How to InHow-to-Invest-Senior-Secured-Loan-Marketvest Senior Secured Loan Market

16

Visi t t www.pionline.com/lsta for exclusive featured content, white papers and web seminar ADVERTISING SUPPLEMENT

-

Upload

diomidis-dorkofikis -

Category

Documents

-

view

12 -

download

1

description

How to InHow-to-Invest-Senior-Secured-Loan-Marketvest Senior Secured Loan Market

Transcript of How to InHow-to-Invest-Senior-Secured-Loan-Marketvest Senior Secured Loan Market

Visitt www.pionline.com/lsta for exclusive featured content, white papers and web seminar

ADVERTISING SUPPLEMENT

pi supp.qxp 5/9/11 10:04 AM Page 1

Navigating the global markets for senior secured loans?

Babson Capital can be your guide.

One of the world’s largest senior secured loan managers with more than $24 billion in loan assets under management1

A staff of 68 investment professionals with dedicated operations in both the U.S. and Europe and superior access to deal flow1

An investment team of great breadth and depth with expertise in analyzing companies and capital structures and experience navigating several market cycles

Uniquely positioned to identify and capture relative value in the global senior secured market

We are also well versed in the many ways you can access senior secured loans, such as commingled vehicles, separate accounts and structured funds like collateralized loan obligations (CLOs).

For senior secured loans, let us help you arrive at your destination.

Global High Yield Private Finance Fixed Income Alternatives & Equity Real Estate

Boston & Springfield, MACharlotte, NCwww.BabsonCapital.com

MORE THAN INVESTING. INVESTED.SM

LSTA5634

Think of us as a GPS for

SENIOR SECURED LOANS.

1. As of March 31, 2011. Assets include Babson Capital Management LLC and its subsidiary Babson Capital Europe Limited

11pi0176.pdf RunDate:05/16/11 PI LSTA Suppl Full Page Color: 4/C

11pi0176.qxp 5/6/11 1:03 PM Page 1

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

ADVERTISING SUPPLEMENT

3

This special advertising supplement is not created, written or produced by the editors of

Pensions & Investments and does not representthe views or opinions of the publication or its parent company, Crain Communications Inc.

Babson Capital Management LLC201 South College St., Suite 2400 Charlotte, NC 28244 Contact: Anthony Sciacca Managing Director, Head of Global Business Development Tel. [email protected] www.BabsonCapital.com

Bank of America Merrill LynchMerrill Lynch, Pierce, Fenner & Smith IncorporatedOne Bryant ParkNY1-100-03-01New York, NY 10036Contact: Wynne ComerManaging DirectorTel. [email protected]

Credit Suisse Asset Management11 Madison Ave.New York, NY 10010Contact: John G. PoppManaging DirectorTel. [email protected]

Prudential Fixed Income 100 Mulberry Street Gateway Center II , 4th Floor Newark, NJ 07102 Contact: Miguel Thames Managing Director, Head of U.S. Sales and Global Consultant Relations Tel. 973-367-9203 [email protected] www.prudential.com

Loans Move to Center Stage

4

Senior Secured Loans: The Primary, The Secondary

and through the Cycle

8

Investing in Senior Secured Loans

12

SPONSOR DIRECTORY

The Loan Syndications and Trading Association - LSTA366 Madison Avenue, 15th FloorNew York, NY 10017Contact: Alicia SansoneExecutive Vice PresidentTel. [email protected]

CONTENTS

pi supp.qxp 5/9/11 10:04 AM Page 2

he long-awaited “discovery” of the floating-rate, seniorsecured loan asset class by traditional investors seems tobe finally taking place. Of course, it is not as if this huge$1.5 trillion dollar asset class had been hiding in theshadows. But “pre-Crash” loan buyers were concentratedamong relatively specialized investors, like traditionalcommercial bank lenders, “prime rate” loan mutualfunds, sophisticated hedge funds, and – especially– a unique form of securitized vehicle called a “collater-alized loan obligation” (CLO).

In recent months more traditional investors, both re-tail and institutional, have been showing interest inloans. What’s more, after years of regarding loans as an “al-ternative” investment to be dabbled in opportunistically oras a “fringe” holding outside of one’s core investments instocks and bonds, many institutions and the consultantswho advise them have begun to view loans as a worthymainstream asset class.

One effect of the great financial crash of 2007-2009was to test financial and investment strategies. Whilemany strategies came up wanting, one that clearly didnot was investing in senior secured corporate loans and insecuritized vehicles comprised of such loans. As in-vestors – both retail and institutional – now review theirtraditional asset allocation strategies in the light of such“post-Crash” realities, many of them have decidedthat loans, an asset providing stable, well-protectedcash-flow with a built-in hedge against rising interestrates and inflation, deserve a permanent position in theirportfolio allocations.

