ICDP Dealer groups ‐driving digital performance · ICDP Dealer groups ‐driving digital...

29

ICDP Dealer groups ‐ driving digital performance Webinar, 26 th January 2016 1 ICDP Project Office: Central Boulevard, Blythe Valley Business Park, Solihull, B90 8AG U.K. Tel.: + 44 (0) 1564 711224 E‐mail: [email protected] Web: www.icdp.net Limited company registered in the UK, no. 6262484

Transcript of ICDP Dealer groups ‐driving digital performance · ICDP Dealer groups ‐driving digital...

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

1

ICDPProject Office: Central Boulevard, Blythe Valley Business Park, Solihull, B90 8AG U.K.Tel.: + 44 (0) 1564 711224 E‐mail: [email protected] Web: www.icdp.net

Limited company registered in the UK, no. 6262484

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

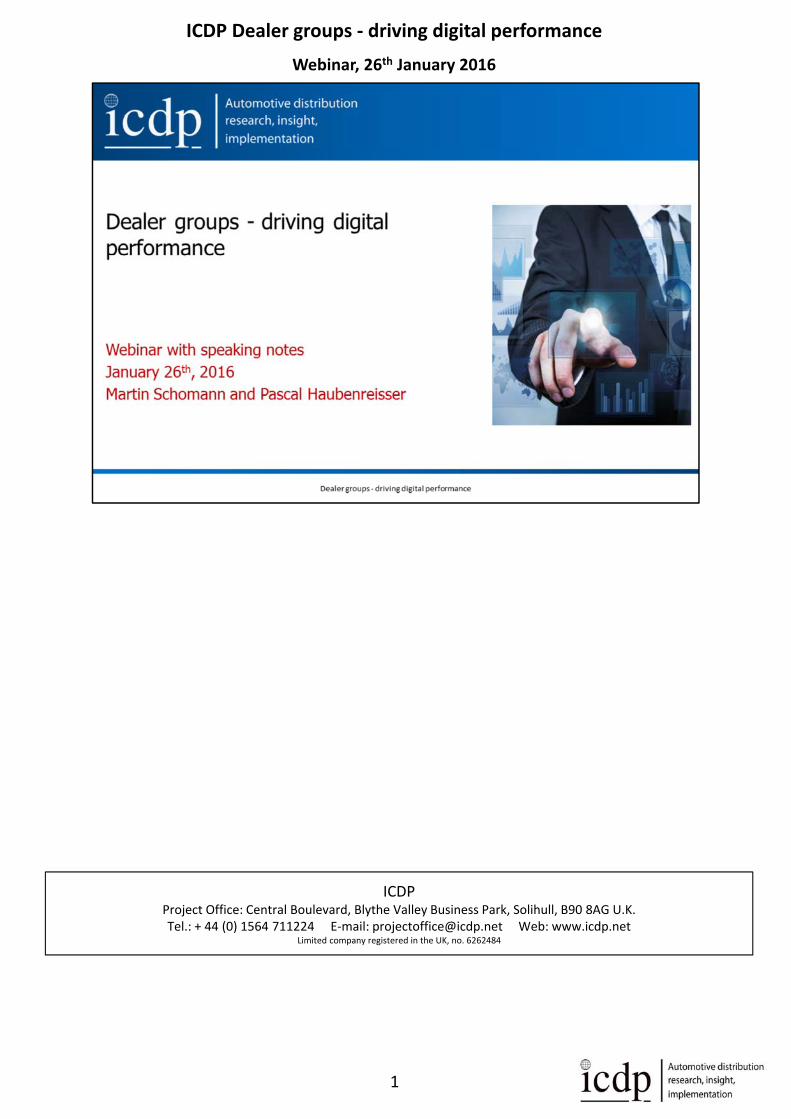

So let‘s start and have a look at our objectives for today. We screen the online research process of new car buyers and reveal the most useful website categories, by visits, from a customer’s point of view. Our focus is then specifically on dealer websites, where different types with different structures exist. This has also an influence on responsibilities and cost management towards the OEM, as well as on the overall performance. Social media potential is also worth to be analysed from our point of view, so we had a closer look at dealer profiles within Facebook and YouTube. We will finally conclude that OEM support, better collaboration, but also individual engagement is necessary in order to provide a more holistic digital approach.

2

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

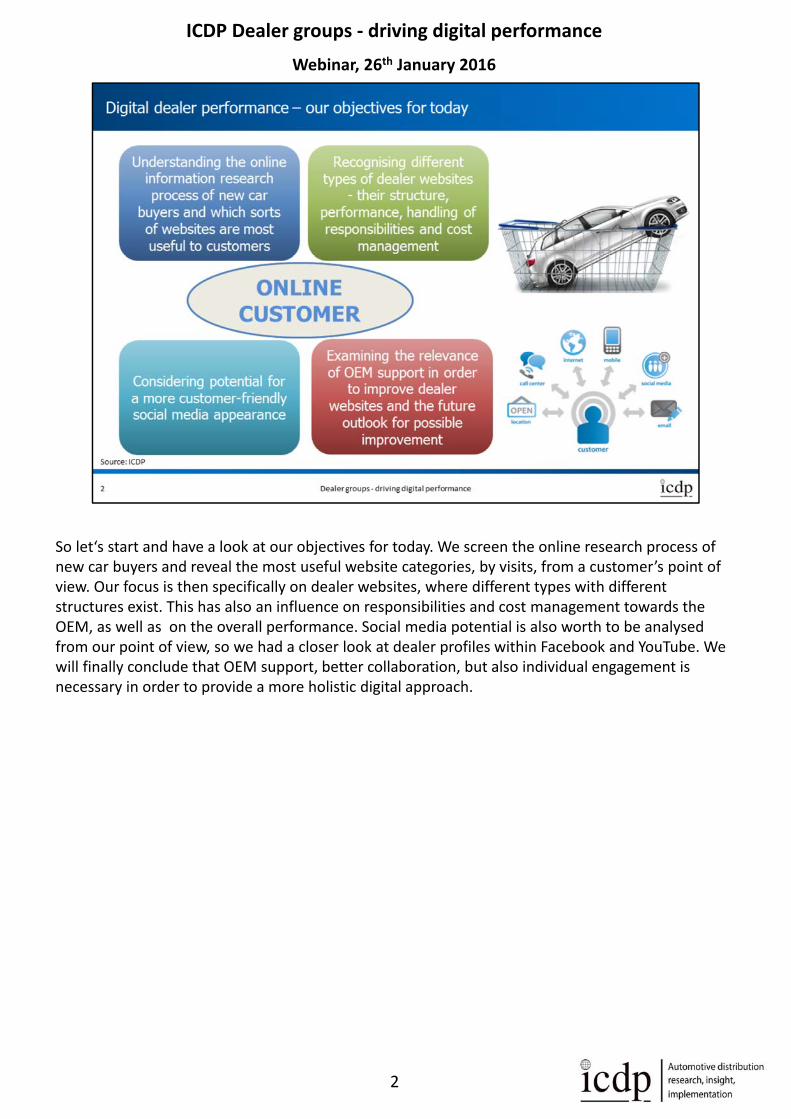

The webinar is split into 5 short sections ‐ At first we’re looking at customer behaviour and needs during the online research‐ In section 2 we will talk about roles and responsibilities of dealer website management‐ Then we surveyed the question, if dealers can satisfy customers digital service expectations‐ The fourth section is a social media appearance analysis of dealer Facebook and YouTube profiles‐ And finally, we will show our conclusion, including a recommendation

3

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

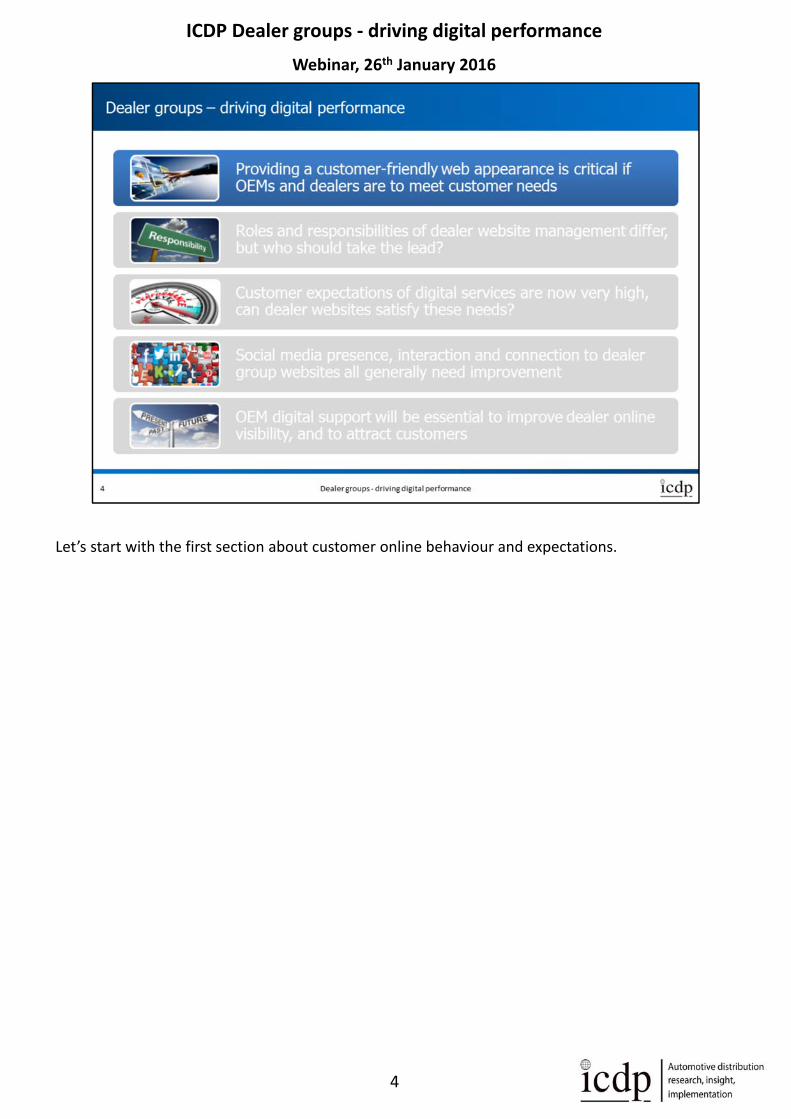

Let’s start with the first section about customer online behaviour and expectations.

