How Deutsche Bank is Preparing for IBOR Transition and ... · IBOR Transition –a message from...

18

Deutsche Bank AG is a stock corporation incorporated under the laws of the Federal Republic of Germany with principal office at Taunusanlage 12, 60325 Frankfurt am Main. It is registered with the district court in Frankfurt am Main under No HRB 30 000 and licensed by the German Federal Financial Supervisory Authority (BaFin) to carry on banking business and to provide financial services as set forth in the German Banking Act (“Kreditwesengesetz”). Deutsche Bank AG is subject to comprehensive supervision by the European Central Bank (‘ECB’), by the BaFin and by the Deutsche Bundesbank (Bundesbank), Germany’s central bank. Deutsche Bank AG, London Branch is a branch of Deutsche Bank AG with Branch Registration in England and Wales BR000005 and registered address at Winchester House, 1 Great Winchester Street, London EC2N 2DB. It is subject to limited regulation in the United Kingdom by the Prudential Regulation Authority (‘PRA’) and Financial Conduct Authority (‘FCA’) as the local “host state” regulators. Further details can be found on Deutsche Bank AG’s website: https://db.com/disclosures How Deutsche Bank is Preparing for IBOR Transition and Benchmark Reform September, 2019

Transcript of How Deutsche Bank is Preparing for IBOR Transition and ... · IBOR Transition –a message from...

81nidZpGqzkSDMpD

Deutsche Bank AG is a stock corporation incorporated under the laws of the Federal Republic of Germany with principal office at Taunusanlage 12, 60325 Frankfurt am Main. It is registered with the district court in Frankfurt am Main under No HRB 30 000 and licensed by the German Federal Financial Supervisory Authority (BaFin) to carry on banking business and to provide financial services as set forth in the German Banking Act (“Kreditwesengesetz”). Deutsche Bank AG is subject to comprehensive supervision by the European Central Bank (‘ECB’), by the BaFin and by the Deutsche Bundesbank (Bundesbank), Germany’s central bank.

Deutsche Bank AG, London Branch is a branch of Deutsche Bank AG with Branch Registration in England and Wales BR000005 and registered address at Winchester House, 1 Great Winchester Street, London EC2N 2DB. It is subject to limited regulation in the United Kingdom by the Prudential Regulation Authority (‘PRA’) and Financial Conduct Authority (‘FCA’) as the local “host state” regulators.

Further details can be found on Deutsche Bank AG’s website: https://db.com/disclosures

How Deutsche Bank is Preparing for IBOR Transition and Benchmark Reform

September, 2019

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 2

Contents

IBOR Transition – a message from Dixit Joshi

How Deutsche Bank is looking to engage with you

The facts – what you need to know

Key factors of each IBOR and risk-free reference rate

Summarising the changes

Key market events

What this may mean for you

Deutsche Bank support

Frequently asked questions

This document will be issued periodically and each version supersedes all previous information.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 3

