HSBC Turning Scale and Complexity into Competitive Advantage

33

Turning Scale and Complexity into Competitive Advantage Douglas Flint Group Finance Director UBS 2006 Global Financial Services Conference

-

Upload

quarterlyearningsreports2 -

Category

Documents

-

view

426 -

download

0

Transcript of HSBC Turning Scale and Complexity into Competitive Advantage

Turning Scale and Complexity into

Competitive Advantage

Douglas FlintGroup Finance Director

UBS 2006 Global Financial Services Conference

2UBS 2006 Global Financial Services Conference

Forward-looking statementsThis presentation and subsequent discussion may contain certain forward-looking statements with respect to the financial condition, results of operations and business of the Group. These forward-looking statements represent the Group’s expectations or beliefs concerning future events and involve known and unknown risks and uncertainty that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Additional detailed information concerning important factors that could cause actual results to differ materially is available in our Annual Report.

3UBS 2006 Global Financial Services Conference

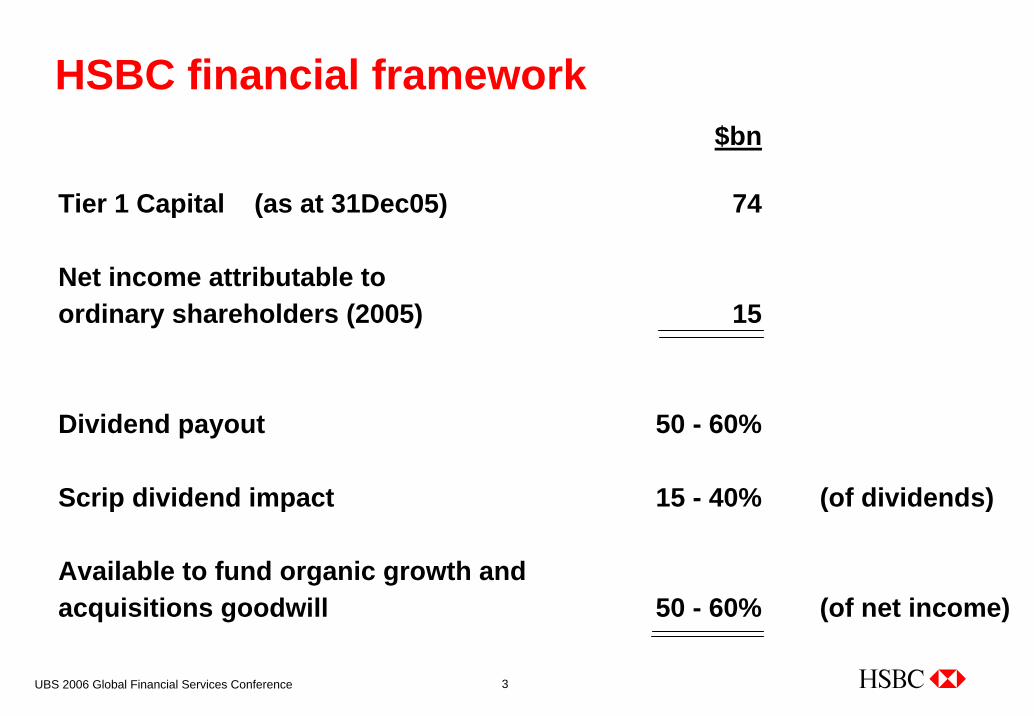

HSBC financial framework$bn

Tier 1 Capital (as at 31Dec05) 74

Net income attributable to ordinary shareholders (2005) 15

Dividend payout 50 - 60%

Scrip dividend impact 15 - 40% (of dividends)

Available to fund organic growth and acquisitions goodwill 50 - 60% (of net income)

4UBS 2006 Global Financial Services Conference

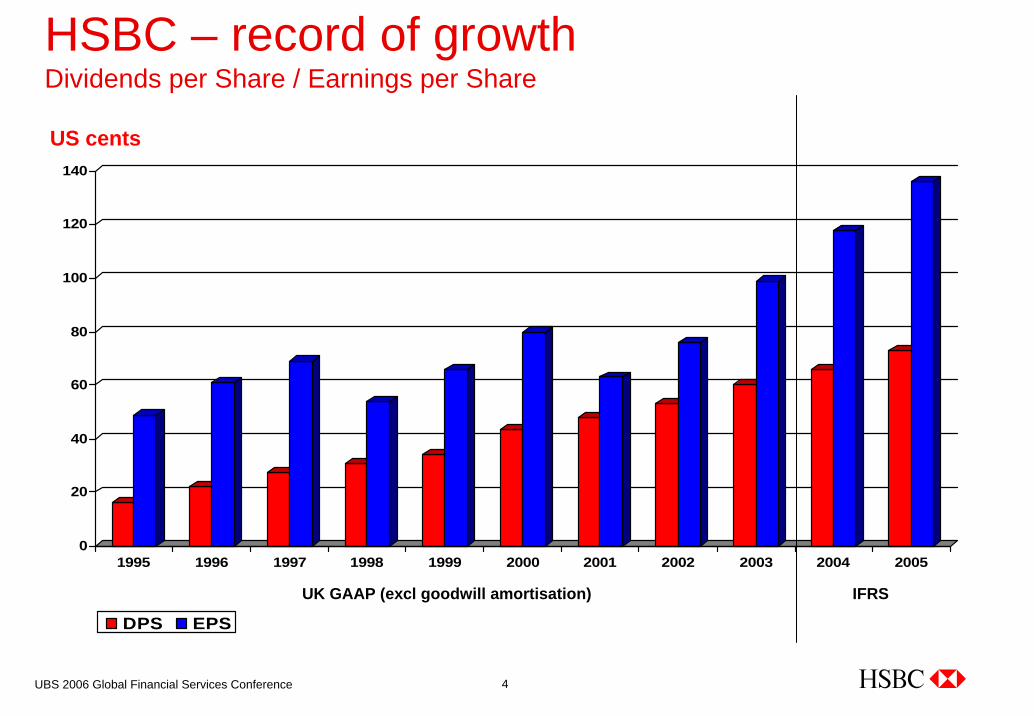

HSBC – record of growthDividends per Share / Earnings per Share

0

20

40

60

80

100

120

140

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

DPS EPS

UK GAAP (excl goodwill amortisation) IFRS

US cents

5UBS 2006 Global Financial Services Conference

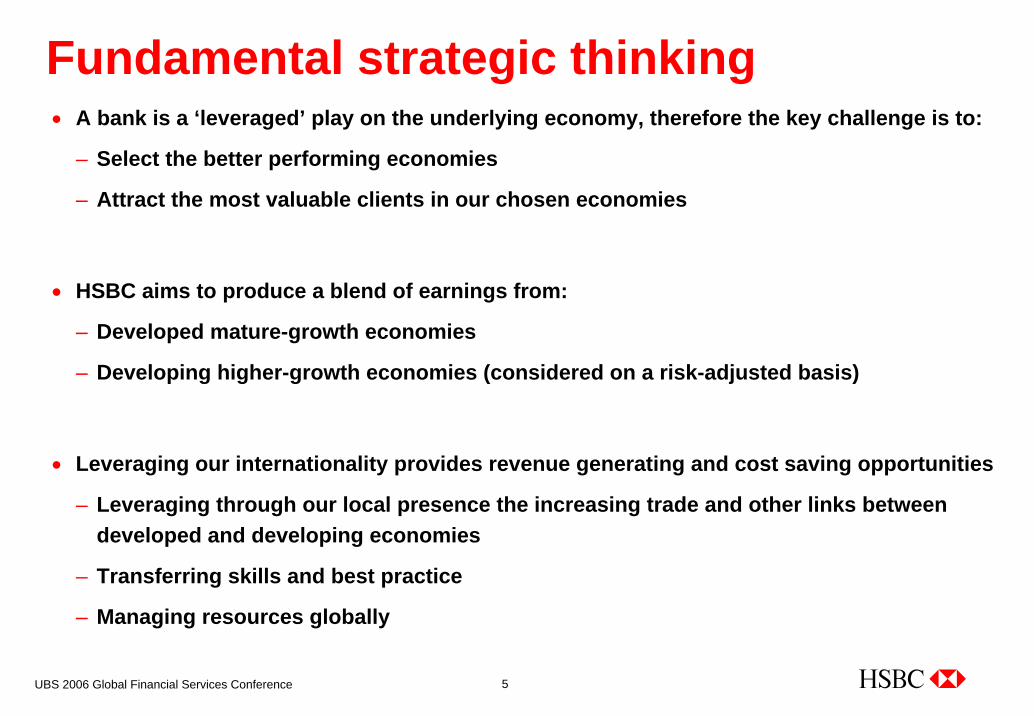

Fundamental strategic thinking• A bank is a ‘leveraged’ play on the underlying economy, therefore the key challenge is to:

