HUD 202 refinanciing: Preserving multifamily properties · Welcome! HUD 202 fi i P i ltif il tiHUD...

40

Welcome! HUD 202 fi i P i ltif il ti HUD 202 refinancing: Preserving multifamily properties Presented by: Don Bernards, Partner – Baker Tilly Brian Coate, Vice President – Lancaster Pollard Ryan Miles, Vice President – Lancaster Pollard Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International.

Transcript of HUD 202 refinanciing: Preserving multifamily properties · Welcome! HUD 202 fi i P i ltif il tiHUD...

Welcome!HUD 202 fi i P i ltif il tiHUD 202 refinancing: Preserving multifamily properties

Presented by:Don Bernards, Partner – Baker Tillyy

Brian Coate, Vice President – Lancaster PollardRyan Miles, Vice President – Lancaster Pollard

Baker Tilly refers to Baker Tilly Virchow Krause, LLP,an independently owned and managed member of Baker Tilly International.

About the presenters

D B d CPAB i C t Don Bernards, CPAPartnerBaker [email protected] 608 240 2643

Brian CoateVice PresidentLancaster [email protected] 614 224 8800 141 608 240 2643614 224 8800 x141

Ryan MilesVice PresidentLancaster [email protected] @ p614 224 8800 x155

2

Agenda

Today we will review:> P ti t l t h t th S ti 202 Di t L> Pertinent regulatory changes to the Section 202 Direct Loan

Program and how those changes effect available financing> Financing sources available, including Low-Income Housing

C ( C) ( )Tax Credit (LIHTC) and Federal Housing Administration (FHA) loan programs

> How HUD is looking at sale proceeds > The ability to transfer ownership under the new guidelines

3

History

> Housing Notice 2002-16– Allowed properties to RefinanceAllowed properties to Refinance

> Housing Notice 2004-21– Allowed a Developers Fee

> H i N ti 2010 11> Housing Notice 2010-11– Modernized underwriting to match industry

> Housing Notice 2012-08– Increased Developers Fee, expanded uses

> Housing Notice 2012-14– Requires owners to use Residual Receipts balancesRequires owners to use Residual Receipts balances

