HOUSING FINANCE IN TRANSITION ECONOMIES - OECD. · PDF file4 Pre-Requisites to a Sizeable...

15

1 HOUSING FINANCE HOUSING FINANCE IN TRANSITION ECONOMIES IN TRANSITION ECONOMIES OECD Workshop OECD Workshop Warsaw, Poland Warsaw, Poland December 5 December 5 - - 6, 2002 6, 2002 Loïc Chiquier The World Bank

-

Upload

nguyenkhanh -

Category

Documents

-

view

218 -

download

2

Transcript of HOUSING FINANCE IN TRANSITION ECONOMIES - OECD. · PDF file4 Pre-Requisites to a Sizeable...

1

HOUSING FINANCEHOUSING FINANCEIN TRANSITION ECONOMIESIN TRANSITION ECONOMIES

OECD WorkshopOECD Workshop

Warsaw, PolandWarsaw, PolandDecember 5December 5--6, 20026, 2002

Loïc ChiquierThe World Bank

2

Challenge in Transition EconomiesChallenge in Transition Economies

!! Key for growth, poverty, wealth Key for growth, poverty, wealth (75(75--90% of household 90% of household wealth), wealth), social stabilitysocial stability

!! Pressure from urbanization and demographics (Pressure from urbanization and demographics (stock stock or flow issue ?) or flow issue ?)

!! HF to become larger part of the financial system HF to become larger part of the financial system and contribute to its stability and profitabilityand contribute to its stability and profitability

!! Role of the state not in lending, but improving Role of the state not in lending, but improving market infrastructure, regulation, targeted subsidiesmarket infrastructure, regulation, targeted subsidies

2

3

Countries Over 50% UrbanCountries Over 50% Urban

Over 50 %

Reaching 50%

Least Urbanized

3

4

PrePre--Requisites to a Sizeable Housing Finance SystemRequisites to a Sizeable Housing Finance System

!! MacroMacro--economic stability economic stability (inflation, real rate, EU convergence)(inflation, real rate, EU convergence)

!! Workable legal frameworkWorkable legal framework (registered property rights, (registered property rights,

effective foreclosure, coeffective foreclosure, co--ownership problems)ownership problems)

!! Efficient housing markets to finance Efficient housing markets to finance (land use, urban (land use, urban and construction norms, taxation, RE industry professionals: and construction norms, taxation, RE industry professionals: developers, appraisers, realtors, brokers, etc.)developers, appraisers, realtors, brokers, etc.)

!! Integration within the financial system Integration within the financial system (liberalized (liberalized credit sector, specialized/earmarked funds, development of credit sector, specialized/earmarked funds, development of fixed income securities, fitting regulatory /oversight frame)fixed income securities, fitting regulatory /oversight frame)

