Housing: What's Next?

25

Housing: What’s Next New College of Florida April 18, 2012 David Crowe Chief Economist

-

Upload

global-interdependence-center -

Category

Documents

-

view

224 -

download

1

description

David Crowe's Presentation at GIC and New College "Housing: What's Next?" Conference

Transcript of Housing: What's Next?

Housing: What’s Next

New College of Florida

April 18, 2012

David Crowe

Chief Economist

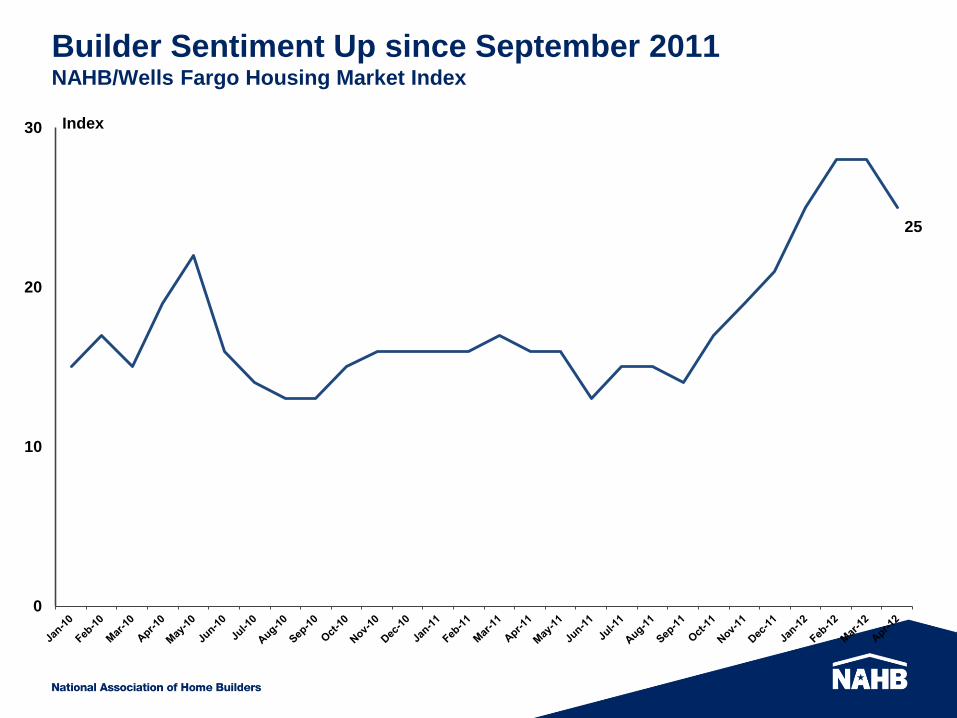

Builder Sentiment Up since September 2011 NAHB/Wells Fargo Housing Market Index

25

0

10

20

30 Index

What Else?

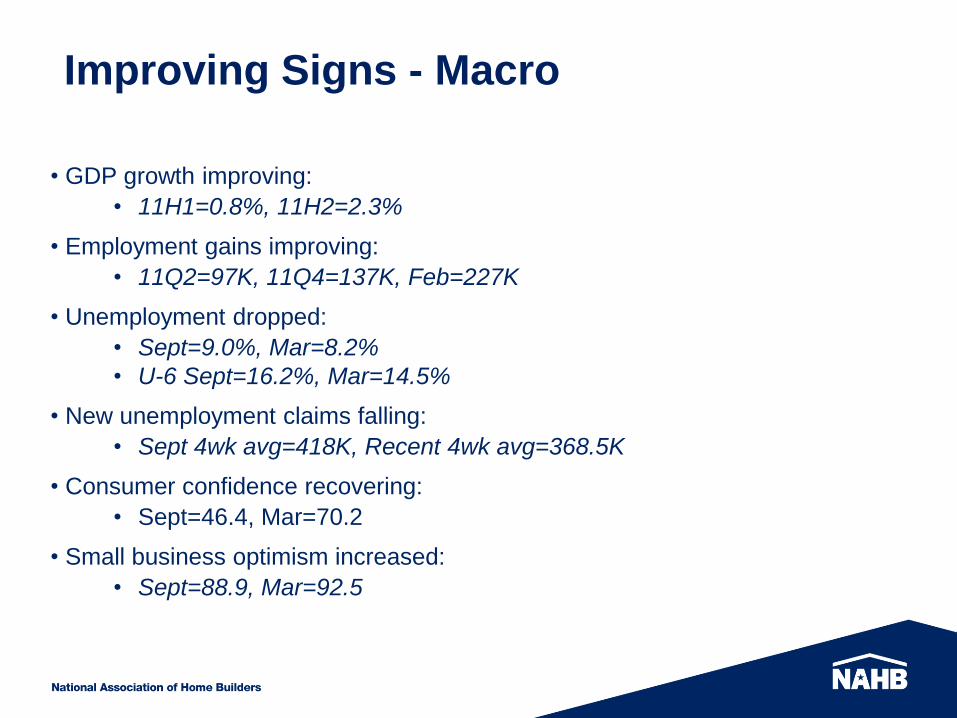

• GDP growth improving:

• 11H1=0.8%, 11H2=2.3%

• Employment gains improving:

• 11Q2=97K, 11Q4=137K, Feb=227K

• Unemployment dropped:

• Sept=9.0%, Mar=8.2%

• U-6 Sept=16.2%, Mar=14.5%

• New unemployment claims falling:

• Sept 4wk avg=418K, Recent 4wk avg=368.5K

• Consumer confidence recovering:

• Sept=46.4, Mar=70.2

• Small business optimism increased:

• Sept=88.9, Mar=92.5

Improving Signs - Macro

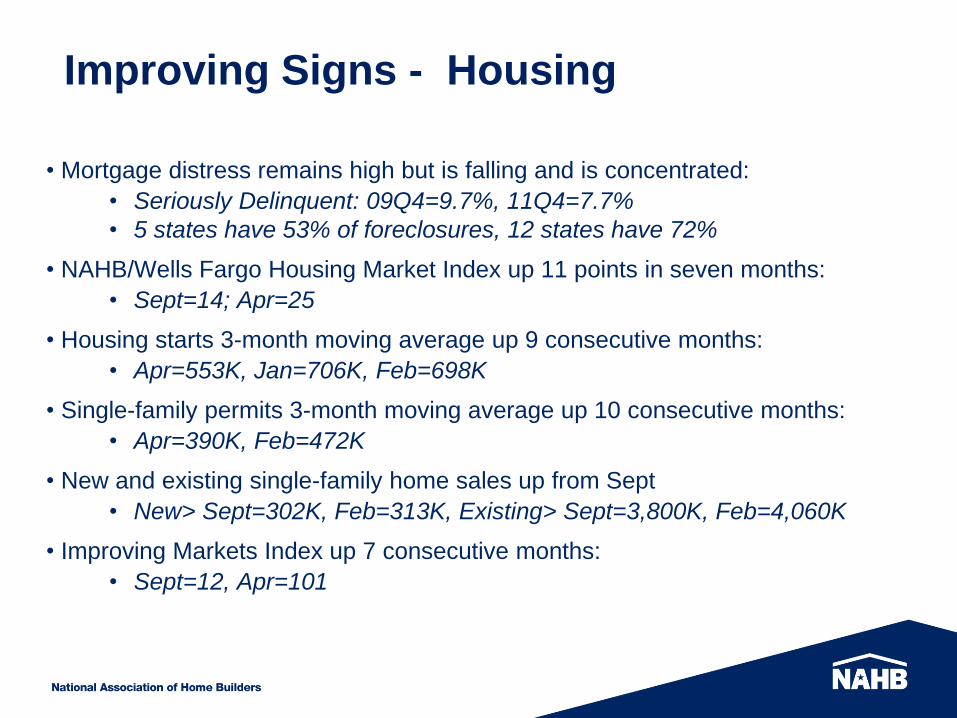

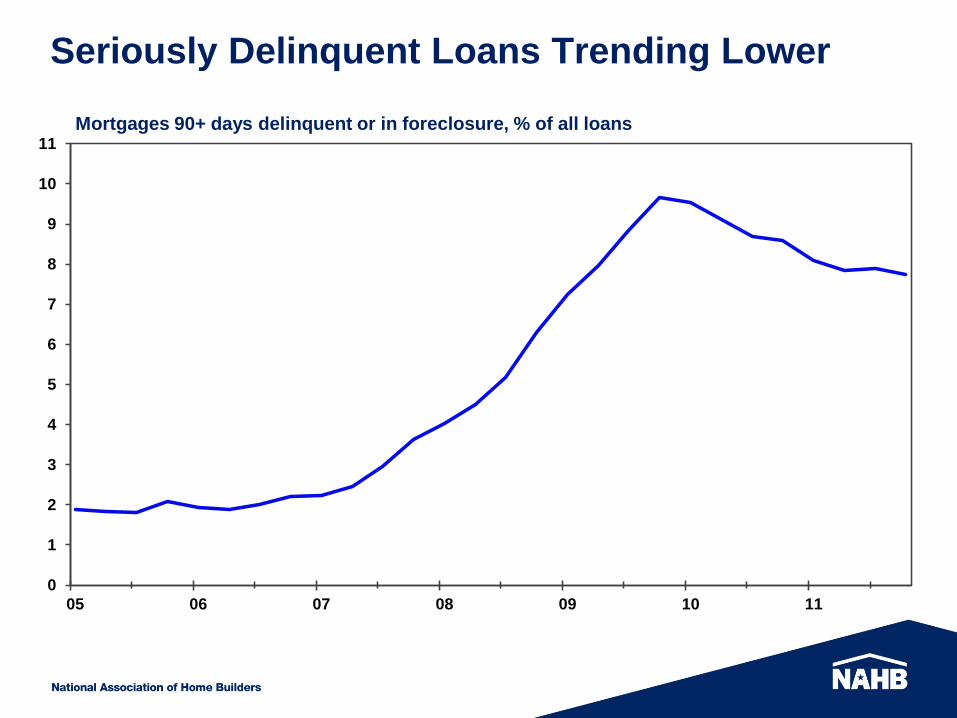

• Mortgage distress remains high but is falling and is concentrated:

• Seriously Delinquent: 09Q4=9.7%, 11Q4=7.7%

• 5 states have 53% of foreclosures, 12 states have 72%

• NAHB/Wells Fargo Housing Market Index up 11 points in seven months:

• Sept=14; Apr=25

• Housing starts 3-month moving average up 9 consecutive months:

• Apr=553K, Jan=706K, Feb=698K

• Single-family permits 3-month moving average up 10 consecutive months:

• Apr=390K, Feb=472K

• New and existing single-family home sales up from Sept

• New> Sept=302K, Feb=313K, Existing> Sept=3,800K, Feb=4,060K

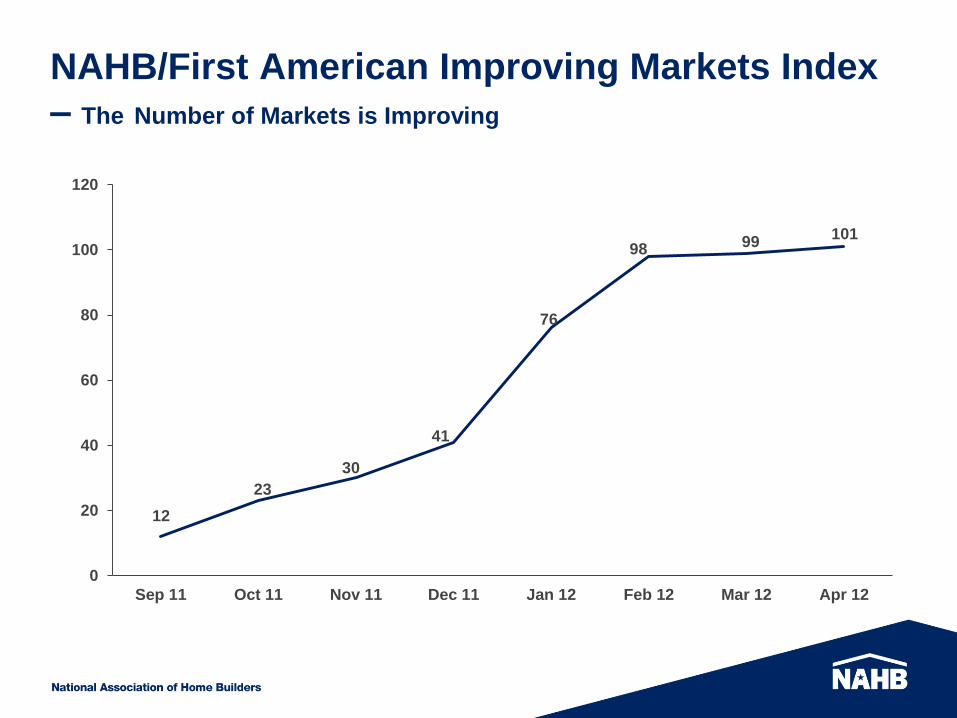

• Improving Markets Index up 7 consecutive months:

• Sept=12, Apr=101

Improving Signs - Housing

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

103

104

105

106

107

108

109

110

111

112

113

114

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

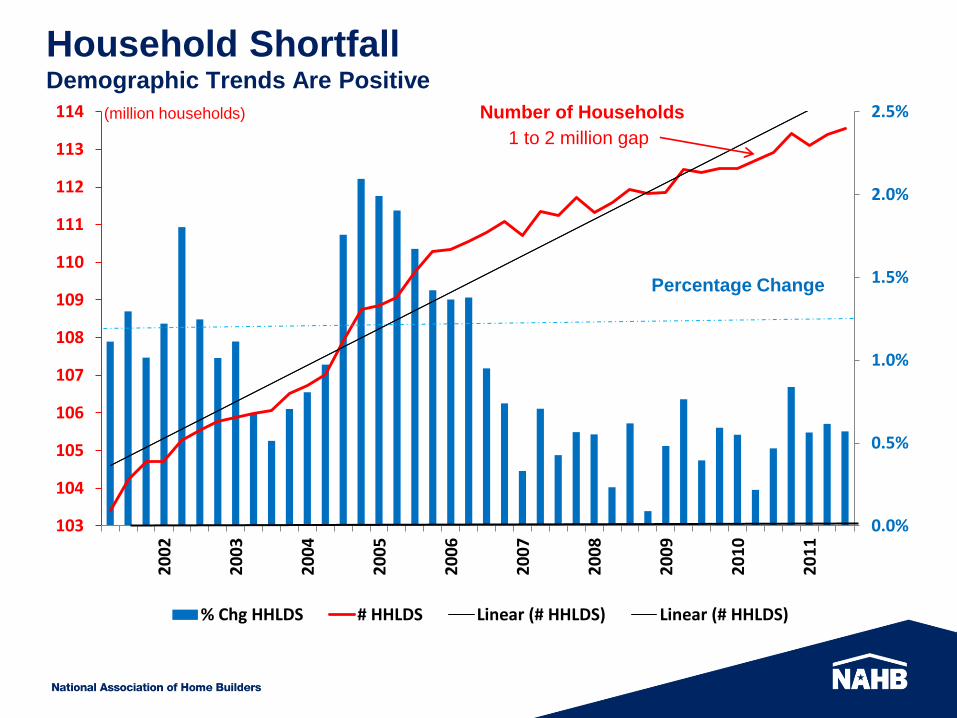

% Chg HHLDS # HHLDS Linear (# HHLDS) Linear (# HHLDS)

Number of Households

Percentage Change

(million households)

1 to 2 million gap

Household Shortfall Demographic Trends Are Positive

Housing Fundamentals Remain Good Mortgage Rates

5.2

0

2

4

6

8

10

12

14

16

18

20

78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Percent

Fixed-Rate

Adjustable-Rate

3.2

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

U.S.

