HVS Market Feasibility Study - City of Modesto

131

FEASIBILITY STUDY Proposed Convention Center Hotel MODESTO, CALIFORNIA SUBMITTED TO : PREPARED BY: Ms. Laurie Smith HVS Convention, Sports & Entertainment City of Modesto Facilities Consulting 1010 10th Street, Suite 4400 205 West Randolph, Suite 1650 Modesto, California, 95353 Chicago, Illinois 60606 +1 (209) 577-5347 +1 (312) 587-9900 [email protected] October 1, HVS

Transcript of HVS Market Feasibility Study - City of Modesto

FEASIBILITY STUDY

Proposed Convention Center Hotel MODESTO, CALIFORNIA

SUBMITTED TO : PREPARED BY:

Ms. Laurie Smith HVS Convention, Sports & Entertainment City of Modesto Facilities Consulting 1010 10th Street, Suite 4400 205 West Randolph, Suite 1650 Modesto, California, 95353 Chicago, Illinois 60606 +1 (209) 577-5347 +1 (312) 587-9900 [email protected]

October 1,

HVS

January 22, 2019

Ms. Laurie Smith City of Modesto 1010 10th Street, Suite 4400 Modesto, California, 95353

Re: Proposed Convention Center Hotel

Modesto, California

Dear Ms. Smith:

Attached you will find our Feasibility Study of the Proposed Convention Center Hotel in Modesto, California.

We certify that we have no undisclosed interest in the property, and our employment and compensation are not contingent upon our findings. This study is subject to the comments made throughout this report and to all assumptions and limiting conditions set forth herein.

It has been a pleasure working with you. Please let us know if you have any questions.

Sincerely,

HVS Convention, Sports & Entertainment

Facilities Consulting

Tom Hazinski

Managing Director

Brian Harris

Senior Director

205 West Randolph

Suite 1650

Chicago, Illinois 60606

+1 312-587-9900

+1 312-488-3631 FAX

www.hvs.com

Atlanta

Boston

Boulder

Chicago

Dallas

Denver

Las Vegas

México City

Miami

Nassau

New York

Newport

San Francisco

Toronto

Vancouver

Washington

Athens

Buenos Aires

Dubai

Hong Kong

Lima

London

Madrid

Mumbai

New Delhi

Sao Paulo

Shanghai

Singapore

Table of Contents

SECTION TITLE

1. Executive Summary 1-1

2. Description of Site and Proposed Hotel 2-1

3. Modesto Market Overview 3-1

4. Supply and Demand Analysis 4-1

5. Modesto Centre Plaza Demand Analysis 5-1

6. Projection of Occupancy and Average Rate 6-1

7. Projection of Income and Expenses 7-1

8. Proposed Hotel Feasibility Analysis 8-1

9. Economic Impact 9-1

10. Public Private Partnerships 10-1

11. Statement of Assumptions and Limiting Conditions 11-1

12. Certification 12-1

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-1

1. Executive Summary

The City of Modesto (the “City”) engaged HVS Convention, Sports, and Entertainment Facilities Consulting (“HVS”) to conduct a Feasibility Study of a Proposed Hotel (“Proposed Hotel”) connected to the Modesto Centre Plaza (“MCP”). The site for the Proposed Hotel is in downtown Modesto, California.

For this study, HVS analyzed the development of 1) a full-service hotel with banquet and meeting space, restaurant and lounge, and 2) a select-service hotel with minimal function space and limited food service. Based on a preliminary analysis, we concluded that the select-service hotel option is more likely to be feasible. Consequently, this report primarily focuses the analysis on the performance of a select-service hotel. Select-service properties typically do not contain extensive meeting, recreational, and retail facilities. But, recent developments in the building programs of select service hotels have blurred the distinction between full-service and select-service brands. Larger dining and lounge facilites have been added to some select-service brands along with improved bedding, furnishings, public spaces, and bathrooms. The primary remaining distinctions are the amounts of function space and customer services such as concierge, valet, and room services that hotel brands required in a full-sevice product.

HVS assumes the Proposed Hotel will open on January 1, 2021, as a 200-room select-service hotel, featuring a restaurant, lounge, 3,800 square feet of meeting space, outdoor pool, outdoor whirlpool, fitness center, business center, gift shop, and guest laundry room. The hotel would also include the appropriate back-of-the-house space necessary to support hotel operations. Parking would be provided in a nearby public parking garage. The operator of the garage would retain all associated parking revenues except for the premium component of any valet parking operated by the Proposed Hotel.

The Proposed Hotel would attract the commercial, meeting and group, and leisure market segments because of the national brand affiliation, downtown locations, and proximity to the MCP. Hotel guests would include value seeking independent travelers who are willing to pay a higher rate for a new product, groups that negotiate lower group rates for large room blocks and banquet space, and more price-sensitive leisure travelers that seek discounted room rates offered on shoulder days and weekends.

Subject of the Feasibility Study

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-2

This study employs the methodology illustrated in Figure 1-1.

FIGURE 1-1 HOTEL FEASIBILITY STUDY METHODOLOGY

Research Potential

Competitive Hotels

Feasibility Analysis using

Discounted Cash Flows

Comparable Hotel

Operating Data

Proposed Hotel Market

Penetration

Occupancy and ADR

Forecasts by Market

Segment

Estimate of Proposed

Hotel Financial

Operations

Market ADR and

Occupancy Estimates

Inflation and Market

Growth Assumptions

Economic Indicators

Competitive Set Analysis

Induced Demand

Unaccommodated

Demand

Room Supply Changes

HVS 1) analyzed the historical performance of a competitive set of hotels, 2) estimated the amounts of induced and unaccommodated demand in the market, and 3) researched potential changes in room supply. Based on these hotel market trends and economic and demographic indicators of future changes in hotel demand, HVS projected the future performance of a competitive set of hotel properties. Through a market penetration analysis, we estimated the average daily room rate and occupancy of the Proposed Hotel in each of the three market segments—commercial, leisure, and meeting and group. An estimate of average daily room rates and occupancies generates a projection of room revenues, which,

Methodology

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-3

when combined with the operating data on comparable hotels, yields a ten-year estimate of financial operations. The feasibility analysis of this study converts the net income from the 10-year pro forma and assumed sale of the hotel after ten years of operation into a net present value at opening based on the assumptions set-forth for the debt and equity components of the financing.

The methodology used to develop this study is based on market research and valuation techniques set forth in the textbooks authored by Hospitality Valuation Services for the American Institute of Real Estate Appraisers and the Appraisal Institute, entitled The Valuation of Hotels and Motels,1 Hotels, Motels and Restaurants: Valuations and Market Studies,2 The Computerized Income Approach to Hotel/Motel Market Studies and Valuations,3 Hotels and Motels: A Guide to Market Analysis, Investment Analysis, and Valuations,4 and Hotels and Motels – Valuations and Market Studies.5 All information was collected and analyzed by the staff of HVS Convention, Sports & Entertainment Facilities Consulting.

The effective date of the study is January 22, 2019. Tom Hazinski and Brian Harris inspected the site for the Proposed Hotel on October 23, 2018. All projections are expressed in inflated dollars.

The approximate 1.50-acre site for the Proposed Hotel is located in downtown Modesto adjacent to the MCP. The site is currently a surface parking lot for the MCP. The developer selected by the City will purchase at market value, all or a portion of the available site, which is currently a public surface parking lot. See page 2-1 for a more thorough description of the site.

The hotel ownership structure has not been determined as of the date of this study, except to rule out any public ownership or financing.

The management agreement will need to be negotiated after a development plan for the Proposed Hotel has been finalized with the selected developer. We have included a market appropriate management fee of 3.0% of gross operating

1 Stephen Rushmore, The Valuation of Hotels and Motels. (Chicago: American Institute of

Real Estate Appraisers, 1978). 2 Stephen Rushmore, Hotels, Motels and Restaurants: Valuations and Market Studies.

(Chicago: American Institute of Real Estate Appraisers, 1983). 3 Stephen Rushmore, The Computerized Income Approach to Hotel/Motel Market Studies and

Valuations. (Chicago: American Institute of Real Estate Appraisers, 1990). 4 Stephen Rushmore, Hotels and Motels: A Guide to Market Analysis, Investment

Analysis, and Valuations (Chicago: Appraisal Institute, 1992). 5 Stephen Rushmore and Erich Baum, Hotels and Motels – Valuations and Market Studies.

(Chicago: Appraisal Institute, 2001).

Pertinent Dates

Site

Ownership and Management

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-4

revenues. Other charges related to the future hotel’s brand affiliation, such as frequent guest programs, are reflected in the appropriate departmental expenses, consistent with the Uniform System of Accounts for the Lodging Industry (“USALI”).

We recommend that the Proposed Hotel operates as an upper-upscale, select-service hotel. While we have placed heavy consideration on the Hilton Garden Inn or Courtyard by Marriott brands, a specific franchise affiliation would be determined as part of a future hotel project. Our projections reflect a Hilton, Marriott or similar brand affiliation. We assume that the Proposed Hotel will obtain a brand from a national brand and will retain its brand affiliation throughout the 10-year holding period. Inherent in this assumption is the expectation that the property will be operated in accordance with brand standards, including requirements for services and cleanliness; that the hotel will be maintained in good condition, with all building systems in good working order; and that any necessary refurbishments or renovations will be completed in a timely manner and in accordance with the requirements of the brand.