4

5

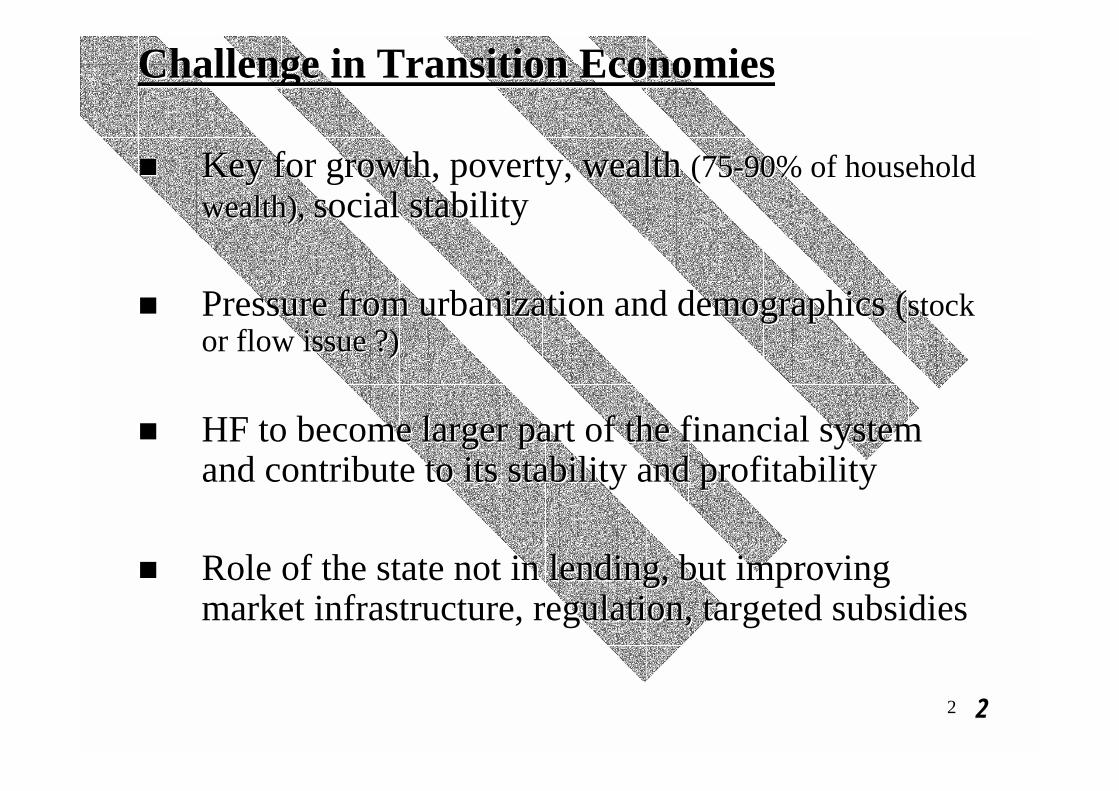

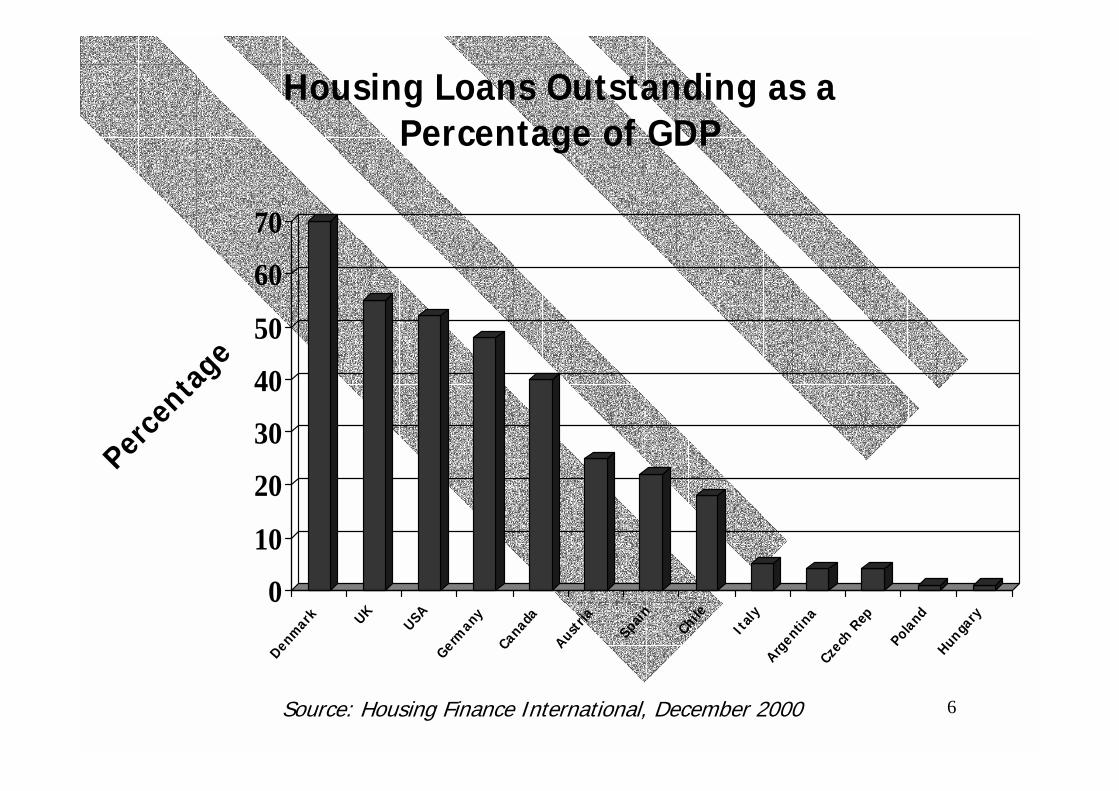

Often small, instable, fragmented mortgage marketsOften small, instable, fragmented mortgage markets

–– Mortgage stock < 5%Mortgage stock < 5%--10% GDP (38% EU, 65% US)10% GDP (38% EU, 65% US)

–– Poor access to HF services for households (if not urban Poor access to HF services for households (if not urban professionals), delayed access to ownership, incremental professionals), delayed access to ownership, incremental or informal housing, limited impact of RE on growthor informal housing, limited impact of RE on growth

