How Royal Dutch/Shell Scenarios: developed a planning ... · PDF file10.02.1972 ·...

18

73 How Royal Dutch/Shell developed a planning technique that teaches managers to think about an uncertain future Scenarios: uncharted waters ahead Pierre Wack It i.s fashionable to downplay and even denigrate the usefulness of economic forecasting. The rea- son is obvious: forecasters seem to be more often wrong than right. Yet most U.S. companies continue to use a vari- ety of forecasting techniques because no one has appar- ently developed a better way to deal with the future's eco- nomic uncertainty Still, there are exceptions, like Royal Dutch/Shell. Beginning in the late 1960s and early 1970s, Shell developed a technique known as "scenario plan- ning." By listening to planners' analysis of the global busi- ness environment. Shell's management was prepared for the eventuality-if not the timing-of the 1973 oil crisis. And again in 1981, when other oil companies stockpiled re- serves in the aftermath of the outbreak of the Iran-Iraq war. Shell sold off its excess before the glut became a real- ity and prices collapsed. Undoubtedly, many readers believe they are familiar with scenarios. But the decision scenarios de- veloped by Shell in Europe are a far cry from their usual U.S. counterparts. In this article and a sequel to come, the author describes their evolution and ultimate impact on Shell's management. Mr. Wack is retired head of the business en- vironment division of the Royal Dutch/Shell Group plan- ning department, which he directed during the turbulent decade from 1971 to 1981. Wack, an economist, developed with Edward Newland the Shell system of scenario plan- ning. He now consults and participates in scenario devel- opment with management teams around the world. In 1983 and 1984, he was senior lecturer in scenario planning at the Harvard Business School. Illustration by Tbm Briggs, Omnigraphics, inc. Few companies today would say they are happy with the way they plan for an increasingly fluid and turbulent business environment. Traditional planning was based on forecasts, which worked reason- ably well in the relatively stable 1950s and 1960s. Since the early 1970s, however, forecasting errors have be- come more frequent and occasionally of dramatic and unprecedented magnitude. Forecasts are not always wrong; more often than not, they can be reasonably accurate. And that is what makes them so dangerous. They are usu- ally constructed on the assumption that tomorrow's world will be much like today's. They often work be- cause the world does not always change. But sooner or later forecasts will fail when they are needed most: in anticipating major shifts in the business environ- ment that make whole strategies obsolete |see the in- sert, "Wrong When It Hurts Most"). Most managers know from experience how inaccurate forecasts can be. On this point, there is probably a large consensus. My thesis-on which agreement may be less general-is this: the way to solve this problem is not to look for better forecasts by perfecting tech- niques or hiring more or better forecasters. Too many forces work against the possibility of getting the right forecast. The future is no longer stable; it has become a moving target. No single "right" projection can be deduced from past behavior. The better approach, I believe, is to accept uncertainty, try to understand it, and make it part of our reasoning. Uncertainty today is not just an occasional, temporary deviation from a reasonable pre- dictability; it ig a basic structural feature of the busi- ness environment. The method used to think about and plan for the future must be made appropriate to a changed business environment. Royal Dutch/Shell believes that deci- sion scenarios are such a method. As Shell's former

Transcript of How Royal Dutch/Shell Scenarios: developed a planning ... · PDF file10.02.1972 ·...

73

How Royal Dutch/Shelldeveloped a planning technique

that teaches managersto think aboutan uncertain future

Scenarios:uncharted waters

ahead

Pierre Wack

It i.s fashionable to downplay and evendenigrate the usefulness of economic forecasting. The rea-son is obvious: forecasters seem to be more often wrongthan right. Yet most U.S. companies continue to use a vari-ety of forecasting techniques because no one has appar-ently developed a better way to deal with the future's eco-nomic uncertainty

Still, there are exceptions, like RoyalDutch/Shell. Beginning in the late 1960s and early 1970s,Shell developed a technique known as "scenario plan-ning." By listening to planners' analysis of the global busi-ness environment. Shell's management was prepared forthe eventuality-if not the timing-of the 1973 oil crisis.And again in 1981, when other oil companies stockpiled re-serves in the aftermath of the outbreak of the Iran-Iraqwar. Shell sold off its excess before the glut became a real-ity and prices collapsed.

Undoubtedly, many readers believe theyare familiar with scenarios. But the decision scenarios de-veloped by Shell in Europe are a far cry from their usualU.S. counterparts. In this article and a sequel to come, theauthor describes their evolution and ultimate impact onShell's management.

Mr. Wack is retired head of the business en-vironment division of the Royal Dutch/Shell Group plan-ning department, which he directed during the turbulentdecade from 1971 to 1981. Wack, an economist, developedwith Edward Newland the Shell system of scenario plan-ning. He now consults and participates in scenario devel-opment with management teams around the world. In1983 and 1984, he was senior lecturer in scenario planningat the Harvard Business School.

Illustration by Tbm Briggs,Omnigraphics, inc.

Few companies today would say theyare happy with the way they plan for an increasinglyfluid and turbulent business environment. Traditionalplanning was based on forecasts, which worked reason-ably well in the relatively stable 1950s and 1960s. Sincethe early 1970s, however, forecasting errors have be-come more frequent and occasionally of dramatic andunprecedented magnitude.

Forecasts are not always wrong; moreoften than not, they can be reasonably accurate. Andthat is what makes them so dangerous. They are usu-ally constructed on the assumption that tomorrow'sworld will be much like today's. They often work be-cause the world does not always change. But sooner orlater forecasts will fail when they are needed most:in anticipating major shifts in the business environ-ment that make whole strategies obsolete |see the in-sert, "Wrong When It Hurts Most").

Most managers know from experiencehow inaccurate forecasts can be. On this point, there isprobably a large consensus.

My thesis-on which agreement maybe less general-is this: the way to solve this problemis not to look for better forecasts by perfecting tech-niques or hiring more or better forecasters. Too manyforces work against the possibility of getting the rightforecast. The future is no longer stable; it has becomea moving target. No single "right" projection can bededuced from past behavior.

The better approach, I believe, is toaccept uncertainty, try to understand it, and make itpart of our reasoning. Uncertainty today is not just anoccasional, temporary deviation from a reasonable pre-dictability; it ig a basic structural feature of the busi-ness environment. The method used to think aboutand plan for the future must be made appropriate to achanged business environment.

Royal Dutch/Shell believes that deci-sion scenarios are such a method. As Shell's former

74 Harvard Business Review September-October 1985

A note on namesThroughout this article, I use "Royal Dutch/Shell"and "Shell" to refer to the Royal Dutch/Shell groupof companies. The terms also serve as a conven-ient shorthand to describe the management andplanning functions within the central servicecompanies of that group in London and The Hague.I am generally excluding Shell Oil Company of theUnited States, which-as a majority-owned publiccompany- had undertaken its own operations plan-ning. I use words like "company" as a shorthand forwhat is a complex group of organizations with vary-ing degrees of self-sufficiency and operational inde-pendence. Most are obliged to plan for a future intheir own national economic and political environ-ments and to be integral parts of the Royal Dutch/Shell group of which they are members. I would notlike to mislead anyone into thinking that any singleperson, manager, or planner is able to have a clearviewof it all.

group managing director, Andre Benard, commented:"Experience has taught us that the scenario techniqueis much more conducive to forcing people to thinkabout the future than the forecasting techniques weformerly used."'

Many strategic planners may claim theyknow all ahout scenarios: they have tried but do notlike them. I would respond to their skepticism withtwo points:

D Most scenarios merely quantify alterna-tive outcomes of obvious uncertainties (for example,the price of oil may be $20 or $40 per barrel in 1995).Such scenarios are not helpful to decision makers. Wecall them "first-generation" scenarios. Shell's decisionscenarios are quite different, as we shall see.

• Even good scenarios are not enough. Tobe effective, they must involve top and middle manag-ers in understanding the changing business environ-ment more intimately than they would in the tradi-tional planning process. Scenarios help managersstructure uncertainty when (1) they are based on asound analysis of reality, and (2) they change the deci-sion makers' assumptions about how the worldworks and compel them to reorganize their mentalmodel of reality. This process entails much more thansimply designing good scenarios. A willingness to faceuncertainty and to understand the forges driving itrequires an almost revolutionary transformation in alarge organization. This transformation process is asimportant as the development of the scenariosthemselves.

My discussion will be in two parts. Inthis first article I will describe the development of sce-

narios in the early 1970s as they evolved out of themore traditional planning process. As you will see, theconcept and the technique we arrived at is very differ-ent from that with which we began-mainly becausethere were some highly instructive surprises along theway for all concerned. The art of scenarios is not mech-anistic but organic; whatever we had learned after onestep advanced us to the next.