4

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

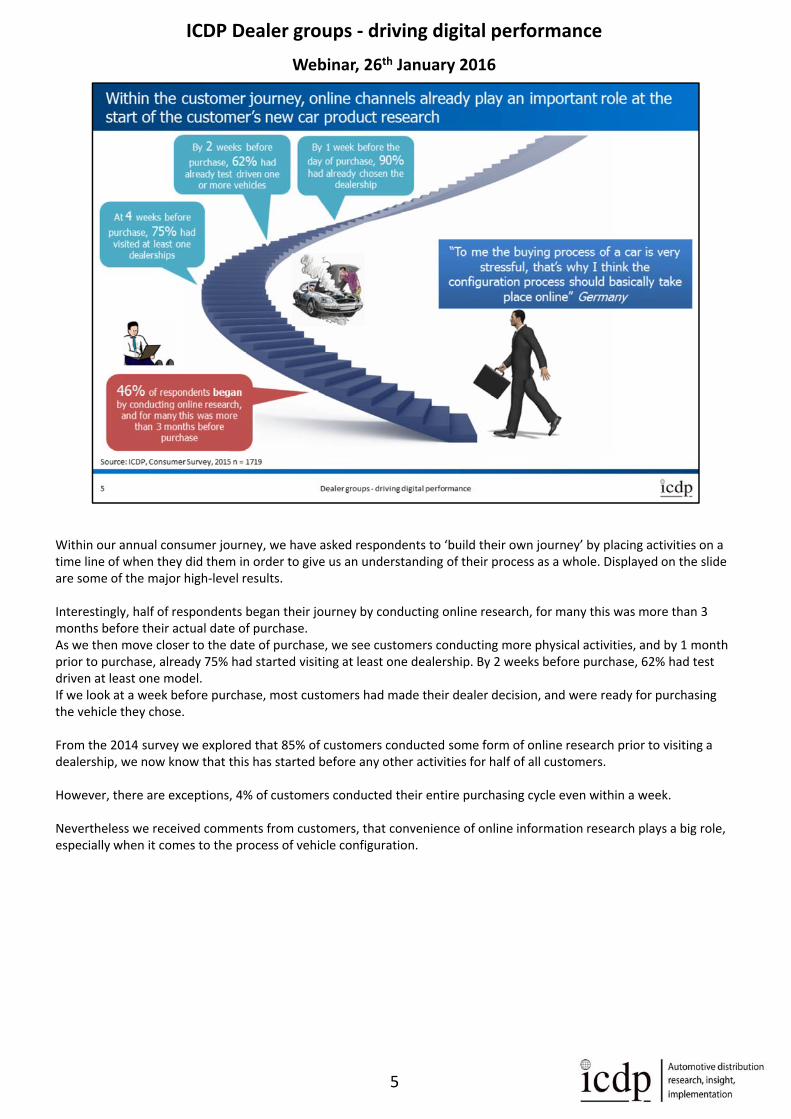

Within our annual consumer journey, we have asked respondents to ‘build their own journey’ by placing activities on a time line of when they did them in order to give us an understanding of their process as a whole. Displayed on the slide are some of the major high‐level results.

Interestingly, half of respondents began their journey by conducting online research, for many this was more than 3 months before their actual date of purchase.As we then move closer to the date of purchase, we see customers conducting more physical activities, and by 1 month prior to purchase, already 75% had started visiting at least one dealership. By 2 weeks before purchase, 62% had test driven at least one model.If we look at a week before purchase, most customers had made their dealer decision, and were ready for purchasing the vehicle they chose.

From the 2014 survey we explored that 85% of customers conducted some form of online research prior to visiting a dealership, we now know that this has started before any other activities for half of all customers.

However, there are exceptions, 4% of customers conducted their entire purchasing cycle even within a week.

Nevertheless we received comments from customers, that convenience of online information research plays a big role, especially when it comes to the process of vehicle configuration.

5

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

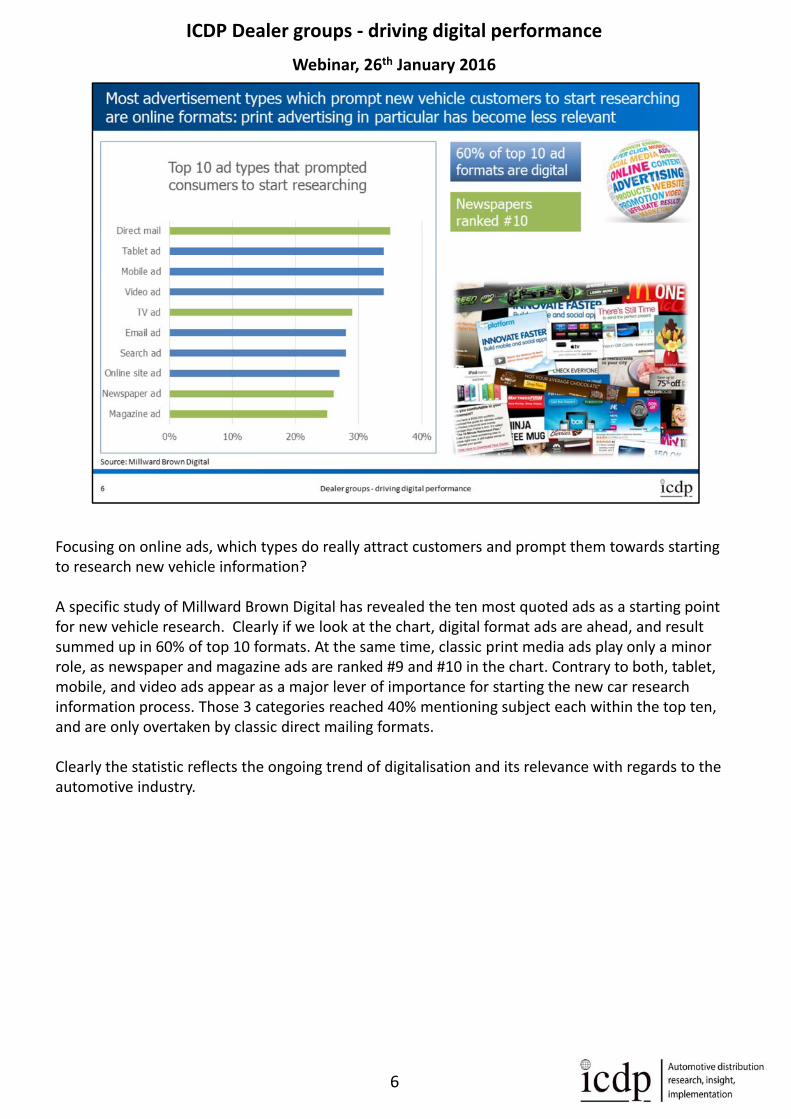

Focusing on online ads, which types do really attract customers and prompt them towards starting to research new vehicle information?

A specific study of Millward Brown Digital has revealed the ten most quoted ads as a starting point for new vehicle research. Clearly if we look at the chart, digital format ads are ahead, and result summed up in 60% of top 10 formats. At the same time, classic print media ads play only a minor role, as newspaper and magazine ads are ranked #9 and #10 in the chart. Contrary to both, tablet, mobile, and video ads appear as a major lever of importance for starting the new car research information process. Those 3 categories reached 40% mentioning subject each within the top ten, and are only overtaken by classic direct mailing formats.

Clearly the statistic reflects the ongoing trend of digitalisation and its relevance with regards to the automotive industry.

6

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

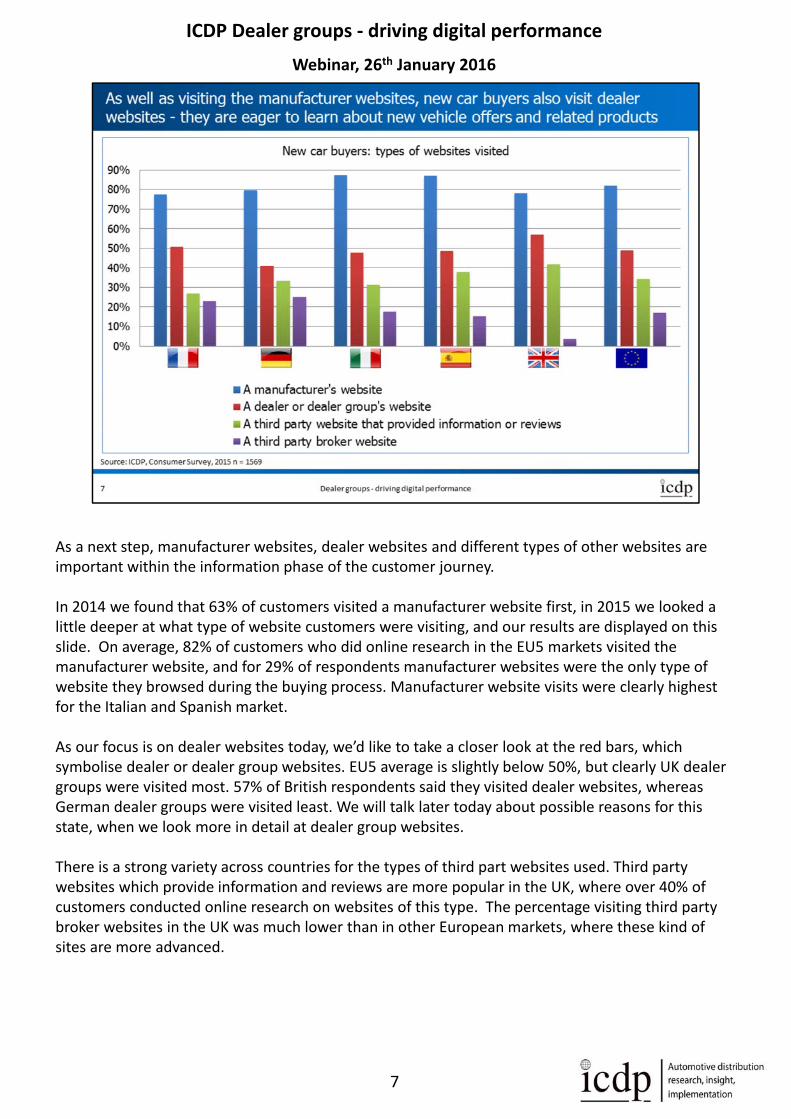

As a next step, manufacturer websites, dealer websites and different types of other websites are important within the information phase of the customer journey.

In 2014 we found that 63% of customers visited a manufacturer website first, in 2015 we looked a little deeper at what type of website customers were visiting, and our results are displayed on this slide. On average, 82% of customers who did online research in the EU5 markets visited the manufacturer website, and for 29% of respondents manufacturer websites were the only type of website they browsed during the buying process. Manufacturer website visits were clearly highest for the Italian and Spanish market.

As our focus is on dealer websites today, we’d like to take a closer look at the red bars, which symbolise dealer or dealer group websites. EU5 average is slightly below 50%, but clearly UK dealer groups were visited most. 57% of British respondents said they visited dealer websites, whereas German dealer groups were visited least. We will talk later today about possible reasons for this state, when we look more in detail at dealer group websites.