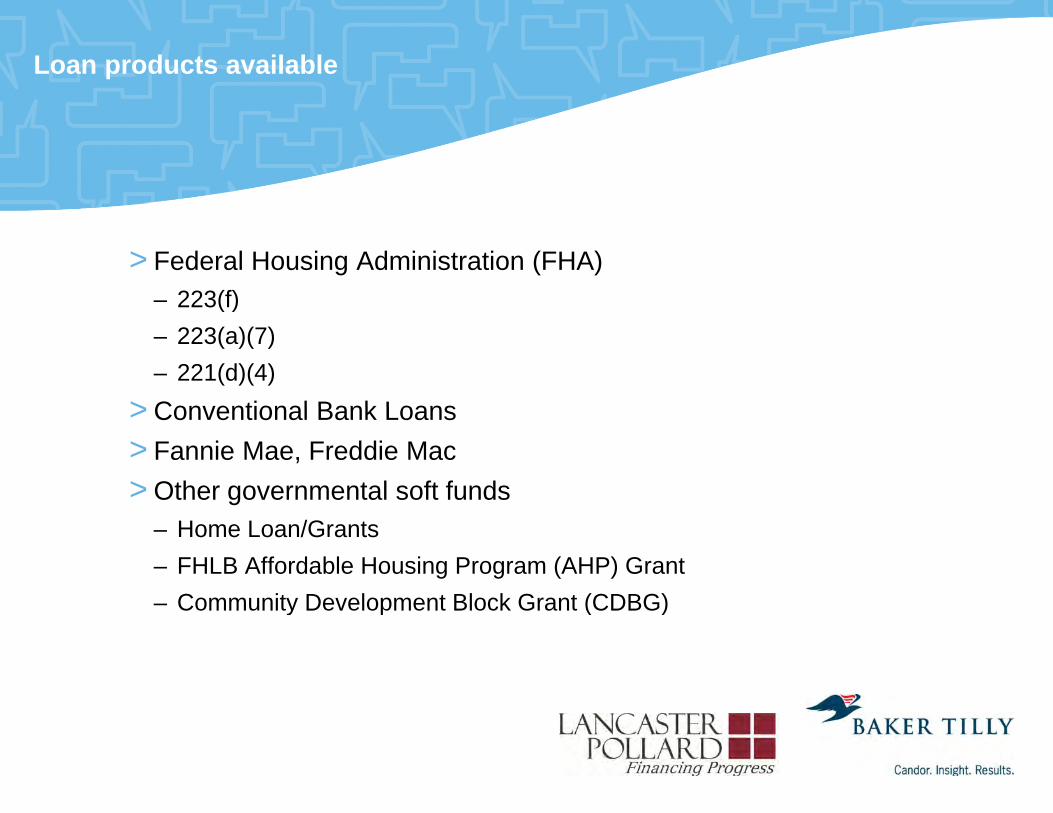

Loan products available

> Federal Housing Administration (FHA)– 223(f)223(f)– 223(a)(7)– 221(d)(4)

> Conventional Bank Loans> Conventional Bank Loans> Fannie Mae, Freddie Mac> Other governmental soft funds

– Home Loan/Grants– FHLB Affordable Housing Program (AHP) Grant– Community Development Block Grant (CDBG)Community Development Block Grant (CDBG)

Why now?

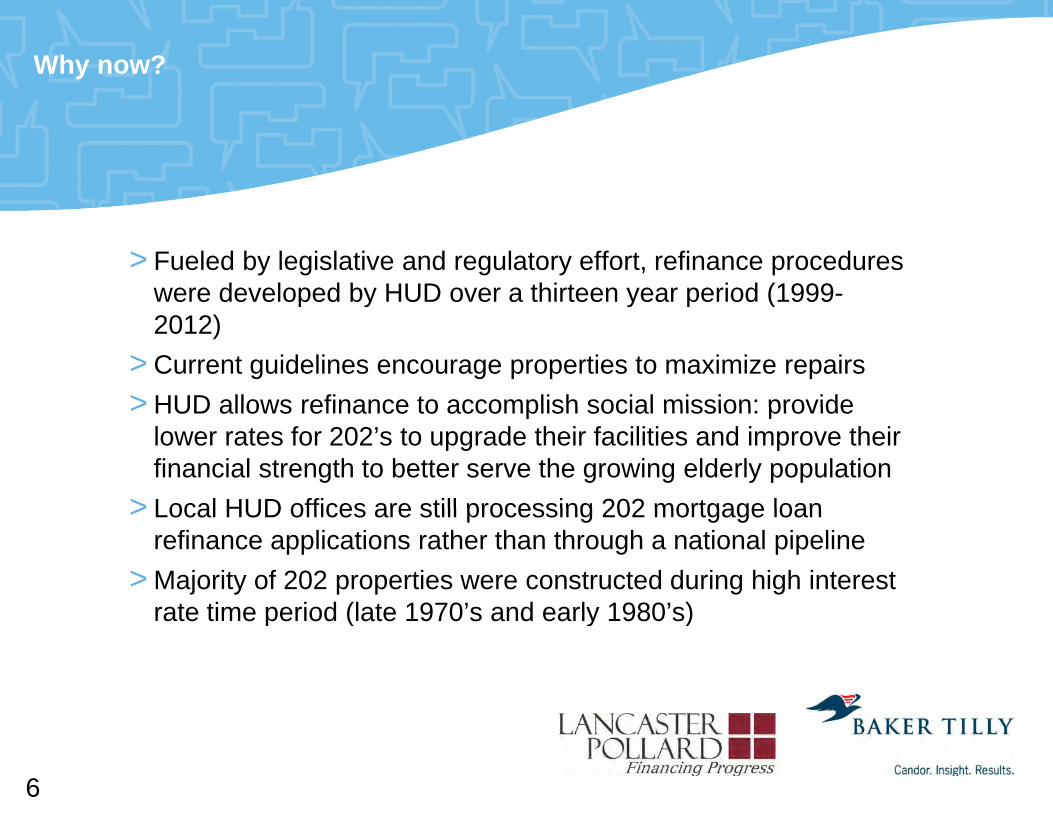

> Fueled by legislative and regulatory effort, refinance procedures were developed by HUD over a thirteen year period (1999-p y y p (2012)

