Huntsville Healthcare Update post eventfiles.ctctcdn.com/769d0cef001/5839a148-0f4c-468f-a... ·...

51

Agenda: 6:00pm – Welcome, Jeremy Russell 6:05pm – Legal Update, Brad Robertson, Esq. 6:35pm – Health Care Reform, Maddox Casey, CPA 7:00pm – Collections & ICD-10, Jim Stroud, CPA 7:30pm – Q&A, Sae Evans, CPA 7:55pm – Closing, Sae Evans, CPA Sponsored By: HEALTHCARE UPDATE

Transcript of Huntsville Healthcare Update post eventfiles.ctctcdn.com/769d0cef001/5839a148-0f4c-468f-a... ·...

Agenda:6:00pm – Welcome, Jeremy Russell6:05pm – Legal Update, Brad Robertson, Esq.6:35pm – Health Care Reform, Maddox Casey, CPA7:00pm – Collections & ICD-10, Jim Stroud, CPA7:30pm – Q&A, Sae Evans, CPA7:55pm – Closing, Sae Evans, CPA

Sponsored By:

HEALTHCARE UPDATE

babc.com ALABAMA I DISTRICT OF COLUMBIA I MISSISSIPPI I NORTH CAROLINA I TENNESSEE

False Claims ActFraud and Abuse Update

October 15, 2013Brad Robertson

© 2013 Bradley Arant Boult Cummings LLP

Introduction• Federal spending on Medicare/Medicaid exceeds $800

billion/year• President and Congress blame fraud for rising healthcare

costs• Top Priority of HHS and Department of Justice

– In 2009, “fighting Medicare and Medicaid fraud became a Cabinet‐level priority for both DOJ and HHS.”

– In 2011 fiscal year, “recovered a record $4.1 billion in criminal and civil fraud payments.”

– In early 2012, “rounded up 107 suspects as a part of the Medicare Fraud Strikeforce.”

– In first half of 2013, expected recovery of $3.28 billion; charges filed against 91 individuals

– Patient Protection and Affordable Care Act made it easier to prove violations.

3

© 2013 Bradley Arant Boult Cummings LLP

Reimbursement Backdrop

• Health Care is unique• Services typically are paid by Third Party Payorswhich have limited or no involvement in the selection and provision of the underlying service

• Amount of reimbursement typically determined by Third Party Payor

• Nature of the Third Party Reimbursement environment increases potential for false claims

4

© 2013 Bradley Arant Boult Cummings LLP

The Federal False Claims Act (FCA)Liability for submission of false claims extends to one who:

“knowingly presents, or causes to be presented a false or fraudulent claim for payment or approval.”

31 USC § 3729(a)(1)(A)

“knowingly makes, uses or causes to be made or used, a false record or statement material to a false

or fraudulent claim”31 USC § 3729(a)(1)(B)

“conspires to commit [an FCA violation].”31 USC § 3729(a)(1)(C)

5

© 2013 Bradley Arant Boult Cummings LLP

False Claims Act: Falsity and Knowledge

• “False or fraudulent” is not defined– What is “false?”

• Factually false (e.g., services not performed)• Express false certification (e.g., medically unnecessary care)• Implied false certification (e.g., noncompliance with other laws)

• “Knowingly” defined as– Actual knowledge of the falsity of the information– Acting in deliberate ignorance – Acting with reckless disregard

6

© 2013 Bradley Arant Boult Cummings LLP

Civil Penalties

• Damages–3 times amount claimed

• Penalties–$5,500 to $11,000 per claim

7

© 2013 Bradley Arant Boult Cummings LLP

Top FCA Settlements• GlaxoSmithKline* $2 billion• Bank of America $1 billion• Pfizer* $1 billion• Tenet Healthcare $900,000,000• Abbott* $800,000,000• HCA* $731,400,000 • Merck $650,000,000 • HCA* $631,000,000 • Serono Group* $567,000,000 • TAP Pharm. Products Inc.* $559,483,560 • New York City and State $540,000,000• AstraZeneca $520,000,000• Eli Lilly $438,000,000

8

* Asterisk means criminal penalties also were assessed in addition to the dollar amounts noted here. Individual states may also have recovered separately in addition to the amounts reflected here.

