How to lower your ltc insurance premiums

21

LTC INSURANCE How to lower your premiums on

-

Upload

ltci-partners-llc -

Category

Economy & Finance

-

view

560 -

download

3

Transcript of How to lower your ltc insurance premiums

LTC INSURANCE

How to lower your premiums on

Let’s say you are a 60 year old married

female interested in LTC Insurance. Your

husband is not interested in buying, but

you had personal experience with

caregiving and want coverage!

You research on the internet and read an article that the best plan design includes coverage that will pay you at least $4,500 per month for three years – with a benefit that will inflate at 5% compound.

You contact a leading insurer and find the premium for the above plan is…

$9,015.68

(per year)

Source: Leading LTCI Insurer, 2015 standard rate class, Alabama

Wait, what?

What if you could reduce that premium –

by a lot???

But…

You can reduce premiums by adjusting benefits. The following

examples represents savings possible through different plan design that

maintain the core value of LTC coverage.

Cost reducing Tip 1

Consider having your husband buy. When

couples both get coverage, premiums are substantially reduced

New annual premium for you when your

husband buys too: $5,281.19

($3,734 savings!)

Source: Leading LTCI Insurer, 2015 standard rate class, Alabama

Why? Carrier claim studies show that when both partners in a

relationship have coverage they don’t claim as much as singles, and especially single woman.

That’s why they price products to attract male buyers – who are usually more reluctant to buy.

Cost reducing Tip 2

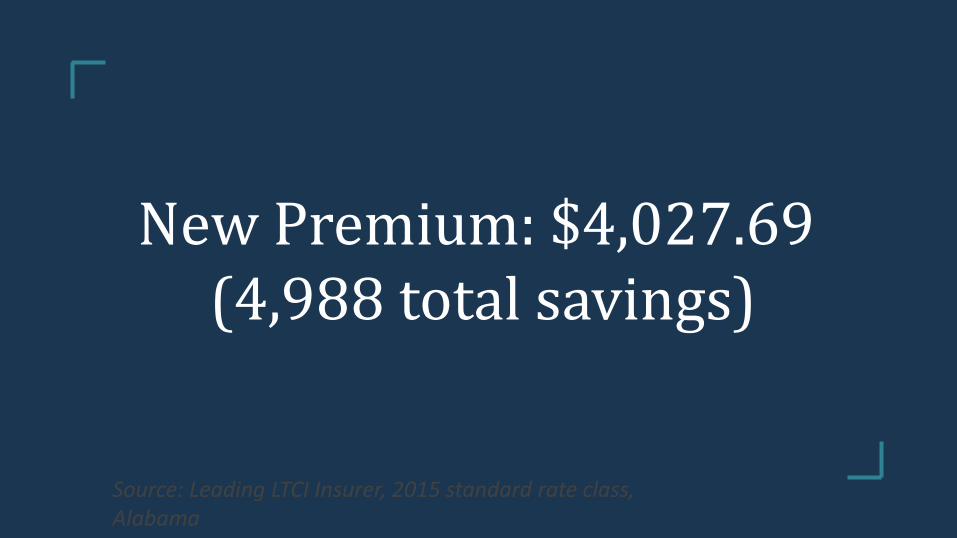

Increase your elimination period, or deductible.

Increasing the period from 90 days to 180 days will result in…

New Premium: $4,027.69 (4,988 total savings)

Source: Leading LTCI Insurer, 2015 standard rate class, Alabama

Not surprisingly, claim studies show that people with longer deductible

periods don’t have as high claims and can be offered lower premiums.

Cost reducing Tip 3

Change the rate of inflation you policy increases each year. If you have the policy increase at a 2%

inflation rate instead of a 5%, the new annual premium would

be:

New premium $1,532.61(7,483.07 total savings)

Source: Leading LTCI Insurer, 2015 standard rate class, Alabama

With inflation and interest rates very low, the cost of insurers to offer 5%

inflation is VERY expensive. For those who want more coverage, it might

make sense to buy a bigger monthly benefit up front instead of choosing an

automatic inflation increase

1,500 Bananas per year? I can afford that.

Let’s compare again. This is a long-term care plan for a 60 year old married female with a leading carrier and standard (non-preferred) rates.

Plan A Plan B

Monthly LTC Benefit for nursing home, assisted living or home care

$4,500 $4,500

Elimination Period (deductible)

90 calendar days 180 days of service

Benefit Pool 36 months x $4,500= $162,000

36 months x $4,500 = $162,000

Annual increase in inflation percentage

5% 2%

Couples coverage Only one spouse buys Both spouses must buy

Annual premium for her $9,015.68 $1,532.61($1,532.61 for him)

Other tips when buying LTC coverage:

• Don’t try and cover 100% of the cost -plan on coinsuring some of the risk

• Come up with a premium budget first than design a plan• Work with a professional who represents several carriers so

you can compare• Don’t always pick the lowest price carrier but instead focus on

benefits important to you• Don’t wait! Premiums are based on your age at issue. The

premiums for a 65 year old are much higher than a 60 year old

Copyright 2015 LTCI Partners, LLC. Products may not be available in all states and product features may vary by

state. If available, invitations for application for LTC Insurance are made through licensed advisors of LTCI

Partners, Lake Forest, IL, the agent in any application; in California and Utah, dba LTCI Partners Insurance

Services. Cal. License # 0D51716. LTCI Partners or its licensed representatives are currently licensed in all 50 states and the District of Columbia. License numbers are

available upon request.

THANK YOU!