> Current guidelines encourage properties to maximize repairs> HUD allows refinance to accomplish social mission: provide> HUD allows refinance to accomplish social mission: provide

lower rates for 202’s to upgrade their facilities and improve their financial strength to better serve the growing elderly population

> Local HUD offices are still processing 202 mortgage loan> Local HUD offices are still processing 202 mortgage loan refinance applications rather than through a national pipeline

> Majority of 202 properties were constructed during high interest rate time period (late 1970’s and early 1980’s)rate time period (late 1970 s and early 1980 s)

6

Favorable interest rate environment

10-Year Treasury Yield Forecast

4.11%4.23%

4.38% 4.43%

4%

5%10 Year Treasury Yield Forecast

Low Median High

2.79%2.78%

3.56%

3%

4%

nth

End

1.60% 1.60% 1.60% 1 50%

1.98% 1.98% 2.04%1.90% 2.00%

2.20% 2.25%2.50%

2.62%9%

2.25%

2.78%

2%

reca

sts

as o

f Mon

1.50%

1%

For

0%Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

Source: Bloomberg Survey, February 14, 2013

7

Refinance of Section 202 Direct Loan

Housing Notice 2012-08U A tUse Agreement> Use agreement is extended to 20 years beyond the maturity of the 202

Direct loanHAP Contract> Projects will require execution of a 20 year HAP contract plus

remaining term of current contract via Preservation Exhibit> Projects refinanced outside of HUD will maintain Exception project

status whether they follow notice requirements or not> Second refinance with FHA insured loan will subject the project to

k t k t i ti f th t HAP t t lmark-to-market upon expiration of the current HAP contract unless owner refinances again with conventional loan prior to expiration

8

Polling question #1

AA. An ownerB. A property managerC. Owner and manager

What description best applies to you?

D. Other

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

9

Refinance of Section 202 Direct Loan

Housing Notice 2012-08Eli ibl R fi C tEligible Refinance Costs> Developer’s fee equal to 15% of “acceptable development costs” where

it used to be limited to repairs and improvements done in the first 12 months12 months. – Acceptable development cost includes the cost of acquisition, rehabilitation,

loan prepayment, initial reserve deposits, and transaction costs. Transaction costs may include costs of third party reports such as market studies or physical inspection reports not otherwise captured in the development costs, and loan fees and closing costs.

10

Refinance of Section 202 Direct Loan

Housing Notice 2012-08Eli ibl R fi C tEligible Refinance Costs> Excess refinance proceeds can be deposited into a segregated

account and be spent over a 5-year period.– Refinance via Section 223(f) will still follow MAP requirements including repair

limits, repair escrow and completion of non-critical repairs within 12 months.– Additional proceeds deposited into segregated account will not be used in

Developer Fee calculation.p– Refinance proceeds can be used to benefit other affordable senior projects

owned by the non-profit (requires additional 10 year use restriction for the receiving property)R fi d b d h bili f ili i f h– Refinance proceeds can be used to construct or rehabilitate facilities for the elderly in the community of the project

