share.

9

India takes the 23rd position with US $9.933 billion annual premium

collections and a meager 0.41% share.

Out of one billion people in India, only 35 million people are covered by

insurance.

India's life insurance premium as a percentage of GDP is just 1.77 per cent.

The income derived by GIC and its subsidiary companies through investment

was Rs.2491.76 crore and the investable fund generated was Rs.2843 crore in

1999-2000.

Indian insurance market is set to touch $25 billion by 2010, on the assumption

of a 7 per cent real annual growth in GDP.

NATURE OF INDUSTRY

The insurance industry provides protection against financial losses resulting from a

variety of perils. By purchasing insurance policies, individuals and businesses can

receive reimbursement for losses due to car accidents, theft of property, and fire and

storm damage; medical expenses; and loss of income due to disability or death.

The insurance industry consists mainly of insurance carriers (or insurers) and

insurance agencies and brokerages. In general, insurance carriers are large companies

that provide insurance and assume the risks covered by the policy. Insurance agencies

and brokerages sell insurance policies for the carriers.

Insurance companies assume the risk associated with annuities and insurance policies

and assign premiums to be paid for the policies. In the policy, the companies states

10

the length and conditions of the agreement, exactly which losses it will provide

compensation for, and how much will be awarded.

The premium charged for the policy is based primarily on the amount to be awarded

in case of loss, as well as the likelihood that the insurance carrier will actually have to

pay. In order to be able to compensate policyholders for their losses, insurance

companies invest the money they receive in premiums, building up a portfolio of

financial assets and income-producing real estate which can then be used to pay off

any future claims that may be brought.

There are two basic types of insurance carriers: Direct and Reinsurance.

Direct carriers are responsible for the initial underwriting of insurance policies and

annuities, while Reinsurance carriers assume all or part of the risk associated with the

existing insurance policies originally underwritten by other insurance carriers.

Direct insurance carriers offer a variety of insurance policies.

Life insurance provides financial protection to beneficiaries—usually spouses and

dependent children—upon the death of the insured.

Disability insurance supplies a preset income to an insured person who is unable to

work due to injury or illness

Health insurance pays the expenses resulting from accidents and illness.

An Annuity (a contract or a group of contracts that furnishes a periodic income at

regular intervals for a specified period) provides a steady income during retirement

for the remainder of one’s life.

11

Property-casualty insurance protects against loss or damage to property resulting from

hazards such as fire, theft, and natural disasters.

Liability insurance shields policyholders from financial responsibility for injuries to

others or for damage to other people’s property. Most policies, such as automobile

and homeowner’s insurance, combine both property-casualty and liability coverage.

Companies that underwrite this kind of insurance are called property-casualty carriers.

12

What is Life Insurance?

Human life is subject to risks of death and disability due to natural and accidental

causes. When human life is lost or a person is disabled permanently or temporarily,

there is a loss of income to the household. The family is put to hardship. Risks are

unpredictable. Death/disability may occur when one least expects it. There are a

number of life insurance products which offer protection and also coupled with

savings.

A Term insurance product provides a fixed amount of money on death during the

period of contract.

A Whole Life insurance product provides a fixed amount of money on death.

An Endowment Assurance product provided a fixed amount of money either on death

during the period of contract or at the expiry of contract if life assured is alive.

A Money Back Assurance product provides not only fixed amounts which are payable

on specified dates during the period of contract, but also the full amount of money

assured on death during the period of contract.

An Annuity product provides a series of monthly payments on stipulated dates

provided that the life assured is alive on the stipulated dates.

A Linked product provides not only a fixed amount of money on death but also sums

of money which are linked with the underlying value of assets on the desired dates.

13

There are a variety of life insurance products to suit to the needs of various categories

of people—children, youth, women, middle-aged persons, old people; and also rural

people, film actors and unorganized laborers.

Life insurance products could be purchased from registered life insurers notified by

the IRDA. Insurers appoint insurance agents to sell their products.

As per regulations, insurers have to give the various features of the products at the

point of sale. The insured should also go through the various terms and conditions of

the products and understand what they have bought and met their insurance needs.

They ought to understand the claim procedures so that they know what to do in the

event of a loss.

INDIAN INSURANCE SECTOR

REGULATORY BODY

Insurance is a federal subject in India. The primary legislation that deals with

insurance business in India is: Insurance Act, 1938, and Insurance Regulatory &

Development Authority Act, 1999.

The Insurance Regulatory and Development

Authority (IRDA)

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill in

Parliament in December 1999. The IRDA since its incorporation as a statutory body

in April 2000 has fastidiously stuck to its schedule of framing regulations and

registering the private sector insurance companies.

14

The other decision taken simultaneously to provide the supporting systems to the

insurance sector and in particular the life insurance companies was the launch of the

IrDA’s online service for issue and renewal of licenses to agents. Since being set up

as an independent statutory body the IRDA has put in a framework of globally

compatible regulations.

MISSION-IRDA

“To protect the interests of the policyholders, to regulate, promote and ensure orderly

growth of the insurance industry and for matters connected therewith or incidental

thereto.”

IMPACT OF LIBERALISATION

The introduction of private players in the industry has added to the colors in the dull

industry. The initiatives taken by the private players are very competitive and have

given immense competition to the on time monopoly of the market LIC. Since the

advent of the private players in the market the industry has seen new and innovative

steps taken by the players in this sector.

The new players have improved the service quality of the insurance. As a result LIC

down the years have seen the declining phase in its career. The market share was

distributed among the private players. Though LIC still holds the 79% of the

insurance sector but the upcoming natures of these private players are enough to give

more competition to LIC in the near future. LIC market share has decreased from

95% (2002-03) to 81 %( 2004-05).

15

LIC has the current market share of 79%.

Among the private players ICICI Prudential has the maximum of appx. 5.60%

Bharti Axa has the current market share of 5%.

Followed by Bajaj Allianz (3.27 %) and HDFC Standard Life of about 3.11%.

Below is the table that shows the market share of various players of the industry.

16

The following companies have the rest of the market share of the insurance industry.

COMPANY NAME MARKET SHARE

LIC 79.30

ICICI PRUDENTIAL

BHARTI AXA

5.63

5

BAJAJ ALLIANZ 3.27

HDFC STANDARD LIFE 3.11

BIRLA SUNLIFE 2.32

TATA AIG 1.45

SBI LIFE 1.24

MAX NEWYORK 0.90

AVIVA LIFE 0.82

ING VYSYA 0.66

OM KOTAK LIFE 0.54

AMP SANMAR 0.38

METLIFE 0.33

RELIANCE LIFE 0.05

The liberalization of the Indian insurance sector has opened new doors to private

competition and the new and improved insurance sector today promises several new

job opportunities. With private players now in the field, there will be innovative

products, better packaging, improved customer service, and, most importantly, greater

employment opportunities.

17

There are a number of options to choose from for a career in Insurance. Ideally an

insurance company will have openings in the following fields:

Actuaries

Underwriter

Surveyor

Investment

Marketing & Distribution

Actuaries

Evaluates the risk for companies to be used for strategic management

decisions.

Actuaries use their analytical skills to predict the risk of writing insurance

policies through the use of mathematical, statistical and economic models.