HVS analyzed the performance of a set of hotels that would compete with the Proposed Hotel (“Competitive Hotels” see page 4-4, Figure 4-2). Based on an evaluation of the occupancy, rate structure, market orientation, location, facilities, amenities, reputation, and quality, as well as the comments of management representatives, we have identified four properties that would compete with the Proposed Hotel on a primary basis, and eight properties that would compete on a secondary basis, for a total of 12 competitors. Due to location, brand quality, and service levels, primary competitors vie for the same customers and are 100 percent competitive with the Proposed Hotel. Secondary competitors have partially overlapping customer bases and their competitiveness with the Proposed Hotel is weighted at less than 100 percent. Section 4 of this study, Supply and Demand Analysis, provides a detailed discussion of the weighting of the secondary competitors.

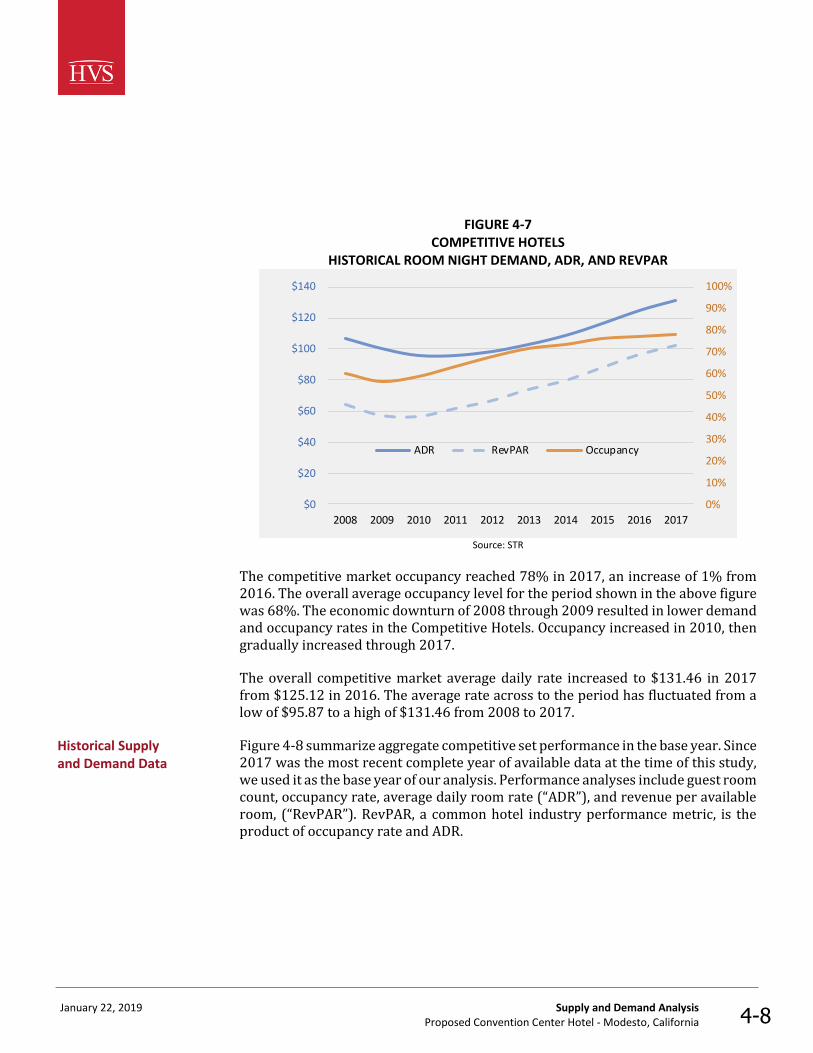

Figure 1-2 provides a long-term perspective on the supply and demand trends of the Competitive Hotels, with data provided by Smith Travel Research (“STR”). STR is an independent research firm that compiles proprietary data on the lodging industry.

Summary of Hotel Market Trends

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-5

FIGURE 1-2 HISTORICAL COMPETITIVE HOTELS ADR, OCCUPANCY, AND REVPAR TRENDS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$20

$40

$60

$80

$100

$120

$140

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

ADR RevPAR Occupancy

Source: STR

Average daily room rate (“ADR”) is the annual revenue of the hotel divided by the number of occupied room nights. Occupancy is a percentage calculated by dividing the annual number of occupied room nights by the annual number of available room nights. Revenue per available room, (“RevPAR”) is a common hotel industry metric, calculated by multiplying the occupancy rate by ADR and provides a combined measure of rate and occupancy.

In 2017, the ADR of Competitive Hotels increased by 5.1% and occupancy increased by 0.9%, causing RevPAR to increase by 6.0%. Demand grew by 5.6% in 2017. This increase was partially offset by an increase in available room nights with the opening of the 85-room Hampton Inn Turlock of 4.7%, causing the occupancy rate to rise to 77.7%.

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-6

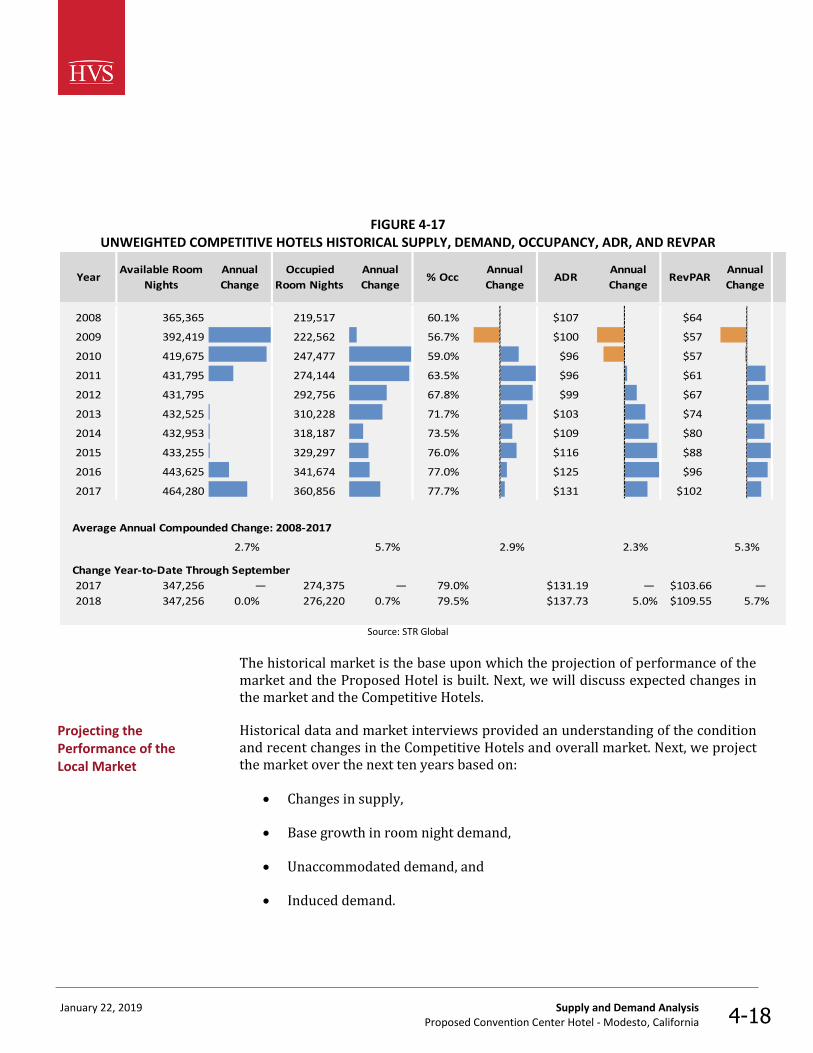

Figure 1-3 reflects HVS’s estimates of operating data of the Competitive Hotels for the years 2015 through 2017. Description of the Competitive Hotels is provided on page 4-3.

FIGURE 1-3 WEIGHTED HISTORICAL SUPPLY, DEMAND, OCCUPANCY, ADR, & REVPAR

(2015 - 2017)

YearRoom Nights

Available

Room Nights

Sold

Competitive

Hotels

Occupancy

Competitive

Hotels ADR

Competitive

Hotels RevPAR

Amount

2015 385,000 293,000 76.1% $116.89 $88.96

2016 393,000 304,000 77.4% $126.22 $97.64

2017 410,000 320,000 78.0% $131.84 $102.90

Percent Change

2016 2.1% 3.8% 1.6% 8.0% 9.8%

2017 4.3% 5.3% 0.9% 4.4% 5.4%

Since 2015, accommodated room nights increased by 9.2%, while the number of available room nights increased by 6.5%. As a result, market occupancy increased 2.6% during the same period. Average daily room rate grew 12.8% since 2015. The combined effect of changes in occupancy and ADR caused RevPAR to grow 15.7% over the three-year period analyzed here. The Competitive Hotels have shown strong growth in demand with occupancy rates rising despite the increase in supply from the opening of the Hampton Inn Turlock.

HVS analyzed changes in the Competitive Hotels over the last 12 months as reported to STR.