– Proceeds from multiple projects can be pooled

11

New regulation HAP contracts residual receipts offsetsreceipts offsets

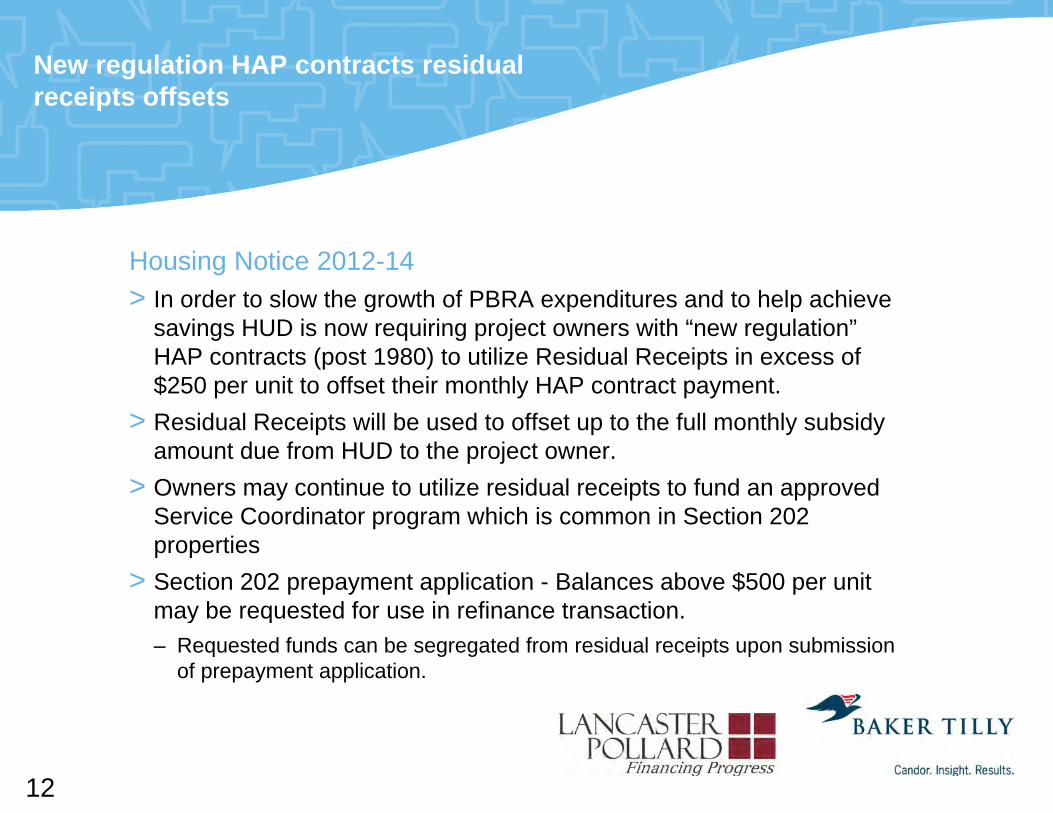

Housing Notice 2012-14> In order to slow the growth of PBRA expenditures and to help achieveIn order to slow the growth of PBRA expenditures and to help achieve

savings HUD is now requiring project owners with “new regulation” HAP contracts (post 1980) to utilize Residual Receipts in excess of $250 per unit to offset their monthly HAP contract payment.

> Residual Receipts will be used to offset up to the full monthly subsidy amount due from HUD to the project owner.

> Owners may continue to utilize residual receipts to fund an approved S i C di t hi h i i S ti 202Service Coordinator program which is common in Section 202 properties

> Section 202 prepayment application - Balances above $500 per unit may be requested for use in refinance transactionmay be requested for use in refinance transaction.– Requested funds can be segregated from residual receipts upon submission

of prepayment application.

12

Polling question #2

AA. YesB. NoC. Not sure

Do you have a “new regulation” HAP contract?

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

13

Section 8 HAP contract renewal

Section 8 Renewal Policy Guide Book> Option 4 Renewal of Projects Exempted from OAHPOption 4 Renewal of Projects Exempted from OAHP> Option 4 Changes - Effective October 15 and later

– Budget based Option 4 rent adjustments in a multiyear contract will only be approved if the proposed rents do not exceed comparable market rents. pp p p p

– OCAF adjustments for Option 4 contracts continue to be available without a rent comparability study, or use of new debt service.

– Owners must use current debt service when submitting a budget-based rent i tincrease request.» This new requirement applies to all Option 4 contracts, even multiyear

contracts signed prior to May 18, 2012. – Lesser of Budget or OCAF test will be required at renewal of HAP contractsLesser of Budget or OCAF test will be required at renewal of HAP contracts.