IBOR Transition – a message from Dixit Joshi

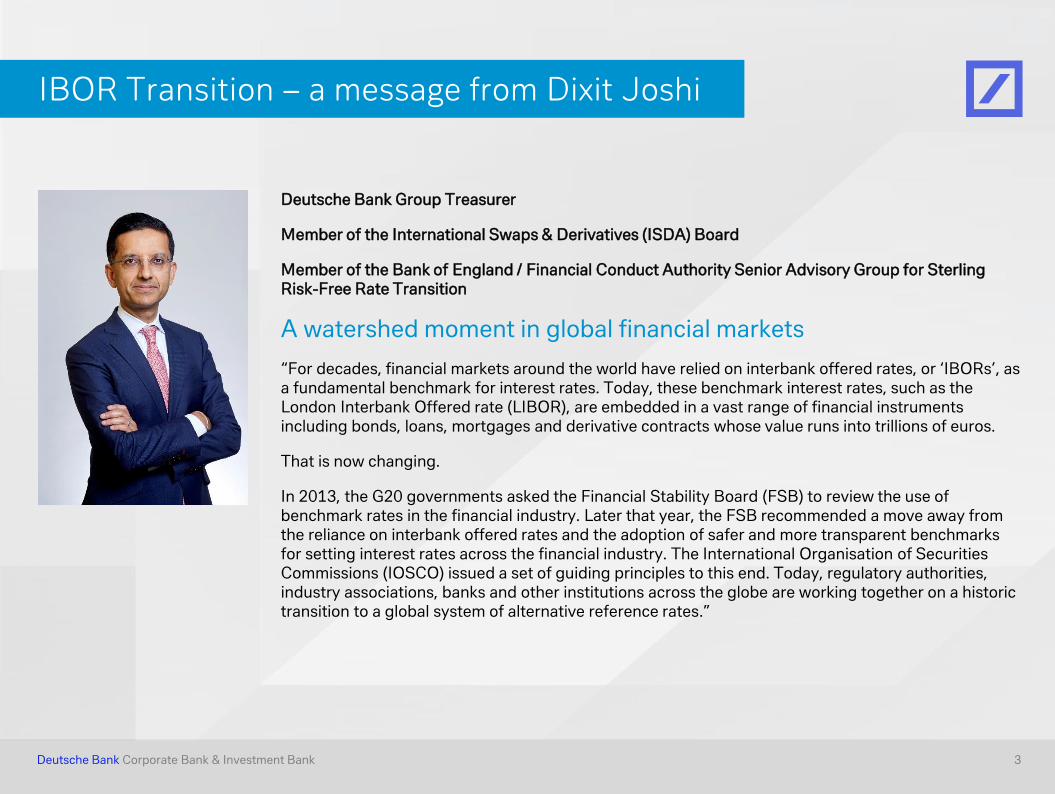

Deutsche Bank Group Treasurer

Member of the International Swaps & Derivatives (ISDA) Board

Member of the Bank of England / Financial Conduct Authority Senior Advisory Group for Sterling Risk-Free Rate Transition

A watershed moment in global financial markets

“For decades, financial markets around the world have relied on interbank offered rates, or ‘IBORs’, as a fundamental benchmark for interest rates. Today, these benchmark interest rates, such as the London Interbank Offered rate (LIBOR), are embedded in a vast range of financial instruments including bonds, loans, mortgages and derivative contracts whose value runs into trillions of euros.

That is now changing.

In 2013, the G20 governments asked the Financial Stability Board (FSB) to review the use of benchmark rates in the financial industry. Later that year, the FSB recommended a move away from the reliance on interbank offered rates and the adoption of safer and more transparent benchmarks for setting interest rates across the financial industry. The International Organisation of Securities Commissions (IOSCO) issued a set of guiding principles to this end. Today, regulatory authorities, industry associations, banks and other institutions across the globe are working together on a historic transition to a global system of alternative reference rates.”

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 4

Supporting you through the transition

Our priority is to continue to provide

products and services to you, our

clients, and to support required

changes to legal documentation in

respect of an orderly transition.

This guide is intended to supplement

any conversations that you have with

your Deutsche Bank representative as

you prepare for benchmark reform.

We greatly value your business and

look forward to developing our

dialogue with you to ensure our

partnership continues to thrive as we

transition to new reference rates.

This transition to new risk-free rates will bring important benefits for all participants in financial markets. However, significant work will be required to ensure a smooth transition and to safeguard the interests of all parties at this time of change.

As a large global bank, Deutsche Bank is committed to serving our clients and to playing our role in the wider financial system as we navigate this change together. We have committed significant resources to the task. The Group’s priority is to engage with and support our clients through all aspects of this transition.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 5

The facts – what you need to know

What is IBOR Transition?

Due to widespread concerns about the sustainability of LIBOR and similar rates, regulators and the wider financial services industry have been developing and identifying alternative reference rates to strengthen existing benchmarks. Across the globe, central banks have convened committees and industry working groups to bring together private-sector market participants to identify and promote the use of robust, transaction-based reference or Risk-Free Rates (RFRs) as alternatives to Interbank Offered Rates (IBORs), such as LIBOR and EURIBOR.