Monthly Room Night Demand

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-7

FIGURE 1-4 UNWEIGHTED HISTORICAL 12 MONTH COMPETITIVE DEMAND TRENDS

MonthOccupied

Room Nights Prior Year Difference

Oct-17 32,352 31,533 819 2.6%

Nov-17 28,532 28,477 55 0.2%

Dec-17 25,597 24,497 1,100 4.5%

Jan-18 27,240 26,776 464 1.7%

Feb-18 26,975 27,204 -229 -0.8%

Mar-18 31,037 31,171 -134 -0.4%

Apr-18 31,033 28,179 2,854 10.1%

May-18 32,827 32,181 646 2.0%

Jun-18 32,385 31,867 518 1.6%

Jul -18 31,113 32,163 -1,050 -3.3%

Aug-18 32,230 33,244 -1,014 -3.1%

Sep-18 31,380 31,590 -210 -0.7%

12 Month Total 362,701 358,882 3,819 1.1%

Change in Demand

Source: STR

Demand within the competitive set showed growth of 1.1% over the last 12 months. Interviews with four hotel managers indicate that the high occupancy rate constrained demand growth during spring, summer and weekend days due to a lack of available rooms to meet demand.

To forecast the occupancy of the Proposed Hotel, HVS performed a market penetration analysis of three market segments, commercial, meeting and group, and leisure. The purpose of segmenting the lodging market is to define each major type of demand, identify customer characteristics, and estimate future growth trends. HVS divided demand into the three market segments based on the nature of travel. Figure 1-5 summarizes estimates of accommodated room night demand by market segment, assuming the Proposed Hotel begins operation on a calendar year starting January 1, 2021.

Summary of Forecast Occupancy and Average Rate

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-8

FIGURE 1-5 PROPOSED HOTEL OCCUPANCY FORECAST

Calendar Year 2021 2022 2023 2024

Avai lable Room Nights 73,000 73,000 73,000 73,000

Absorption by Segment

Commercia l 25,500 27,000 28,200 28,200

Meeting and Group 6,200 8,100 9,300 9,300

Leisure 16,000 16,900 17,500 17,500

Total Absorption 47,700 52,000 55,000 55,000

Projected Occupancy 66% 71% 75% 75%

Percent Segmentation

Commercia l 53% 52% 51% 51%

Meeting and Group 13% 16% 17% 17%

Leisure 34% 33% 32% 32%

Figure 1-6 compares the projected occupancy of the Proposed Hotel with the Competitive Hotels for the first four years of operation.

FIGURE 1-6 COMPETITIVE HOTELS AND PROPOSED HOTEL OCCUPANCY FORECAST

0%

10%

20%

30%

40%

50%

60%

70%

80%

2021 2022 2023 2024

Competitive Hotels Proposed Hotel

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-9

The Proposed Hotel would open on January 1, 2021, and for this analysis we assume would take three years to stabilize. Based on our analysis presented in chapter four, in a stabilized year of demand, the property could absorb room nights and achieve a stabilized occupancy level of 75%.

In positioning the ADR, we consider the ADR of Competitive Hotels as well as the location of the Proposed Hotel, its brand and quality, and its adjacency to the MCP. Figure 1-7 compares the estimated ADR of the Proposed Hotel with the ADR of Competitive Hotels during four calendar years starting January 1, 2021.

FIGURE 1-7 COMPETITIVE HOTELS & PROPOSED HOTEL AVERAGE RATE FORECAST

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2021 2022 2023 2024

Competitive Hotels Proposed Hotel

We positioned the ADR in the base year 2017 at an average rate of $145.46. This rate would grow with inflation and in proportion to the rate of growth in the competitive set. The positioned ADR is further discounted by 3.0% in 2021 and 1.0% in 2022 to reflect typical management practices during the years before the hotel stabilizes in the market.

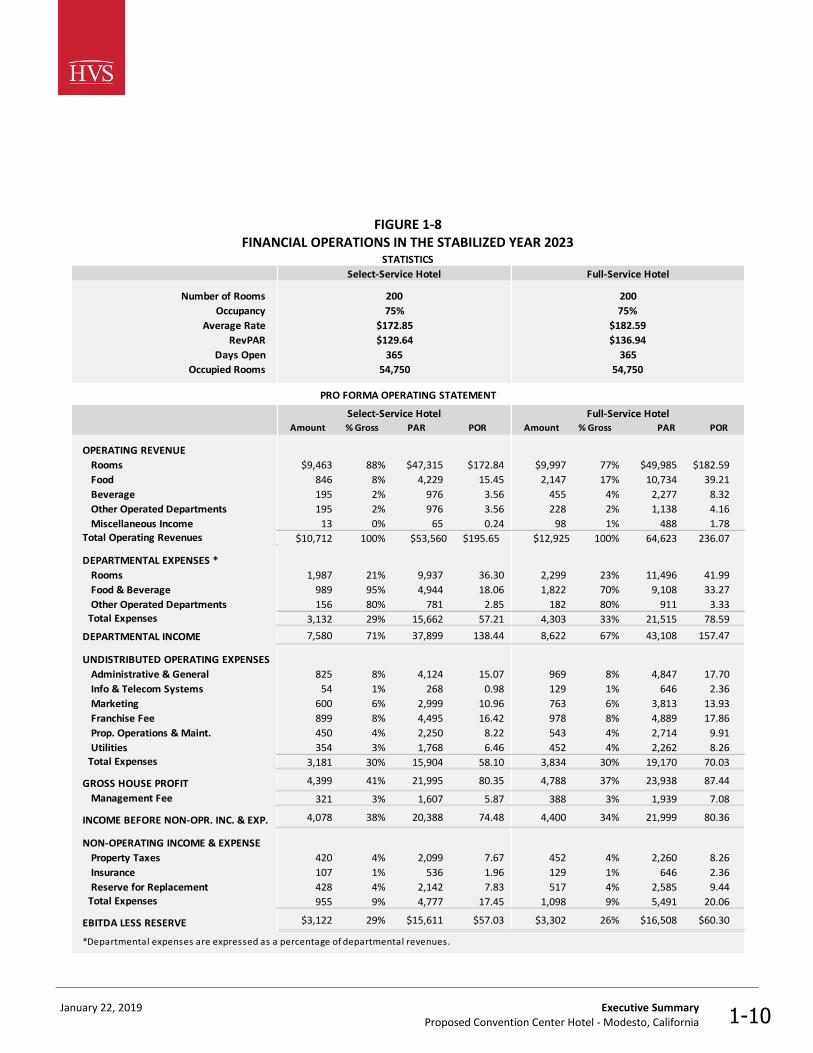

HVS supports its estimates of revenue and expense levels using data on the operations of comparable hotels and factors specific to this market. Three common measures of hotel financial performance are 1) ratio to sales (“RTS”), 2) amounts per available room (“PAR”), and 3) amounts per occupied room night (“POR”) which are used to present the financial data. Figure 1-8 presents the HVS forecast of income and expense for a stabilized year of operation for the Proposed Hotel. HVS has also studied a full-service hotel, which is included for comparison purposes.

Summary of Forecast Income and Expense Statement

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-10

FIGURE 1-8 FINANCIAL OPERATIONS IN THE STABILIZED YEAR 2023

STATISTICS

Select-Service Hotel Full-Service Hotel

Number of Rooms 200 200

Occupancy 75% 75%

Average Rate $172.85 $182.59

RevPAR $129.64 $136.94

Days Open 365 365

Occupied Rooms 54,750 54,750

PRO FORMA OPERATING STATEMENT

Select-Service Hotel Full-Service HotelAmount % Gross PAR POR Amount % Gross PAR POR

OPERATING REVENUE

Rooms $9,463 88% $47,315 $172.84 $9,997 77% $49,985 $182.59

Food 846 8% 4,229 15.45 2,147 17% 10,734 39.21

Beverage 195 2% 976 3.56 455 4% 2,277 8.32

Other Operated Departments 195 2% 976 3.56 228 2% 1,138 4.16

Miscellaneous Income 13 0% 65 0.24 98 1% 488 1.78Total Operating Revenues $10,712 100% $53,560 $195.65 $12,925 100% 64,623 236.07

DEPARTMENTAL EXPENSES *

Rooms 1,987 21% 9,937 36.30 2,299 23% 11,496 41.99

Food & Beverage 989 95% 4,944 18.06 1,822 70% 9,108 33.27

Other Operated Departments 156 80% 781 2.85 182 80% 911 3.33 Total Expenses 3,132 29% 15,662 57.21 4,303 33% 21,515 78.59

DEPARTMENTAL INCOME 7,580 71% 37,899 138.44 8,622 67% 43,108 157.47

UNDISTRIBUTED OPERATING EXPENSES

Administrative & General 825 8% 4,124 15.07 969 8% 4,847 17.70

Info & Telecom Systems 54 1% 268 0.98 129 1% 646 2.36

Marketing 600 6% 2,999 10.96 763 6% 3,813 13.93

Franchise Fee 899 8% 4,495 16.42 978 8% 4,889 17.86

Prop. Operations & Maint. 450 4% 2,250 8.22 543 4% 2,714 9.91

Utilities 354 3% 1,768 6.46 452 4% 2,262 8.26 Total Expenses 3,181 30% 15,904 58.10 3,834 30% 19,170 70.03

GROSS HOUSE PROFIT 4,399 41% 21,995 80.35 4,788 37% 23,938 87.44

Management Fee 321 3% 1,607 5.87 388 3% 1,939 7.08

INCOME BEFORE NON-OPR. INC. & EXP. 4,078 38% 20,388 74.48 4,400 34% 21,999 80.36

NON-OPERATING INCOME & EXPENSE

Property Taxes 420 4% 2,099 7.67 452 4% 2,260 8.26

Insurance 107 1% 536 1.96 129 1% 646 2.36

Reserve for Replacement 428 4% 2,142 7.83 517 4% 2,585 9.44 Total Expenses 955 9% 4,777 17.45 1,098 9% 5,491 20.06

EBITDA LESS RESERVE $3,122 29% $15,611 $57.03 $3,302 26% $16,508 $60.30

*Departmental expenses are expressed as a percentage of departmental revenues.