An actuary not only fixes the premium rates for new products, but also revises

both products and prices. They calculate costs to assume risk

Underwriters

Insurance underwriters review insurance applications and decide whether they

should be accepted or rejected based on the degree of risks involved in

insuring the people or objects of concern.

In the life insurance business, an underwriter is expected to filter the "bad or

substandard lives". Whereas, in the general insurance segment, he takes care

of risk management.

18

CURRENT SCENARIO OF THE INDUSTRY

INSURANCE MARKET IN INDIA

India with about 200 million middle class household shows a huge untapped potential

for players in the insurance industry. Saturation of markets in many developed

economies has made the Indian market even more attractive for global insurance

majors. The insurance sector in India has come to a position of very high potential and

competitiveness in the market.

Innovative products and aggressive distribution have become the say of the day.

Indians, have always seen life insurance as a tax saving device, are now suddenly

turning to the private sector that are providing them new products and variety for their

choice. Life insurance industry is waiting for a big growth as many Indian and foreign

companies are waiting in the line for the green signal to start their operations. The

Indian consumer should be ready now because the market is going to give them an

array of products, different in price, features and benefits. How the customer is going

to make his choice will determine the future of the industry.

19

DISTRIBUTION CHANNELS

LIC has already well established and have an extensive distribution channel and

presence. New players may find it expensive and time consuming to bring up a

distribution network to such standards. Therefore they are looking to the diverse areas

of distribution channel to have an advantage. At present the distribution channels that

are available in the market are:

• Direct selling/Retail

• Corporate agents

• Group selling

• Brokers and cooperative societies

• Bancassurance

An agent should be a pleasing personality with complete knowledge about the various

plans and solutions which the company has to offer and must also understand the

customer’s psychology well to deal in an efficient manner.

BANCASSURANCE

Bancassurance is the distribution of insurance products through the bank's distribution

channel. It is a phenomenon wherein insurance products are offered through the

distribution channels of the banking services along with a complete range of banking

and investment products and services. To put it simply, Bancassurance, tries to exploit

synergies between both the insurance companies and banks.

20

Advantages to banks

Productivity of the employees increases.

By providing customers with both the services under one roof, they

can Improve overall customer satisfaction resulting in higher customer retention

Levels.

Increase in return on assets by building fee income through the sale of

Insurance products.

Can leverage on face-to-face contacts and awareness about the

financial Conditions of customers to sell insurance products.

Banks can cross sell insurance products e.g.: Term insurance products with loans.

Advantages to insurers

Insurers can exploit the banks' wide network of branches for distribution of

products. The penetration of banks' branches into the rural areas can be

utilized to sell products in those areas.

Customer database like customers' financial standing, spending habits,

investment and purchase capability can be used to customize products and sell

accordingly.

Since banks have already established relationship with customers, conversion

ratio of leads to sales is likely to be high. Further service aspect can also be

tackled easily.

21

Advantages to consumers

Comprehensive financial advisory services under one roof. i.e., insurance

services along with other financial services such as banking, mutual funds,

personal loans etc.

Enhanced convenience on the part of the insured

Easy accesses for claims, as banks are a regular go.

Innovative and better product ranges

WHAT DOES LIFE INSURANCE HAVE TO OFFER?

Life insurance is many different things to many different people. For some, it is a

premium to be paid on time. For others it offers liquidity since cash can be borrowed

when needed. For the investment-minded, it denotes a constantly growing capital

account and numerous other benefits.

The contractual guarantee is the promise to pay, backed by one of the oldest and most

stably regulated financial industry operating in the Indian sub-continent today.

1) Insurance Buys Time and Money

People like to refer to life insurance as time insurance, the reason being that life

insurance proceeds are paid to the insured's beneficiaries in case of death. The money

proffered by life insurance helps buy time to adjust to the change of circumstances.

Insurance provides large amounts of cash that will keep the lifestyle for the survivors

the way it was before the insured's death.

2) Insurance Offers Peace of Mind

22

For the person who buys an insurance policy, it offers absolute and complete peace of

mind. He or she knows that the decision made by him will provide sound benefits in

the future, whether or not the individual may live to see it.

3) Multiple Applications

The future is uncertain for each and every one. No one knows how long he or she will

live. The investment benefit is paid to the insured's beneficiaries after his death or it

can be used during the life as well. Life insurance policy owners can turn to the cash

value of the policy in case of a financial emergency when all avenues are either

blocked or denied.

4) Enduring Elasticity

Since life insurance is flexible enough to serve several needs, the insured can keep

several long-term goals in mind once he or she invests in the insurance plan. The cash

value of the policy can be allocated towards augmenting the monthly income during

the retirement years. Leisure years should be turned into pleasure years. Permanent

life insurance is designed on the concepts of long-term flexibility.

5) Financial Security

The insurance policy offers contractual guarantees to people looking for peace of

mind when they buy life insurance. Life insurance offers complete financial security.

The purchase of life insurance demonstrates concern for a family's future financial

well being.

6) Regard for Family

23

The purchase of life insurance clearly displays care and concern for the people the

policy owner loves.

7) Insurance is Safer

No financial institution can do what life insurance does. No industry can back its

products with reserves and surplus as sound as those of the insurance industry.

The proof of strength and safety that insurance companies have ensured even under

the most adverse of conditions is a matter of pride for the entire insurance industry.

For generation after generation, life insurance has been acclaimed as the very

benchmark of security against which the other industries are measured.

OPPORTUNITIES FOR INSURANCE COMPANIES

In the now open sector on insurance, the following is what I feel will determine the

success of the company in particular and the industry in general:

A change in the attitude of the population

Indians have always been wary of employing their hard-earned money in a venture

that will pay them on their death. Insurance has always been used as a Tax saving

tool. No more, no less. It is upon the insurers to educate the people to secure/insure

their future against any unknown calamity and make a shield around their families

and businesses.

An open and transparent environment created under the IRDA.

The reason for this being on the top of our understanding is that when ever we have

seen any sector open up in India there are always grey areas and unsure policies.

24

These are not exactly what any player, be it Indian or foreign, looks for. It creates an

air of uncertainty in all the decision making process. Insurance as a sector requires

players who are strong financially and are willing to wait for returns. Their confidence

can be bolstered only if there is an open and a transparent policy guidelines. This will

also help the consumers feel safe that the regulatory is an active one and cares to do

everything possible to keep things under control and help the insurance environment

grow maturely.

A well-established distribution network.

To cater to the largest democracy in the world is by no means a cakewalk. Insurance

profits are directly related to number of insured and this is in turn related to the reach.

Trained professionals to build and sell the product.

It is said that the insurance agent is the best salesman in the world. He makes you pay,

regularly, an amount promising to pay back only on your death. Thus the players will

require an excellent sales team to sell their products in the now competitive

environment.

Encouragement of new and better products and letting the hackneyed ones die out.

This will itself ensure the market grows. And that every class/society gets a product

that best suits them.

25

SPECIAL PROVISIONS

The Income Tax Act and Life Insurance policies

Under Section 10(10D), any sum received under a Life Insurance policy (not

being a Key Man policy) is also exempt from taxation. But it is wise to remember

that Pensions received from Annuity plans are not exempted from Income Tax.