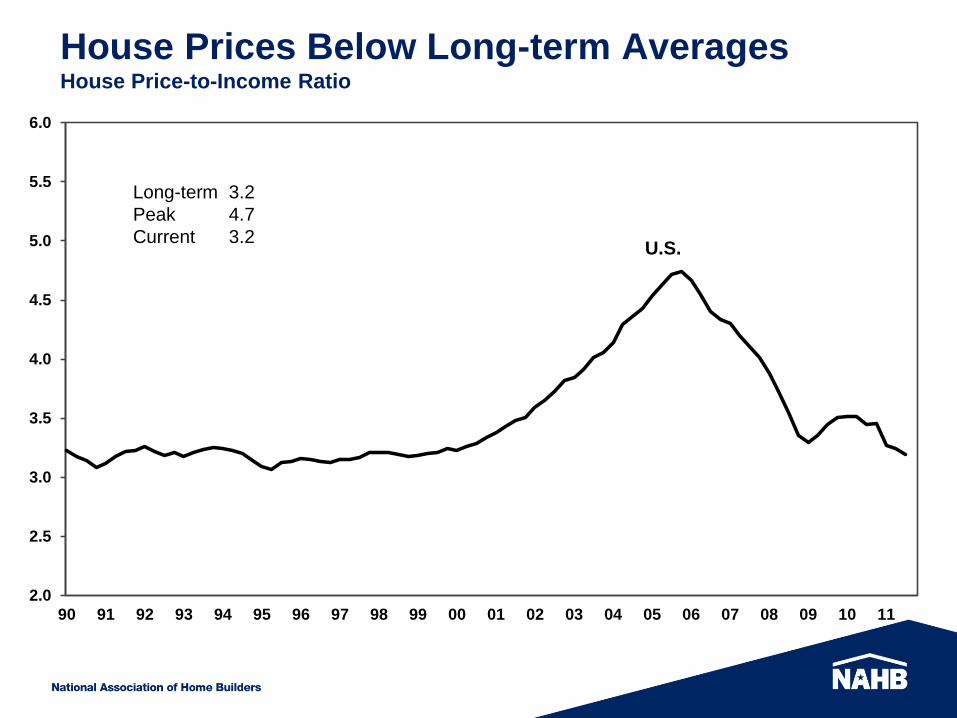

House Prices Below Long-term Averages House Price-to-Income Ratio

Long-term 3.2

Peak 4.7

Current 3.2

Seriously Delinquent Loans Trending Lower

0

1

2

3

4

5

6

7

8

9

10

11

05 06 07 08 09 10 11

Mortgages 90+ days delinquent or in foreclosure, % of all loans

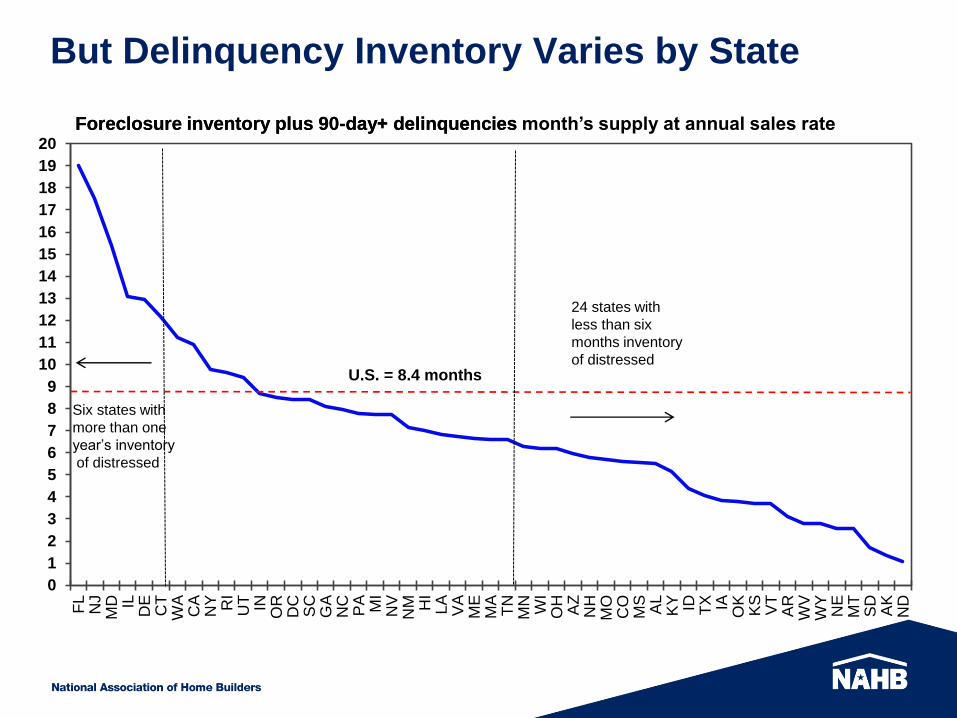

But Delinquency Inventory Varies by State

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

FL

NJ

MD IL

DE

CT

WA

CA

NY RI

UT IN

OR

DC

SC

GA

NC

PA MI

NV

NM HI

LA

VA

ME

MA

TN

MN

WI

OH

AZ

NH

MO

CO

MS

AL

KY ID TX IA

OK

KS

VT

AR

WV

WY

NE

MT

SD

AK

ND

Six states with

more than one

year’s inventory

of distressed

24 states with

less than six

months inventory

of distressed

Foreclosure inventory plus 90-day+ delinquencies

U.S. = 8.4 months

Foreclosure inventory plus 90-day+ delinquencies month’s supply at annual sales rate