In a forthcoming article, I will examinea short-term application of the technique and concludeby discussing key aspects that make the disciplinecreative.

The first steps

For ten years after World War II, Shellconcentrated on physical planning: the company hadto expand its production capacity and build tankers,depots, pipelines, and refineries. Its biggest challenge,like that of many companies, was to coordinate thescheduling of new facilities. Then from 1955 to 1965,financial considerations became more important butprimarily on a project basis.

In 1965, Shell introduced a new systemcalled "Unified Planning Machinery" (UPM) to pro-vide planning details for the whole chain of activity-from moving oil from the ground, to the tanker, to therefinery, all the way to the gas station on the corner.UPM was a sophisticated, worldwide system thatlooked ahead six years: the first year in detail, the nextfive in broader lines. Unconsciously, managers de-signed the system to develop Shell's businesses in afamiliar, predictable world of "more of the same."

Given the long lead times for new proj-ects in an oil company, however, it was soon decidedthat the six-year horizon was too limited. Shell there-fore undertook experimental studies to explore thebusiness environment of the year 2000. One of themrevealed that expansion simply could not continue andpredicted that the oil market would switch from a buy-ers' to a sellers' market, with major discontinuities inthe price of oil and changing interfuel competition.The study also signaled that major oil companies couldbecome huge, heavily committed, and much less flexi-bie-almost like dinosaurs. And dinosaurs, as we allknow, did not adjust well to sudden environmentalchanges.

In view of the study's findings. Shell be-lieved it had to find a new way to plan. It asked a dozenof its largest operating companies and business sectors

1 Andre Benard,"World Oil and Cold Reality,"HBR November-December 1980, p. 91.

Scenario planning 75

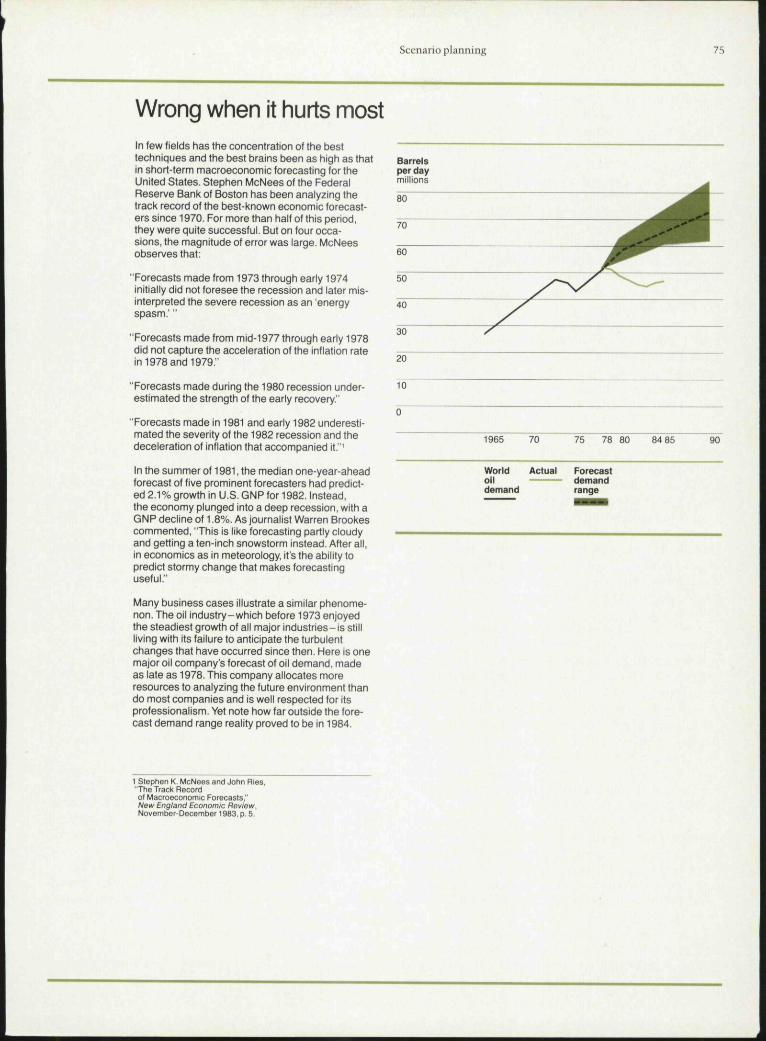

Wrong when it hurts mostIn few fields has the concentration of the besttechniques and the best brains been as high as thatin short-term macroeconomic forecasting for theUnited States. Stephen McNees of the FederalReserve Bank of Boston has been analyzing thetrack record of the best-known economic forecast-ers since 1970. For more than half of this period,they were quite successful. But on four occa-sions, the magnitude of error was large. McNeesobserves that:

"Forecasts made from 1973 through early 1974initially did not foresee the recession and later mis-interpreted the severe recession as an 'energySpasm.'"

"Forecasts made from mid-1977 through early 1978did not capture the acceleration of the inflation ratein 1978 and 1979."

"Forecasts made during the 1980 recession under-estimated the strength of the early recovery,"

"Forecasts made in 1981 and early 1982 underesti-mated the severity of the 1982 recession and thedeceleration of inflation that accompanied it."'

In the summer of 1981, the median one-year-aheadforecast of five prominent forecasters had predict-ed 2.1% growth in U.S. GNP for 1982. Instead,the economy plunged into a deep recession, with aGNP decline of 1.8%. As journalist Warren Brookescommented, "This is like forecasting partly cloudyand getting a ten-inch snowstorm instead. After all,in economics as in meteorology, it's the ability topredict stormy change that makes forecastinguseful."

Many business cases illustrate a similar phenome-non. The oil industry-which before 1973 enjoyedthe steadiest growth o1 ali major industries-is stillliving with its failure to anticipate the turbulentchanges that have occurred since then. Here is onemajor oil company's forecast of oil demand, madeas late as 1978. This company allocates moreresources to analyzing the future environment thando most companies and is well respected for itsprofessionalism. Yet note how tar outside the fore-cast demand range reality proved to be in 1984.

Barrelsper daymjlljons

80

1965 70 75 78 80 84 85 90

World Actual Forecastoil demanddemand range

1 Stephen K. McNees and John Ries."The Track Recordof Macroeconomic Forecasts,"New England Economic Review,November-December 1983, p. 5.

76 Harvard Business Review September-October 1985

to experiment and look ahead 15 years in an exercisecalled "Horizon Year Planning."

At the time, I worked for Shell Fran-^aise. We were familiar with the late Herman Kahn'sscenario approach and were intrigued hy its possihili-ties for corporate planning.

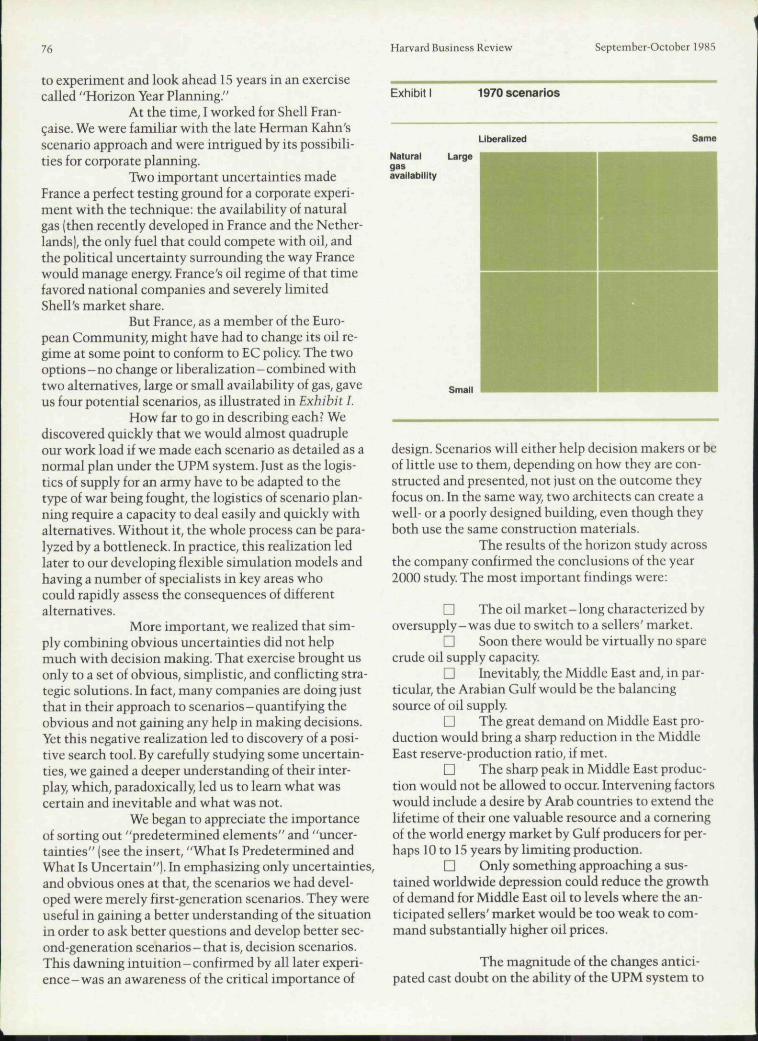

Two important uncertainties madeFrance a perfect testing ground for a corporate experi-ment with the technique: the availability of naturalgas (then recently developed in France and the Nether-lands), the only fuel that could compete with oil, andthe political uncertainty surrounding the way Francewould manage energy. France's oil regime of that timefavored national companies and severely limitedShell's market share.