What is Benchmark Reform?

EU Benchmarks Regulation (EU BMR) came into full force on 1 January 2018, calling for a common framework across the industry. Itis aimed at ensuring the integrity of benchmarks used in financial contracts, financial instruments and where used to measure performance of investment funds in the EU. It also requires that more robust fallback language exists in all relevant contracts and agreements. The purpose of a fallback is to define the steps that will be taken to identify and agree an alternative benchmark in the event that the original benchmark ceases to be available or materially changes and what happens if an alternative cannot be agreed. EU BMR impacts any client of an EU supervised entity no matter where they are located globally.

What you will need to consider

When entering into new transactions referencing benchmark rates the following should be considered: the risks and benefits of using a particular benchmark and an understanding of the consequences if such a benchmark is changed or discontinued; and for existing transactions, you should also consider whether you have suitable contingency plans in place such as appropriate fallback language and your strategy to transition from IBOR to a new RFR.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 6

Key factors of each IBOR and risk-free reference rate

Current Benchmarks Alternative Risk-Free Rates

Jurisdiction Benchmark IR AdministratorAlternative RFR

Alternative RFR Administrator

Transaction based?

Overnight rate?

Secured/ Unsecured

Underlying Transactions

Rates Published

EU

EONIAEuropean MoneyMarkets Institute

(EMMI)

€STR(euro short-term rate)

European Central Bank (ECB)

Yes

Yes (€STR)

UnsecuredMoney

Markets

October 2019

(€STR)EURIBOR

Reformed EURIBOR

European Money Markets Institute

(EMMI)Partly

UK

GBP LIBORICE Benchmark

Administration (IBA)

SONIA(reformed sterling

overnight index Average)

Bank of England Yes Yes UnsecuredMoney

Markets23 April

2018

US

USD LIBORICE Benchmark

Administration (IBA)

SOFR(secured overnight

financing rate)

Federal Reserve Bank

of New York (FRBNY)Yes Yes Secured

Repo Transactions

3 April 2018

Switzerland

CHF LIBORICE Benchmark

Administration (IBA)

SARON(Swiss average rate overnight)

Swiss National Bank(SNB)

and SIX Swiss Exchange

Yes Yes SecuredRepo

Transactions25 August

2009

Japan

JBA TIBORJBA TIBOR

AdministrationTONA Bank of Japan

Yes

Yes UnsecuredMoney

MarketsJuly 1985

EUROYEN TIBOR

JPY LIBORICE Benchmark

Administration (IBA)Yes

Note: The above table represents the key rates. Additional rates may also be impacted. Source: Deutsche Bank and gfma www.gfma.org as at 2 April 2019

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 7

Summarising the changes

What is changing?

– Authorities around the world are now driving initiatives to reduce the financial system’s dependence on IBORs and to transition to alternative RFRs.

– Deutsche Bank is a committed supporter of alternative reference rate initiatives for benchmark reform, serving as a member of relevant central bank and industry groups since their inception.

– Alternative RFRs are based on robust, highly liquid underlying markets and on actual transactions rather than expert judgement.

– Deutsche Bank will work with you to bilaterally agree the required changes to legal documentation and to transition contracts to RFRs.

Why the change?

– The drive for reform reflects several concerns around reliance on IBOR. One is potential systemic risk. This arises from the shrinking of underlying markets on which IBORs are based relative to the huge volume of transactions which rely on them.

– Transaction volumes in unsecured interbank markets are very low, so banks are making IBOR submissions based partly on ‘expertjudgement’ rather than actual transactions.

– There are key dependencies such as: (1) development of the new RFRs and creation of term versions; and (2) the timing and sequencing of transition and the repapering of existing contracts.

Who will be affected

and how?

– The transition to alternative RFRs will affect individuals, companies and institutions who use a huge variety of financial services which rely on IBORs as a reference rate.

– There is a risk that if a benchmark’s methodology is changed in order to comply with regulation, then it may perform differently.

– If a financial product references an affected benchmark then any changes to the benchmark including its discontinuation, may affect the economics and viability of the product.