–– Lenders / regulators perceive relative large risk exposure Lenders / regulators perceive relative large risk exposure and difficult low profitability (vs. other credit sectors) and difficult low profitability (vs. other credit sectors)

–– Limited economic/cultural demand from borrowers Limited economic/cultural demand from borrowers (mortgaged home, informal income, tax avoidance)(mortgaged home, informal income, tax avoidance)

–– Perceived need for more subsidies (fiscally costly) but Perceived need for more subsidies (fiscally costly) but subsidized loans run against marketsubsidized loans run against market--oriented competition oriented competition 5

6

0

10

20

30

40

50

60

70

Perce

ntage

Denmark UK

USAGerm

any

Canada

Austria

Spain

Chile

Ital

yArg

entina

Czech

Rep

Poland

Hungary

Housing Loans Outstanding as a Percentage of GDP

Source: Housing Finance International, December 2000

7

Underdeveloped Mortgage Markets ? Underdeveloped Mortgage Markets ?

!! Slow development of mortgage securities Slow development of mortgage securities

–– Dominant depositDominant deposit--base funding model (when very liquid base funding model (when very liquid banks), acceptable market risks with variable rate credits banks), acceptable market risks with variable rate credits

(contrast with $ 2.6 trillion MBS in the US in 1999)(contrast with $ 2.6 trillion MBS in the US in 1999)

–– Yet more longYet more long--term fixedterm fixed--rate funding opportunities with rate funding opportunities with the diversification needs of institutional investors the diversification needs of institutional investors (notably pension funds)(notably pension funds)

–– Complex vs. simple variants of mortgage securities Complex vs. simple variants of mortgage securities (different ways to manage market risks and equity, but (different ways to manage market risks and equity, but also different prealso different pre--requisites, objectives, costs of funds)requisites, objectives, costs of funds)

7

8

Main Housing Finance Related RisksMain Housing Finance Related Risks

Credit RiskCredit Risk (losses due to default: capacity and will) (losses due to default: capacity and will)

Liquidity RiskLiquidity Risk (fear cash need) and (fear cash need) and Market RiskMarket Risk (impact of a (impact of a change of interest rates on assets, liabilities, net interest rechange of interest rates on assets, liabilities, net interest results)sults)

Political RiskPolitical Risk (including change of legal and regulatory system (including change of legal and regulatory system affecting the overall mortgage portfolio)affecting the overall mortgage portfolio)

Operation RiskOperation Risk (inadequate (inadequate organization, controls, IS, corporate organization, controls, IS, corporate governance)governance)

Agent riskAgent risk (misuse funds by intermediaries) for 2(misuse funds by intermediaries) for 2ndnd--tiertierinstitutions (insurance, securitization, liquidity facilities)institutions (insurance, securitization, liquidity facilities)

8

9

Management of Market and Liquidity Risks (I)Management of Market and Liquidity Risks (I)

Impact of changing interest rates on the value of assetsImpact of changing interest rates on the value of assets& liabilities, and on net & liabilities, and on net interest results (ex: S&L crisis)interest results (ex: S&L crisis)

Various subVarious sub--categories: categories: commitment risk, pipeline risk, commitment risk, pipeline risk, prepayment risk , foreign exchange riskprepayment risk , foreign exchange risk

Different measure methods, hypothesis, tolerance levelsDifferent measure methods, hypothesis, tolerance levels

More difficult context in emerging countries: volatile More difficult context in emerging countries: volatile interest rates, no hedge derivatives, limited yield curveinterest rates, no hedge derivatives, limited yield curve

9

10

Management of Market and Liquidity Risks (II)Management of Market and Liquidity Risks (II)

!! Adjust the credit design according to the funding structure Adjust the credit design according to the funding structure (adjustable / discretionary rates, hard(adjustable / discretionary rates, hard--currency loans: more credit risks)currency loans: more credit risks)

!! Manage liquidity needs and cashManage liquidity needs and cash--flows flows (adequate capital, (adequate capital, funding sources, treasury departmentfunding sources, treasury department), determine ALM policy), determine ALM policy

!! Possible access to liquidity facility Possible access to liquidity facility (simple, residual market risks) (simple, residual market risks)

!! Adjust duration matching, use hedging derivativesAdjust duration matching, use hedging derivatives

!! Issue mortgage securities (securitization, mortgage bonds) Issue mortgage securities (securitization, mortgage bonds) although no panacea (cost of funds, preconditions)although no panacea (cost of funds, preconditions)

!! Price residual risks through the credit (+ prepayment fees)Price residual risks through the credit (+ prepayment fees)10

11

Management of Mortgage Credit Risks (I)Management of Mortgage Credit Risks (I)

Residential mortgages: expected Residential mortgages: expected excellent riskexcellent risk and and attractive asset attractive asset (US NPL > 3 months 0.3% (US NPL > 3 months 0.3% --3.7%) 3.7%) but different but different perception in countries where severe recent crisisperception in countries where severe recent crisis(NPL > 20%: see next slide about Colombia, Mexico, Thailand, etc(NPL > 20%: see next slide about Colombia, Mexico, Thailand, etc.) .)