But France, as a member of the Euro-pean Community, might have had to change its oil re-gime at some point to conform to EC policy. The twooptions-no change or liberalization-combined withtwo alternatives, large or small availability of gas, gaveus four potential scenarios, as illustrated in Exhibit I.

How far to go in describing each? Wediscovered quickly that we would almost quadrupleour work load if we made each scenario as detailed as anormal plan under the UPM system. Just as the logis-tics of supply for an army have to be adapted to thetype of war being fought, the logistics of scenario plan-ning require a capacity to deal easily and quickly withalternatives. Without it, the whole process can be para-lyzed by a bottleneck. In practice, this realization ledlater to our developing flexible simulation models andhaving a number of specialists in key areas whocould rapidly assess the consequences of differentalternatives.

More important, we realized that sim-ply combining obvious uncertainties did not helpmuch with decision making. That exercise brought usonly to a set of obvious, simplistic, and conflicting stra-tegic solutions. In fact, many companies are doing justthat in their approach to scenarios-quantifying tbeobvious and not gaining any help in making decisions.Yet this negative realization led to discovery of a posi-tive search tool. By carefully studying some uncertain-ties, we gained a deeper understanding of their inter-play, which, paradoxically, led us to learn what wascertain and inevitable and what was not.

We began to appreciate the importanceof sorting out "predetermined elements" and "uncer-tainties" (see the insert, "What Is Predetermined andWhat Is Uncertain"). In emphasizing only uncertainties,and obvious ones at that, the scenarios we had devel-oped were merely first-generation scenarios. They wereuseful in gaining a better understanding of the situationin order to ask better questions and develop better sec-ond-generation scenarios-that is, decision scenarios.This dawning intuition-confirmed by all later experi-ence-was an awareness of tbe critical importance of

Exhibit 1970 scenarios

Liberalized Same

Naturalgasavailability

Large

Smail

design. Scenarios will either help decision makers or beof little use to tbem, depending on how they are con-structed and presented, not just on the outcome theyfocus on. In the same way, two architects can create awell- or a poorly designed building, even though theyboth use the same construction materials.

The results of the horizon study acrossthe company confirmed the conclusions of the year2000 study. The most important findings were:

D The oil market-long characterized byoversupply-was due to switch to a sellers' market.

n Soon there would be virtually no sparecrude oil supply capacity.

n Inevitably, the Middle East and, in par-ticular, the Arabian Gulf would be the balancingsource of oil supply.

D The great demand on Middle East pro-duction would bring a sharp reduction in the MiddleEast reserve-production ratio, if met.

n The sharp peak in Middle East produc-tion would not be allowed to occur. Intervening factorswould include a desire by Arab countries to extend thelifetime of their one valuable resource and a corneringof the world energy market by Culf producers for per-haps 10 to 15 years by limiting production.

• Only something approaching a sus-tained worldwide depression could reduce the growthof demand for Middle East oil to levels where the an-ticipated sellers' market would be too weak to com-mand substantially higher oil prices.

The magnitude of the changes antici-pated cast doubt on the ability of the UPM system to

Scenario planning 77

provide realistic planning assumptions. How could itprovide the right ansv er if the forecasts on which itwas based were likely to be wrong? In 1971, Shell there-fore decided to try scenario planning as a potentiallybetter framework for thinking about the future thanforecasts-which were now perceived as a dangeroussubstitute for real thinking in times of uncertainty andpotential discontinuity But Shell, like many largeorganizations, is cautious. During the first year, whenscenario analysis was done on an experimental basis,the company continued to employ the UPM system. In1972, scenario planning was extended to central officesand certain large Shell national operating companies.In the following year, it was finally recommendedthroughout the group and UPM was then phased out.

The next step

The scenario process started with theconstruction of a set of exploratory first-generationscenarios. A& we hjVe learned, it is almost impossibleto jump directly to proper decision scenarios.

• Scenario I was surprise-free, virtuallylifted whole from the work done under the old UPMsystem. The surprise-free scenario is one that rarelycomes to pass but, in my experience, is essential in thepackage. It builds on the implicit views of the futureshared by most managers, making it possible for themto recognize their outlook in the scenario package. Ifthe package only contains possibilities that appearalien to the participants, they will likely find the sce-nario process threatening and reject it out of hand.

• Scenario II postulated a tripling of host-government tax take in view of the 1975 renegotiationof the Teheran Agreement (which set the take forOPEC) and anticipated lower economic growth anddepressed energy and oil demand as a consequence.

n Scenario III treated the other obviousuncertainty: low growth. Based on the 1970-1971 reces-sion model, a proliferation of "me-first" values, and agrowing emphasis on leisure, it assumed an economicgrowth rate only half of that projected under Scenario I,with a slowdown in international trade, economicnationalism, and protective tariffs. Low oil demandwould limit oil price rises and lower producer govern-ment take.

n Scenario IVassumed increased demandfor coal and nuclear energy-at the expense of oil.

All four scenarios assumed that the taxtake of the producer governments would be increasedat the 1975 Teheran renegotiation (see Exhibit II).

What is predeterminedand what is uncertainStrictly speaking, you can forecast the future onlywhen all of its elements are predetermined. By pre-determined elements. I mean those events thathave already occurred (or that almost ceriainly willoccur) but whose consequences have not yetunfolded.

Suppose, for example, heavy monsoon rains hit theupper part of the Ganges River basin. With littledoubt you know that something extraordinary willhappen within two days at Rishikesh at the foothillsof the Himalayas; in Allahabad, three or four dayslater; and at Benares, two days after that. Youderive that knowledge not from gazing into a crystalball but from simply recognizing the future implica-tions of a rainfall that has already occurred.

Identifying predetermined elements is fundamentalto serious planning. You must be careful, however.Paul Valery. the twentieth-century French philoso-pher, said, "Un fait mal observe est plus pernicieuxqu'un mauvais raisonnement." (A fact poorlyobserved is more treacherous than faulty reason-ing.) Errors in futures studies usually result frompoor observation rather than poor reasoning.

There are always elements of the future that arepredetermined. But there are seldom enough ofthem to permit a single-line forecast that encom-passes residual uncertainties. Decision makers fac-ing uncertain situations have a right to know justhow unceriain they are. Accordingly, it is essentialto try to put as much light on critical uncertainties ason the predetermined elements. They should not beswept under the carpet.

OK as numbers bu t -

This set of scenarios seemed reasonablywell designed and would fit most definitions of whatscenarios should be. It covered a wide span of possiblefutures, and each scenario was internally consistent.

When the set was presented to Shell'stop management, the problem was the same as in theFrench scenarios; no strategic thinking or action couldbe taken from considering this material.

Many companies reach this same pointin planning scenarios. Management reaction? "Sowhat! What do I do with scenarios?" And plannersabandon the effort, often because they believe theproblem is, in part, management's inability to dealwith uncertainty.

Yet this group of Shell managers washighly experienced in dealing with risk and uncer-tainty. For example, many of the decisions they makedeal with exploratory drilling, a true uncertainty sinceyou never know what you'll find until you drill. Theymust often decide whether to risk $5 million or $50

78 Harvard Business Review September-October 1985

Exhibit tt Producer government take*1970-1985

Dollars perbarrei

1969 70 71 72 73 74 75 76

'Constant 1970 dollars

77 78 79 80 81 83 84 85

million on exploration projects and distinguish therisks, say, in Brazil or the North Sea. What was so dif-ferent about the uncertainties of scenarios? Quite sim-ply, they needed structuring. In oil exploration, therewere theories to call on, concepts to use, an organizedbody of geological and geophysical analyses, compari-sons with similar geological structures, and ways tospread the risk that were familiar to the decisionmaker. The first-generation scenarios presented theraw uncertainties but they offered no basis on whichmanagers could exercise their judgment. Our next taskwas to provide that basis so that executives could un-derstand the nature of these uncertainties and come togrips with them.