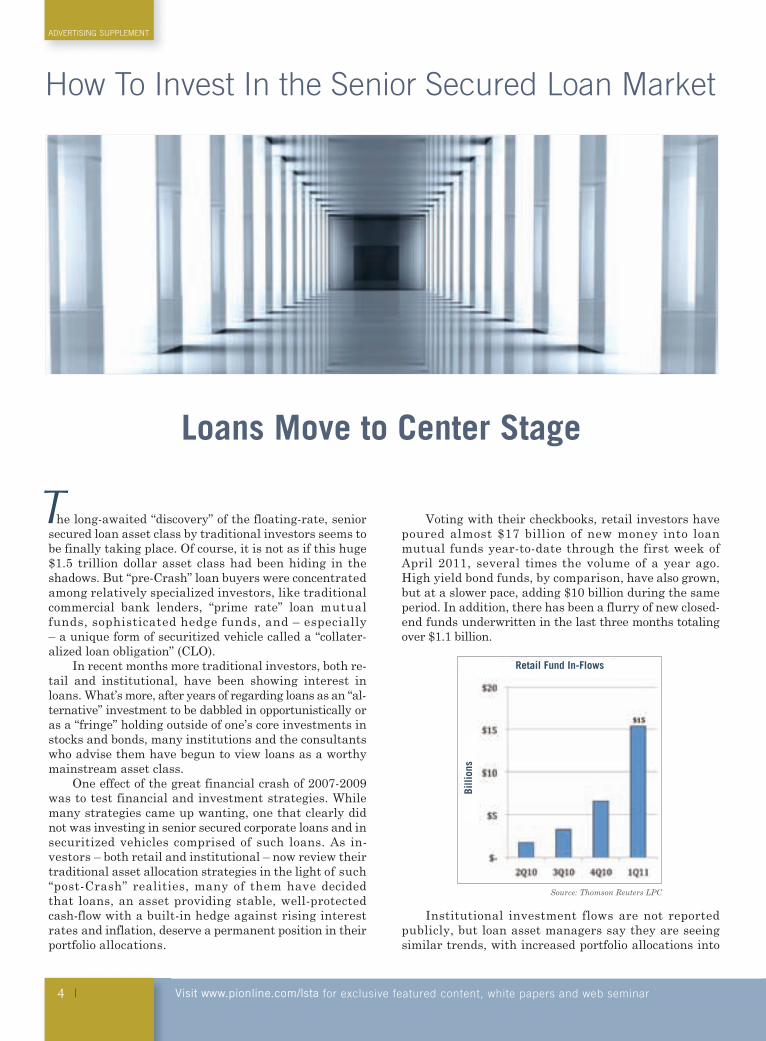

Voting with their checkbooks, retail investors havepoured almost $17 billion of new money into loanmutual funds year-to-date through the first week ofApril 2011, several times the volume of a year ago.High yield bond funds, by comparison, have also grown,but at a slower pace, adding $10 billion during the sameperiod. In addition, there has been a flurry of new closed-end funds underwritten in the last three months totalingover $1.1 billion.

Institutional investment flows are not reportedpublicly, but loan asset managers say they are seeingsimilar trends, with increased portfolio allocations into

4

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

How To Invest In the Senior Secured Loan Market

Loans Move to Center Stage

TBi

llion

s

Retail Fund In-Flows

Source: Thomson Reuters LPC

pi supp.qxp 5/9/11 10:04 AM Page 3

loans and away from traditional bonds and equities bypensions, endowments and other mainstream investmentgroups.

“Most of the money we’re raising is institutional,”said John Popp, Managing Director and Head of theCredit Investments Group at Credit Suisse Asset Man-agement. Marketing the loan asset class to pensions, en-dowments and other institutions also means reaching outto the consultants who advise these groups in their choiceof strategy, asset class selection and allocation, and theirpick of portfolio managers. “This is the first time we’veseen such broad interest in the loan asset class from con-sultants.”

But whatever order it’s happening in, there seems tobe no doubt that loans are now on the institutionalinvestment community’s radar scope. Most loan profes-sionals welcome the arrival of the major investment players– pensions, endowment funds, insurance companies –to the floating-rate loan market. “It’s a good thing for theloan market to have a more diverse investor base,” said Popp.

What goes without saying by most loan originatorsand investors – but is on many of their minds – is howvulnerable many in the market felt during the depths ofthe crash, or “great deleveraging” as some in the loanmarket called it, to have had so much of the pre-crashloan market demand dependent on specialized investorsand investment vehicles that were leveraged and subjectto margin calls of one sort or another. Of course, the goodnews is that cash flow based loan vehicles and their un-derlying loans performed well through the crash andrichly rewarded the faith and patience of those who heldthem through the duration of the crisis. But the other les-son is that there probably would have been fewer sleep-less nights and a lot less angst if the loan market investorbase had been even broader and included more tradi-tional institutional investors, as it appears it surely willgoing forward.

Ironically, it was the financial crash and thebargain-basement opportunities it presented for “bot-tom fishing” among investments whose market priceshad been driven to unrealistically low prices throughmargin-call induced selling, that first brought loans tothe attention of many traditional and non-traditionalinstitutional investors.

Prices on healthy, performing loans dropped – in linewith drops in equity and high yield bond prices – to whatnow appear in retrospect to have been irrationally absurdlevels of about 60 cents on the dollar. These prices seemedirresistible to some investors, like hedge funds and privateequity firms, who were among the first major buyers tore-enter the market. They were followed shortly there-after by major institutional buyers, like pensions,endowment funds and insurance companies.

“While retail investor interest has grown recently,institutional investors re-entered the loan market over ayear ago,” said Joe Lemanowicz, head of US Bank Loanportfolio management at Prudential Financial. “PensionFunds that began investing in loans in 2009 and early2010 captured some of the price recovery,” he added. Re-tail investors, coming in currently, will still get a couponreturn – 4.5 to 5% – that is attractive relative to bothother fixed income asset classes and historical loanreturns, Lemanowicz went on to explain.

“Post-Crash” realitiesWhat are these “post-Crash” realities that are sparkingsuch a review of time-honored investment philosophies?One is the widespread awareness that thirty years offalling interest rates provided a “wind at the back” to thefixed income market that can hardly repeat itself in thefuture, given how low rates currently are and theprospect of public deficits and debt as far as the eye cansee conspiring to push interest and inflation rates in anupward direction. The other reality is an economic recoverythat may be tepid at best, dependent as it is on risingdemand from a consumer base that is both weary andcautious after its recent economic and investmentexperience.