Crisis triggersCrisis triggers (on default probability and/or loss severity):(on default probability and/or loss severity):

•• Economic crisis: unemployment, lower housing values, Economic crisis: unemployment, lower housing values, negative equity (disincentives to repay)negative equity (disincentives to repay)

•• Financial shock, higher rates passed to variable rate creditsFinancial shock, higher rates passed to variable rate credits•• Unsound amortization schemes, lack of prudential lending Unsound amortization schemes, lack of prudential lending

standards and regulations standards and regulations •• Ineffective foreclosure (delays, appeals, adverse judiciary)Ineffective foreclosure (delays, appeals, adverse judiciary)•• Spreading culture of nonSpreading culture of non--payment (fueled by political risk)payment (fueled by political risk)

11

12

NPL Mortgage Colombia

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Jan-9 8Mar-9

8May-98

Jul-98

Sep -98Nov-98Jan-9 9Mar-9

9May-99

Jul-99

Sep -99Nov-99Jan-00Mar-0

0May-00

Jul-00

Sep -00Nov-00Jan-0 1Mar-0

1May-01

Jul-01

Sep -01Nov-01

13

Management of Credit Risks (II)Management of Credit Risks (II)

Expansion and deepeningExpansion and deepening to largerto larger--scale portfolios scale portfolios (including lower(including lower--income) if wellincome) if well--managed credit risksmanaged credit risks

!! Optimal credit design: riskOptimal credit design: risk--adjusted profitability of the adjusted profitability of the lender vs. affordability of borrower, choice of interest rate lender vs. affordability of borrower, choice of interest rate and amortization scheme (including indexation)and amortization scheme (including indexation)

!! Sound mortgage lending standards (underwriting, servicing)Sound mortgage lending standards (underwriting, servicing)

!! Sufficient, effective and appraised mortgage collateral, and Sufficient, effective and appraised mortgage collateral, and search for alternative collateral (pension, thirdsearch for alternative collateral (pension, third--party, etc)party, etc)

!! Access to reliable incomes, capacity and willing to repay, Access to reliable incomes, capacity and willing to repay, automated underwriting, credit information systems (credit automated underwriting, credit information systems (credit history, past rental payments, relevancy of scoring models)history, past rental payments, relevancy of scoring models)

13

14

Management of Credit Risks (III)Management of Credit Risks (III)

!! Risk adjusted pricing, modified credit policy (term, LTV)Risk adjusted pricing, modified credit policy (term, LTV)

!! Related insurance productsRelated insurance products

!! Capacity to monitor pool performance (needed for SMM)Capacity to monitor pool performance (needed for SMM)

!! Active debt recovery capacities (prevention, menu of Active debt recovery capacities (prevention, menu of restructuring/waivers/foreclosure/resale/leasing solutions)restructuring/waivers/foreclosure/resale/leasing solutions)

!! Appropriate information of borrowers (code conduct?) Appropriate information of borrowers (code conduct?)

!! Capacity building of lending institutionsCapacity building of lending institutions ((capital, expertise)capital, expertise)

!! Development of partial credit insurance / guarantee schemes Development of partial credit insurance / guarantee schemes (risk allocation, actuarial premium, standards, moral hazard)(risk allocation, actuarial premium, standards, moral hazard)14

15

Jordan: liquidity facility issuing bonds to refinance lenders, lending standards, robust catalyst of more affordable mortgage markets

Colombia: restructure distressed S&Ls industry (management of large market and credit risks, regulations, subsidies, securities)

Mexico: access to bond market, separate subsidies from credit, management of risks, prudential norms, credit and MBS guarantees

Latvia: pilot credit guarantees for homeowner associations, lower down-payment for homeowners, reverse mortgage loans

Peru: registration /formalization of property titles (“dead” assets)

Algeria: assistance to lenders (training, funding, insurance), regularizing titles, enhancing mortgage rights

Examples of World Bank Projects

15