House View - IDFC Bank...Equity –Our view Maintain equity exposure, use any corrections to further...

44

House View 15 th Mar to 15 th Apr

Transcript of House View - IDFC Bank...Equity –Our view Maintain equity exposure, use any corrections to further...

House View

15th Mar to 15th Apr

Agenda

1. Equity

2. Fixed Income

3. Our Portfolio Construction Approach

4. Model Portfolios

3 – 16

17 – 26

27 - 34

35 – 43

EQUITY

Equities: Geo Political concerns slow momentum, valuations and earnings in focus now

4

■ Markets continued to rally in early April (with continued FII flows and the Parliament passingfour GST-related bills), paving the way for the new indirect tax to be implemented nationwide.

■ Geopolitical tensions (North Korea, Syria and Afghanistan) weighed on markets, arrestingmomentum

■ As the financial year ends, investor focus will shift once again to the Q4FY17 earnings season.The earning season assumes importance given that this would be the quarter that would capturethe full impact of demonetization and should form the basis for expectations for FY18

26,500

27,000

27,500

28,000

28,500

29,000

29,500

30,000

Sensex

Source: BSE India

1 Month Performance: Realty and Capital Goods rallied while IT, Metals witnessed corrections; FII flows in March was >30 K Cr, continued to be positive

■ Realty and Capital Goods were the best performerslast month while IT, Teck and Metals were the worstperformers

■ FII flows were in Feb (+$1.5 bn) and march (~$5 bn)increased significantly, March saw the highestmonthly FII inflows in the past 10 years

■ Domestic flows had reduced in Feb but againincreased in march and continue to be positive for9th month running

51M perf as on 13th April; For April, FII Flows data as on 13th April; MF flows as on 10th April; Source: Accord Fintech

-7.4

-6.4

-4.5

-1.4

-0.4

-0.2

-0.0

0.9

1.6

1.9

2.2

3.2

3.5

5.5

6.0

6.2

7.1

11.9

-10.0 -5.0 - 5.0 10.0 15.0

S&P BSE IT

S&P BSE TECk Index

S&P BSE METAL Index

S&P BSE AUTO Index

S&P BSE SENSEX

S&P BSE Health Care

NIFTY 50

S&P BSE 200

S&P BSE 500

S&P BSE BANKEX

S&P BSE Power Index

S&P BSE Mid-Cap

S&P BSE FMCG

S&P BSE OIL & GAS Index

S&P BSE Consumer Durables

S&P BSE Small-Cap

S&P BSE Capital Goods

S&P BSE Realty Index

1M Performance

-19,000

-14,000

-9,000

-4,000

1,000

6,000

11,000

16,000

21,000

26,000

31,000

MF FII Trend (Cr)

MF FII

Continue to believe that Earnings placed well to rise…

■ Both Earnings and index were flat in last month butas mentioned earlier we expect that lowering ofinterest rates should lead to reduced cost ofborrowings, leaving more money in the hands ofconsumers, which will help in the growth of theeconomy

■ Further, Implementation of GST With a greater focuson digital payments, the organised sector will be theclear winner, as the tax arbitrage often available inthe unorganised sector will vanish

6

12001250130013501400

24000250002600027000280002900030000

01-0

4-2

016

01-0

5-2

016

01-0

6-2

016

01-0

7-2

016

01-0

8-2

016

01-0

9-2

016

01-1

0-2

016

01-1

1-2

016

01-1

2-2

016

01-0

1-2

017

01-0

2-2

017

01-0

3-2

017

01-0

4-2

017

Sensex Vs EPS (Closer look)

sensex EPS (RHS)

600

700

800

900

1000

1100

1200

1300

1400

8000

13000

18000

23000

28000

02-01-2007 02-01-2008 02-01-2009 02-01-2010 02-01-2011 02-01-2012 02-01-2013 02-01-2014 02-01-2015 02-01-2016 02-01-2017

Sensex Vs EPS

sensex EPS (RHS)