– Terms and conditions of financial products typically contain fallback provisions, which identify how a successor or substitute rate will be selected if LIBOR, EURIBOR, EONIA or a similar benchmark is not published. There is a risk that fallback terms do not adequately cater for the circumstances in which they need to be used.

When are the

timings?

– Regulatory authorities in major jurisdictions around the world have signalled their aim to substantially complete the transition process by the end of 2021.

– Andrew Bailey, Chairman of the UK Financial Conduct Authority (FCA), has announced that the FCA would no longer compel banks to make LIBOR submissions from the end of 2021, adding that from that point on, ‘the survival of LIBOR could not and would not be guaranteed.’

– For legal documentation upgrades, we will begin reaching out to our clients in a phased approach from Q4 2019. The initial focus will be on updating the fallback provisions in master agreements and contracts.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 8

Key market events

2012

2021

2013 2014 2015

201620172018

Large UK investment bank fined for

manipulation of LIBORand EURIBOR rates

G20 asks the Financial Stability Board (FSB) to review and reform major interest rate benchmarks

FSB Official Sector Steering Group (OSSG) publishes a report recommending a “multiple-rate” approach with reformed

and more robust reference rates

Jun 2012 Feb 2013 Jul 2014

FCA’s Andrew Bailey states that after 2021 “the survival of LIBOR on

the current basis…could not and would not be guaranteed”

Jul 2017

EU Benchmarks Regulation

published in the official journal

Jun 2016

LIBOR submissions

no longer guaranteed

Jan 2022

EU Benchmarks Regulation comes into force. Benchmark users must observe compliance with governance and control obligations as

well as ensuring that any ‘benchmarks’ themselves comply with the BMR

Jan 2018

2019ISDA LIBOR

protocol anticipated to be available for use

Q4 2019

Under EU BMR, non-

compliant European non-

critical benchmarks can no

longer be used in the EU

Jan 2020

Under EU BMR, non-compliant

Third Country and Critical

benchmarks can no longer be

used in the EU

ISDA Benchmark Supplement Protocol

publishedDec

2018

Source: Deutsche Bank as at 11 September 2019

September 2019

future

20222020

The Alternative Reference Rates Committee (ARRC) recommended fallback language for

Floating Rate Notes, Syndicated Loans, Bilateral Business Loans and Securitisations