The goal of these exploratory first-generation scenarios is not action but understanding.Their purpose is to give insight into the system, toidentify tbe predetermined elements, and to perceiveconnections among various forces and events drivingthe system. As the system's interrelatedness becameclear, we realized that what may appear in some casesto be uncertain might actually be predetermined—thatmany outcomes were simply not possible.

These exploratory scenarios were noteffective planning devices. Without them, however, wecould not have developed the next generation ofscenarios.

What will happen-what cannot

To understand the fluctuations that givethe oil system its character and determine its future,we had to understand the forces that drive it. Work onthe next set of scenarios began with a closer look at theprincipal actors in Shell's business environment: oilproducers, consumers, and companies. Because self-interest determined the fundamental concerns of thesegroups, significant behavioral differences existed. Sowe began to study the characters on the stage and howthey would behave as the drama unfolded.

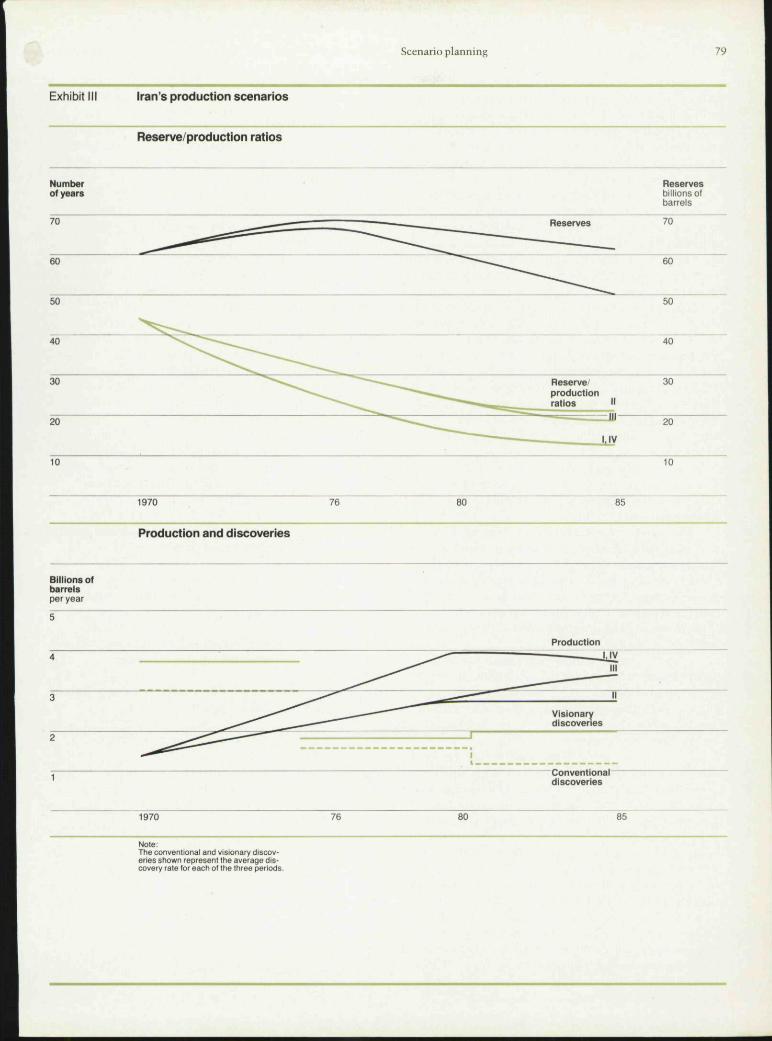

In analyzing the major oil-producingcountries one by one, for example, it was clear thatIran's interests differed from Saudi Arabia's or Nigeria'sand that their strategies would reflect these differ-ences. The lower panel of Exhibit III shows Iran's oilproduction as its share of projected oil demand undereach of the 1971 scenarios, as well as discovery ratesand additions to reserves. For the first five years, we ex-pected that Iran's reserves would grow as the industryfound more new oil than it would produce. For the sec-ond five years, we expected the situation to reverse andreserves to fall.

As the upper panel of Exhibit III shows,reserve-production ratios would drop rapidly under all

Scenario planning 79

Exhibit III Iran's production scenarios

Reserve/production ratios

Numberot years

70

Reservesbillions ofbarrels

Reserves 70

60

50

-..,__^_^ 60

50

40

30 Reserve/productionratios

20

30

20

10 10

1970 76 80 85

Production and discoveries

Billions ofbarrelsper year

Production

"Conventionaldiscoveries

1970 76 80 85

The convenlional and vistonary discov-eries shown represent the average dis-covery rate tor each of the Ihree periods.

Harvard Business Review September-October 1985

scenarios. Our conclusion was that Iran would thenstrive to change its oil policy from one of expandingproduction to one of increasing prices and possiblycurbing production. Such a policy change would stemnot from an anti-Westem attitude but simply from thelogic of national interest. If we were Iranian, we wouldbehave the same way.

Saudi Arabia's situation was different.Except in the low-growth scenario, production wouldgenerate more revenue than the government couldpurposefully spend, even allowing for some "manage-able" surplus. We concluded that even though oil com-pany logic would have the Saudis producing 20 millionbarrels per day by 1985, the government could not doso in good political conscience. It was no surprise whenSheikh Zhaki Ahmed Yamani, Saudi Arabia's ministerfor oil affairs, later remarked: "We should find thatleaving our crude in the ground is by far more profit-able than depositing our money in the banks, particu-larly if we take into account the periodic devaluationof many of the currencies. This reassessment wouldlead us to adopt a production program that ensuresthat we get revenues which are only adequate for ourreaineeds."^