14

Section 8 HAP contract renewal

Section 8 Renewal Policy Guide Book> Added option for Early Termination and Renewal of Section 8 ContractAdded option for Early Termination and Renewal of Section 8 Contract

(Section 2-8)> Provides the ability for the owner to terminate the current contract and

execute a 20 year Contract with Preservation Exhibit.> Preservation Exhibit – requires automatic renewal for number of years

remaining on current contract.– Example: 3 years remaining on current HAP contract will result in 20 year

contract with automatic 3 year renewal

15

Possible owner objectives

> Moderate Improvements and/or Increase Reserves> Substantial Rehabilitation> Competitive Repositioning of Facility> Modernize Building Systems for Efficiency> Earn Unrestricted Developer Fee> Earn Unrestricted Developer Fee> Fund increased Services (i.e., Service Coordinator, Wellness

Coordinator, etc.)

16

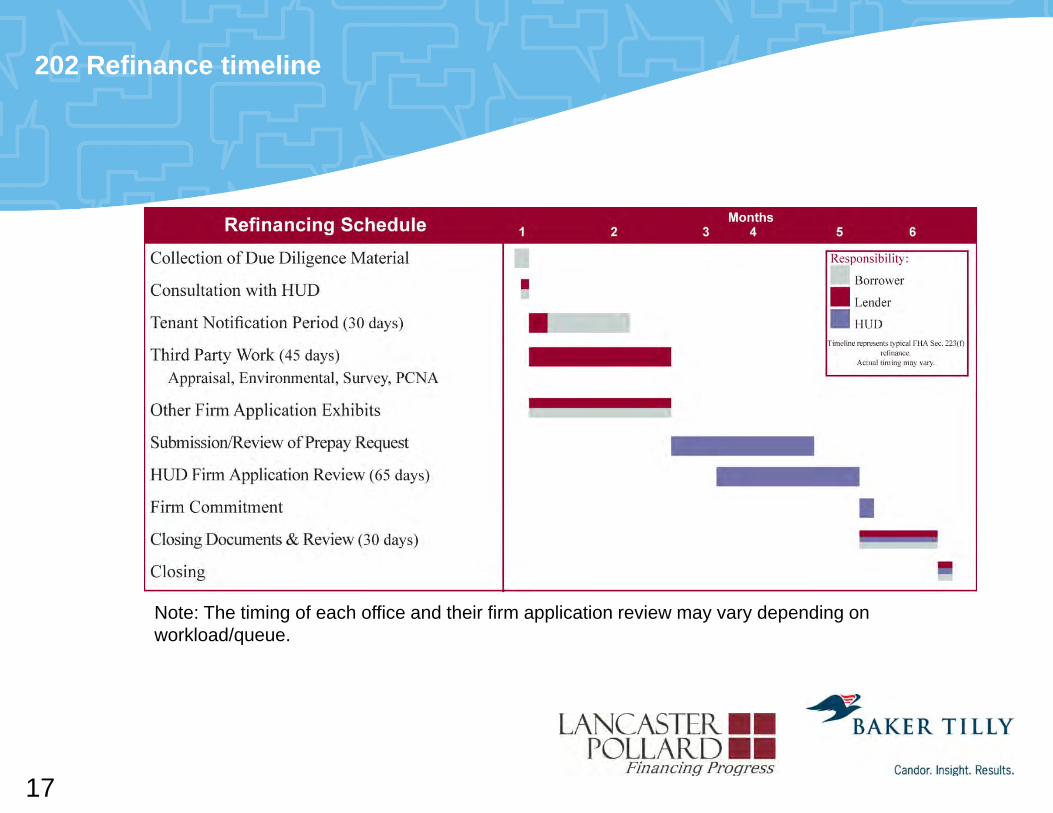

202 Refinance timeline

Note: The timing of each office and their firm application review may vary depending onNote: The timing of each office and their firm application review may vary depending on workload/queue.

17

Polling question #4

AA. YesB. NoHave you re-financed

your original 202 loan?

