HY 2002 RESULTS - ab-inbev.com · Execution of Four Strategic Themes Strategic themes Rationale...

44

HY 2002 RESULTS HY 2002 RESULTS

Transcript of HY 2002 RESULTS - ab-inbev.com · Execution of Four Strategic Themes Strategic themes Rationale...

HY 2002 RESULTSHY 2002 RESULTS

1

SummarySummary

Solid underlying growth of the business

Investments in sustainable long-term growth

On track to achieve our financial targets

2

Key HighlightsKey Highlights

Post-Restructuring

Pre-Restructuring

HY 2001(3)

(IAS)

HY 2002 (IAS)(1)(2)

%Change(4)

€569m

€0.52

€630m

€0.62

€516m

€0.54

+22%

+15%

EBITDA

EPS Before Goodwill(5)

(1) Excluding Carling(2) Including €19m cost of Canadian lock-out & related pension costs(3) Excluding Bass UK (Carling, Scotland, Northern Ireland)(4) Change between HY 2001 and HY2002 pre-restructuring(5) Calculated using the average outstanding number of shares

3

'The World's Local Brewer' Vision 'The World's Local Brewer' Vision RealisedRealised Through Parallel Through Parallel Execution of Four Strategic ThemesExecution of Four Strategic Themes

Strategic themes Rationale

Building and leveraginglocal platforms driveprofitable growth

Local brands and access to economic scale in distribution are key value drivers in most geographical markets

11

Broad brand portfolioallows access to all segments

22A broad portfolio of brands can be tailored to local needs and requirements which enables value capture in all segments of the beer market

Superior risk-returnprofile with balance of mature and developing markets

33Stability of mature market cash flows allows flexibility for investment in higher-risk but higher growth areas

Market consolidationsecures position andcreates value

44 Consolidation is a major driver of value creation through scale economies and market leadership

4

CContinuous Shareholderontinuous Shareholder VValue Creationalue Creation

Achieving operational excellence requires

• Re-engineering of existing operations

• Obtaining integration benefits of previous acquisitions

• Investing in business to successfully achieve change

Sustained OrganicGrowth

Acqu

isitio

n

Operational

Excellence

Continuous shareholder

value creation

5

Presentation OutlinePresentation Outline

1.1. HY 2002 ResultsHY 2002 Results

2. Investing For Sustainable Growth

3. Integrating Beck & Co

4. Outlook & Conclusion

6

Description of Scope ChangesDescription of Scope Changes

Bass Scotland / Northern Ireland (Jan 02)Diebels (Sep 01)Beck & Co (Feb 02)

ScopeInclusions

ScopeExclusions

Heineken UK contract (Jan 02)Service fee changes (Dec 01)

Carling included in reported HY 02 numbers for 5 weeks (sold Feb 02)Bass UK excluded from HY 01 and Carling excluded from HY 02

Bass UK / Carling

RestructuringCharge

UK distribution restructuring charge shown separately for group and Western Europe

7

Breakdown of HY02 ResultsBreakdown of HY02 Results

Net TurnoverNet Turnover€€ millionmillion

VolumeVolume(1)(1)

Hl millionHl million

+122,784 +115 +421 3,332

+4.1% +15.1% +0.4% +19.7%

- 40.9+5.3+0.834.8

+2.3% +15.2% +17.5%

HY01 HY 02 Foreign ExchangeScope(2)Organic

GrowthHY01 HY 02 Foreign ExchangeScope(2)

OrganicGrowth

80.0 81.5Net Turnover/ HNet Turnover/ Hll€ per Hl€ per Hl

(1) Excluding FEMSA Cerveza(2) Inclusions: Bass Scotland / Northern Ireland, Diebels and Beck & Co