Q2 2019

past

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 9

Deutsche Bank support

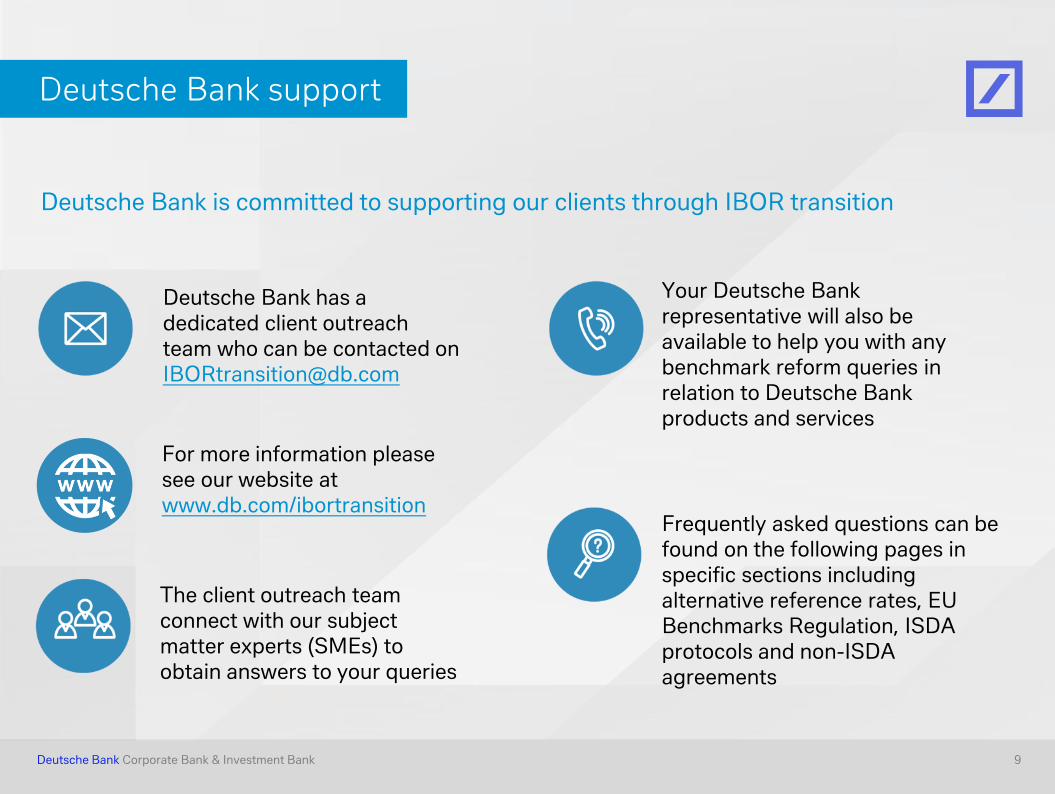

The client outreach team connect with our subject matter experts (SMEs) to obtain answers to your queries

Deutsche Bank has a dedicated client outreach team who can be contacted on [email protected]

Your Deutsche Bank representative will also be available to help you with any benchmark reform queries in relation to Deutsche Bank products and services

Frequently asked questions can be found on the following pages in specific sections including alternative reference rates, EU Benchmarks Regulation, ISDA protocols and non-ISDA agreements

Deutsche Bank is committed to supporting our clients through IBOR transition

For more information please see our website at www.db.com/ibortransition

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 10

?

Frequently asked questions General (1/4)

Why are benchmarks being reformed?The G20 asked the Financial Stability Board (FSB) in 2013 to review and recommend reforming major interest rate benchmarks. In 2014 the FSB published its recommendations, which were composed of two pillars: (1) reforming LIBOR (and equivalents) to ensure they are as reflective of underlying market conditions and anchored in transactions as far as possible; and (2) developing alternative near risk free rates for use where neither term nor bank credit properties are required.

What is European Benchmarks Regulation (EU BMR)?The EU BMR, which came into full force on 1 January 2018, introduces a common framework governing administration, contribution and usage of benchmarks within the European Economic Area (EEA). It is aimed at ensuring the integrity of benchmarks used in financial contracts, financial instruments, or used to measure performance of investment funds in the EU.

It also requires that more robust fallback language exists in all relevant contracts and agreements. The purpose of fallbacks is to define the steps that will be taken to identify and agree an alternative benchmark in the event that the original benchmark ceases to be available or materially changes and what happens if an alternative cannot be agreed.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 11

?

Frequently asked questions General (2/4)

What is the situation with LIBOR?The London Inter-bank Offered Rate (LIBOR) is an interest rate average calculated from estimates submitted by a panel of banks in London. LIBOR rates are calculated for five currencies and seven maturities ranging from overnight to 12 months and are administered by ICE Benchmark Administration (IBA), and regulated by the Financial Conduct Authority (FCA).

In a 2017 speech by the Chief Executive of the FCA Andrew Bailey highlighted the risks of permanent LIBOR discontinuation and stated that the FCA would no longer compel the panel banks to submit LIBOR beyond 2021.

Global regulators, working groups and committee have selected alternative reference rates which are based on transaction data rather than submissions. Regulators, banks, industry bodies and trade associations are working together to replace thee interbank interest rate benchmarks with the alternative risk-free rates.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 12

?

Frequently asked questions General (3/4)

What is the situation with EURIBOR?The Euro Interbank Offered Rate (EURIBOR) is a daily reference rate derived from quote submissions from a panel of banks. It is administered by the European Money Markets Institute (EMMI) and is based on the averaged interest rates at which Eurozone banks offer to lend unsecured funds to other banks in the interbank market.