There is a strong variety across countries for the types of third part websites used. Third party websites which provide information and reviews are more popular in the UK, where over 40% of customers conducted online research on websites of this type. The percentage visiting third party broker websites in the UK was much lower than in other European markets, where these kind of sites are more advanced.

7

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

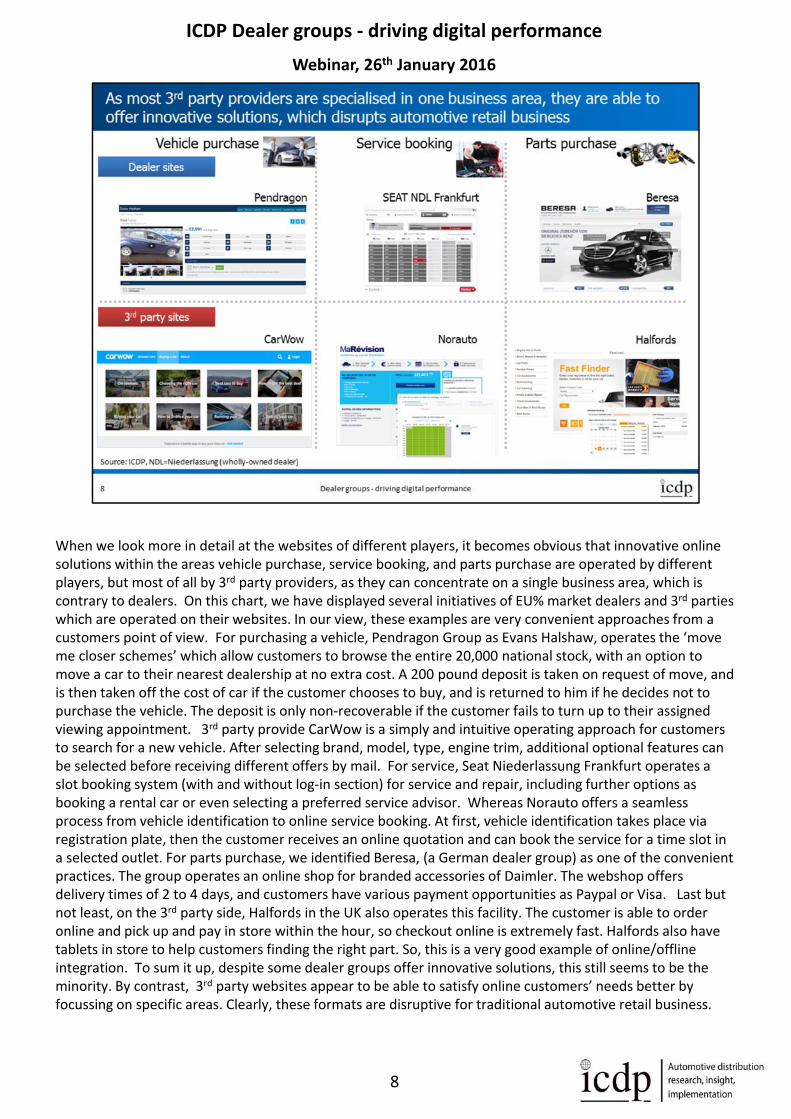

When we look more in detail at the websites of different players, it becomes obvious that innovative online solutions within the areas vehicle purchase, service booking, and parts purchase are operated by different players, but most of all by 3rd party providers, as they can concentrate on a single business area, which is contrary to dealers. On this chart, we have displayed several initiatives of EU% market dealers and 3rd parties which are operated on their websites. In our view, these examples are very convenient approaches from a customers point of view. For purchasing a vehicle, Pendragon Group as Evans Halshaw, operates the ‘move me closer schemes’ which allow customers to browse the entire 20,000 national stock, with an option to move a car to their nearest dealership at no extra cost. A 200 pound deposit is taken on request of move, and is then taken off the cost of car if the customer chooses to buy, and is returned to him if he decides not to purchase the vehicle. The deposit is only non‐recoverable if the customer fails to turn up to their assigned viewing appointment. 3rd party provide CarWow is a simply and intuitive operating approach for customers to search for a new vehicle. After selecting brand, model, type, engine trim, additional optional features can be selected before receiving different offers by mail. For service, Seat Niederlassung Frankfurt operates a slot booking system (with and without log‐in section) for service and repair, including further options as booking a rental car or even selecting a preferred service advisor. Whereas Norauto offers a seamless process from vehicle identification to online service booking. At first, vehicle identification takes place via registration plate, then the customer receives an online quotation and can book the service for a time slot in a selected outlet. For parts purchase, we identified Beresa, (a German dealer group) as one of the convenient practices. The group operates an online shop for branded accessories of Daimler. The webshop offers delivery times of 2 to 4 days, and customers have various payment opportunities as Paypal or Visa. Last but not least, on the 3rd party side, Halfords in the UK also operates this facility. The customer is able to order online and pick up and pay in store within the hour, so checkout online is extremely fast. Halfords also have tablets in store to help customers finding the right part. So, this is a very good example of online/offline integration. To sum it up, despite some dealer groups offer innovative solutions, this still seems to be the minority. By contrast, 3rd party websites appear to be able to satisfy online customers’ needs better by focussing on specific areas. Clearly, these formats are disruptive for traditional automotive retail business.

8

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

Within the next section we will talk about roles and responsibility for dealer websites.

9

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

Dealer websites are operated very differently depending on brand standards and on dealer groups strategy to have an individual online appearance. But also manufacturer standards differ in terms of efficiency. OEM are providing standardised websites, by offering a frontend related to the corporate design. But some manufacturers offer individual domains like ford.birmingham.co.uk and others provide a central domain audi‐partner.de. In terms of Search engine optimisation this results into low traffic on the individual domains, which is not beneficial for the ranking and on the other hand this result into duplicated content. Google rate websites according to the importance of the website compared to others and ranks them within their results. When there are 700 individual domains that deliver the same content, the importance of the individual website gets down‐ranked. Only with a lot of money spend on advertising, the websites appears on top of the google results. In terms of central domains like Audi, the traffic gets bundled. The whole traffic at a dealer website lands on a sub‐category for the outlet on the central domain. This leads to high traffic on the single domain and an up‐ranking within the google results as google interprets the high traffic as a high importance of the website. Own websites with individual domain are in control of the dealer group. Typically high traffic is generated on the group website and distributed to the outlet website. Indeed the dealer group has a more personalised presence, but also much more efforts to deliver the needed content and traffic, which results in potentially higher costs. For these type of websites an efficient search engine advertising requires also a close coordination with the OEM/NSC as both advertise within the same channel, the risk is that both booking the same keywords simultaneous that could cause into unnecessary expense. To avoid this, regular communications about current advertising campaigns have to be done.

10

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

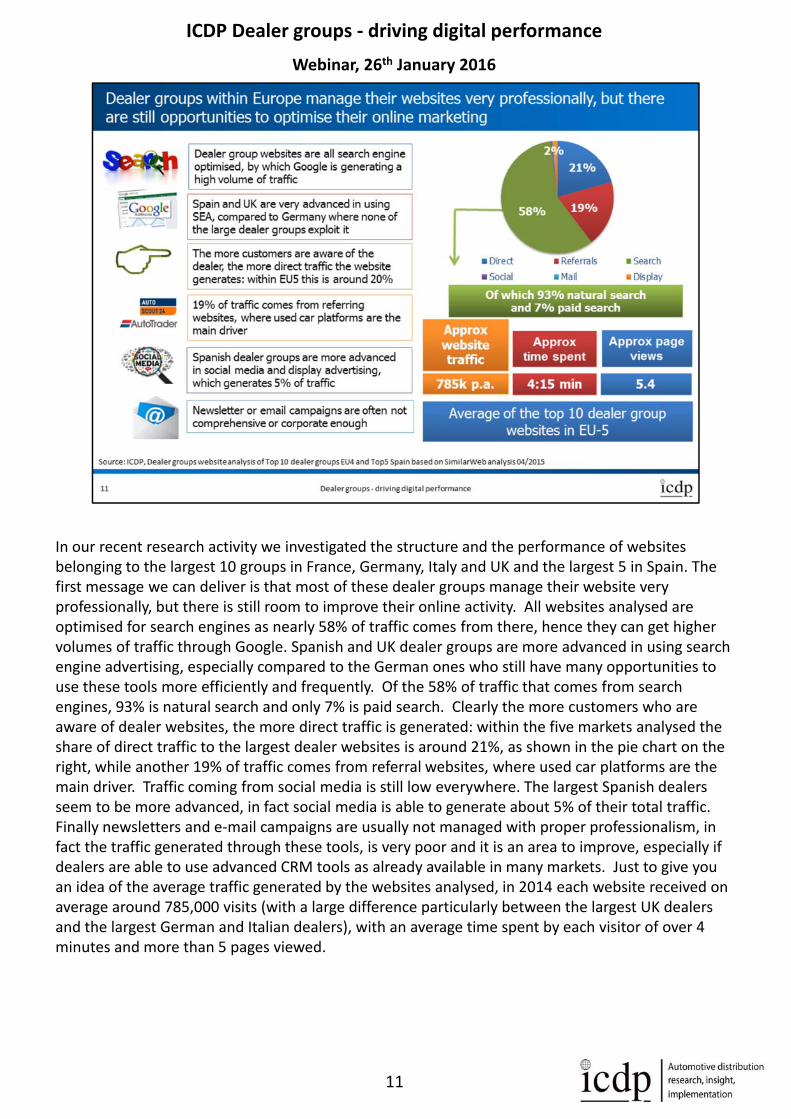

In our recent research activity we investigated the structure and the performance of websites belonging to the largest 10 groups in France, Germany, Italy and UK and the largest 5 in Spain. The first message we can deliver is that most of these dealer groups manage their website very professionally, but there is still room to improve their online activity. All websites analysed are optimised for search engines as nearly 58% of traffic comes from there, hence they can get higher volumes of traffic through Google. Spanish and UK dealer groups are more advanced in using search engine advertising, especially compared to the German ones who still have many opportunities to use these tools more efficiently and frequently. Of the 58% of traffic that comes from search engines, 93% is natural search and only 7% is paid search. Clearly the more customers who are aware of dealer websites, the more direct traffic is generated: within the five markets analysed the share of direct traffic to the largest dealer websites is around 21%, as shown in the pie chart on the right, while another 19% of traffic comes from referral websites, where used car platforms are the main driver. Traffic coming from social media is still low everywhere. The largest Spanish dealers seem to be more advanced, in fact social media is able to generate about 5% of their total traffic. Finally newsletters and e‐mail campaigns are usually not managed with proper professionalism, in fact the traffic generated through these tools, is very poor and it is an area to improve, especially if dealers are able to use advanced CRM tools as already available in many markets. Just to give you an idea of the average traffic generated by the websites analysed, in 2014 each website received on average around 785,000 visits (with a large difference particularly between the largest UK dealers and the largest German and Italian dealers), with an average time spent by each visitor of over 4 minutes and more than 5 pages viewed.