Exclusions: Heineken UK contract and service fee changes

8

+1 630516 +17 +96

569-61

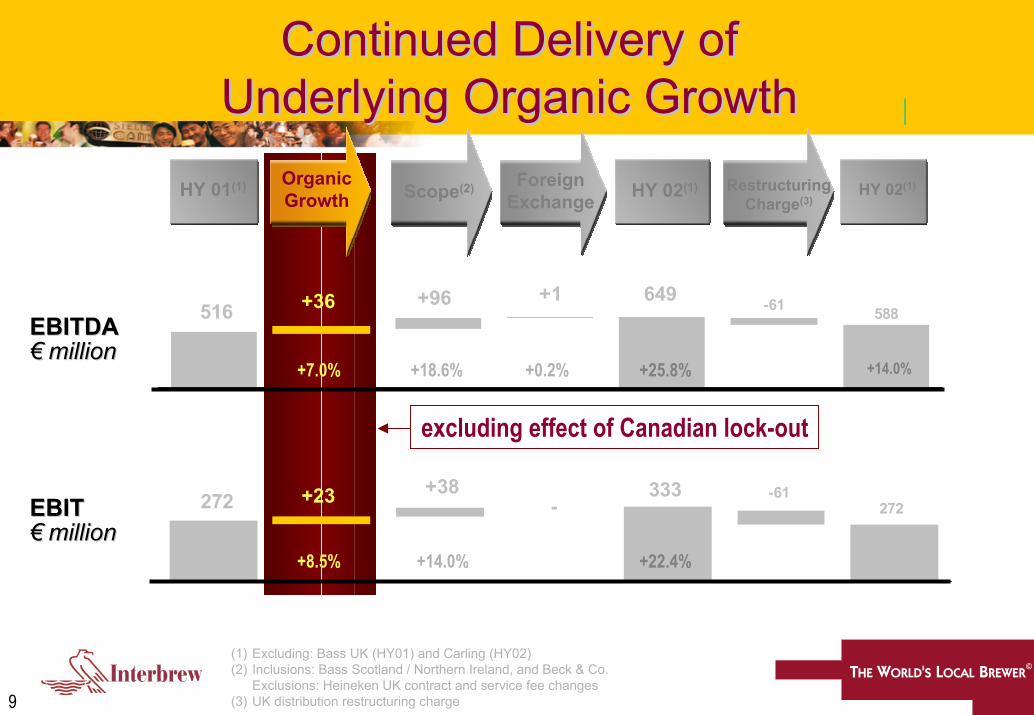

Continued Delivery ofContinued Delivery ofUnderlying Organic GrowthUnderlying Organic Growth

+3.3% +18.6% +10.3%+22.1%

HY 01(1) HY 02(1)Foreign ExchangeScope(3)Organic

Growth(2)Restructuring

Charge(4)HY 02(1)

+0.2%

EBITDAEBITDA€€ millionmillion

253-61+38+4272 314

-

-7.0%+1.5% +13.9% +15.4%

EEBITBIT€€ millionmillion

(1) Excluding: Bass UK (HY01) and Carling (HY02)(2) Includes €19m cost of Canadian lock-out(3) Inclusions: Bass Scotland / Northern Ireland, Diebels and Beck & Co.

Exclusions: Heineken UK contract and service fee changes(4) UK distribution restructuring charge

9

272-61+38

272 333-

+1 649516 +96

588-61

Continued Delivery ofContinued Delivery ofUnderlying Organic GrowthUnderlying Organic Growth

+18.6% +14.0%

+14.0%

+25.8%

+22.4%

HY 01(1) HY 02(1)Foreign ExchangeScope(2)Organic

GrowthRestructuring

Charge(3)HY 02(1)

+0.2%

+36

+7.0%

+23

+8.5%

excluding effect of Canadian lock-out

EBITDAEBITDA€€ millionmillion

EEBITBIT€€ millionmillion

(1) Excluding: Bass UK (HY01) and Carling (HY02)(2) Inclusions: Bass Scotland / Northern Ireland, and Beck & Co.