© 2013 Bradley Arant Boult Cummings LLP

Top FCA Settlements• Schering Plough $435,000,000• Novartis Pharmaceuticals* $422,500,000• Abbott Labs * $400,000,000 • Fresenius Med. Care of N. America* $385,000,000 • Cephalon* $375,000,000• Bristol‐Myers Squibb $328,000,000• SKB Clinical Labs $325,000,000• Northrop Grumman $325,000,000• HealthSouth * $325,000,000• National Medical Enterprises * $324,200,000• Gambro Healthcare $310,000,000• Mylan $280,000,000• Roxanne $280,000,000

9

© 2013 Bradley Arant Boult Cummings LLP

Top FCA Settlements• St. Barnabas Hospitals $265,000,000• Bayer Corp. * $257,200,000• Schering Plough $250,000,000 • Quest Diagnostics * $241,000,000• Tuomey Healthcare System (judgment) $237,000,000• Amerigroup (judgment) $225,000,000 • First Amer. Health Care Of Ga. $225,000,000• Deutsche Bank $202,000,000• Actavis $202,000,000• BankAmerica * $187,000,000• Lab. Corporation of America * $182,000,000 • Aventis Pharmaceuticals $180,000,000 • Beverly Enterprises Inc. * $170,000,000 • Zimmer Inc. $169,500,000

10

© 2013 Bradley Arant Boult Cummings LLP

Recent Provider FCA SettlementsFacility Millions Description

Staten Island University Hospital 88

Hospital billed Medicaid and Medicare for inpatient alcohol and substance abuse detoxification treatment beds for which it did not have certification, inflated its patient count, and fraudulently billed Medicare for stereotactic body radiosurgery treatment that was provided on an out‐patient basis to cancer patients

Medline Industries 85 Bribes/Kickbacks

Cox Medical Centers 60Violations of Stark self‐referral law based on agreement with physician group, providing financial inducements for physicians to refer patients to Cox; Submission of false cost reports improperly reporting overhead costs

Condell Medical Center 36 Violations of Stark self‐referral law and Anti‐Kickback Statute

Detroit Medical Center 30 FCA, Anti‐Kickback Statute and Stark allegations based on improper financial relationships with referring physicians

Saint Joseph's Hospital of Atlanta Inc. and Saint Joseph's Health System Inc 26 Billed outpatient visits as inpatient admissions

HealthSouth Corporation and two physicians, Drs. James Andrews and Lawrence Lemak

14.9 Paid illegal kickbacks to physicians who referred patients for care in some of its hospitals, outpatient rehabilitation clinics, and ambulatory surgery centers

Baptist Health South Florida Inc. 7.75 Stark violations based on excessive compensation to oncology group that was a source of patient referrals to two of Baptist's hospitals

Warren Hospital in Phillipsburg, N.J., 7.5 Hospital system improperly increased charges to Medicare in order to obtain enhanced outlier payments

MedCath Corporation (Arizona Heart Hospital) 5.8 Billed for endoluminal graft devices (utilized to treat aneurysms) that had not

received final marketing approval from the Food and Drug Administration

Cathedral Healthcare System Inc 5.3 Hospital system improperly increased charges to Medicare in order to obtain enhanced outlier payments

11

© 2013 Bradley Arant Boult Cummings LLP

Variety of Potential Enforcers

• Criminal Assistant US Attorneys• Civil Assistant US Attorneys• Office of the Inspector General• State Attorneys General• Medicaid Fraud Control Units• Qui Tam Relators (whistleblowers)

12

© 2013 Bradley Arant Boult Cummings LLP

Qui Tam Provisions• Action may be brought by a relator (whistleblower) on behalf of the U.S. government under the statute’s qui tam provisions

• Relator can be anyone with knowledge, for example– Current or former employee– Competitor– Consultant

• Relator files the case under seal; Government gets a chance to determine whether it wants to intervene and take over prosecution

• Relator’s share– 15% to 25% if government intervenes– 25% to 30% if government does not intervene

13

© 2013 Bradley Arant Boult Cummings LLP

Enhanced Investigation Techniques• Government using data mining tools to spot billing irregularities in Medicare and Medicaid– Aug. 2012 – Opening of $3.6 million Medicare fraud command center

• Giant screen surrounded by semicircles of computer workstations for data processing and communication with investigators around the country.

• “NCIS‐Medicare”– May 2013 – New rule allows State Medicaid Fraud Control Units to receive federal financial support for data mining efforts

• Result: More audits and investigations seemingly initiated based on statistical irregularities

© 2013 Bradley Arant Boult Cummings LLP

Investigatory Tools• Document Collection

– Subpoenas– Civil Investigative Demands

• Interviews– Current Employees– Former Employees– Others

• Grand Jury Investigations• Search Warrants

If you encounter any of these, call an attorney.