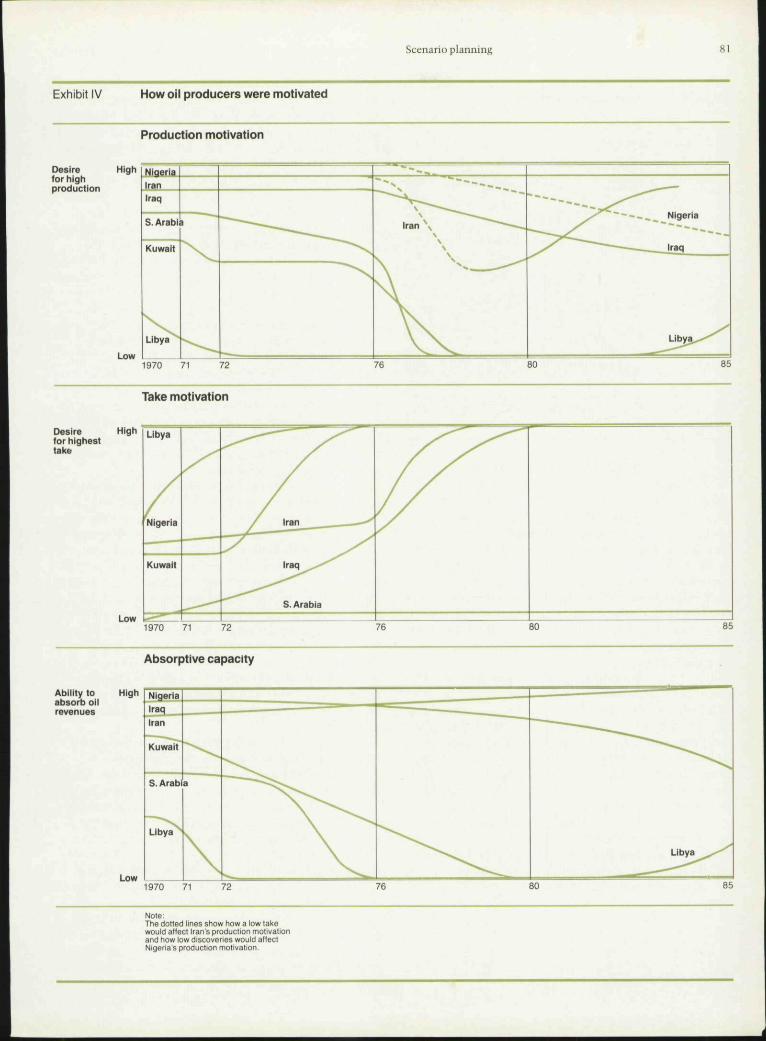

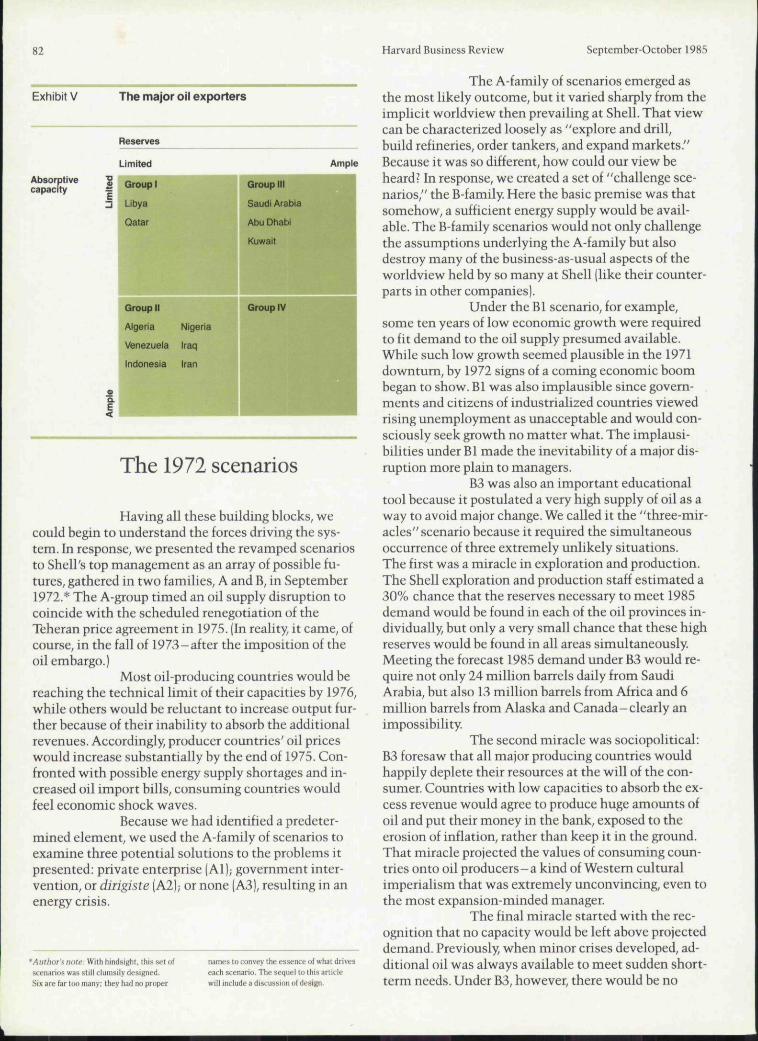

We analyzed each of the producer coun-tries according to their oil reserves and their need andability to spend oil income productively {Exhibit IV).When arrayed in the simple matrix shown in Exhibit V,the power that was to become OPEC emerged clearly:no nation had both ample reserves and ample absorp-tive capacity, that is, the motivation to produce thesereserves. If Indonesia, with its large population andenormous need for funds, had Saudi Arabia's reserves,then the growth of demand foreseen under the firstscenario might have developed. But such was not thecase.

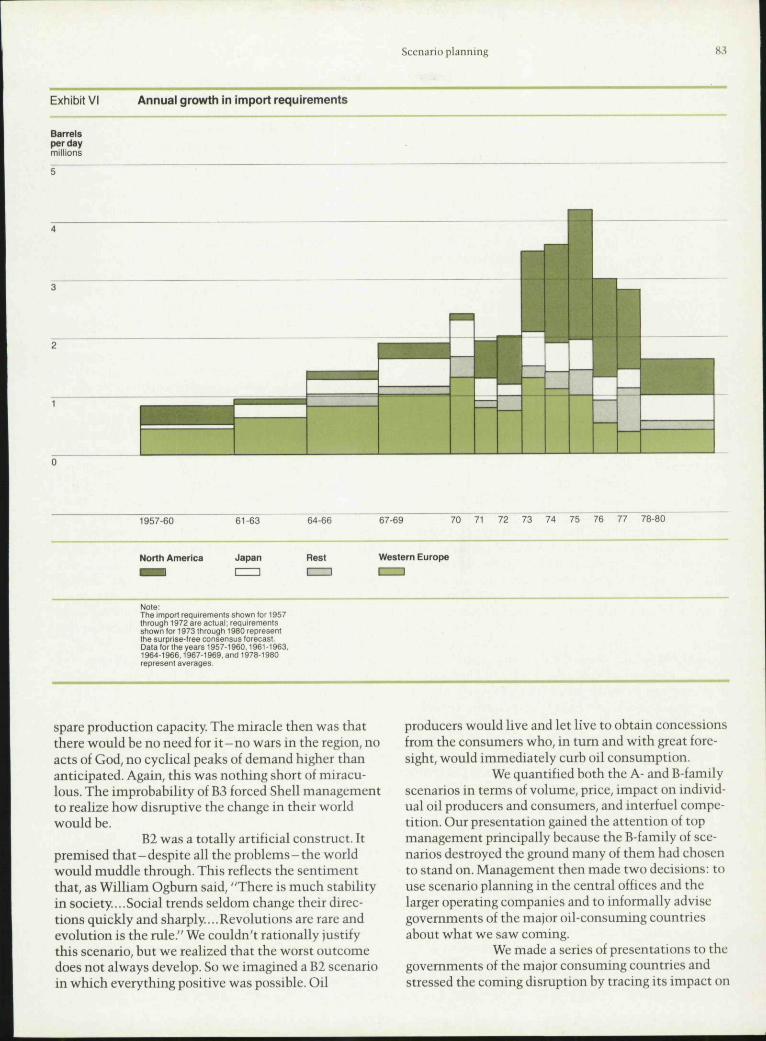

We then analyzed the oil-consumingcountries and saw their annual increments in importrequirements (see Exhibit VI). For many years, oilimports had increased at a rate of about one millionbarrels per day; then for a long time the rate was abouttwo million barrels per day

Suddenly, in the mid-1970s, oil importswere expected to increase annually at much higherrates. This change can be understood by looking at Ex-hibit VII. which shows the sources of energy supply inthe United States, Western Europe, and Japan. In theUnited States, oil supply had peaked early, and the in-cremental demand for energy had been satisfied by nat-ural gas. Because of its regulated price, however, natu-ral gas production plateaued in 1972. Coal productionmight have increased, but in light of the forecasts offuture nuclear power generation, coal resources werenot being developed. Nuclear plants, however, were notfunctioning in sufficient numbers to meet the demand,which was increasing annually at a rapid pace. Sincethe base was so large to begin with, even a 3% or 4%

increase in the U.S. energy demand would in tumdemand a great deal of the only available incrementalenergy source—imported oil.

In Japan - then like a new continentemerging on the world economic map - circumstanceswere different. In 1953, as the U.S. occupation ended,Japanese industrial production was 40% of the UnitedKingdom's; in 1970, it was more than double. With theeconomy growing by 11 % or 12% a year, armualdemand for oil increased by some 20%. The result:huge increases in oil imports.

Beyond the need to view each partici-pant individually and as part of a group, we discoveredthat "soft" data were as important to us as "hard" datain analyzing outcomes. For example, because the Japa-nese become anxious when faced with a possible de-nial of imports, any tension over oil supply would beespecially trying. Furthermore, they would project onmultinational oil companies the type of behavior theyexpect from their own companies in a crisis: givingloyalty to the home country and ignoring the rest ofthe world. This attitude would add to the probable ten-sion over oil supplies.

Having collected and analyzed hard andsoft data, and in order to expand the number of prede-termined elements and get at the core of what re-mained uncertain, we looked at:

Oil demand by market class and at dif-ferent rates of growth.

The implications of high oil prices foreach nation's balance of payments andinflation.

The possible reactions of consumer gov-ernments to higher oil prices.

Interfuel competition and the impact ofhigher oil prices.

The changing "cut of the barrel."

Construction of refinery marine, andmarket facilities.

2 Quoted in P/aii's Oilgiam.February 10,1972,

Scenario planning 81

Exhibit IV How oil producers were motivated

Production motivation

Desirefor highproduction

High

Low1970 71 72

Take motivation

Desire Highfor highesttake

Low

Libya

Nigeria

—

Kuwait

— — —El/ iran ^

I r a a . - - ^

S. Arabia1970 71 72 76 80 85

Absorptive capacity

Ability toabsorb oilrevenues

High

Low1970 71

Note:The dotted lines show how a low takewould alfecl Iran's production motivationand how low discoveries would aflectNigeria s production motivation.