As a result of this, many investment professionalsanticipate a future that has been described as the “newnormal” by Pimco’s Bill Gross, an era of reducedexpectations for investment returns, with targeted per-formance in the mid to high single digits. Such an envi-ronment may be perfect for the senior secured loan assetclass, with its “steady Eddie” returns in the mid single-digits, and floating rates that will actually benefit fromthe eventual rise in interest rates.

Many experts also expect high yield bonds to dorelatively well in a rising interest rate environment, comparedto investment grade and government bonds. Treasurybonds have virtually no credit risk, given that the issuercan pay them off with money it is able to create itself, andhigh grade corporates have relatively little credit risk,compared to high yield. This means an investor in eitherof them is being paid mostly to take interest rate risk asopposed to credit risk, if one were to allocate the couponbetween the two risks. Because high yield bonds involveconsiderably more credit risk (empirical data shows highyield companies default at a rate several times that of in-vestment grade firms), and have less interest rate riskbecause of their generally shorter terms, the high yieldbond coupon – if one were to allocate it between the returnfor taking credit risk versus the return for taking inter-est rate risk – would skew far more to the credit risk side.

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

ADVERTISING SUPPLEMENT

5

Average Secondary Loan Market Bid

continued on page 6Source: S&P/LSTA LLI

pric

e

pi supp.qxp 5/9/11 10:04 AM Page 4

6

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

The extra spread on high yield bonds “will absorbsome of the potential decline in prices if interest ratesrise,” said Prudential’s Lemanowicz. Even within highyield bonds, the impact will be uneven, he added, pointingout that if the economy remains on sound footing, the lowerrated high yield bonds – say, single-B and below – will holdup better if rates rise because they currently have thickercredit spreads. “Double-Bs may actually behave more likeinvestment grade when rates rise,” he said.

So the question for many institutional investors iswhether to split their high yield debt allocation betweenbonds and loans and – if so – in what proportion. Thechoice, as expressed by several high yield debt managers,is between (1) loans where you can earn 4.5-5%, incur nointerest rate risk, enjoy upside protection if rates go up,and have a senior secured position if credit problemsarise, and (2) high yield bonds where you can earn about7%, but have the risk of capital losses if rates go up anda junior position with consequent greater credit losses.

How will investors address this question? Pre-crash,before loans were on the radar scopes of many asset man-agers, most investors probably would have stuck withtheir high yield allocations, perhaps shortened maturi-ties somewhat and just endured the impact of higherrates as best they could. This time around, with loans aviable, respectable alternative, market observers expectto see many more investors creating a formal sub-alloca-tion “bucket” for loans within their fixed income allocation.

“We’re still early in the movement of traditionalinvestors into the loan asset class, said Russ Morrison,Head of High Yield Investments at Babson CapitalManagement LLC. “For most pensions, endowments,family office investment firms, they’re not there yet, interms of making loans a permanent investment cate-gory,” he said, “but most of them are thinking about it,and a few have made the move.”

Institutional investors’ motivations for entering thefloating rate loan arena are diverse. “For some it’s a fearof rising interest rates driving them to consider loans, butfor many it’s a diversification move,” said Morrison.“They see loans as an attractive asset class that theywere not previously involved in.”

Stability, predictability…and versatility!Those investors that have made the commitment to loansare able to consider a wide variety of investment vehiclesand structures, in determining what role loans can playin their portfolios. “Versatility” is a word that comes upoften in describing the possible ways that loans can be used.

“There is a whole spectrum of ways investors can getexposure to it,” said Prudential’s Joe Lemanowicz. Retailinvestors have a choice of over 70 traditional open-endmutual funds, as well as at least 22 closed-end funds, andone recently established loan ETF.

Straightforward “cash” investors, holding loansdirectly or through unleveraged mutual funds andcommingled vehicles, can probably expect to earn a

coupon yield of 4.5-5%, minus credit losses estimated tobe 1% or less (depending on the skill of the loan portfoliomanager and the vagaries of the economic cycle), alongwith enjoying the advantage of a floating-rate “hedge”against rising interest rates (i.e. if and/or when interestrates rise, the loan coupon will rise with them.)

Closed-end loan fund investors can often earn anextra 2-3% as a result of the limited leverage (up to 33%of total assets) closed-end funds are allowed to have perthe Investment Company Act of 1940 (“the ’40 Act”). Howmuch extra return they can generate depends on thespread between what they can borrow at and the aver-age return on their loan portfolio. A fund that can borrowat 1% and buy loans yielding 4.5%, can increase its re-turn to shareholders by the difference (3%, minus certainexpenses) times the percent of its net equity that it bor-rows. Since the maximum is 50% of debt to equity inorder to stay within the 33% of total assets limit, in thisexample the maximum boost to per share yield would be1.5% (i.e. 50% of 3%).

Institutional investors have the above options andmore as they work with their investment consultantsand managers to structure tailored vehicles to suittheir risk/reward comfort levels and strategic returnobjectives. Those that view loans as an essential part oftheir fixed income allocation may see a stable return of4.5-5%, with no interest rate downside and an upsideyield pick-up when rates increase, as relatively quiteattractive on a purely unleveraged basis when com-pared to the projected performance of traditional gov-ernment, investment grade and even high yield bondsin a long-term rising rate scenario. Others may wish touse loans, with their stable cash flows and senior, se-cured position in the borrower’s capital structure, asbuilding blocks to create more aggressive risk/rewardinvestment structures.