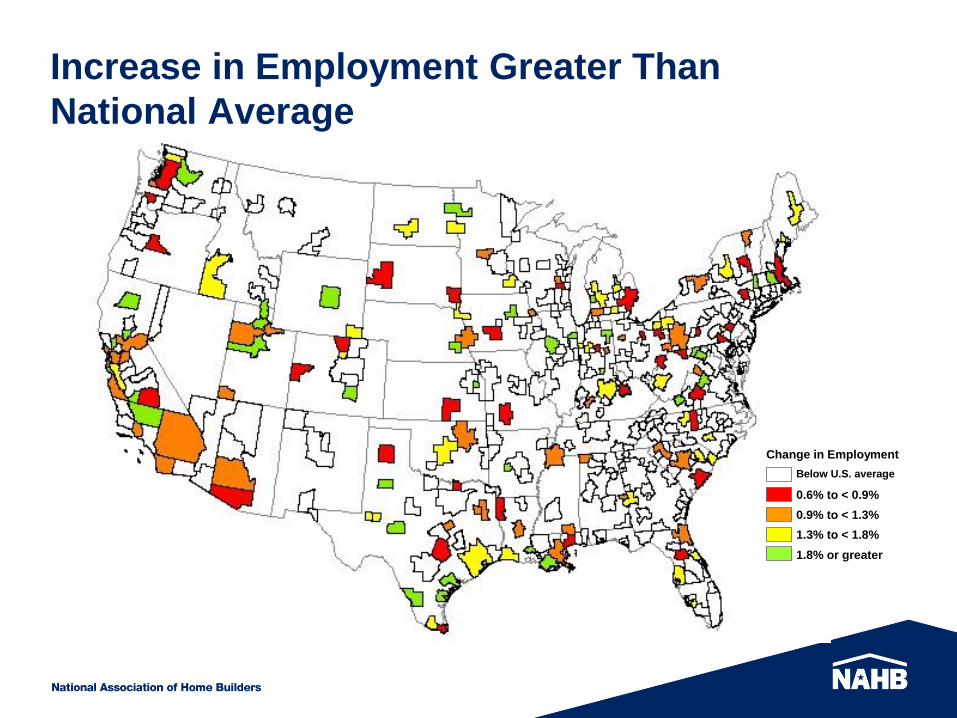

Markets Are Local

Increase in Employment Greater Than

National Average

Change in Employment

Below U.S. average

0.6% to < 0.9%

0.9% to < 1.3%

1.3% to < 1.8%

1.8% or greater

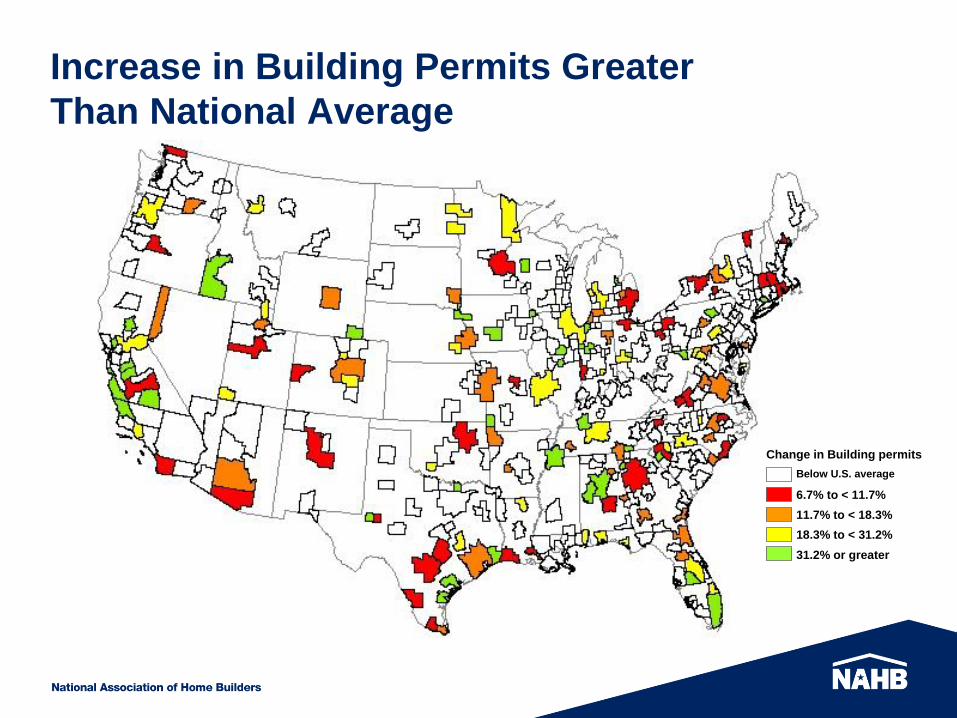

Increase in Building Permits Greater

Than National Average

Change in Building permits

Below U.S. average

6.7% to < 11.7%

11.7% to < 18.3%

18.3% to < 31.2%

31.2% or greater

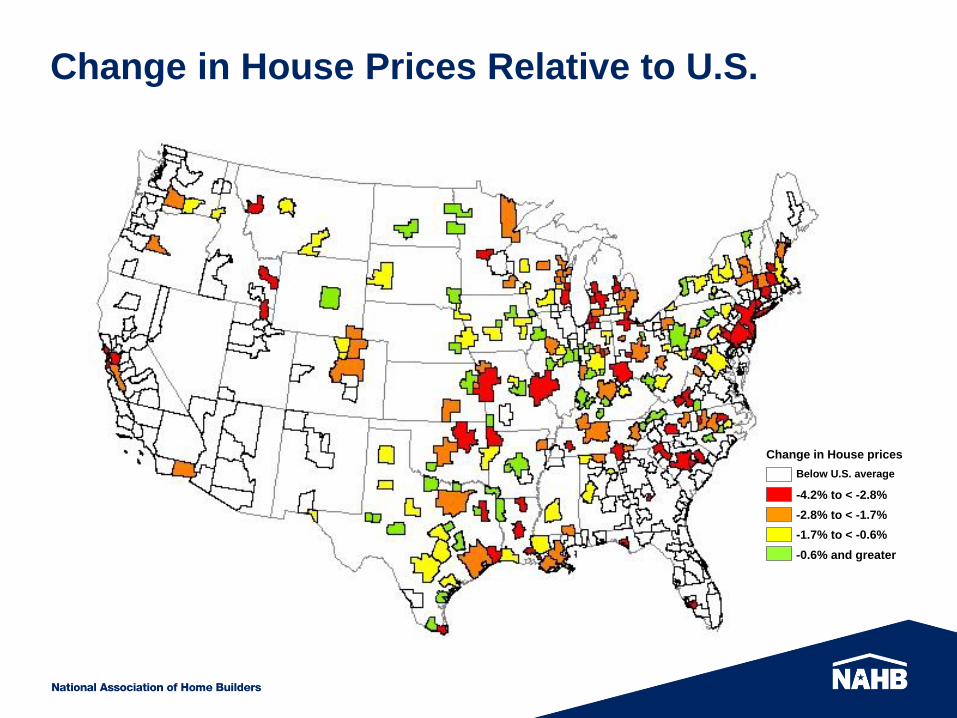

Change in House Prices Relative to U.S.