Over the past few years EMMI has been developing a plan to gradually reform the existing benchmark in order to anchor it to transactions instead of quotes. The reformed hybrid EURIBOR methodology is deemed compliant with the EU BMR and EMMI has stated that the hybrid methodology will be implemented by the end of 2019.

What is the situation with EONIA?The current Eurozone risk-free reference rate is EONIA which is the daily weighted average of overnight rates for unsecured interbank lending in the euro-zone. Under its current construct, it has been deemed non-compliant with EU BMR and with no plans to change the underlying methodology, its use will not be permitted beyond the end of 2021 (extended from 1 January 2020 as it is classed as a critical benchmark).

In 2018 the euro working group recommended the euro short-term rate (€STR) as the alternative euro risk-free rate and replacement for EONIA. The rate is administered by the ECB and is due to be published by October 2019.

If you have a CSA (Credit Support Annex) in place with Deutsche Bank that references EONIA as the EUR cash collateral remuneration rate, then the terms of this agreement will need to be amended in order to remove references to EONIA, and replace them with €STR, before EONIA is discontinued at the end of 2021.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 13

?

Frequently asked questions General (4/4)

What is the difference between secured and unsecured?Secured risk-free rates are based on underlying financial transactions where the securities are collateralized by an asset. Unsecured transactions are not secured by a specific asset and therefore generally represent a higher risk.

Why are some RFRs secured and others unsecured?Choices between unsecured and secured overnight RFRs have to a large extent been made on the basis of the liquidity and structural features of underlying money markets. Each administrator has chosen secured or unsecured rates which are suitable for the market they are representing.

Will term rates be developed? The alternative risk free rates that have been chosen are based on a backward looking overnight calculation methodology. LIBOR however, is a forward looking term rate, with an embedded credit spread.

The FSB have indicated that the use of term rates should be limited for use in products only where necessary. The sterling working group consultation on term rates notes that corporate lending markets, securitizations, FRNs and retail loans/mortgages are likely to have a demand for such rates. The forward looking distinction is important, as backward looking term RFR rates can be derived by compounding the overnight rate over the term (indeed this is ISDAs fallback methodology for the term calculation) however this would mean that payments would only be known at the end of the period.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 14

?

Frequently asked questions ISDA Benchmarks Supplement

What is the ISDA Benchmarks Supplement?The ISDA Benchmarks Supplement enables parties to update ISDA master agreements to include certain triggers and generic fallbacks in transactions (OTC derivatives) which reference benchmarks. The Supplement was written in the context of the EU BMR (Article 28(2)) which requires robust fallback language to be included in all contracts referencing benchmarks. The market is anticipating an ISDA IBOR Fallback Protocol later this year, which would supersede the ISDA Benchmarks Supplement Protocol.

What is Deutsche Bank’s approach?Deutsche Bank has adhered to the ISDA Benchmark Supplements protocol and will be electing for new transactions only. At this stage we are not able to adhere in respect of legacy trades due to the lack of clarity about whether to do so would trigger mandatory clearing and margining requirements. We are waiting for regulators to provide clarity on that issue, which would then enable us to reconsider whether to adhere in respect of legacy transactions also.

Where can I find further information relating to this protocol?– ISDA Benchmarks Supplement & ISDA Benchmarks Supplement FAQs

– ISDA Benchmarks Supplement Protocol & Protocol FAQs

– ISDA Benchmarks Supplement How to Adhere: Step-by-Step instructions

– What is an ISDA protocol?

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 15

?

Frequently asked questions Non-ISDA agreements and contracts

What about transactions not conducted under an ISDA master agreement?For Deutsche Bank’s Corporate Bank and Investment Bank, EU BMR covers derivatives, Deutsche Bank Issuance and UCITs. Deutsche Bank Issuance and UCITs have newly drafted fallbacks to incorporate into new issuance documentation.

Non-ISDA agreements and contracts also need to be updated with more robust fallback language similar to ISDA master agreements, however the mechanism to do this is more bespoke.

In addition, there are derivative contracts entered into outside of a Master Agreement –these are known as long form confirmations and the terms that would otherwise be included within the Master Agreement are to be found within the confirmation itself.