© 2013 Bradley Arant Boult Cummings LLP

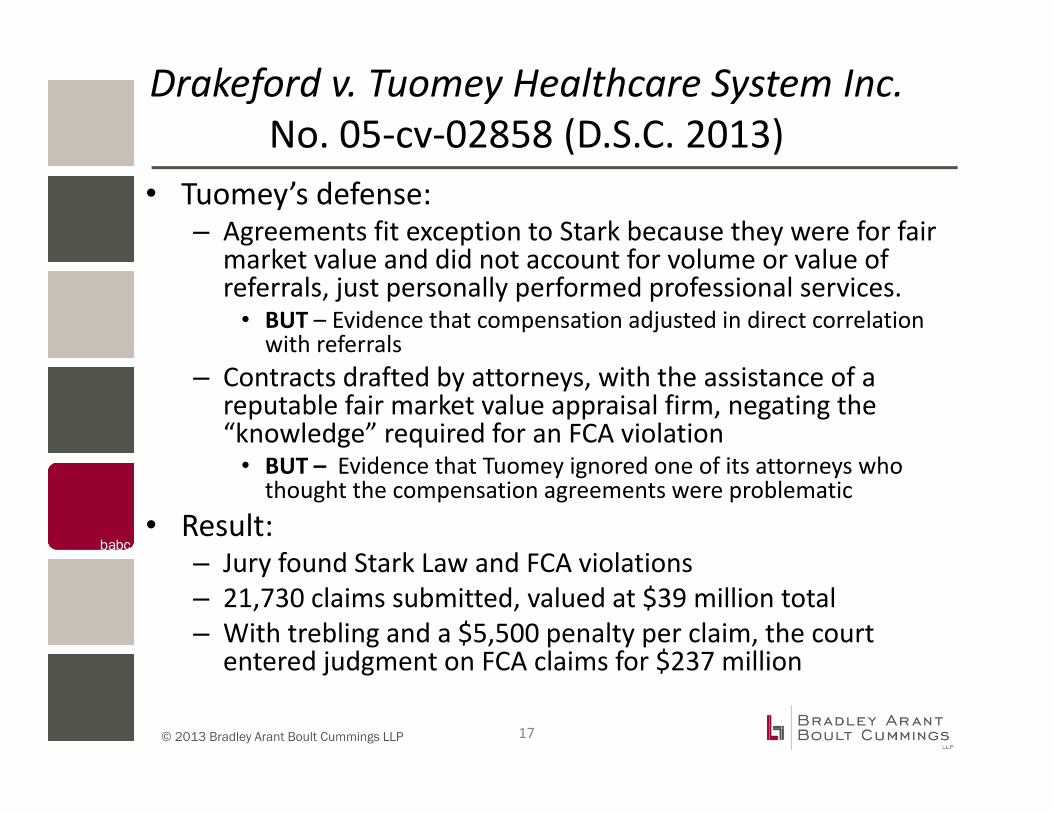

Drakeford v. Tuomey Healthcare System Inc. No. 05‐cv‐02858 (D.S.C. 2013)

• Hospital subsidiaries contracted with physicians– Collected the professional fees for the physicians’ work from

payors– Paid the physicians

• A base salary tied to their collections• A “productivity bonus” of 80% of their collections• An additional quality incentive bonus up to 5.6% of their collections

• Hospital received corresponding facility fees from payors for each procedure performed

• Government’s theory: Contracts constituted impermissible self‐referral agreements in violation of Stark Law; any resulting claims submitted to Medicare were false in violation of False Claims Act– Even though physicians did not contract directly with Tuomey, but

with its subsidiaries, they had “indirect compensation arrangements” because their compensation “varies with, or otherwise takes into account, the volume or value of referrals.”

16

© 2013 Bradley Arant Boult Cummings LLP

Drakeford v. Tuomey Healthcare System Inc. No. 05‐cv‐02858 (D.S.C. 2013)

• Tuomey’s defense: – Agreements fit exception to Stark because they were for fair

market value and did not account for volume or value of referrals, just personally performed professional services.