11

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

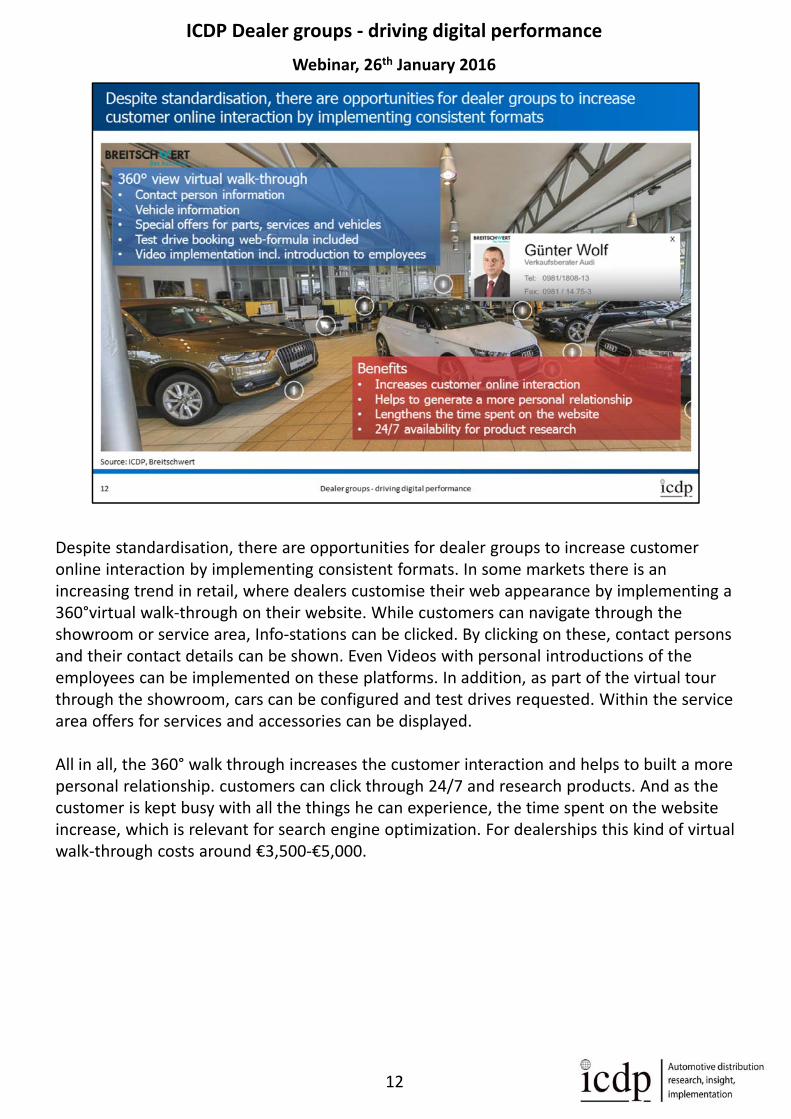

Despite standardisation, there are opportunities for dealer groups to increase customer online interaction by implementing consistent formats. In some markets there is an increasing trend in retail, where dealers customise their web appearance by implementing a 360°virtual walk‐through on their website. While customers can navigate through the showroom or service area, Info‐stations can be clicked. By clicking on these, contact persons and their contact details can be shown. Even Videos with personal introductions of the employees can be implemented on these platforms. In addition, as part of the virtual tour through the showroom, cars can be configured and test drives requested. Within the service area offers for services and accessories can be displayed.

All in all, the 360° walk through increases the customer interaction and helps to built a more personal relationship. customers can click through 24/7 and research products. And as the customer is kept busy with all the things he can experience, the time spent on the website increase, which is relevant for search engine optimization. For dealerships this kind of virtual walk‐through costs around €3,500‐€5,000.

12

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

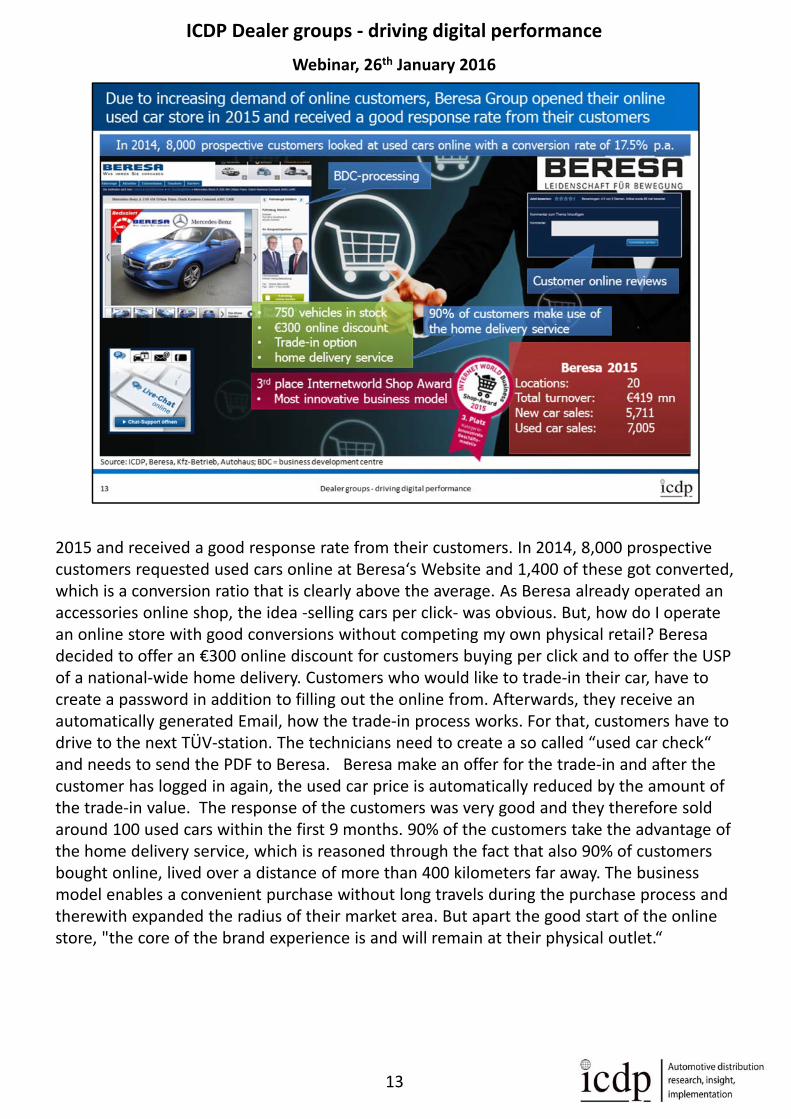

2015 and received a good response rate from their customers. In 2014, 8,000 prospective customers requested used cars online at Beresa‘s Website and 1,400 of these got converted, which is a conversion ratio that is clearly above the average. As Beresa already operated an accessories online shop, the idea ‐selling cars per click‐ was obvious. But, how do I operate an online store with good conversions without competing my own physical retail? Beresadecided to offer an €300 online discount for customers buying per click and to offer the USP of a national‐wide home delivery. Customers who would like to trade‐in their car, have to create a password in addition to filling out the online from. Afterwards, they receive an automatically generated Email, how the trade‐in process works. For that, customers have to drive to the next TÜV‐station. The technicians need to create a so called “used car check“ and needs to send the PDF to Beresa. Beresa make an offer for the trade‐in and after the customer has logged in again, the used car price is automatically reduced by the amount of the trade‐in value. The response of the customers was very good and they therefore sold around 100 used cars within the first 9 months. 90% of the customers take the advantage of the home delivery service, which is reasoned through the fact that also 90% of customers bought online, lived over a distance of more than 400 kilometers far away. The business model enables a convenient purchase without long travels during the purchase process and therewith expanded the radius of their market area. But apart the good start of the online store, "the core of the brand experience is and will remain at their physical outlet.“