“Prudently structured loan vehicles can be an idealinvestment for investors seeking stable low to mid-teensreturns,” said Wynne Comer, Managing Director andHead of CLO Structuring at Bank of America MerrillLynch. By adding specific degrees of leverage, an investorcan target various levels of risk/reward in order toachieve a range of returns from straight fixed incomethrough “equity income” to a full equity return.

Every one-time “turn” of leverage increases the in-vestor’s return by the difference between the cost of theleverage funding and the return on the additional loan as-sets acquired, minus any expenses, fees and credit losseson the incremental loans. For example, let us assume aninvestor can leverage itself at an incremental interest rateof 1.5% and purchase loans yielding 4.5 %. If the creditcost and other expenses are 1%, then the net yield pick-upfor every one-time turn of leverage will be 2%. Of coursethere are diminishing returns for every additional one-timeturn of leverage, since the credit risk increases for everytime you leverage the same equity, and the incrementalcost of additional leverage rises accordingly. �

continued from page 5

pi supp.qxp 5/9/11 10:04 AM Page 5

“ Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp., all of which are registered broker dealers and members of FINRA and SIPC, and, in other jurisdictions, by locally registered entities. Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured May Lose Value Are Not Bank Guaranteed. ©2011 Bank of America Corporation.

Covering leveraged loans

from start to finish.

Bank of America Merrill Lynch is a leader in all aspects of the leveraged loan product,

driving execution in both primary and secondary loan sales as well as new issue

and secondary trading for CLOs, winning International Financing Review’s highly

prestigious Global Loan House of the Year award in 2010. Across the spectrum

of investment alternatives in the loan asset class, Bank of America Merrill Lynch

is the partner of choice.

11pi0177.pdf RunDate:05/16/11 PI LSTA Suppl Full Page Color: 4/C

11pi0177.qxp 5/9/11 10:34 AM Page 1

nly in the past two decades, as floating rate corporateloans have migrated off the books of commercial banksand into the portfolios of non-bank investors, have fixedincome buyers been able to purchase a pure corporatecredit instrument, one that unbundled the credit bet fromthe interest rate bet.

Sitting at the very top of the capital structure withgenerally a first lien collateral security interest in most orall of the assets of the issuer, loan holders get theirinterest and principal paid first in the event of bank-ruptcy, ahead of bondholders and other unsecured creditors.

But unlike bondholders, loan investors are protected bycovenants, which are contractual restrictions on theborrower’s taking certain specified actions that woulddiminish its credit prospects during the term of the loan.Also included are financial maintenance covenants thatthe borrower must meet on a continuing basis, or else ei-ther renegotiate fees, spreads or other terms to the sat-isfaction of the lenders or otherwise repay the loan. Thisgives a loan investor much more control over the creditthan a typical high yield bondholder would have, even iflending to the same issuer.

Due to the additional credit protection, loan investorshave consistently recovered a substantially higher percentageof their debt outstanding in the event of default than havebondholders. As a result, credit losses on loan portfoliostypically amount to less than half the losses on high yieldbond portfolios with issuers of equivalent credit quality.

Besides loans representing a better protected creditrisk than high yield bonds, they also represent an in-vestment in “pure” credit risk. This means, simply, thatloan coupons are paid at a floating rate, adjusted usuallyevery three months at a spread over LIBOR. As a result,they carry virtually no duration, or interest rate risk. Afixed rate bond’s market value goes up and down withmovements in interest rates, precisely because its incomestream is fixed. Since a loan’s actual coupon rate and in-come stream are flexible and adjust as interest ratesmove up and down, the value of the loan itself does nothave to. This means loan assets are likely to have a more

O

8

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

Senior Secured LoansThe Primary, The Secondary and

through the Cycle

Source Babson Capital Management LLC

Position of Loans in Captital Structure

pi supp.qxp 5/9/11 10:04 AM Page 6

stable value, for mark-to-market investors, than fixedrate bonds whose price must be marked up and down asinterest rates fluctuate. Of course loans may still undergonon-interest rate-related pricing moves, most likely dueto changes in credit quality and market risk appetites.

One attractive feature that has been added to theloan market in recent years, as short-term market interestrates, including LIBOR, have become almost negligible, isthe “LIBOR floor.” Nearly every new loan issued in re-cent years has a minimum base rate (irrespective of whatthe actual 3-month LIBOR is) in a typical range of 1.00%to 1.50%. This has made the bond/loan trade-off an eas-ier decision for investors who appreciated the protectionagainst interest rate rises that loans afford, but balked atthe opportunity cost of an asset based on a reference ratehovering close to zero. LIBOR floors provide a "have yourcake and eat it too" quality in that they significantly boostloan spreads in the short term, while the floating rate na-ture of the loan instrument still kicks in once rates ex-ceed the LIBOR floor, providing a long-term hedgeagainst inflation and soaring interest rates.

Having a “pure” non-duration-laden corporate creditinstrument available is a radical change and uniqueopportunity for most institutional investors. Many fixed-income investors are so accustomed to buying fixed in-

come instruments (i.e. bonds) that have interest ratebets integrally attached to them, that they may not al-ways fully appreciate how much they are being paid totake credit risk and to take interest rate risk, respec-tively. Yet it is relatively easy to calculate the interestrate bet premium for a bond of any maturity by lookingat the difference between the short-term T-bill rate andthe risk-free Treasury note or bond rate for that samematurity. Using today’s Treasury yield curve we see thatthe interest rate bet premium on a typical 5 to 8 year highyield bond would be 2 to 3%, which would probably leaveabout 4.5-5% of the coupon to reimburse the investor forthe issuer’s credit risk. A loan to an equivalent loan is-suer would likely pay a coupon in the 4.5-5% range, withno interest rate bet, and none of the volatility associatedwith interest rate movements.