82 Harvard Business Review September-October 1985

Exhibit V The major oil exporters

Reserves

Ample

Absorptivecapacity

Group II

Algeria Nigeria

Venezuela Iraq

indonesia Iran

The 1972 scenarios

Having all these building blocks, wecould begin to understand the forces driving the sys-tem. In response, we presented the revamped scenariosto Shell's top management as an array of possible fu-tures, gathered in two families, A and B, in September1972.* The A-group timed an oil supply disruption tocoincide with the scheduled renegotiation of theTeheran price agreement in 1975. (In reality, it came, ofcourse, in the fall of 1973-after the imposition of theoil embargo.)

Most oil-producing countries would bereaching the technical limit of their capacities by 1976,while others would be reluctant to increase output fur-ther because of their inability to absorb the additionalrevenues. Accordingly, producer countries' oil priceswould increase substantially by the end of 1975. Con-fronted with possible energy supply shortages and in-creased oil import bills, consuming countries wouldfeel economic shock waves.

Because we had identified a predeter-mined element, we used the A-family of scenarios toexamine three potential solutions to the problems itpresented: private enterprise jAl); government inter-vention, or dirigiste (A2); or none (A3), resulting in anenergy crisis.

'Author'snote: Wilh hindsiKht, ihis sel ofscenarios was still clumsily designed.Six are (ar too niany; they had no proper

names to convey the essence of wfiat drivt'Seach scenario. The sequel lo this articlewill include a discussion of design.

The A-family of scenarios emerged asthe most likely outcome, but it varied sharply from theimplicit worldview then prevailing at Shell. That viewcan be characterized loosely as "explore and drill,build refineries, order tankers, and expand markets."Because it was so different, how could our view beheard? In response, we created a set of "challenge sce-narios," the B-family Here the basic premise was thatsomehow, a sufficient energy supply would be avail-able. The B-family scenarios would not only challengethe assumptions underlying the A-family but alsodestroy many of the business-as-usual aspects of theworldview held by so many at Shell (like their counter-parts in other companies).

Under the Bl scenario, for example,some ten years of low economic growth were requiredto fit demand to the oil supply presumed available.While such low growth seemed plausible in the 1971downturn, by 1972 signs of a coming economic boombegan to show. Bl was also implausible since govern-ments and citizens of industrialized countries viewedrising unemployment as unacceptable and would con-sciously seek growth no matter what. The implausi-bilities under Bl made the inevitability of a major dis-ruption more plain to managers.

B3 was also an important educationaltool because it postulated a very high supply of oil as away to avoid major change. We called it the "three-mir-acles" scenario because it required the simultaneousoccurrence of three extremely unlikely situations.The first was a miracle in exploration and production.The Shell exploration and production staff estimated a30% chance that the reserves necessary to meet 1985demand would be found in each of the oil provinces in-dividually, but only a very small chance that these highreserves would be found in all areas simultaneously.Meeting the forecast 1985 demand under B3 would re-quire not only 24 million barrels daily from SaudiArabia, but also 13 million barrels from Africa and 6million barrels from Alaska and Canada-clearly animpossibility.

The second miracle was sociopolitical:B3 foresaw that all major producing countries wouldhappily deplete their resources at the will of the con-sumer. Countries with low capacities to absorb the ex-cess revenue would agree to produce huge amounts ofoil and put their money in the bank, exposed to theerosion of inflation, rather than keep it in the ground.That miracle projected the values of consuming coun-tries onto oil producers-a kind of Western culturalimperialism that was extremely unconvincing, even tothe most expansion-minded manager

The final miracle started with the rec-ognition that no capacity would be left above projecteddemand. Previously, when minor crises developed, ad-ditional oil was always available to meet sudden short-term needs. Under B3, however, there would be no

Scenario planning

Exhibit VI Annual growth in import requirements

Barrelsper daymillions

1957-60 61-63 64-66 67-69 70 71 72 73 74 75 76 77 78-80

North America Japan Rest Western Europe

Note:The import requirements stiown tor 1957througt) 1972 are actual, requirementsshown for 1973 througti 1980 representthe surprise-tree consensus forecast.Datafortheyears 1957-1960,1961-1963,1964-1966,1967-1969, and 1978-1980represent averages.

spare production capacity. The miracle then was thatthere would he no need for i t -no wars in the region, noacts of God, no cychcal peaks of demand higher thananticipated. Again, this was nothing short of miracu-lous. The improhahihty of B3 forced Shell managementto realize how disruptive the change in their worldwould be.

B2 was a totally artificial construct. Itpremised that-despite all the prohlems-the worldwould muddle through. This reflects the sentimentthat, as William Oghum said, "There is much stabilityin society...,Social trends seldom change their direc-tions quickly and sharply.... Revolutions are rare andevolution is the rule." We couldn't rationally justifythis scenario, hut we realized that the worst outcomedoes not always develop. So we imagined a B2 scenarioin which everything positive was possible. Oil

producers would live and let live to ohtain concessionsfrom the consumers who, in turn and with great fore-sight, would immediately curb oil consumption.

We quantified both the A- and B-familyscenarios in terms of volume, price, impact on individ-ual oil producers and consumers, and interfuel compe-tition. Our presentation gained the attention of topmanagement principally because the B-family of sce-narios destroyed the ground many of them had chosento stand on. Management then made two decisions: touse scenario planning in the central offices and thelarger operating companies and to informally advisegovernments of the major oil-consuming countriesabout what we saw coming.

We made a series of presentations to thegovernments of the major consuming countries andstressed the coming disruption by tracing its impact on

84 Harvard Business Review September-October 1985

their balance of payments, rates of inflation, and re-source allocation.

Banging the drum quickly

Shell first asked its major downstreamoperating companies to evaluate current strategiesagainst two A-type scenarios, using the B2 scenario as asensitivity check. By asking "what if," the B2 checkedstrategies already conceived in another conceptualframework (the A-family).

To this intent, we presented the A and Bscenarios to the second echelon of Shell's management- i ts first exposure to scenarios. The meetings stood instark contrast to traditional UPM planning sessions,which dealt out forecasts, trends, and premises - allunder an avalanche of numhers. The scenarios focusedless on predicting outcomes and more on understand-ing the forces that would eventually compel an out-come; less on figures and more on insight. The meet-ings were unusually lengthy and the audience clearlyappreciative. We thought we had won over a large shareof these managers.

The following months would show,however, that no more than a third of Shell's criticaldecision centers were really acting on the insightsgained through the scenarios and actively preparing forthe A-family of outcomes. The scenario package hadsparked some intellectual interest hut had failed tochange hehavior in much of the Shell organization.This reaction came as a shock and compelled us to re-think how to design scenarios geared for decisionmaking.

Reality was painful; most studies deal-ing with the future business environment, includingthese first scenarios, have a low "existential effective-ness." (We can define existential effectiveness assingle-mindedness, but the Japanese express it muchbetter: "When there is no break, not even the thick-ness of a hair, between a man's vision and his action.")A vacuum cleaner is mostly heat and noise; its actualeffectiveness is only around 40%. Studies of the future,particularly when they point to an economic disrup-tion, are less effective than a vacuum cleaner.

If your role is to be a corporate lookoutand you clearly see a discontinuity on the horizon, youhad better learn what makes the difference between amore or a less effective study. One of the differencesinvolves the basic psychology of decision making.

Every manager has a mental model ofthe world in which he or she acts based on experienceand knowledge. When a manager must make a deci-sion, he or she thinks of behavior alternatives withinthis mental model. When a decision is good, otherswill say the manager has good judgment. In fact, what

has really happened is that his or her mental mapmatches the fundamentals of the real world. We callthis mental model the decision maker's "microcosm";the real world is the "macrocosm."

There is also a corporate view of theworld, a corporate microcosm. During a sabbatical yearin Japan, for example, I found that Nippon Steel did not"see" the steel market in the same way as Usinor, theFrench steel giant. As a result, there were marked dif-ferences in the behavior and priorities of the two cor-porations. Each acted rationally, given its worldview. Acompany's perception of its business environment is asimportant as its investment infrastructure because itsstrategy comes from this perception. I cannot overem-phasize this point: unless the corporate microcosmchanges, managerial behavior will not change; the in-ternal compass must be recalibrated.

From the moment of this realization,we no longer saw our task as producing a documentedview of the future business environment five or tenyears ahead. Our real target was the microcosms of ourdecision makers: unless we influenced the mental im-age, the picture of reality held by critical decision mak-ers, our scenarios would be like water on a stone. Thiswas a different and much more demanding task thanproducing a relevant scenario package.

We had first tried to produce scenariosthat we would not be ashamed of when we subsequent-ly compared them with reality. After our initiationwith these first sets of scenarios, we changed our goal.We now wanted to design scenarios so that managerswould question their own model of reality and changeit when necessary, so as to come up with strategic in-sights beyond their minds' previous reach, This changein perspective-from producing a "good" document tochanging the image of reality in the heads of criticaldecision makers-is as fundamental as that experi-enced when an organization switches from selling tomarketing.