13

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

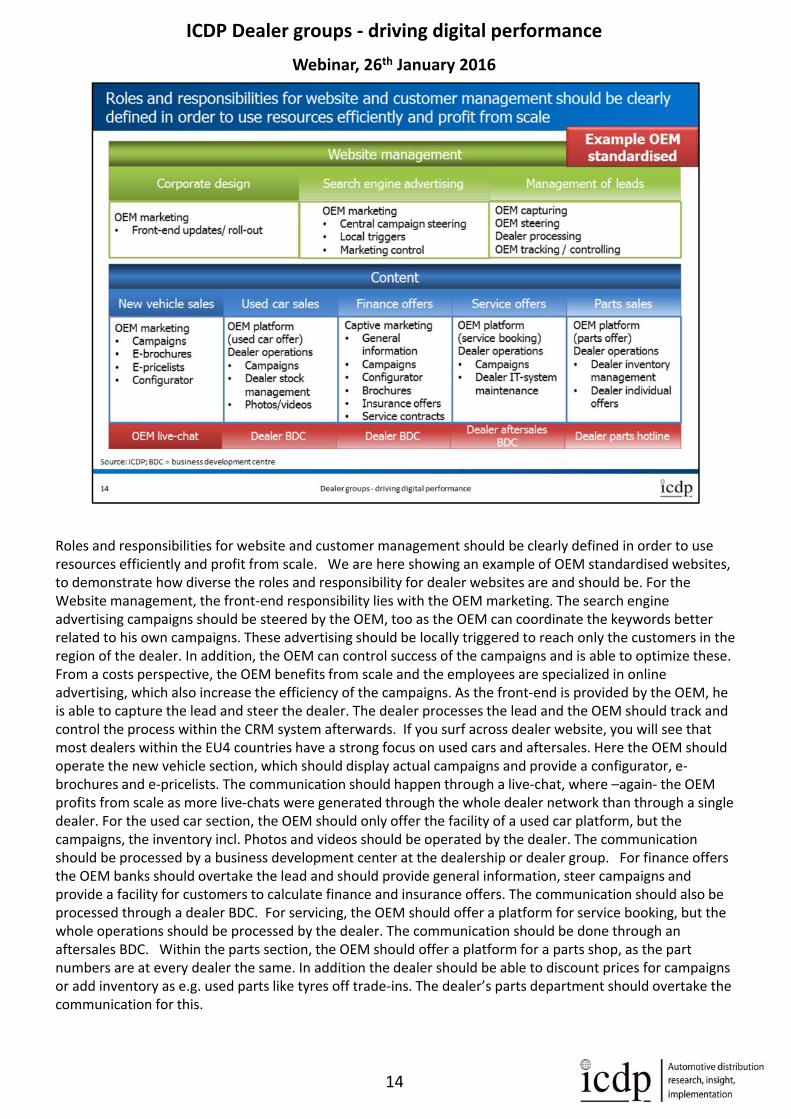

Roles and responsibilities for website and customer management should be clearly defined in order to use resources efficiently and profit from scale. We are here showing an example of OEM standardised websites, to demonstrate how diverse the roles and responsibility for dealer websites are and should be. For the Website management, the front‐end responsibility lies with the OEM marketing. The search engine advertising campaigns should be steered by the OEM, too as the OEM can coordinate the keywords better related to his own campaigns. These advertising should be locally triggered to reach only the customers in the region of the dealer. In addition, the OEM can control success of the campaigns and is able to optimize these. From a costs perspective, the OEM benefits from scale and the employees are specialized in online advertising, which also increase the efficiency of the campaigns. As the front‐end is provided by the OEM, he is able to capture the lead and steer the dealer. The dealer processes the lead and the OEM should track and control the process within the CRM system afterwards. If you surf across dealer website, you will see that most dealers within the EU4 countries have a strong focus on used cars and aftersales. Here the OEM should operate the new vehicle section, which should display actual campaigns and provide a configurator, e‐brochures and e‐pricelists. The communication should happen through a live‐chat, where –again‐ the OEM profits from scale as more live‐chats were generated through the whole dealer network than through a single dealer. For the used car section, the OEM should only offer the facility of a used car platform, but the campaigns, the inventory incl. Photos and videos should be operated by the dealer. The communication should be processed by a business development center at the dealership or dealer group. For finance offers the OEM banks should overtake the lead and should provide general information, steer campaigns and provide a facility for customers to calculate finance and insurance offers. The communication should also be processed through a dealer BDC. For servicing, the OEM should offer a platform for service booking, but the whole operations should be processed by the dealer. The communication should be done through an aftersales BDC. Within the parts section, the OEM should offer a platform for a parts shop, as the part numbers are at every dealer the same. In addition the dealer should be able to discount prices for campaigns or add inventory as e.g. used parts like tyres off trade‐ins. The dealer’s parts department should overtake the communication for this.

14

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

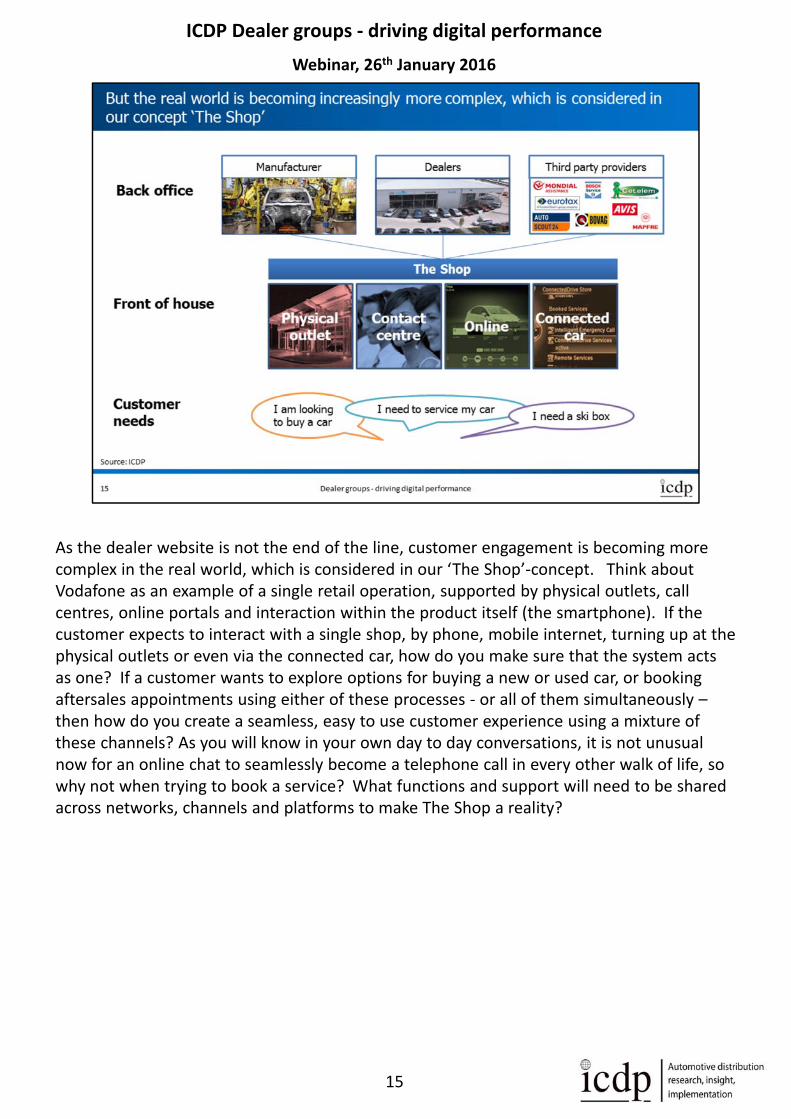

As the dealer website is not the end of the line, customer engagement is becoming more complex in the real world, which is considered in our ‘The Shop’‐concept. Think about Vodafone as an example of a single retail operation, supported by physical outlets, call centres, online portals and interaction within the product itself (the smartphone). If the customer expects to interact with a single shop, by phone, mobile internet, turning up at the physical outlets or even via the connected car, how do you make sure that the system acts as one? If a customer wants to explore options for buying a new or used car, or booking aftersales appointments using either of these processes ‐ or all of them simultaneously –then how do you create a seamless, easy to use customer experience using a mixture of these channels? As you will know in your own day to day conversations, it is not unusual now for an online chat to seamlessly become a telephone call in every other walk of life, so why not when trying to book a service? What functions and support will need to be shared across networks, channels and platforms to make The Shop a reality?

15

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

Customer expectations of digital services are very high, as they are already spoilt by other business sectors. Within the next section, we are showing you what functions automotive customers expect on a dealer website and if dealer can satisfy these needs.

16

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

In order to understand better how dealers are exploiting the digital channel, we have made a qualitative analysis of the websites among the ten largest groups and of OEM wholly‐owned dealer groups within the major European markets in order to understand how they are using the web to attract customers and to offer products and services. Already mentioned earlier, that consumers enjoy watching videos during their research phase and that these are influential to their purchase decision. However, 57% of vehicle customers use online video for their purchase decision; and especially 31% of automotive customers want to watch more videos about products and service. For used car business this area dealers should improve, in fact only in the UK 55% of the largest dealer groups offer videos for most used cars on sale, while in the other markets no large dealer exploit this opportunity, as shown in the top right chart on the slide. But also OEM wholly‐owned dealer groups rarely adopt this additional services. In France only 17% and UK only 10% of wholly‐owned dealer groups show videos for used cars. During their research, 82% of customers would use a live chat, if it is available. And 62% of customers expect a live chat to be available even on their mobile device. ICDPs consumer research has shown that only 1% of the respondents had used a live chat during their purchase process, what can be explained by the limited availability of live chats within the automotive sector. To add a live chat to a website is a cost and resource intense investment. The investment for the live chat function on a website as well as the equipment like microphones, webcams etc. is more than €10,000, plus the ongoing costs. And here again, only UK independent dealer groups offer a live chat functionality on their website. On OEM wholly‐owned group websites in UK every second website offers this function, followed by France with 17% and Italy 14%. In Germany only 7% of wholly owned group websites offer a live chat. And what’s about the trade‐in? ICDPs consumer research has revealed that 39% of customer would conduct a trade‐in valuation online. And 17% of customer even define an online trade‐in valuation as their ideal buying process. Therefor 82% of UK independent dealer groups offer a facility for trade‐in quotation, followed by 40% of French dealer groups who offer this facility. Italian and German independent dealer groups don’t offer such a service.