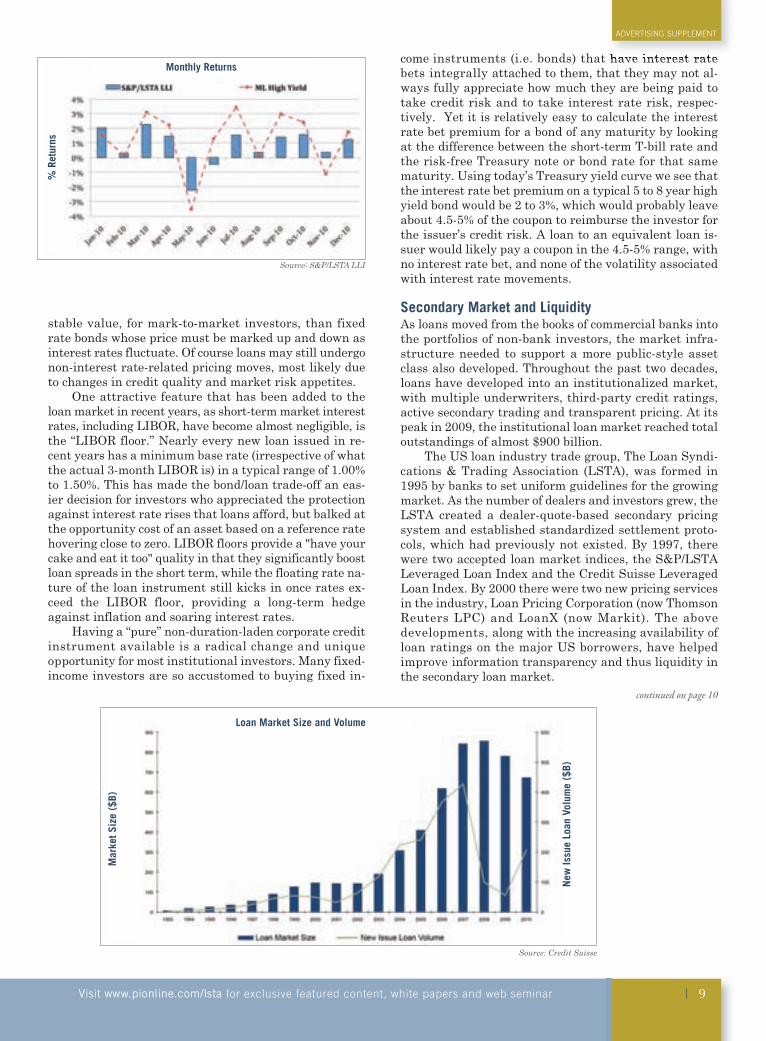

Secondary Market and LiquidityAs loans moved from the books of commercial banks intothe portfolios of non-bank investors, the market infra-structure needed to support a more public-style assetclass also developed. Throughout the past two decades,loans have developed into an institutionalized market,with multiple underwriters, third-party credit ratings,active secondary trading and transparent pricing. At itspeak in 2009, the institutional loan market reached totaloutstandings of almost $900 billion.

The US loan industry trade group, The Loan Syndi-cations & Trading Association (LSTA), was formed in1995 by banks to set uniform guidelines for the growingmarket. As the number of dealers and investors grew, theLSTA created a dealer-quote-based secondary pricingsystem and established standardized settlement proto-cols, which had previously not existed. By 1997, therewere two accepted loan market indices, the S&P/LSTALeveraged Loan Index and the Credit Suisse LeveragedLoan Index. By 2000 there were two new pricing servicesin the industry, Loan Pricing Corporation (now ThomsonReuters LPC) and LoanX (now Markit). The abovedevelopments, along with the increasing availability ofloan ratings on the major US borrowers, have helpedimprove information transparency and thus liquidity inthe secondary loan market.

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

ADVERTISING SUPPLEMENT

9

Monthly Returns

Source: S&P/LSTA LLI

Source: Credit Suisse

Mar

ket S

ize

($B)

New

Issu

e Lo

an V

olum

e ($

B)