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-11

A full-service hotel operation varies from a select-service operation in the following ways.

• Due to brand quality and a greater concentration of high rated commercial and meeting and group guests, a full-service hotel generates a higher ADR.

• Higher ADR and comparable levels of occupancy generate more rooms revenue.

• With larger amounts of function space, a full-service hotel generates more catering revenue.

• The ratio of rooms department expense to rooms revenue is higher due to service standards,

• The ratio of food and beverage department expenses to revenues is due because catering sales have better profit margins than the food outlets,

Given these considerations, a full-service hotel would generate approximately, $200,000 more in earnings before interest, tax, depreciation, and amortization (“EBITDA”) in a stabilized year of operation. Please refer to Section 8 of this study, Projection of Income and Expense, for a detailed explanation of the methodology used in deriving our forecast of financial operations.

In a stabilized year of operations, approximately $3.12 million would be available to pay debt service and provide a return on equity on a select-service hotel. If the full-service option was developed $3.3 million would be available to pay debt service and provide a return on equity. While the full-service hotel would generate more income, its capital costs would be substantially higher than a select-service hotel. Consequently, the full-service hotel would have a financing gap as explained in the following discussion.

We used a discounted cash flow analysis to estimate the present value of hotel net operating income using the assumptions shown in Figure 1-9.

Opinion of Net Present Value of the Proposed Hotel

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-12

FIGURE 1-9 PRELIMINARY ESTIMATE OF VALUE

Select-Service

(Proposed Hotel)Full-Service

Loan/Value 65% 65%

Amortization 25 25Term 10 10

Interest Rate 5.0% 5.0%Terminal Cap Rate 8.5% 8.0%Transaction Costs 2.0% 2.0%

Equity Yields 16.0% 16.0%Tax Rate 1.086% 1.086%

Tax Inflation Rate 2.0% 2.0%

Value per room $186,000 $200,000

The financing assumptions for the Proposed Hotel reflect current credit market conditions for hotel financing. HVS relied on its survey of hotel transactions to determine debt–equity splits, yield requirements, and capitalization rates. The discounted cash flow analysis includes a calculation of a reversionary value of the hotel after ten-years of operations. The reversionary value is estimated by dividing the tenth year of operating income by a capitalization rate and subtracting transactions costs as if the hotel were sold. Due to the Proposed Hotel's California location and the higher property tax implications upon the hypothetical sale at the end of ten years, the terminal capitalization rate is loaded with the tax rate and applied to the net operating income estimate before property taxes.

The full-service hotel estimated value per room of $200,000 per room is $14,000 higher than the select-service hotel estimated value of $186,000 per room.

But the costs of construction of a full-service hotel are significantly higher than a select service property. Factors contributing to the higher cost per room for the full-service hotel option include,

• Larger ballroom and meeting space

• Larger and more upscale restaurant and lounge,

• Upgraded furnishing in the guest rooms and public spaces,

• Larger public spaces, and

• More expensive fit and finish to both the rooms and the public spaces.

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-13

A 200-room select-service hotel would have a value of approximately $37.2 million or $186,000 per room. Development costs including land could range from $185,000 to $215,000 per room. Consequently, the funding gap could range from slightly above breakeven to $5.8 million. In the absence of a specific project plan, these estimates should be considered rough approximations of value and costs.

A 200-room full-service hotel would have a value of approximately $40.0 million or $200,000 per room. Development costs including land could range from $225,000 to $275,000 per room. Consequently, the funding gap could range from ($5.0) million to ($15.0) million. These cost estimates should be considered rough approximations.

The higher funding gap for the full-service hotel makes this option infeasible without a significant financial contribution by the City to the project. The select-service hotel is the preferred option for hotel development because it would:

• Require a significantly lower funding gap with the lower range of potential development costs slightly above breakeven,

• Provide the ability to offer two different hotel options to MCP users, the full-service DoubleTree Hotel and the select-service Proposed Hotel, and

• Respond to the overall market demand for high-quality select-service hotels with potential commercial and leisure travelers.

The City should identify practical next steps to determine whether the Proposed Hotel can be developed which may include the following.

• Updating the appraisal of the MCP to determine the fair market value of the site.

• Evaluating physical attributes of the site through American Land Title Association (“ALTA”) survey or other methods to determine possible impact to development (i.e. utilities, fee title ownership, paper streets, etc.).

• Ascertaining the City’s ability to negotiate a property purchase and hotel development project with a single party (adjacent hotel owner) and preferred path forward, which may include preparing and issuing a Request for Qualifications and Proposals concerning the Proposed Hotel.

• The City should determine the options for providing parking for both the needs for the Proposed Hotel and the surrounding downtown area, and to

January 22, 2019 Executive Summary Proposed Convention Center Hotel - Modesto, California 1-14

replace the lost surface public parking that would be displaced by the Proposed Hotel.

• The City should determine what tools it is willing to consider that would ensure an economically viable hotel project, an updated and efficiently operated convention center, and ample infrastructure.

• Exploring the sale or long-term lease of the MCP to the ownership of the DoubleTree or developer of the Proposed Hotel as part of a negotiated agreement. Debt is still owned on the MCP.

An extraordinary assumption is one which relates directly to the Proposed Hotel development and which, if found to be false, could alter our opinions or conclusions. Extraordinary assumptions presume as fact otherwise uncertain information about physical, legal, or economic characteristics of the Proposed Hotel, or about conditions external to the property such as market conditions or trends, or about the integrity of data used in an analysis. An extraordinary assumption may be used in the analysis only if it is required to develop credible options and conclusions; a reasonable basis exists for the assumption, use of the extraordinary assumption results in a credible analysis. HVS discloses the use of any extraordinary assumption.

• The development of a parking facility that will serve the parking demand generated by the Proposed Hotel along with other downtown parking demand and replace the public surface parking lost due to the construction of the Proposed Hotel.

• The MCP would be improved to meet the standards of the adjacent hotels either by the City or the developer of the Proposed Hotel through a public-private partnership.

• Through common ownership or cooperative marketing and sales efforts, the DoubleTree, MCP and the Proposed Hotel would attract new group room night demand to Modesto as discussed later in this study.

Our analysis does not address unforeseeable events that could alter the financial performance of the proposed project and the market conditions reflected in the analyses. We assume that no significant changes, other than those anticipated and explained in this study, would take place from the date of HVS’ site visit or from the date of this study. Our findings are subject to all the assumptions and limiting conditions described herein. The reader should contact the authors with any questions after reading the study.

Extraordinary Assumptions

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-1

2. Description of Site and Proposed Hotel

The suitability of the land for the operation of a lodging facility is an important consideration affecting the economic viability of a property and its ultimate marketability. The key site characteristics that affect the viability of a hotel property include its capacity to accommodate the project, accessibility, visibility, and supporting road and utility infrastructure, as well as land use policies such as zoning criteria, design guidelines, and building standards. The quality of a lodging facility's physical improvements has a direct influence on marketability, occupancy, and average room rate. The design and functionality of the structure can also affect operating efficiency and overall profitability.

The site for the Proposed Hotel is in downtown Modesto at the site of the MCP in the temporary surface parking on 11th street between L Street and K Street, as shown on the following site plan.

SITE PLAN FOR DOUBLETREE HOTEL, MCP, AND TEMPORARY PARKING

For the purposes of this study, HVS assumes that the hotel will be a select-service hotel conforming to the brand-specific guidelines, including construction and operational brand standards. Our forecast assumes that the property will be

Site Description

Description of the Proposed Hotel

L STREETr'

rOu j1

^WuCtKOlLL/COCK

Proposedi

Hotel Site•_CONFERENCE / CONVENTIONa HOTEL tcrtuCENTERK -

E I IUU«OC«-'vctriNS JPi« XC

.ST*.AN

~ i d at^«cw-.ZWITO* -UJNMT

K STREET

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-2

maintained in a competitive condition, undergoing regular renovations of soft goods and case goods funded primarily by a reserve for replacement.

Figure 2-1 shows the features of the Proposed Hotel.

FIGURE 2-1 PROPOSED HOTEL FACILITIES

Guestroom Configuration Keys

Kings 110

Queen/Queen 80

One-Bedroom Suite 10

Tota l (ADA-Compl iant Rooms per Loca l Code) 200

Food & Beverage FacilitiesSeating

Capacity

Restaurant 70

Lounge 30

Indoor Meeting & Banquet FacilitiesSquare Feet

Combined

Bal l room 2,400Meeting Room 800Board Room 600

Total Square Feet of Meeting Space 3,800

Amenities & Services

Outdoor Pool Bus iness Center

Outdoor Whirlpool Gi ft Shop

Fitness Center Guest Laundry Room

Infrastructure

Parking Spaces Hotel 200

Elevators 2 Guest/1 Service

Li fe Safety Systems Sprinklers , Smoke Detectors

Construction Deta i ls Steel/Concrete

The lobby will be appropriate for a select-service hotel with limited meeting space. The Proposed Hotel will offer a restaurant, lounge, room service, and banquet operations. The hotel will feature standard and suite-style guestroom configurations. Guestroom bathrooms will be of a standard size, with a shower-in-tub, commode, and single sink with vanity area, featuring a stone countertop. The property will be attached to the MCP. The hotel structure is a single building, which

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-3

will be constructed of steel and poured concrete with a minimum of five stories and a maximum of 15 stories. The Proposed Hotel is expected to become one of the premier lodging and meeting facilities in the City of Modesto.

