Comparative Advantage: Scarcity Comparative Advantage: Scarcity.

Upload

laurent-barbezieuxCategory

view

286download

11

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to FINRA regulations.

Ab

un

dan

t Scarc

ity

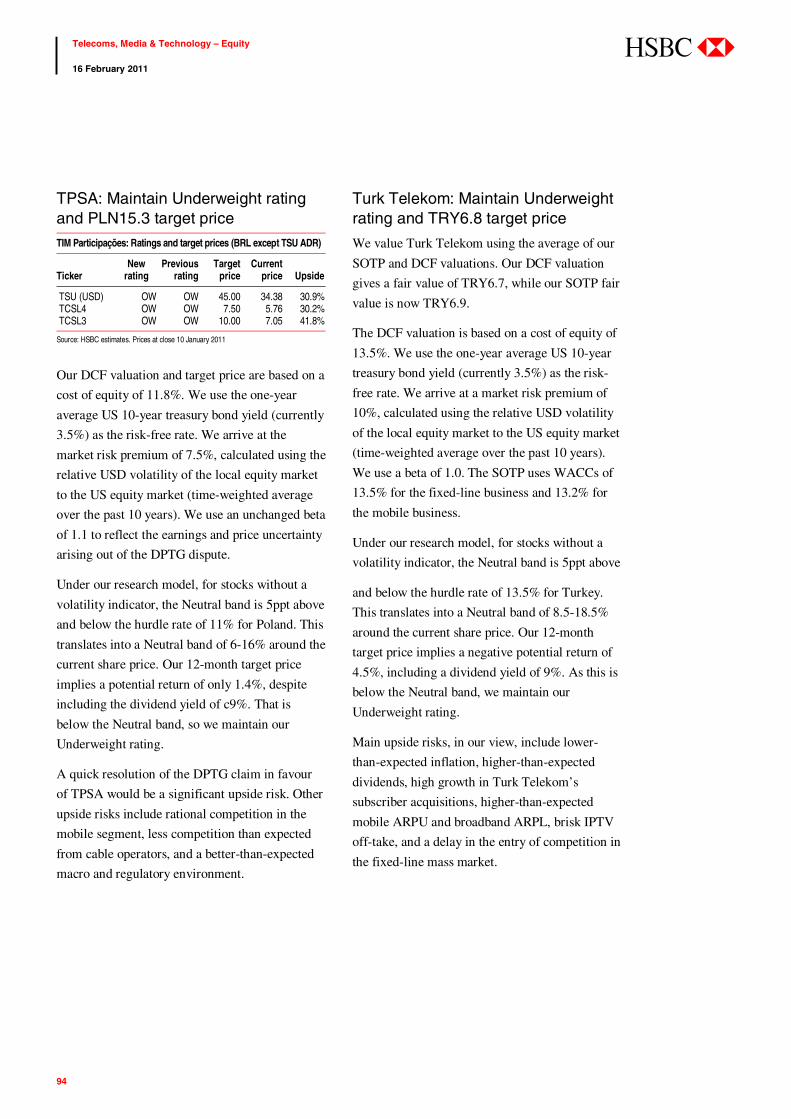

The capital intensity of fibre is now improving fixed-line competitive dynamics and pricing conditions

Mobile capacity constraints are starting to make their effect felt, both in terms of capex and better tariffs

European cable operators, mobile players (Vodafone) and some vendors (Ericsson) are best placed

Disclosures and Disclaimer This report must be read with the disclosures and analyst

certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Glo

bal T

ele

co

ms, M

ed

ia &

Tech

no

log

y –

Eq

uity

Feb

ruary

2011

Abundant ScarcityPricing power is returning to telecoms

Global Telecoms, Media & Technology – Equity

February 2011

Main Contributors

Luis A Hilado*Analyst, Global Telecoms, Media & Technology ResearchThe Hongkong and Shanghai Banking Corporation Limited, Singapore+65 6239 [email protected]

Luis Hilado joined HSBC in 2010 from a US investment bank, where he covered the SE Asia telecom sector. He has over 15 years of equity research experience primarily covering SE Asia telecoms. Luis held a number of positions on the sell-side including Head of Research, Philippines for a European stock brokerage. He holds a BA in Economics and a BS in Commerce and BusinessManagement from De La Salle University.

Dominik Klarmann*, CFAAnalyst, Global Telecoms, Media & Technology ResearchHSBC Trinkaus & Burkhardt AG, Dusseldorf+49 211 910 2769 [email protected]

Dominik Klarmann has worked as a telecoms analyst since 2007. He obtained a degree in management at Bamberg and Madrid Universityin 2004. He has been with HSBC since 2007, having previously worked in management consulting and investor relations at Deutsche TelekomAG. Dominik is a CFA charterholder.

Richard DineenAnalyst, Global Telecoms, Media & Technology ResearchHSBC Securities (USA) Inc, New York+1 212 525 [email protected]

Richard joined HSBC in 2004 to work on the Global Telecoms Research team, with a particular emphasis on technology strategy. Prior tothis, he was research director for Mobile Telecoms at Ovum, a highly respected industry analyst firm, where he spent seven years.

Hervé Drouet*Analyst, Global Telecoms, Media & Technology ResearchHSBC Bank plc+44 20 7991 [email protected]

Hervé has been covering GEMs/CEEMEA Telecoms research for more than 9 years and has been ranked highly and regularly acrossnumerous external surveys. Prior to this, he worked as a senior management consultant in the TMT practice at Deloitte Consulting. He has15 years experience in the Media, Telecoms and Technology sectors, having worked previously as a project manager for SchlumbergerTechnologies. He holds a Full time MBA from London Business School and graduated from Ecole Supérieure d'Ingénieurs enElectrotechnique et Electronique in France.

Tucker Grinnan*Analyst, Global Telecoms, Media & Technology ResearchThe Hongkong and Shanghai Banking Corporation Limited, Hong Kong+852 2822 [email protected]

Tucker joined HSBC in November 2005 and has 15 years of experience as an analyst in the telecommunications, media and technologyindustries. Prior to joining HSBC, he spent five years as a head of regional telecoms for Asia and Latin America. Tucker also spent five yearswith a management consulting firm servicing clients in telecommunications and media. He holds degrees from the University of Virginiaand George Washington University.

Neale Anderson*Analyst, Global Telecoms, Media & Technology ResearchThe Hongkong and Shanghai Banking Corporation Limited, Hong Kong+852 2996 [email protected]

Neale Anderson joined HSBC in March 2007. Previously he spent seven years at the specialist consultancy Ovum, where he was ResearchDirector for Asia-Pacific telecommunications markets. He holds a BA from Oxford University and an MA in Advanced Japanese Studiesfrom Sheffield University.

Nicolas Cote-Colisson*Head of European Telecoms, Media & Technology ResearchHSBC Bank plc+44 20 7991 [email protected]

Nicolas joined HSBC in 2000 as a telecoms analyst in the Global Telecoms research team. Prior to that, he worked as an economist with CCFin Paris for five years and also with the French Ministry of Finance. Nicolas holds a DEA in Econometrics from Paris la Sorbonne.

Kunal Bajaj*Analyst, Global Telecoms, Media & Technology ResearchHSBC Bank Middle East Limited, Dubai+9714 507 [email protected]

Kunal joined HSBC in 2005. Before covering Middle Eastern telecoms, he was a member of HSBC’s EMEA telcos team, working on Eastern European and South African telecoms companies. Kunal is a Chartered Accountant and has an MBA in Finance.

Stephen Howard*Head, Global Telecoms, Media & Technology ResearchHSBC Bank plc+44 20 7991 [email protected]

Stephen Howard is Head of the Global Telecoms, Media & Technology Research team. He has covered the telecoms sector since joiningHSBC in 1996. He also brings experience in the technology industry, having worked previously with IBM.

Luigi Minerva*Analyst, Global Telecoms, Media & Technology ResearchHSBC Bank plc+44 20 7991 [email protected]

Luigi joined HSBC in 2005 as a telecoms analyst in the Global Telecoms Research team. Before this, he was a buy-side analyst at a fundmanager, having previously worked in the Telecoms Practice of McKinsey & Co based in Milan. Luigi holds a Masters in Finance from theLondon Business School and an M.Sc. in Economics and Econometrics from the University of Southampton.

Steve Scruton*Head of Equity Research, CEEMEAHSBC Bank plc+44 20 7992 [email protected]

Steve Scruton is the Head of Equity Research, CEEMEA. He has been with HSBC since 1997, and was previously the co-head of Global TMTin London and Head of Research, Bangalore, a team that provides support to Global Research across countries, sectors, products andservices. Prior to joining HSBC, Steve worked with British Petroleum, Cable & Wireless and a banking house in London.

110214_28253 Telecoms thematic - Stephen Howard_R3:Layout 1 2/16/2011 1:09 AM Page 1

1

Telecoms, Media & Technology – Equity 16 February 2011

abc

Abundant scarcity One way to think about the telecoms sector’s complexities is to break it down into its constituent portions.

A popular division is frequently made between the fixed-line (wireline) and mobile (wireless) portions of

the industry. We would overlay this with a second distinction: between the provision of connectivity (ie

raw bandwidth or capacity) and applications (ie the services that exploit the underlying connectivity).

Combined, this approach yields a two-by-two grid that acts as a convenient means of analysing the sector.

Focusing first on the connectivity layer, our argument is that there is much to play for. The key quality to

bear in mind is scarcity. We believe that this vital ingredient has been largely missing in both the fixed-

line and mobile elements of the sector over the last decade, but is now making a reappearance; as a

consequence, we think that telecoms should – at long last – begin to enjoy a measure of pricing power.

This is of tremendous importance: volumes in telecoms traditionally look after themselves; the problem is

that price deflation is commonly still more powerful, with the result that revenues decline. But if prices

fall less rapidly, the growth in volumes actually has the chance to translate into growth in revenues.

Mobile connectivity

Take the mobile subsector. Although this part of the industry enjoyed heady growth in the late 1990s,

since then the relentless deflationary nature of pricing has taken its toll. However, in a series of research

Summary

A degree of pricing power is (at long last) becoming apparent in the telecoms sector, thanks to scarcity emerging as a factor on both the fixed-line and the mobile sides of the industry. In fixed line, the capital required in the shift from copper-based infrastructure to fibre platforms is re-asserting the importance of scale at the expense of the unbundlers, and resulting in a more benign pricing environment. Meanwhile, in mobile, the intrinsically finite nature of cellular resource has already led operators to begin rationing capacity on price. In view of this new-found ‘abundant scarcity’, we believe that the prospects for monetising connectivity services look very encouraging. Alas, we are much less sanguine about the operators’ ability to monetise the applications that run over this connectivity (such as IPTV or mobile ‘apps’). In our opinion, the connectivity opportunity will have to suffice – but it is enough.

