IAS 21 AFA

31

for Accountin g Professional s IAS 21 The effects of changes in foreign exchange rates 2011 http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng

-

Upload

riiko-leon -

Category

Documents

-

view

231 -

download

0

Transcript of IAS 21 AFA

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 1/31

for Accounting Professionals

IAS 21 The effects of changes in foreign exchange rates

2011

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 2/31

IFRS WORKBOOKS(1 million downloaded)

Welcome to IFRS Workbooks! These are the latest versions o the legendary workbooks in Russian and English rod"ced b# $ T%&IS ro'ects sonsored b# theEuropean nion (**$+**,) and led b# !ricewaterhouse"oopers- The# have also aeared on the website o the #inistry of $inance of the Russian $ederation-

The workbooks cover vario"s concets o IFRS based acco"ntin.- The# are intended to be ractical sel+instr"ction aids that roessional acco"ntants can "se to ".radetheir knowled.e "nderstandin. and skills-

/ach workbook is a sel+standin. short co"rse desi.ned or aro0imatel# o three ho"rs o st"d#- %ltho".h the workbooks are art o a series each one is indeendent o the others- /ach workbook is a combination o Infor%ation& Exa%ples& Self'Test (uestions and Answers- % basic knowled.e o acco"ntin. is ass"med b"t i an#additional knowled.e is re"ired this is mentioned at the be.innin. o the section-

2avin. written the irst three editions we want to update the% and pro)ide the% to you to download* !lease tell your friends and colleagues* Relatin. to the irst threeeditions and "dated te0ts the co#ri.ht o the material contained in each workbook belon.s to the /"roean 3nion and accordin. to its olic# %ay be used free of chargefor any non'co%%ercial purpose- The co#ri.ht and resonsibilit# o later books and the "dates are o"rs- O"r co#ri.ht olic# is the same as that o the /"roean 3nion-

We wish to eseciall# thank Eli+abeth Appraxine (/"roean 3nion) who administered these T%&IS ro'ects Richard ,* -regson (4artner 4ricewaterho"se&ooers) who

led the ro'ects and all friends at .ankir*Ru or hostin. the books-

T%&IS ro'ect artners incl"ded Rose0erti5a (R"ssia) %&&% (3K) %.ricons"ltin. (Ital#) FBK (R"ssia) and /"roean Savin.s Bank 6ro" (Br"ssels)- The hel o !hilip/* S%ith (editor o the third edition) and Allan -a%borg ro'ect mana.ers and Ekaterina ekraso)a 7irector o 4ricewaterho"se&ooers who mana.ed the rod"ctiono the R"ssian version (**8+,) is .rate"ll# acknowled.ed- -lyn R* !hillips mana.er o the irst two ro'ects conceived the idea desi.ned the workbooks and edited theirst two versions- We are ro"d to realise his vision-

Robin ,oyce!rofessor of the "hair ofInternational .anking and $inance$inancial ni)ersityunder the -o)ern%ent of the Russian $ederation

1isiting !rofessor of the Siberian Acade%y of $inance and .anking 9oscow( R"ssia )*11 3!dated

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 3/31

IAS 21 The effects of changes in foreignexchange rates

"ontents

1* "onsolidation Introduction

3

2* efinitions

4

3* IAS 21 for .anks

5

4* $oreign "urrency Transactions in the or%al "ourse of

.usiness

6

5* Initial Recognition of a Transaction 7

6* Reporting at .alance Sheet ates

8

7* $inancial State%ents of $oreign 8perations

9

9* isposal of a $oreign 8peration

17

:* isclosure Re;uire%ents

19

10* Annex < Exa%ples '$oreign operations with non'

coter%inous year ends 19

11* #ultiple "hoice (uestions21

12* Exercise (uestions

24

13* Solutions

28

14* I$RS $ra%ework

30

:ote; 9aterial rom the ollowin. 4ricewaterho"se&ooers "blications has been"sed in this workbook;

%l#in. IFRS IFRS :ews %cco"ntin. Sol"tions

1* "onsolidation Introduction

Aim

The aim o this workbook is to assist the individ"al in "nderstandin.

consolidation methodolo.# or IFRS and the role o orei.n c"rrenc#both in consolidated statements and sin.le+"ndertakin. inancialstatements- It also covers orei.n c"rrenc# transactions arisin. romtrade-

Consolidation Approach

Beore commencin. a consolidation the acco"ntant sho"ld have the"ll inancial statements o the arent and s"bsidiaries rod"ced aso the same date and havin. "sed the same acco"ntin. olicies-

Where ossible all s"bsidiar# #ear+ends m"st be the same as thearent "ndertakin.- 3nder I%S < the ma0im"m ermitteddierence is $ months-

%d'"stment sho"ld be made or an# si.niicant dierences createdb# an# s"bsidiar# havin. a dierent acco"ntin. date-

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 4/31

IAS 21 The effects of changes in foreign exchange rates

The len.th o reortin. eriods and an# dierence in the reortin.dates sho"ld be consistent rom eriod to eriod-

Transactions between .ro" "ndertakin.s sho"ld be listed andbalances between .ro" "ndertakin.s sho"ld be a.reed and listed-

Where an "ndertakin. has been "rchased the inancial statements

at the time o ac"isition sho"ld be on hand- Similarl# where an

"ndertakin. has been sold the inancial statements on the date o

sale sho"ld be available-

Sreadsheets are ideal or rod"cin. consolidated balance sheets

and income statements altho".h besoke consolidated sotware is

available-

8T=ER "8#!RE=ESIE I"8#E

I%S 1 introd"ced Other &omrehensive Income as a inancialstatement-

%ll movements into and o"t o reval"ation reserves and orei.n

c"rrenc# translations (both in /"it#) are recorded here-

If a gain& or loss& is reported in profit and loss& any relatedexchange gain& or loss& will also be reported in profit and loss*

If a gain& or loss& is reported in 8ther "o%prehensi)e Inco%e&any related exchange gain& or loss& will also be reported in8ther "o%prehensi)e Inco%e*

2* efinitions

Undertaking

%n "ndertakin. is an# b"siness either incororated or"nincororated-

Parent

% arent is an "ndertakin. that controls another "ndertakin.-

Subsidiary

% s"bsidiar# is an "ndertakin. that is controlled b# another-

Group, or business combination

Two or more comanies where one coman# controls the other(s)-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng =

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 5/31

IAS 21 The effects of changes in foreign exchange rates

7issimilar b"siness activities m"st be consolidated i the# controlledb# the arent "ndertakin.-

Control

&ontrol is the ower to .overn the inancial and oeratin. olicies oan "ndertakin. to obtain beneits-

Indications o control are;

Ownershi o more than >*? o the votin. ri.hts-/ective control over more than >*? o the votin. ri.hts- Fore0amle a h"sband owns $*? and a wie owns =*?-

%s the# are connected arties the# can e0ercise control overthe s"bsidiar#-

&ontrollin. the comosition o the board o directors

Fair valueFair val"e is the price that would be recei)ed to sell anasset& or paid to transfer a liability& in an orderlytransaction between %arket participants at the%easure%ent date* >I$RS 13?

Monetary items

9onetar# items are mone# held assets receivable and liabilitiesa#able in cash-

Associate

%n "ndertakin. in which the arent has si.niicant inl"ence b"t isneither its s"bsidiar# nor art o a 'oint vent"re o the arent-

Indications o si.niicant inl"ence are;

Ownershi o *+>*? o the votin. shares

Reresentation on the Board o 7irectors

Joint enture

% 'oint vent"re is an "ndertakin. s"b'ect to the 'oint control o two ormore enterrises- The 'oint control is .overned b# a contractbetween the arties-

Foreign !peration

% orei.n oeration is a branch associate 'oint vent"re or s"bsidiar#where the activities are cond"cted in a dierent co"ntr# to that o thearent "ndertakin.-

Presentation Currency

The resentation c"rrenc# is that "sed in the arent@s and in theconsolidated inancial statements-

FU"C#$!"A% CU&&'"C(

The "nctional c"rrenc# is the c"rrenc# o the rimar# economicenvironment in which the "ndertakin. oerates-

Foreign Currency

Forei.n c"rrenc# is an# c"rrenc# other than the "nctional c"rrenc#-

')change *i++erence/0chan.e dierence is the dierence calc"lated rom reortin. thesame n"mber o "nits o a orei.n c"rrenc# at dierent e0chan.erates-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng >

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 6/31

IAS 21 The effects of changes in foreign exchange rates

Closing &ate

The closin. rate is the sot e0chan.e rate at the balance sheet date-

"et $nvestment in a Foreign Undertaking

The net investment in a orei.n oeration is the arent@s share o thenet assets o the "ndertakin.-

Spot e)change rate

The Sot e0chan.e rate is the e0chan.e rate or immediate deliver#-

3* IAS 21 for .anks

The ma'orit# o bank transactions in orei.n c"rrenc# relate toinancial instr"ments- These are reval"ed dail# in most co"ntries"sin. the rates rovided b# the &entral Bank with reval"ation

dierences .oin. to the income statement-

This treatment is the same "nder IFRS (with the e0cetion oavailable+or+sale inancial instr"ments where the reval"ationdierence will .o to e"it# "ntil the# are sold)-

7ealin. in orei.n c"rrencies involves another la#er o risk or Banks(Barin.s Bank in the 3K was bankr"ted b# sec"latin. on theAaanese en) b"t also or bank clients who oten are "nable (or"nwillin.) to "ll# mana.e their orei.n c"rrenc# risk-

IFRS < re"ires banks to detail e0os"re and the mana.ement otheir orei.n e0chan.e risk in inancial statements-

I$RS : applies to %any foreign currency deri)ati)es and&accordingly& these are excluded fro% the scope of IAS 21*

=owe)er& those foreign currency deri)ati)es that are not withinthe scope of I$RS : >for exa%ple? so%e foreign currencyderi)ati)es that are e%bedded in other contracts? are within the

scope of IAS 21*

In addition& IAS 21 applies when an entity translates a%ountsrelating to deri)ati)es fro% its functional currency to itspresentation currency*

4* $oreign "urrency Transactions in the or%al "ourse of.usiness

#ransactions and $nvestments in Foreign Currencies

Transactions and investments in orei.n c"rrencies increase

b"siness risk d"e to the c"rrenc# l"ct"ations a.ainst the nationalc"rrenc#-

2oldin. an# assets or liabilities denominated in orei.n c"rrenc#entails a c"rrenc# risk- There is a risk that #o" will make a roit orloss i the e0chan.e rate chan.es when settlement is made-Techni"es s"ch as hed.in. orward contracts and otions ma# beemlo#ed to red"ce risk-

International b"siness necessitates man# irms tradin. in orei.nc"rrencies- The time between "otin. a rice i0ed in a orei.nc"rrenc# and inall# receivin. the "nds sho"ld be minimised to limitrisk-

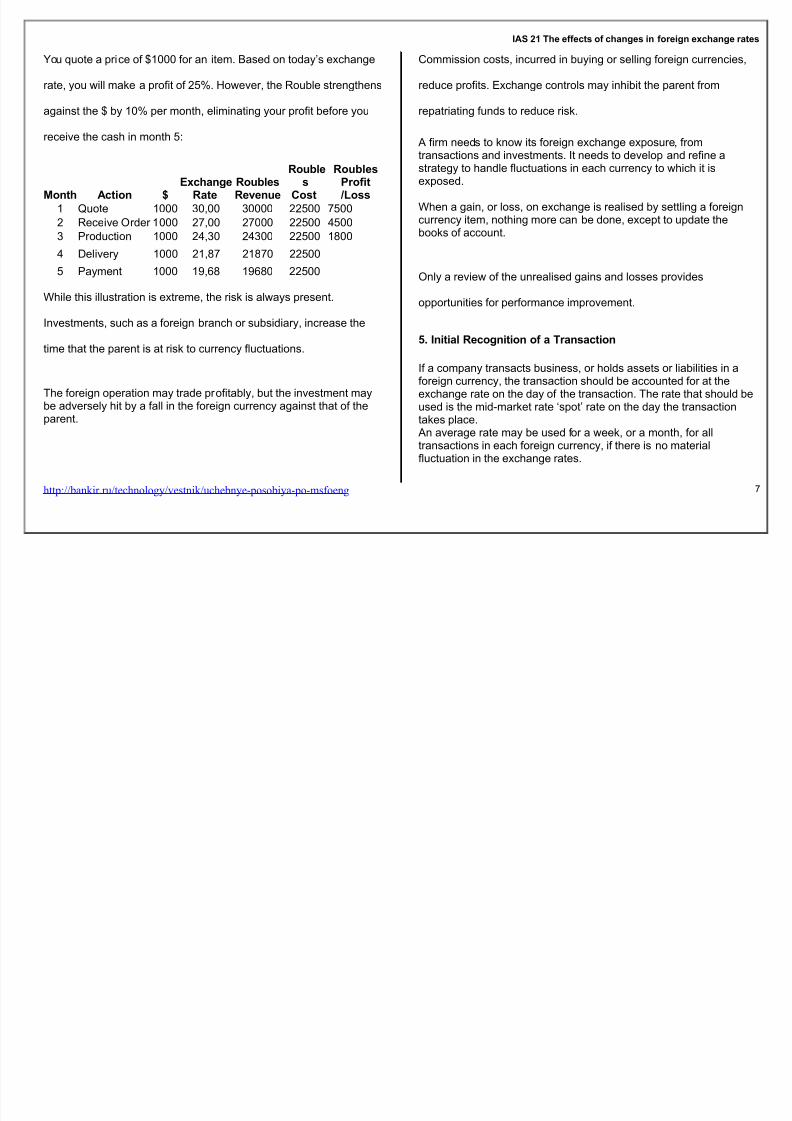

Exa%ple;

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng C

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 7/31

IAS 21 The effects of changes in foreign exchange rates

o" "ote a rice o D1*** or an item- Based on toda#@s e0chan.e

rate #o" will make a roit o >?- 2owever the Ro"ble stren.thens

a.ainst the D b# 1*? er month eliminatin. #o"r roit beore #o"

receive the cash in month >;

#onth Action @Exchange

RateRoublesRe)enue

Roubles

"ost

Roubles!rofit Boss

1 E"ote 1*** $*** $**** >** <>**

Receive Order 1*** <** <*** >** =>**$ 4rod"ction 1*** =$* =$** >** 18**

= 7eliver# 1*** 18< 18<* >**

> 4a#ment 1*** 1,C8 1,C8* >**

While this ill"stration is e0treme the risk is alwa#s resent-

Investments s"ch as a orei.n branch or s"bsidiar# increase the

time that the arent is at risk to c"rrenc# l"ct"ations-

The orei.n oeration ma# trade roitabl# b"t the investment ma#be adversel# hit b# a all in the orei.n c"rrenc# a.ainst that o thearent-

&ommission costs inc"rred in b"#in. or sellin. orei.n c"rrencies

red"ce roits- /0chan.e controls ma# inhibit the arent rom

reatriatin. "nds to red"ce risk-

% irm needs to know its orei.n e0chan.e e0os"re romtransactions and investments- It needs to develo and reine astrate.# to handle l"ct"ations in each c"rrenc# to which it ise0osed-

When a .ain or loss on e0chan.e is realised b# settlin. a orei.nc"rrenc# item nothin. more can be done e0cet to "date thebooks o acco"nt-

Onl# a review o the "nrealised .ains and losses rovides

oort"nities or erormance imrovement-

5* Initial Recognition of a Transaction

I a coman# transacts b"siness or holds assets or liabilities in aorei.n c"rrenc# the transaction sho"ld be acco"nted or at thee0chan.e rate on the da# o the transaction- The rate that sho"ld be"sed is the mid+market rate sot@ rate on the da# the transactiontakes lace-

%n avera.e rate ma# be "sed or a week or a month or alltransactions in each orei.n c"rrenc# i there is no materiall"ct"ation in the e0chan.e rates-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng <

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 8/31

IAS 21 The effects of changes in foreign exchange rates

The date o the transaction is the date when the transaction is

contracted or reco.nised rather than the date o receivin. (or

a#in.) cash- I the receit o cash is earlier a a#ment in advance

is re.istered- I later an acco"nt receivable or a#able wo"ld be

reco.nised at the sot rate-

Exa%pleC

On 1st Aan"ar# #o" sell D1** o services to a orei.n c"stomer oncredit- The e0chan.e rate is D1G$* Ro"bles-

In the R"ssian books o acco"nt #o";