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

18

Amount of new debt and new term driven by cash flow and interest ratesby cash flow and interest rates

Revenue (1) 1,234,810$ Minus: Expenses (2) 833,170$ Minus: Replacement Reserve Adjustment (3) 41,500$

$Cash Flow 360,140$

Assumed Term (years) 35Assumed Interest Rate (4) 3.70%( ) %Assumed Debt Service Coverage (x) 1.11Debt Constant 5.3135%

Estimated Amo nt of S pported Debt $6 100 024 15Estimated Amount of Supported Debt $6,100,024.15

(1) Based on Rent Schedule and includes 5% vacancy factor.(2) Expenses do not included depreciation or interest.(3) $250 per unit per annum.(4) Includes HUD annual mortgage insurance premium of 0.45%.

19

Amount of new debt determines how much available for improvement projectsavailable for improvement projects

% If% IfApplicable

New Mortgage 6,100,000$

Uses:Existing Indebtedness 3,502,400 Improvements 1,493,100 Non-profit Developer's Fee 795,700 HUD Related:HUD Related:

Mortgage Insurance Premium 1.00% 61,000 Application Fee 0.30% 18,300 Inspection Fee 15,000

Lender Related:Financing Fee 1.50% 91,500 Permanent Loan Fee 1.00% 61,000

Fixed ExpensesTitle and Survey 20,000 Appraisal PCNA & Phase One 17 000Appraisal, PCNA & Phase One 17,000 Legal (Lender and Borrower) 25,000

Total Uses 6,100,000

20

Re-Refinance of Section 223(f)/202’s

Challenges> Re-refinance with FHA insurance results in the loss of exemption fromRe refinance with FHA insurance results in the loss of exemption from

Mark-to-Market> Underwriting must include market rents for mortgage term beyond

Section 8 ContractSolutions> Complete rent comp study – not only provides market levels for use in

underwriting but also provides project management valuable g p p j ginformation for budgeting and expense control

> Request termination and execution of 20 year HAP contract> Section 223(a)(7) loan will include step down in note payment for ( )( ) p p y

projects with above market rents which mitigates the risk of a Mark-to-Market upon contract expiration.

21

Polling question #3

AA. YesB. NoHave you re-refinanced

your 202 loan?

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

22

Process

> Commission Rent Comp Study and PCNA (if previous report is older than 5 years)

23

Process

> Determine remaining term of current HAP contract> If minimal term remains, contact HAP contract administrator to discuss ,

termination and renewal of a 20 year contract

24

Process

> Once 20 year HAP contract is finalized, submit Section 223(a)(7) application to local field office

25

When to consider a mixed-finance transaction (adding tax credits totransaction (adding tax credits to your project)

When to consider Low-Income Housing Tax CreditsCreditsGeneral rules of thumb:> Less than $10,000 of rehab needed per unit – refinance$ , p> Approximately $20,000 – 30,000 of rehab needed per unit – 4% tax

credit project> More than $30,000 of rehab needed per unit – 9% tax credit project$ , p p j

26

Polling question #5

AA. 4%B. 9%C. Both

Which LIHTC programs have you used?

D. Neither

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

27

4% tax credit program

> Low-Income Housing Tax Credits that come with an allocation of private activity volume cap tax-exempt bonds from the state finance agency

> Typically non-competitive> Each state’s 2013 private activity bond cap will be the greater of $95

per capita and $291,875,000 (this volume cap may also be used for single family homes, among other items)

> Provides approximately 25% of a project’s development costs

28

9% tax credit program

> Competitive process governed by each state’s Qualified Allocation Plan> Typically one or two funding rounds per yearyp y g p y> Each state’s 9% tax credit authority will be the greater of $2.25 per

capita and $2,590,000> Provides approximately 70% of a project’s total development costspp y p j p