Source: BSE India

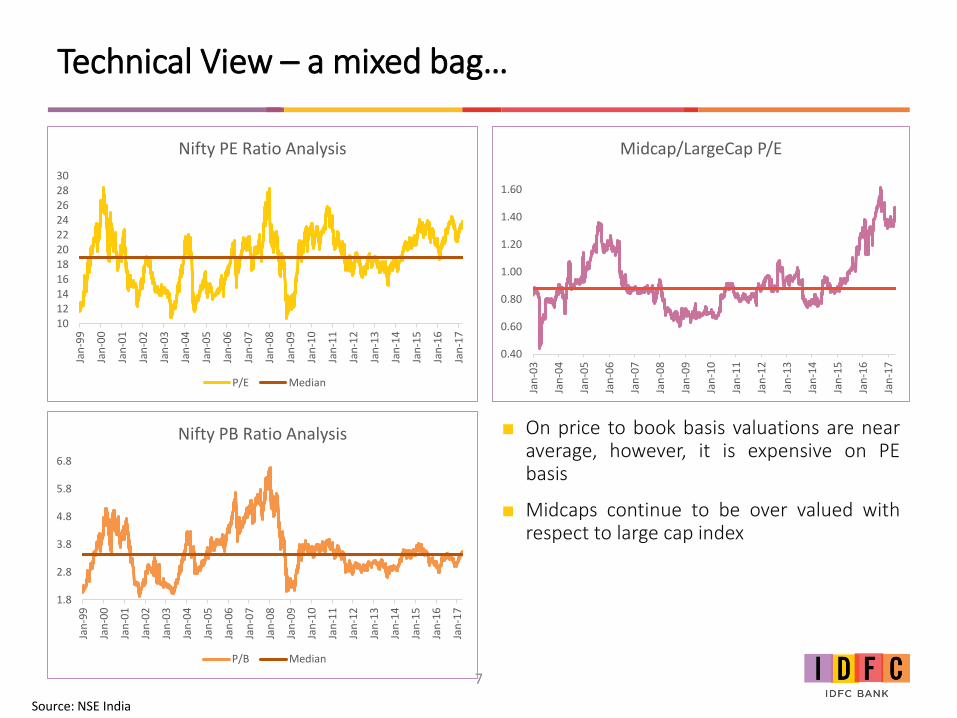

Technical View – a mixed bag…

■ On price to book basis valuations are nearaverage, however, it is expensive on PEbasis

■ Midcaps continue to be over valued withrespect to large cap index

7

1.8

2.8

3.8

4.8

5.8

6.8

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Nifty PB Ratio Analysis

P/B Median

1012141618202224262830

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Nifty PE Ratio Analysis

P/E Median

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Midcap/LargeCap P/E

Source: NSE India

Equity – Our view

Maintain equity exposure, use any corrections to further increase allocation:

We believe earnings could see an upward movement with lower cost of capital and

reduction of tax arbitrage on organized sector viz-a-viz unorganized sector.

However, global uncertainties with Trump’s policies and upcoming elections in

Europe will keep the market volatile. Corrections, if any, can be used to add equity

exposure. Clients with lower equity can increase allocation in line with risk profile

(details on following slides)

Shift from large polarized funds to niche managers: recommend clients to shift

investments to niche managers with smaller AUM (details to follow). Focus on

absolute returns and smaller AUM’s will help managers remain agile and deliver

better returns.