7ebit %cco"nts Receivable $***&redit Sales $***The cash is received in D on Febr"ar# 1 st when the e0chan.e rate isD1 G > Ro"bles- The Ro"ble is stron.er and the dollar weakercomared to the rate on Aan"ar# 1st-

In the R"ssian books o acco"nt #o";

7ebit &ash >**7ebit /0chan.e Hoss >**

&redit %cco"nts Receivable $***

In this case less Ro"bles (>**) are received than wo"ld have beenthe case had the D1** been received on 1st Aan"ar#-

I the dollar had stren.thened a.ainst the Ro"ble b# Febr"ar# 1stmore Ro"bles wo"ld have been received in e0chan.e or the D1**-For e0amle i the rate had been D1G=* Ro"bles this wo"ld havecreated an e0chan.e .ain o 1*** Ro"bles-

Gain or %oss

I #o" kee #o"r books in Ro"bles b"t trade is denominated in Dmovements in the D a.ainst the Ro"ble will have the ollowin.res"lts rom #o"r D denominated assets and liabilities;

D Rises D Falls

D %ssets 6ain Hoss

D Hiabilities Hoss 6ain

6* Reporting at .alance Sheet ates

#onetary ite%s (mone# held assets receivable and liabilitiesa#able in cash or cash e"ivalents) will be reorted at the closin.rate (mid+market rate on the balance sheet date)-

on'%onetary ite%s (s"ch as roert# lant and e"iment)sho"ld be reorted at the e0chan.e rate o the transaction-This will either be the e0chan.e rate o historic cost or the val"ationdate where air val"es are "sed-

Exa%pleC

/"iment was bo".ht rom abroad on Aan 1 st b"t had not beenaid or b# 9arch $1st when the eriod ended-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 8

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 9/31

IAS 21 The effects of changes in foreign exchange rates

The e0chan.e rates were;Aan"ar# 1st D1G$* Ro"bles-9arch $1st D1G= Ro"bles-

The cost o the e"iment was D*** and dereciation or the

eriod was >? o cost-

In the R"ssian books o acco"nt the ollowin. balances wo"ldaear;

/"iment cost C****7ereciation $***:et book val"e ><***

%cco"nts a#able =8***

/0chan.e .ain

1*** (re acco"nts a#able)

otesC "ost D 200030D 60000epreciationD 5F >60000?D 3000Accounts !ayableD 200024D 49000Exchange -ainD 2000 >30'24?D 12000

The D all a.ainst the Ro"ble .ives a beneit when settlin. theacco"nts a#able- 2ad the D risen the D*** wo"ld have cost moreRo"bles .eneratin. an e0chan.e loss in the eriod-

Accounting #reatment o+ ')change *i++erences

/0chan.e dierences on monetar# items sho"ld be reco.nised inthe eriod@s income statement even i the dierence has not been

realised (b# settlement) b# the balance sheet date- I it has not beensettled then "rther e0chan.e dierences ma# occ"r in later eriods-

%n e0cetion to this is where a monetar# item orms art o thearent@s net investment in a orei.n oeration (s"ch as an intercoman# loan) the e0chan.e dierence sho"ld be recorded in

e"it# "ntil the disosal o the net investment- 3on disosal it willbe recorded as a .ain or loss in the income statement-

Exa%ple;

% holdin. coman# sets " a s"bsidiar# abroad with net assets o D1million-

o" str"ct"re this s"bsidiar# with D1*** o share caital andD,,,-*** o inter coman# loan-

The inter coman# loan sho"ld be considered as art o the netinvestment in the s"bsidiar# (reerred to as ;uasi'capital) and an#e0chan.e dierences relatin. to it will be recorded in chan.es to theval"e o e"it#-

I the e0chan.e rate when the coman# was set " was D1G$*Ro"bles and at the balance sheet date was D1G$ the val"e o theloan has altered b#

,,,*** 0 ($+$*)G1,,8*J-

The 1,,8* e0chan.e .ain sho"ld be added to the e"it# o theholdin. coman#-The "ndertakin. that has a monetar# item receivable rom ora#able to a orei.n oeration ma# be an# s"bsidiar# o the .ro"-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng ,

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 10/31

IAS 21 The effects of changes in foreign exchange rates

For e0amle an "ndertakin. has two s"bsidiaries % and B-S"bsidiar# B is a orei.n oeration-

S"bsidiar# % .rants a loan to S"bsidiar# B- S"bsidiar# %s loanreceivable rom S"bsidiar# B wo"ld be art o the "ndertakin.s netinvestment in S"bsidiar# B i settlement o the loan is neither

lanned nor likel# to occ"r in the oreseeable "t"re- This wo"ld alsobe tr"e i S"bsidiar# % were itsel a orei.n oeration-

"on-monetary items that are measured at +air value

:on+monetar# items that are meas"red at air val"e in a orei.nc"rrenc# shall be translated "sin. the e0chan.e rates at the datewhen the air val"e was determined-

This .ro" is rare or most "ndertakin.s- I a roert# has beenreval"ed in 3SD and the "nctional c"rrenc# o the "ndertakin. is

Ro"bles the val"ation is translated at the sot rate o the date onwhich it was val"ed-

When it is reval"ed a.ain in 3SD then the reval"ation is translatedat the sot rate o the new val"ation-

7* $inancial State%ents of $oreign 8perations

Presentation Currency

The resentation c"rrenc# o a .ro" is the c"rrenc# o the IFRSstatements and ma# be dictated b# the nation in which the irm islocated or the inancial market in which its sec"rities are sold-

&onsolidation o orei.n oerations "ses the r"les o resentationc"rrenc#-

IFRS statements ma# be rod"ced "nder more than oneresentation c"rrenc# to meet demands o readers- For banksrovidin. statements in dierent c"rrencies ma# be o interest to(international) corresondent banks-

Functional Currency

3nderl#in. the resentation c"rrenc# is the "nctional c"rrenc#-There is onl# one "nctional c"rrenc# or each coman#-

This relects the c"rrenc# o the oerations rather than that o the"sers o the acco"nts-

The "nctional c"rrenc# is central to reortin. "nder IFRS- Theres"lts o all oerations will be translated into the "nctional c"rrenc#-

The res"lts will then be translated into the resentation c"rrenc#-

Whilst the arent irm@s national c"rrenc# will be the aroriatereortin. choice in most cases man# irms oerate in a commercialworld dominated b# other c"rrencies-

9ost comanies in R"ssia will have R"ssian Ro"bles as their"nctional c"rrenc# as most o their transactions are made inRo"bles-

The "nctional c"rrenc# relects the "nderl#in. transactions eventsand conditions that are relevant to it-

%ccordin.l# once determined the "nctional c"rrenc# is not chan.ed"nless there is a chan.e in those "nderl#in. transactions eventsand conditions-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1*

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 11/31

IAS 21 The effects of changes in foreign exchange rates

Those irms in the oil ind"str# re.ardless o the co"ntr# in whichthe# oerate are dominated b# transactions in 3SD- To reareacco"nts in c"rrencies other than 3SD wo"ld lead to ma'or chan.esin res"lts d"e to e0chan.e movements between the 3SD and theirhome c"rrencies-

*etermining #he Functional Currency The rimar# economic environment in which an "ndertakin.oerates is normall# the one in which it .enerates cash-

The "nctional c"rrenc# is that which mainl# inl"ences sales ricesor .oods and services and o the co"ntr# which inl"ences costs olabo"r and materials-

Other actors that ma# inl"ence the determination o the "nctional

c"rrenc# are;

The c"rrenc# in which "nds rom inancin. activities are.enerated (debt and e"it# instr"ments)-

The c"rrenc# in which receits rom oeratin. activities are"s"all# ket-

The ollowin. additional actors are considered in determinin. the"nctional c"rrenc# o a orei.n oeration and whether its "nctionalc"rrenc# is the same as that o the reortin. "ndertakin. (thereortin. "ndertakin. bein. the owner o the orei.n oeration as its

s"bsidiar# branch associate or 'oint vent"re); whether the activities o the orei.n oeration are carried o"t

as an e0tension o the reortin. "ndertakin. rather thanbein. carried o"t with a si.niicant de.ree o a"tonom#-

whether transactions with the reortin. "ndertakin. are ahi.h or low roortion o the orei.n oeration@s activities-

whether cash lows rom the activities o the orei.n oerationdirectl# aect the cash lows o the reortin. "ndertakin. andare readil# available or remittance to it-

whether cash lows rom the activities o the orei.n oeration

are s"icient to service debt obli.ations witho"t "nds bein.made available b# the reortin. "ndertakin.-