Section 80C provides a deduction up to Rs.1,00,000/- to an individual assesses

for any amount paid as a premium.

26

POLICYHOLDERS GRIEVANCES

Policyholders may have complaints against insurers either in respect of their policies

or their claims. As per Regulations for Protection of policyholders’ interests, 2002,

every insurer should have in place, a grievance redressal system to address the

complaints of policyholders. The IRDA has a Grievance Redressal Cell which plays a

facilitative role by taking up complaints against insurers with the respective

companies for speedy resolution. The IRDA however does not adjudicate on

complaints.

SWOT ANALYSIS OF INSURANCE INDUSTRY

STRENGTH

1. Best returns with the added advantage of 100% life insurance coverage.

2. Good option for new investors into the market as all the money is invested by best

fund managers so with less knowledge also they can earn good Returns.

3. Best commission charges paid to the agents which vary from 12% to 35% which is

much higher as compared to mutual funds i.e. , only 2-2.5%.

WEAKNESS

1. BHARTI AXA could not able to match LIC in remote areas services.

2. Misleading facts given by life advisors about the returns of ULIPs.

3. Hidden charges taken by the companies.

4. Less Promotional Campaigns.

27

OPPORTUNITY

1. 80 percent of Indian population is still under insured. So there is a big opportunity

for insurance companies.

2. As the stock market can be under the mark any time so it can bring loss to the

investors but as in ULIPs there is proper mixture of debt securities and equity so

the loss is incurred during dark trading days also.

3. Unit-linked products are exempted from tax and they provide life insurance.

4. Increasing consumer awareness about Insurance and its use.

THREAT

1. Cannibalism within the industry by providing misleading figures to the investors.

2. Govt.’s instability has a long term repercussions affecting company’s policies

and its growth.

To protect your family financially

You love your family and feel responsible towards them in every way. A life

insurance plan covers your life at nominal costs so that you can fulfill your

responsibility with ease and your family never has to face financial constraints.

Why do I need to secure my family when I'm there for them?

A life insurance plan will take care of your family in case you are not around for

them.

You need to protect your family against unforeseen events. A life insurance plan helps

you do so very easily.

28

Protect your loved ones against financial contingencies at nominal costs

You love your family and feel responsible towards them in every way. But life can be

uncertain and unforeseen contingencies can meet you anytime. At such times, life

insurance comes to your rescue. As someone who wants only the best for their family,

we understand your need to safeguard your family against any crisis. Our protection

plans offer you high life cover at nominal costs so that you can fulfill your

responsibility with ease and your family never has to face financial constraints.

To maximise your savings

Life insurance plans not only ensure your family's security but are also a healthy

investment option. These investments ensure your money works hard for you by

giving you good returns along with peace of mind, as your family is protected. So

whether it is your own home, the best education for your child or even a comfortable

lifestyle, life insurance plans are the best solutions.

How does a Life Insurance plan maximise my savings?

There are variants of Life Insurance plans available today that can maximise your

savings.

The traditional plans give you definite amount as assured money back. ULIPs or

market-linked plans invest your money in the markets to help you reap high returns

along with life insurance benefits.

29

Fund managers are the experts that take care of your investment plans to ensure you

maximise your savings.

Do I need to worry about the safety of my investments?

There are different plans that you can invest in, depending on how much risk you are

ready to take. The plans can be summed up into - Traditional Plans, ULIPs and

Guarantee Plans

Traditional Plans

Traditional Plans give you guaranteed returns on the invested money. The returns you

earn through these plans are pre-decided and communicated to you at the time of

issuance of policy.

ULIPs

Unlike Traditional Plans, Unit Linked Insurance Plans (ULIPs) invest a part of your

premium amount into the financial markets. The returns under these policies depend

on market performance. Market upswings can ensure you earn high returns. There are

various fund options available under these plans. Basis your risk appetite, you can opt

for the appropriate fund option.

Guarantee Plans

Guarantee Plans are Unit Linked Plans, with an in-built 'guarantee' feature. These

plans safeguard the money invested against any market downturns. When the market

30

is up, you can enjoy high returns and in case of market downswings, there is a

minimum guaranteed amount paid to you that ensures you do not lose your hard

earned money.

Ensure your family's security as you maximise your savings

You can make your money work harder with our Wealth Creation with Protection

plans. These plans come with the double advantage of:

Complete peace of mind as your family is financially protected and

Good investment option that ensures long-term financial goals are met

Whether it is a bigger home, a dream vacation or even a comfortable future, these life

insurance plans are the best solutions along with the surety of financial protection.

Our life insurance coverage plans include 'traditional' plans that give guaranteed

money on maturity. While, we also offer market-linked plans that give you the benefit

of good market performance to maximise your savings.

Plans that help your child realise his potential and let him achieve what he

dreams of

As a responsible parent you will never want to make any compromises when it comes

to your child. Wouldn’t it be nice if you have a trusted friend who takes care of all the

finances for your child's growing dreams? Child plans, with a life insurance company

31

like ours, have been created to help you provide the best for your child's key stages

and help him secure a bright future.

To fulfill your child's dreams

As a responsible parent, you wouldn’t like to make compromises when it comes to

your child. Child plans help you secure your child's future in a planned and systematic

manner. These plans can help you fulfill your responsibilities towards your child

conveniently.

You can systematically plan for the finances required for your child's future with

these plans. You can select the term of the plan depending on your child's

requirements at their key life stages- his/her education, higher studies or even

marriage. And through periodic withdrawals from the policy, you can provide

financial assistance for the key milestones of your child. By investing in this plan, you

can make your money grow over a period of time, thereby securing your child's

dreams.

Will my child get the benefit from this plan, in case I'm not around?

The unique Waiver of Premium feature takes care of this concern. During the term of

the policy, should anything unfortunate happen to you, the protection cover is paid out

and all future premiums are waived off. This ensures that the policy continues till

maturity and you need not fear of policy lapse because you are not around to pay the

future premiums. Child plans in that sense will take care of your child and his future,

even in your absence.

32

Enjoy a golden retirement

Retirement plans are the best way to systematically plan for your golden years. By

investing in these long-term plans, you can earn a regular income even after you've

stopped working. Without worrying about rising costs, you can be self-reliant and

lead a comfortable retired life.

These are long-term plans since they aim to provide a regular income to you post your

retirement. The earlier you start, the better it is, so that when the term of the plan

ends, you can enjoy a good corpus as pension.

By investing in retirement plans today, you can ensure you lead a comfortable life,

even after you've stopped working.

Stay worry-free about your medical expenses

Health problems often hit us suddenly and they bring with them huge medical bills.

To avoid being financially strained, due to health contingencies, you can opt for a

health insurance plan and stay worry-free.

Health problems can arise anytime. With the help of a health plan, you can invest

systematically today, so that in case of any health crisis, your hefty medical bills are

taken care of.

What’s more, health insurance plans also take care of certain critical illnesses and

disabilities to ensure health problems do not impact your family's financial security.

33

NATURE & DEFINITION OF INSURANCE

Insurance is defined as a co-operative device to spread the loss

caused by a particular risk over a number of persons who are

exposed to i t and who agree to ensure themselves against that

risk. Risk is uncertainty of a financial loss. It should not be

confused with the chance of loss, which is the probable number

of losses out of confused with peril, which is defined as the

cause of loss or with hazard, which is a condition, may increase

the chance of loss.