2

Telecoms, Media & Technology – Equity 16 February 2011

abc

reports from late 2009 through 2010 (The Capacity Crunch, Frequonomics, The Cell Side,

SuperFrequonomics), we have argued that scarcity is at long last making an appearance. The physics of

mobile telecommunications (specifically Shannon’s Law) mean that the amount of capacity available is

finite. Even new technologies like 4G/LTE, while offering some efficiency gains versus their

predecessors, are not sufficient an answer to the explosive demand seen from mobile data capacity. As a

result, we have argued that capex is likely to trend upwards, but also that operators will need to ration

their scarce capacity by means of price – in other words, operators will enjoy a measure of pricing power.

Although this view remains very controversial, supporting evidence continues to accumulate. For

example, at its interim results, market bellwether Vodafone indicated the need for a modest increase in

capex, but at the same time not only raised its revenue guidance but also announced it was on-track to

introduce tiered tariffs in all its European markets by the end of calendar Q1 2011. And while, admittedly,

plenty of questions remain about the profitability of data services, we would highlight the excellent

margins achieved by eMobile (one of the world’s very few data-only wireless operators).

Fixed-line connectivity

Although much of our 2010 thematic research focused on the mobile subsector, a parallel set of points

could be made about the fixed-line side of the industry: here too, the power of scarcity is finally making

itself felt, even if its origins are very different. To be clear, the scarcity involved is certainly not related to

the bandwidth available down superfast pipes: instead, it is associated with the prodigious capex required

to deploy such technologies, which limits the number of such competing platforms in any one market.

Clearly, in one sense, the scarcity of access infrastructure platforms is nothing new. But, over the last

decade, regulators have undermined this barrier to entry by enabling entrants to unbundle the incumbent’s

infrastructure at a price related to the incumbent’s own unit costs. Not only has this meant competitors

have had no need to secure billions in funding to roll out infrastructure of their own, but it also ensured

that they could behave, in terms of pricing, as if they had the same scale as the incumbent. With network

reach and economies of scale no longer points of differentiation, the competitive battleground moved on

to areas like marketing, where nimble entrants have tended to get the better of the incumbents.

But now the shift towards next generation access (NGA) platforms providing superfast broadband gives

an opportunity to redress the balance, and reassert the importance of scale. In the present-day, copper-

based ADSL broadband world, unbundling has required little capital. By contrast, in networks that mix

fibre and copper (like FTTN/VDSL), unbundling is intrinsically expensive (as a result of the need to

install electronics not at a handful of local exchanges but instead at tens of thousands of street cabinets);

while in those networks that consist entirely of fibre, it is currently practically impossible. We therefore

Breaking down the telecoms sector into its component platforms and services, with examples of each category

Applications layer Eg IPTV Eg mobile ‘apps’

Eg superfast broadband Eg tiered data plansConnectivity layer

Fixed-line network Mobile network

Source: HSBC

3

Telecoms, Media & Technology – Equity 16 February 2011

abc

believe that the landscape of competition is set to change, moving away from an unbundled framework

and towards being based around wholesale offerings. Crucially, the economics of the latter are radically

better than those of the former, so far as incumbents are concerned. Indeed, there are already indications

that this transition is underway, as well as that pricing conditions are improving as a result.

Naturally, there is the risk that regulators turn tough on the wholesale pricing of fibre-based connectivity.

However, to do so would be to jeopardise the roll-out of this infrastructure in less economically attractive

areas, thereby creating a ‘digital divide’. Our survey of recent regulatory developments points to an

environment much improved by comparison with that pertaining to copper infrastructure, though still

disappointing in some respects. On the closely related issue of net neutrality, a trans-Atlantic divide is

evident, with European bodies adopting a more pragmatic and telecoms-sympathetic stance.

We therefore believe that there is, for the first time in recent history, ‘abundant scarcity’ evident in the

telecoms connectivity layer, on both the fixed-line and mobile sides. Unfortunately, though, we think that

prospects in the industry’s other layer – applications – are rather less rosy.

Mobile applications

Almost wherever one looks, the telecoms players have failed in their ambitions to become providers of

applications. Perhaps the most high profile instance of this has been in the mobile space, where the very

term ‘application’ is now synonymous with Apple and its iPhone. And while Apple does face competition

in this area, the most conspicuous source of rivalry is from Google’s Android platform, rather than from

telecoms companies. The risk here is that, by losing control of the applications layer, the operators will

find themselves disintermediated from some of their most traditional activities.

For example, consider the rise of social networking sites, and the way that they might very well become

the obvious address book intermediary for users looking to contact one of their social circle. Any

software like Facebook, which effectively organises an individual’s contacts, is in a strong position to

help guide how communications between those individuals takes place – and could readily direct a call to

take place via a VoIP application, like Skype. Efforts by telecoms operators in the mobile space to meet

this threat, and bring address book management out of the era of the telephone directory and into the

modern age (via platforms like RCS, the Rich Communications Suite) look to be too little too late. The

dangers here will be self-evident, although it should be emphasised that even service such as VoIP still

rely on underlying connectivity. This remains the preserve of the telecoms operators, and is not territory

that we see players in the applications layer as having either the skills or the appetite to pursue. Even

modest or oblique encroachments in this area by the vendors or technology companies (such as by setting

up as a MVNO or introducing soft SIM functionality) would likely be dilutive and/or counter-productive.

Fixed-line applications

Companies like Skype and Facebook are generally termed ‘over-the-top’ (OTT) providers, since they

offer an application that runs over the top of the connectivity that the telecoms operators deliver. In the

mobile subsector, it is already difficult to avoid the conclusion that this is the natural arrangement of

things. However, OTT is also becoming increasingly relevant in the fixed-line market, especially with

reference to payTV services – a topic closely examined in our thematic report, DisContent (September,

2009). Since this publication, ever more parties have entered the fray, with recent initiatives from players

4

Telecoms, Media & Technology – Equity 16 February 2011

abc

as diverse as Google and Tesco. We suspect that even established media players will struggle in this

environment, let alone telecoms operators. Arguably the incumbents, by investing in what are termed

content delivery networks (CDNs), are themselves tacitly acknowledging this state of affairs, by looking

to provide the hosting services required by OTT providers of video content.

In this confusing environment, we would argue that there remain only two fixed poles: firstly, customers

want the best content; and, secondly, this content is in need of delivery (with ‘content’ here referring to

any application, whether IPTV, VoIP offerings like Skype, iPhone apps, etc). So, content is king, but it

cannot be ‘teleported’ to the customer: it requires delivery – and hence connectivity.

We would argue that, at the very least in the developed world, it is time the telecoms operators embraced

the realities – positive and negative – of the market’s structure. The industry is well placed to be able to

monetise connectivity; it is much less clear what it can really add in the applications layer. Admittedly,

there is an argument for a degree of continued activity in this latter space, if only to retain bargaining

power with the other market participants and to stimulate the uptake of the connectivity services upon

which applications depend. But it is perhaps time that operators embraced the fact that one of the fastest

and most efficient means of encouraging the uptake of new forms of connectivity (such as superfast

broadband and mobile data packages) is to adopt open platforms, as it is these that best foster innovation.

Ironically, the appeal – from a profitability perspective – of applications like IPTV has long been dubious.

Although this service might generate healthy revenues, the bulk of these would need to be passed onto the

content owners. As a result, whether or not a telecoms company owns an IPTV revenue stream matters

less, in our view, than the fact that this service is likely to promote adoption of superfast broadband

connectivity – a field where the operator is much more clearly poised to benefit. Moreover, third parties

might be less anxious of the need to push net neutrality regulation if they could be confident that

prioritisation would not be used to favour the incumbents’ own retail services in the applications layer.

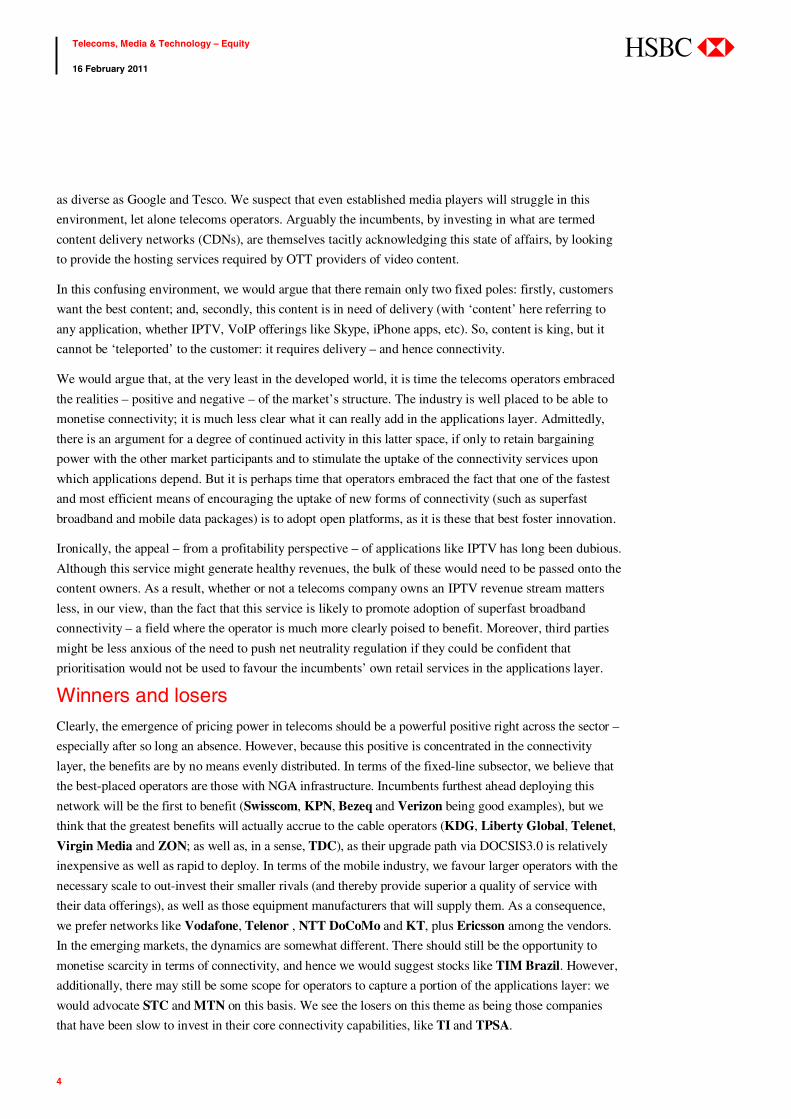

Winners and losers Clearly, the emergence of pricing power in telecoms should be a powerful positive right across the sector –

especially after so long an absence. However, because this positive is concentrated in the connectivity

layer, the benefits are by no means evenly distributed. In terms of the fixed-line subsector, we believe that

the best-placed operators are those with NGA infrastructure. Incumbents furthest ahead deploying this

network will be the first to benefit (Swisscom, KPN, Bezeq and Verizon being good examples), but we

think that the greatest benefits will actually accrue to the cable operators (KDG, Liberty Global, Telenet,

Virgin Media and ZON; as well as, in a sense, TDC), as their upgrade path via DOCSIS3.0 is relatively

inexpensive as well as rapid to deploy. In terms of the mobile industry, we favour larger operators with the

necessary scale to out-invest their smaller rivals (and thereby provide superior a quality of service with

their data offerings), as well as those equipment manufacturers that will supply them. As a consequence,

we prefer networks like Vodafone, Telenor , NTT DoCoMo and KT, plus Ericsson among the vendors.