continued on page 10

Loan Market Size and Volume

% R

etur

ns

pi supp.qxp 5/9/11 10:04 AM Page 7

10

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

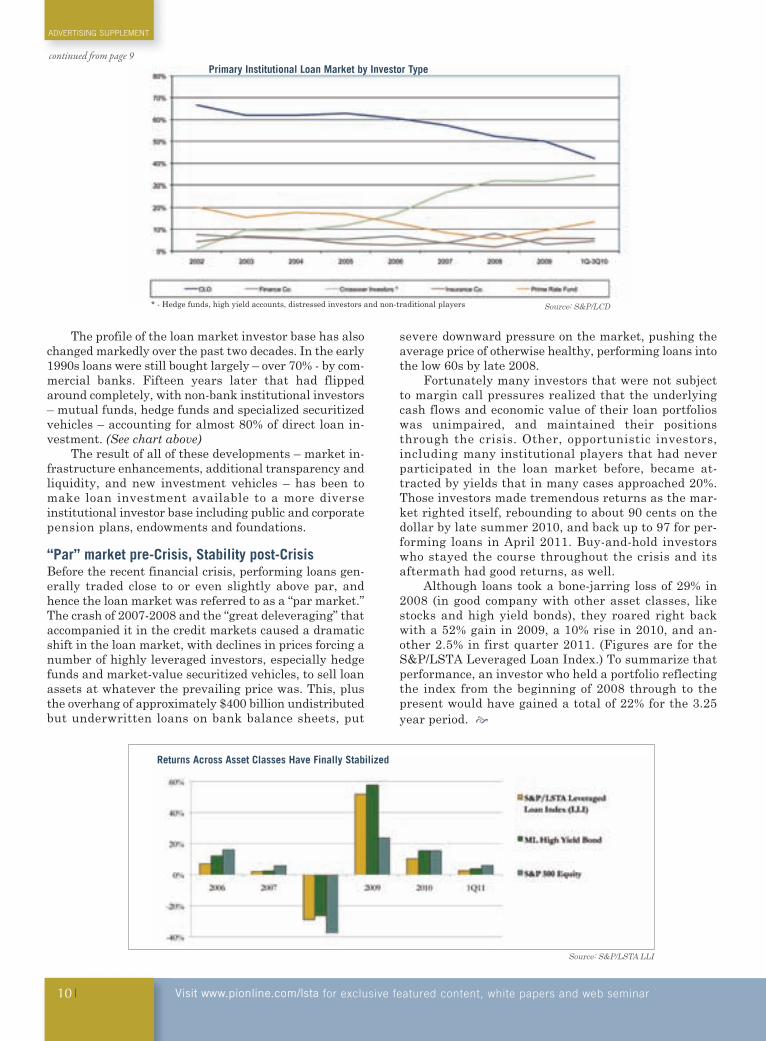

The profile of the loan market investor base has alsochanged markedly over the past two decades. In the early1990s loans were still bought largely – over 70% - by com-mercial banks. Fifteen years later that had flippedaround completely, with non-bank institutional investors– mutual funds, hedge funds and specialized securitizedvehicles – accounting for almost 80% of direct loan in-vestment. (See chart above)

The result of all of these developments – market in-frastructure enhancements, additional transparency andliquidity, and new investment vehicles – has been tomake loan investment available to a more diverseinstitutional investor base including public and corporatepension plans, endowments and foundations.

“Par” market pre-Crisis, Stability post-CrisisBefore the recent financial crisis, performing loans gen-erally traded close to or even slightly above par, andhence the loan market was referred to as a “par market.”The crash of 2007-2008 and the “great deleveraging” thataccompanied it in the credit markets caused a dramaticshift in the loan market, with declines in prices forcing anumber of highly leveraged investors, especially hedgefunds and market-value securitized vehicles, to sell loanassets at whatever the prevailing price was. This, plusthe overhang of approximately $400 billion undistributedbut underwritten loans on bank balance sheets, put

severe downward pressure on the market, pushing theaverage price of otherwise healthy, performing loans intothe low 60s by late 2008.

Fortunately many investors that were not subjectto margin call pressures realized that the underlyingcash flows and economic value of their loan portfolioswas unimpaired, and maintained their positionsthrough the crisis. Other, opportunistic investors,including many institutional players that had neverparticipated in the loan market before, became at-tracted by yields that in many cases approached 20%.Those investors made tremendous returns as the mar-ket righted itself, rebounding to about 90 cents on thedollar by late summer 2010, and back up to 97 for per-forming loans in April 2011. Buy-and-hold investorswho stayed the course throughout the crisis and itsaftermath had good returns, as well.

Although loans took a bone-jarring loss of 29% in2008 (in good company with other asset classes, likestocks and high yield bonds), they roared right backwith a 52% gain in 2009, a 10% rise in 2010, and an-other 2.5% in first quarter 2011. (Figures are for theS&P/LSTA Leveraged Loan Index.) To summarize thatperformance, an investor who held a portfolio reflectingthe index from the beginning of 2008 through to thepresent would have gained a total of 22% for the 3.25year period. �

Source: S&P/LSTA LLI

Returns Across Asset Classes Have Finally Stabilized

* - Hedge funds, high yield accounts, distressed investors and non-traditional players

Primary Institutional Loan Market by Investor Type

Source: S&P/LCD

continued from page 9

pi supp.qxp 5/9/11 10:04 AM Page 8

credit-suisse.com

11pi0178.pdf RunDate:05/16/11 PI LSTA Suppl Full Page Color: 4/C

11pi0178.qxp 5/6/11 1:10 PM Page 1

12

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

any of the new investors – institutions like pensions,endowment funds, foundations – that were enticed intothe market toward the end of the crisis by the bargainprices still to be had on healthy, performing assets, arenow assessing whether they want to stay in the marketon a more lasting basis. Market professionals are hopingthat many of these opportunistic buyers will decide to belong-term permanent loan investors.

Credit Suisse’s John Popp thinks many of them will.Popp believes the loan market is currently “reconstitutingdemand,” as it replaces more specialized and leveragedbuyers with more traditional and non-leveraged in-vestors. “It’s a three phase process, where phase 1 wascommercial banks syndicating to other banks, phase 2was broadening the investor base to specialized non-bankloan buyers, and now we are in phase 3 where the loanasset class is finally being accepted by traditional insti-tutional buyers,” he explained. The institutional in-vestors are entering the market at a good time, Poppbelieves, because “loan spreads are still cheap compared tohistorical spreads.” He also said that “many institutions areconcerned about duration management in their fixedincome portfolios” right now, which makes floating rateloans an attractive option.

As mentioned earlier, loans are a versatile assetclass offering investors a wide variety of vehicles for in-vesting in it. From the simplest to the most complex, aninvestor’s primary options are:

• Retail open-end mutual funds• Retail closed-end mutual funds• Institutional commingled funds• Institutional separate managed accounts• Securitized vehicles (e.g. collateralized loan obligations)

Retail open-end mutual funds have grown rapidly inrecent years and now total over 70. Their main advan-tage is the convenience of daily liquidity at the net assetvalue of the underlying assets. Of course, you pay a pricefor that liquidity in that the fund manager mustprudently maintain cash of 10% or so to ensure immedi-ate access to funds in the event of investor with-drawals. Recent returns have been in the 6-7% range.