– Select the better performing economies

– Attract the most valuable clients in our chosen economies

• HSBC aims to produce a blend of earnings from:

– Developed mature-growth economies

– Developing higher-growth economies (considered on a risk-adjusted basis)

• Leveraging our internationality provides revenue generating and cost saving opportunities

– Leveraging through our local presence the increasing trade and other links between developed and developing economies

– Transferring skills and best practice

– Managing resources globally

6UBS 2006 Global Financial Services Conference

HSBC’s ‘Broadbrush’ 25-year scenario• Key economic areas will be:

– NAFTA

– Greater China

• 50% of the increase in world demand will come from developing countries such as:– China, India, Mexico and Brazil

• Major opportunities within the diaspora of:– Chinese, Hispanic, Indian and many other expatriate communities

7UBS 2006 Global Financial Services Conference

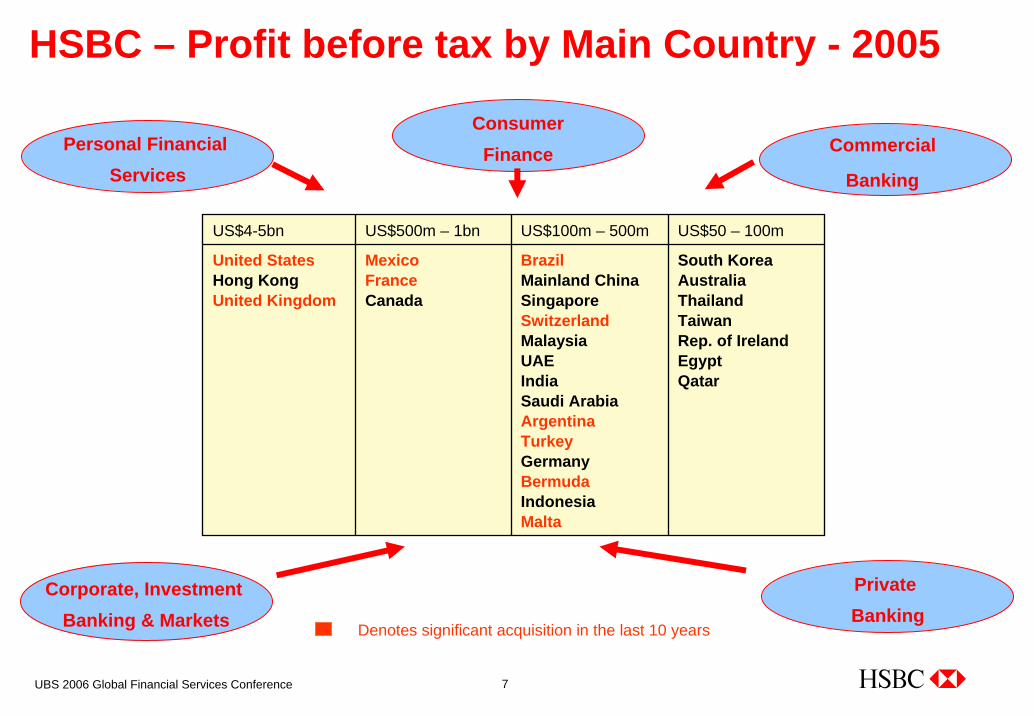

Denotes significant acquisition in the last 10 years

HSBC – Profit before tax by Main Country - 2005

US$4-5bn US$500m – 1bn US$100m – 500m US$50 – 100m

United StatesHong KongUnited Kingdom

MexicoFranceCanada

BrazilMainland ChinaSingaporeSwitzerlandMalaysiaUAEIndiaSaudi ArabiaArgentinaTurkeyGermanyBermudaIndonesiaMalta

South KoreaAustraliaThailandTaiwanRep. of IrelandEgypt Qatar

Personal Financial Services

Commercial

Banking

ConsumerFinance

Corporate, Investment Banking & Markets

Private Banking

8UBS 2006 Global Financial Services Conference

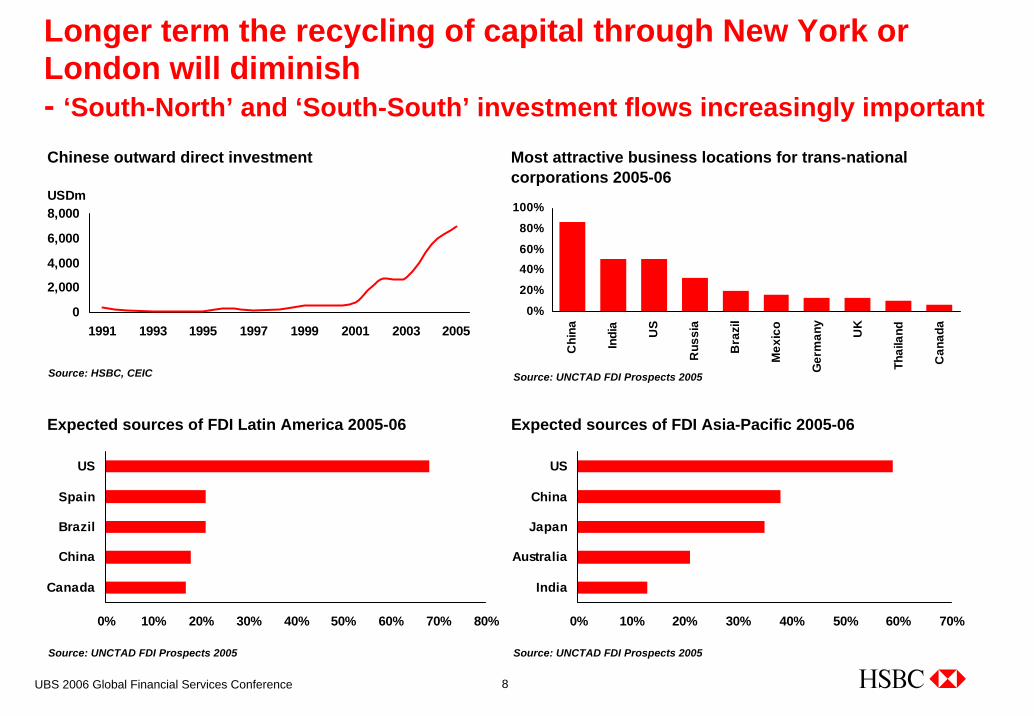

Longer term the recycling of capital through New York or London will diminish- ‘South-North’ and ‘South-South’ investment flows increasingly important

0% 10% 20% 30% 40% 50% 60% 70%

US

China

Japan

Australia

India

Source: UNCTAD FDI Prospects 2005Source: UNCTAD FDI Prospects 2005

0%

20%

40%60%

80%

100%

Chi

na

Indi

a

US

Rus

sia

Bra

zil

Mex

ico

Ger

man

y

UK

Thai

land

Can

ada

Most attractive business locations for trans-national corporations 2005-06

Source: UNCTAD FDI Prospects 2005Source: HSBC, CEIC

Chinese outward direct investment

Expected sources of FDI Latin America 2005-06 Expected sources of FDI Asia-Pacific 2005-06