In the emerging markets, the dynamics are somewhat different. There should still be the opportunity to

monetise scarcity in terms of connectivity, and hence we would suggest stocks like TIM Brazil. However,

additionally, there may still be some scope for operators to capture a portion of the applications layer: we

would advocate STC and MTN on this basis. We see the losers on this theme as being those companies

that have been slow to invest in their core connectivity capabilities, like TI and TPSA.

5

Telecoms, Media & Technology – Equity 16 February 2011

abc

Global Telecoms: Coverage universe

_______________________Overweight________________________ ___________________ Neutral _____________________ _________________Underweight __________________ Company Currency TP Price Company Currency TP Price Company Currency TP Price

Axiata MYR 5.8 5.0 China Mob HKD 81.0 73.1 FET TWD 39.0 42.2CCS HKD 4.6 5.0 KDDI JPY 525000 527000 China Uni HKD 6.7 13.5China Tel HKD 5.1 4.4 M1 SGD 2.5 2.4 GTL Infrastructure* INR 39.0 36.7DiGi.com MYR 29.0 25.6 NTT JPY 4000 3925 MTNL* INR 59.0 42.5Indosat IDR 5800 5000 SingTel SGD 3.3 3.0 Tata Com* INR 225.0 210.1NTT DoCoMo JPY 172000 151100 SKT KRW 177000 162500 Tata Tele* INR 15.0 15.4PT Telkom IDR 9600 7600 RCOM INR 152.0 97.2 KT KRW 60000 41200 SKB KRW 6200 5010 LGT U+ KRW 8900 5970 CHT TWD 91.2 86.7 SmarTone HKD 26.0 24.8 SoftBank JPY 3200 2997 Telstra AUD 3.4 2.9 TWM TWD 69.0 66.7 Tulip Tel INR 235.0 164.6 Maxis MYR 5.8 5.4 Baidu.com* USD 158.0 129.6 PCCW HKD 4.0 3.7 CITIC* HKD 2.7 2.6 StarHub SGD 2.9 2.6 Comba T. Sys* HKD 11.1 8.1 Tel Malaysia MYR 3.9 3.9 eAccess* JPY 79000 51400 Bharti* INR 370.0 318.9 Netease.com* USD 54 44 Idea* INR 75.0 63.7 Tencent* HKD 240 197 J:COM* JPY 97000 86900 XL Axiata* IDR 7700 5200 Perfect World* USD 33.0 21.4 Shanda* USD 43.0 44.8

Asia

ZTE* HKD 32.0 30.3

Bezeq ILS 11.60 10.11 Comstar USD 7.5 6.7 TPSA PLN 15.3 16.6Cellcom ILS 135.0 117.5 Etisalat AED 12.0 11.1 Turk Tel TRY 6.8 7.1EE (Mobily) SAR 71.0 54.8 Qtel QAR 192 171.5 Zain Group* KWD 1.2 1.4Millicom USD 110.0 92.8 Magyar T. HUF 575 537.0 MTN ZAR 148.0 126.0 MarocTel MAD 160 154.2 MTS USD 29.0 19.8 Mobinil EGP 185 133.2 Oman Tel OMR 1.5 1.2 Safaricom KES 5.3 4.4 Partner ILS 90.0 70.6 Zain KSA SAR 8.5 7.9 Sonatel XOF 175000 160000 Telkom SA ZAR 40.0 34.0 STC SAR 48.0 40.3 Turkcell USD 20.6 16.0 TefO2 CZ CZK 450.0 400.0 Vodacom ZAR 83.0 75.3 Tel Egypt EGP 21.0 16.0 Rostelecom* USD 29.6 33.1 Wataniya KWD 2.2 1.8 VimpelCom* USD 18.0 14.4 Orascom T.* USD 6.2 3.3

CEEM

EA

Sistema* USD 33.0 25.0

Aegis Group GBP 1.7 1.5 Belgacom EUR 30.0 27.0 BSkyB GBP 4.8 7.5Atos-Origin EUR 43.0 41.4 BT GBP 2.0 1.9 DT EUR 9.5 9.9Bouygues EUR 41.0 33.7 JC Decaux EUR 23.0 24.3 Elisa EUR 15.0 16.8Capgemini EUR 43.0 39.6 OTE EUR 6.0 7.6 ITV GBP 0.6 0.9Ericsson SEK 95.0 82.1 PagesJaunes EUR 9.0 6.9 Mediaset EUR 4.3 4.9Eutelsat EUR 33.0 28.8 Portugal T. EUR 9.0 8.6 Mobistar EUR 42.0 45.6Freenet EUR 10.0 8.6 Publicis EUR 40 40.9 Nokia EUR 6.5 7.0FT EUR 21.0 16.2 SAP EUR 40 44.4 Fastweb EUR 18.0 18.0Havas EUR 4.9 4.2 Tele2 SEK 160 148.7 Pearson GBP 9.3 10.6Iliad EUR 103.0 77.2 TeliaSonera SEK 58 54.5 TI EUR 1.1 1.1Inmarsat GBP 8.8 7.2 Tel. Austria EUR 11.0 10.5 COLT* GBP 0.8 1.5KPN EUR 15.0 11.8 Informa Group* GBP 4.6 4.6 QSC* EUR 1.4 3.0Lagardere EUR 37.0 33.1 Forthnet* EUR 0.8 0.6 Meetic EUR 22.5 16.8 Telecinco* EUR 9.2 9.9 Reed Elsevier GBP 6.6 5.9 Versatel* EUR 5.5 5.8 Ses Sa EUR 23.0 18.5 Swisscom CHF 470.0 430.9 TDC DKK 58.0 46.3 Telefonica EUR 22.0 18.3 Telenet EUR 34.0 31.2 Telenor NOK 111.0 91.5 Virgin Media USD 33.0 27.4 Vivendi EUR 28.0 20.8 Vodafone GBP 2.3 1.8 WPP Group GBP 8.4 8.3 ZON EUR 4.4 3.8 C&W* GBP 0.8 0.5 Drillisch* EUR 6.0 7.0 Jazztel* EUR 4.0 3.9 Kabel Deutschland* EUR 44.0 38.1 United Bueiness Media* GBP 7.5 7.2 United Internet* EUR 14.0 12.6

Euro

pe

XING* EUR 36.0 39.3

Liberty Global USD 44.0 42.3 AMX USD 64.0 56.8 Net Serv BRL 19.0 18.5Tim Part BRL 7.5 6.0 AT&T Inc. USD 30.0 28.5 Telmex USD 16.0 17.4Verizon USD 41.0 36.4 Tele Norte BRL 31.0 26.1 Vivo Part BRL 69.0 54.1 Telesp BRL 41.0 39.5