Every risk involves the loss of one or other kind. The function

of insurance is to spread the loss over a large number of persons

who are agreed to co-operate each other at the t ime of loss. The

risk cannot be over rated but loss occurring due to a certain risk

can be distributed amongst the agreed persons. They are agreed

to share the loss because the chance of loss is there.

Everybody’s greatest asset during his/her working years is

his/her abili ty to earn an income. It is important to adequately

safeguard this asset to ensure his/her cash flow will continue in

the event of an unexpected disaster. His/her insurance policies

will help to protect him/her (if any) against any unforeseen odds.

34

There are two kinds of insurance available viz. Life Insurance

and General Insurance.

Provides for dependents in case of death.

Replaces earning power, if disabled.

Protects his/her ability to meet accumulation /

education / marriage goals.

General Insurance

Addresses health care concerns.

Provides for auto, home and personal liabili ty

protection.

Provides for potential long-term care costs.

Plans for business continuation.

GENERAL DEFINITION

The general definit ions are given by the social scientists &

they consider insurance as a device to protection against

risks, or a provision against inevitable contingencies or a

co-operative device of spreading risks. Some of such

definitions are given below:

In the words of John Magee , “Insurance is a plan by

which large number of people associate themselves

& transfer to the shoulder of all, risks that attach to

individuals.”

35

In the words of Sir William Bevridges , “The

collective bearing of risks is insurance.”

In the words of Boone & Kurtz , “Insurance is a

substi tution for a small known loss (the insurance

premium) for a large unknown loss, which may or

may not occur.”

In the words of Thomas , “Insurance is a provision,

which a prudent man makes against for the loss or

inevitable contingencies, loss or misfortune.”

In the words of Allen Z. Mayerson , “Insurance is a

device for the transfer to an insurer of certain risks

of economic loss that would otherwise come by the

insured.”

In the words of Ghosh & Agarwal , “Insurance is a

co-operative form of distributing a certain risk over

a group of persons who are exposed to it.”

FUNDAMENTAL STATEMENT

These are based on economic or business oriented since it

is a device providing financial compensation against risk

or misfortune.

In the words of D. S. Harsell , “Insurance may be

defined as a social device providing financial

compensation for the effects of misfortune, the

payments being made from the accumulated

36

contribution of all parties participating in the

scheme.”

In the words of Robert I. Mehr & Emerson

Cammark , “Insurance is purchased to offset the risk

resulting from hazards, which exposes a person to

loss.”

In the words of Riegel & Miller , “Insurance is a

social device whereby the uncertain risks of

individuals may be combined in a group & thus

made more certain small periodic contributions, by

the individuals providing a fund, out of which, those

who suffer losses may be reimbursed.”

Insurance follows important characterist ics.

Sharing of Risks

Insurance is a co-operative device to share the burden of

risk, which may fall on happening of some unforeseen

events, such as the death of head of the family, or on

happening of marine perils or loss of by fire.

Co-operative Device

Insurance is a co-operative form of distributing a certain

risk over a group of persons who are exposed to it (Ghosh

& Agarwal). A large number of persons share the losses

arising from a particular risk.

37

Evaluation of Risk

For the purpose of ascertaining the insurance premium, the

volume of risk is evaluated, which forms the basis of

insurance contract.

Payment of happening of specified event

On happening of specified event, the insurance company is

bound to make payment to the insured. Happening of the

specified event is certain in life insurance, but in the case

of fire, marine or accidental insurance, it is not necessary.

In such cases, the insurer is not liable for payment of

indemnity.

Amount of payment

The amount of payment in indemnity insurance depends on

the nature of losses occurred, subject to a maximum of the

sum insured. In life insurance, however, a fixed amount is

paid on the happening of some uncertain event or on the

maturity of the policy.

Large number of insured persons

The success of insurance business depends on the large

number of persons insured against similar risk. This will

enable the insurer to spread the losses of risk among large

number of persons, thus keeping the premium rate at the

minimum.

38

Insurance is not a gambling

Insurance is not a gambling. Gambling is il legal, which

gives gain to one party & loss to the other. Insurance is a

valid contract to indemnity against losses. Moreover,

insurable interest is present in insurance contracts & it has

the element of investment also.

Insurance is not charity

Charity pays without consideration but in the case of

insurance, premium is paid by the insured to the insurer in

consideration of future payment.

Protection against risks

Insurance provides protection against risks involved in

life, materials & property. It is a device to avoid or

reduce risks.

Spreading of risk

Insurance is a plan, which spread the risks & losses of few

people among a large number of people. John Magee

writes, “Insurance is a plan by which large number of

people associates themselves & transfer to the shoulders

of all , risks attached to individuals.”

39

Transfer of risk

Insurance is a plan in which the insured transfers his risk

on the insurer. This may be the reason that Mayerson

observes, that insurance is a device to transfer some

economic losses to the insurer, and otherwise such losses

would have been borne by the insured themselves.

Ascertaining of losses

By taking a l ife insurance policy, one can ascertain his

future losses in terms of money. This is done by the

insurer to determining the rate of premium, which is

calculated on the basis of maximum risks.

A contract

Insurance is a legal contract between the insurer & insured

under which the insurer promises to compensate the

insured financially within the scope of insurance policy, &

the insured promises to pay a fixed rate of premium to the

insurer.

Based upon certain principle

Insurance is a contract based upon certain fundamental

principles of insurance, which includes utmost good faith,

insurable interest , contribution, indemnity, causa proxima,

subrogation, etc., which are the basis for successful

operation of insurance plan.

40

Utmost Good Faith

Insurance is a contract based on good faith between the

parties. Therefore, both the parties are bound to disclose

the important facts affecting to the contract before each

other. Utmost good faith is one of the important

principles of insurance.

To conclude, insurance is a device for the transfer of risks from

the insured to the insurers, who agree to i t for a consideration

(known as premium), & promises that the specified extent of loss

suffered by the insured shall be compensated. It is a legal

contract of a technical nature.

To conclude, insurance is a device for the transfer of risks from the insured to

the insurers, who agree to it for a consideration (known as premium), &

promises that the specified extent of loss suffered by the insured shall be

compensated. It is a legal contract of a technical nature.

41

INTRODUCTION TO INSURANCE COMPANY.

In order to go through the journey of LIC – Path of private sector

insurance companies to nationalize company to again private sector

insurance companies is given as below:

Path

Private Life Insurance Companies

Nationalization

Privatization of Life Insurance Sector

1870 –

1956

Life Insurance concept was

accepted with almost 250 Private

Life Insurance Companies

1956

Merging of almost 250 Private

Sector Life Insurance Companies

in one nationalized

Life Insurance Corporation of

India

1995Proposal to privatize life

insurance business

42

June

2000Registration process was notified

August

2000Application was filed

Octobe

r 2000

1st license was issued with

introduction of IRDA

2002

During the month of January, 11

Life and Non-Life Private

Insurance license were issued

In order to elaborate the above path lets go through the history of Life

Insurance Sector.

On 3rd December 1670, seven earnest men of Bombay with just seven rupees

for initial expenses gave shape to a plan of offering insurance to the public

without the risk of ruin and the Bombay Mutual Life Insurance Society came

into existence.