The site does not have the capacity to support the development of the Proposed Hotel and adequate parking to serve the hotel’s parking demand, without costly construction of underground or structured parking. A limited number of surface parking spaces could be available on the site of the Proposed Hotel depending on the final development plan. But a minimum of 200 spaces are necessary to support the Proposed Hotel and the existing parking supply displaced by the project would most likely need to be replaced. For the purposes of this study, we assume that parking would be available in an adjacent parking garage.

Figure 2-2 shows the Proposed Hotel’s ballroom and meeting space which will allow the property to host small events.

FIGURE 2-2 PROPOSED HOTEL MEETING SPACE CAPACITY

Approximate Guest Capacity

Banquet Classroom Reception

Bal l room 2,400 150 96 180

Meeting Room 800 50 32 60

Floor Area

(square feet)Function Space

The proposed hotel would be part of a larger hotel and convention center complex that includes the DoubleTree Hotel and the MCP. Our projections assume that cooperative efforts to attract group business to this complex would generate room night demand for the Proposed Hotel.

Figure 2-3 shows the combined meeting space for the DoubleTree Hotel, the MCP, and the Proposed Hotel.

FIGURE 2-3 COMBINED MEETING SPACE

DoubleTree Hotel, MCP, and Proposed Hotel

DoubleTree

Hotel

Modesto

Centre Plaza

Proposed

HotelTotal

Square Feet

per Room

Bal l rooms 5,152 16,000 2,400 23,552 51

Meeting Space 2,895 7,000 800 10,695 23

Boardrooms 460 600 1,060 2

Total Meeting Space 8,507 23,000 3,800 35,307 77

Hotel and MCP Complex

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-4

For this study, we assume the Proposed Hotel would include the following:

• A well-designed, functional layout of support areas, restaurant & lounge, ballroom & meeting space, and guestrooms.

• The hotel staff would be adequately trained to allow for a successful opening.

• Pre-marketing efforts would have introduced the product to major local accounts for at least six months in advance of the opening date.

• Meet all pertinent codes and brand standards.

• Open and operational on the assumed opening date,

• Construction would not create any environmental hazards.

After its opening, the Proposed Hotel would require ongoing upgrades and periodic renovations to maintain its competitive level in this market. The forecasted reserve for replacement should adequately fund these costs if the hotel’s staff employs a successful, ongoing maintenance program.

The topography of the site is generally flat, and the shape permits efficient use of the site for building and site improvements, including ingress and egress. The site will not contain any significant portion of undeveloped land that could be sold, entitled, and developed for alternate use. Building and site improvements will occupy the entire site.

According to the City of Modesto, the site is served by all necessary utilities.

Geological and soil reports were not provided to us or made available for our review during the preparation of this study. We are not qualified to evaluate soil conditions other than by visual inspection of the surface; no extraordinary conditions were apparent.

The City of Modesto did not inform HVS of any site-specific nuisances or hazards at the proposed site, and there were no visible signs of toxic ground contaminants at the time of our inspection. Because we are not experts in this field, we do not warrant the absence of hazardous waste and urge the reader to obtain an independent analysis of these factors.

State Route 99 is a north–south state highway, stretching almost the entire length of the Central Valley. From its southern end at Interstate 5 near Wheeler Ridge to its northern end at State Road 36 near Red Bluff, State Road 99 goes through the densely populated eastern parts of the valley. Cities served include Bakersfield, Delano, Tulare, Visalia, Kingsburg, Selma, Fresno, Madera, Merced, Turlock,

Capital Expenditures

Site Utility

Soil and Subsoil Conditions

Nuisances and Hazards

Access and Visibility

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-5

Modesto, Stockton, Sacramento, Yuba City, and Chico. The site for the Proposed Hotel in downtown Modesto is easily accessible and visible from State Route 99.

REGIONAL ACCESS

Norman Y. Mineta San Jose International Airport, which is located approximately 80 miles by car to the west of the Site for the Proposed Hotel, provides the closest air service. Sacramento International Airport is located approximately 85 miles by car to the north of the Site. Additional airport options include San Francisco International Airport, Oakland International Airport, Stockton Metropolitan Airport, and Fresno Yosemite International Airport.

The neighborhood surrounding a lodging facility often has an impact on a hotel's status, image, class, style of operation, and sometimes its ability to attract and properly serve a market segment.

The site for the Proposed Hotel is adjacent to the MCP and near the DoubleTree Hotel. Downtown Modesto has numerous dining and entertainment options, the McHenry Mansion and Museum, the Gallo Center for the Arts, the City/CountyAdministration Building, office buildings, and public transit facilities. The Altamont Commuter Express is expected to expand to Modesto by 2023.

Airport Access

Neighborhood

uroisom KirkwoodHealdsburgo ©Sacramento

o r nL J

Santa Rosa Elk GroveoVacaville o

o

BridgeportStanislausNational Forest

©Lee Vining

O

Concord SonoraStockton oo O oTuolumne Yosemite

National ParkSan Franciscoipo °Mam Inyo Na

ForMol^stoo ^Oakdale o

YosemiteValley O

MammLakeTurlock Mariposa Fish CampPalo Alto

o

fgijSan Joseo

Oakhurst Sierra NationalForestMercedo oo

Chowchillao

Los BanosO

Maderao

Hollistero

Google MonHn+a r----- ''--p* fMap data ©2018 Google Terms of Use Report a map errorr'-i;

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-6

NEIGHBORHOOD

According to the Federal Emergency Management Agency map illustrated on the following page, the site is in flood zone X (shaded).

Flood Zone

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-7

COPY OF FLOOD ZONE MAP

The flood zone definition for the X designation is as follows: areas of minimal flood hazard, which are the areas outside the Special Flood Hazard Area and higher than the elevation of the 0.2% annual-chance flood, are labeled Zone C or Zone X

(unshaded).

The site is zoned CD Central Downtown. This zone is intended to foster the most intensive and active urban environment in the downtown while ensuring an overall human scale to development. This is accomplished with large, but unobtrusive building envelopes that accommodate a mixture of uses, including residential, with an interface that promotes a very strong public-private connection and lively streetscape. A hotel is a permitted use in the CD zone.

We are not aware of any easements attached to the possible sites that would significantly affect the utility of the property or marketability of this project.

Zoning

Easements and Encroachments

National Flood Hazard Layer FIRMette LegendFEMA37'38'43 83"N SEE FIS REPORT FOR DETAILED LEGEND US INDEX M*P FOR FIRM PANEL LAYOUT

Without Base Flood Elevation (BFE)A.v.Ata

With BFE or Depth *E to AH «.AR

Regulatory FloodwaySPECIAL FLOODHAZARD AREAS

0.2*Annual Chance Flood Hazard.Areasof 1* annual chance flood with averagedepth less than one foot or with drainageareas of less than one square mile z««« xFuture Conditions1*AnnualChance Flood Hazard axitx

Area with ReducedFloodRisk due toLevee.See Notes. X

Area with Flood Risk due to Leveezsn* oOTHER AREAS OF

FLOOD HAZARD

IO SCREEN! Area of MinimalFlood Hazard zo»* xEffective LOMRs

OTHER AREAS Area of Undetermined Flood Hazard zw»

- channel, Culvert, or storm Sewer

111111 Levee.Dike, or FloodwallGENERAL

STRUCTURES

Q ;°: Cross Sections w ith1*Annual Chance—H2 water surface Elevation© Coastal Transect—n— Base Flood Elevation Line (BFE)

Limit of StudyJurisdiction BoundaryCoastal Transect Baseline

- - Profile BaselineHydrographic Feature

OTHERFEATURES

Digital Data Available

No Digital Data AvailableMAP PANaS Unmapped

The pin displayed on the map is an approximatepoint selected bythe user and does not representan authoritative property location.

This map complies with FEMA's standards for the use ofdigital flood maps if it is not void as described below.The basemap shown complies with FEMA's basemapaccuracy standardsThe flood hazard information is derived directly from theauthoritative NFHL web services provided by FEMA.This mapwas exported on1J/5/2018 at3:07:11PM and does notreflect changes or amendments subsequent to this date andtime The NFHL and effective information may change orbecome superseded by new data over time.This map image is void if the one or more of the following mapelements do not appear: basemap imagery, flood zone labels,legend,scale bar.map creation date,community identifiers,FIRM panel number, and FIRM effective date. Map images forunmapped and unmodemized areas cannot be used forregulatory purposes.1,000 1,500 2,000

January 22, 2019 Description of Site and Proposed Hotel Proposed Convention Center Hotel - Modesto, California 2-8

The ownership structure for the Proposed Hotel has not been determined as of the date of this study, except to rule out any public ownership or financing. A hotel management agreement would be negotitated upon the future sale of the site and approval of a hotel development. We have included a market-appropriate management fee of 3.0% of gross operating revenues. Other charges related to the affiliation, such as frequent guest programs, are reflected in the appropriate departmental expenses, consistent with the Uniform System of Accounts for the Lodging Industry (“USALI”).