29

Comparison of 4% and 9%

9% 4%Interest rates Typically higher Typically lowerEquity 60-70% of project costs 20-30% of project costsCompetition 3 4 applications per 1 Typically automatic ifCompetition 3-4 applications per 1

awardTypically automatic if financially feasible

30

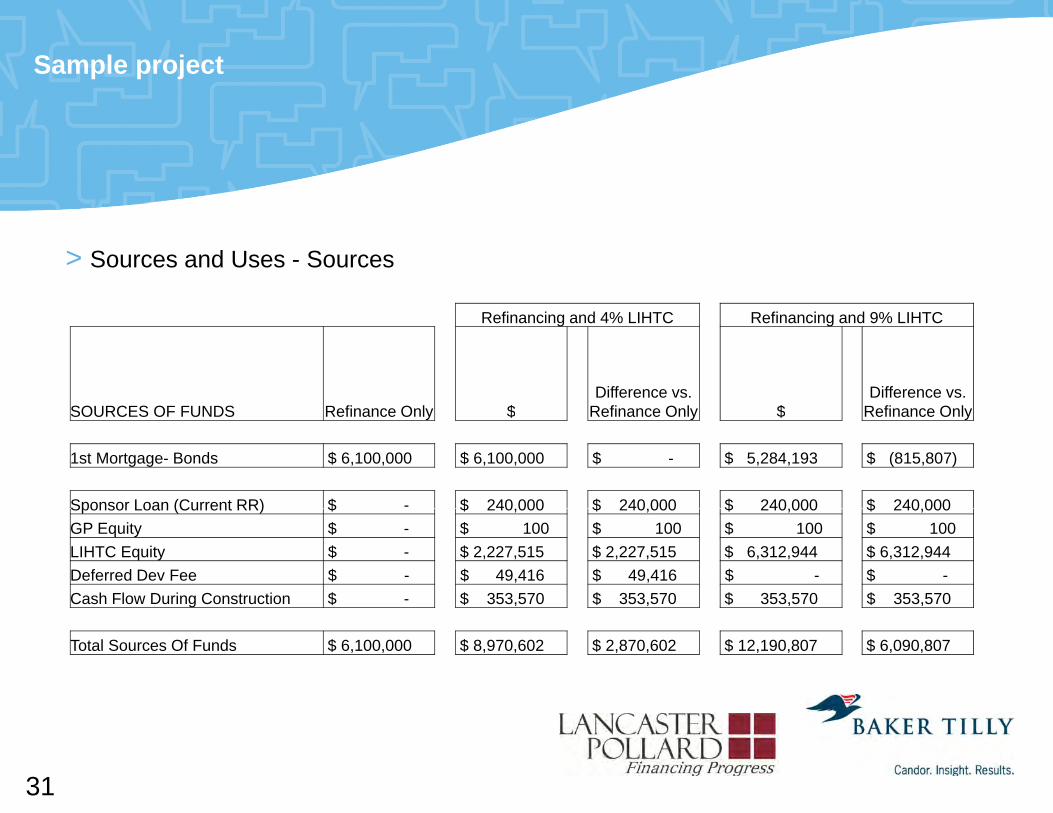

Sample project

> Sources and Uses - Sources

Refinancing and 4% LIHTC Refinancing and 9% LIHTC

SOURCES OF FUNDS R fi O l $Difference vs.

R fi O l $Difference vs.

R fi O lSOURCES OF FUNDS Refinance Only $ Refinance Only $ Refinance Only

1st Mortgage- Bonds $ 6,100,000 $ 6,100,000 $ - $ 5,284,193 $ (815,807)

Sponsor Loan (Current RR) $ - $ 240 000 $ 240 000 $ 240 000 $ 240 000Sponsor Loan (Current RR) $ $ 240,000 $ 240,000 $ 240,000 $ 240,000 GP Equity $ - $ 100 $ 100 $ 100 $ 100 LIHTC Equity $ - $ 2,227,515 $ 2,227,515 $ 6,312,944 $ 6,312,944 Deferred Dev Fee $ - $ 49,416 $ 49,416 $ - $ -Cash Flow During Construction $ - $ 353,570 $ 353,570 $ 353,570 $ 353,570

Total Sources Of Funds $ 6,100,000 $ 8,970,602 $ 2,870,602 $ 12,190,807 $ 6,090,807

31

Sample project

> Sources and Uses - UsesRefinancing and 4% LIHTC Refinancing and 9% LIHTCRefinancing and 4% LIHTC Refinancing and 9% LIHTC

Refinance Only $Diff. vs.