0

2,000

4,000

6,000

8,000

1991 1993 1995 1997 1999 2001 2003 2005

USDm

0% 10% 20% 30% 40% 50% 60% 70% 80%

US

Spain

Brazil

China

Canada

9UBS 2006 Global Financial Services Conference

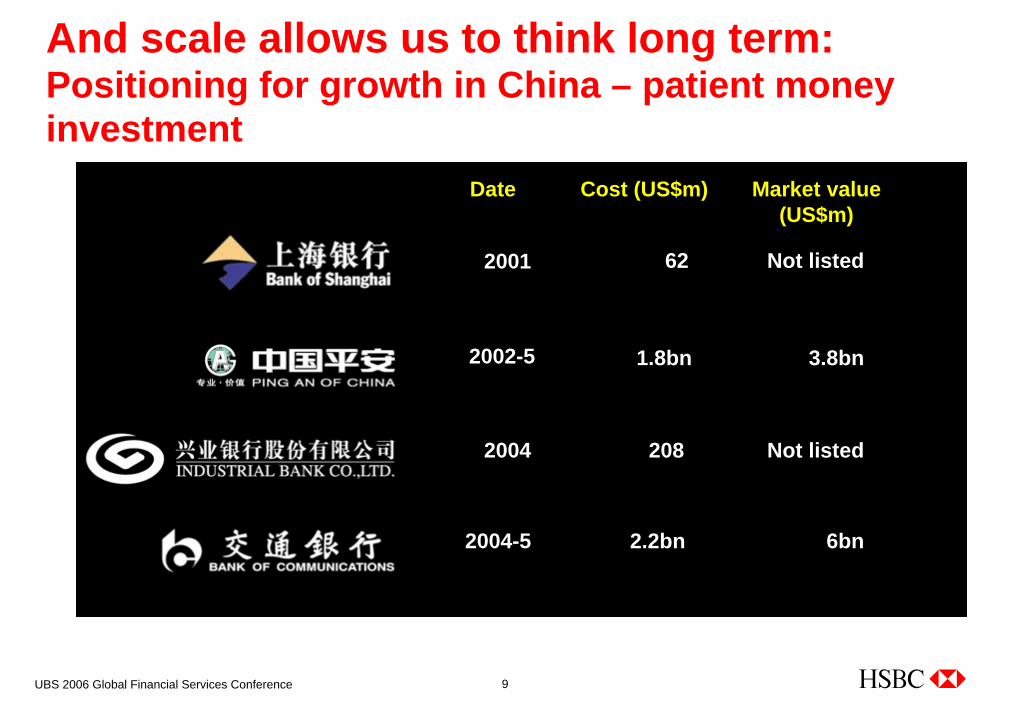

And scale allows us to think long term:Positioning for growth in China – patient money investment

Date Cost (US$m) Market value (US$m)

2001 62

2002-5

2004

2004-5

Not listed

Not listed208

1.8bn 3.8bn

6bn2.2bn

10UBS 2006 Global Financial Services Conference

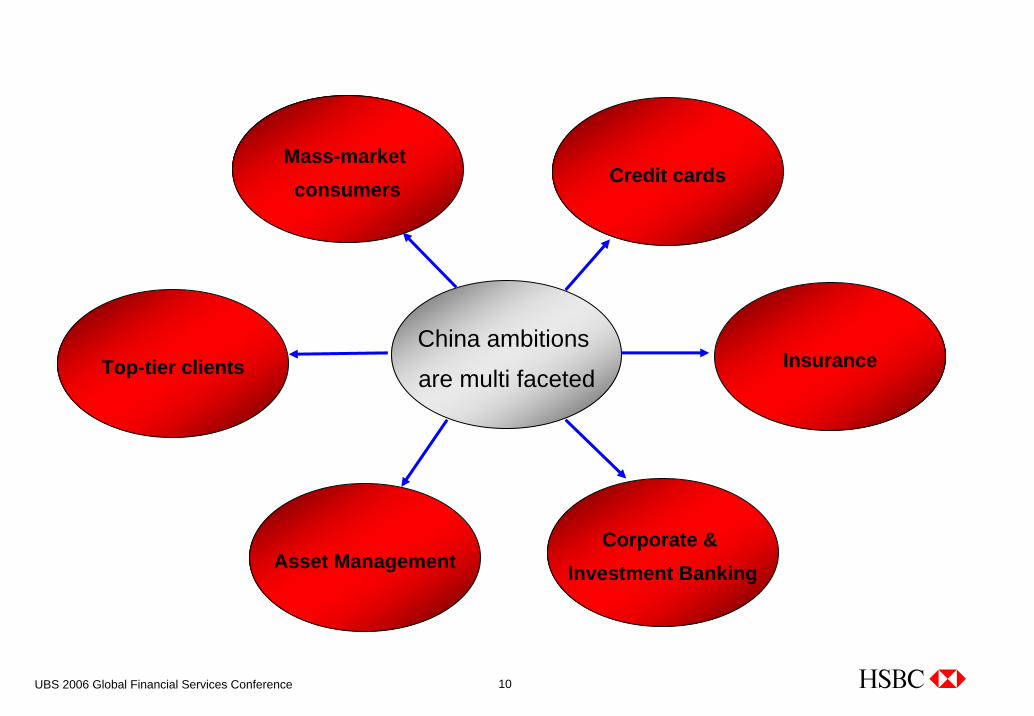

China ambitions

are multi facetedTop-tier clients

Mass-market consumers

Credit cards

Insurance

Corporate & Investment BankingAsset Management

11UBS 2006 Global Financial Services Conference

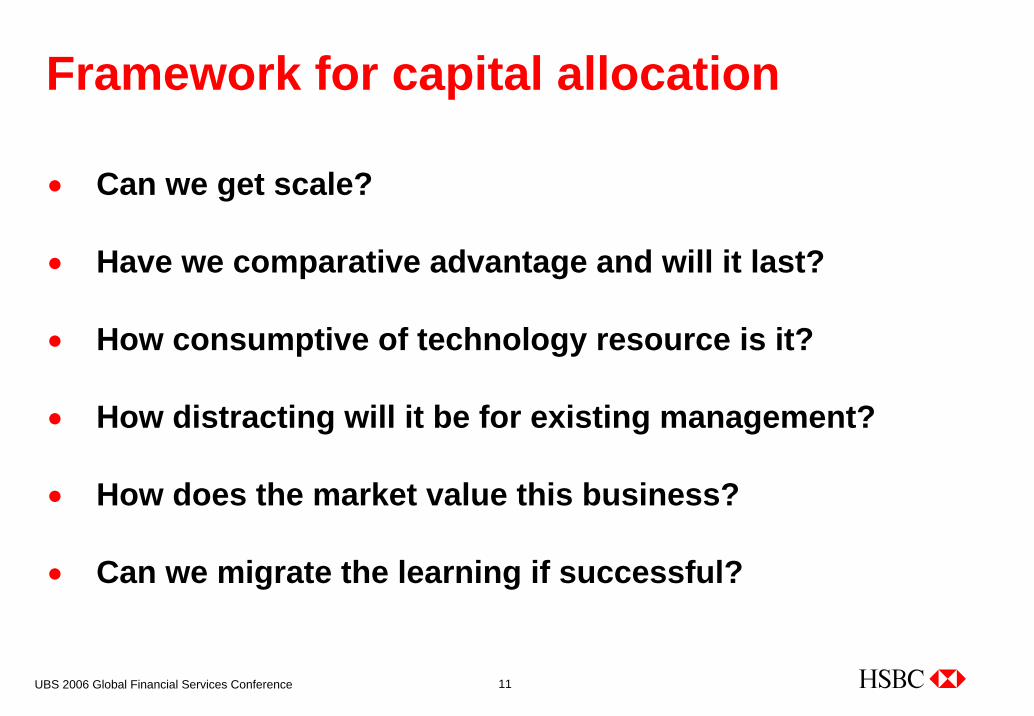

Framework for capital allocation

• Can we get scale?

• Have we comparative advantage and will it last?

• How consumptive of technology resource is it?

• How distracting will it be for existing management?

• How does the market value this business?

• Can we migrate the learning if successful?