We recommend that the Proposed Hotel operates as an AAA three diamond upper-upscale or upscale, select-service hotel. While we have placed heavy consideration on the Hilton or Marriott brand, a specific franchise affiliation has yet to be finalized. Our projections reflect a Hilton, Marriott or similar brand affiliation. We assume that the Proposed Hotel will obtain a brand from a national brand and will retain its brand affiliation throughout the holding period. Inherent in this assumption is the expectation that the property will be operated in accordance with brand standards, including requirements for services and cleanliness; that the hotel will be maintained in good condition, with all building systems in good working order; and that any necessary refurbishments or renovations will be completed in a timely manner and in accordance with the requirements of the brand.

For this analysis, we assume that the Proposed Hotel would be financed and designed sometime in 2019 and after a one-year construction period, the hotel would open on January 1, 2021.

Ownership, Franchise, and Management Assumptions

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-1

3. Modesto Market Overview

HVS explored economic and demographic factors that affect the level of lodging demand in the market including population, income, employment, retail sales, business presence, major tourism attractions, and transportation access. We relied on third party data sources to review historical trends and provide forecasts of the rate of growth or decline of the local economy. We also assessed whether the neighborhood surrounding the site would support the development of the Proposed Hotel. This market overview provides a framework for projections of lodging demand and revenue growth in the local market.

Our analysis of the outlook for this specific market also considers the broader context of the national economy. The U.S. economy expanded during the last three years, with a relatively low point in growth occurring during the fourth quarter of 2015. Most recently, the U.S. economy expanded by 2.2% and 4.2% in the first two quarters of 2018, respectively. The recent growth is the highest level since the third quarter of 2014. In the second quarter of 2018, non-residential fixed investment increased more than anticipated, primarily boosted by software and information processing equipment; conversely, imports fell, mainly related to petroleum.

National Economic Trends

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-2

FIGURE 3-1 UNITED STATES GDP GROWTH RATES

2010 Q1 1.6%

Q2 3.9%

Q3 2.8%

Q4 2.8%

2011 Q1 -1.3%

Q2 3.2%

Q3 0.8%

Q4 4.6%

2012 Q1 2.3%

Q2 1.6%

Q3 2.5%

Q4 0.1%

2013 Q1 1.9%

Q2 1.1%

Q3 3.1%

Q4 4.0%

2014 Q1 -1.2%

Q2 4.0%

Q3 5.0%

Q4 2.0%

2015 Q1 3.2%

Q2 2.7%

Q3 1.0%

Q4 0.4%

2016 Q1 1.5%

Q2 2.3%

Q3 1.9%

Q4 1.8%

2017 Q1 1.8%

Q2 3.0%

Q3 2.8%

Q4 2.3%

2018 Q1 2.2%

Q2 4.2%

Source: Bureau of Economic Analysis

U.S. economic growth continues to support expansion of lodging demand. In 2018, demand growth through July registered 2.9%, stronger than the 2.7% level recorded in 2017. The economic growth, low unemployment, higher levels of personal income, and stability in the U.S. economy as of mid-year 2018 is helping to maintain strong interest in hotel investments by a diverse array of market participants.

The market area includes all of Modesto, California and the surrounding area, as illustrated in the following map.

Market Area Definition

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-3

MAP OF MARKET AREA

HVS used the Complete Economic and Demographic Data Source published by Woods & Poole Economics, Inc., a well-regarded forecasting service based in Washington, D.C. as a source of economic and demographic data. Using a database containing more than 900 variables for each county in the nation, Woods & Poole employs a sophisticated regional model to forecast economic and demographic trends. Census data and information published by the Bureau of Economic Analysis provide the basis for historical statistics. Woods & Poole formulates the projections, and all dollar amounts have been adjusted for inflation, thus reflecting real change. Figure 3-2 summarizes this data.

Economic and Demographic Review

© © aan Miiuieas

LockefordRio Vista © r nL JLodi

Angels CampMorada Columbia© Antioch

Copperopolis Sonorajncord

t Creek ^Mt Diablo Discovery Bay G)TuolumneStockton

©(© Groveland Buck

Meadows_ Manteca @)Oakdale<3* Tracy

f® Modesto ®Ceres

(?32) CoultervilleSalidaLa GrangePleasanton

Vernalis

iwards —nciscoitional HornitosTurlockife... MariPatterson

Catheys Valleytain Livingston #w

AtwaterSan JoseNewman

^ Gustine

(165) ® Merced Planada

Goggle Map data ©2018 Google Terms of Use , Report a map error

Jan

uar

y 2

2, 2

01

9

Mo

de

sto

Mar

ket

Ove

rvie

w

P

rop

ose

d C

on

ven

tio

n C

ente

r H

ote

l - M

od

esto

, Cal

ifo

rnia

3-4

FIG

UR

E 3

-2

ECO

NO

MIC

AN

D D

EMO

GR

AP

HIC

DA

TA S

UM

MA

RY

E

con

om

ic I

nd

ica

tor/

Are

aB

eg

inn

ing

A

mo

un

t2

00

02

01

02

01

82

02

5E

nd

ing

A

mo

un

tR

esi

de

nt

Po

pu

lati

on

(m

illi

on

s)S

tan

isla

us

Co

un

ty0

.45

0.5

91

.0%

Mo

de

sto

, C

A M

SA

0.4

0.6

1.0

%M

od

es

to-M

erc

ed

, C

A C

SA

0.7

0.9

1.0

%S

tate

of

Ca

l ifo

rnia

33

.99

42

.93

1.0

%U

nit

ed

Sta

tes

28

2.1

63

50

.94

0.9

%P

er-

Ca

pit

a P

ers

on

al

Inco

me

* (

tho

usa

nd

s)S

tan

isla

us

Co

un

ty$

28

.92

$4

1.1

1.1

%M

od

es

to,

CA

MS

A$

28

.92

$4

1.1

1.1

%M

od

es

to-M

erc

ed

, C

A C

SA

$2

7.2

7$

39

.61

.1%

Sta

te o

f C

al i

forn

ia$

39

.81

$5

6.8

1.1

%U

nit

ed

Sta

tes

$3

6.8

1$

50

.21

.2%

W&

P W

ea

lth

In

de

xS

tan

isla

us

Co

un

ty$

78

.22

$8

1.7

5-0

.1%

Mo

de

sto

, C

A M

SA

$7

8.2

2$

81

.75

-0.1

%M

od

es

to-M

erc

ed

, C

A C

SA

$7

4.2

0$

78

.88

-0.1

%S

tate

of

Ca

l ifo

rnia

$1

07

.97

$1

12

.69

-0.1

%U

nit

ed

Sta

tes

$1

00

.00

$1

00

.00

0.0

%F

oo

d a

nd

Be

ve

rag

e S

ale

s* (

bil

lio

ns)

Sta

nis

lau

s C

ou

nty

$0

.46

$0

.84

1.6

%M

od

es

to,

CA

MS

A$

0.4

6$

0.8

41

.6%

Mo

de

sto

-Me

rce

d,

CA

CS

A$

0.6

1$

1.1

51

.7%

Sta

te o

f C

al i

forn

ia$

46

.67

$8

4.6

51

.5%

Un

ite

d S

tate

s$

36

8.8

3$

66

2.6

11

.5%

To

tal

Re

tail

Sa

les*

(b

illi

on

s)S

tan

isla

us

Co

un

ty$

5.6

6$

7.9

01

.5%

Mo

de

sto

, C

A M

SA

$5

.66

$7

.90

1.5

%M

od

es

to-M

erc

ed

, C

A C

SA

$7

.52

$1

0.5

11

.5%

Sta

te o

f C

al i

forn

ia$

44

6.4

8$

65

4.1

41

.5%

Un

ite

d S

tate

s$

3,9

02

.83

$5

,59

8.2

41

.4%

* In

fla

tio

n A

dju

ste

d

Est

ima

ted

An

nu

al

Co

mp

ou

nd

Ch

an

ge

2

01

8 t

o 2

02

5

So

urc

e: W

oo

ds

& P

oo

le E

con

om

ics,

Inc.

Th

e ch

arac

teri

stic

s o

f an

are

a's

wo

rkfo

rce

ind

icat

e th

e ty

pe

and

am

ou

nt

of t

ran

sien

t vi

sita

tio

n l

ikel

y to

be

gen

erat

ed b

y lo

cal

bu

sin

esse

s.

Sect

ors

su

ch

as f

inan

ce,

insu

ran

ce,

and

re

al

esta

te

(“F

IRE

”);

wh

ole

sale

tr

ade;

an

d

serv

ices

p

rod

uce

a

con

sid

erab

le

nu

mb

er

of

visi

tors

w

ho

ar

e n

ot

par

ticu

larl

y

rate

-sen

siti

ve.

Th

e go

ver

nm

ent

sect

or

oft

en

gen

erat

es

tran

sien

t ro

om

n

igh

ts,

bu

t p

er-d

iem

re

imb

urs

emen

t al

low

ance

s o

ften

lim

it t

he

acco

mm

od

atio

ns

sele

ctio

n t

o b

ud

get

and

Wo

rkfo

rce

Ch

arac

teri

stic

s

p

*

1

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-5

mid-priced lodging facilities. Contributions from manufacturing, construction, transportation, communications and public utilities (“TCPU”) employers can also be important, depending on the company type.