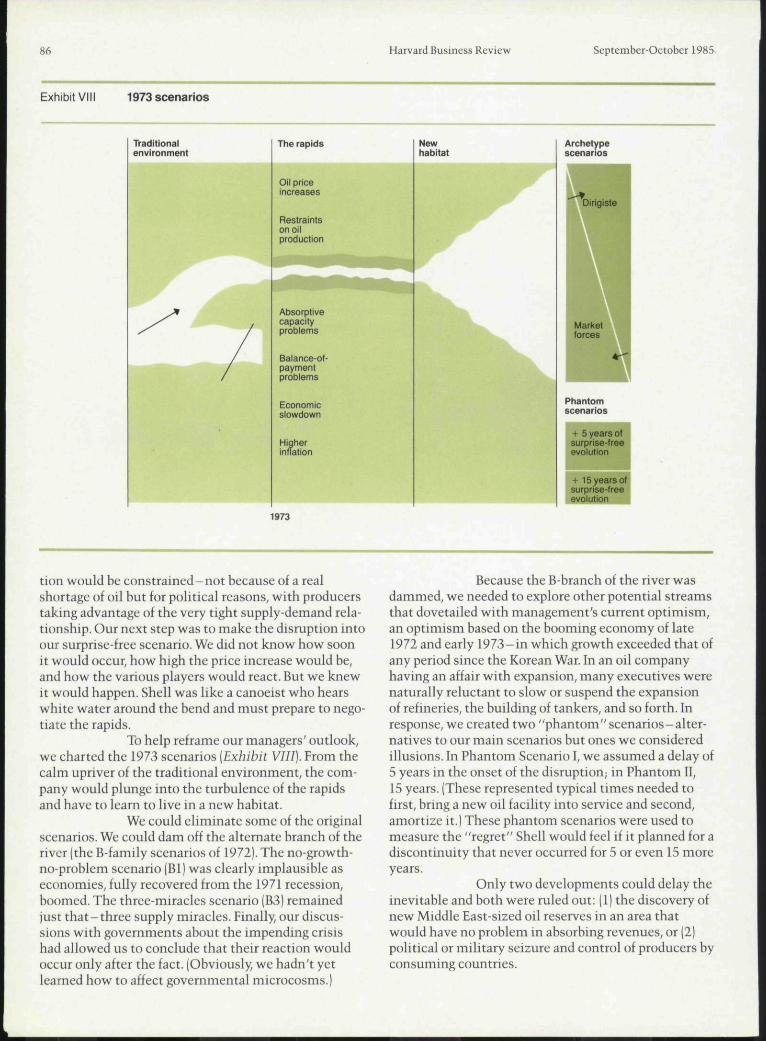

The 1973 scenarios-the rapids

More than 20 centuries ago, Ciceronoted, "It was ordained at the heginning of the worldthat certain signs should prefigure certain events." Aswe prepared the 1973 scenarios, all economic signspointed to a major disruption in oil supply. New analy-ses foretold a tight supply-demand relationship in thecoming years.

Now we saw the discontinuity as pre-determined. No matter what happened in particular,prices would rise rapidly in the 1970s, and oil produc-

Scenario planning 85

Exhibit VII Energy demand by sources

United States Japan

Barreisper daymillions

50

30

Bafreisper daymillions

50

40

30

20

1966 68 70 72 74 76 78 80 1966 68 70 72 74 76 78 80

Western Europe i = Imported energy indigenous

Barrelsper daymillions

50

10

N = nuciear

H = hydroeiectricity

C = coai

G = naturaigas

0 = oii

Note:The energy demand shown for 1966through 1972 ts actual; demand shown for1974 ttifough 1980 represents thesurprjse-tree consensus forecast.

1966 68 70 72 74 76 78 80

86 Harvard Business Review September-October 1985

Exhibit Vllt 1973 scenarios

TVadltJonalenvironment

The rapids

Oil priceincreases

Restraintson oilproduction

Absorptivecapacityproblems

Balance-of-paymentproblems

Economicslowdown

Higherinflation

Newhabitat

Phantomscenarios

+ 5 years otsurprise-freeevolution..

ysurprise-freeevolution

1973

tion would be constrained-not because of a realshortage of oil but for politieal reasons, with producerstaking advantage of the very tight supply-demand rela-tionship. Our next step was to make the disruption intoour surprise-free scenario. We did not know how soonit would occur, how high the price increase would be,and how the various players would react. But we knewit would happen. Shell was like a canoeist who hearswhite water around the bend and must prepare to nego-tiate the rapids.

To help reframe our managers' outlook,we charted the 1973 scenarios [Exhibit VIII). From thecalm upriver of the traditional environment, the com-pany would plunge into the turbulence of the rapidsand have to learn to live in a new habitat.

We could eliminate some of tbe originalscenarios. We could dam off the alternate brancb of theriver (tbe B-family scenarios of 1972). The no-growtb-no-prohlem scenario (Bl) was clearly implausible aseconomies, fully recovered from the 1971 recession,boomed. The three-miracles scenario (B3) remainedjust tbat—three supply miracles. Finally, our discus-sions with governments about the impending crisishad allowed us to conclude that tbeir reaction wouldoccur only after the fact. (Obviously, we badn't yetlearned how to affect governmental microcosms.)

Because the B-branch of the river wasdammed, we needed to explore other potential streamsthat dovetailed with management's current optimism,an optimism based on the booming economy of late1972 and early 1973-in whicb growtb exceeded that ofany period since the Korean War. In an oil companyhaving an affair witb expansion, many executives werenaturally reluctant to slow or suspend the expansionof refineries, the building of tankers, and so fortb. Inresponse, we created two "phantom"scenarios-alter-natives to our main scenarios but ones we consideredillusions. In Phantom Scenario I, we assumed a delay of5 years in the onset of the disruption; in Phantom II,15 years. (These represented typical times needed tofirst, bring a new oil facility into service and second,amortize it.) These phantom scenarios were used tomeasure the "regret" Shell would feel if it planned for adiscontinuity tbat never occurred for 5 or even 15 moreyears.

Only two developments could delay theinevitable and both were ruled out: (1) the discovery ofnew Middle East-sized oil reserves in an area thatwould have no problem in absorbing revenues, or (2)political or military seizure and control of producers byconsuming countries.

Scenario planning 87

Exhibit IX A new worldview

Alternativefuels

Cost Delay

Crudereservesdeveloped atproducers'logic andscramble —for oil(U.S.,Japan,W. Europe)

PriceInsecurity

Accidents Negativesupplyelasticity

The "snecessarycrisis

Archetypescenarios

Dirigiste

Marketforces

Phantomscenarios

+ 5 years ofsurprise-freeevolution

+ 15 years ofsurprise-freeevolution

Newhabitat

More than water on a stone

On the surface, the 1973 scenariosseemed much like the A-scenarios constructed in1972. Driven hy a new sense of urgency, however, wesaw them in a different light. The time we had to antic-ipate, prepare for, and respond to the new environmenthad shrunk greatly.

More important, we wanted the 1973scenarios to be more than water on a stone: we wantedto change our managers' view of reality. The first stepwas to question and destroy their existing view of theworld in which oil demand expanded in orderly andpredictable fashion, and Shell routinely could add oilfields, refineries, tankers, and marketing outlets. Infact, we had been at this job of destruction now for sev-eral years.

But exposing and invalidating an obso-lete worldview is not where scenario analysis stops.Reconstructing a new model is the most important joband is the responsibility of the managers themselves.The planners' job is to engage the decision makers' in-terest and participation in this reconstruction. We lis-ten carefully to their needs and give them the highestquality materials to use in making decisions. The plan-ners will succeed, however, only if they can securely

link the new realities of the outside world-the unfold-ing business environment - to the managers' micro-cosm. Good scenarios supply this vital "bridge"; theymust encompass both managers' concerns and exter-nal reality Otherwise, no one will bother to cross thebridge.

If the planners design the package well,managers will use scenarios to construct a new modelof reality by selecting from them those elements theybelieve relevant to their business world. Because theyhave heen making decisions-and have a long trackrecord to show that they're good at i t-they may, ofcourse, not see any relevant elements. Or they may gowith what their "gut" tells them. But that should notdiscourage the planner who is drawing up the scenario.