12UBS 2006 Global Financial Services Conference

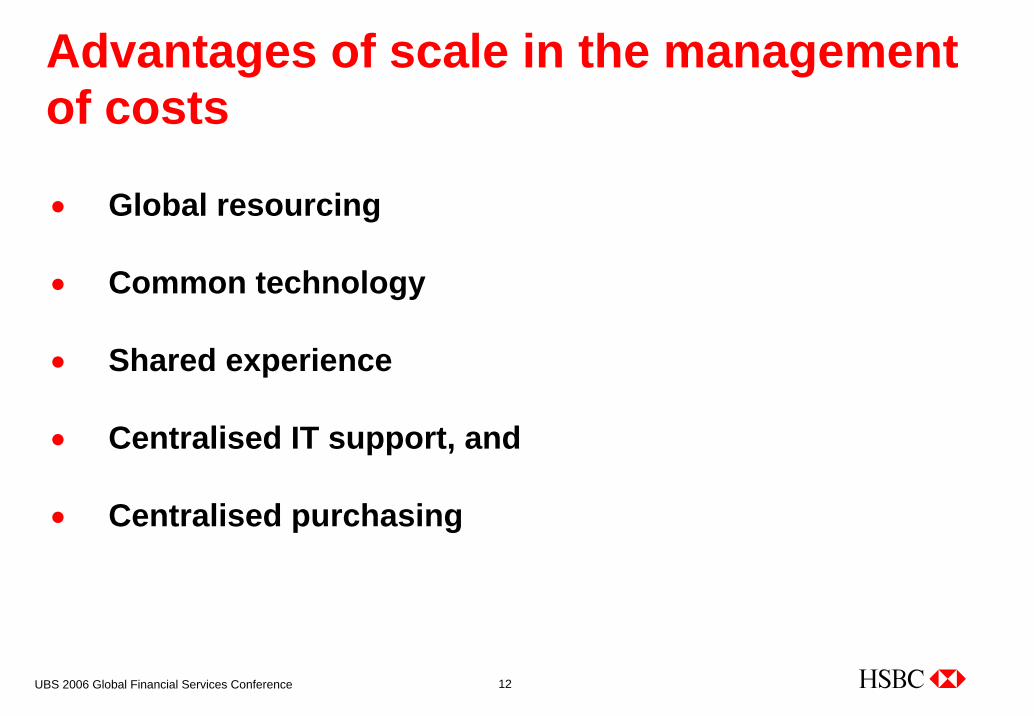

Advantages of scale in the management of costs

• Global resourcing

• Common technology

• Shared experience

• Centralised IT support, and

• Centralised purchasing

13UBS 2006 Global Financial Services Conference

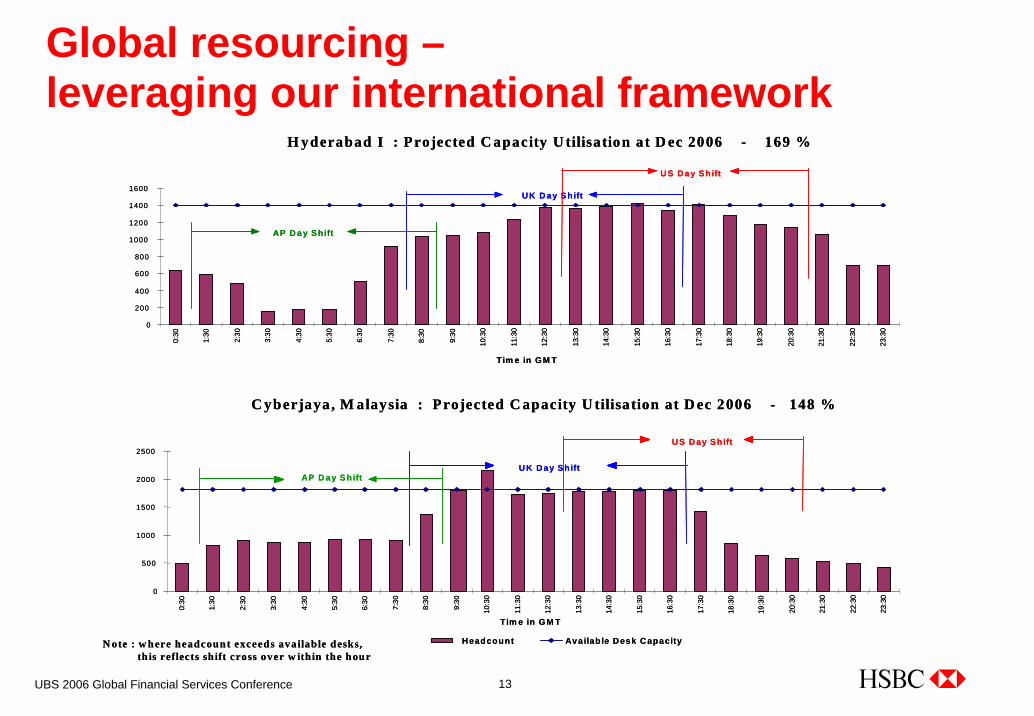

C yberjaya, M alaysia : Projected C apacity U tilisation at D ec 2006 - 148 %

0

500

1000

1500

2000

2500

0:30

1:30

2:30

3:30

4:30

5:30

6:30

7:30

8:30

9:30

10:3

0

11:3

0

12:3

0

13:3

0

14:3

0

15:3

0

16:3

0

17:3

0

18:3

0

19:3

0

20:3

0

21:3

0

22:3

0

23:3

0

Tim e in GM T

Headcount Availab le D esk Capacity

U K D ay ShiftAP D a y S hift

U S D ay Shift

H yderabad I : Projected C apacity U tilisation at D ec 2006 - 169 %

0

200

400

600

800

1000

1200

1400

1600

0:30

1:30

2:30

3:30

4:30

5:30

6:30

7:30

8:30

9:30

10:3

0

11:3

0

12:3

0

13:3

0

14:3

0

15:3

0

16:3

0

17:3

0

18:3

0

19:3

0

20:3

0

21:3

0

22:3

0

23:3

0

Tim e in GM T

US Day S hift

AP D a y Shift

UK D ay Shift

N ote : w here headcount exceeds available desks, th is reflects shift cross over w ithin the hour

C yberjaya, M alaysia : Projected C apacity U tilisation at D ec 2006 - 148 %

0

500

1000

1500

2000

2500

0:30

1:30

2:30

3:30

4:30

5:30

6:30

7:30

8:30

9:30

10:3

0

11:3

0

12:3

0

13:3

0

14:3

0

15:3

0

16:3

0

17:3

0

18:3

0

19:3

0

20:3

0

21:3

0

22:3

0

23:3

0

Tim e in GM T

Headcount Availab le D esk Capacity

U K D ay ShiftAP D a y S hift

U S D ay Shift

H yderabad I : Projected C apacity U tilisation at D ec 2006 - 169 %

0

200

400

600

800

1000

1200

1400

1600

0:30

1:30

2:30

3:30

4:30

5:30

6:30

7:30

8:30

9:30

10:3

0

11:3

0

12:3

0

13:3

0

14:3

0

15:3

0

16:3

0

17:3

0

18:3

0

19:3

0

20:3

0

21:3

0

22:3

0

23:3

0

Tim e in GM T

US Day S hift

AP D a y Shift

UK D ay Shift

N ote : w here headcount exceeds available desks, th is reflects shift cross over w ithin the hour