Closed-end loan funds differ from open-end funds inthat there is a fixed number of shares that are under-written and sold to investors. Future investors must purchaseshares on the open market from existing investors, justas one would buy shares in other publicly traded compa-nies. This means that the publicly quoted price of theshares may diverge from the underlying net asset value(NAV) of the shares, as market supply and demand forcesdrive the public price up and down. This can be an ad-vantage or a disadvantage, depending on an investor’sinvesting goals and sensitivity to market price volatility.Unlike open-end funds, closed-end funds trade in the sec-ondary market and are often subject to premiums or dis-counts to NAV. For long term investors that want tomaximize return, having the opportunity to follow theshare price and buy in when the market price is at a dis-count to NAV is a distinct advantage and provides aslight yield pickup to the yield calculated on the NAV.

Closed-end funds have another advantage in that, asdescribed above, pursuant to the Investment CompanyAct of 1940 they are allowed to leverage themselves byborrowing up to one-third the asset value of the fund (i.e.equity, at any time, must be twice the amount of totaldebt). The extra leverage can add to the potential return,which is why leveraged closed-end fund returns have

Investing in Senior Secured Loans

M

pi supp.qxp 5/9/11 10:04 AM Page 9

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

ADVERTISING SUPPLEMENT

13

tended to range as high as the 8-9% range, as opposed tothe 6-7% range for unleveraged open-end funds.

In the case of both open-end and closed-end loanfunds, portfolio manager experience and credit analyticalskill are critical factors. In loan investing, making andkeeping the coupon depends on keeping credit lossesminimal. Earning more than the coupon typically de-pends on a manager picking loans in the secondary mar-ket that are selling below par, and pocketing the discountas they pay off at 100%. Whether future returns willmatch those of the past is always a difficult question, al-though Prudential’s Joe Lemanowicz is estimating 2011returns, for unleveraged buyers, in the 6-7% range, whichis close to pre-Crash returns. “Although spreads havenarrowed in recent months, the loan market is still some-what cheap from a historical perspective,” he added.

Besides loan mutual funds, an exchange-traded fund(ETF) – Invesco PowerShares Senior Loan Portfolio(BKLN) – was launched in March 2011 and designed toreplicate the performance of the S&P/LSTA U.S. LeveragedLoan 100 Index, which tracks the 100 largest and mostwidely traded loans in the US market. As an exchange-traded fund, BKLN provides investors the opportunity tomove in and out of the asset class during the trading day.It is unleveraged, although investors can provide theirown leverage through the use of margin, if they wish. Al-though it is too new to have a track record, if returnstrack the index, then they should reflect the coupons ofthe underlying assets plus any capital gains from pick-ing up the discounts on non-par traded loans that pay offin full. Missing from an index product like this is anyadded value from the portfolio manager’s credit andanalytical judgment, like you would have in a traditionalopen-end or closed-end fund.

More options for institutional accounts“Historically, there was not a lot of direct investment

in the loan market by institutions,” said Babson Capital’sRuss Morrison. “What there was,” he explained, “was

mostly in CLOs and total return swaps, which theinvestors regarded as ‘alternative investments.’ Now,”Morrison said, “there is a broad universe of potential di-rect loan investors.”

Today, as institutional investors consider how tomake loans more of a core holding, they have manyoptions – far more than retail investors – in terms ofinvestment vehicles. Some are geared for the straightcash fixed-income buyer, with the lowest return expectationsand the lowest risk, while others are more leveraged.

One option is a “commingled fund,” where theirfunds are combined with other investors in a limitedpartnership structure, and managed together in a pool,like an exclusive, privately managed mutual fund. Theminimum institutional investment for commingled fundsis generally about $1 million, and some funds are mod-estly leveraged (up to approximately 1.5 times). The com-mingled fund route would likely be taken by a smallinstitution, or by larger investors that are new to loansand want to “test the waters” first before committing amore substantial amount. Commingled fund investors,depending on the degree to which their funds use leverage,have been able to achieve a similar range of returns – 6to 7% unleveraged, 8 to 9% leveraged – as retail fund in-vestors. Achieving that will probably involve earning acoupon of about 5%, with some additional yield pickup onloans bought at discounts that pay off at par.

An institutional investor with more to invest (mini-mum commitment typically $75-$100 million) and/ormore experience with the asset class might opt for a sep-arately managed account. This allows for a more tailoredinvestment strategy, and possibly greater leverage, al-though still most likely limited to 2-3 times in a sepa-rately managed account. (Investors wanting moreleverage will probably turn to CLOs; see below.) Sepa-rate accounts tend to be used by sophisticated investorswho want to control the quality, industry and concentra-tion of their exposure. Working closely with their invest-ment managers, they can set specific parameters toclosely match their risk appetite and return targets.This might mean targeting above or below the return tar-gets of retail and commingled clients.

CLOs, like all securitized vehicles, are bankruptcy-remote vehicles that own income-earning assets (in thiscase loans), and finance themselves by issuing multi-level tranches of debt, plus equity. If structured appro-priately, the senior debt tranches, which are the last toabsorb losses from any asset shrinkage, are protectedbeyond the level required to withstand highly stressedcredit scenarios, and get very high credit ratings. Suc-cessively junior debt tranches are designed to absorblosses prior to the senior tranches above them, andhave credit ratings (and coupon rates) to reflect that.The CLO’s equity, of course, is the first in line to ab-sorb losses, and would have to be eliminated completelybefore the debt tranches are affected.