• BUT – Evidence that compensation adjusted in direct correlation with referrals

– Contracts drafted by attorneys, with the assistance of a reputable fair market value appraisal firm, negating the “knowledge” required for an FCA violation

• BUT – Evidence that Tuomey ignored one of its attorneys who thought the compensation agreements were problematic

• Result:– Jury found Stark Law and FCA violations– 21,730 claims submitted, valued at $39 million total– With trebling and a $5,500 penalty per claim, the court

entered judgment on FCA claims for $237 million

17

© 2013 Bradley Arant Boult Cummings LLP

US ex rel. Heesch v. Diagnostic Physicians GroupNo. 11‐0364 (S.D. Ala.)

• Interventional cardiologist Dr. Christian Heesch brought suit against his former employer Diagnostic Physicians Group (DPG) and Infirmary Health Systems entities (IHS) in Mobile

• IHS clinics allegedly provided financial incentives for DPG physicians to refer diagnostic imaging tests to IHS– Tests performed by IHS personnel on IHS equipment; billed by IHS– Allegedly remunerated DPG with a percentage of the government

reimbursement for the technology fees – DPG tracked physicians’ “Stark collections”

• Heesch alleges that violations of Stark Law, Anti‐Kickback Statute and False Claims Act tainted $522 million in claims

• Federal government intervened to take over the case

© 2013 Bradley Arant Boult Cummings LLP

Reverse False Claims• Liability for reverse false claims extends to anyone who:

• This language is broader than it used to be, due to 2009 amendments.– The final clause (“or knowingly conceals or knowingly and

improperly avoids or decreases an obligation to pay or transmit money or property to the Government”) is a new addition.

“knowingly makes, uses, or causes to be made or used, a false record or statement material to an

obligation to pay or transmit money or property to the Government, or knowingly conceals or

knowingly and improperly avoids or decreases an obligation to pay or transmit money or property to

the Government.”31 USC § 3729(a)(1)(G)

19

© 2013 Bradley Arant Boult Cummings LLP

Overpayments

• Affirmative obligation to report and return overpayments now imposed, due to amendments in the Affordable Care Act:

• “Overpayment’’ means “any funds that a person receives or retains under [Medicare or Medicaid] to which the person, after applicable reconciliation, is not entitled.”

”A person that has received an overpayment shall—(A) report and return the overpayment to the

Secretary, the State, an intermediary, a carrier, or a contractor, as appropriate, at the correct address; and

(B) Explain in writing the reason for the overpayment.”

42 U.S.C. § 1320a-7k(d)

20

© 2013 Bradley Arant Boult Cummings LLP

Failure to Refund Overpayments• What if a provider holds money it shouldn’t have?

• Affordable Care Act requires report and return of “overpayment” by the later of – 60 days after overpayment is “identified”; or– The date any corresponding cost report is due, if applicable

• Failure to report and return in time makes overpayment a “false claim” subject to penalties under the FCA

• If no attempt to identify over‐payments, was failure still “knowing?”

21

© 2013 Bradley Arant Boult Cummings LLP

US ex rel. Keltner v. Lakeshore Med. Clinic, Ltd.No. 11‐cv‐00892 (E.D. Wis. March 28, 2013)

• Action brought by former billing employee alleging failure to repay overpayments.

• Alleged that defendant discovered in an annual audit that two physicians had upcoding error rates greater than 10%.

• Hospital repaid the specific identified overpayments, but did not go back to review other claims from the physicians. Also, ceased auditing these physicians going forward.

• Court denied defendant’s motion to dismiss.– Relator “plausibly suggest[ed] that [Lakeshore] acted with reckless

disregard for the truth and submitted some false claims.”– Lakeshore “intentionally refused to investigate the possibility that

it was overpaid” and “may have unlawfully avoided an obligation to pay money to the government.”

22

© 2013 Bradley Arant Boult Cummings LLP

Self‐Disclosure Protocol• Option to admit potential violations via OIG’s Provider Self‐Disclosure

Protocol (SDP)– Must specify law potentially violated, agree to waive statute of limitations

defense, and ensure that corrective actions have been implemented and misconduct ceased

• Benefits– Likelihood of lesser damages and no Corporate Integrity Agreement

• General practice is to require “a minimum multiplier of 1.5 times single damages”• Required Corporate Integrity Agreement in only 1 out of 235 settled SDP matters

– Lower risk of government investigation or whistleblower action– Obligation to report and return overpayments suspended while self‐

disclosure is pending• Risks

– No guarantee of acceptance into the SDP program– Self‐disclosure could become evidence against you in any pending sealed

qui tam– OIG does not guarantee DOJ leniency or participation in settlement

OIG’s Provider Self‐Disclosure Protocol (updated April 17, 2013)

© 2013 Bradley Arant Boult Cummings LLP

Expanded Applicability of the FCAUnder the Affordable Care Act

• Anti‐Kickback Statute (AKS) amended to state:

• Health insurance exchanges explicitly covered; Damages enhanced. 42 U.S.C. § 18033(a)(6).• “Payments made by, through, or in connection with an

Exchange are subject to the False Claims Act (31 U.S.C. 3729 et seq.) if those payments include any Federal funds.”