Global resourcing –leveraging our international framework

14UBS 2006 Global Financial Services Conference

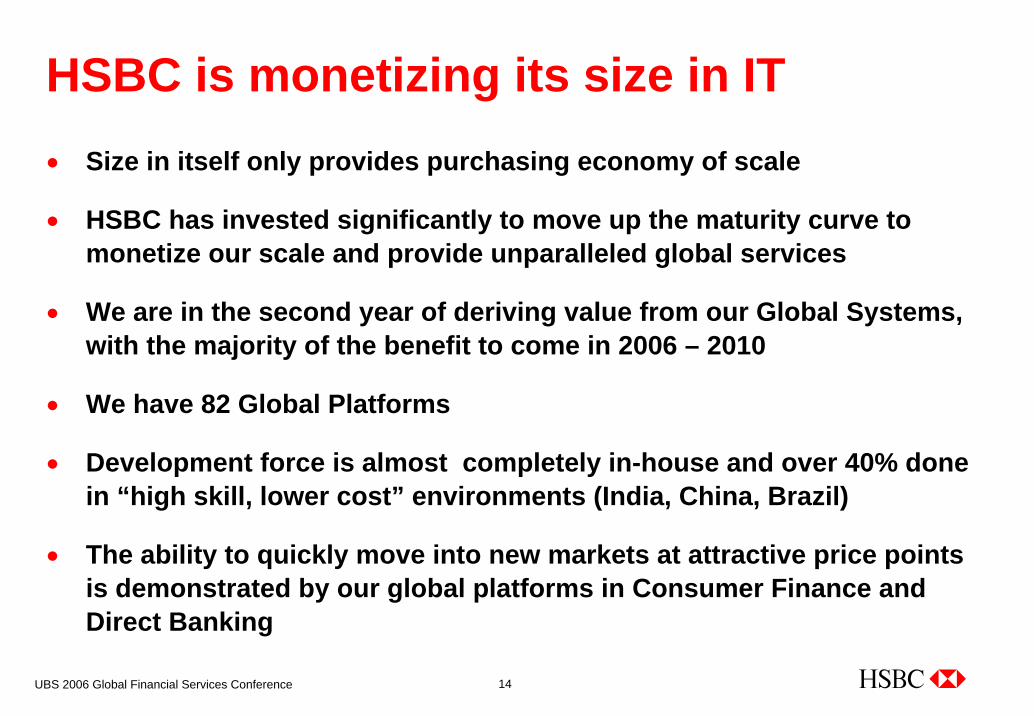

HSBC is monetizing its size in IT• Size in itself only provides purchasing economy of scale

• HSBC has invested significantly to move up the maturity curve tomonetize our scale and provide unparalleled global services

• We are in the second year of deriving value from our Global Systems, with the majority of the benefit to come in 2006 – 2010

• We have 82 Global Platforms

• Development force is almost completely in-house and over 40% done in “high skill, lower cost” environments (India, China, Brazil)

• The ability to quickly move into new markets at attractive price points is demonstrated by our global platforms in Consumer Finance and Direct Banking

15UBS 2006 Global Financial Services Conference

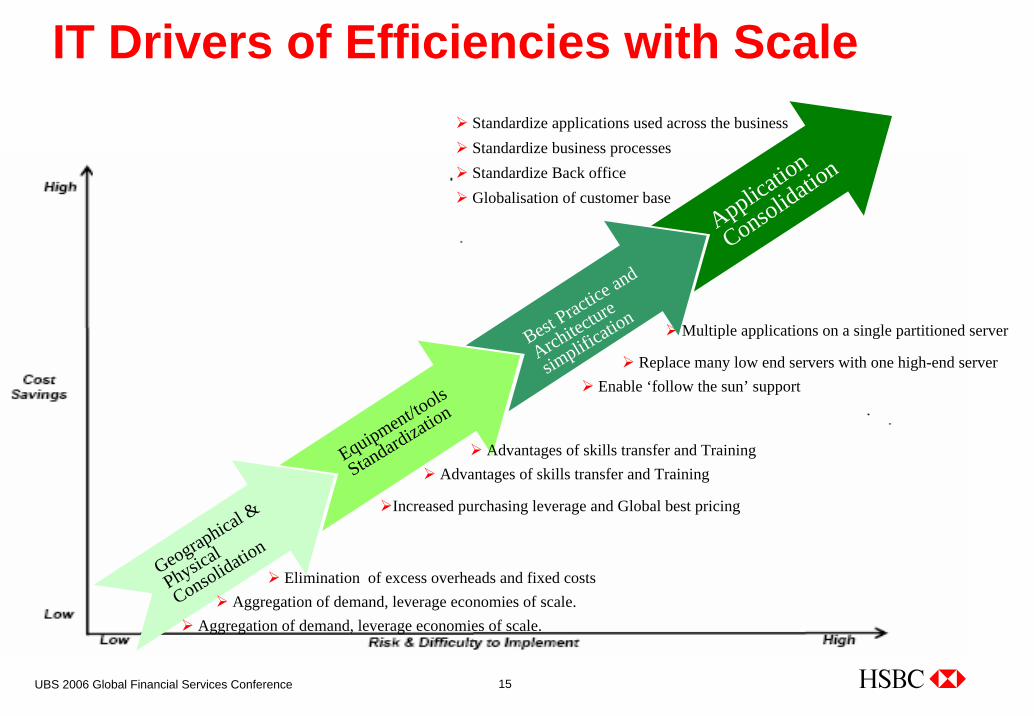

Geographical &

Physical

Consolidation

Standardize applications used across the businessStandardize business processesStandardize Back officeGlobalisation of customer base

Multiple applications on a single partitioned server

Replace many low end servers with one high-end serverEnable ‘follow the sun’ support

Elimination of excess overheads and fixed costsAggregation of demand, leverage economies of scale.

Aggregation of demand, leverage economies of scale.

IT Drivers of Efficiencies with Scale

Equipment/tools

Standardization

Application

Consolidation

Best Practice and

Architecture

simplific

ation

Increased purchasing leverage and Global best pricing

Advantages of skills transfer and TrainingAdvantages of skills transfer and Training

16UBS 2006 Global Financial Services Conference

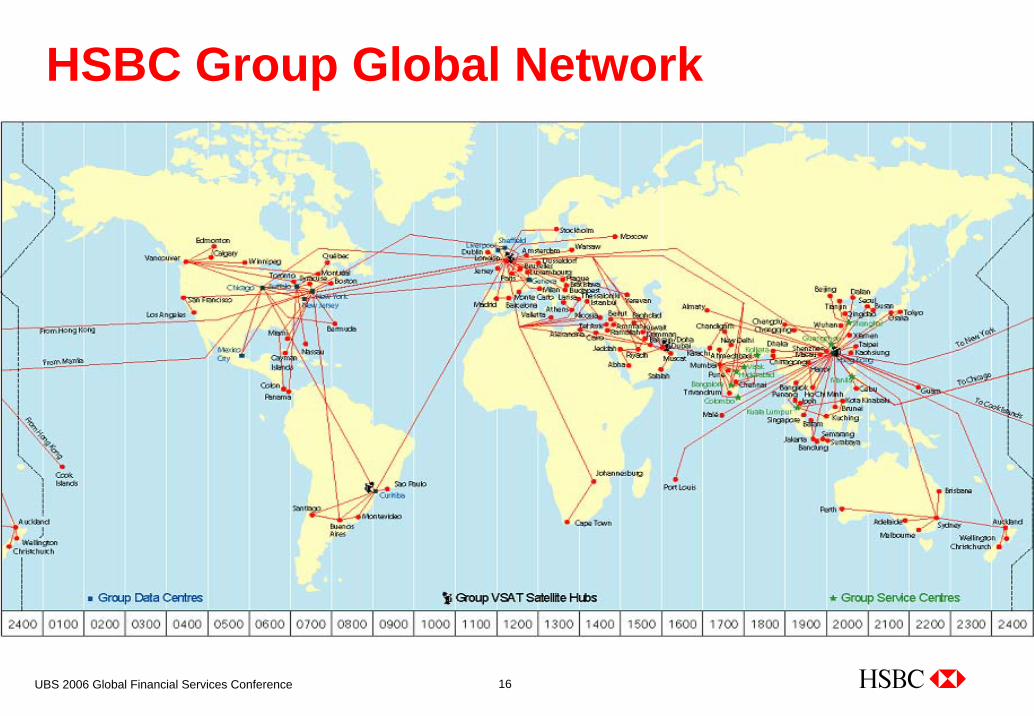

Common global network infrastructure permitting any connection to any Group destination- Global utility irrespective of corporate affiliation- Top quartile of comparable network cost & availability- Internal uniformity & ease of interconnect- Traffic based tariffing by destination