US &

Lat

am

Sprint Nextel* USD 5.0 4.6

Source: HSBC estimates, priced as at 11 February 2011

6

Telecoms, Media & Technology – Equity 16 February 2011

abc

Fixed-line connectivity 7

Mobile connectivity 28

Fixed-line applications 54

Mobile applications 67

Winners and Losers 74

Company profiles 97 America Movil (Neutral, TP USD64) 98

AT&T (Neutral, TP USD30) 100

Belgacom (Neutral, TP EUR30) 102

BT Group (Neutral, TP 200p) 104

Bezeq (Overweight, TP ILS11.6) 106

Deutsche Telekom (Underweight, TP EUR9.5) 108

eAccess (Overweight (V), TP 79,000) 110

France Telecom (Overweight, TP EUR21 112

KPN (OW, TP EUR15) 114

KT Corp (Overweight, TP KRW60,000) 116

Mobily (Overweight, TP SAR71) 118

MTN (Overweight, TP ZAR148) 120

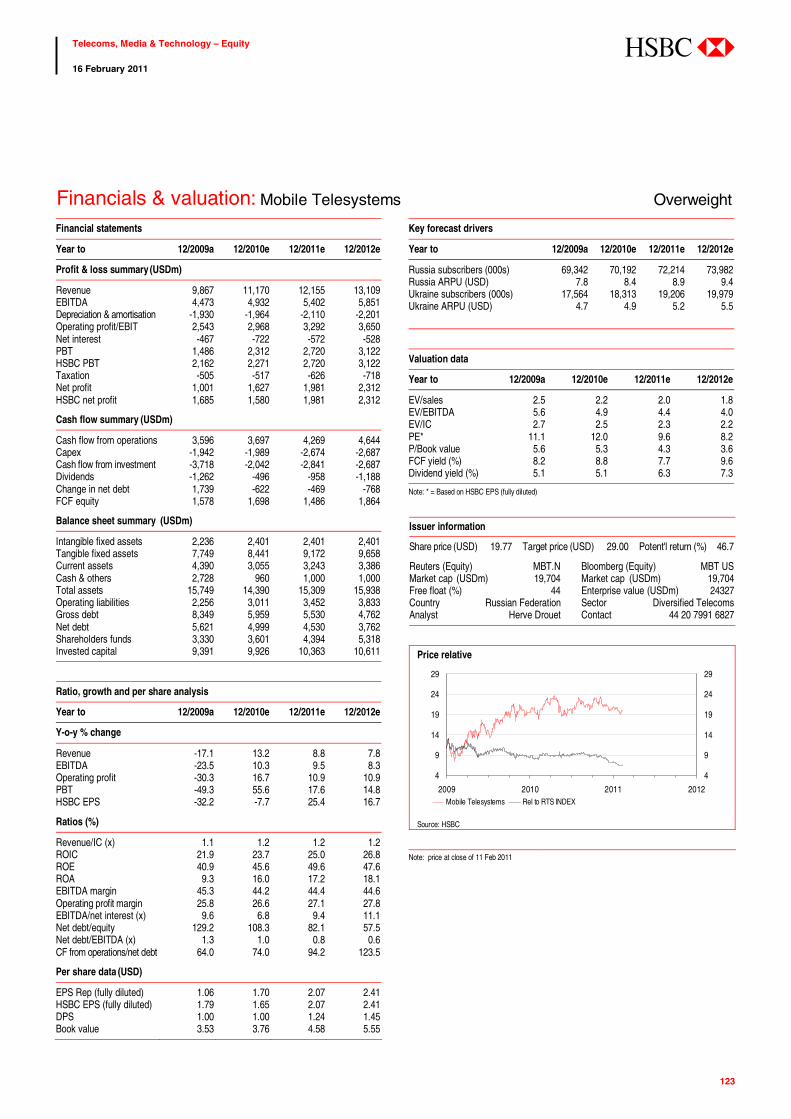

Mobile Telesystems (Overweight, TP USD29) 122

NTT DoCoMo (Overweight, TP JPY172,000) 124

Portugal Telecom (Neutral, TP EUR9) 126

Saudi Telecom Company (Overweight, TP SAR48) 128

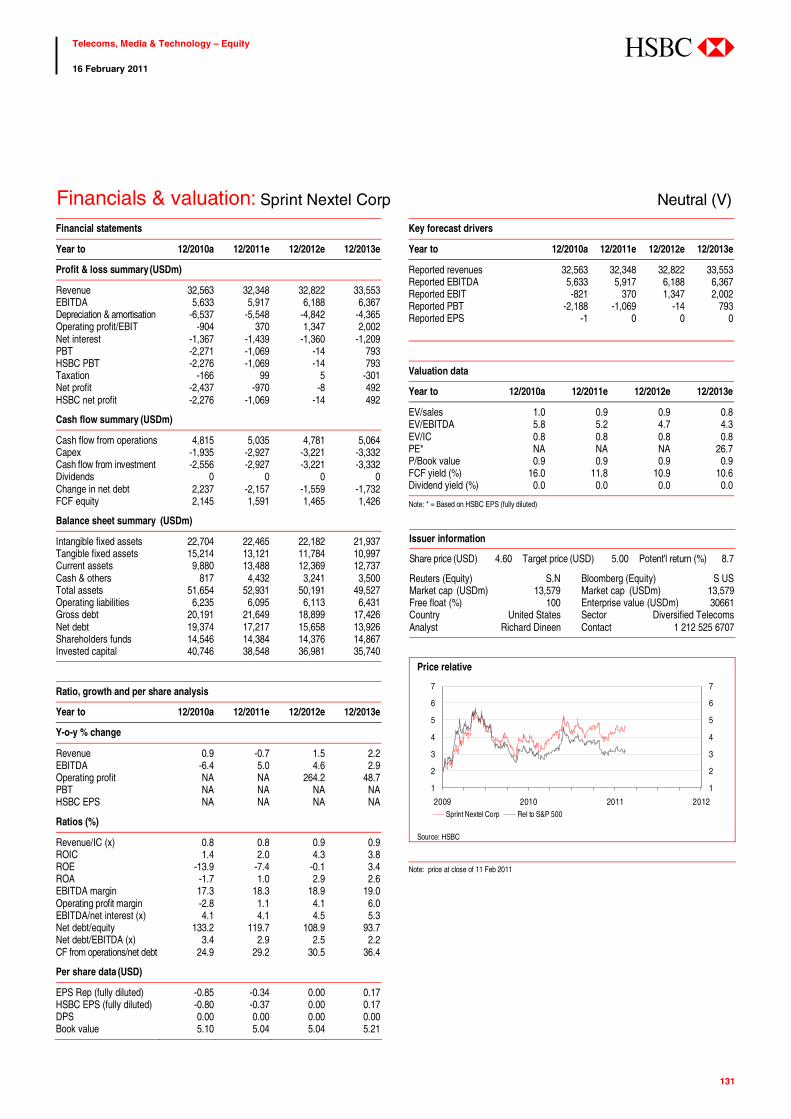

Sprint Nextel (Neutral (V), TP USD5) 130

Swisscom (Overweight, TP CHF470) 132

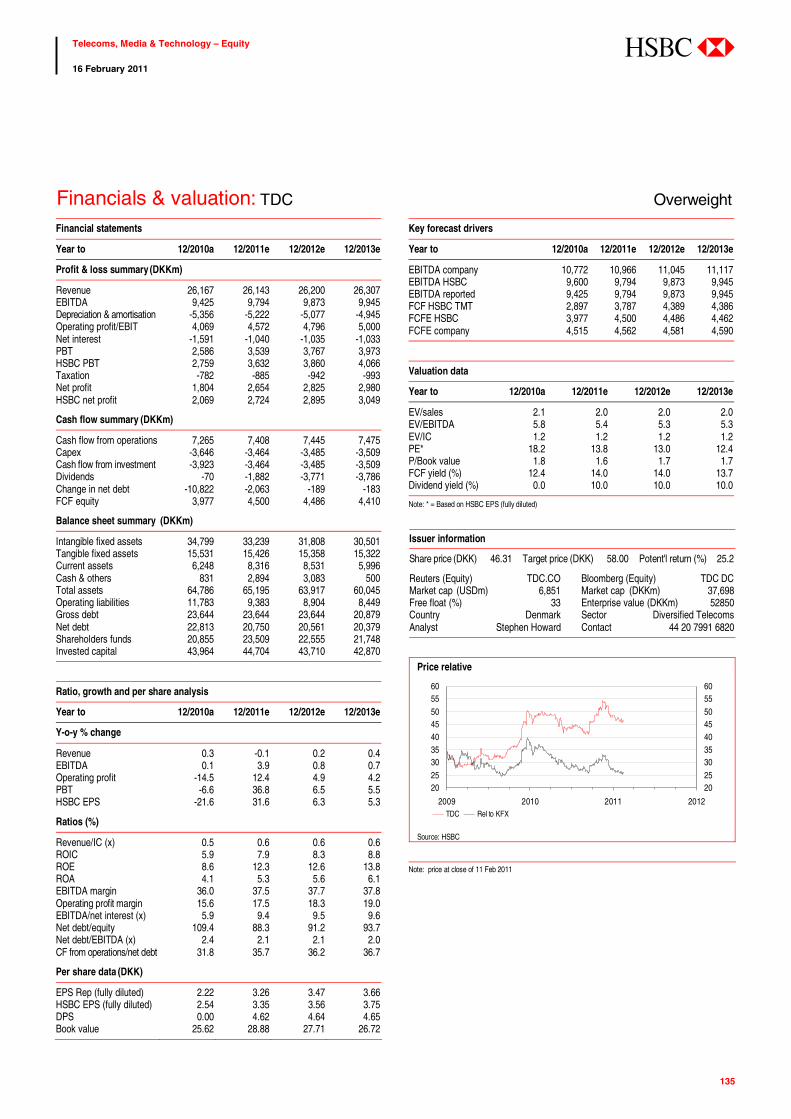

TDC (Overweight, TP DKK58) 134

Tele2 (Neutral, TP SEK160) 136

Telecom Italia (Underweight, TP EUR1.05) 138

Telefonica (Overweight, TP EUR22) 140

Telekom Austria (Neutral, TP EUR11) 142

Telenor (Overweight, TP NOK111) 144

TeliaSonera (Neutral, TP SEK58) 146

Telstra (Overweight, TP AUD3.40) 148

TIM Participações (Overweight, TP BRL7.50) 150

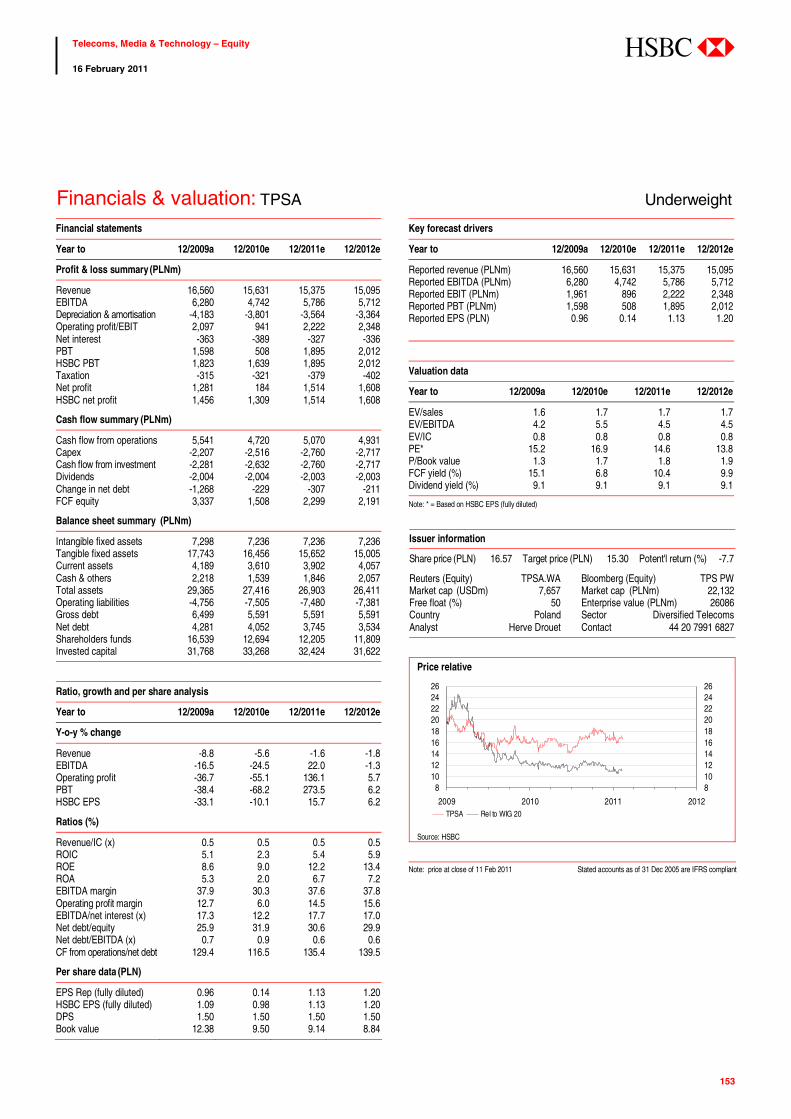

TPSA (Underweight, TP PLN15.3) 152

Turk Telekom (Underweight, TP TRY6.80) 154

Verizon (Overweight, TP USD41) 156

Vodafone (Overweight, TP 230p) 158

Disclosure appendix 161

Disclaimer 164

Contents

7

Telecoms, Media & Technology – Equity 16 February 2011

abc

Introduction There are now the first clear signs emerging that

the transition to next generation access (NGA)

superfast broadband is shifting the competitive

landscape away from unbundling and towards

wholesale. This should provide incumbents (as

well as their cable rivals) with a considerably

better operating environment than has been the

case during the last decade, when the highly

corrosive regulatory intervention that is the

unbundling of the local loop (ULL) dominated the

picture.

Generally, it is only fair to acknowledge that

European regulation is becoming more

sympathetic to those deploying fibre upgrades,

although some of the detailed terms still fall far

short of what the Federal Communications

Commission (FCC) offered to supercharge NGA

roll outs in the US. However, the situation is

reversed on the topic of net neutrality, where it is

the Europeans, in our opinion, who have adopted

the more rational policy – accepting that there are

actually benefits to being able to prioritise certain

types of data traffic, provided the process is

transparent and non-discriminatory.