Change in House prices

Below U.S. average

-4.2% to < -2.8%

-2.8% to < -1.7%

-1.7% to < -0.6%

-0.6% and greater

NAHB/First American Improving Markets Index

– The Number of Markets is Improving

12

23

30

41

76

98 99 101

0

20

40

60

80

100

120

Sep 11 Oct 11 Nov 11 Dec 11 Jan 12 Feb 12 Mar 12 Apr 12

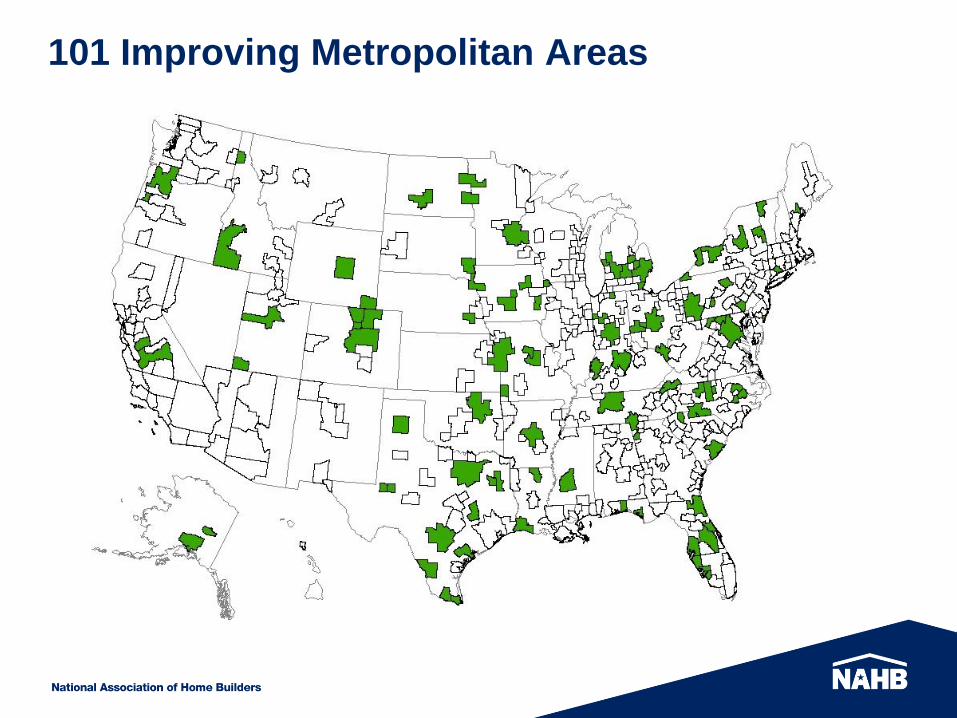

AR Little Rock FL Tampa MD Cumberland NC Charlotte OH Springfield TX College Station

CA Fresno GA Rome Hagerstown Goldsboro OK Tulsa Dallas

CA Merced IA Ames ME Lewiston Greensboro OR Corvallis Laredo

CO Boulder Des Moines MI Detroit Greenville OR Portland Longview

Denver Dubuque Flint Rocky Mount PA Altoona McAllen

Fort Collins Iowa City Grand Rapids Winston-Salem Erie Midland

Greeley Sioux City Lansing ND Bismarck Lancaster Odessa

CT New Haven Waterloo Monroe Fargo Pittsburgh San Antonio

DC Washington ID Boise City Muskegon Grand Forks Williamsport Tyler

FL Cape Coral Coeur d’Alene Saginaw NE Lincoln SC Charleston Victoria

Crestview IN Elkhart MN Minneapolis NJ Ocean City Spartanburg UT Provo

Deltona Evansville MO Columbia NY Buffalo SD Sioux Falls St. George

Jacksonville Indianapolis Jefferson City Glens Falls TN Chattanooga VT Burlington