Annual capacity increase 70% over last 3 years 179 Group corporate users57% p.a increase in traffic 26% increase in billable devices (1H05) to 106KVoice and Data network rates reduced for 16

consecutive yearsLarge Purchase Economies of scale Diverse

HSBC Group Global Network

17UBS 2006 Global Financial Services Conference

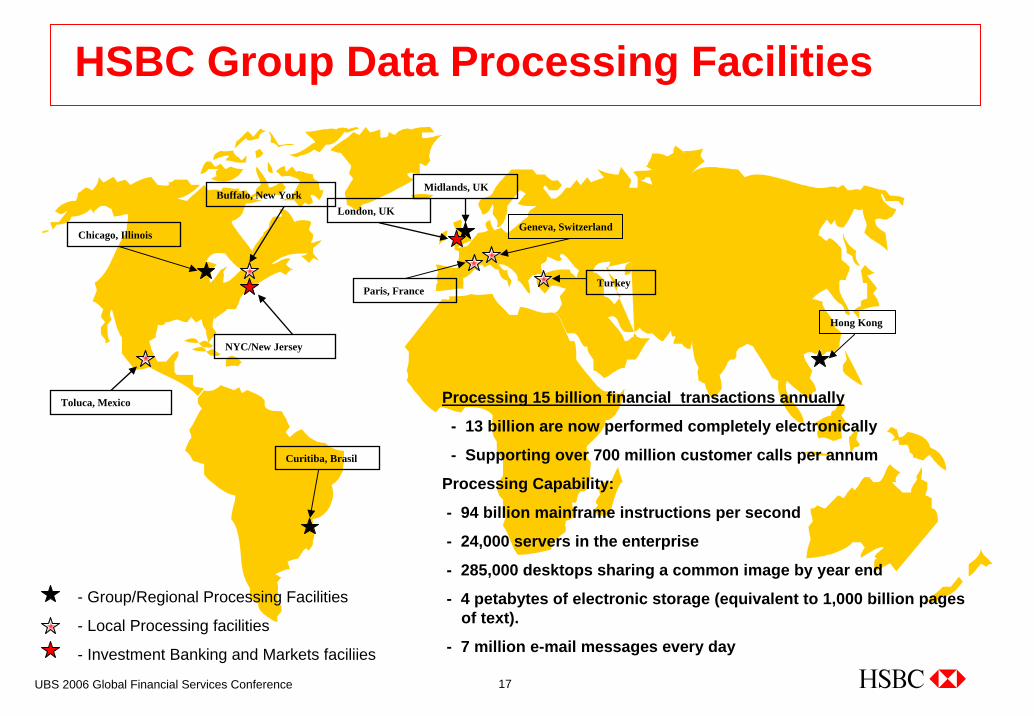

HSBC Group Data Processing Facilities

Chicago, Illinois

Buffalo, New York

NYC/New Jersey

Toluca, Mexico

Midlands, UK

Hong Kong

London, UK

Paris, France

Geneva, Switzerland

Curitiba, Brasil

Turkey

Processing 15 billion financial transactions annually

- 13 billion are now performed completely electronically

- Supporting over 700 million customer calls per annum

Processing Capability:

- 94 billion mainframe instructions per second

- 24,000 servers in the enterprise

- 285,000 desktops sharing a common image by year end

- 4 petabytes of electronic storage (equivalent to 1,000 billion pages of text).

- 7 million e-mail messages every day

- Group/Regional Processing Facilities

- Local Processing facilities

- Investment Banking and Markets faciliies

18UBS 2006 Global Financial Services Conference

HSBC Global Transaction Banking

“[transaction services] businesses have certain attractive attributes to investors: they are diversified and fee-based; the bank serves the role of intermediary rather than principal; and they are scale intensive, (these businesses) …have substantial operating leverage” - Bernstein (2005)“

3 May 2006

19UBS 2006 Global Financial Services Conference

The Benefit of ScaleHSBC formed the Global Transaction Banking division - grouping scale processing businesses ( Payments, Trade and Security Services ) in 2003

Global focus has allowed Transformation by synchronised / optimised Business Model, IT infrastructure and Process Quality change programs :

– Transformation of delivery by efficient and systematic transition of manual processing to offshore “centres of excellence” for Trade, Payments and Securities Services which deliver :

– High quality & low cost processing, and– Value added / differentiating capability and services that would not be possible to deliver

economically in sub-scale onshore locations.

– Prioritised IT infrastructure investment that balances need to deliver new product enhancement with need to

– rationalise architecture to support future growth – to efficiently address global investment to address regulatory requirement– Enhance and deliver consistently high quality client experience across the network

– Systematic & Continuous Quality Improvement (CQI) effort across the network and business lines by– Best Practice identification, transfer and adoption – Embedding of 6Sigma, LEAN and CQI techniques through cost effective training and

mentoring by small team of specialist global practitioners.

20UBS 2006 Global Financial Services Conference

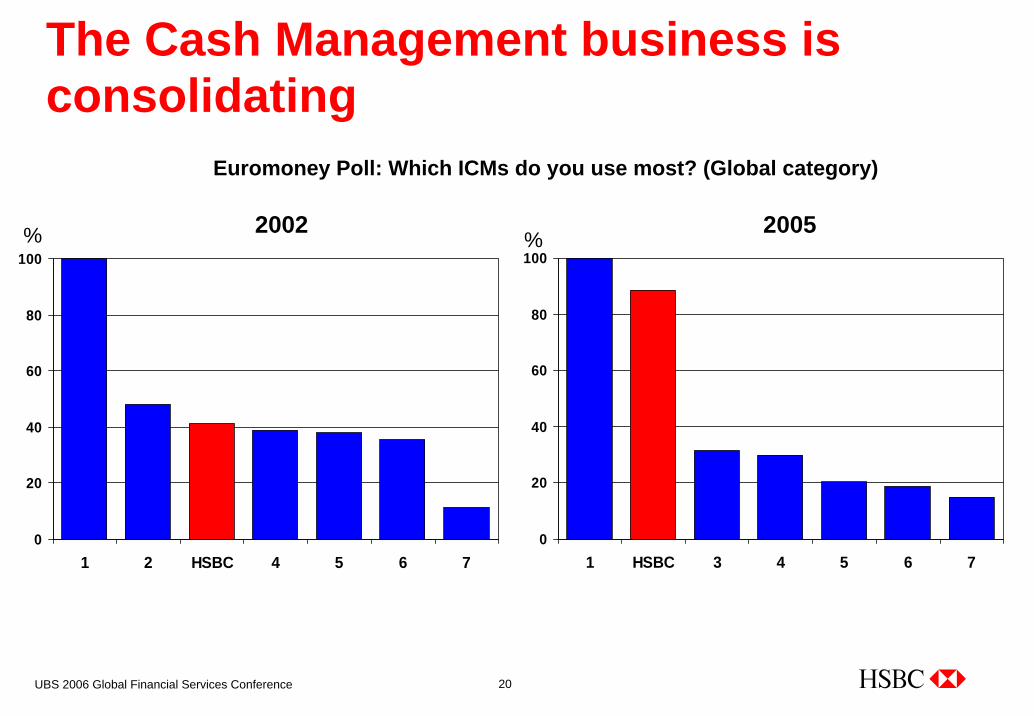

The Cash Management business is consolidating

0

20

40

60

80

100

1 2 HSBC 4 5 6 70

20

40

60

80

100

1 HSBC 3 4 5 6 7

2002 2005% %

Euromoney Poll: Which ICMs do you use most? (Global category)

21UBS 2006 Global Financial Services Conference

Leveraging the Group skills: three examplesMexico

• Internationality of Group key to ensuring success of acquisition

– Influx of Group talent

– Tightened controls (compliance and internal audit)

– Installed new systems (treasury, branches, trade services and credit card)

• Leverage Mexico’s ATM capabilities – location selection, direct sales channel, charity donations.