Such a pragmatic approach seems entirely

appropriate for a wide variety of reasons. One

worth mentioning is the operators’ increasing

interest in entering the content delivery network

(CDN) space, which effectively signals their

interest in hosting providers of over-the-top

(OTT) services. Hence, far from using their

network ownership to discriminate against third-

party suppliers of services utilising their

infrastructure, they are now specifically setting

out to sell to such players.

Age of enlightenment It is obviously ironic to even be discussing

scarcity in the context of the tremendous

bandwidths that NGA access network upgrades

deliver. But the speeds involved do come at a

price, particularly for incumbent operators that

must generally replace all or part of their existing

twisted-copper pair infrastructure with fibre.

Historically, regulators have undermined the

incumbents’ traditional barrier to entry (the

enormous expense of replicating their access

infrastructure) by making it available to third

parties at a unit-cost based price. With the

infrastructure (and its price) effectively common

ground, the terms of competition have migrated

elsewhere – into areas like marketing and

customer service. In such territory, it has all too

often been the entrants rather than the incumbents

that have held the upper ground.

However, the shift towards NGA platforms looks

set to redress the balance, and highlight once more

the importance of scale in the telecoms industry.

Fixed-line connectivity

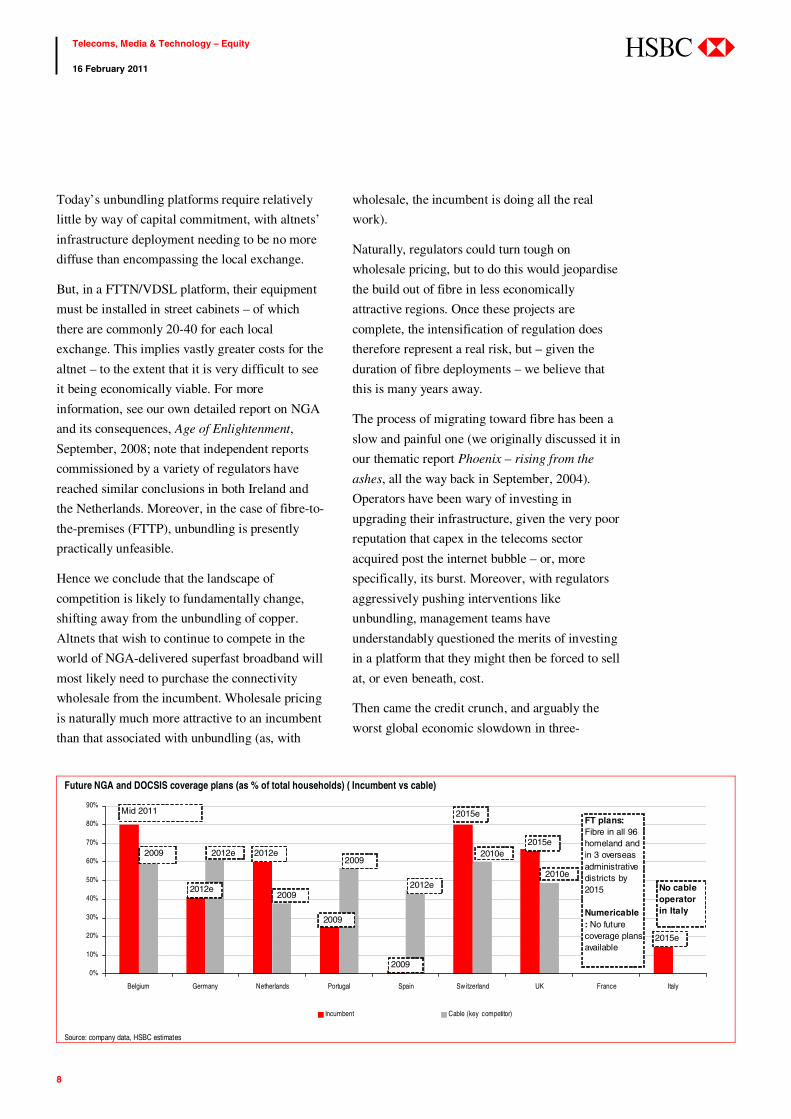

NGA already resulting in competitive landscape shifting to wholesale

EC regulation more sympathetic to NGA, but concerns remain

Net neutrality threat receding in Europe; CDN opportunity emerging

8

Telecoms, Media & Technology – Equity 16 February 2011

abc

Today’s unbundling platforms require relatively

little by way of capital commitment, with altnets’

infrastructure deployment needing to be no more

diffuse than encompassing the local exchange.

But, in a FTTN/VDSL platform, their equipment

must be installed in street cabinets – of which

there are commonly 20-40 for each local

exchange. This implies vastly greater costs for the

altnet – to the extent that it is very difficult to see

it being economically viable. For more

information, see our own detailed report on NGA

and its consequences, Age of Enlightenment,

September, 2008; note that independent reports

commissioned by a variety of regulators have

reached similar conclusions in both Ireland and

the Netherlands. Moreover, in the case of fibre-to-

the-premises (FTTP), unbundling is presently

practically unfeasible.

Hence we conclude that the landscape of

competition is likely to fundamentally change,

shifting away from the unbundling of copper.

Altnets that wish to continue to compete in the

world of NGA-delivered superfast broadband will

most likely need to purchase the connectivity

wholesale from the incumbent. Wholesale pricing

is naturally much more attractive to an incumbent

than that associated with unbundling (as, with

wholesale, the incumbent is doing all the real

work).

Naturally, regulators could turn tough on

wholesale pricing, but to do this would jeopardise

the build out of fibre in less economically

attractive regions. Once these projects are

complete, the intensification of regulation does

therefore represent a real risk, but – given the

duration of fibre deployments – we believe that

this is many years away.

The process of migrating toward fibre has been a

slow and painful one (we originally discussed it in

our thematic report Phoenix – rising from the

ashes, all the way back in September, 2004).

Operators have been wary of investing in

upgrading their infrastructure, given the very poor

reputation that capex in the telecoms sector

acquired post the internet bubble – or, more

specifically, its burst. Moreover, with regulators

aggressively pushing interventions like

unbundling, management teams have

understandably questioned the merits of investing

in a platform that they might then be forced to sell

at, or even beneath, cost.

Then came the credit crunch, and arguably the

worst global economic slowdown in three-

Future NGA and DOCSIS coverage plans (as % of total households) ( Incumbent vs cable)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Belgium Germany Netherlands Portugal Spain Sw itzerland UK France Italy

Incumbent Cable (key competitor)

Mid 2011

2009 2012e

2012e

20092012e

2009

2015e

2015e

2009

2009

2012e 2010e

2010e

FT plans: Fibre in all 96 homeland and in 3 overseas administrative districts by 2015

Numericable : No future coverage plans available

2015e

No cable operator in Italy

Source: company data, HSBC estimates

9

Telecoms, Media & Technology – Equity 16 February 2011

abc

quarters of a century. Although the free cash flow

yields currently seen in the telecoms sector might

give the impression that the industry is

particularly fragile (given these valuation levels,

the markets would certainly seem to perceive it as

such), in fact the sector displayed a quite

remarkable degree of resilience during the

downturn. Admittedly, revenues were negatively

impacted by the troubled macro environment;

however, operators were able to offset this

pressure by making cost savings – with capex

being a primary focus in this regard.

Inevitably, such cuts had an impact on the pace at

which operators invested in NGA upgrades, which

are intrinsically expensive. In Europe, even those

incumbents that were among the more

enthusiastic (like KPN) adopted cautious roll-out

schedules. Meanwhile, in the US, although

Verizon pushed ahead with its highly ambitious

FiOS project, AT&T extended its U-verse

programme over a longer period, effectively

slowing the pace of deployment.

As we argued at the time (in our thematic Déjà vu,

February, 2009), the extent of the cuts possible in

discretionary capex on a short-term view meant

that the sector’s cash flow generation could

remain robust. The key phrase here, though, is

‘short-term’. Operators can indeed cut back on

capex over brief timescales – a process that is

made even easier if their primary rivals are

engaged in the same behaviour. But it is

dangerous to overly prolong this hiatus – and,

indeed, undesirable to do so if there is an

appealing opportunity in the offing. We believe

that NGA upgrades fall into this category.

Despite the macro difficulties, these investments

are now broadly underway, and some of the

benefits that they bring to the competitive

landscape are becoming apparent. The most

important aspect of NGA builds, so far as we are

concerned, are not that they will enable operators

to drive retail ARPUs higher (though, of course,

this is a distinct possibility), but rather that they

encourage a shift away from unbundled-based

competition towards that based on wholesale

products. The latter are typically priced on terms

far more attractive to the incumbent than the

former.

Unbundled to wholesale

We have already seen several altnet competitors

accepting the logic of this transition. For example,

in an event of – we would argue – seismic

significance (but one that went largely

unrecognised by the financial press), UK

broadband provider Orange (better known for its

mobile network) decided to abandon its

German broadband market in 2007… …and 2010: NGA drives consolidation

DT44%

Arcor13%

UTDI14%

Vodafone1%

others1%

TEF O21%

Cable4%

Alice12%

freenet7%

Versatel3%

DT46%

UTDI13%

Cable13%

TEF O28%

Vodafone14%

others4%

Versatel2%

Source: company data, HSBC Source: company data, HSBC

10

Telecoms, Media & Technology – Equity 16 February 2011

abc

unbundled ADSL offering and move onto BT’s

wholesale platform. Admittedly, Orange is now a

relatively small player in the UK broadband

market (though once having been far stronger). Its

DSLAM equipment may have been somewhat

antiquated, and so may well have required

significant investment even to maintain an

unbundled ADSL service. The prospect of having

to invest capex in an ADSL offering at just the

time BT is beginning to deploy fibre was clearly

an unattractive one – given that any new assets

Orange put in place would have a fairly limited

lifespan (in the face of the incumbent’s faster

NGA technology).

Hence, even if Orange had invested in upgrading

its unbundled ADSL platform, it would still have

faced the dilemma of whether or not to invest a

great deal more in a few years time. Maintaining

its presence as an unbundler with ADSL would

have been relatively inexpensive, but becoming an

unbundler of BT’s FTTN/VDSL platform would

involve an immense outlay. And if this capital

commitment was too large to contemplate, what

would be the point in remaining an unbundler in

the meantime? In the end, Orange presumably

decided that, given it could not afford to unbundle

the FTTN/VDSL platform, there was little point

in continuing to invest in unbundling ADSL, and

the company moved directly into taking a

wholesale service.