17

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

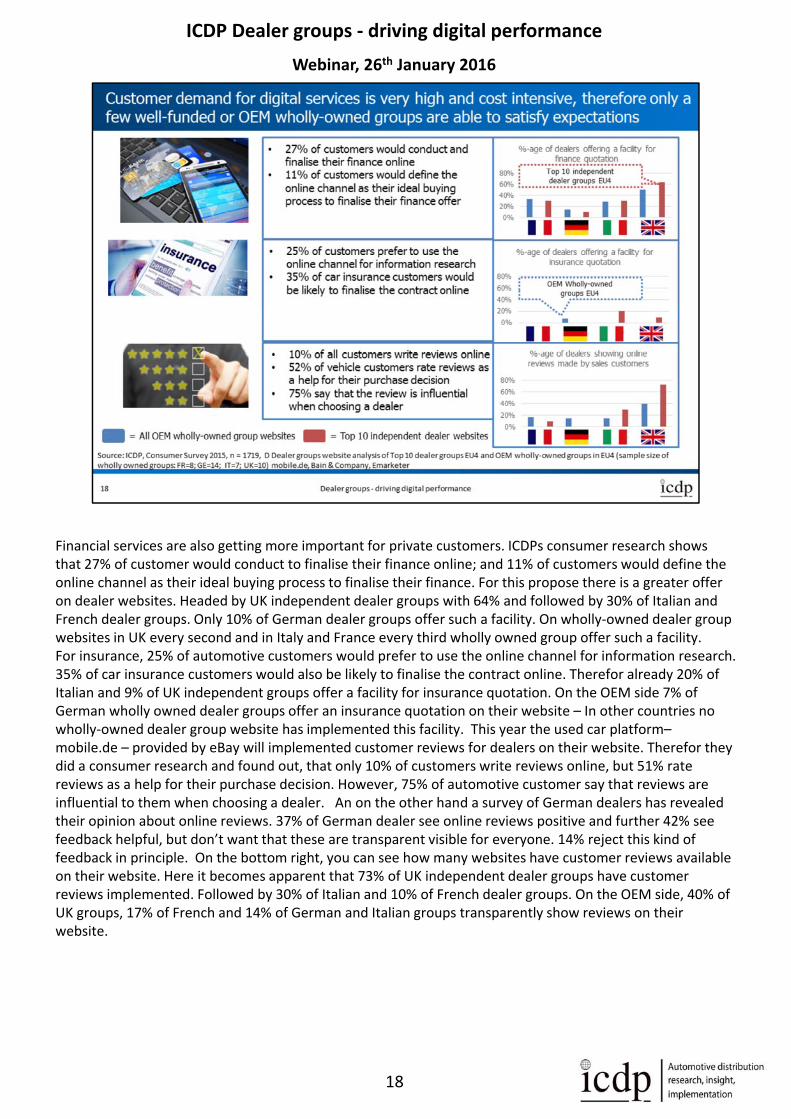

Financial services are also getting more important for private customers. ICDPs consumer research shows that 27% of customer would conduct to finalise their finance online; and 11% of customers would define the online channel as their ideal buying process to finalise their finance. For this propose there is a greater offer on dealer websites. Headed by UK independent dealer groups with 64% and followed by 30% of Italian and French dealer groups. Only 10% of German dealer groups offer such a facility. On wholly‐owned dealer group websites in UK every second and in Italy and France every third wholly owned group offer such a facility. For insurance, 25% of automotive customers would prefer to use the online channel for information research. 35% of car insurance customers would also be likely to finalise the contract online. Therefor already 20% of Italian and 9% of UK independent groups offer a facility for insurance quotation. On the OEM side 7% of German wholly owned dealer groups offer an insurance quotation on their website – In other countries no wholly‐owned dealer group website has implemented this facility. This year the used car platform–mobile.de – provided by eBay will implemented customer reviews for dealers on their website. Therefor they did a consumer research and found out, that only 10% of customers write reviews online, but 51% rate reviews as a help for their purchase decision. However, 75% of automotive customer say that reviews are influential to them when choosing a dealer. An on the other hand a survey of German dealers has revealed their opinion about online reviews. 37% of German dealer see online reviews positive and further 42% see feedback helpful, but don’t want that these are transparent visible for everyone. 14% reject this kind of feedback in principle. On the bottom right, you can see how many websites have customer reviews available on their website. Here it becomes apparent that 73% of UK independent dealer groups have customer reviews implemented. Followed by 30% of Italian and 10% of French dealer groups. On the OEM side, 40% of UK groups, 17% of French and 14% of German and Italian groups transparently show reviews on their website.

18

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

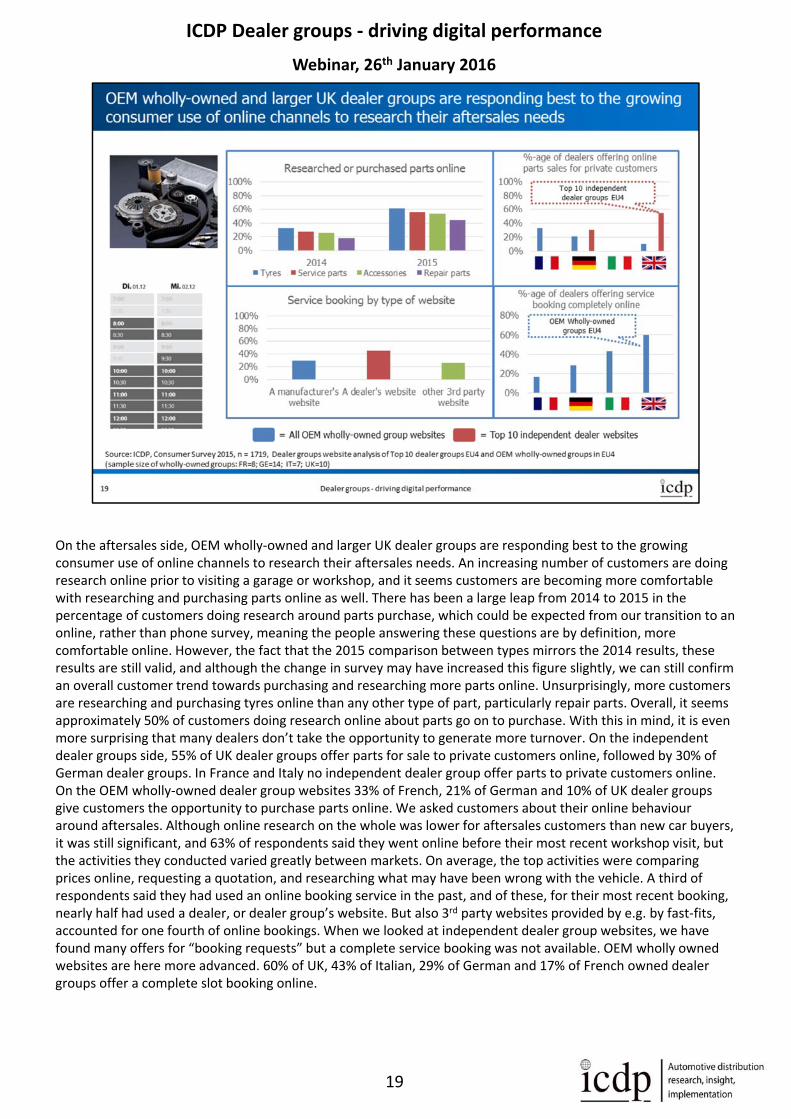

On the aftersales side, OEM wholly‐owned and larger UK dealer groups are responding best to the growing consumer use of online channels to research their aftersales needs. An increasing number of customers are doing research online prior to visiting a garage or workshop, and it seems customers are becoming more comfortable with researching and purchasing parts online as well. There has been a large leap from 2014 to 2015 in the percentage of customers doing research around parts purchase, which could be expected from our transition to an online, rather than phone survey, meaning the people answering these questions are by definition, more comfortable online. However, the fact that the 2015 comparison between types mirrors the 2014 results, these results are still valid, and although the change in survey may have increased this figure slightly, we can still confirm an overall customer trend towards purchasing and researching more parts online. Unsurprisingly, more customers are researching and purchasing tyres online than any other type of part, particularly repair parts. Overall, it seems approximately 50% of customers doing research online about parts go on to purchase. With this in mind, it is even more surprising that many dealers don’t take the opportunity to generate more turnover. On the independent dealer groups side, 55% of UK dealer groups offer parts for sale to private customers online, followed by 30% of German dealer groups. In France and Italy no independent dealer group offer parts to private customers online. On the OEM wholly‐owned dealer group websites 33% of French, 21% of German and 10% of UK dealer groups give customers the opportunity to purchase parts online. We asked customers about their online behaviour around aftersales. Although online research on the whole was lower for aftersales customers than new car buyers, it was still significant, and 63% of respondents said they went online before their most recent workshop visit, but the activities they conducted varied greatly between markets. On average, the top activities were comparing prices online, requesting a quotation, and researching what may have been wrong with the vehicle. A third of respondents said they had used an online booking service in the past, and of these, for their most recent booking, nearly half had used a dealer, or dealer group’s website. But also 3rd party websites provided by e.g. by fast‐fits, accounted for one fourth of online bookings. When we looked at independent dealer group websites, we have found many offers for “booking requests” but a complete service booking was not available. OEM wholly owned websites are here more advanced. 60% of UK, 43% of Italian, 29% of German and 17% of French owned dealer groups offer a complete slot booking online.

19

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

In this section, we have taken a closer look at the channels Facebook and YouTube, more exactly we looked at how and why dealer groups operate them and what their structures look like. In doing so,we considered these channels as important interaction tools and suitable ways to present products and staff to potential customers. Hence, we each surveyed the profiles of top 10 dealer groups within the EU4 markets.

20

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

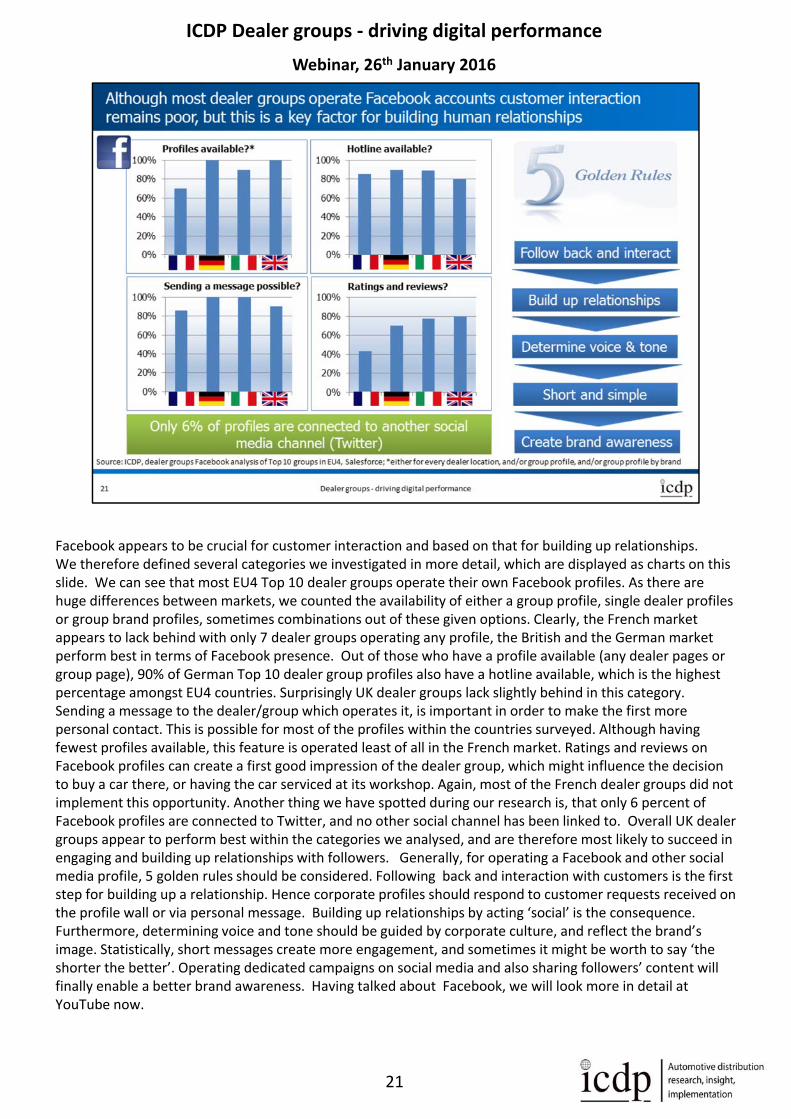

Facebook appears to be crucial for customer interaction and based on that for building up relationships. We therefore defined several categories we investigated in more detail, which are displayed as charts on this slide. We can see that most EU4 Top 10 dealer groups operate their own Facebook profiles. As there are huge differences between markets, we counted the availability of either a group profile, single dealer profiles or group brand profiles, sometimes combinations out of these given options. Clearly, the French market appears to lack behind with only 7 dealer groups operating any profile, the British and the German market perform best in terms of Facebook presence. Out of those who have a profile available (any dealer pages or group page), 90% of German Top 10 dealer group profiles also have a hotline available, which is the highest percentage amongst EU4 countries. Surprisingly UK dealer groups lack slightly behind in this category. Sending a message to the dealer/group which operates it, is important in order to make the first more personal contact. This is possible for most of the profiles within the countries surveyed. Although having fewest profiles available, this feature is operated least of all in the French market. Ratings and reviews on Facebook profiles can create a first good impression of the dealer group, which might influence the decision to buy a car there, or having the car serviced at its workshop. Again, most of the French dealer groups did not implement this opportunity. Another thing we have spotted during our research is, that only 6 percent of Facebook profiles are connected to Twitter, and no other social channel has been linked to. Overall UK dealer groups appear to perform best within the categories we analysed, and are therefore most likely to succeed in engaging and building up relationships with followers. Generally, for operating a Facebook and other social media profile, 5 golden rules should be considered. Following back and interaction with customers is the first step for building up a relationship. Hence corporate profiles should respond to customer requests received on the profile wall or via personal message. Building up relationships by acting ‘social’ is the consequence. Furthermore, determining voice and tone should be guided by corporate culture, and reflect the brand’s image. Statistically, short messages create more engagement, and sometimes it might be worth to say ‘the shorter the better’. Operating dedicated campaigns on social media and also sharing followers’ content will finally enable a better brand awareness. Having talked about Facebook, we will look more in detail at YouTube now.