Exclusions: Heineken UK contract and service fee changes(3) UK distribution restructuring charge

10

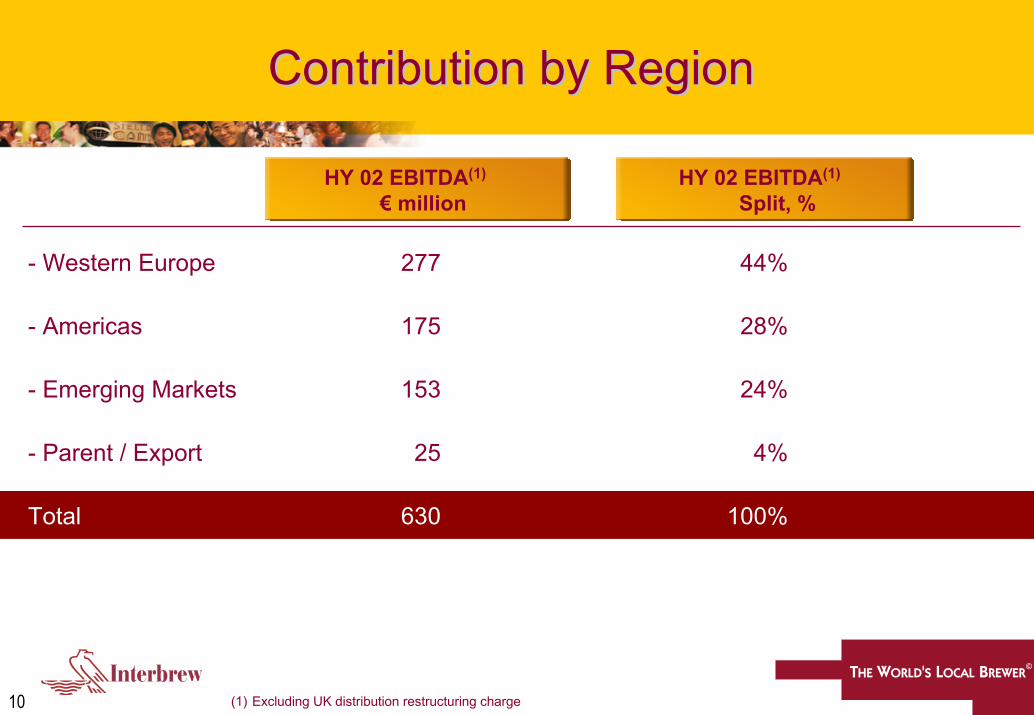

Contribution by RegionContribution by Region

HY 02 EBITDA(1)

€ millionHY 02 EBITDA(1)

Split, %

- Western Europe

- Americas

- Emerging Markets

- Parent / Export

Total

277

175

153

25

630

44%

28%

24%

4%

100%

(1) Excluding UK distribution restructuring charge

11

Breakdown of Growth in Western EuropeBreakdown of Growth in Western Europe

OrganicGrowth Scope(2) FX Organic

Growth Scope(2)HY 01(1) FX HY 02(1) Restr.Chrg.(3)HY 01(1) HY 02(1) HY 02(1)

+29+5

1,241+324 1,599

+0.216.8-+4.7

11.9

Volu

me

Volu

me

Milli

on H

lM

illion

Hl

+39.5% +41.2%

193

277-+18

+66 -61

216

EBIT

DA

EBIT

DA

€ m

illion

€ m

illion

+9.3% +11.9%+34.2%

Net

Tur

nove

rN

et T

urno

ver

€ m

illion

€ m

illion

+2.3% +28.8%

66

-61127-

+10+2196

EBIT

EBIT

€ m

illion

€ m

illion

+21.9% -31.3%+10.4%+26.1% +0.4%

(1) Excluding: Bass UK (HY 01) and Carling (HY 02)(2) Inclusions: Bass Scotland / Northern Ireland, Diebels and Beck & Co

Exclusions: Heineken UK contract and service fee changes(3) UK distribution restructuring charge

+1.7% +43.5%

+32.3%

12

Western EuropeWestern Europe

• Market share stable or growing in all countries

• Continued strong value growth of Stella Artois in the UK (+9.4%)