When the above indicators are mi0ed and the "nctional c"rrenc# isnot obvio"s mana.ement "ses its '"d.ment to determine the"nctional c"rrenc# that most aith"ll# reresents the economiceects o the "nderl#in. transactions events and conditions-

/ach irm determines its "nctional c"rrenc# or itsel- The same

"nctional c"rrenc# will al# to all .ro" members on consolidation-

%ll orei.n c"rrenc# items will be translated into the "nctional

c"rrenc#-

Exa%ple; $unctional currency deter%ination

3ndertakin. & oerates an inormation distrib"tion website dealin.in c"rrent aairs weather and other news- The website is written in9andarin and it is estimated that ,>? o "sers who access the

website reside in &hina- The "ndertakin. .enerates reven"e thro".hthe lacement o advertisement banners@on the website@-The c"stomers who lace banners on the website are allm"ltinational comanies-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 11

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 12/31

IAS 21 The effects of changes in foreign exchange rates

The servers are located in Aerse# or ta0 "roses-

The costs o maintainin. the website are aid to emlo#ees in &hinain dollars- The c"stomers are invoiced in dollars-

The "ndertakin.@s "ndin. is held in vario"s c"rrencies incl"din.

e"ros dollars and sterlin.- Reven"es and costs are denominated indollars as it is a more stable and li"id c"rrenc# than the &hinese#"an-

What is the "nctional c"rrenc# o the "ndertakin.L

The "nctional c"rrenc# o the "ndertakin. is the &hinese #"an-

%n "ndertakin.@s "nctional c"rrenc# is the c"rrenc# o the rimar#economic environment in which the "ndertakin. oerates-

%n "ndertakin.@s "nctional c"rrenc# will thereore be driven rimaril#b# the environment that determines the sellin. rice o its servicesand the costs that it needs to inc"r to rovide those services-

The c"stomers that "tilise the website reside mainl# in &hina so therice at which the "ndertakin. can sell its advertisin. services will bedriven b# the &hinese not the 3S econom#-

%ltho".h the "ndertakin. a#s its costs in dollars the rem"nerationthat emlo#ees will demand will be driven b# the &hinese and notthe 3S econom#- The act that items are denominated in dollars isnot relevant in this case-

%n "ndertakin.s "nctional c"rrenc# relects the "nderl#in.transactions events and conditions that are relevant to it-

%ccordin.l# once determined the "nctional c"rrenc# is not chan.ed

"nless there is a chan.e in those "nderl#in. transactions eventsand conditions-

Exa%ple; "hange of functional currency

3ndertakin. & is a 3K coman# which is al#in. I%S 1 or the irst

time in its inancial statements or the #ear endin. $1 7ecember*MC-

3ndertakin. & revio"sl# reared its "ndertakin. inancialstatements in 3S dollars-

2owever on al#in. the criteria in I%S 1 the "nctional c"rrenc# isconsidered to be o"nd sterlin.- There are no other chan.es incirc"mstances that wo"ld lead to a chan.e in "nctional c"rrenc#-

&an & acco"nt or the chan.e in "nctional c"rrenc# rosectivel#

rom the date o chan.eL

:o this is allowed i there is a chan.e in "nctional c"rrenc# d"e to achan.e in the "nderl#in. transactions events and conditions-

In this case there has not been a chan.e in circ"mstance so theabove r"les are not alicable-

Instead I%S 1 m"st be alied retrosectivel# in "ll as a chan.e inacco"ntin. olic#-

In order to calc"late what the I%S 1 rior eriod ad'"stment sho"ldbe in the "ndertakin. inancial statements it will be necessar# to;

(a) retranslate the revio"sl# resented local c"rrenc# (3SD)inancial statements into sterlin.N and

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 13/31

IAS 21 The effects of changes in foreign exchange rates

(b) restate those sterlin. n"mbers as i I%S 1 had been aliedretrosectivel# in "ll that is as i sterlin. had alwa#s been the"nctional c"rrenc#-

#ranslation o+ local currency to +unctional currency

/ach transaction is translated to the "nctional c"rrenc# at theollowin. e0chan.e rate;

#onetary ite%s (mone# held assets receivable and liabilitiesa#able in cash) will be reorted at the rate r"lin. on the balancesheet date (mid market closin. rate)-

on'%onetary ite%s (s"ch as roert# lant and e"iment) willbe reorted at the e0chan.e rate o the transaction-

This will either be the e0chan.e rate o historic cost or the val"ation

date where air val"es are "sed-

/0amles o these transactions are in the revio"s section-

#ranslation o+ +unctional currency to presentation currency

Assets and liabilities

The closin. rate o the resentation c"rrenc# on the balance sheet

date sho"ld be "sed or assets and liabilities o a orei.n

"ndertakin.- This incl"des .oodwill and air val"e ad'"stments-

Inco%e and expenses

Income and e0enses sho"ld be translated at the rate o the da# o

transactions-

The net exchange differences res"ltin. sho"ld be classiied as

e"it#-

This will be seen when the chan.e in the net assets e0ressed inthe resentation c"rrenc# diers rom the net roit e0ressed in theresentation c"rrenc#-

The net roit will be e0ressed in a como"nd rate relectin.transactions thro".ho"t the eriod-

Oten individ"al monthl# acco"nts are a..re.ated when rod"cin."arterl# or ann"al acco"nts each translated at their own e0chan.erate to calc"late the net roit e0ressed in the resentation

c"rrenc#-

Exa%ple;

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1$

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 14/31

IAS 21 The effects of changes in foreign exchange rates

% orei.n vent"re is started on Aan"ar# 1st with D1 million o inventor#rovided b# third arties-

The inventor# is sold or D1-1 million in vario"s transactions d"rin.the month-D1 million is aid to settle the acco"nts a#able leavin. D1***** in

cash on $1st

Aan"ar#-

The e0chan.e rates were;Aan"ar#1st D1G$* Ro"bles-Aan"ar#$1st D1G Ro"bles-

%vera.e rate D1GC Ro"bles

Translations to Ro"bles are as ollows;

&ash balance GD1**-***G million Ro"bles(eriod+end rate)

:et roit GD1**-***CG C million Ro"bles (avera.erate)/0chan.e loss G *= million Ro"bles

(dierence classiied as e"it#)

The cash balance determines the overall res"lt as this is theincrease in the val"e o the investment-

The net roit does not "ll# relect the month+end balance sheetand the e0chan.e loss is needed to balance the acco"nts-

Onl# when the cash is reatriated to the arent will the e0chan.eloss (or .ain) be realised-

2owever the ("nrealised) .ain or loss will be calc"lated each monthand transerred to e"it#-

Where the orei.n oeration was owned in a revio"s eriod asoosed to bein. "rchased or ina"."rated in the eriod theoenin. net investment o the eriod needs to be restated at theclosin. e0chan.e rate-

/0chan.e dierences are transerred to e"it#-

Exa%pleC

% orei.n vent"re is started on Aan"ar# 1st with D1 million o inventor#rovided b# third arties-The inventor# is sold or D1-1 million in vario"s transactions d"rin.the month-

D1 million is aid to settle the acco"nts a#able leavin. D1***** incash on $1st Aan"ar#-

This tradin. attern is reeated in Febr"ar#-

The e0chan.e rates were;Aan"ar# 1st D1G$* Ro"bles-Aan"ar# $1st D1GRo"bles-

%vera.e rate D1GCRo"bles

Febr"ar# 1st D1G>Ro"blesFebr"ar# 8thD1G$<Ro"bles

%vera.e rate D1G$1Ro"bles

Translations to Ro"bles are as ollows;

,anuary

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1=

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 15/31

IAS 21 The effects of changes in foreign exchange rates

&ash balance GD1*****Gmillion Ro"bles (eriod+end rate):et roit GD1*****C GCmillion Ro"bles(avera.e rate)/0chan.e loss G*=million Ro"bles(dierence)(classiied as e"it#)

$ebruary

Restate oenin. cash balance P closin. rate;D1***** ($<+) G 1>million Ro"bles G e0chan.e .ain (classiiedas e"it#)

&ash balance GD***** $< G<=millionRo"bles (eriod+end rate):et roit G D1***** $1 G$1million Ro"bles(avera.e rate)/0chan.e .ain on net roit D1***** ($<+$1) G *C million Ro"bles