• Damages “shall be increased by not less than 3 times and not more than 6 times the amount of damages.”

“In addition to the penalties provided for in this section . . . a claim that includes items or services resulting from a violation of this section [the AKS]

constitutes a false or fraudulent claim.”42 U.S.C. § 1320-7b(g)

24

Healthcare Reform

D. Maddox Casey, CPAWarren Averett

• Employer mandate provision takes effect Jan. 1, 2015

• The act doesn’t require employers to provide coverage• May impose penalties on larger employers that don’t offer

coverage or that provide coverage that doesn’t qualify as “affordable”

• Employers with 50+ full-time employees that don’t provide coverage may be penalized

• A full-time employee is one working at least 30 hours per week or 130 hours per month

Pay or play provisionHealthcare Reform

• Employed an average of at least 50 full-time employees, including full-time equivalent employees during the preceding year

• The employer will need to determine the total number of full-time employees and full-time equivalent employees on a monthly basis and take the average for the year

• Full-time equivalents are computed by dividing the aggregate number of hours of service by employees who are not full-time for the month by 120

• An employer with 40 part timers who average 90 hours per month would have 30 FTEs (40 x 90 = 3,600/120 = 30)

• Transition relief is afforded for the 2013 look-back period where employers can look to a time period of less than 12 months, but not less than 6 months (which must be consecutive)

Large employer status test (TEST 1)Healthcare Reform

• Methods for determining hours worked for part-time employees

• For hourly employees this is based on the hours worked and hours for which payment is made or due for vacation, holiday, illness, incapacity, layoff, jury duty, military duty or leave of absence

• For salaried employees may use:

• The same method used for hourly employees

• A days-worked equivalency method (credited for 8 hours per day worked)

• A weeks-worked equivalency method (credited for 40 hours per week worked)

Large employer status testHealthcare Reform

• Must combine employees for companies that share a common owner or are otherwise related

• Stock possessing at least 80 percent of the total combined voting power of all classes of stock entitled to vote or at least 80 percent of the total value of shares of all classes of stock of each of the corporations

• Two or more corporations if 5 or fewer persons who are individuals, estates, or trusts own stock possessing more than 50 percent of the total combined voting power of all classes of stock entitled to vote or more than 50 percent of the total value of shares of all classes of stock of each corporation, taking into account the stock ownership of each such person only to the extent such stock ownership is

Large employer status testHealthcare Reform

• Not required to include seasonal employees defined as those working 120 days or less during a calendar year

• For example, an employer has 40 full-time employees, no full-time equivalent employees and 90 full-time seasonal employees for 4 months out of the year. The employer does not meet the definition of a large employer because the employees in excess of 50 are all seasonal employees.

Large employer status testHealthcare Reform

• Two options for a defined large employer

1. Drop group coverage

2. Continue group coverage

Large employer status test (TEST 2)Healthcare Reform

• The annual penalty for a large employer not offering coverage is $2,000 per full-time employee in excess of 30 workers

• The penalty will be calculated on a monthly basis at $166.67 per full-time employee in excess of 30 workers

• Penalties will only be assessed if one or more full-time employees purchases coverage through an exchange and receives a premium credit

1. Assessing the penalty for dropping coverageHealthcare Reform

Penalty exampleHealthcare Reform

• Employers that provide coverage must meet two requirements:

• Minimum essential value• Affordability

If either is not met:

• The annual penalty is the lesser of $3,000 per employee for each worker receiving a premium credit, or $2,000 for each full-time employee beyond first 30 employees

• This requires two penalty computations to determine the lower penalty

2. Continue group coverageHealthcare Reform

• The health plan must cover at least 60% of the healthcare expenses for a typical population

• The IRS and U.S. Department of Health and Human Services will provide an online minimum value calculator

• The employee’s share of the premium coverage cannot exceed more than 9.5% of their annual household income

• Employee’s cost of single coverage won’t exceed 9.5% of W-2 wages (look back approach)

• Employee’s contribution for the self-only premium is equal to or less than 9.5% of the computed monthly wages (current pay approach)

• Employee’s cost for self-only coverage doesn’t exceed 9.5% of the federal poverty level for a single individual (for 2013 = $11,490 x 9.5% = $1,092)

Minimum value and affordabilityHealthcare Reform

Employer offers healthcare coverage that meets the minimum value requirements and the total cost the of coverage is $6,000 per year for employee coverage.