Deutsche Bank will outreach to its clients in due to course to begin the process of updating the agreements and contracts. Clients may also contact Deutsche Bank at [email protected] if they would like to discuss their contracts.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 16

?

Frequently asked questions Regional – US

What is the ARRC?In the U.S. in 2014, the Fed & New York Fed established the Alternative Reference Rates Committee (ARRC) to lead the transition away from LIBOR. The ARRC continues to lead the transition from LIBOR to SOFR – as well as encourage the development of the SOFR futures market – and its Paced Transition Plan for a smooth transition away from LIBOR is ahead of schedule.

What is SOFR?The ARRC selected SOFR as the recommended alternative reference rate for the US. While LIBOR is not fully transaction based, SOFR is based on the overnight repo markets with ~ $1 trillion of transactions per day. SOFR is fully secured (no credit risk).

How is SOFR Calculated?SOFR is calculated as a volume-weighted median of transaction level tri-party repo data from the Bank of New York Mellon, GCF Repo transaction data, and data on bilateral Treasury repo transactions cleared through FICC’s DVP service (from DTCC Solutions). SOFR is published each business day on the New York Fed’s website at 8 AM.

How is the Market Uptake of SOFR?As of June 2019, 27 institutions have issued more than $136 billion notional in floating rate securities tied to SOFR, with a record $24 billion in June. Outstanding SOFR-linked notional across all products has grown from under $100 billion in May 2018 to over $9 trillion as of April 2019, an increase of 9,000%.

Source: https://apps.newyorkfed.org/markets/autorates/sofr as at 1st August 2019

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 17

?