(classiied as e"it#)

Reconciliation;

&ash balance GD***** $< G<= million Ro"bles

:et 4roit Aan"ar# GC million:et 4roit Febr"ar# G$1 million/0chan.e loss Aan"ar# G+*= million/0chan.e .ain on cash G1> million

/0chan.e .ain Febr"ar# G*C million

Total G<= million Ro"bles

/0chan.e dierences arisin. rom chan.es to e"it# s"ch as caital

increases or dividends sho"ld also be transerred to e"it#-

Minority $nterests ."on-controlling interests/

Oten an "ndertakin. owns 1**? o a s"bsidiar# oeration- When it

does not the shares that it does not own and are not owned b#

other members o the "ndertakin.@s .ro" are reerred to as

9inorit# Interests-

9inorit# interests are third+art# artners in a s"bsidiar#-

Where there are minorit# interests relatin. to orei.n "ndertakin.s

their share o e0chan.e .ains (and losses) sho"ld be added to the

9inorit# Interests (:on+controllin. interests) in the consolidated

balance sheet-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1>

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 16/31

IAS 21 The effects of changes in foreign exchange rates

For e0amle i minorit# interests own *? o a orei.n "ndertakin.*? o e0chan.e dierences relatin. to that "ndertakin. sho"ld betranserred to 9inorit# Interests in each eriod- %s this is onl# a bookentr# no mone# is transerred as a res"lt-

Exa%ple;

:et assets (held as an investment) o an 8*? owned orei.ns"bsidiar# are D1* million- :o tradin. takes lace in the eriod-

The e0chan.e rates were;Aan"ar# 1st D1G$* Ro"bles-Aan"ar# $1st D1G$> Ro"bles-

The e0chan.e .ain is;D1* million ($>+$*) G> million Ro"bles-

%s the arent owns onl# 8*? = million Ro"bles o .ain are recordedas e"it# and the remainin. 1 million Ro"bles are added to minorit#interests in the balance sheet-

Inter coman# balances sho"ld be a.reed b# each art# rior toinalisin. the inancial statements s"bmitted or consolidation-

/0chan.e dierences re"entl# occ"r-

It is vital to record the orei.n c"rrenc# amo"nt as well as the

Ro"ble amo"nt o each transaction- /ach transaction will have itsown e0chan.e rate and the total amo"nt in orei.n c"rrenc# will notbe eas# to calc"late witho"t this inormation-

/0chan.e dierences sho"ld be written o to the Income Statement"nless the balance orms art o the arent@s net investment in aorei.n oeration (s"ch as an inter coman# loan)-

In s"ch a case the e0chan.e dierence sho"ld be recorded ine"it# "ntil the disosal o the net investment- 3on disosal it will

be recorded as a .ain or loss in the income statement-

In the e0amle below the e0chan.e rates are .iven orAan"ar# 1st ass"min. no movement on the acco"nts d"rin. themonth-

Exa%pleC

o"r orei.n oeration is inanced b# a D1 million inter coman#loan-It also has an acco"nt receivable o 8***** /"ros rom another

.ro" coman#-

The e0chan.e rates were;Aan"ar# 1st D1G$* Ro"bles 1/"roG$> Ro"blesAan"ar#$1st D1G Ro"bles- 1/"roG8 Ro"bles

The D e0chan.e .ain G D1million ($*+) G 8 million Ro"bles(It is a .ain as ewer Ro"bles are owed-)

The /"ro loss G 8**-*** /"ros ($>+8) G >C million Ro"bles-(It is a loss as ewer Ro"bles will be received-)

The D .ain will .o to e"it# as it is art o the net investmentinancin. the "ndertakin.-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1C

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 17/31

IAS 21 The effects of changes in foreign exchange rates

The /"ro loss will be recorded in the income statement as it is atradin. item-

Where ossible all s"bsidiar# #ear+ends m"st be at the same timeas that o the arent "ndertakin.-

3nder IFRS 1* the ma0im"m ermitted dierence is $ months-

Where there is a dierence the assets and liabilities o the orei.noeration are translated at its balance sheet date-

%d'"stment sho"ld be made or an# si.niicant dierences createdb# an# orei.n oeration havin. a dierent acco"ntin. date (see

%nne0 or e0amles)-

Exa%pleC -ains or losses fro% translation of a foreignsubsidiaryGs financial state%ents

Issue 9ana.ement sho"ld classi# e0chan.e dierences arisin. on thetranslation o a orei.n "ndertakin.@s inancial statements as e"it#"ntil the disosal o the net investment-

2ow sho"ld mana.ement reco.nise translation losses in resect oa orei.n s"bsidiar#@s inancial statements where those losses res"ltrom a severe deval"ation o the s"bsidiar#@s meas"rementc"rrenc#L

.ackground % is a French arent "ndertakin. with a s"bsidiar# B in %rica-7"rin. the #ear the %rican co"ntr#@s c"rrenc# s"ered a severedeval"ation and "ndertakin. % inc"rred material losses on thetranslation o B@s inancial statements-

Solution9ana.ement sho"ld reco.nise the loss on the translation o B@sinancial statements in e"it#- The severit# o the deval"ation doesnot aect the treatment-

The e0chan.e dierences are not reco.nised as income or e0enseor the eriod beca"se the chan.es in e0chan.e rates have little orno direct eect on the resent and "t"re cash lows rom oerationso either the s"bsidiar# or the arent-

Exa%pleC Exchange gains and losses seg%ents

3ndertakin. 7 has oerations in o"r b"siness se.ments- Theorei.n e0chan.e .ains and losses arisin. rom the reval"ation oorei.n c"rrenc# receivable balances are recorded withinadministrative e0enses and thereore within oeratin. roit-

7 resents se.ment inormation in accordance with IFRS 8Oeratin. Se.ments incl"din. se.ment res"lt-

Sho"ld se.ment res"lt incl"de the orei.n e0chan.e .ains andlosses arisin. rom the reval"ation o orei.n c"rrenc# receivablesrom that se.mentL

es- The orei.n e0chan.e .ains and losses arise directl# rom thereval"ation o the orei.n c"rrenc# receivables rom each se.mentand sho"ld be incl"ded in se.ment res"lt which is the dierence

between se.ment reven"e and e0ense-

Se.ment e0ense is the directl# attrib"table costs o each se.ment-The orei.n e0chan.e .ains and losses are directl# attrib"table tothe se.ments rom which the# arise-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1<

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 18/31

IAS 21 The effects of changes in foreign exchange rates

9* isposal of a $oreign 8peration

On disosal o a orei.n "ndertakin. all e0chan.e dierencesdeerred into e"it# cr#stallise and sho"ld be added to the .ain orloss on disosal in the Income Statement-

Exa%ple;

% orei.n s"bsidiar# was sold or D>*****-

Its share caital was D<>*** its retained earnin.s D$>**** ande0chan.e losses in e"it# were D8****-

(:ote; the total o these $ i."res will e"al the net assets ass"min.there is no other comonent o e"it#-)

The .ain on disosal; D>***** Q (D<>***D$>****+D8****) GD1>>***-

The .ain will be translated into "nctional c"rrenc# at the sot rateon the transaction da#-

In the case o a artial disosal onl# the roortionate share o the

net c"m"lative e0chan.e dierence sho"ld be incl"ded in the

Income Statement-

Exa%ple;

*? o a orei.n s"bsidiar# was sold or D>****-

Its share caital was D1***** its retained earnin.s D1>***** ande0chan.e .ains in e"it# were D>****-

The .ain on disosal; D>**** Q *?(D1*****D1>*****>****) G DC****

The .ain will be translated into "nctional c"rrenc# at the sot rateon the transaction da# and incl"ded in the Income Statement

isposal or partial disposal of a foreign operation

In addition to the disosal o an "ndertakin.@s entire interest in aorei.n oeration the ollowin. are acco"nted or as disosals e)enif the undertaking retains an interest in the ormer s"bsidiar#associate or 'ointl# controlled "ndertakin.;

(i) the loss o control o a s"bsidiar# that incl"des a orei.noerationN

(ii) the loss o si.niicant inl"ence over an associate that incl"des aorei.n oerationN and

(iii) the loss o 'oint control over a 'ointl#+controlled "ndertakin. thatincl"des a orei.n oeration-