Figure 3-3 shows the estimated change in employment in the top ten sectors in the Stanislaus County workforce distribution by the various business sectors in 2000, 2010, and 2018, and a forecast for 2025.

FIGURE 3-3 TOP TEN EMPLOYMENT SECTORS IN STANISLAUS COUNTY

Sector/Geographic Area Employment

Beginning

Amount

(thousands)

2000 2010 2018 2025

Ending

Amount

(thousands)

Stanislaus County

Health Care And Socia l Ass is tance 19.7 41.3

Retai l Trade 25.4 33.2

State And Local Government 23.8 32.0

Manufacturing 25.0 24.0

Accommodation And Food Services 12.1 22.0

Other Services , Except Publ ic Adminis tration 11.8 16.4

Construction 13.5 15.1

Adminis trative And Waste Services 11.0 13.9

Transportation And Warehous ing 5.7 13.6

Real Estate And Rental And Lease 6.0 11.5

Other 51.3 59.8

Total Stanislaus County 205.3 282.9

U.S. 165,372 223,254

Source: Woods & Poole Economics, Inc.

The health care and social assistance, retail trade, state and local government, accommodation and food service, other services except public administration, construction, administrative and waste services, transportation and warehousing, and real estate and rental and lease sectors of the economy should continue to expand along with the overall growth in the local economy. From 2018 to 2025 Health Care And Social Assistance are expected to expand at the faster rate for a total increase of 20.4%. The only top ten sector projected to decline from 2018 to 2025 is Manufacturing, for a total decline of -0.8%. The construction sector has continued to recover from the significant decline due to the last recession.

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-6

Figure 3-4 presents historical unemployment rates for the Proposed Hotel’s market area.

FIGURE 3-4 UNEMPLOYMENT STATISTICS

Year Modesto MSA California USA

2008 9.5 % 11.1 % 7.3 % 5.8 %

2009 13.4 15.5 11.2 9.3

2010 16.6 16.9 12.2 9.6

2011 16.2 16.5 11.7 8.9

2012 14.6 14.9 10.4 8.1

2013 12.7 12.9 8.9 7.4

2014 10.9 11.2 7.5 6.2

2015 9.3 9.5 6.2 5.3

2016 7.8 8.6 5.5 4.9

2017 6.8 7.5 4.8 4.4

Recent Month - Oct

2017 5.8 % 6.0 % 4.2 % 4.1 %

2018 5.5 5.5 4.0 3.8

Source: U.S. Bureau of Labor Statistics

Locally, the unemployment rate was 6.8% in 2017; for this same area in 2018, the most recent month’s unemployment rate was registered at 5.5%, versus 5.8% for the same month in 2017. Unemployment rates in the Modesto, CA MSA have historically exceeded those of the state and nation. Farming and agriculture, as well as food distribution and related industries, make up a sizeable portion of the total area employment; these sectors are traditionally labor-intensive and seasonal.

Figure 3-5 shows the largest employers in the region.

Unemployment Statistics

Major Business and Industry

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-7

FIGURE 3-5 TOP EMPLOYERS IN MODESTO

Employer Industry

Save Mart Supermarkets Retail Grocer

E. & J. Gallo Winery Winery, Manufacturing and Distribution

Stanislaus County Community Service/Local Government

Modesto City Schools School District

Doctors Medical Center Hospital

Memorial Medical Center Hospital

Foster Farms Food Manufacturing

Del Monte Foods Food Manufacturing

Stanislaus Food Products Food Manufacturing

Ceres Unified School District School District

Source: City of Modesto

A significant number of the largest employers in Stanislaus County are in the wine, food products, poultry, and food processing companies. Agricultural related activities are the foundation of the local economy.

The following bullet points highlight major demand generators for this market:

• Agriculture is the primary industry in the region due to the fertile lands in the surrounding area. The Modesto area is home to Blue Diamond Growers, one of the largest suppliers of nuts in the county, as well as other agriculture-related companies such as Foster Farms, Royal Robbins, Fiscalini Cheese, and Sciabica Olive Oil.

• Modesto is the home of the corporate headquarters and primary facilities of E & J Gallo Winery. Founded in 1933 by brothers Ernest and Julio Gallo, E & J Gallo Winery is the largest family-owned winery in the United States. The Gallo Glass Company, an affiliate of Gallo Winery, is also located in the area and is considered the largest wine-bottle manufacturing company in the world.

• Due to the large concentration of agriculture companies in the area that produce food products, the food processing industry is also a significant sector in the region. Food processing companies in the area include Del Monte, Ceres, and Frito-Lay.

The agriculture industry and wineries, as well as the area's proximity to Yosemite National Park, have created a strong base of tourism and employment. From 2007 through mid-year 2009, however, the market realized a slowdown consistent with that of the national economy. The market has recovered from the recession with increasing activity in agricultural related product with an emphasis on nuts, and

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-8

wine production & processing. The prevalence of food processing and agriculture firms, as well as the wineries, places the area in an advantageous position for economic development and growth in the future.

Norman Y. Mineta San Jose International Airport, which is approximately 82 miles by car from the site, is located at the north end of San Jose, near the intersections of three major freeways. San Jose International is the smallest of the three Bay Area airports offering scheduled service. Like Oakland International Airport, this airport attracts suburban residents who find SFO to be inconveniently distant from their homes. The airport also serves as a “reliever” airport in the Bay Area; discount carriers prefer this airport to San Francisco International because of better weather conditions and a lack of fog. The airport is serviced by a variety of commercial airlines. Phase I of the facility’s $1.3-billion terminal upgrade project, which was completed in June 2010, included the reconstruction of Terminal B, upgrades to Terminal A, and the addition of a new rental car and parking garage. An $82-million, 240,000-square-foot terminal (designed specifically to serve corporate planes owned by Google) opened in 2016. In January 2018, the aviation director announced plans for another expansion at the airport to accommodate the recent surge in demand. The new $1-billion expansion is anticipated to extend Terminal B to the south and increase the number of gates from 31 to at least 40 by 2024.

The airport has recently experienced rapid growth with new international flights from the expansion of Alaska Airlines following the acquisition of Virgin America. Jet Blue, Frontier Airlines, Delta Air Lines, and United Airlines have all added service to additional cities.

Airport Traffic

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-9

FIGURE 3-6 AIRPORT PASSENGERS

NORMAN Y. MINETA SAN JOSE INTERNATIONAL AIRPORT

YearPassenger

Traffic

Annual Percentage

Change

2008 9,717,717

2009 8,321,750 -14.4%

2010 8,246,064 -0.9%

2011 8,357,384 1.3%

2012 8,296,174 -0.7%

2013 8,783,319 5.9%

2014 9,385,212 6.9%

2015 9,799,427 4.4%

2016 10,796,725 10.2%

2017 12,480,232 15.6%

YTD through November

2017 11,387,495

2018 13,130,215 15.3%

Source: Norman Y. Mineta San Jose International Airport

Passenger traffic has increased for the last five years after a decline in 2009 and three years of stagnation. Through the most recent monthly data of 2018, passenger traffic has grown to 13,130,215 from 11,387,49 an increase of 15.3%.

Oakland International Airport (OAK) is located eight miles south of Downtown Oakland in Alameda County, California, and is one of three international airports in the San Francisco Bay Area. Major commercial airlines, specifically low-cost carriers, service the airport. The Bay Area Rapid Transit (BART) line to Oakland International Airport opened to the public on November 2014. Interior construction is underway to modernize the Terminal 1 complex and to make needed seismic retrofitting improvements; most of the project has been completed, with only improvements to the areas around the Terminal 1 security checkpoint remaining. In June 2017, the airport received a $37.4-million grant from the Federal Aviation Administration to rehabilitate the airport's main runway. The $67-million renovation of 8,300 feet of runway asphalt was completed in September 2017. Aside from the runway renovations, the airport also debuted the first phase of its expanded International Arrivals Building in December 2017, a $45-million project doubling the building’s capacity.

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-10

FIGURE 3-7 AIRPORT PASSENGERS

OAKLAND INTERNATIONAL AIRPORT

YearPassenger

Traffic

Annual Percentage

Change

2008 11,474,456

2009 9,505,281 -17.2%

2010 9,542,333 0.4%

2011 9,266,570 -2.9%

2012 10,040,864 8.4%

2013 9,742,887 -3.0%

2014 10,336,788 6.1%

2015 11,205,063 8.4%

2016 12,070,967 7.7%

2017 13,072,245 8.3%

YTD thru November

2017 11,985,857

2018 12,504,182 4.3%

Source: Oakland International Airport

Passenger traffic has increased for the last five years after a decline in 2009 and three years of stagnation. Through the most recent monthly data of 2018, passenger traffic has grown to 12,504,182 from 11,985,857an increase of 4.3%.

Sacramento International Airport is the gateway to Northern California and serves the greater Sacramento region, including Stockton, Chico, and Napa. This four-runway facility services multiple international and national carriers, offering 145 nonstop flights to 30 destinations. Completed in 2012, The Big Build was a $1.08-billion airport modernization project to replace the airport’s almost 40-year-old Terminal B to meet the rising demand for passenger services and improve the airport’s ability to attract new carriers and routes. The new 680,000-square-foot Terminal B facility was completed in the fall of 2011, including offices for airline support services, parking, and an automated people mover to connect the two terminals. Demolition of the old Terminal B and construction of new overnight aircraft parking space were completed in August 2012. The 17,000-square-foot food court in Terminal A was remodeled in 2015, and new local restaurants were added. Sacramento became one of nine airports to join the Global Entry program by the U.S. Customs and Border Protection Department in July 2016; the program currently includes 75 airports worldwide.