Rolling out the consumer finance model

• Marketing skills Asia

• Sophisticated analytics Mexico

• Scaleable systems Brazil

22UBS 2006 Global Financial Services Conference

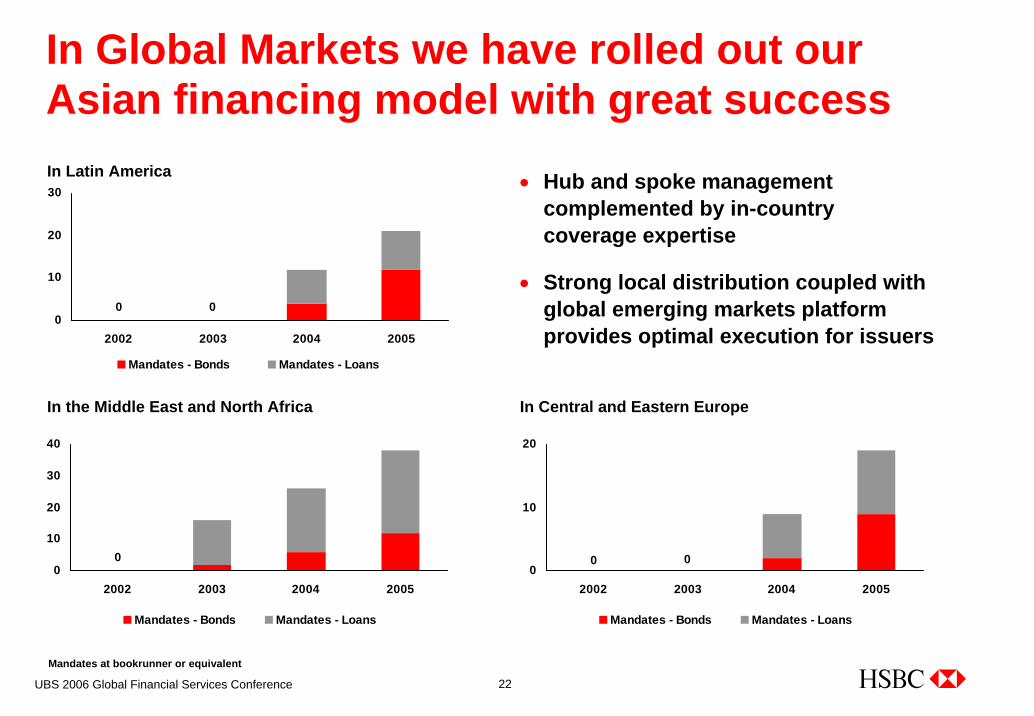

In Global Markets we have rolled out our Asian financing model with great success

• Hub and spoke management complemented by in-country coverage expertise

• Strong local distribution coupled with global emerging markets platform provides optimal execution for issuers

In Latin America

In the Middle East and North Africa In Central and Eastern Europe

Mandates at bookrunner or equivalent

0 00

10

20

30

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

00

10

20

30

40

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

000

10

20

2002 2003 2004 2005

Mandates - Bonds Mandates - Loans

23UBS 2006 Global Financial Services Conference

Is there a conflict in balancing competing demands for capital and other resources while seeking to retain corporate character?• Tone from the top

• Collective Management

• Rotation of senior management

• Training at all levels

• Reward mechanisms

24UBS 2006 Global Financial Services Conference

Distribution remains the key competitive advantage – and therefore highlights the importance of the brand

SydneyAuckland

Wellington

Christchurch

BrisbanePerth

Adelaide

Melbourne

JakartaBandung

SemarangSurabaya

Manila

MedanKuala Lumpur

Singapore Bandar Seri Begawan

Kota Kinabalu

Kuching

Labuan

Bangkok

TaipeiHong KongMacau

Guangzhou

Hanoi

Shenzhen

Ho Chi Minh City

Colombo

Mumbai

Trivandrum

New Delhi

BangaloreChennai

KolkataVisakhapatnam

ChengduChongqing

DhakaMuttrah

Salalah

DubaiKarachi

MuscatJeddah

RiyadhDammam

ManamaTehran

DohaAbu Dhabi

Beirut

AmmanCairoAlexandria

RamallahNicosia

Tel Aviv Wuhan

QingdaoTianjin

Beijing

Osaka

Tokyo

Xiamen

Shanghai

Dalian

Pusan

Seoul

Almaty

Istanbul

Moscow

Valletta

Yerevan

BaghdadAthens

Bratislavia

WarsawPrague

ZurichFrankfurt

Stockholm

RomeMilan

LuganoMonacoMadrid

GenevaParis

Channel IslandsCardiff

Valencia

Barcelona

Birmingham

Dublin

Kuwait City

Luxembourg

Isle of ManLeeds

ManchesterEdinburgh

London

DüsseldorfBrusselsAmsterdam

Port Louis (Mauritius)

Durban

Johannesburg

Cape TownSantiago

Salta

Manaus

Córdoba

San Juan

Mendoza

Neuquén

ResistenciaTucumán

Bahía Blanca

Buenos AiresLa Plata

Pergamino

Porto Alegre

Montevideo

Mar del Plata

Curitiba

CorrientesPosadas

Santa FéPunta del Este

Paraná

São Paulo

Campo Grande

Brasília

Ribeirão Preto

SalvadorRecife

FortalezaBelém

Rio de JaneiroBelo Horizonte

Nassau

CaymanIslands

Colón

Panama CityCaracas

Miami

New York City

Chicago

HoustonDallas

VancouverCalgary

SaskatoonWinnipeg

Seattle Portland

San Francisco

Los Angeles

BostonGlastonbury

Philadelphia

Fredericton

St John’sQuébecMontréal

Bermuda

Ottawa

Washington

Mexico City

Monterrey

Beverly Hills

Buffalo

TorontoTigard

Salinas

San DiegoTijuana

TorreónGuadalajara

PueblaAcapulco

Veracruz

CancúnMérida

BrandonJacksonville

Las Vegas ChesapeakeVirginia Beach

Atlanta

Lewisville

Prospect HeightsKansas City

Sioux Falls

New Castle

Bridgewater

Algiers

Tripoli

Belfast

Budapest

AnkaraAdana

Izmir

Malé (Maldives)

Pune

Chandigarh

Hyderabad

Ahmedabad

Cebu City

Cook Islands

Tortola (British Virgin Islands)

Penang

Chittagong

Suzhou

Inchon

DaeguDaejon

HSBC Group international network

25UBS 2006 Global Financial Services Conference

What is our unique point of view on the world?

In a world where homogeneity and standardisation dominate, we are building our business in the belief that different people from different cultures and different walks of life create value.

We believe that it is the combination of different people, and the fusion of different ideas, that provides the essential fuel for progress and success.

26UBS 2006 Global Financial Services Conference

What does this position demand of each and every one of us?To provide people from different cultures and different walks of life with the financial support that helps them to live the life that best reflects who they are and what they want to achieve.