The example provided by Orange proved to be an

early warning of a broader trend. The choice

confronting Orange arrived sooner than for most

of its peers, owing to the age of some of its

existing infrastructure, and therefore its need to

make an investment to maintain even its existing,

unbundled ADSL capability. However, the same

issue would sooner or later confront every

unbundler. TalkTalk remains an enthusiastic

unbundler of BT’s copper at the local exchange,

but (although it is conducting a small-scale fibre

trial) looks set to wholesale the incumbent’s NGA

product rather than unbundle at the street cabinet

level. Indeed, although Ofcom is insisting that BT

make available unbundled FTTN/VDSL reference

products, the regulator acknowledges that these

have not attracted a great deal of attention.

TalkTalk has made the point in its strategy

presentation that it can still obtain the same,

healthy margin reselling BT’s wholesale NGA

offerings that it achieves today with unbundled

ADSL. BT’s Openreach division, which has the

task of deploying the NGA platform, needs to

tread a difficult line in setting its prices. On the

one hand, obviously, these must be sufficient to

justify the investment made (and the not

inconsiderable risk involved); on the other, these

must not be so high as to deter take up. On

TalkTalk’s suggested numbers, it can indeed

maintain its gross margin, but the really standout

aspect is surely rather the fact that its payment to

NGA builds encourage shift from unbundled products to wholesale

Status quoStatus quo NGA buildsNGA builds

Copper linesLower cost

Credit crunch lower capex NGA upgrade delayed copper still important

US-FCC: unbundling abandoned on networks bringing fibre within 1,000 feet of customer homes

Copper lines

Lower costCredit crunch lower capex NGA upgrade

delayed copper still importantUS-FCC: unbundling abandoned on networks

bringing fibre within 1,000 feet of customer homes

Replace twisted copper with fibreFTTN/VDSL rollout to street cabinet

Higher cost, but superfast broadbandManagement wary

Regulatory risk, but LTScale importanceEncourage shift from unbundled to wholesale

Replace twisted copper with fibre

FTTN/VDSL rollout to street cabinetHigher cost, but superfast broadband

Management waryRegulatory risk, but LTScale importance

Encourage shift from unbundled to wholesale

Status quoStatus quo NGA buildsNGA builds

Copper linesLower cost

Credit crunch lower capex NGA upgrade delayed copper still important

US-FCC: unbundling abandoned on networks bringing fibre within 1,000 feet of customer homes

Copper lines

Lower costCredit crunch lower capex NGA upgrade

delayed copper still importantUS-FCC: unbundling abandoned on networks

bringing fibre within 1,000 feet of customer homes

Replace twisted copper with fibreFTTN/VDSL rollout to street cabinet

Higher cost, but superfast broadbandManagement wary

Regulatory risk, but LTScale importanceEncourage shift from unbundled to wholesale

Replace twisted copper with fibre

FTTN/VDSL rollout to street cabinetHigher cost, but superfast broadband

Management waryRegulatory risk, but LTScale importance

Encourage shift from unbundled to wholesale

Source: HSBC

11

Telecoms, Media & Technology – Equity 16 February 2011

abc

BT approximately doubles when comparing

wholesale NGA to unbundled copper.

The utility of NGA upgrades to the incumbent

should therefore be perfectly clear. The

incumbents are the only operators with the

necessary scale, capital and experience to

undertake nationwide fibre upgrades; even

unbundling such a platform becomes prohibitively

expensive, and this should leave unbundled

copper competitors shifting towards a wholesale

NGA service, for which they will have to pay

(quite properly) considerably more.

Incipient fixed-line pricing power

What is important to emphasise here is that the

prerequisite for a more orderly pricing

environment is the upgrade to NGA infrastructure

(to fibre in the case of incumbents, or to

DOCSIS3.0 on cable platforms). Unfortunately,

because the process of migrating towards fibre

platforms is so expensive and time-consuming,

progress here has often been frustratingly slow.

It is for this reason that the evidence for incipient

pricing power emerging on the fixed-line side of

the industry is much less clear cut than that seen

in the mobile subsector.

Nevertheless, we feel that the anecdotal evidence

is increasingly convincing. The slow pace of

incumbent NGA upgrades also explains why the

clearest examples of pricing power in the fixed-

line market are often to be found among the cable

operators, since their upgrade path to NGA status

via DOCSIS3.0 technology is relatively swift.

Those cable operators already using DOCSIS3.0

in significant portions of their footprint have been

able to show a remarkably resilient top line, even

during the difficult macro environment of the past

few years.

ZON Multimedia (ZON.LS, EUR3.78, OW) in

Portugal provides an example of a cable operator

that has been able to command a certain degree of

pricing power – having found itself able to

increase the pricing on its services for each of the

last three years. In the course of 2010, ZON was

able to raise its tariffs in the region of 3-4% across

the board. This move was then followed by the

incumbent, Portugal Telecom. PT was able to lift

its prices because it has itself conducted a

substantial NGA network upgrade. ZON expects

to be able to increase its prices by about 1% in

2011, despite the austerity measures that have

been implemented in Portugal and the 2ppt

increase in VAT effective from January 2011.

Turning to the UK, cable operator Virgin Media

(VMED.O, USD27.38, OW) has been a

frontrunner among its European peers in

upgrading to DOCSIS3.0, which enabled it to

offer a service that is clearly differentiated from

that of the incumbent, BT. But BT is now also

rolling out a NGA deployment of its own – which

seems to be persuading present-day unbundlers

(like Orange) that a move towards wholesale-

based services is inevitable. Note that despite the

difficult macro conditions in the UK, Virgin

Media announced in February 2011 a set of tariff

increases in its TV packages: the price of its ‘L’

package is to rise by GBP1.25 per month, while

that of its ‘XL’ package is to step up by GBP1.0

per month. In addition, its broadband packages are

to cost an extra GBP0.75 per month. Conversely,

though, the price of the 30Mbps package has been

reduced from GBP20 to GBP18.5 per month.

The above examples therefore suggest that

investing in network upgrades creates the

conditions necessary for the exercise of pricing

power. In our view, failure to invest tends

inevitably to condemn operators to pure price-

based competition. Arguably, one good example

of this is Telecom Italia. On the plus side, the lack

of a cable infrastructure in Italy has limited the

damage that the company’s decision to repeatedly

postpone its NGA roll-out plans would otherwise

12

Telecoms, Media & Technology – Equity 16 February 2011

abc

have caused. However, the resulting lack of

service differentiation has exposed TI to the

aggressive pricing of altnets exploiting

unbundling. For instance, in Q4 2010

Wind/Infostrada, Tele2 and Tiscali started

offering double-play broadband products for a

two year (sic) promotional price of EUR19.95 per

month. TI has opted not to follow this move, but

this decision is likely to have hit the performance

of its domestic fixed-line business in Q4 2010.

The same risk potentially applies to other

operators that have elected to postpone NGA

capex during the recent recession – and so may

also apply to the likes of Telefonica de Espana,

for example.

There is also the hint in some of those (rare)

markets where the deployment of NGA could be

relatively broad based that the elevated levels of

capital involved (a particular step change so far as

the incumbent’s competitors are concerned) will

trigger more responsible pricing policies. This

would seem to be the case in France, a market that

has been the cheapest in Europe in terms of triple-

play services effectively ever since Iliad launched

its EUR29.99 per month offer back in 2003. Its

competitors were forced to align their pricing to

Iliad’s, with only FT managing to retain some sort

of premium to this. (Even this premium has been

eroding, following FT’s price cuts in summer

2010.)

However, in Q4 2010, retail prices were raised by

all the major operators, in response to a hike in the

VAT rate. What is significant, though, is that the

price rises were in excess of what the higher VAT

charge alone would have justified, and therefore

also represents an increase in the underlying

pricing at Iliad and SFR. These operators can

legitimately claim that they now incorporate

additional features in their offerings, such as

unlimited calls to mobile phones or a new set-top

box – but the fact remains that triple-play

packages now cost more on a headline basis than

previously. For example, Iliad's new customers

will be paying EUR37.97 per month (for its triple-

play, fully unbundled, unlimited calls to mobile

package), compared with EUR29.99 previously.

Of the total price increase, only a third can be

attributed to the higher VAT rate. Similarly, at

SFR, the new triple-play offer now costs EUR36.9

per month compared with EUR29.9 previously.

The equivalent bundles would cost EUR39.9 per

month at Bouygues (including three hours of calls

to mobile, rather than unlimited calls) and EUR37

at Orange (but with only one hour of calls to

mobile phones included, and excluding EUR3 for

set-top box rental).

Note that fibre is currently priced at the same

level as ADSL in France, although it has not yet

received any mass-market push. Hence, there

remains the possibility that the operators will also

attach a price premium to the superior bandwidth

services that fibre can support.

Finally, there is the example of the US. In this

market, traditional fixed-line revenues have been

under sustained pressure, driven in particular by

line losses in the region of 8-10% per annum.

An additional headwind arises from the weak

economy. Nevertheless, the absence of regulator-

mandated wholesale or unbundled fibre products,

as well as the growing popularity of services that

exploit superfast broadband connectivity, do

together have the potential to lead to some form of

pricing power.

Of course, because of the very different

bandwidths available over fibre compared with

copper, life-for-like price comparisons are

somewhat spurious. Nonetheless, it is worth

drawing attention to the positive nature of the

‘share of wallet’ effects as seen at the RBOCs.

The ARPU from Verizon’s FiOS customers in Q4

increased by 4% year-on-year, reaching USD146.

Similarly, AT&T’s fixed-line revenues are

13

Telecoms, Media & Technology – Equity 16 February 2011

abc

benefiting from growth generated by its U-Verse

connectivity offerings and related services. Fixed-

line consumer revenues per household have now

been growing for the last 12 quarters in

succession. Additionally, the evidence suggests

that fibre offerings are helping to mitigate the

traditional process of line loss.