21

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

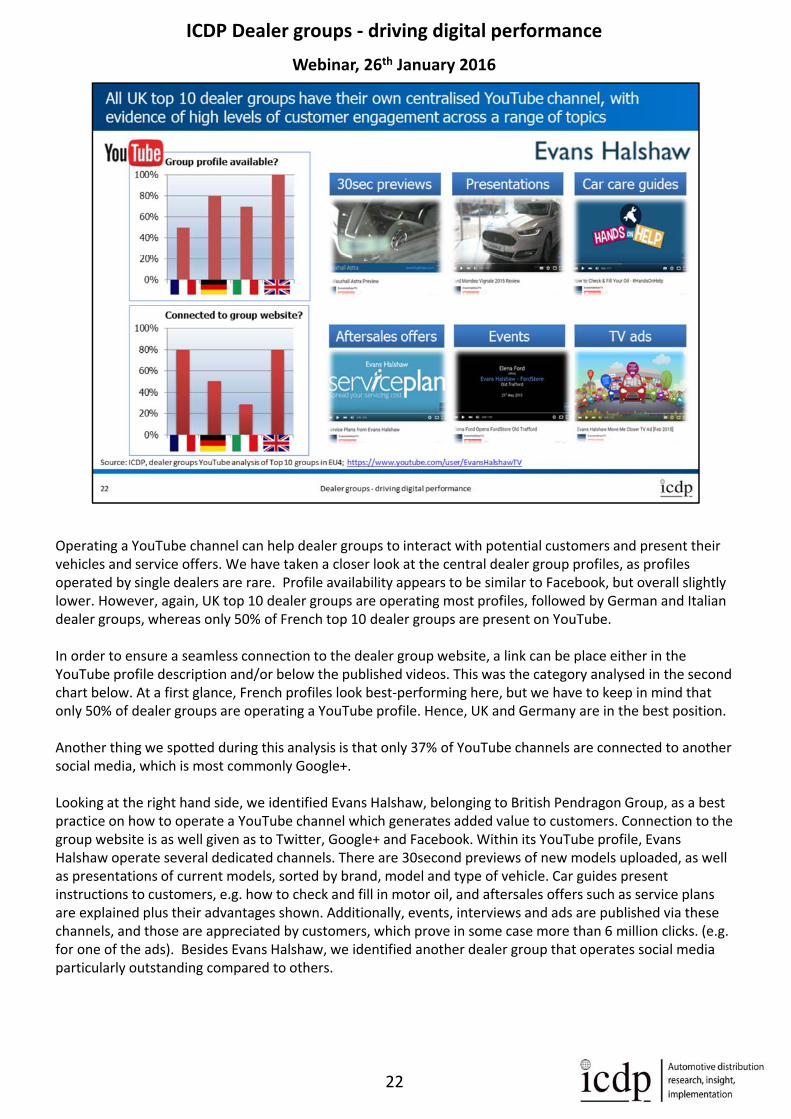

Operating a YouTube channel can help dealer groups to interact with potential customers and present their vehicles and service offers. We have taken a closer look at the central dealer group profiles, as profiles operated by single dealers are rare. Profile availability appears to be similar to Facebook, but overall slightly lower. However, again, UK top 10 dealer groups are operating most profiles, followed by German and Italian dealer groups, whereas only 50% of French top 10 dealer groups are present on YouTube.

In order to ensure a seamless connection to the dealer group website, a link can be place either in the YouTube profile description and/or below the published videos. This was the category analysed in the second chart below. At a first glance, French profiles look best‐performing here, but we have to keep in mind that only 50% of dealer groups are operating a YouTube profile. Hence, UK and Germany are in the best position.

Another thing we spotted during this analysis is that only 37% of YouTube channels are connected to another social media, which is most commonly Google+.

Looking at the right hand side, we identified Evans Halshaw, belonging to British Pendragon Group, as a best practice on how to operate a YouTube channel which generates added value to customers. Connection to the group website is as well given as to Twitter, Google+ and Facebook. Within its YouTube profile, Evans Halshaw operate several dedicated channels. There are 30second previews of new models uploaded, as well as presentations of current models, sorted by brand, model and type of vehicle. Car guides present instructions to customers, e.g. how to check and fill in motor oil, and aftersales offers such as service plans are explained plus their advantages shown. Additionally, events, interviews and ads are published via these channels, and those are appreciated by customers, which prove in some case more than 6 million clicks. (e.g. for one of the ads). Besides Evans Halshaw, we identified another dealer group that operates social media particularly outstanding compared to others.

22

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

Perrys, ranked on #15 by revenue in UK, is a British dealer group that operates website, Facebook and YouTube profile with their own online channel marketing strategy. Activities within the social media channels are not steered centrally, the ‘social bunch’ within the company, as to say the staff, is in charge and acts in an authentic and professional way.

Dealers belonging to Perrys operate a centralised website, including individual content such as used car offers and new car offers. This individual content is managed by members of a digital team at location level. In terms off seamless connection, the website is linked to Facebook, Twitter, YouTube, Google+ and Pinterest via buttons and ensures that switching channels is always possible. (YouTube videos are directly integrated on the website and the number of Facebook followers is shown.) As of December 2015, the main group page generates approx. 65k visits a month, 4.5 page views on average and an average total time spent on the website of 4 minutes. Looking at Facebook, Perrys operates a group profile in addition to separate dealer managed profiles with individual content. The main page has a huge number of likes and offers virtual tours, besides being well connected to other social media and the group website.

Within Perrys YouTube profile, the company operates 3 different channels in order to fully satisfy customers needs. The vital drive channel shows exciting car videos, whereas car care guides explain customers e.g. how to change tyres properly. Car buyer guide videos offer in‐depth information about desired models and comparisons. Within the videos, employees act as brand ambassadors, and intend to appeal customers for the models and the dealer group. Clearly, entertainment, providing information (also via links to different parts of the website) and moving a step towards brand engagement is the objective of Perrys YouTube approach. As an indicator for success, customer response in the form of likes, and subscribers is high. Besides Perrys, we would like to mention a successful and well‐known social media campaign that is called ‘Lost Bunny’. It is aimed at reuniting a bunny with its owner, which has been lost in a Ridgeway’s Land Rover dealership (British dealership). The campaign has spread viral across social media. This is another indicator that authentic campaigns with a personal and human character are accepted well by customers.

23

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

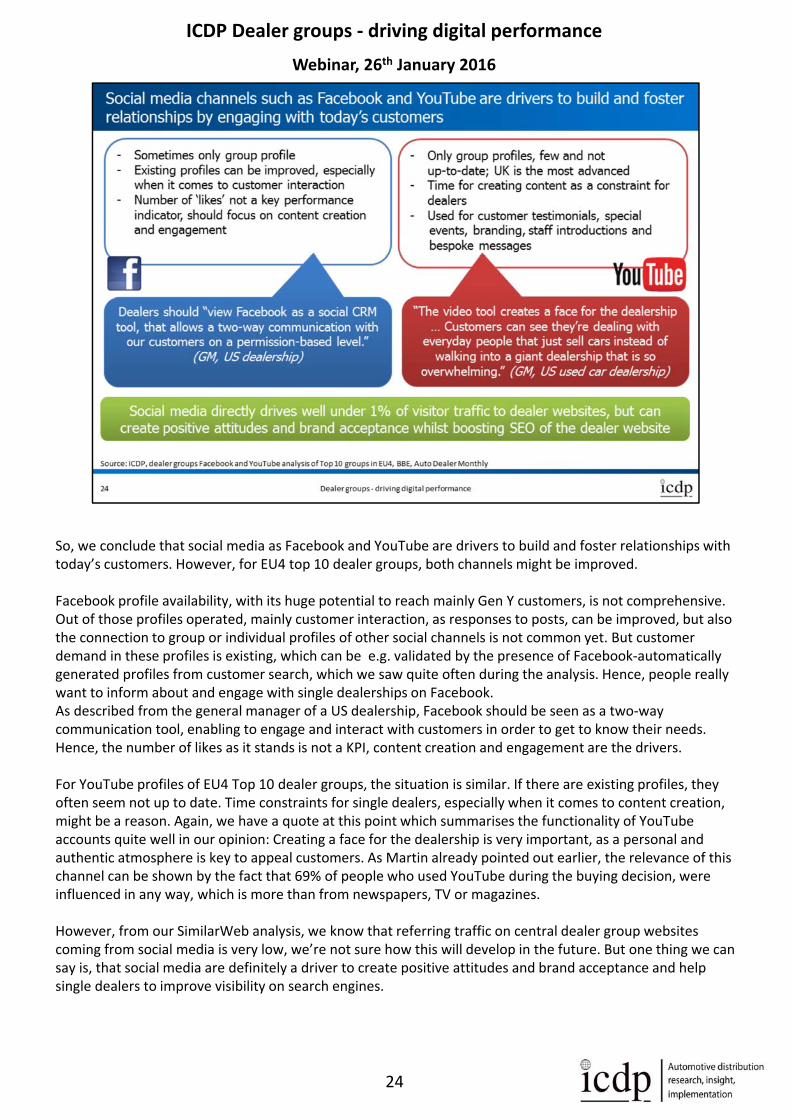

So, we conclude that social media as Facebook and YouTube are drivers to build and foster relationships with today’s customers. However, for EU4 top 10 dealer groups, both channels might be improved.