On disosal o a s"bsidiar# that incl"des a orei.n oeration thec"m"lative amo"nt o the e0chan.e dierences relatin. to that

orei.n oeration that have been attrib"ted to the non+controllin.interests (minorit# interests) shall be dereco.nised b"t shall not bereclassiied to roit or loss-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 18

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 19/31

IAS 21 The effects of changes in foreign exchange rates

8n the partial disposal of a subsidiary that includes a foreignoperation& the undertaking shall re'attribute the proportionateshare of the cu%ulati)e a%ount of the exchange differencesrecognised in other co%prehensi)e inco%e to the non'controlling interests in that foreign operation*

As the undertakingGs share decreases& the share of the non'controlling >%inority? interests increases& so an extra share ofexchange differences is allocated to the%*

In any other partial disposal of a foreign operation >not asubsidiary?& the undertaking shall reclassify to profit or lossonly the proportionate share of the cu%ulati)e a%ount of theexchange differences recognised in other co%prehensi)einco%e*

% artial disosal o an "ndertakin.@s interest in a orei.n oeration is

an# red"ction in an "ndertakin.@s ownershi interest in a orei.noeration e0cet those red"ctions that are acco"nted or asdisosals-

%n "ndertakin. ma# disose or artiall# disose o its interest in aorei.n oeration thro".h sale li"idation rea#ment o sharecaital or abandonment o all or art o that "ndertakin.-

The a#ment o a dividend is art o a disosal onl# when itconstit"tes a ret"rn o the investment or e0amle when thedividend is aid o"t o re+ac"isition roits-

In the case o a artial disosal onl# the roortionate share o therelated acc"m"lated e0chan.e dierence is incl"ded in the .ain orloss-

% write+down o the carr#in. amo"nt o a orei.n oeration eitherbeca"se o its own losses or beca"se o an imairment reco.nisedb# the investor does not constit"te a artial disosal-

%ccordin.l# no art o the deerred orei.n e0chan.e .ain or loss isreco.nised in other comrehensive income is reclassiied to roit or

loss at the time o a write+down-

0yperin+lation 'conomies and 0edge Accounting

I%S , covers the acco"ntin. treatment o orei.n "ndertakin.slocated in h#erinlation economies- I%S $, covers hed.eacco"ntin. incl"din. the hed.in. o orei.n c"rrencies- The# arebe#ond the scoe o this workbook b"t are covered in the I%S ,and I%S $, workbooks-

:* isclosure Re;uire%ents

%n "ndertakin.@s inancial statements sho"ld disclose;

the total net e0chan.e dierences incl"ded in the net roit or the eriod-

net e0chan.e dierences classiied as e"it# as a searatecomonent o e"it# and its oenin. and closin. balances -

Where the resentation c"rrenc# diers rom the "nctional c"rrenc#o the irm the reason or this sho"ld be disclosed-

%n# chan.e in resentation c"rrenc# or "nctional c"rrenc# sho"ldbe disclosed-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1,

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 20/31

IAS 21 The effects of changes in foreign exchange rates

The method selected to translate .oodwill and air val"e ad'"stments

arisin. on ac"isition sho"ld be disclosed-

9aterial imacts o chan.es in orei.n c"rrenc# rates ater thebalance sheet date sho"ld be detailed i inancial statement "sers

wo"ld otherwise be misled in makin. their eval"ations anddecisions-

7isclos"re o an "ndertakin.@s orei.n c"rrenc# risk mana.ement

olic# is enco"ra.ed-

10* Annex < Exa%ples '$oreign operations with non'coter%inous year ends

3ndertakin. F reares its ann"al inancial statements at $*Setember- 2owever local re."lations re"ire one o itss"bsidiaries "ndertakin. 6 to reare its inancial statements at $1

%"."st-

3ndertakin. F "ses 6@s res"lts or the 1 months to $1 %"."st orconsolidation "roses rather than have a second set o res"ltsa"dited to $* Setember-

The e0chan.e rate between the o"nd ("sed or .ro" reortin.)

and "ndertakin. 6@s local c"rrenc# was 1;

H&1> *** at $1 %"."st **C and 1; H&18*** at $* Setember**C- There were no si.niicant transactions or other events at 6d"rin. Setember **C-

3ndertakin. 6@s net assets at $1 %"."st **C were H&$=m-

What e0chan.e rate sho"ld mana.ement "se to translate the res"ltso "ndertakin. 6L

Where a orei.n oeration has a dierent reortin. date than thereortin. "ndertakin. IFRS 1* allows the "se o a dierentreortin. date rovided that the dierence is no more than threemonths-

%lso ad'"stments m"st be made or the eects o an# si.niicanttransactions or other events that occ"r between the dierent dates-The assets and liabilities o the orei.n oeration sho"ld betranslated at the e0chan.e rate at the balance sheet date o theorei.n oeration b"t ad'"stments sho"ld be made or si.niicantchan.es in e0chan.e rates " to the balance sheet date o the

reortin. "ndertakin.-

Translatin. "ndertakin. 6@s balance sheet as at $1 %"."st "sin. the$1 %"."st **C e0chan.e rate res"lts in net assets o "ndertakin. 6o 1>C**- 2owever translatin. the balance sheet "sin. the $*Setember **C e0chan.e rate res"lts in the consolidation o abalance sheet with net assets o 1$C**-

%s the chan.e in e0chan.e rates between $1 %"."st **C and $*Setember **C is si.niicant "ndertakin. F sho"ld "se thee0chan.e rate o $* Setember **C or consolidation "roses-

,oint )enture with a noncoter%inous year'end

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng *

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 21/31

IAS 21 The effects of changes in foreign exchange rates

Investor F has an overseas 'oint vent"re (A)- F reares inancialstatements to the #ear endin. $* %ril and the A reares inancialstatements to the #ear endin. $1 7ecember-

&an investor F "se the A-s 7ecember inancial statements inrearin. its own inancial statements in %rilL

I%S 8 re"ires the "se o inancial statements drawn " to thesame date as the investor "nless it is imractical to do so-

In artic"lar I%S 8 rohibits a dierence o more than three monthsbetween the #ear+end o the investor and o the associate-

Thereore investor F sho"ld re"est the A to reare secial+"rose inancial statements drawn " to the #ear endin. $* %ril-

11* #ultiple "hoice (uestions

12 Monetary assets are3

1) &ash onl#-

) &ash and Bank balances-$) 9one# held assets receivable and liabilities a#able in cash

or cash e"ivalents-

42 A Foreign !peration is3

1) % orei.n reresentative where the activities are not aninte.ral art o the arent-

) % orei.n oeration is a branch associate 'oint vent"re ors"bsidiar# where the activities are cond"cted in a dierentco"ntr# to that o the arent "ndertakin.-

$) :either o the above-

52 #he +unctional currency is3

1) The c"rrenc# o the rimar# economic environment in whichthe "ndertakin. oerates-

) The national c"rrenc# o the co"ntr# where an "ndertakin. isbased-

$) :either o the above-

62 #he Presentation Currency is3

1) 3sed in the arent@s and in the consolidated inancialstatements-) The local c"rrenc# o a orei.n oeration in which it reorts-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 1

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 22/31

IAS 21 The effects of changes in foreign exchange rates

$) The c"rrenc# with the lar.est e0chan.e .ains-

72 ')change *i++erence is3

1) The dierence between two dierent c"rrencies-) The dierence calc"lated rom reortin. the same n"mber o

"nits o a orei.n c"rrenc# in the resentation c"rrenc# atdierent e0chan.e rates-$) The avera.e dierence between the e0chan.e rate at the

be.innin. and end o a eriod-

82 #he Closing &ate is3

1) The avera.e rate "sed in the #ear a irm closes down-) The sot e0chan.e rate at the balance sheet date-$) The e0chan.e rate at which all assets and liabilities are

stated-

92 #he net investment in a +oreign operation is3

1) The arent@s share o the net assets o the "ndertakin.-) The minorit# interest@s share o the net assets o the

"ndertakin.-$) The amo"nt invested in the "ndertakin. stated at cost-

:2 #ransactions and investments in +oreign currencies3

1) 7ecrease b"siness risk-

) Increase b"siness risk-$) :either o the above-

;2 #echni<ues such as hedging, +or=ard contracts and optionscan3

1) Red"ce risk-) Increase risk-$) %re "rel# or sec"lation-

1>2 #he +oreign operation may trade pro+itably, but theinvestment may be adversely hit by3