• Increase of Jupiler crate market share

• Pleasing developments in Germany

13

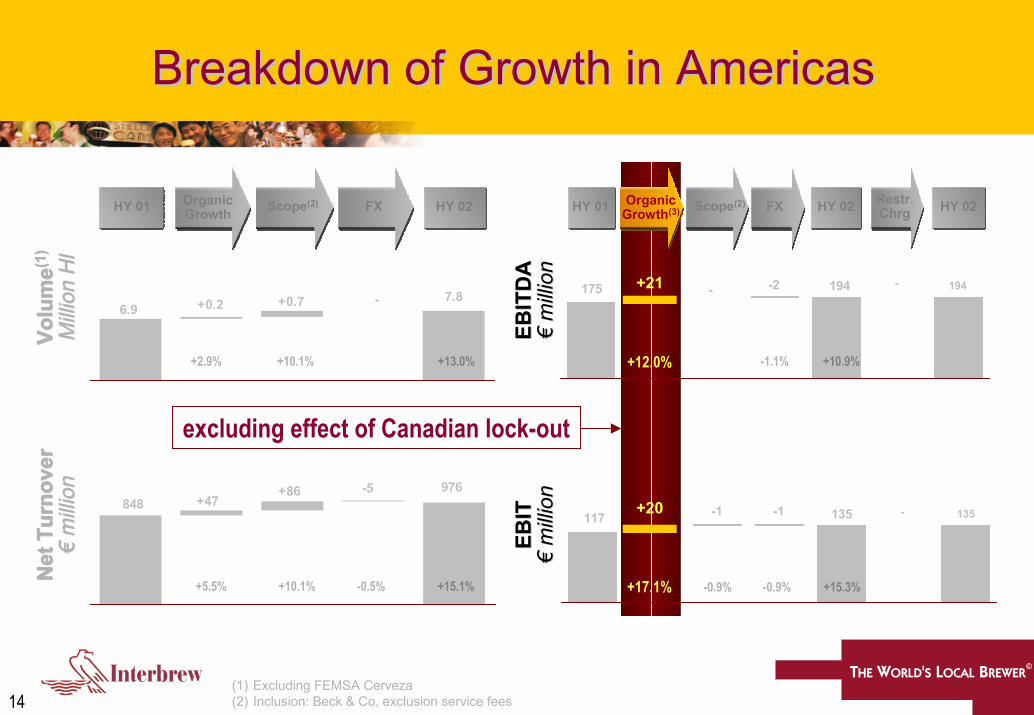

Breakdown of Growth in AmericasBreakdown of Growth in Americas

OrganicGrowth Scope(2) FX HY 02 Organic

Growth(3)HY 01 Scope(2) FX HY 02 Restr. Chrg HY 02HY 01

+47+86 -5 976

848

Net

Tur

nove

rN

et T

urno

ver

€ m

illion

€ m

illion

+5.5% +15.1%

+1 - 116-1-1 116117EB

ITEB

IT€

milli

on€

milli

on

+0.9% -0.9%-0.9%+10.1% -0.5% -0.9% -0.9%

7.8+0.2 -+0.76.9

Volu

me

Volu

me

Milli

on H

lM

illion

Hl

+2.9% +13.0%

+2 175--2 175-175

EBIT

DA

EBIT

DA

€ m

illion

€ m

illion

+1.1% -1.1%+10.1%

(1)

(1)

(1) Excluding FEMSA Cerveza(2) Inclusion: Beck & Co, exclusion service fees(3) Includes €19m cost of Canadian lock-out

14

Breakdown of Growth in AmericasBreakdown of Growth in Americas

+47+86 -5 976

848

7.8+0.2 -+0.76.9

Volu

me

Volu

me(

1)(1)

Milli

on H

lM

illion

Hl

+2.9% +13.0%

194--2 194-175

OrganicGrowth Scope(2) FX HY 02HY 01

+12.0% +10.9%-1.1%

Net

Tur

nove

rN

et T

urno

ver

€ m

illion

€ m

illion

+5.5% +15.1%

135--1-1 135117

+17.1% +15.3%-0.9%+10.1%

+10.1%

-0.5% -0.9%

+21

+20

excluding effect of Canadian lock-out

OrganicGrowth(3) Scope(2) FX HY 02HY 01 Restr.