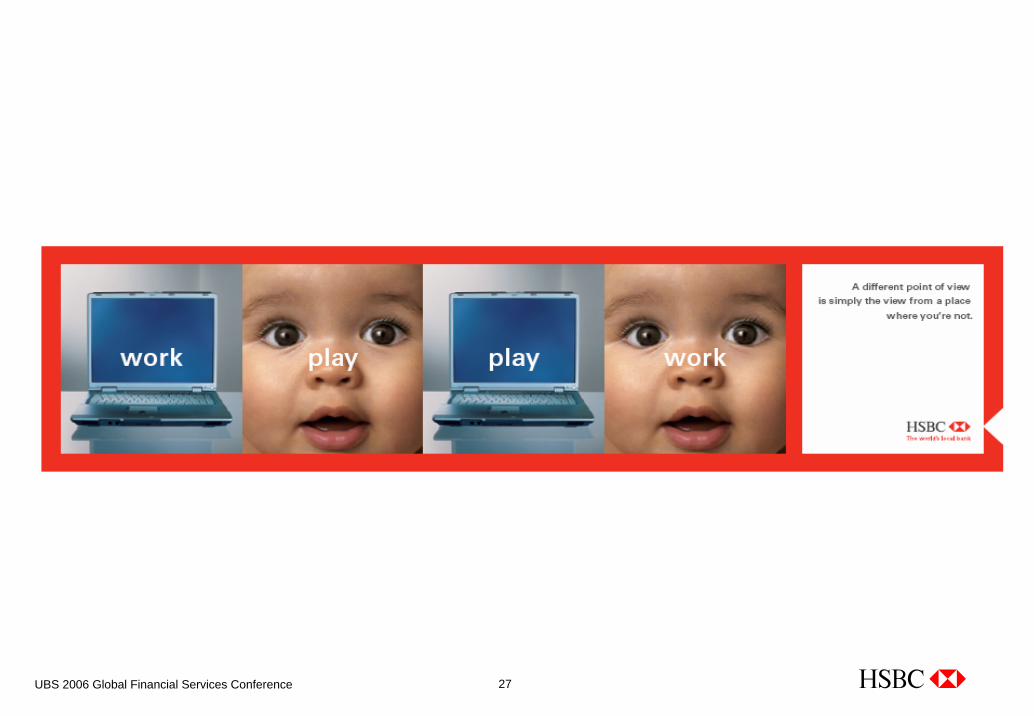

27UBS 2006 Global Financial Services Conference

28UBS 2006 Global Financial Services Conference

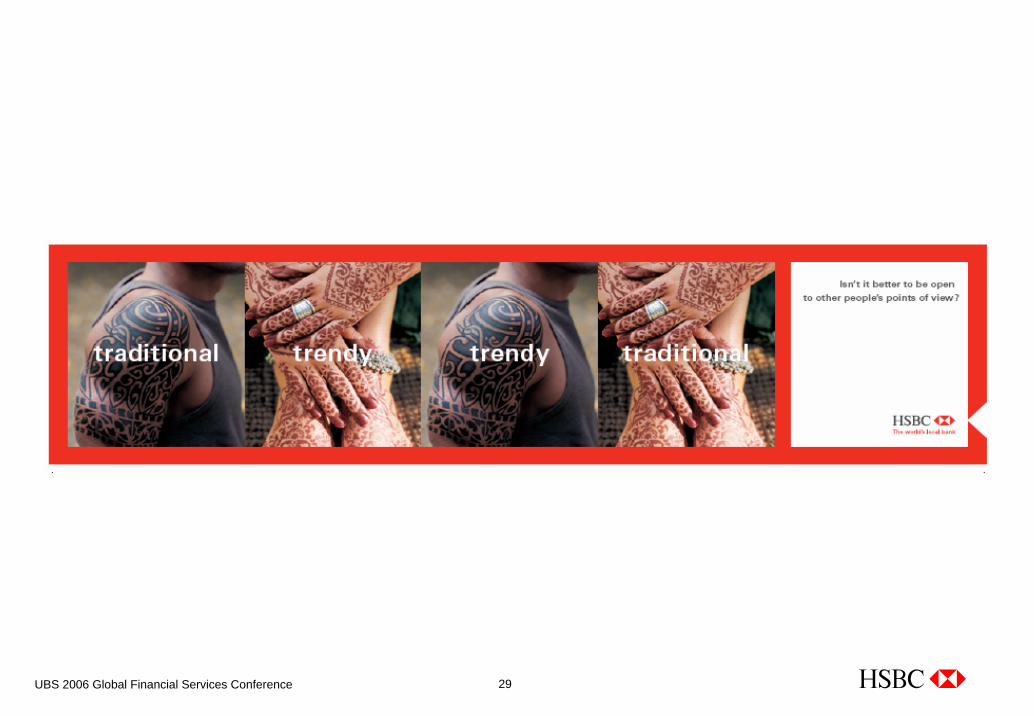

29UBS 2006 Global Financial Services Conference

30UBS 2006 Global Financial Services Conference

Hong Kong

31UBS 2006 Global Financial Services Conference

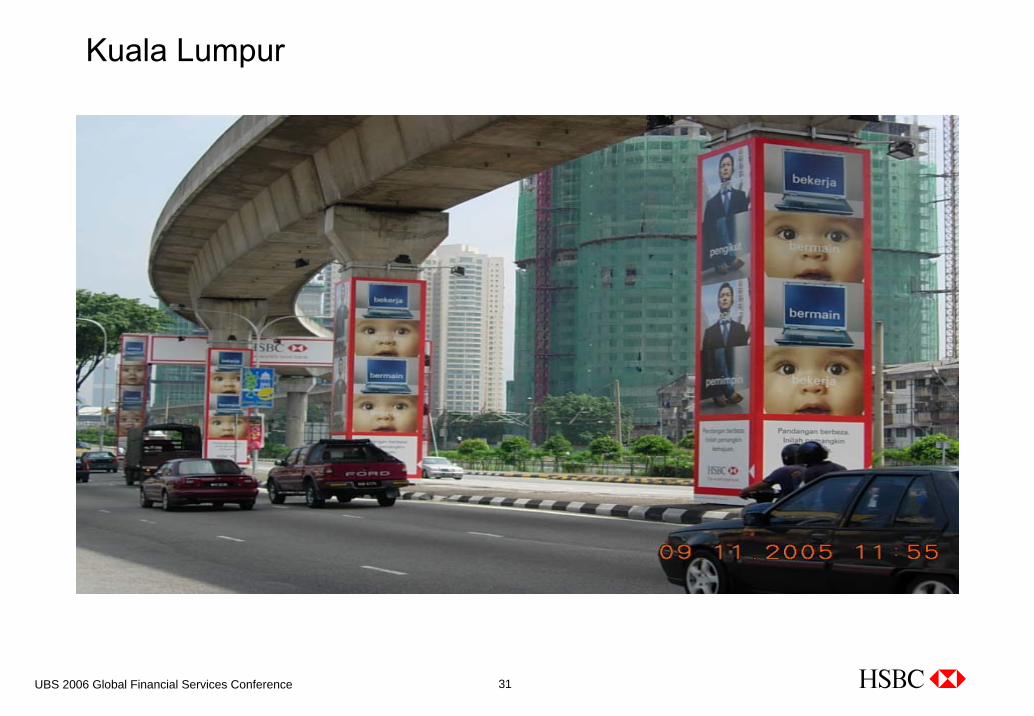

Kuala Lumpur

32UBS 2006 Global Financial Services Conference

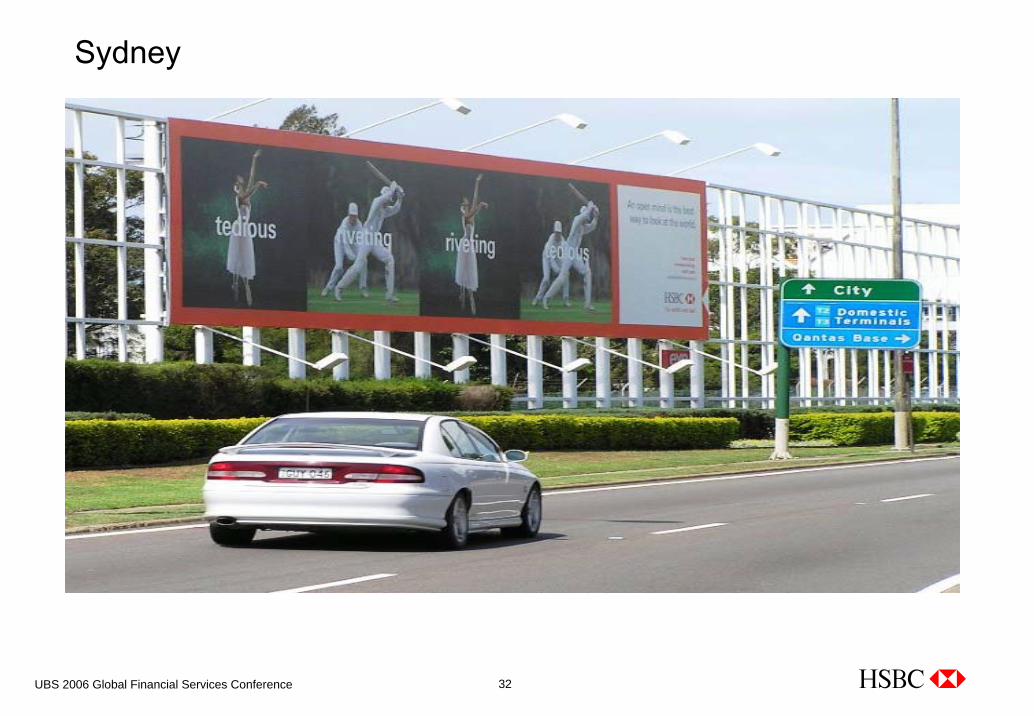

Sydney