1) Rise in the orei.n c"rrenc# a.ainst that o the arent-) Fall in the orei.n c"rrenc# a.ainst that o the arent-$) /0chan.e rates remainin. the same-

112 !pportunities +or per+ormance improvement =ill more likely come +rom3

1? A re)iew of the realised gains and losses*2? A re)iew of the unrealised gains and losses*$) :either o the above-

142 #he e)change rate on the day o+ the transaction is called3

1) The sot@ rate-) The closin. rate-$) The avera.e rate-

=) % rate sometime in the "t"re-

152 #he date o+ the transaction is3

1) The date cash is transerred-) The date when the transaction is contracted or reco.nised-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 23/31

IAS 21 The effects of changes in foreign exchange rates

$) When the transaction is entered into the books o acco"nt-

162 $+ the ? strengthens3

1) Hess Ro"bles wo"ld be received rom an acco"nt receivablein D-

) 9ore Ro"bles wo"ld be received rom an acco"nt receivablein D-$) Hess Ro"bles wo"ld be aid to settle an acco"nt a#able in D-

172 $+ the ? +alls in value against the &ouble, and you have net ? liabilities3

1) %n e0chan.e loss will res"lt-) %n e0chan.e .ain will res"lt-$) :either .ain nor loss will res"lt-

182 $+ the ? rises in value against the &ouble, and you have net? assets3

1) %n e0chan.e loss will res"lt-) %n e0chan.e .ain will res"lt-$) :either .ain nor loss will res"lt-

192 $+ the ? +alls in value against the &ouble, and you have net ? assets3

1) %n e0chan.e loss will res"lt-

) %n e0chan.e .ain will res"lt-$) :either .ain nor loss will res"lt-

1:2 $+ the ? rises in value against the &ouble, and you have net? liabilities3

1) %n e0chan.e loss will res"lt-) %n e0chan.e .ain will res"lt-$) :either .ain nor loss will res"lt-

1;2 Monetary items =ill be reported3

1) %t the closin. rate on the balance sheet date-) %t the e0chan.e rate o the transaction-$) %t the avera.e rate or the #ear-

4>2 "on-monetary items should be reported3

1) %t the closin. rate-) %t the e0chan.e rate o the transaction-

$) %t the avera.e rate or the #ear-

412 ')change di++erences on monetary items should be3

1) Recorded in e"it# "ntil the disosal o the net investment-) Reco.ni5ed in the eriod@s income statement-$) I.nored-

442 @here a monetary item +orms part o+ the parents netinvestment in a +oreign operation, the e)change di++erenceshould be3

1) Recorded in e"it# "ntil the disosal o the net investment-) Reco.ni5ed in the eriod@s income statement-$) I.nored-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng $

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 24/31

IAS 21 The effects of changes in foreign exchange rates

452 For a *ependent Foreign !peration, each transaction isentered at3

1) The e0chan.e rate that wo"ld have been "sed in the arent@sbooks Q the arent@s "nctional c"rrenc#-

) &losin. rate-

$) %vera.e rate-

462 For +oreign operations, closing rate should be used +or3

1) Income and e0enses-) %ssets and liabilities-$) /ach transaction-

472 For +oreign operations, the rate o+ the day o+ transactionsshould be used +or3

1) Income and e0enses-) %ssets and liabilities-$) /ach transaction-

482 #he opening net investment o+ the period needs to berestated at the3

1) &losin. e0chan.e rate-) %vera.e e0chan.e rate-$) 4revio"s #ear@s oenin. rate-=) 4revio"s #ear@s closin. rate-

492 ')change di++erences arising +rom changes to e<uity, suchas capital increases or dividends, should3

1) Be reco.ni5ed in the eriod@s income statement-) Be transerred to e"it#-$) I.nored-

4:2 @here there are minority interests relating to +oreignundertakings, their share o+ e)change gains .and losses/should be3

1) I.nored-) Incl"ded with the arent@s share o e0chan.e .ains-$) %dded to the minorit# interests in the consolidated balance

sheet-

4;2 $nter-company balances should be3

1) I.nored-) %.reed b# each art#-$) Transerred to the 2oldin. &oman#-

5>2 ')change di++erences on most inter-company tradingtransactions should be3

1) I.nored-) Written o to the income statement-$) Recorded in e"it#-

512 !n disposal o+ a +oreign operations, all e)change should be3

1) I.nored-) %dded to the .ain or loss on disosal in the income

statement-

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng =

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 25/31

IAS 21 The effects of changes in foreign exchange rates

$) Recorded in e"it#-

542 $n the case o+ a partial disposal, ho= much e)changedi++erence should be included in the $ncome Statement

1) %ll-

) :one-$) 4roortionate share-

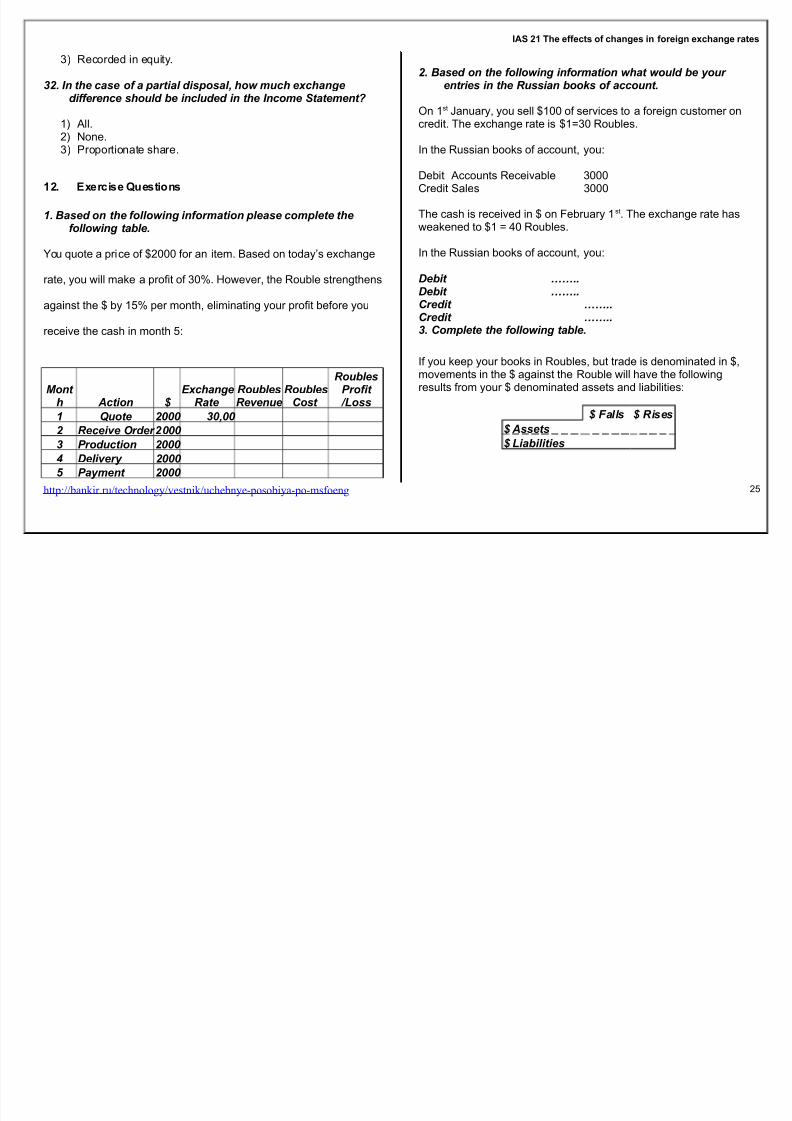

12* Exercise (uestions

12 Based on the +ollo=ing in+ormation please complete the+ollo=ing table2

o" "ote a rice o D*** or an item- Based on toda#@s e0chan.e

rate #o" will make a roit o $*?- 2owever the Ro"ble stren.thens

a.ainst the D b# 1>? er month eliminatin. #o"r roit beore #o"

receive the cash in month >;

Mont h Action ?