Right up to the end of the 19th century, foreign insurance companies had an

upper hand in the matter of insurance business and they enjoyed mere

monopoly and the partiality were observed in the form that Indian lives were

insured with 10% extra premium as a common practice, at that time Lala

Harikishan Lal from Lahore was called “The Napoleon of Indian Finance” as

he was then called to launch the Bharat Insurance Company at Lahore (1896)

in Punjab.

43

Prior to 1912, India had no legislation for regulating insurance. The Life

Insurance Companies Act 1912 and the Provident Fund Act 1912 were

passed.

The Insurance Act 1938 was the first comprehensive legislation governing not

only life but also non-life branches of insurance to provide strict state control

over insurance business.

But after the introduction of Insurance Act 1938, the demand for

nationalization of Life Insurance Industry was raised, there were so many

reasons in order to nationalize the insurance sector.

They are:

Policyholders will be provided cent percent security.

Expenses will be reduced due to Absence of duplication,

wasteful competition

Better service due to absence of profit motive.

The funds will be available for nation building activities.

Insurance is servicing sector and so that it should be in the

hands of government only.

Above are few but strong reasons, which have contributed towards

nationalization of insurance sector, and then after in the year 1956, all

insurance companies were merged in to one and Life Insurance Corporation of

India came into existence.

44

Till the year 1999, LIC of India was the only insurance sector in economic

market with ever-increasing growth rate and market share with the capacity to

earn high rate of profit and thus profitability. In spite of all these merits of

LIC, the overall status of insurance sector was not so satisfactory.

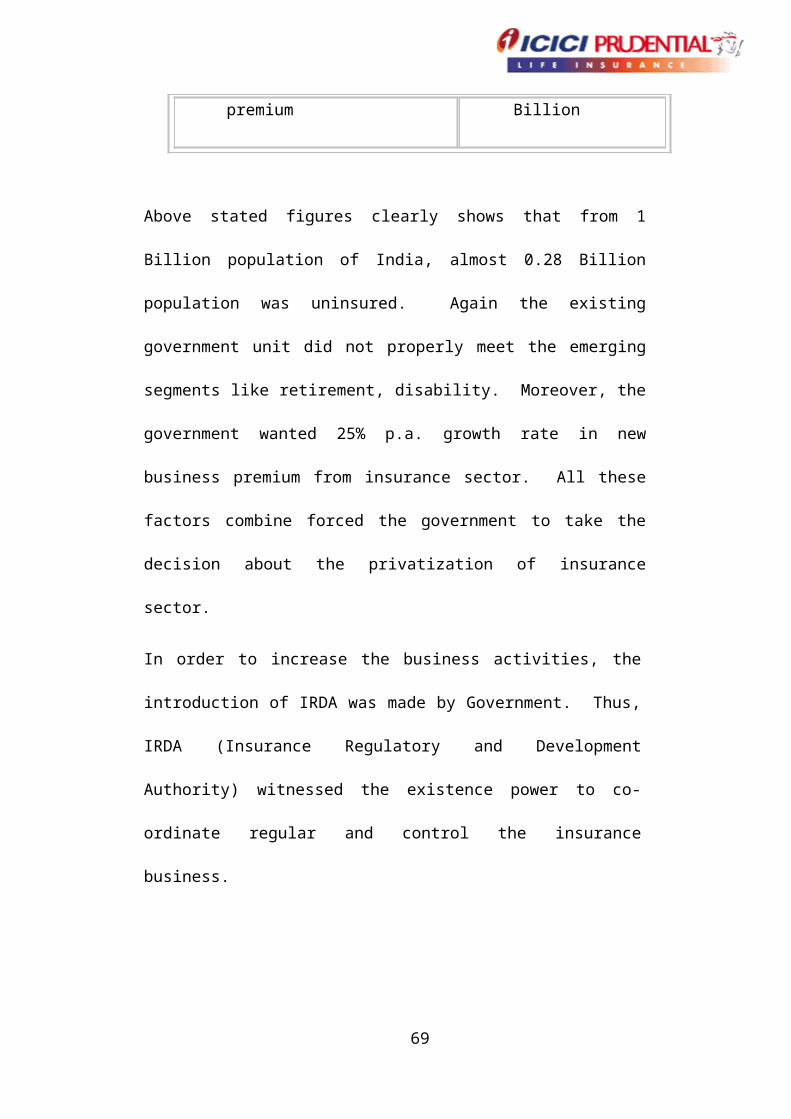

Business figure before the introduction of IRDA

Population 1.00 Billion

Insurable Population 0.36 Billion

No. Of insured individuals 0.08 Billion

Potential uninsured

individuals

0.28 Billion

New Business premium 0.66 Billion

Above stated figures clearly shows that from 1 Billion population of India,

almost 0.28 Billion population was uninsured. Again the existing government

unit did not properly meet the emerging segments like retirement, disability.

Moreover, the government wanted 25% p.a. growth rate in new business

premium from insurance sector. All these factors combine forced the

government to take the decision about the privatization of insurance sector.

In order to increase the business activities, the introduction of IRDA was

made by Government. Thus, IRDA (Insurance Regulatory and Development

Authority) witnessed the existence power to co-ordinate regular and control

the insurance business.

45

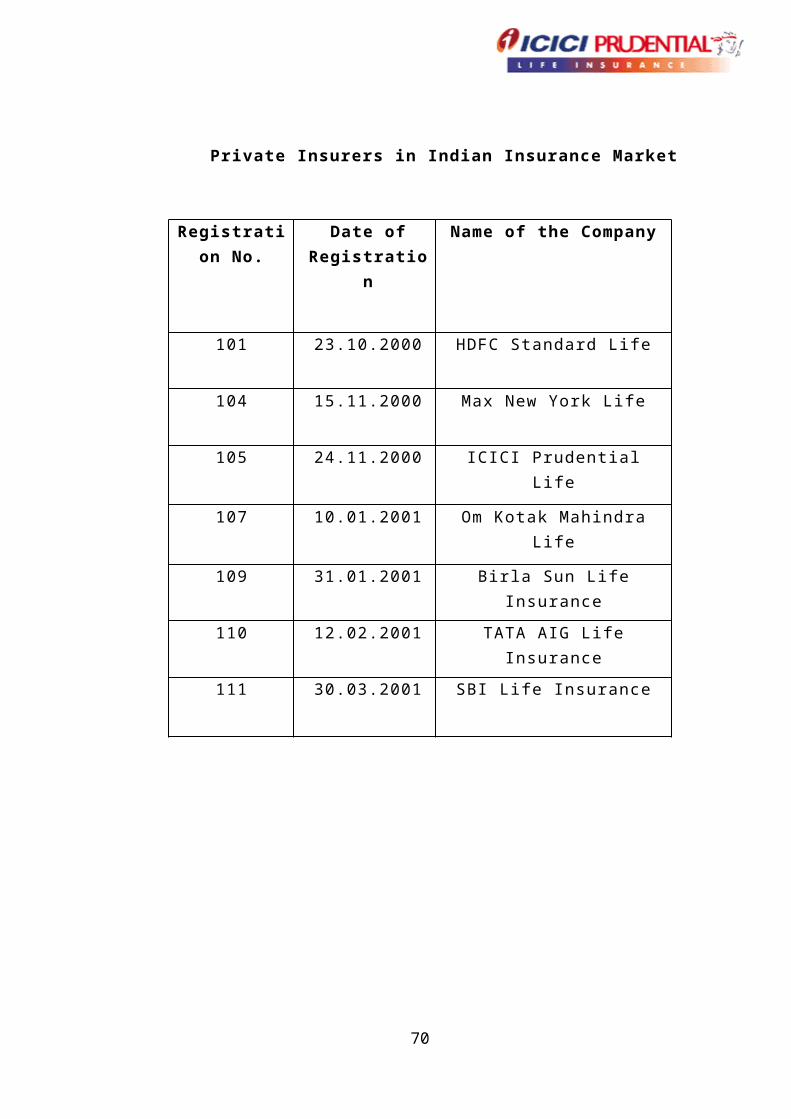

Private Insurers in Indian Insurance Market

Registration No.