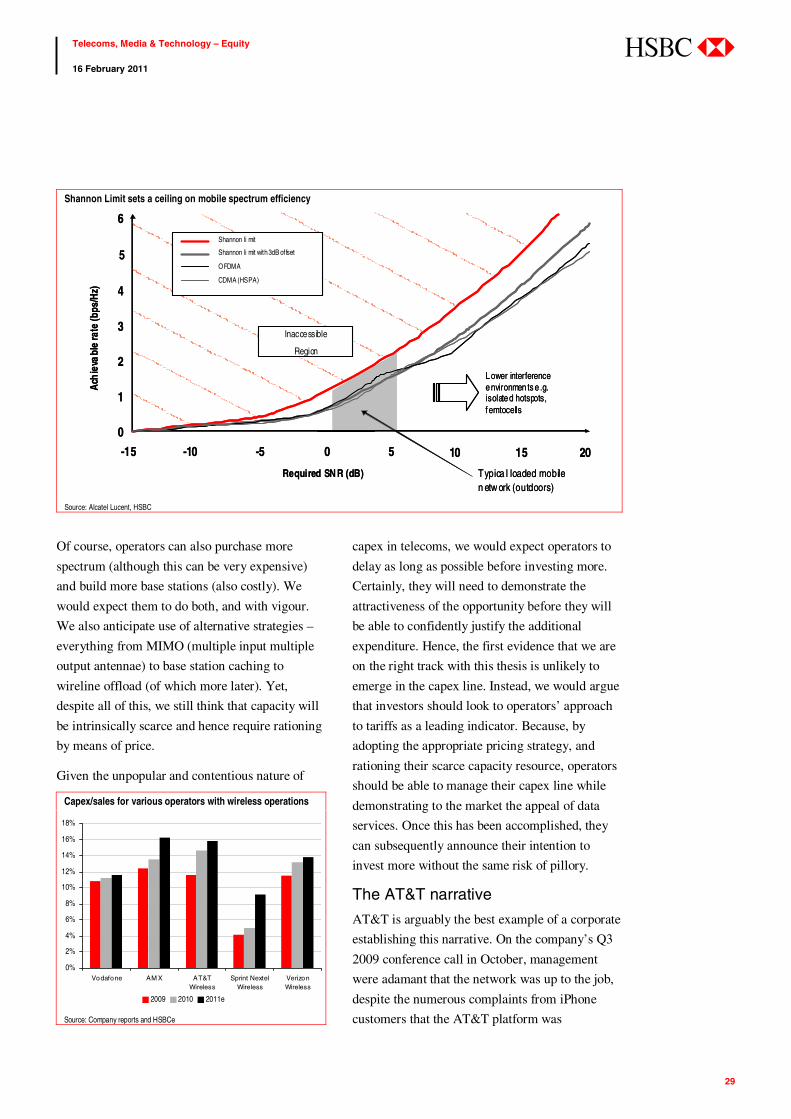

Ray of light One concern about any scenario in which the

incumbent’s scale and ability to deploy capital

work to its advantage must inevitably be that the

regulator will intervene to the detriment of the

incumbent. To an extent, this is inevitable.

However, incumbents still have some powerful

bargaining chips that should ensure they are more

equitably treated than in the present, copper-

dominated world.

The first point to make is simply to repeat that it

will be very difficult – at any conceivable price –

to make activities like unbundling at the street

cabinet very financially attractive, because of the

capital outlay involved (not to mention the

logistical challenges). Most unbundled players

have relatively limited experience with

infrastructure, given that they are presently tasked

with installing their DSLAMs in perhaps a few

hundred local exchanges. They are not generally

geared up for deployments that would involve

visiting literally thousands of street cabinets. So,

even though regulators will undoubtedly define

products and pricing on unbundled FTTN/VDSL

platforms, this does not imply that they will

actually be used.

There have been efforts in some countries by

governments, notably in Australia, to wrest

responsibility for upgrading the infrastructure to

fibre away from the incumbent, namely Telstra.

However, this has proven hugely controversial,

time-consuming and complex. Most governments

would likely prefer to see the work done by the

local expert (ie the incumbent), using the latter’s

access to capital (rather than potentially impacting

an already over-extended state).

Incumbents, in our view, should be enthusiastic to

build NGA platforms, provided the regulation is

supportive. In practice, they likely will look to

receive sympathetic treatment, via (for instance)

flexibility on pricing, or – if it must be dictated –

tariffs established with the use of generous cost of

capital assumptions.

Ultimately, once capital has been irrevocably

committed, regulators have generally shown a

tendency to turn more aggressive. But, in the

meantime, while they are looking to see

substantial quantities of capital deployed, they

have an incentive to remain more generous. And

this ‘meantime’ could represent a considerable

period – fibre networks can take years to deploy,

particularly if there are to be upgrades beyond

FTTN/VDSL towards FTTP.

Hence the incumbents should possess a

bargaining tool that they can make use of for

years to come. If regulators were to turn unduly

harsh mid-build, this could potentially jeopardise

further deployment of fibre. And because

operators are likely to begin their roll out in the

more affluent, densely populated areas, and only

Fibre to the node vs fibre to the premises

FTTN

FTTP

Fibre optic Copper

En

d u

ser

bui

ldin

gE

nd u

ser

bui

ldin

g

Telco office

Telco office

FTTN

FTTP

Fibre optic Copper

En

d u

ser

bui

ldin

gE

nd u

ser

bui

ldin

g

Telco office

Telco office

FTTN

FTTP

Fibre optic Copper

FTTN

FTTP

Fibre optic Copper

En

d u

ser

bui

ldin

gE

nd u

ser

bui

ldin

g

Telco office

Telco office

Source: HSBC

14

Telecoms, Media & Technology – Equity 16 February 2011

abc

then move onto less financially compelling

regions, it becomes particularly important that

regulatory decisions do not impair the profitability

of earlier build – which, in a sense, must cross-

subsidise that which follows.

In our view, the most enlightened approach (pun

intended) is that adopted by the FCC in the US,

which decided to abandon unbundling altogether

on networks bringing fibre within 1,000 feet of

the customer premises. This has encouraged the

very rapid deployment of fibre NGA platforms in

the US. European regulators have not taken this

approach, and consequently have not triggered

anything like the same speed of build out.

However, regulators like Ofcom have at least

conferred pricing flexibility on BT – in other

words, the incumbent has the freedom to set its

own prices for both retail and wholesale NGA

products.

Commission regulation

It will be interesting to see how this particular

arrangement can co-exist with the line coming out

of the European Commission. The Commission’s

earlier documents on the subject of NGA

regulation were very worrying from the

perspective of those hoping to see a supportive

regime put in place to encourage fibre investment.

For instance, the Commission has previously

suggested that the use of fibre between local

exchange and street cabinet was to be considered

a conventional upgrade, and therefore not one that

should attract any cost of capital premium. This

despite the fact that there would be no

conceivable to reason to make such an upgrade

other than to offer superfast broadband services –

services that the Commission itself recognises

entail taking on board a good deal of risk.

The latest documents from the Commission show

some relaxation of its attitude, although arguably

still leave much to be desired from the perspective

of a prospective investor. The Commission’s

argument for its adopting an active role in this

process is that regulation in Europe might

otherwise become fractured, given the wide

variety of approaches national regulators have

already adopted towards NGA. We would be

tempted to see this as something of an advantage

– providing an opportunity to test out a variety of

techniques, and then evolve regulation across the

region towards the most successful variants.

The Commission is adamant that the principle of

the so-called ‘ladder of investment’ must be

maintained, despite the fact that it has been of

only limited success to date. The idea here is to

attract players into the market via products that

require relatively little capital to exploit (ie

wholesale offerings, where the incumbent service

is simply resold), and then have them graduate

towards taking on a greater degree of

responsibility in terms of infrastructure as they

gain in terms of size and experience (ie towards

unbundled offerings, where the altnet provides the

electronics and relies on the incumbent only for

passive network components). The same concept

was applied to ADSL broadband services, and –

indeed – many altnets began with wholesale and

later migrated to unbundling. However, there was

no obvious next stage, given the enormous capital

involved in access infrastructure. Arguably this is

still very much the case.

With respect to NGA, the regulatory mandated

products cover everything from the basic passive

infrastructure (eg trenches and poles) for those

wishing to deploy their own fibre connections, up

through unbundling (eg of the copper loop

between the street cabinet and customer) for those

looking to launch unbundled FTTN/VDSL, and

culminating in wholesale offerings (ie where the

reseller simply resells the incumbent’s service).

But it will be a very tall order, in our view, for an

altnet successful with a wholesale product (given

the relatively thin margins that a relatively

15

Telecoms, Media & Technology – Equity 16 February 2011

abc

undifferentiated product such as this implies) to

make sufficient profit to justify committing the

capital required for unbundling, let alone laying

fibre of its own.

More positively, the Commission does seem clear

that part of its role is to encourage investment in

network:

The [EC] Recommendation… does emphasize the

need for NRAs [national regulatory authorities]

to reflect investment risk in terms of risk premia

and, importantly, in terms of price flexibility

We feel it is a pity, though, that this approach is

not more clearly reflected in its comments on

FTTP unbundling. Clearly, all forms of NGA are

risky, but the degree of capital required for FTTP

puts it in a different league to even FTTN. Hence,

while we see it as regrettable that European

regulators have not followed the FCC in ruling

out unbundling even on FTTN, we would concede

that this form of regulatory intervention does

make more sense applied to FTTN rather than to

FTTP. Given the costs of FTTP, it might have

been hoped that unbundling would have been

ruled out. In fact, with today’s technology,

unbundling FTTP is not really technically

practically feasible, but the Commission still

seems determined that it ought to be introduced as

soon as it becomes so.

Cost orientation

Another weakness, in our opinion, of the

Commission's approach is the focus (for both

unbundling and wholesale, as well as for FTTN

and FTTP) on cost-orientated pricing. The

problem here is that the regulator is referring to

the costs of the incumbent – the largest player in

the market and therefore that with the lowest unit

cost. This tends to penalise those competitors that

have gone to the expense and trouble to deploy

infrastructure of their own, the most prominent

example of which are the cable operators. But

cable companies typically lack the market share

and geographic reach of the incumbents, and

hence also their scale efficiencies. In our view, if

the regulator really wants to encourage

infrastructure-based competition, it ought to be

pricing unbundled infrastructure at a unit cost

price determined not from the incumbent, but

rather from its smaller rivals. The smaller the rival

selected, the greater the incentive for competitors

to commit to investing in infrastructure. (It is also

worth pointing out that the cable operators

themselves might be tempted to extend their

footprints were the potential returns adequately

attractive).

It is worth highlighting the potential injustice

here. An altnet could theoretically simply resell a

wholesale superfast broadband service at a price

offering it a higher return than a cable operator

could generate from its own infrastructure (which

would be smaller scale and, thus, higher unit cost

than the network of the incumbent that the reseller

was wholesaling). This is hardly a circumstance

likely to incentivise future investment.

Ultimately, though, despite the discouraging

nature of the Commission’s philosophical

approach, a great deal rests simply on the cost of

capital that regulators apply to NGA investments.

Here the Commission is clear (without prescribing

actual figures) that the incumbent is entitled to a

premium:

In cases where investment into NGAs depends for

its profitability on uncertain factors such as

assumptions of significantly higher ARPUs or

increased market shares, NRAs should assesss

whether the cost of capital reflects the higher risk

of investment relative to investment into current

networks based on copper.

We have long argued that the immense cost of the

upgrade to NGA platforms could be in part paid

for out of the elimination of the artificial and

16

Telecoms, Media & Technology – Equity 16 February 2011

abc

transient arbitrage that is local loop unbundling.

However, one alternative would admittedly be for

regulators to choose to permit a greater share of

the returns to accrue to the provider of the NGA

infrastructure. The problem with this is simply

that it is likely to translate into higher retail prices,

which is likely to deter uptake – thereby

potentially damaging the economics of the entire

programme.

