Household Growth Loan Engine - Merkle Inc. · Banking & Finance case study Household Growth Loan...

2

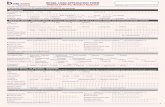

case study Banking & Finance Household Growth Loan Engine Business Challenge With a multitude of lending products and poor direct mail response rates, a top-10 bank needed to improve growth in its lending portfolio. The bank was also challenged to prioritize products and offers. Customer experience was also a concern, in that a household could receive multiple direct mail offers within a short period of time. Approach Merkle developed product-level direct mail response models to: predict booking and balance; determine the primary and secondary product optimized on both value and contact history; and determine the offer at the customer level. f Prescreen benefits: The use of prescreen allowed for the greatest efficiency to maintain high campaign approval rates, minimize risk and maximize ROI. Because Merkle had the ability to target households that met stringent risk criteria, we were able to maximize direct mail response, as the offers could be highly targeted to include specific rate and payment information. f Modeling: Merkle developed highly customized, direct mail focused, product-level models drawing on known customer information, previous marketing contact history (type, recency, frequency), consumer activity (e.g. inquiries, customer service activity), and augmented with geographic, household, competitor and market data as key inputs. f Model governance: In addition to sourcing the right data, Merkle also invested in deriving insights from data to gain the most value out of the existing data assets. Our focus on variable transformations, recoding, and collapsing of variables in a relevant model differentiates a good model from a great one. We then applied rigor around the modeling and validation steps to ensure that the model was as strong as possible and that it would perform optimally in-market. Current model inventory and assessment Net booking models Balance propensity modeling Profit/Revenue models Data Sources Modeling Strategy • Credit • Mortgage • Demographics • Behaviors • Geographic • New credit inquiries • Account closings • Increase/decrease in debt • Bureau-based • Behavior-based • Lifestage • Open checking account • Apply for loan • Pay off existing loan • Risk • LTV • Available Equity • AVM Velocity • Mortgage Characteristics • Income / Affluency • New mover • Recently married • Birth of a child Pre-Screened Data Sources Bureau Triggers Behavioral Triggers Lifestage Triggers Triggers Key Data Dimensions

Transcript of Household Growth Loan Engine - Merkle Inc. · Banking & Finance case study Household Growth Loan...

case studyBanking & Finance

Household Growth Loan Engine

Business ChallengeWith a multitude of lending products and poor direct mail response rates, a top-10 bank needed to improve growth in its lending portfolio. The bank was also challenged to prioritize products and offers. Customer experience was also a concern, in that a household could receive multiple direct mail offers within a short period of time.

ApproachMerkle developed product-level direct mail response models to: predict booking and balance; determine the primary and secondary product optimized on both value and contact history; and determine the offer at the customer level.

f Prescreen benefits: The use of prescreen allowed for the greatest efficiency to maintain high campaign approval rates, minimize risk and maximize ROI. Because Merkle had the ability to target households that met stringent risk criteria, we were able to maximize direct mail response, as the offers could be highly targeted to include specific rate and payment information.

f Modeling: Merkle developed highly customized, direct mail focused, product-level models drawing on known customer information, previous marketing contact history (type, recency, frequency), consumer activity (e.g. inquiries, customer service activity), and augmented with geographic, household, competitor and market data as key inputs.

f Model governance: In addition to sourcing the right data, Merkle also invested in deriving insights from data to gain the most value out of the existing data assets. Our focus on variable transformations, recoding, and collapsing of variables in a relevant model differentiates a good model from a great one. We then applied rigor around the modeling and validation steps to ensure that the model was as strong as possible and that it would perform optimally in-market.

Current model inventory and assessment

Net booking modelsBalance propensity

modelingProfit/Revenue

models

Dat

a So

urce

sM

odel

ing

Stra

tegy

• Credit• Mortgage• Demographics• Behaviors• Geographic

• New credit inquiries• Account closings• Increase/decrease in debt

• Bureau-based• Behavior-based• Lifestage

• Open checking account• Apply for loan• Pay off existing loan

• Risk• LTV• Available Equity• AVM Velocity• Mortgage Characteristics• Income / Affluency

• New mover• Recently married• Birth of a child

Pre-Screened

Data Sources

Bureau Triggers Behavioral Triggers Lifestage Triggers

Triggers Key Data Dimensions

Merkle, a customer relationship marketing (CRM) firm, is the nation’s largest privately-held agency. For more than 20 years, Fortune 1000 companies and leading nonprofit organizations have partnered with Merkle to maximize the value of their customer portfolios. By combining a complete range of marketing, technical, analytical and creative disciplines, Merkle works with clients to design, execute and evaluate connected CRM programs. With more than 1,600 employees, Merkle is headquartered near Baltimore in Columbia, Maryland with additional offices in Boston; Chicago; Denver; Little Rock; Minneapolis; New York; Philadelphia; Pittsburgh; San Francisco; Hagerstown, MD and Shanghai. For more information, contact Merkle at 1-877-9-Merkle or visit www.merkleinc.com.

Jim CoyVP, Financial ServicesBusiness Development [email protected]

f Arbitration engine: Next, we deployed a business-rules approach to arbitrate offers by product. The intention was to get the right offer to the right customer at the right time. The engine used a combination of value (profit/revenue proxy), propensity (model scores) and contact history (recency, frequency). The entire universe was then scored to determine best and next best product to offer through direct mail, at the customer level.

f Offer strategy: Using the appended data, we tailored offers at the product level: » Mortgage offers – to focus on rate and savings messaging, where customers had refinanced their mortgage in

the last 6 months as identified on Merkle DataSource. » Credit card offers – with extended duration and low promotional rates to customers with high loan-to–value

(LTV) ratios and bankcard revolving debt totaling less than $25,000 as reported on the credit bureau. » Home equity line of credit (HELOC) offers – to customers who have high available equity and non-mortgage

revolving debt greater than $50,000 reporting on the credit bureau. » Auto refinance lending offers – to those whose existing auto loan is set to expire in the next 12-18 months.

OutcomeThrough the development of product-level models, and use of Merkle DataSource and value-based arbitration, we were able to effectively optimize what product and offer to mail households, substantially improve marketing ROI. In addition, the customized offer messaging improved response and conversion substantially in historically low-utilized, low-response segments.

f Home equity ROI improved 4x from historical campaigns driven by increases in average balances, booking rates and the lower number of customers mailed.

f Specific marketing communications based on need and behavior were introduced. Understanding that customers use similar products to meet different kinds of needs and tailoring marketing messages to address those specific needs were more appealing to the customer and drove better response.

Looking AheadAs direct mail programs mature, we will leverage the wealth of appended data to create segmentation to improve future targeting, tailor marketing communication and apply to the bank’s prospect universe. This will allow us to acquire similar households that will be highly profitable, establish foundational relationships with the bank, and create opportunities for future cross-sell programs.

Bureau• Credit Prescreen• Multi-Level Criteria• Offer Assignment• LTV• State Selects

Purge Recent Responders

and Opt Outs

Solicitation History

Net Booking and Balance

Models• Mortgage & Property Data• Rate Triggers• Mortgage Triggers

Product TypeMortgage REFI, HELOC, HEIL, Auto, Unsecured

Product OfferRate, Payment, Amount

Offer TypePre Approved

Segment Type• Bank Customer• Prospect• Winback/Handraisers

Input Files

Mortgage

Credit Card

HELOC/HEIL

Unsecured

Auto

Triggers

Data Sourcing and Processing Campaign OfferingTargeting

CustomerDatabase

ProspectDatabase