Refinance Only $Diff. vs.

Refinance OnlyTotal Sources Of Funds $ 6,100,000 $ 8,970,602 $ 2,870,603 $ 12,190,807 $ 6,090,807

USES OF FUNDSAcquisition & Site Costs $ 3,502,500 $ 3,502,500 $ - $ 3,502,500 $ -Construction Costs $ 1,493,000 $ 3,109,830 $ 1,616,830 $ 5,626,377 $ 4,133,377 Engineering, Architectural & RE Attorney $ 25,000 $ 243,414 $ 218,414 $ 350,000 $ 325,000 Construction Interest & Fees $ 20,000 $ 280,708 $ 260,708 $ 329,635 $ 309,635 Permanent Financing $ 246,800 $ 294,300 $ 47,500 $ 147,000 $ (99,800)Soft Costs $ 17,000 $ 167,130 $ 150,130 $ 217,130 $ 200,130 Syndication Costs $ - $ 30,000 $ 30,000 $ 30,000 $ 30,000 Developer Fees / Reserves $ 795,700 $ 1,342,720 $ 547,020 $ 1,988,166 $ 1,192,466

Total Uses Of Funds $ 6,100,000 $ 8,970,602 $ 2,870,603 $ 12,190,807 $ 6,090,807

32

Considerations

> Joint venture if need a development partner– Split of dutiesp– Split of fees/cash flow– Split of guarantees– Working relationship

> Financial guarantees> Back on the tax rolls> Right of first refusal of the 15 year tax credit compliance periodRight of first refusal of the 15 year tax credit compliance period

33

Risks/rewards

RewardsAdditional equity to fund> Additional necessary rehab> Reserves> Architect/owner’s repArchitect/owner s rep> Developer fees

RisksGuarantees> Construction completion> Construction completion> Operating deficits> Compliance

34

Polling question #6

AA. YesB. NoDo you think the

rewards are worth the risks?

Pl d i th lli ti i th W bE t th i htPlease respond using the polling section in the WebEx screen to the right.

35

Summary

To sum up:> R l t h t th S ti 202 Di t L P ff t> Regulatory changes to the Section 202 Direct Loan Program effect

available financing by encouraging repairs today> The Financing sources available to refinance a 202 loan are:

L I H i T C dit (LIHTC)– Low-Income Housing Tax Credits (LIHTC)– FHA 223(f)– FHA Sec. 223(a)(7) programs

> HUD ll l d> HUD now allows sale proceeds

36

Questions

Questions?

Please feel free to ask questions in the screen to your right.

We will answer as many questions as time permits.

37

CPE

To receive CPE credit for today’s presentation you MUSTTo receive CPE credit for today’s presentation, you MUST complete the survey at the end of today’s webinar.

CPE certificates will be mailed to you in about six weeks.

Thank you for your attendance and participation!

38

Baker Tilly Disclosure

The content in this presentation is a resource for Baker Tilly Virchow Krause, LLP clients and prospective clients. Nothing contained in this presentation shall be construed as legal advice, opinion, or as an offer to buy or sell any property or services. In conformity with U.S. Treasury Department Circular 230, tax advice contained in this communication and any attachments is not intended to be used and cannot be used for theany attachments is not intended to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code, nor may any such tax advice be used to promote, market or recommend to any person any transaction or matter that is the subject

f fof this communication and any attachments. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.or matter that is the subject of this communication and any attachments.

39

Lancaster Pollard Disclosure

Information in this presentation has been obtained from sources believed to be accurate and reliable. However, we do not guarantee the accuracy, adequacy or completeness of any information and are not responsible for any errors or omissions or for the results obtained from the use of such information. In the ordinary course of its business, Lancaster Pollard and its affiliates provide underwriting investment management and consultingits affiliates provide underwriting, investment management and consulting services to our clients. Information contained in this publication should not be the basis of any management decision without proper professional counsel by a qualified adviser.

40