Facebook profile availability, with its huge potential to reach mainly Gen Y customers, is not comprehensive. Out of those profiles operated, mainly customer interaction, as responses to posts, can be improved, but also the connection to group or individual profiles of other social channels is not common yet. But customer demand in these profiles is existing, which can be e.g. validated by the presence of Facebook‐automatically generated profiles from customer search, which we saw quite often during the analysis. Hence, people really want to inform about and engage with single dealerships on Facebook. As described from the general manager of a US dealership, Facebook should be seen as a two‐way communication tool, enabling to engage and interact with customers in order to get to know their needs. Hence, the number of likes as it stands is not a KPI, content creation and engagement are the drivers.

For YouTube profiles of EU4 Top 10 dealer groups, the situation is similar. If there are existing profiles, they often seem not up to date. Time constraints for single dealers, especially when it comes to content creation, might be a reason. Again, we have a quote at this point which summarises the functionality of YouTube accounts quite well in our opinion: Creating a face for the dealership is very important, as a personal and authentic atmosphere is key to appeal customers. As Martin already pointed out earlier, the relevance of this channel can be shown by the fact that 69% of people who used YouTube during the buying decision, were influenced in any way, which is more than from newspapers, TV or magazines.

However, from our SimilarWeb analysis, we know that referring traffic on central dealer group websites coming from social media is very low, we’re not sure how this will develop in the future. But one thing we can say is, that social media are definitely a driver to create positive attitudes and brand acceptance and help single dealers to improve visibility on search engines.

24

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

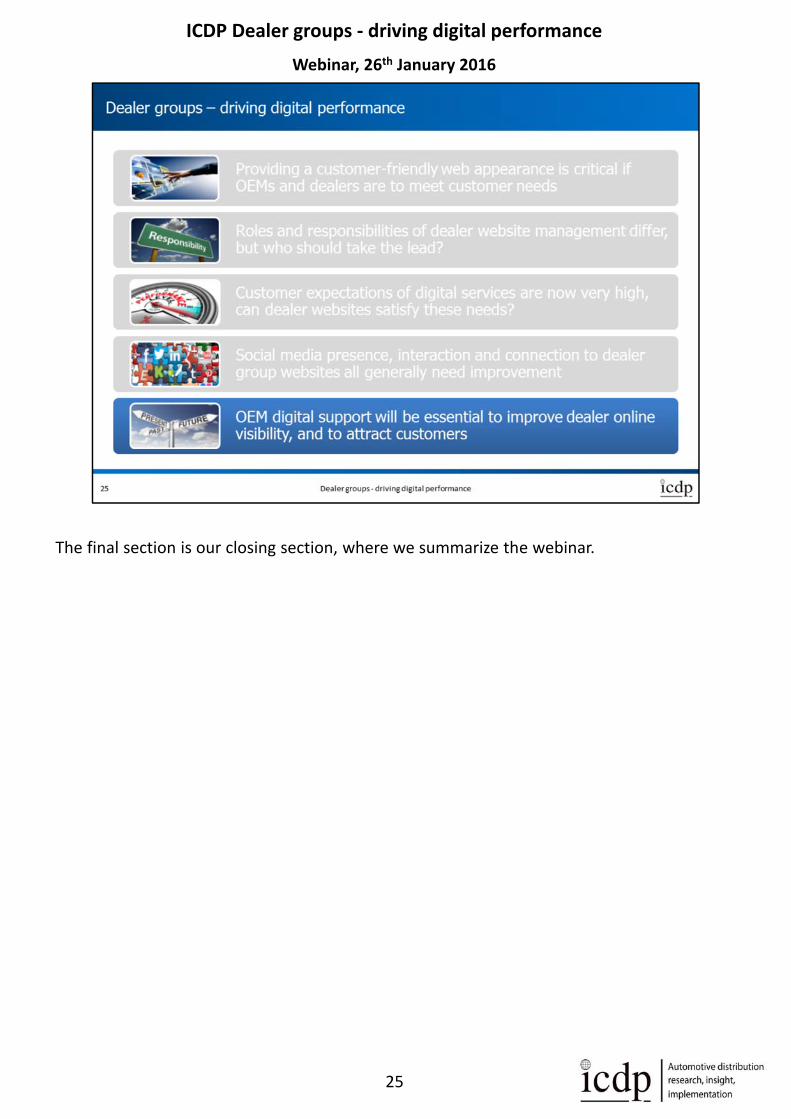

The final section is our closing section, where we summarize the webinar.

25

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

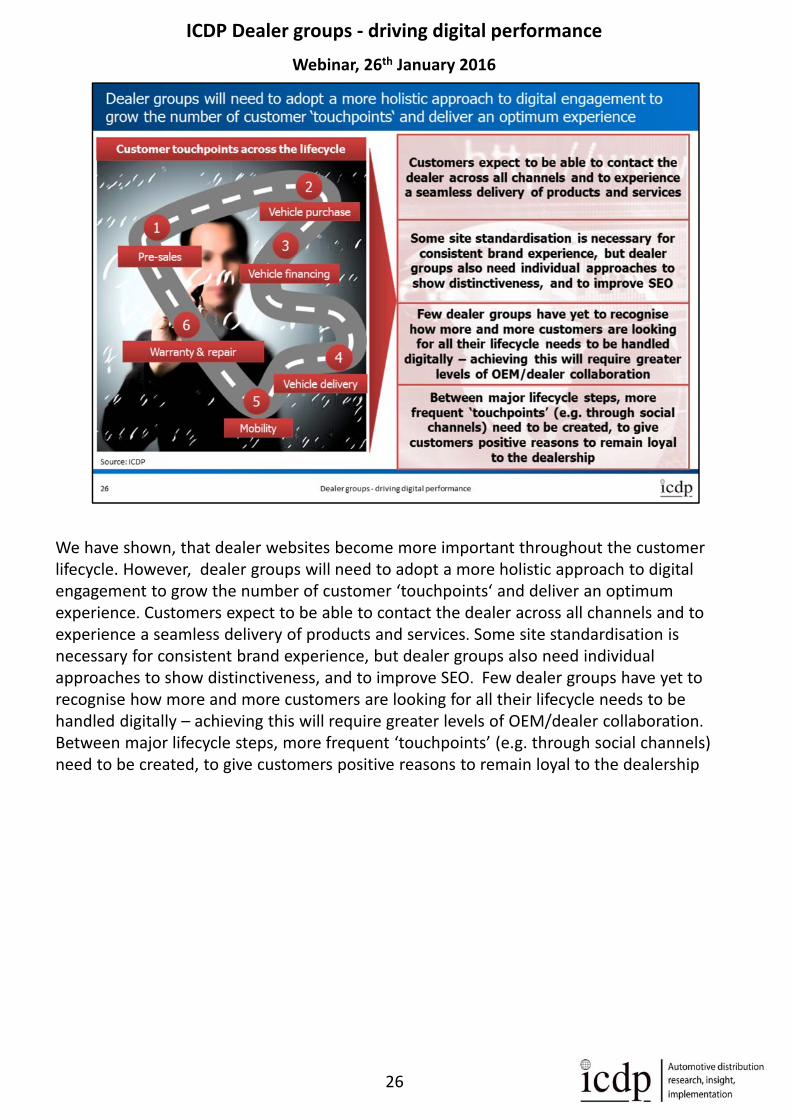

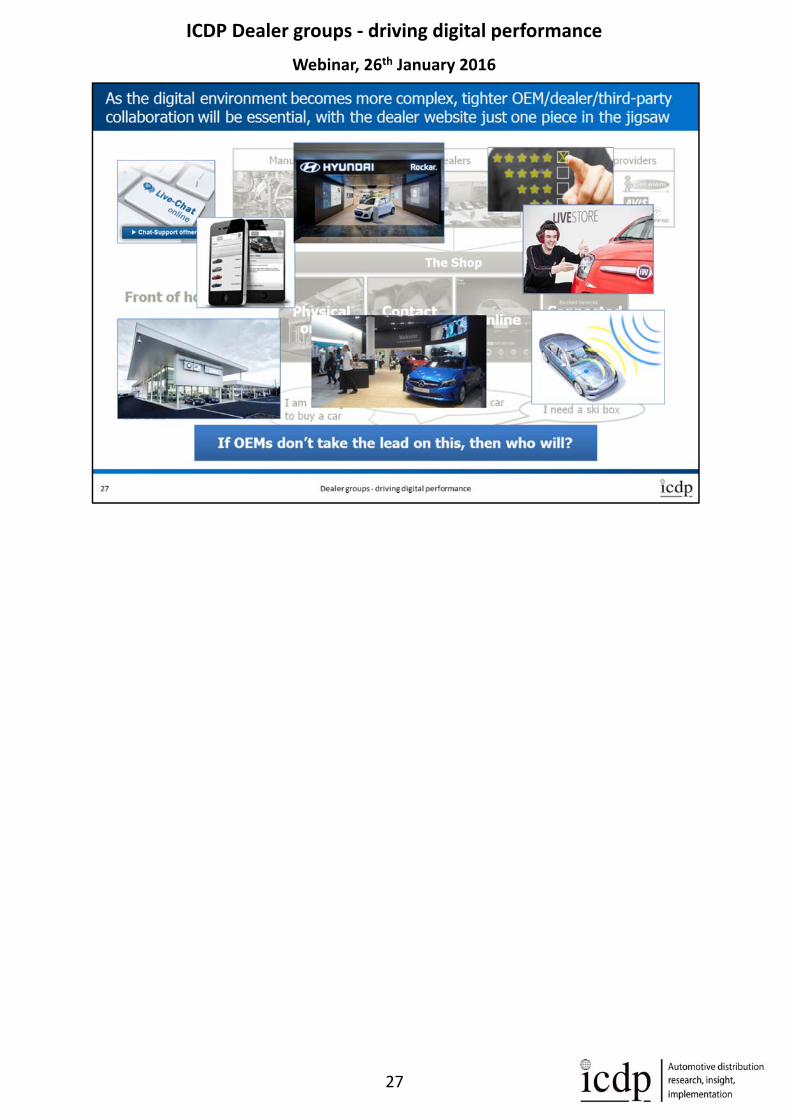

We have shown, that dealer websites become more important throughout the customer lifecycle. However, dealer groups will need to adopt a more holistic approach to digital engagement to grow the number of customer ‘touchpoints‘ and deliver an optimum experience. Customers expect to be able to contact the dealer across all channels and to experience a seamless delivery of products and services. Some site standardisation is necessary for consistent brand experience, but dealer groups also need individual approaches to show distinctiveness, and to improve SEO. Few dealer groups have yet to recognise how more and more customers are looking for all their lifecycle needs to be handled digitally – achieving this will require greater levels of OEM/dealer collaboration. Between major lifecycle steps, more frequent ‘touchpoints’ (e.g. through social channels) need to be created, to give customers positive reasons to remain loyal to the dealership

26

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

27

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

28

ICDP Dealer groups ‐ driving digital performance

Webinar, 26th January 2016

29