Date of Registration

Name of the Company

101 23.10.2000 HDFC Standard Life

104 15.11.2000 Max New York Life

105 24.11.2000 ICICI Prudential Life

107 10.01.2001 Om Kotak Mahindra Life

109 31.01.2001 Birla Sun Life Insurance

110 12.02.2001 TATA AIG Life Insurance

111 30.03.2001 SBI Life Insurance

46

COMPANY PROFILE

47

COMPANY PROFILE

INTRODUCTION TO ICICI GROUP

ICICI BANK

ICICI Bank is India’s second-largest bank with total assets of about

Rs.112.024 crore and a network of about 450 branches and offices and about

1750 ATMs. ICICI Bank offers a wide range of banking products and

financial services to corporate and retail customer through a variety of

delivery channels and through its specialized subsidiaries and affiliates in the

areas of investment banking, life and non-life insurance, venture capital, asset

management and information technology. ICICI Bank’s equity shares are

listed in India on stock exchanges at

Chennai. Delhi, Kolkata and Vadodara, the Stock Exchange, Mumbai and the

National Stock Exchange of India Limited and its American Depositary

Receipts (ADRs) are listed on the New York Stock Exchange (NYSE).

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian

financial institution, and was its wholly owned subsidiary. ICICI’s

shareholding in ICICI Bank was reduced to 46% through a public offering of

shares in India in fiscal 1998, an equity offering in the form of ADRs listed on

the NYSE in fiscal 2000, ICICI Bank’s acquisition of Bank of Mathura

Limited in an all-stock amalgamation in fiscal 2001, and secondary market

sales by ICICI to institutional investors in fiscal 2001 and fiscal 2002. ICICI

48

was formed in 1955 at the initiative of the World Bank, the Government of

India and representatives of Indian industry. The principal objective was to

create a development financial institution for providing medium term and long

term project financing to Indian businesses. In the 1990s, ICICI transformed

its business from a development financial institution offering only project

finance to a diversified financial services group offering a wide variety of

products and services, both directly and through a number of subsidiaries and

affiliates like ICICI Bank, In 1999, ICICI become the first Indian company

and the first bank or financial institution from non-Japan Asia to be listed on

the NYSE.

After consideration of various corporate structuring alternatives in the context

of the emerging competitive scenario in the Indian banking industry, and the

move towards universal banking, the management of ICICI and ICICI Bank

formed the view that the merger of ICICI with ICICI Bank would be the

optimal strategic alternative for both entities, and would create the optimal

legal structure for the ICICI group’s universal banking strategy. The merger

would enhance value for ICICI shareholders through the merged entity’s

access to low-cost deposits, greater opportunities for earning fee-based

income and the ability to participate in the payment system and provide

transaction-banking services. The merger would enhance value for ICICI

Bank shareholders through a large capital base and scale of operations,

seamless access to ICICI’s strong corporate relationships built up over five

decades, entry into new business segments, higher market share in various

business segments, Particularly fee-based services, and access to the vast

49

talent pool of ICICI Bank approved the merger of ICICI and two of its

wholly-owned retail finance subsidiaries, ICICI Personal Financial Services

Limited and ICICI Capital Services Limited, With ICICI Bank.

Shareholders of ICICI and ICICI BANK approved the merger in January

2002, by the High Court of Gujarat at Jalandhar in March 2002, and by the

High Court of

Judicature at Mumbai and the Reserve Bank of India in April 2002.

Consequent to the merger, the ICICI group’s financing and banking

operations, both wholesale and retail, have been integrated in a single entity.

ICICI Bank is the only Indian company to be rated above the country rating

by the international rating agency moody “s and the only Indian company to

be awarded an investment grade international credit rating. The Bank enjoys

the highest AAA (or equivalent) rating from all Leading Indian rating

agencies.

Prudential P.L.C.

Established in 1848, today prudential plc is a leading international financial

services company with some 16 million customers, policyholders and unit

holders and some 20,000 employees worldwide. In the UK Prudential is a

leading life and pensions provider with around seven million customers.

M&G was acquired by Prudential in 1999 and is the Group’s UK and

European fund manager, responsible for managing over of 111 billion of

funds (as at December 2003). Launched by Prudential in 1998, Egg is an

50

innovative financial services company, with over three million customers,

with nearly six per cent of UK credit card balances. In Asia, Prudential is the

leading European life insurer with 23 life and fund management operations in

12 countries serving some five million customers. In the US, Prudential owns

Jackson National Life, a leading life insurance company, and has more than

1.5 millions policies and contracts in force.

Prudential has brought to market an integrated range of financial services

products that now includes life assurance, pensions, mutual funds, banking,

investment management and general insurance. In Asia, Prudential is UK”s

Largest life insurance company with a vast network of 22 life and mutual fund

operations in twelve countries – China, Hong Kong, India, Indonesia, Japan,

Korea, Malaysia, the Philippines, Singapore, Taiwan, Thailand and Vietnam.

Since 1923, Prudential has championed customer-centric products and

services, supported by over 60,000 staff and agents across the region.

Prudential plc’s strong mix of business around the world positions us well to

benefit form the growth in customer demand for asset accumulation and

income in retirement. Our international reach and diversity of earnings by

geographic region and product will continue to give us significant advantage.

Our commitment to the shareholders who own Prudential is to maximize the

value over time of their investment. We do this by investing for the long term

to develop and bring out the best in our people and our businesses to produce

51

superior products and services, our international peer group in terms of total

shareholder returns.

At Prudential our aim is lasting relationships with our customers and

policyholders, through products and services that offer value for money and

security. We also seek to enhance our Company’s reputation, built over 150

years, for integrity and for acting responsibly within society.

ICICI Prudential Life Insurance:

ICICI Prudential Life Insurance Company is a joint venture between ICICI

Bank, a premier financial powerhouse and Prudential Plc, a leading

international financial services group headquartered in the United Kingdom.

ICICI Prudential was amongst the first private sector insurance companies to

begin operations in December 2000 after receiving approval from insurance

Regulatory Development Authority (IRDA).