Like Ofcom, the Commission is also prepared to

countenance a degree of pricing flexibility. This

seems to boil down to permitting the incumbent a

limited degree of flexibility in terms of pricing

use of its FTTx infrastructure at a discount to

those prepared to purchase it either on a longer-

term basis or in higher volumes (since both reduce

the risk of the NGA investment). However, it does

not seem very apparent that the regulator is

permitting the type of price differentiation that is

commonly seen in other industries.

In the scenario where a scarcity of capital on the

scale required for superfast broadband platforms

results in a diminishing number of infrastructure

competitors, it is – in theory – possible to see the

operators being able to introduce a broader range

of price differentiation techniques. The most

obvious mechanism available is to price

differentiate according to the bandwidth provided,

selling faster services at a premium. It is possible

this could meet with regulatory approval, if only

by virtue of the fact that the faster bandwidths

possible over a FTTP platform as compared to

FTTN/VDSL cost greatly more to provide,

because of the need to take the fibre all the way to

the customer’s premises.

In a more conventional market, though, other

forms of price differentiation would likely appear.

For example, operators might sell tiers of data

capacity, just as they are starting to do in the

mobile side of the industry. The size of the tiers

would be considerably greater for fixed-line

broadband than for mobile, but this might

nonetheless be a good way of differentiating

between casual users of broadband (who would

tend to value the service less) and those reliant

upon it satisfy all their entertainment needs,

thereby consuming a great deal of capacity-

hungry video (who would tend to value the

service more highly).

However, it remains to be seen whether the

wholesale pricing structures to be imposed by the

regulators will support this type of price

differentiation. This is despite the fact that it

would perform a useful function: enabling

operators to charge intensive users a figure more

closely representative of the utility they derive

from the service, and therefore helping to pay for

the deployment of this controversial technology

sooner than would be the case had the build out

depended exclusively on the price that less

committed users would be prepared to pay.

The specific issue here is that there is not

necessarily a substantial differential between the

cost to supply a modest and a large quantity of

data over a broadband network (given the

essentially fixed-cost structure of the industry). A

regulatory-imposed, cost-orientated wholesale

pricing regime would therefore tend to undermine

any attempt to price differentiate based on

volumes, because a reseller could always undercut

any materially premium-priced high-usage

offering. While such a pricing regime might be

justified, were the only goal to eliminate

‘distortions’ relating to the misalignment of costs

and pricing, it would also prevent useful price

differentiation aimed at charging customers more

closely in relation to their derived utility – and

thereby securing an improved revenue outlook of

just the type that might encourage a faster

deployment of NGA infrastructure.

17

Telecoms, Media & Technology – Equity 16 February 2011

abc

Could try harder

Overall, we would argue that the regulatory regime

does show some limited signs of being more

sympathetic, with the motive being to encourage

incumbents to deploy NGA platforms. At the same

time, we would continue to emphasise that there

are aspects of the transition to NGA that are

intrinsically unfavourable to unbundling (ie the

expense of visiting the street cabinet). It is evident

that regulators themselves do seem nervous that

they might be perceived as becoming overly

tolerant towards the incumbents, even though the

‘concessions’ involved (as discussed above) would

be solely aimed at encouraging an expensive, risky

investment programme (ie NGA) while

acknowledging the realities imposed by physics (ie

the fact that unbundling is unlikely to be economic

at the street cabinet level).

It is this anxiety that is perhaps the best way to

interpret innovations like the rebranding of

Ofcom’s Active Line Access (ALA) wholesale

product as ‘virtual unbundling’. These labels refer

to a sophisticated wholesale product that Ofcom

intends to impose upon BT – one which will

enable the wholesaler to exert a good deal more

control over its service than would be possible via

equivalent ADSL products. This makes perfect

sense, but the decision to rechristen this service

‘virtual unbundling’ – when what is on offer is

quite obviously a wholesale product – looks

decidedly odd. It is almost as if Ofcom felt the

desire to retain the ‘unbundling’ moniker in order

to emphasise the fact that it is not relaxing its

stance towards BT (a fact that no one would likely

dispute in any case). Note that the European

Commission has accepted Ofcom’s proposal, but

indicated that the virtual unbundling product will

not be sufficient in itself. The Commission wants

Ofcom to secure the unbundling of BT’s NGA

infrastructure as soon as this is practicable.

Net neutrality However, there is one further area of activity

where European regulators – if not their US

counterparts – seem to be leaning towards a

stance that really should be supportive of

investment: on the fraught topic of net neutrality.

The question here boils down to the degree of

freedom that operators should have in how they

manage and tariff their networks, and could have

wide ranging implications in terms of the structure

of the overall market and the degree of incentive

operators are provided to invest in NGA platforms

(and hence the likely speed of their deployment).

Operators can use deep packet inspection (DPI) technology to implement traffic management policies, such as prioritisation according to the requirements of the underlying service (e.g. delay-intolerant voice and video prioritised over email and browsing)

Payload

Hea

der

Policy Engine (PE)

- Prioritize premium users

- Prioritize by service need

- Block objectionable content

Node

Deep packet inspection

Fixed/mobile Internet

Users

Payload

Hea

der

Policy Engine (PE)

- Prioritize premium users

- Prioritize by service need

- Block objectionable content

Node

Deep packet inspection

Fixed/mobile Internet

Users

Source: HSBC

18

Telecoms, Media & Technology – Equity 16 February 2011

abc

We have never found the arguments for net

neutrality to be in the least convincing (see Net

Neutrality, April 2006). Unfortunately, this has not

prevented the concept from gaining widespread

acceptance in certain quarters, and with certain

regulators – especially the FCC in the US.

The scope for conflicts of interest in this area will

be readily apparent. Operators, faced with the

colossally expensive challenge of rolling out

superfast broadband networks would like

maximum flexibility in terms of managing, and

charging for, the use of their infrastructure. This

boils down to two key areas:

First, telecoms companies would like to

manage their resources as efficiently as

possible with the use of traffic management

techniques. This would involve, for example,

prioritising the packets of a time-sensitive

video stream (time-sensitive because the

viewer will be immediately conscious of any

delays or interruptions) over that of an email

(where the recipient is likely to be less

sensitive to a modest delay); see the

accompanying diagram.

Second, the operators would like flexibility in

charging for this prioritisation. This would

involve not only applying a premium for the

delivery of prioritised traffic, but also

potentially billing not only the recipient but

also the party sending the packets.

Naturally, the internet players are concerned that

their services might be de-prioritised in favour of

services sponsored by the telecoms operator (rival

video streaming services, for instance); and/or that

they would start having to foot more of the bill for

the ongoing explosion in data traffic volumes

(rather than this being borne by the end-user).

The FCC has been largely sympathetic to these

worries - one of the reasons that we have become

progressively less positive on the US RBOCs as

investments and more upbeat about prospects for

the incumbents in Europe, where the regulation on

net neutrality is looking more reasonable. It will

not have escaped the FCC’s attention that the US

has produced a set of enormous internet

powerhouses, such as Google and Amazon. Such

companies can export their services across the

globe in a way that domestic telecoms providers

cannot. In terms of US industrial policy, therefore,

it arguably makes sense to privilege the internet

names over their telecoms peers. This is

particularly the case given that much of the NGA

fibre upgrade has already been completed in the

US. In other words, the capital has already been

committed, and hence the regulator no longer

needs to create a more attractive returns

environment in order to stimulate the relevant

capex.

One flashpoint has been the legal case embroiling

the FCC and Comcast, the US cable giant.

Comcast had been de-prioritising peer-to-peer

traffic on its network from services like

BitTorrent. The FCC objected to this, and

intervened; in response, Comcast changed its

approach but nonetheless introduced a 250GB

usage cap on its customers. This move did not

please the regulator, which then decided to

sanction Comcast. The latter took the matter to

court, winning the case on the grounds that the

FCC lacked the necessary authority to intervene.

The longer-term implications of this tussle,

however, remain unclear. One risk is that it

incentivises the FCC to secure the necessary

authority via the statute book. However, the

regulator has also been pursuing a more informal

approach, with the aim of keeping regulation of

the internet to a minimum (which seems to be

something that most sides can at least agree is

desirable).

Nonetheless, the fact that this dispute entered the

courts in the first place is surely somewhat

19

Telecoms, Media & Technology – Equity 16 February 2011

abc

alarming. Comcast acted to ensure that it could

preserve a good quality of service on its

contended cable network despite the excessive

burdens placed on its platform by a small minority

of its customers using peer-to-peer applications.

Cable networks are intrinsically contended, as all

customers on a given street share the same coaxial

cable; hence capacity taken by one user is no

longer available for another. In such

circumstances, individual customers can degrade

the service of their neighbours, and Comcast’s

actions were taken to prevent this. It is surely an

added irony that probably the most popular use of

the application in question – peer-to-peering – is

video piracy.

Atlantic divide

In Europe, circumstances are somewhat different

to those across the Atlantic. Most of the

investment in NGA upgrades has yet to be made,

and incumbents are cautious about the economic

case for fibre. Given this environment, it makes

sense to give telecoms players as much freedom

as possible to create business models that will

support NGA deployment. Europe’s politicians

have made it perfectly plain that fibre is a priority,

out of fear that the continent’s economy might fall

behind; supporting NGA investment will arguably

be more important (in their eyes) than ensuring

that existing internet giants – largely foreign in

origin – enjoy the benefits of connecting to their

end users at the minimum price.

Ultimately, we remain of the view that hard-line

net neutrality is simply unworkable. Even in the

fixed-line network, there will always be

bottlenecks where capacity is scarce. It is simply

not possible to build a network that at all times

and in all places will be free of constraints. Given

this reality, it will always be necessary to apply

some traffic management policies. Packets

belonging to services that are particularly time-

sensitive to delay (with that most traditional of

offerings, voice, being the clearest example) need

to be conveyed with priority over and above data

traffic relating to, for example, an overnight

routine system backup. Indeed, services that are

really demanding in terms of bandwidth – such as

high-definition video – will arguably never be

able to mature successfully unless supported by

techniques such as prioritisation. It is thus,

ironically, actually in the internet players own

interests’ that prioritisation be permitted, because

otherwise they will likely find themselves

practically constrained in terms of what they are

able to offer customers with an adequate quality

of service.

Although net neutrality advocates often suggest to

the contrary, the presence of prioritisation is

actually the status quo. For example, to take a

case reduction ad absurdum, a corporate taking a

leased line is purchasing dedicated capacity

between two points, in other words, full

prioritisation. Note that traditional switched voice

services are also, in effect prioritised, given that

the circuit conveying the communications is held

open between the callers for the duration of the

call, with no other traffic being permitted over

that portion of the pipe.

It is further worth highlighting that the presence

of net neutrality should not be thought of as

necessarily helping the ‘little guy’. Net neutrality

advocates often suggest that prioritisation charges

would hamper the development of the next

generation of internet entrepreneurs, but it is

revealing that the current giants of this space

invest prodigious quantities of capital in

optimising their response times. For instance, the

likes of Google have constructed numerous data

centres at optimally located points on the global