Chrg HY 02

EBIT

DA

EBIT

DA

€ m

illion

€ m

illion

EBIT

EBIT

€ m

illion

€ m

illion

(1) Excluding FEMSA Cerveza(2) Inclusion: Beck & Co, exclusion service fees

15

AmericasAmericas

• US

• Import depletions up 7.7%

• Repositioning Rolling Rock

• Canada

• Pricing environment remains strong

• Overall market share stable

• Oland Specialty Beer Company - 20% organic volume growth

• Cuba

16

Breakdown of Emerging Markets GrowthBreakdown of Emerging Markets Growth

15.3+0.4 --14.9

Volu

me

Volu

me

Milli

on H

lM

illion

Hl

+2.7% +2.7%

+6 +3 153-2146

EBIT

DA

EBIT

DA

€ m

illion

€ m

illion

+4.1% +4.8%+2.1%

OrganicGrowth Scope FX HY 02HY 01 Organic

Growth Scope(1) FX HY 02HY 01

-1.4%

+41 +11 681-629

Net

Tur

nove

rN

et T

urno

ver

€ m

illion

€ m

illion

+6.5% +8.3%

+258-5 -2

63

EBIT

EBIT

€ m

illion

€ m

illion

-7.9% -7.9%+3.2%+1.8% -3.2%

(1) Exclusion: Service fee changes

17

Central EuropeCentral Europe

• Czech Republic, Croatia and Hungary performance above expectations with a strong core segment

• Romania and Bulgaria: tough economic environment

• Continued loss of market share to value brands

• Montenegro performance impacted by politically driven strike

18

Eastern EuropeEastern Europe

• Russia

• Two new PET lines and can line in Klin operational as of June• Acceleration of 2003 CAPEX• Implementation of cross-brewing

• Ukraine• Growth market with potential• Strong performance

Market VolumeJun-01 vs. Jun-02

MarketGrowth

+600,000

+392,000

5x

+24%

Cans

PET

19

AsiaAsia

• South Korea

• Industry growth of 5% YTD

• Cass reached 19.7% market share

• Rejuvenation of OB brand

• Strong financial performance

20

Return on Invested Capital by RegionReturn on Invested Capital by Region

June 2002Post Scope

Invested Capital

June 2001

ROIC(1)

June 2002Pre-Scope

ROIC

June 2002Post Scope

ROIC(1)

- Western Europe

- Americas(2)

- Emerging Markets

- Parent / Export

Total

2,305

2,028

1,736

541

6,610

18.7%

13.2%

7.9%

-4.9%

10.1%

19.7%

15.3%

9.1%

0.9%

13.2%

8.4%

15.3%

9.1%

4.8%

10.4%

(1) As reported(2) Including investment in FEMSA Cerveza

21

EPS ProgressionEPS Progression

HY 00(1) HY 01(2) HY 02(2)

€0.46

€0.46

€0.46

€0.56

€0.54

€0.54+17%

€0.51

€0.52

€0.62+15%

EPS (excluding goodwill)

EPS (excluding goodwill, Bass UK/Carling)

EPS (excluding goodwill, Bass UK / Carling, restructuring)

€ €1.44

%

(1) Belgian GAAP(2) IAS

22

Presentation OutlinePresentation Outline

1. HY 2002 Results

2.2. Investing For Sustainable GrowthInvesting For Sustainable Growth

3. Integrating Beck & Co

4. Outlook & Conclusion

23

Investing for Sustainable GrowthInvesting for Sustainable Growth

• New Long Range Plan: 2003 – 2005

• New variable compensation

• Re-engineering: optimise global integration

• Build a platform for sustainable long-term, top and bottom-line growth

24

Challenging the Status QuoChallenging the Status Quo

Re-engineering actions taken to date

• UK

• Distribution

• Castlemaine XXXX / Murphy’s

• Canadian workforce negotiations

• Brascan settlement

Further projects to follow

25

Financial Impact of ReFinancial Impact of Re--engineeringengineering

• One off charge £25m Cash / £37.5m (€61m) EBIT

• Impact for Interbrew (€m)UK Distribution

2005 onward

Cash

+10

EBIT

+9

Canada• Negative EBIT impact of €19m in HY 02 • Avoided cost increase of €93m in FY 03 and going forward