North Port Lafayette Joplin Rochester Kingsport WV Huntington

Orlando KY Louisville Kansas City Utica Nashville WY Casper

Panama City LA Lake Charles MS Jackson OH Columbus TX Amarillo Cheyenne

Punta Gorda

Monroe NC Burlington Dayton Brownsville

101 Improving Metropolitan Areas

Improving Markets 101 Improving Metropolitan Areas

Forecast

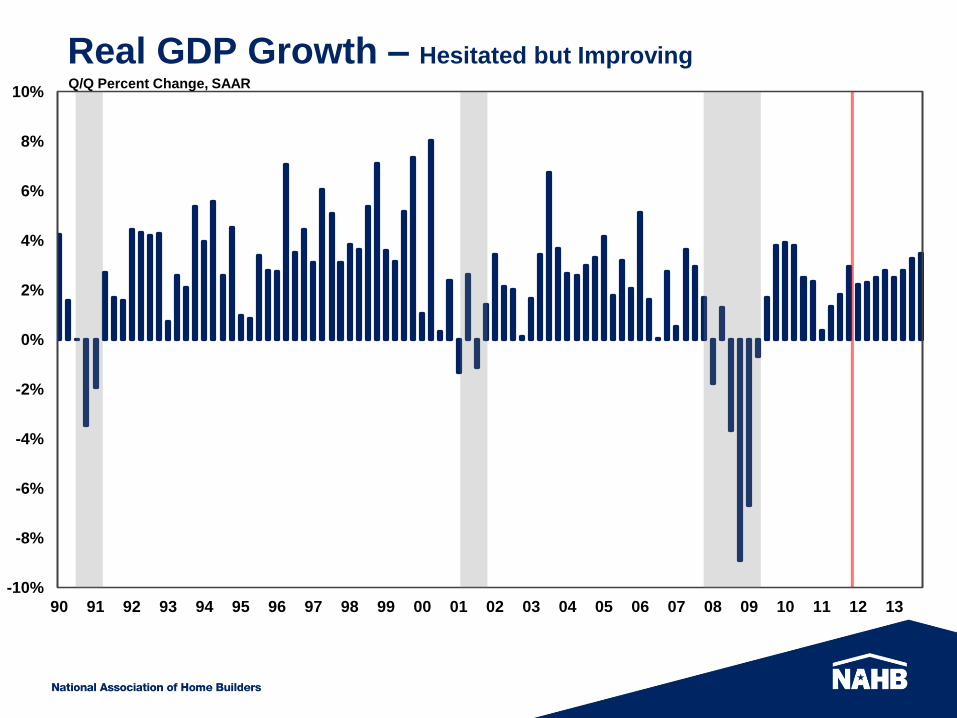

Real GDP Growth – Hesitated but Improving

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Q/Q Percent Change, SAAR

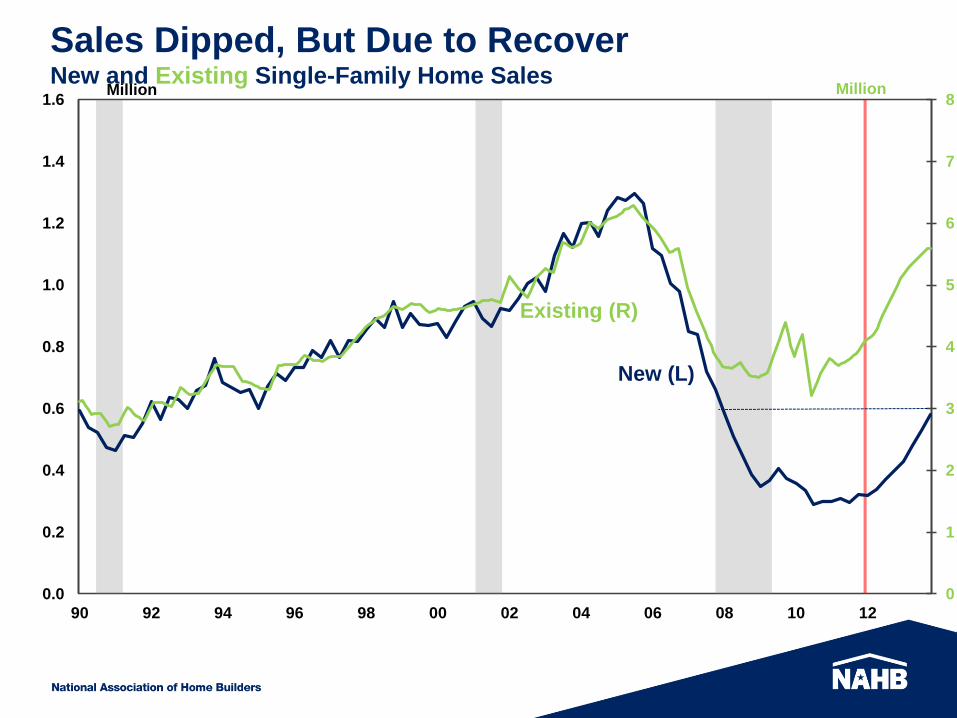

Sales Dipped, But Due to Recover New and Existing Single-Family Home Sales

0

1

2

3

4

5

6

7

8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

90 92 94 96 98 00 02 04 06 08 10 12

Million

Existing (R)

New (L)

Million

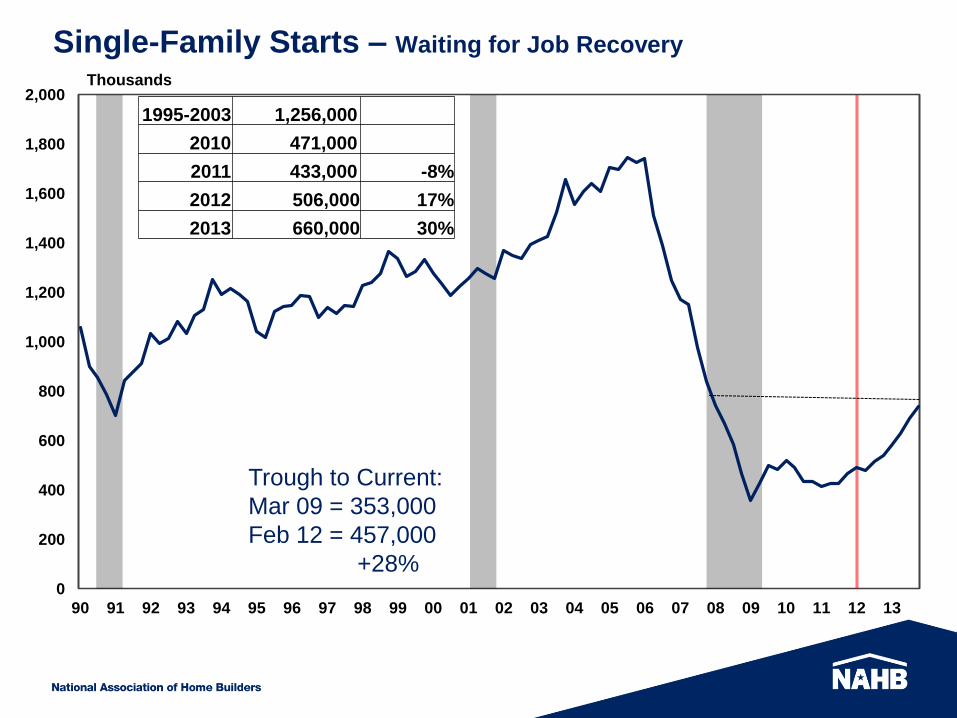

Single-Family Starts – Waiting for Job Recovery

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Thousands

Trough to Current:

Mar 09 = 353,000

Feb 12 = 457,000

+28%

1995-2003 1,256,000

2010 471,000

2011 433,000 -8%

2012 506,000 17%

2013 660,000 30%

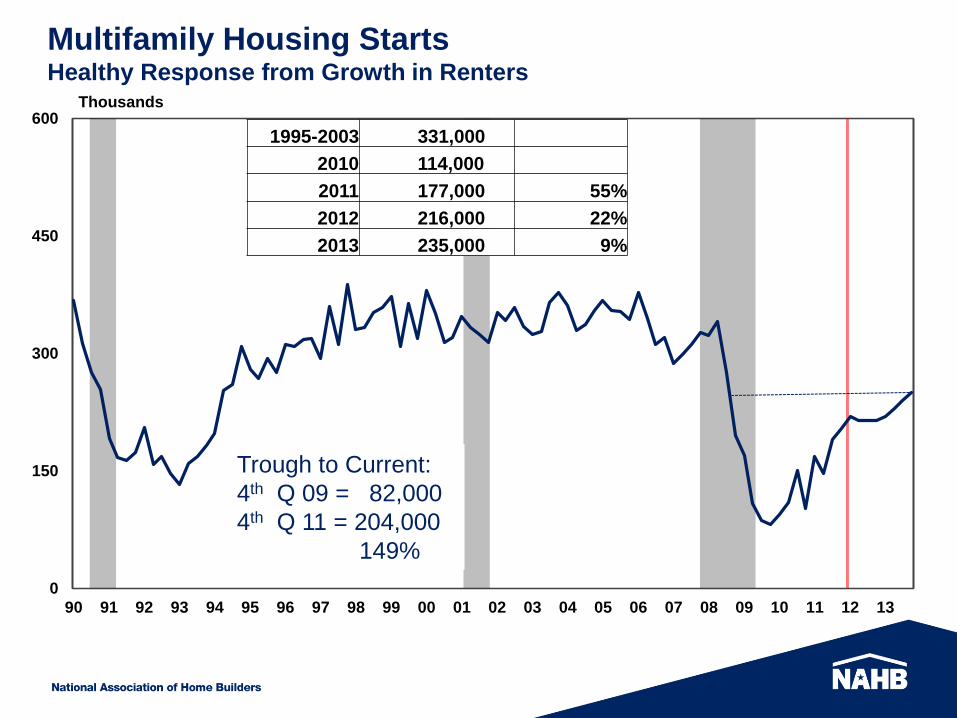

Multifamily Housing Starts Healthy Response from Growth in Renters

0

150

300

450

600

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Thousands

Trough to Current:

4th Q 09 = 82,000

4th Q 11 = 204,000

149%

1995-2003 331,000

2010 114,000

2011 177,000 55%

2012 216,000 22%

2013 235,000 9%

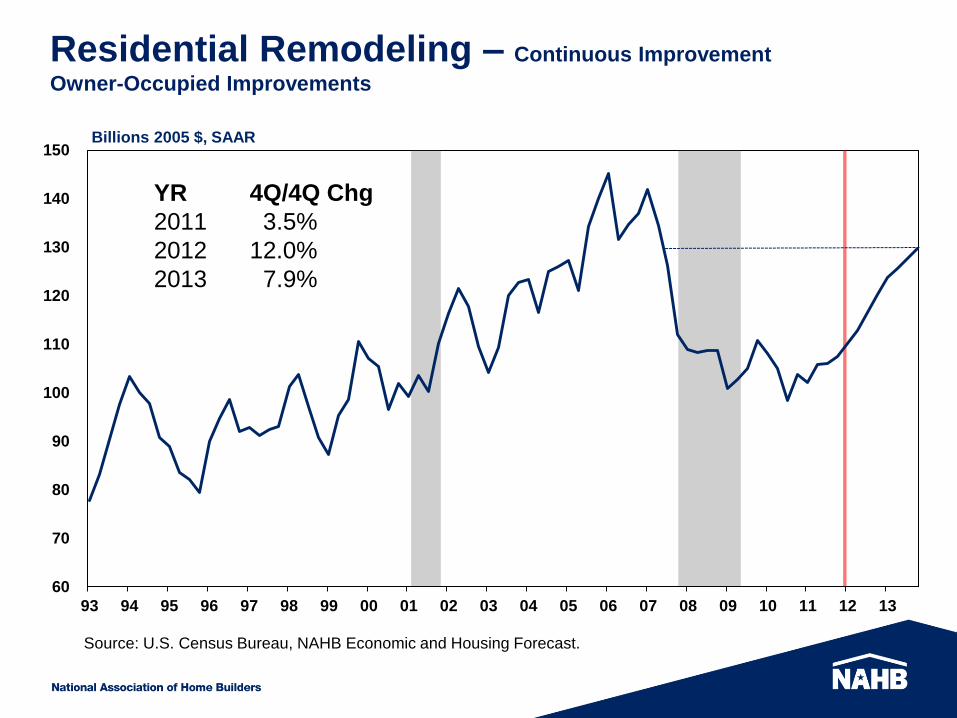

Residential Remodeling – Continuous Improvement

Owner-Occupied Improvements

60

70

80

90

100

110

120

130

140

150

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

YR 4Q/4Q Chg

2011 3.5%

2012 12.0%

2013 7.9%

Billions 2005 $, SAAR

Source: U.S. Census Bureau, NAHB Economic and Housing Forecast.

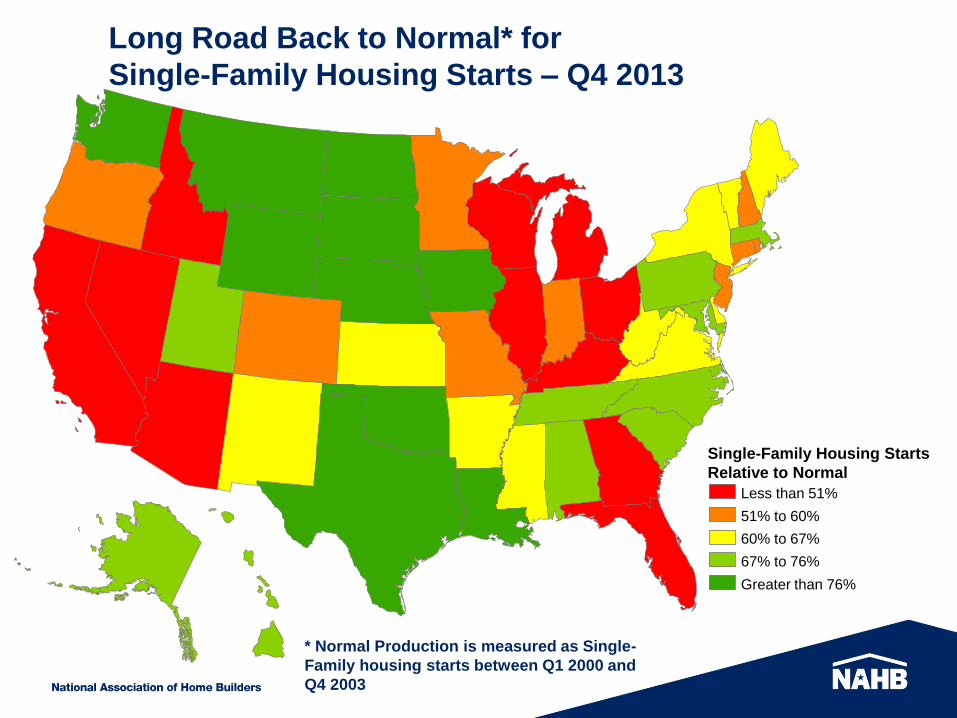

Long Road Back to Normal* for

Single-Family Housing Starts – Q4 2013

* Normal is the average from Q1 2000 to Q4 2003

* Normal Production is measured as Single-

Family housing starts between Q1 2000 and

Q4 2003

Single-Family Housing Starts

Relative to Normal

Less than 51%

51% to 60%

60% to 67%

67% to 76%

Greater than 76%

Questions?

Answers:

www.housingeconomics.com

eyeonhousing.wordpress.com