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-11

The recent increase in passenger traffic can be attributed in large part to expanded service by major air carriers in response to stronger economic conditions and a rise in demand. Within the last few years, airlines have added new direct flights to cities including Seattle, Boston, Chicago, Baltimore, Mexico City, Orlando, St. Louis, and Cabo.

FIGURE 3-8 AIRPORT PASSENGERS

SACRAMENTO INTERNATIONAL AIRPORT

YearPassenger

Traffic

Annual Percentage

Change

2008 9,982,427

2009 8,914,510 -10.7%

2010 8,850,239 -0.7%

2011 8,929,289 0.9%

2012 8,910,570 -0.2%

2013 8,685,368 -2.5%

2014 8,972,756 3.3%

2015 9,609,880 7.1%

2016 10,118,794 5.3%

2017 10,912,079 7.8%

YTD through August

2017 7,065,416

2018 7,872,054 11.4%

Source: Sacramento International Airport

Passenger traffic has increased for the last five years after a decline in 2009 and three years of stagnation. Through the most recent monthly data of 2018, passenger traffic has grown to 7,872,054 from 7,065,416 an increase of 11.4%.

San Francisco International Airport (SFO) is situated about 90 miles by car from the Site. SFO is one of the busiest airports in the country, with extensive international and national service. The airport features ample amenities and services, which include various restaurants, shops, spa treatments, business centers, an aviation library, and a children's area. In May 2013, airport officials unveiled a ten-year, $4.1-billion capital improvement plan to upgrade the airport's facilities, creating more than 36,000 jobs over the next ten years. A new air-traffic-control tower, which replaced a control tower located atop Terminal 2, was completed in January 2014. In November 2015, the airport unveiled a 53,000-square-foot expansion of its Terminal 3 East Concourse, which connects boarding areas E and F; this project also

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-12

included three new boarding gates, a new United Club location, and a larger central security checkpoint. In June 2016, a groundbreaking ceremony was held for the renovation of Terminal 1, the airport’s oldest facility. The $2.4-billion project, slated to be completed in phases between 2016 and 2024, will create an interim boarding area to accommodate passenger activity while a new structure takes shape; once completed, Boarding Area B will feature a total of 24 gates. Furthermore, a 351-room Grand Hyatt is currently under construction on the site of the former Hilton Hotel. The hotel will feature direct access to the airport’s AirTrain light-rail system when it opens in July 2019.

FIGURE 3-9 AIRPORT PASSENGERS

SAN FRANCISCO INTERNATIONAL AIRPORT

YearPassenger

Traffic

Annual Percent

Change

2008 37,403,000

2009 37,454,000 0.1%

2010 39,117,000 4.4%

2011 40,810,000 4.3%

2012 44,477,000 9.0%

2013 45,012,000 1.2%

2014 47,155,000 4.8%

2015 50,067,000 6.2%

2016 53,096,000 6.0%

2017 55,815,000 5.1%

YTD through November

2017 51,171,825

2018 53,129,871 3.8%

Source: San Francisco International Airport

Passenger traffic has increased every year since 2008. Through the most recent monthly data of 2018, passenger traffic has grown to 53,129,871 from 51,171,825, an increase of 3.8%.

The City of Modesto offers a variety of affordable attractions throughout the region; from the local ranch tours to water sports on Don Pedro to Tuolumne range excursions. Primary attractions in the area include the following:

• According to the Modesto Convention and Visitors Bureau, the Bloomingcamp Ranch, Modesto Certifies Farmer’s Market, Hilmar Cheese Company, and

Tourist Attractions

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-13

Oakdale Cheese & Specialties are among the most frequented attractions by leisure travelers visiting Modesto. Due to the large amount of acreage required to contain the facilities necessary to produce the area’s agricultural products, these attractions are situated around Modesto's periphery.

• John Thurman Field is home to the Class A–Advanced team in the California League Modesto Nuts baseball team (minor league farm team for the Seattle Mariners) and hosts annual concerts and tradeshows.

• Rainbow Fields, a privately-owned sports complex, offers six ball fields total; four fields are equipped with lights and 300-foot fences. The two additional fields are non-lit youth-fields; with fences reaching 200 feet, plus a 6,000-square-foot clubhouse, and a large children's playground area outdoors.

• Mary Grogan Park, a 42-acre community park located in Modesto has seven fields. Three of the fields are synthetic turf and the entire complex is lighted.

• Downtown tourism attractions include museums and historical sites. Once the home of a prominent local banker and rancher, the Robert McHenry Mansion was constructed in 1883 and shows the Victorian and Italianate architectural styles of the late 1800s. Works of art depicting life in Modesto’s early days are on display at the Robert McHenry Museum. Crystal Creamery, EJ Gallo, Fiscallini, Sciabica and Ratto Bros Farm all offer pre-arranged private tours.

• The Gallo Center for the Performing Arts opened in October of 2007. The performing arts center is in Downtown Modesto, adjacent to the Tenth Street Place, a mixed-use development that features a 1,200-seat concert theatre, a 400-seat performance theatre, concession stands, and a landscaped outdoor plaza. The concert hall is home to the Modesto Symphony.

• The 1,200 square mile Yosemite National Park in the Sierra Nevada mountains is located 85 miles from Modesto. The park features giant, ancient sequoia trees, and Tunnel View, the iconic vista of towering Bridal Veil Falls and the granite cliffs of El Capitan and Half Dome. Yosemite Village offers shops, restaurants, lodging, the Yosemite Museum, and the Ansel Adams Gallery.

• Agricultural Attractions: According Yelp, the region offers 46 farm stands that offer a variety of fresh produce and nuts. These range from Modesto Certified Farmers Market to Loretelli Farms and from Stewart & Jasper to the Strawberry Stand on North McHenry. There are also 5 U-Pick farms within a short drive from Modesto.

January 22, 2019 Modesto Market Overview Proposed Convention Center Hotel - Modesto, California 3-14

• Sports & Recreation; The Modesto Marathon draws a large attendance as a qualifier for the Boston and NYC Marathons. Ride-for-Mom draws cycling enthusiasts throughout northern California every May. Other sports attractions include several private and public golf courses, tennis tournament facilities at Brenda Athletic Clubs, and a swim master’s program at Modesto Junior College. The area supports eight shooting ranges and Gun Clubs. Modesto offers two popular bowling alleys.

• Natural Recreation Facilities; Fly and Bass fishing in the region regularly draw anglers from the Bay Area. Water sports and reservoir boating activities bring in regulars from Silicon Valley’s Tech Companies as well as local families. Though skiing, hiking, fishing, camping, and high-country fishing are in Tuolumne County, many who participate travel to Modesto for a ‘base’ to take in these activities. Calaveras Big Trees are some of the world’s largest trees.

• Shopping; Modesto offers a large variety of local shops, chain stores, and the region’s busiest shopping mall - Vintage Faire Mall. Shops range from an Apple Store to DWS and from Pier 1 to the eclectic range of stores at McHenry Village.

The regional economy was significantly affected by the recent recession, as noted by the high level of unemployment. Given that the agricultural industry is the cornerstone of this region, the local economy is not as diversified as other markets; however, diversification has increased over the last couple of decades. The services, food processing, and manufacturing sectors do help to balance out the economic make-up of the area. While the local economy is expected to remain somewhat suppressed in the near term, an increase in the area's population, coupled with the City's expanding role as a regional center for the surrounding counties, should support moderate growth over the long term as the local and national economies recover in earnest. The outlook for the area is optimistic.

Conclusion

January 22, 2019 Supply and Demand Analysis Proposed Convention Center Hotel - Modesto, California 4-1

4. Supply and Demand Analysis

Changes in the national lodging market indirectly affect local markets. HVS reviewed national lodging trends to provide context for the forecast of the supply and demand for the Proposed Hotel’s competitive set.

Figure 4-1 presents annual hotel occupancy and average rate data since 1987. RevPAR, the product of occupancy and average rate provides a combined measure of rate and occupancy.

Figure 4-1 shows the hotel occupancy, average rate, and RevPAR throughout the U.S.

FIGURE 4-1 U.S. OCCUPANCY, AVERAGE RATE, AND REVPAR TRENDS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$0

$20

$40

$60

$80

$100

$120

$140

ADR RevPAR Occupancy

Source: STR

Following the significant RevPAR decline experienced during the last recession, demand growth resumed in 2010, led by select markets that had recorded growth trends in the fourth quarter of 2009. A return of business travel and some group activity contributed to these positive trends. The resurgence in demand was partly fueled by the significant price discounts that were widely available in the first half of 2010. These discounting policies were largely phased out in the latter half of the

National Hotel Market Trends

January 22, 2019 Supply and Demand Analysis Proposed Convention Center Hotel - Modesto, California 4-2

year, balancing much of the early rate loss. Demand growth remained strong, but decelerated from 2011 through 2013, increasing at rates of 4.7%, 2.8%, and 2.0%, respectively. Demand growth then surged to 4.0% in 2014, driven by a strong economy, a robust oil and gas sector, and limited new supply of hotels, among other factors. By 2014, occupancy had surpassed the 64% mark. Average rate rebounded similarly during this time, bracketing 4.0% annual gains from 2011 through 2014.