ICICI Prudential’ s equity base stands at Rs.6.75 billion with ICICI Bank and

Prudential plc holding 74% and 26% stake respectively. In the year ended

March 31,2004 the company had issued over 430,000 policies, for a total sum

assured of over Rs 8,000 crore and premium income in excess of Rs.980

crore. The company has a network of about 30,000 advisors; as well as 12

banc assurance tie-ups. Today the company is the number one private life

insurer in the country.

Management

52

K. V. Kamath

Managing Director and Chief Executive Officer

53

Lalita Gupte

Joint Managing Director Kalpana Morparia

Joint Managing Director

Chanda Kochhar

Deputy Managing Director Nachiket Mor

Deputy Managing Director

Board Committees

Audit Committee Board Governance &

Remuneration Committee

Mr. Sridar Iyengar

Mr. Narendra Murkumbi

Mr. M. K. Sharma

Mr. N. Vaghul

Mr. Anupam Puri

Mr. M. K. Sharma

Mr. P. M. Sinha

Prof. Marti G. Subrahmanyam

Customer Service

Committee Credit Committee

N. Vaghul

Narendra Murkumbi

M.K. Sharma

P.M. Sinha

K. V. Kamath

Mr. N. Vaghul

Mr. Narendra Murkumbi

Mr. M .K. Sharma

Mr. P. M. Sinha

Mr. K. V. Kamath

Fraud Monitoring

CommitteeRisk Committee

Mr. M. K. Sharma

Mr. Narendra Murkumbi

Mr. N. Vaghul

Mr. Sridar Iyengar

Prof. Marti G. Subrahmanyam

54

Mr. K. V. Kamath

Ms. Kalpana Morparia

Ms. Chanda D. Kochhar

Mr. V. Prem Watsa

Mr. K. V. Kamath

Share Transfer &

Shareholders'/

Investors' Grievance

Committee

Asset-Liability Management

Committee

Mr. M. K. Sharma

Mr. Narendra Murkumbi

Ms. Kalpana Morparia

Ms. Chanda D. Kochhar

Ms. Lalita D. Gupte

Ms. Kalpana Morparia

Ms. Chanda D. Kochhar

Dr. Nachiket Mor

Committee of Directors

Mr. K. V. Kamath

Ms. Lalita D. Gupte

Ms. Kalpana Morparia

Ms. Chanda D. Kochhar

Dr. Nachiket Mor

55

PRODUCTS & SERVICES

56

PRODUCTS & SERVICES

Insurance solution for individuals…..

ICICI Prudential Life Insurance offers a range of innovative,

customer-centric products that meet the needs of customers at every

life stage. Its 17 products cab is enhanced with up to 6 riders, to create

a customized solution for each policyholder.

Savings Solutions…..

Secure Plus is a transparent and feature-packed savings plan that offers 3

levels of protection. Cash Plus is a transparent, feature-packed savings plan

that offers 3 levels of protection as well as liquidity options. Save n Protect is

a traditional endowment savings plan that offers life protection along with

adequate returns. Cash Back is an anticipated endowment policy ideal for

meeting milestone expenses like a child’s marriage, expenses for a child’s

higher education or purchase of an asset.

57

Protection Solutions…….

LifeGuard is a protection plan, which offers life cover at very low

cost. It is available in 3 coupons – level term assurance, level term

assurance with return or premium and single premium.

Child Solutions…….

Smart kid child plans provide guaranteed educational benefits to a

child along with life insurance cover for the parent who purchases the

policy. The policy is designed to provide money at important

milestones in the child’s life. SmartKid child planed are also available

with in unit-linked form – both single premium and regular premium.

Market-linked Solutions

LifeLink is a single premium Market Linked Insurance Plan, which

combines life insurance cover with the opportunity to stay, invested in

58

the stock market. Life Time offers customers the flexibility and control

to customize the policy to meet the changing needs at different life

stages. It offers 3 investment options –Growth Plan, Income plan and

Balance plan.

Retirement Solutions……

Forever Life is a retirement products targeted at individual in there

thirties. Secure Plus Pension is a flexible pension plan that allows one

to select between 3 levels of cover.

Market-linked retirement products

Life Time Pension is a regular premium market-linked pension plan.

Life Link Pension is a single premium market linked pension plan.

ICICI Prudential also launched “Salaam Zindagi”, a social sector

group insurance policy targeted at the economically underprivileged

sections of the society.

59

Group Insurance Solutions……

ICICI Prudential also offers Group Insurance Solutions for companies

seeking to enhance benefits to their employees.

Group Gratuity Plan……

ICICI Pru”s group gratuity plan helps employers fund their statutory

gratuity obligation in a scientific manner. The plan can also customize

to structure schemes that can provide benefits beyond the statutory

obligations.

Group Superannuation Plan

ICICI Bank offers flexible defined contribution superannuation

scheme to provide a retirement kitty for each member of the group.

Employees have the option of choosing from various annuity options

or opting for partial commutation of the annuity at the time of

retirement.

Group Term Plan

60

Group Term Plan……

ICICI Pru”s flexible group term solution helps provides affordable

cover to members of group. The cover could be uniform or based on

designation/rank or a multiple of salary. The benefit under the policy

is paid to the beneficiary nominated by the member on his/her death.

Flexible Rider Options

ICICI Pru Life offers flexible riders, which can be added to the basic policy at

marginal cost, depending on the specific of the customer.

Accident & disability benefit: If death occurs as the result of an accident

during the term of the policy, the beneficiary receives an additional amount

equal to the sum assured under the policy. If the death occurs while traveling

in an authorized mass transport vehicle, the beneficiary will be entitled to

twice the sum assured as additional benefit.

Accident benefit: This rider option pays the sum assured the rider on death

due to accidents.

61

Critical Illness Benefit: protects the insured against financial loss in the

event of 9 specified critical illnesses. Benefits are payable to the insured for

medical prior to death.

Major Surgical Assistance Benefits: provides financial support in the event

of medical emergencies, ensuring that benefits are payable to the life assured

for medical expenses Incurred for surgical procedures. Cove is offered against

43 different surgical procedures.

Income Benefit: This rider pays the 10% of the sum assured to the nominee

every year, till maturity, in the event of the death of the life assured. It is

available on SmartKid, SecurePlus and Cashplus.

Waiver of Premium: In Case of total and permanent due to an accident, the

premiums are waived till maturity. This rider is available with SecurePlus and

CashPlus.

62

PART-II

63

INTRODUCTION OF TOPIC

64

INTRODUCTION OF TOPIC

Customer Satisfaction

What is customer satisfaction?

Customer satisfaction refers to how satisfied customers are with the products or

services they receive from a particular agency. The level of satisfaction is determined

not only by the quality and type of customer experience but also by the customer’s

expectations.

A customer may be defined as someone who:

has a direct relationship with, or is directly affected by your agency and

receives or relies on one or more of your agency’s services or products.

Customers in human services are commonly referred to as service users, consumers or

clients. They can be individuals or groups.

An organisation with a strong customer service culture places the customer at the

centre of service design, planning and service delivery. Customer centric

organisations will:

determine the customers expectations when they plan

listen to the customer as they design

focus on the delivery of customer service activities

65

Value customer feedback when they measure performance.

Why is it important?

There are a number of reasons why customer satisfaction is important in Insurance

Sector:

Meeting the needs of the customer is the underlying rationale for the existence

of community service organizations. Customers have a right to quality

services that deliver outcomes.