Just as managers had to change theirworldview, so planners had to change the way theyviewed the planning process. So often, planning isdivorced from the managers for whom it is intended.We came to understand that making the scenarios rele-vant required a keener knowledge of decision makersand their microcosm than we had ever imagined. Inlater years, we built some bridges that did not get used.The reason for this failure was always that we did notdesign scenarios that responded to managers' deepestconcerns.

Harvard Business Review September October 1985

Building blocks for newmicrocosms

In developing tbe 1973 scenarios, werealized that if managers v ere to reframe their view ofreality, they would need a clear overview of a new mod-el. Exhibit IX, one way to portray that model, summa-rizes tbe anticipated business environment and its keyelements: tbe predetermined events, which are shownon the left, and the major discontinuities, which areshown in tbe center.

We focused attention on the followingfeatures of the business environment [shown inExhibit IX):

• Alternative fuels, which we could de-velop only very slowly Even under a wartime crash de-velopment program, none could be available before the1980s. We analyzed the cost in three stages. First, eventhough other fuels might replace oil for generatingpower and steam in large industrial settings, the oil-producing nations would not be impressed. On the con-trary, they welcomed the alternative of coal and nuclearpower in what they considered low-value markets.Second, oil used for heating was a different story. Burn-ing coal was not a satisfactory alternative. You wouldhave to gasify or transform coal into electricity, withaccompanying thermodynamic loss. Tbe price for tbisalternative was bigh; the price for oil would not exceedtbis threshold in tbe near future. The third possibihtyoil used in transport, had an even bigber fuel cost thanoil used for heating and was obviously irrelevant.

D Accidents, which included both politi-cal and internal and physical incidents, are events thatany oil executive considers a matter of course. In thesame way a Filipino knows that a roof must be builtcarefully; even tbougb the weather in the Philippinesis usually balmy, typhoons are frequent enough thattbe only uncertainty is when tbe roof's strength will betested.

• Negative supply elasticity, which meansthat unlike other commodities the supply of oil doesnot increase witb increases in its price, at least for anumber of years. On the contrary, the higher the price,the lower the volume of oil it would be in the interestof the major exporting countries to produce.

As planners at the center of a diversegroup of companies, we faced a special problem beyondthe construction of a new worldview. We bad to makeits message useful not only to managing directors butalso to operating companies from Canada to Germany,Japan to Australia. And yet tbe dramatic changes weanticipated would affect each differently. What basicmessage could we convey to all of tbem?

To construct a framework for the mes-sage, we borrowed the concept of archetypes frompsychology. Just as we often view individuals as com-posites of archetypes (for example, part introvert andpart extrovert), so we developed governmental arche-types to help us examine differing national responses.In t)ur view, nations would favor either a market-forceor government-intervention [dirigiste] approach. Nocountry would follow one path exclusively. We expect-ed, for example, that West Germany's response wouldbe more market oriented, whereas France's would bemore dirigiste. We analyzed the actions anticipatedunder each archetypal response in terms of price in-creases, taxes, alternative fuel development, and regu-lations by market class.

We led the managers towater...

while we didn't fully comprehend thatinfluencing managers required a tailor-made fit be-tween the seenarios and their deepest concerns, weknew intuitively that events in 1973 gave us this fit inseveral ways. The arrows on the right side of ExhibitIX symbolize four of tbe implications stressed.

We told our upstream managers, en-gaged in exploration and production, that tbe unthink-able was going to happen: "Be careful! You are about tolose tbe major part of your concessions and miningrents." Tbe traditional profit base in the upstreamworld would be lost and new relationships would baveto be developed between tbe company and producingnations.

To tbe downstream world of refiners,transporters, and marketers, we said somethingequally alarming: "Prepare! You are about to become alow-growth industry." Oil demand had always grownmore rapidly than GNI something Shell's manage-ment took for granted. In the past, we did not have toeonsider the consequences of overinvestment; one ortwo years of normal market growtb would cure anypremature moves. Now oil consumption in industrialcountries would increase at rates less than the increasein GNR and Shell would bave to develop new instinctsand reflexes to function in a low-growth world.

A third serious implication was theneed to furtber decentralize the decision-making andstrategic process. One basic strategy would no longerbe valid for operating companies in most parts of theworld. Shell companies bad generally-and success-fully-aimed for a higher share of conversion in refin-eries than did the competition. Now we understoodtbat the energy shock would affect each nation so dif-

Scenario planning 89

ferently that each would have to respond independent-ly. Shell, which was already decentralized comparedwith other oil majors, did in fact decentralize further,enabling it to adjust faster to the turbulence experi-enced later. (For some time now, it has been the mostdecentralized of all the major oil companies.)

Finally, we made managers see thatbecause we didn't know when the disruption wouldcome, they should prepare for it in different phases ofthe business cycle. We developed three simulations. Inthe first, the oil shock occurred before tbe cyclicaldownturn; in the second, the events were simultane-ous; and in the third, the oil shock followed the down-turn. These simulations led us to prepare for a far moreserious economic decline than might otherwise havebeen expected.

...and most finally drank

We hit planning pay dirt with the 1973scenarios because they met the deepest concerns ofmanagers. If any managers were not fully convinced,the events of October soon made them believers. Wehad set out to produce not a scenario booklet simplysummarizing views but a change in the way managersview their world. Only when the oil embargo begancould we appreciate the power of scenarios-powerthat becomes apparent when the world overturns,power that has immense and immediate value in alarge, decentralized organization.

Strategies are the product of a world-view. When the world changes, managers need to sharesome common view of the new world. Otherwise,decentralized strategic decisions will result in manage-ment anarchy Scenarios express and communicatethis common view, a shared understanding of the newrealities to all parts of the organization.

Decentralized management in world-wide operating companies can adapt and use that viewfor strategic decisions appropriate to its varied circum-stances. Its initiative is not limited by instructionsdictated from the center but facilitated and freed by abroad framework; all will speak the same language inadapting their operations to a new husiness environ-ment. Companies from Finland to New Zealand nowknew what "the rapids" meant, were alert to the impli-cations of producer logic, and recognized the need toprepare for a new environment.

From studying evolution, we learn howan animal suited to one environment must become anew animal to survive when the environment under-goes severe change. We believed that Shell wouldhave to become a new animal to function in a newworld. Business-as-usual decisions would no longersuffice.

In the next installment, I will discusshow we adapted the technique to develop scenarios forthe short term. As the time span between decisionssteadily hecame shorter, this refinement becamenecessary. ^

What executivesexpected from the1970sNational income in current dollars will increase atroughly the same rate in the 1970s as in the 1960s.

Industrial production will grow more slowly in the1970s...the servioe sector will continue to outpacethe rest of the economy and industrial productionwill shrink from the 60% growth of the last decadeto 55% in this decade.

Government spending v ill continue to increaseboth absolutely and relatively, despite slowergrowth in the defense sector Government's shareof national output will grow from Its current 25% to30% in the 1970s, and. by 1980, purchases ofgoods and services at federal, state, and local lev-els should reach $500 billion in a $1,700 billioneconomy.

Inflation will not be any worse than it is right now.But it will remain a problem throughout the decade...with an average annual rate of nearly 4V2%.This rate is slightly more pessimistic than econo-mists' projections and Is roughly 50% higher thanthe 3% average during the 1960s.

Unemployment may be somewhat more of a prob-lem in the 1970s than it was in the past decade.While the average rate was about 5% in the 1960s,the average for this decade may be closer to thepresent 5V2% rate. However, businessmen stillexpect cyclioal recurrences of labor shortagessimilar to those which prevailed in 1968-1969.

Corporate profits may not keep pace with nationalincome. Profits are the most volatile component ofnational income accounts, and the HBR panel'soverall profit pessimism is consistent with its predic-tions of national income and inflation.

Recessions will continue to be relatively mild. Itseems unlikely that we will experience a downturnany more severe than that of 1960-1961, whenindustrial production dropped 9%, The economyhas apparently become more "recession-proof"owing to increased government spending and therapid growth of comparatively stable serviceindustries.

FromDean S. Ammer,

"What Businessmen ExpectFrom the 1970s,HBR January-February 1971,p.41.

Harvard Business Review Notice of Use Restrictions, May 2009

Harvard Business Review and Harvard Business Publishing Newsletter content on EBSCOhost is licensed for

the private individual use of authorized EBSCOhost users. It is not intended for use as assigned course material

in academic institutions nor as corporate learning or training materials in businesses. Academic licensees may

not use this content in electronic reserves, electronic course packs, persistent linking from syllabi or by any

other means of incorporating the content into course resources. Business licensees may not host this content on

learning management systems or use persistent linking or other means to incorporate the content into learning

management systems. Harvard Business Publishing will be pleased to grant permission to make this content

available through such means. For rates and permission, contact [email protected].