Affordability exampleHealthcare Reform

• Employer with 53 full-time employees providing coverage with employee premiums in excess of 9.5% of employee income for a number of employees. Plus add the cost of coverage from our previous example.

• 10 employees receive premium credit – penalty is lesser of:10 x $3,000 = $30,00023 x $2,000 = $46,000

• 20 employees receive premium credit – penalty is lesser of:20 x $3,000 = $60,00023 x $2,000 = $46,000

Penalty examplesHealthcare Reform

First test (large employer status test)

• Possibility for outsourcing business tasks such as accounting, finance, public relations or CFO function to an unrelated entity

• Limiting seasonal employees to less than 120 days per year

Minimizing penalties (test 2)

• Managing the total hours of certain employees to under 30 hours per week on average

Planning opportunitiesHealthcare Reform

Employers will be allowed to implement a 90 day waiting period before providing coverage to new full-time employee

Additional GuidanceHealthcare Reform

Mandate requires most Americans to purchase health insurance by 2014.

They will have the following options:

• Pay the penalty• Year 1- $95 or 1% of taxable income• Year 2-$325 or 2% of taxable income• Year 3-$695 of 2.5% of taxable income

• Purchase coverage through an exchange• States have the option of implementing and running their own exchange or the

federal government will run the exchange in states that do not• An exchange is a government-regulated marketplace for purchasing

affordable healthcare coverage• Premium credits will be available for individuals with income less than or equal

to 400% of the federal poverty level. For a family of 4 in 2012 this is $92,200

Options for individuals without coverageIndividual Mandate

Healthcare Reform

D. Maddox Casey, CPASenior Manager, [email protected]

Maddox Casey joined Warren Averett in 2004 and is a Managerin the Firm’s Healthcare Consulting Group. He specializes inmatters such as tax compliance, year-end planning consultationand personal income tax planning for closely held entities andtheir ownership. Maddox also works with many physicianpractices providing medical practice management, physiciancompensation and incentive plan services.

Profile

Collections andICD-10

James A. Stroud, CPAWarren Averett

Collections

The perfect storm• Technology

• Practice management system up to date

• Electronic eligibility to determine co-pay and out-of-pocket cost

• Enhanced merchant services for drafting credit cards and checking accounts

Collections

The perfect storm• Process

• Prepare front desk to increase point of service collections

• Train surgery scheduler and financial counselors to collect prior to scheduled services

• Shorten the statement period

• Train billing staff to call patients with balances

• No more promissory notes, only payment arrangements with merchant service

Collections

The perfect storm• Policies

• Prepare consistent billing and collection policies

• Physicians should be consistent and support the staff in collection efforts

ICD-10

Time line• Payer testing March 2014

• Physician training March 2014

• October 1, 2014

ICD-10

Vital Statistics• Currently 13,000 ICD-9 codes but ICD-10 incorporates 140,000

diagnosis codes

• ICD-10 will require an increased level of specificity not currently documented

• Only 5% of ICD-9 codes have a one to one match with and ICD-10 code

• 30 – 40% of ICD-9 codes utilized by physicians are unspecified codes

• Hiring a coder will not solve vague medical records

ICD-10

Challenges• Early Planning

• Super bills

• Accurate coding

• EMR or date practice management system

• Consultant

James A. Stroud, [email protected]

Jim Stroud has been with Warren Averett since 1988 and is aMember of the Firm’s Healthcare Consulting Group. With over30 years of accounting and consulting experience, Jimrepresents a diverse client base spanning various industries.Jim specializes in working with medical and dental practices inmatters such as compensation and incentive plans, ownershipand management succession, staff training and motivation, andimplementation of continuous practice improvementmechanisms. Jim serves as facilitator for management andstaff retreats and is a frequent speaker to various groups.

Profile