Frequently asked questions Regional – Asia Pacific

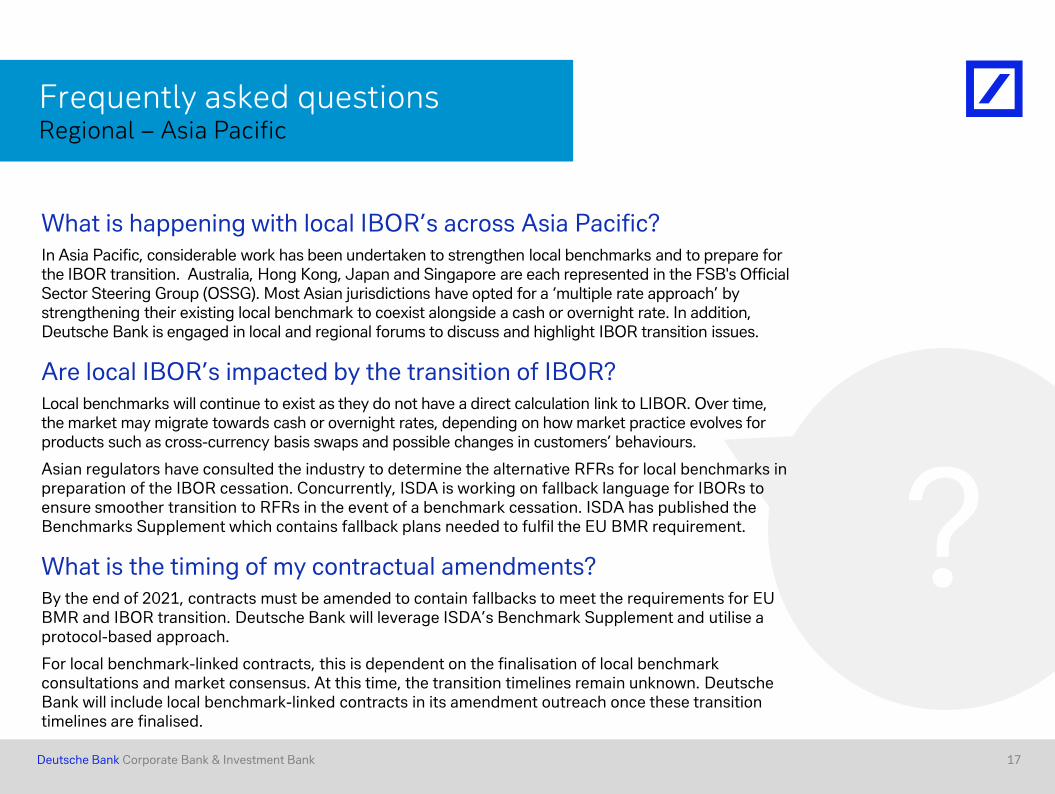

What is happening with local IBOR’s across Asia Pacific?In Asia Pacific, considerable work has been undertaken to strengthen local benchmarks and to prepare for the IBOR transition. Australia, Hong Kong, Japan and Singapore are each represented in the FSB's Official Sector Steering Group (OSSG). Most Asian jurisdictions have opted for a ‘multiple rate approach’ by strengthening their existing local benchmark to coexist alongside a cash or overnight rate. In addition, Deutsche Bank is engaged in local and regional forums to discuss and highlight IBOR transition issues.

Are local IBOR’s impacted by the transition of IBOR?Local benchmarks will continue to exist as they do not have a direct calculation link to LIBOR. Over time, the market may migrate towards cash or overnight rates, depending on how market practice evolves for products such as cross-currency basis swaps and possible changes in customers’ behaviours.

Asian regulators have consulted the industry to determine the alternative RFRs for local benchmarks in preparation of the IBOR cessation. Concurrently, ISDA is working on fallback language for IBORs to ensure smoother transition to RFRs in the event of a benchmark cessation. ISDA has published the Benchmarks Supplement which contains fallback plans needed to fulfil the EU BMR requirement.

What is the timing of my contractual amendments?By the end of 2021, contracts must be amended to contain fallbacks to meet the requirements for EU BMR and IBOR transition. Deutsche Bank will leverage ISDA’s Benchmark Supplement and utilise a protocol-based approach.

For local benchmark-linked contracts, this is dependent on the finalisation of local benchmark consultations and market consensus. At this time, the transition timelines remain unknown. Deutsche Bank will include local benchmark-linked contracts in its amendment outreach once these transition timelines are finalised.

81nidZpGqzkSDMpD

Deutsche Bank Corporate Bank & Investment Bank 18

Disclaimer

IMPORTANT NOTICE

These materials have been prepared by Deutsche Bank or one of its subsidiaries, affiliates or branches, solely for the benefit of the recipient (the “Recipient”) and are being provided for information purposes only, to assist the Recipient to evaluate the matter to which these materials relate. By accepting these materials, the Recipient agrees to use them only for such purpose and to be bound by the following limitations

These materials speak only as of their date of publication and may not be complete or up to date. The views expressed herein are subject to change and do not represent a formal or official view of Deutsche Bank and shall not be deemed to be an assurance or guarantee as to expected results of any transaction.

Neither Deutsche Bank nor any of its affiliates has acted or is acting (and does not purport to act in any way) in a fiduciary capacity. Information provided in these materials does not create any legally binding obligations on Deutsche Bank. Nothing herein should be construed as financial, legal, regulatory, tax, accounting,, investment advice (within the definition set out in Directive 2014/65/EU (“MiFID”)) or other specialist advice or as an offer, invitation, solicitation, inducement or recommendation of securities or other financial products, and is not personalised or in any way tailored to reflect the Recipient’s particular investment objectives, financial situation or needs. Nothing herein constitutes a recommendation or endorsement by DB of any investment, trading strategy or algorithm and should not be relied upon by the Recipient to make a determination as to whether or not to invest or to use any strategy or algorithm. The Recipient should obtain independent financial advice that addresses its particular investment objectives, financial situation and needs before making investment decisions.

These materials have been provided on the basis that the Recipient and its representatives, directors, officers, employees and advisers keep these materials (and any other information that may be provided to the Recipient) confidential and the contents of this document and any information provided herein should not be further distributed or duplicated in whole or in part by any means without the prior written consent of Deutsche Bank. Deutsche Bank shall not be liable for any errors or omissions contained in the information contained herein or for any loss or for any damages (incidental, consequential or otherwise) which may arise from reliance by the Recipient any third party on such information.