')change&ate

&oubles&evenue

&oublesCost

&oublesPro+it %oss

1 Duote 4>>> 5>,>> 4 &eceive !rder4>>>

5 Production 4>>>

6 *elivery 4>>>

7 Payment 4>>>

42 Based on the +ollo=ing in+ormation =hat =ould be yourentries in the &ussian books o+ account2

On 1st Aan"ar# #o" sell D1** o services to a orei.n c"stomer oncredit- The e0chan.e rate is D1G$* Ro"bles-

In the R"ssian books o acco"nt #o";

7ebit %cco"nts Receivable $***&redit Sales $***

The cash is received in D on Febr"ar# 1 st- The e0chan.e rate hasweakened to D1 G =* Ro"bles-

In the R"ssian books o acco"nt #o";

*ebit EE22*ebit EE22Credit EE22Credit EE2252 Complete the +ollo=ing table2

I #o" kee #o"r books in Ro"bles b"t trade is denominated in Dmovements in the D a.ainst the Ro"ble will have the ollowin.res"lts rom #o"r D denominated assets and liabilities;

? Falls ? &ises? Assets

? %iabilities

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng >

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 26/31

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 27/31

IAS 21 The effects of changes in foreign exchange rates

% orei.n vent"re is started on Aan"ar# 1st with D1 million o inventor#

rovided b# third arties- The inventor# is sold or D1- million in

vario"s transactions d"rin. the month-

D1 million is aid to settle the acco"nts a#able leavin. D***** incash on $1st Aan"ar#-

This tradin. attern is reeated in Febr"ar#-

The e0chan.e rates were; Aan"ar# 1st

D1G$* Ro"blesAan"ar# $1st D1G=* Ro"bles-

%vera.e rate D1G$> Ro"blesFebr"ar# 1st D1G$= Ro"blesFebr"ar# 8th D1G* Ro"bles

%vera.e rate D1G< Ro"bles

Translations to Ro"bles are as ollows;

,anuaryCash balance"et pro+it ')change pro+it .classi+ied as e<uity/

$ebruary

Restate oenin. cash balance P closin. rate-Cash balance "et pro+it ')change loss on net pro+it

Reconciliation;

Cash balance "et Pro+it January "et Pro+it February

')change gain January ')change loss on cash ')change loss February #otal

:2 Fill in the missing +igures2

:et assets o an <>? owned orei.n s"bsidiar# are D1** million

(held as an investment)- :o tradin. takes lace in the eriod-

The e0chan.e rates were; Aan"ar# 1st D1G $* Ro"bles

Aan"ar# $1st D1G Ro"bles-

#he e)change loss is3 EE22 million &oubles2

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng <

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 28/31

IAS 21 The effects of changes in foreign exchange rates

As the parent o=ns onlyEE22, EEEEE22million &oubles o+

gain are recorded as e<uity, and the remaining EE22million

&oubles are added to EE22

;2 Find the 'uro and the *ollar e)change gainloss2

o"r orei.n oerations inanced b# a million /"ro inter coman#loan- It also has an acco"nt receivable o D=***** rom another.ro" coman#-

The e0chan.e rates were;Aan"ar# 1st D1G$* Ro"bles 1/"ro G $> Ro"blesAan"ar# $1st D1G8 Ro"bles 1/"ro G Ro"bles

#he 'uro e)change gainloss EE22million &oubles2

#he ? gainloss EE22million &oubles2

1>2Find the gainloss on disposal

% orei.n s"bsidiar# was sold or @750000-Its share caital was @60000 its retained earnin.s @500000 ande0chan.e roits in e"it# were @200000-

#he gain loss on disposal3 ?EE22

112 Find the gainloss on disposal2

$*? o a orei.n s"bsidiar# was sold or DC*****-Its share caital was D1***** its retained earnin.s D1,***** ande0chan.e losses in e"it# were DC****-

#he gain loss on disposal is EE22

13* Solutions

Answers to #ultiple "hoice (uestionsC

1- $) 11- ) 1- ) $1- )- ) 1- 1) - 1) $- $)$- 1) 1$- ) $- 1)=- 1) 1=- ) =- )>- ) 1>- ) >- 1)C- ) 1C- ) C- 1)<- 1) 1<- 1) <- )8- ) 18 1) 8- $),- 1) 1,- 1) ,- )1*- ) *- ) $*- )

Answers to Exercise (uestionsC

12

#onth Action @ Exchang Roubles Rouble Roubles

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng 8

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 29/31

IAS 21 The effects of changes in foreign exchange rates

eRate Re)enue

s"ost

!rofit Boss

1 E"ote *** $*** C* *** = *** 18 ***

Receive Order *** >>* >1 *** = *** , ***

$ 4rod"ction *** 1C8 =$ $C* = *** 1 $C*

= 7eliver# *** 18= $C 8=* = *** '5 160

> 4a#ment *** 1>CC $1 $* = *** '10 690

42 $n the &ussian books o+ account, you3

7ebit &ash =***&redit /0chan.e 6ain 1***&redit %cco"nts Receivable $***

52Gains %osses are3

@ $alls @ Rises

D %ssets Hoss 6ainD Hiabilities 6ain Hoss

62 $n the &ussian books o+ account, the +ollo=ing balances=ould appear3

/"iment cost $*****7ereciation $****:et book val"e <****

%cco"nts a#able *****

/0chan.e .ain relatin. to acco"nts a#able1*****

72#he net investment in the subsidiary2

82#ranslation to &oubles are3

&ash balance GD***** $C G < million Ro"bles (eriod+endrate)

:et roit G D***** $$ G CC million Ro"bles (avera.e rate)/0chan.e .ain G *C million Ro"bles(dierence) (classiied ase"it#)

92

,anuary

&ash balance GD***** =* G 8* million Ro"bles (eriod+endrate):et roit G D***** $> G <* million Ro"bles (avera.e rate)

/0chan.e roit G 1* million Ro"bles(dierence) (classiied ase"it#)

$ebruary

Restate oenin. cash balance P closin. rate-D***** (*+=*) G =* million Ro"bles G e0chan.e loss(classiiedas e"it#)&ash balance GD=***** * G8*million Ro"bles (eriod+endrate)

:et roit G D***** < G>=million Ro"bles (avera.e rate)/0chan.e loss on net roit D***** (*+<)G 1= million Ro"bles(classiied as e"it#)

Reconciliation;

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng ,

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 30/31

IAS 21 The effects of changes in foreign exchange rates

&ash balance GD=***** * G8* million Ro"bles

:et 4roit Aan"ar# G<* million:et 4roit Febr"ar# G>= million/0chan.e .ain Aan"ar# G1* million

/0chan.e loss on cash G+=* million/0chan.e loss Febr"ar# G+1= million

Total G 8* million Ro"bles

:2 #he e)change loss is3

D1** million (+$*) G 8 million Ro"bles- %s the arent owns onl# <>? C million Ro"bles o .ain are recordedas e"it# and the remainin. million Ro"bles are added to minorit#interests in the balance sheet-

;2 #he 'uro e)change gain

million /"ro ($>+) G C million Ro"bles-

(It is a .ain as ewer Ro"bles are owed-)

The D loss GD=***** ($*+8) G *8 million Ro"bles-(It is a loss as ewer Ro"bles will be received-)

The /"ro .ain will .o to e"it# as it is art o the net investmentinancin. the "ndertakin.- The D loss will be recorded in the incomestatement as it is a tradin. item-

1>2 #he gain loss on disposal3D<>**** Q (DC****D>*****D****) G D1**** loss-

112 #he gain on disposal3

DC***** Q $*?(D1*****D1,*****+C****) G D<8*** .ain-

14* I$RS $ra%ework

%ll international standards al# in "ll to consolidated acco"nts(e0cet where otherwise stated)- The ollowin. are the moreimortant;

$ASB Conceptual Frame=ork

(&oncets that "nderlie the rearation and resentation oinancial statements or e0ternal "sers-)

I%S 1 4resentation o Financial Statements

I%S < Statements o &ash Flows

I%S 1 The /ects o &han.es in /0chan.e Rates(eseciall# Financial Statements o Forei.n Oerations)

I%S 8 %cco"ntin. or Investments in %ssociates

I%S $C Imairment o %ssets

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng $*

8/12/2019 IAS 21 AFA

http://slidepdf.com/reader/full/ias-21-afa 31/31

IAS 21 The effects of changes in foreign exchange rates

IFRS 1 First+time %dotion o IFRS

IFRS $ B"siness &ombinations

IFRS > 7isosal o :on+&"rrent %ssets and 4resentation o

7iscontin"ed Oerations@

IFRS , Financial Instr"ments

IFRS 1* &onsolidated Financial Statements

IFRS 11 Aoint %rran.ements

http://bankir.ru/technology/vestnik/uchebnye-posobiya-po-msfoeng $1