Brascan • Cash in/minimal impact on P&L

26

Invested CapitalInvested Capital

Increased CAPEX

• Russia: Packaging + Capacity

• Cuba: Capacity + Distribution

• South Korea: Investment in brands

HY 02 CAPEX €229m, versus HY 01 CAPEX €227m

Link between CAPEX and organic growth

27

Investing in Growth MarketsInvesting in Growth Markets

Top High Growth Beer Markets(1)

10.1

6.75.9

3.0 3.0 2.6

48.4

Chin

a

Braz

il

Mex

ico

Russ

ia

USA

Pola

nd

Ukra

ine

Well-established presence in high growth markets

Continuing investment program

• China

Interbrew presence

% o

f Glo

bal

% o

f Glo

bal

Gro

wth

Gro

wth

(1) Canadean, Fastest Growing Top 20 Beer Markets (2001A-2006F)

28

Presentation OutlinePresentation Outline

1. HY 2002 Results

2. Investing For Sustainable Growth

3.3. Integrating Beck & CoIntegrating Beck & Co

4. Outlook & Conclusion

29

Integrating Beck & CoIntegrating Beck & Co

Detailed financials for Beck’s at year end

21 integration teams with full staff commitment

Focus on core business

Germany• Integration of Beck & Diebels completed in 78 working days

30

Beck’s: GermanyBeck’s: Germany (1)(1)

Sales Volume: Beck’s (Total Brand) Sales Volume: Beck’s (Rtn. Bottles)

1,400

1,500

1,600

1,700

1,800

1,900

2,000

1998 1999 2000 2001 2002380400420440460480500520540560

1998 1999 2000 2001 2002

6.7% Price Increase executed1-Jun-00

8.5% Second Price Increase 1-Jul-02

5.0% Price Increase executed 1-Jun- 00

The new crate

5.0% Second Price Increase1-Jul-02

Announcement ofBeck’s acquisition

6-Aug-01

Announcement ofBeck’s acquisition

6-Aug-01

31

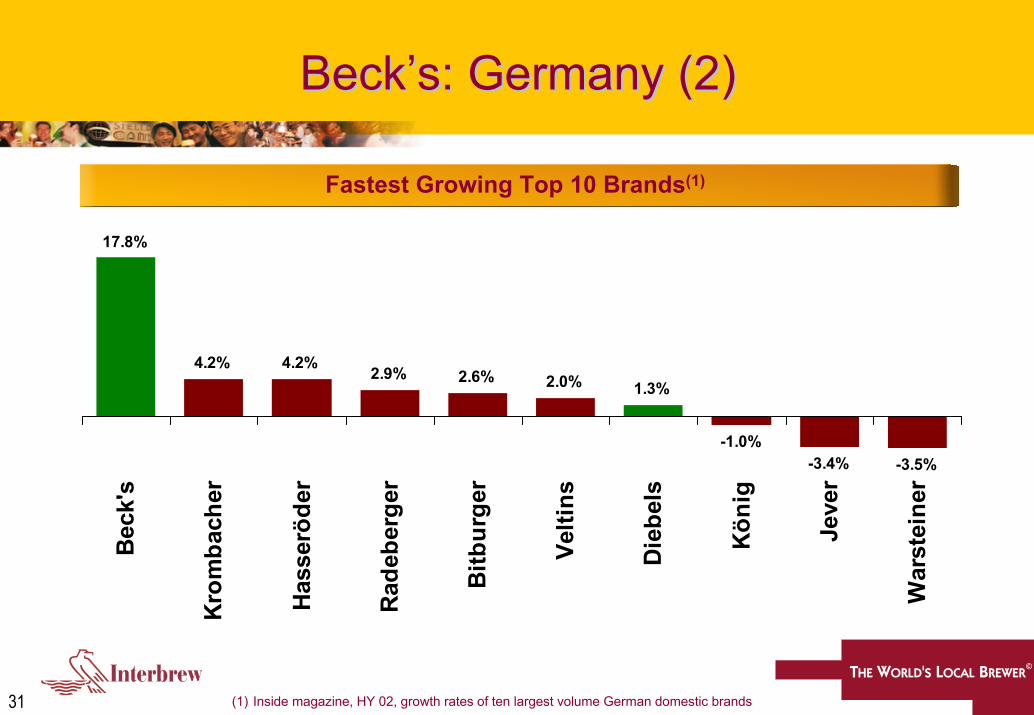

Beck’s: GermanyBeck’s: Germany (2)(2)