Organizations that strive beyond minimum standards and exceed the

expectations of their customers are likely to be leaders in their sector.

Customers are recognized as key partners in shaping service development and

assessing quality of service delivery.

The process for measuring customer satisfaction and obtaining feedback on

organizational performance are valuable tools for quality and continuous service

improvement.

66

RESEARCH METHODOLOGY

67

RESEARCH METHODOLOGY

Statement Of Problem:

The research is carried on in a proper planned and systematic manner.

The research was particularly a telephonic research. We have to sell products

to list of people which include their names and contact numbers given by

ICICI.

During the telephonic we have to sell different products by explaining the

benefits of a particular product, but. The minimum amount for selling a policy

to a customer is equal to or more then Rs. 12000 only.

Age limit for selling a product/policies was 1 month to 60 yrs – this mean that

a policy can be sold to person between the age of 1 month to 60 yrs and not

anything exceeding or below it.

Research Design:

The research design of this project is exploratory. Though each research study has its

own specific purpose but the research design of this project on ICICI is exploratory in

nature as the objective is the development of the hypothesis rather than their testing.

METHODOLOGY

Every project work is based on certain methodology, which is a way to systematically

solve the problem or attain its objectives. It is a very important guideline and lead to

completion of any project work through observation, data collection and data analysis.

68

According to Clifford Woody,

“Research Methodology comprises of defining & redefining problems, collecting,

organizing &evaluating data, making deductions &researching to conclusions.”

Accordingly, the methodology used in the project is as follows: -

Defining the objectives of the study

Framing of questionnaire keeping objectives in mind (considering the objectives)

Feedback from the employees

Analysis of feedback

Conclusion, findings and suggestions.

Sampling Technique Used:

This research has used convenience sampling technique.

1) Convenience sampling technique : Convenience sampling is used in exploratory

research where the researcher is interested in getting an inexpensive approximation of

the truth. As the name implies, the sample is selected because they are convenient

Selection of Sample Size:

For the survey, a sample size of 50 has been taken into consideration.

Sources of Data Collection:

Research will be based on two sources:

1. Primary data

2. Secondary data

69

1) PRIMARY DATA:

Questionnaire: Primary data was collected by preparing questionnaire for customers.

The questionnaire was filled through telephonic research.

2) SECONDARY DATA:

Secondary data will consist of different literatures like books which are published,

articles, internet , the company manuals and websites of company-

www.iciciprulife.com.

In order to reach relevant conclusion, research work needed to be designed in a proper

way.

This research methodology also includes:-

Familiarization with the concept of insurance and its various terms.

Thorough study of the information collected.

Conclusions based on findings.

Statistical Tools Used

The main statistical tools used for the collection and analyses of data in this project

are:

Questionnaire

Pie Charts

Bar Diagrams

70

71

Limitations of study

Due to the following unavoidable and uncontrollable factors the factors,the result

might not be accurate. Some of the problems faced while conducting the survey are as

follows:-

Time and cost constraints were also there.

Chances of some biasness could not be eliminated.

A Samples size of fifty has been use due to time limitations.

A majority of respondents show lack of cooperation and are biased towards

their own opinions.

72

OBJECTIVE

73

OBJECTIVE OF THE STUDY

The main objective of this study is to carry on brief study on “Customer satisfaction

survey on insurance products of ICICI PRUDENTIAL” through this I am able to

get the different Life Insurance Policies and their products.

Other objectives of this project are as follows:

To identify the insurance needs of the Indian population with respect to their

emotional, physical and financial conditions.

Comparative study of various insurance players in the market

To study the varied reasons of availing life insurance plans

74

DATA ANALYSIS AND

INTERPRETATION

75

DATA ANALYSIS AND INTERPRETATION

Q1. Are you currently insured?

Particulars No. of Respondents Percentage

Yes 31 62%No 19 38%Total 50 100%

No. of Respondents

31

19

YesNo

76

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 62% of the respondents are already insured.

b) 38% of the respondents are not insured.

Q2. Are you satisfied with your current insurer?

Particulars No. of Respondents Percentage

Yes 41 82%No 9 18%Total 50 100%

No. of Respondents

41

9

YesNo

77

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 82% of the respondents are satisfied.

b) 18% of the respondents are not satisfied.

Q3. Which one is your favored insurance company?

Particulars No. of Respondents Percentage

LIC 24 48%ICICI 7 14%HDFC 5 10%Birla Sun Life 4 8%Bajaj Allianz 4 8%Others 6 12%Total 50 100%

Q4. Are you interested in the products offered by ICICI Prudential ?

78

0

0.1

0.2

0.3

0.4

0.5

0.6

LIC ICICI HDFC Birla Sun BajajAllianz

Others

Insurance companies

Shar

e in

%

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 48% of the respondents likes LIC.

b) 14% of the respondents likes ICICI.

c) 10% of the respondents likes HDFC.

d) 8% of the respondents likes Birla Sun Life.

e) 8% of the respondents likes Bajaj Allianz.

f) 12% of the respondents likes other companies.

Q4. Are you interested in the products offered by ICICI Prudential ?

Particulars No. of Respondents Percentage

Yes 30 60%No 12 24%Can’t Say 8 16%Total 50 100%

No. of Respondents

3012

8

YesNoCan't Say

79

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 60% of the respondents are attracted towards ICICI products.

b) 24% of the respondents are not attracted towards ICICI

products.

c) 16% of the respondents Can’t Say about it.

Q5. What is your main concern while taking an insurance policy ?

Particulars No. of Respondents Percentage

Tax Benefit 20 40%Security 16 32%Investments/Savings 14 28%Total 50 100%

2016 14

0

5

10

15

20

25

Tax B

enefi

t

Security

Investm

ent/S

aving

s

No. o

f Res

pond

ents

Series1

80

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 40% of the respondents are concerned about Tax Benefit.

b) 32% of the respondents are concerned about their Security.

c) 28% of the respondents are concerned about

Investment/Savings.

Q6. Does this policy satisfy your financial needs? (Please rate on the

scale of 1 to 5 with 1 being least satisfied)

Rating No. of Respondents Percentage

1 9 18%2 9 18%3 8 16%4 10 20%5 14 28%Total 50 100%

81

1

2

3

4

512345

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 18% of the respondents are Highly unsatisfied.

b) 18% of the respondents are Unsatisfied.

c) 16% of the respondents are Moderate.

d) 20% of the respondents are Satisfied.

e) 28% of the respondents are Highly satisfied.

Q7. Please express your opinion for the premiums paid for the above policy?

Particulars No. of Respondents Percentage

Very High 14 28%High 11 22%Moderate 13 26%Low 8 16%Very Low 4 8%Total 50 100%

82

ANALYSIS:

From the survey it was found that amongst 50 respondents

a) 28% of the respondents think that Premium is Very High.

b) 22% of the respondents think that Premium is High.

c) 23% of the respondents think that Premium is Moderate.

d) 15% of the respondents think that Premium is Low.

e) 12% of the respondents think that Premium is Very Low.

Q8. How do you come to know about this policy?

Particulars No. of Respondents Percentage

Advertisements 10 20%Friends and Relatives 12 24%Direct Selling Agents 21 42%Others 7 14%Total 50 100%

83