A typical CLO holds anywhere from 100 separateloans, each one rated by a major rating agency and withcredit information readily available to the CLO investors.They are relatively simple and transparent structures,

Loan Spreads Rally From Crisis Levels and Remain Elevated

continued on page 14

pi supp.qxp 5/9/11 10:04 AM Page 10

14

ADVERTISING SUPPLEMENT

Visit www.pionline.com/lsta for exclusive featured content, white papers and web seminar

on which any reasonably professional investor could doadequate due diligence.

CLOs that were designed around the cash flows ofthe underlying loan assets, and were therefore indifferentto the market gyrations around the theoretical prices ofthose assets, performed well through the crash. “CLOstructures did what they were supposed to do in terms ofprotecting investors by deleveraging during times ofstress,” said Bank of America’s Wynne Comer. “Ingeneral, we believe that average equity returns acrossthe market for outstanding CLOs will be in the low dou-ble digits,” said Prudential's Joe Lemanowicz.

The fact that CLOs have a similar name and legalstructure to the sub-prime-mortgage-backed collateral-ized debt obligations (CDOs), whose demise is widelycredited with precipitating the debt crisis, has not been ahelpful marketing feature over the past several years.“One important difference,” Wynne Comer pointed out,“is that CLOs are ‘first level securitizations,’ that directlyhold the underlying reference assets.” In other words,CLOs actually own the 100 or more loans on whose fortunesthey and their creditors are dependent for repayment. Theinfamous CDOs did not actually own the underlyingmortgages on whose financial health they had so muchat stake. What they owned were liabilities (tranches) ofother securitizations, usually mortgage-backed securi-ties, which in turn owned the mortgages. In many cases,the CDOs were a further step removed, and actuallyowned pieces of other CDOs that in turn owned theliabilities of the mortgage-backed securities that ownedthe underlying mortgages. That made due diligence onCDOs challenging, to say the least. The rest is history.

Today’s CLOs are more conservatively structuredthan pre-crash CLOs. Today’s CLOs are leveraged 8 to10 times, versus the previous CLOs’ leverage of 11 to 12times. Equity today would be 10-12% of the capitalstructure, while before it was 7 or 8%. The expected re-turn target still averages in the low to mid-teens, de-pending on credit performance, funding costs and othervariables, but the variability around that return is ex-pected to be much less. And the tenor – previously 14years, has been reduced to about 11 years, with the run-off period starting after only 2-3 years, rather than 6-7in the earlier models. So there is more capital and CLOmanagers are on a shorter leash. All this should be reas-suring to investors and potential investors in CLOs, sincethe old models worked pretty well through the worstcrash in 70 years, and now the structures are eventighter.

While 8 to 10 times leverage may seem high to someinvestors, loan professionals are quick to point out thatall the CLO vehicles now being created are closed-end,cash-flow oriented instruments designed to be immuneto market price movements of the underlying loans. Inother words, as long as the loans continue to performand pay off as scheduled (with generous allowance fordefaults factored into the structure), price movementsare largely irrelevant and will not derail the investmentperformance.

Having proven themselves through the crash, are

CLOs now ready for “prime time” as an “equity replace-ment” vehicle for pensions and other long term investorslooking for consistent, predictable returns in the low dou-ble digits? Many traditional equity buyers seemprepared, in our “new normal” investing environment,to accept high single digits/low double digits as their newstandard. Bankers are hopeful. “CLO equity is theoptimal investment vehicle for long-term investors seek-ing consistent performance,” said Bank of America’sWynne Comer. “It provides equity-like returns while itsrisk is based on senior secured loans at the top of thecorporate capital structure.”

Will investors accept the idea that floating rate,senior secured loans “at the top of the capital struc-ture,” prudently leveraged, can offer a less volatile risk-adjusted likelihood of achieving an “equity return” thanbuying “real” equity? That is the proposition that loanmarket proponents are now out to demonstrate to thelarger investment community. �

Today, as institutional investors

consider how to make loans

more of a core holding,

they have manyoptions – far more than

retail investors – in terms of

investment vehicles.

continued from page 13

pi supp.qxp 5/9/11 10:04 AM Page 11

PRU KNOWSCREDIT.

© 2011. All data as of 12/31/10. Prudential Fixed Income is a unit of Prudential Investment Management, Inc., a registered investment adviser and a Prudential Financialcompany. Prudential Financial and the Rock logo are registered service marks of The Prudential Insurance Company of America and its affiliates.2011-0631

Find out how the research-driven strategies ofPrudential Fixed Income can make a differencefor your portfolio. You’ll also benefit from:

STRONG CREDIT ORIENTATION: $270 billion undermanagement, with $182 billion credit-related

LEVERAGED FINANCE EXPERTISE: more than$22 billion under management

GLOBAL INTEGRATION: more than 175 investmentprofessionals in the US, Europe and Asia

SOPHISTICATED RISK MANAGEMENT: risk budgeting,attribution and valuation models

BREADTH OF INVESTMENT SOLUTIONS: traditional,long-duration and alternative

To learn more, please contact Miguel Thames,Head of US Sales and Global ConsultantRelations, at 973-367-9203.

Download our recent publication,Questions You Should Be Asking AboutSenior Secured Loans atwww.prudentialfixedincome.com

PRUDENTIAL FIXED INCOME

11pi0179.pdf RunDate:05/16/11 PI LSTA Suppl Full Page Color: 4/C

11pi0179.qxp 5/6/11 1:16 PM Page 1

11pi0031.pdf RunDate:05/16/11 PI LSTA Suppl Full Page Color: 4/C

11pi0031.qxp 5/6/11 1:13 PM Page 1