Fastest Growing Top 10 Brands(1)

17.8%

4.2% 4.2% 2.9% 2.6% 2.0% 1.3%

-1.0%-3.4% -3.5%

Beck

's

Krom

bach

er

Hass

eröd

er

Rade

berg

er

Bitb

urge

r

Velti

ns

Dieb

els

Köni

g

Jeve

r

War

stei

ner

(1) Inside magazine, HY 02, growth rates of ten largest volume German domestic brands

32

Beck’s: GermanyBeck’s: Germany (3)(3)

Total Beck’s Margin (Indexed to 100)

100

104102

122

100

97/9

8

98/9

9

99/0

0

00/0

1

01/0

2

33

Beck’s: Rest of WorldBeck’s: Rest of World

• Canadian licence

• Total cost of €3.5m over 5 years

• Wider distribution through Oland Specialty Beer Company

• EFES agreement in Turkey

• Export business - strong performance

34

Beck’s: AmericasBeck’s: Americas

• Update on legal situation

• Currently operating independently of Labatt USA

• Uncertainty over integration has had some impact on sales performance

• Encouraging recent trading trends

• Marketing initiatives to reinvigorate brand for US consumers

35

Presentation OutlinePresentation Outline

1. HY 2002 Results

2. Investing For Sustainable Growth

3. Integrating Beck & Co

4.4. Outlook & ConclusionOutlook & Conclusion

36

Current Trading ConditionsCurrent Trading Conditions

• Western Europe

• Americas

• Emerging Markets

37

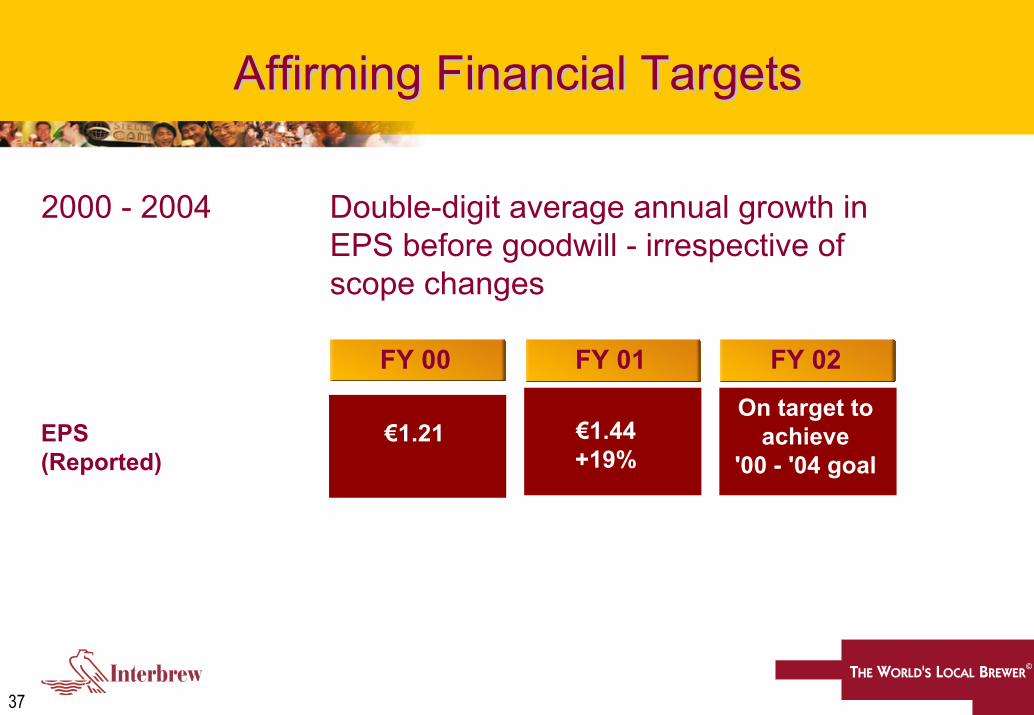

Affirming Financial TargetsAffirming Financial Targets

2000 - 2004 Double-digit average annual growth in EPS before goodwill - irrespective of scope changes

FY 00 FY 01 FY 02

€1.44+19%

On target to achieve

'00 - '04 goal€1.21EPS

(Reported)

Questions & AnswersQuestions & Answers

HY 2002 RESULTSHY 2002 RESULTSAnnexes

40

FXFX

Main currencies• CAD, USD, GBP, RUB, KRW

Translation risks• Local currency income & costs• Minimise equity in local currency• Leverage in local currency

Transaction risks• Operational exposure: 100% hedged 12 months• Intra company financial exposure:

100% hedged 6 months50% hedged next 6 months

41

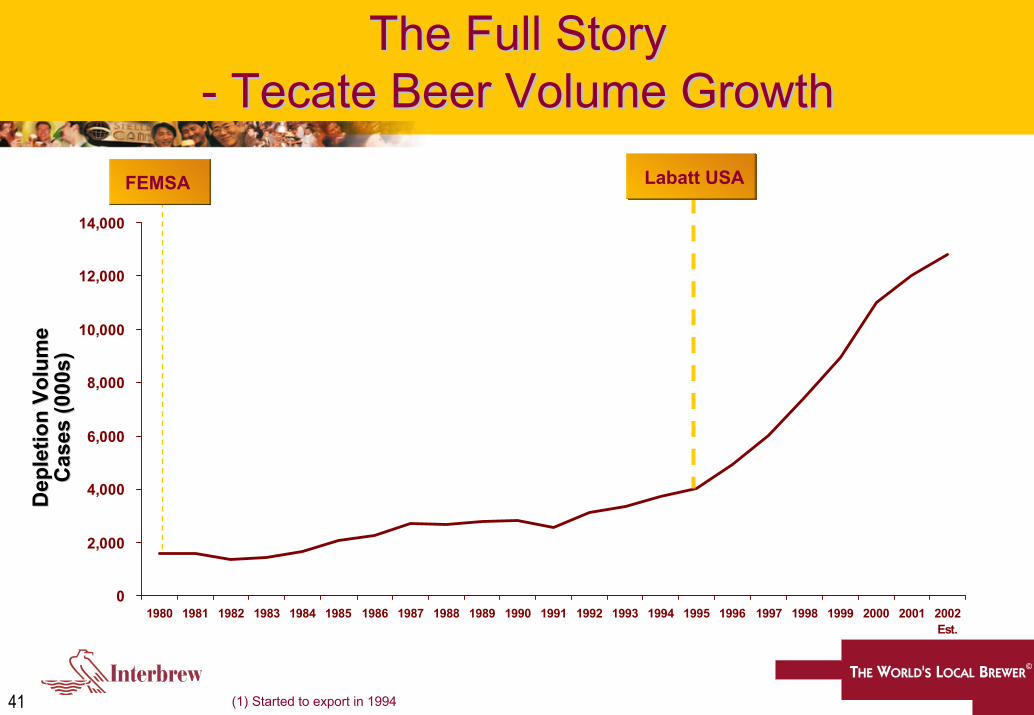

The Full StoryThe Full Story-- TecateTecate Beer Volume GrowthBeer Volume Growth

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002Est.

Labatt USAFEMSA

Dep

letio

n Vo

lum

eD

eple

tion

Volu

me

Cas

es (0

00s)

Cas

es (0

00s)

(1) Started to export in 1994

42

The Full StoryThe Full Story-- Dos Dos EquisEquis Beer Volume GrowthBeer Volume Growth

0

1,000

2,000

3,000

4,000

5,000

6,000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002Est.

Labatt USAFEMSA

Dep

letio

n Vo

lum

eD

eple

tion

Volu

me

Cas

es (0

00s)

Cas

es (0

00s)

43

Sound Financial StructureSound Financial Structure

HY 02 HY 01

2741

4.8

4.7

€ 2,741m

4.8

4.7

€ 3,158m

4.8

4.8

Net Financial Debt

Net Financial Debt / EBITDA

Cash Interest Coverage