8

Recommended Mutual Funds - Equity

Scheme Name AUMExit load period

Mid/Small cap exposure

2017 YTD

2016 2015 2014 2013 2012

Large Cap

SBI Blue Chip Fund 12,586 1Y 11.8 13.10 4.83 7.99 47.86 7.58 38.23

Birla Sun Life Frontline Equity 16,352 1Y 12.7 13.46 7.43 1.10 44.72 9.25 36.07

Reliance Top 200 Fund 2,701 1Y 12.9 16.58 2.23 1.11 54.65 4.15 40.97

ICICI Prudential Focused Bluechip Equity Fund

12,843 1Y 0.0 12.54 7.74 -0.21 41.10 10.21 26.79

Nifty 11.79 3.01 -4.06 31.39 6.76 27.70

Sensex 10.65 1.95 -5.03 29.89 8.98 25.70

Flexi Cap

Franklin India Prima Plus Fund 10,703 1Y 16.8 13.90 4.98 4.38 56.79 5.55 31.04

IDFC Classic Equity Fund 852 365D 22.4 16.63 7.99 5.21 28.62 2.51 37.26

Kotak Select Focus Fund 9,323 1Y 17.2 17.16 9.44 2.96 57.87 6.13 33.45

ICICI Prudential MultiCap Fund 2,501 18M 43.9 16.56 10.14 3.08 49.82 6.42 36.53

Motilal Oswal MOSt Focused Multicap 35 Fund

5,992 17.4 23.28 8.45 14.60

BSE 200 14.05 3.95 -1.48 35.47 4.38 30.98

9

YTD as on 13th Apr; Portfolio Details as on Mar 31st

Recommended Equity Funds

10

Scheme Name AUMExit load period

Mid/Small cap exposure

2017 YTD

2016 2015 2014 2013 2012

Balanced

HDFC Balanced Fund 10,186 1Y 24.3 11.04 9.72 3.01 51.47 8.78 26.56

ICICI Prudential Balanced Advantage Fund

18,221 18M 9.6 7.98 7.35 6.70 29.04 10.93 33.33

IDFC Balanced Fund 594 1Y 11.5 6.48

Crisil Balanced Fund Aggressive Index

7.88 6.66 0.48 25.34 6.05 21.28

Mid/Small Cap

Mirae Asset Emerging Bluechip Fund

3,532 365D 53.6 20.52 12.17 14.08 84.62 8.61 45.56

SBI Magnum MidCap Fund 3,583 1Y 81.7 15.24 4.98 14.92 71.94 13.57 47.98

HDFC Midcap Opportunities Fund

15,734 1Y 62.1 18.91 11.35 5.81 76.63 9.64 39.62

Franklin India Smaller Companies Fund

5,238 1Y 79.6 19.08 10.19 9.56 89.92 13.22 51.70

Nifty Free Float Mid Cap 100

22.29 7.13 6.46 55.91 -5.10 39.16

YTD as on 13th Apr; Portfolio Details as on 31st March

Equity – Our solutions – Portfolio Management Services

India Opportunities

Portfolio -Motilal

Unifi Capital

Birla SunlifeSelect Sector

Portfolio

New mid/small cap focussed strategy from Motilal Oswal Currently manage AUM of ` 1,474 crores, invested in 15-20 stocks

with an average market cap of ~ 6,700 Crores Key Themes: Make in India, Consumption & Capex revival

Specialized PMS provider with 15 years of track record, managesaround ` 2000 Crs

Identify unique themes based on market opportunity Strong alignment with client interest, revenue model only linked

to client returns (12% hurdle)

Concentrated portfolio of 15 to 25 stocks with 80% of portfolio

invested in 4- 6 sectors

Follows 4 pillar investment approach – a blend of top down and

bottom up factors including Piotroski Score

11

Motilal Oswal India Opportunity Portfolio Strategy

Objective

The Strategy aims to generate long termcapital appreciation by creating a focusedportfolio of high growth stocks having thepotential to grow more than the nominal GDPfor next 5-7 years across and which areavailable at reasonable market prices. Focusis on identifying well run companies that areexisting/potential leaders in their field ofoperations.

12

Focus Themes for IOP

Make in India

Making India a manufacturing hub

• Auto and auto components

• Pharma Outsourcing

• Engineering Products

Third trillion dollar consumption opportunities

Increasing discretionary consumer spending

• Consumer Durables• Consumer Staples• Building Products• Kitchenware• Housing Finance

Revival in Capex Cycle

Increasing public investments on Infrastructure

• Cement• Railway• Ports• Metro

Strategy Conduct

No. of Stocks - 15 – 20 stocks for a portfolio

Scrip Allocation – not more than 10% in asingle stock at the time of initiation

Sector Allocation Limit – 35% in a sector

Strategy Focus – Identifying well runcompanies that are existing/potentialleaders in field of operations

Investment horizon – 3+ years

59.57

30.2421.81

17.49

34.8525.92

17.412.89

0

10

20

30

40

50

60

70

1 year 3 years 5 years Since Inception

Performance

IOP Nifty Free Float Midcap 100

Performance as on 31st March

Unifi Capital – An Unique Equity Proposition

Unifi Capital is a discretionary, long-only India centric fund manager; specializing in event oriented top-down themes and a bottom-up focus on “growth with value”.Established – 2001 ( 16 year track record)AUM – approx. 1,600 Cr ObjectiveFocus on identifying unique investment opportunities that consistently generate superior (risk adjusted) returns with due emphasis on capital preservation.

Theme Development Concept Validation & Review Portfolio Management

Investment Philosophy

15.7%21.2%

43.0%

13.8%

44.0%

57.6%

21.0%

34.6%

0.0%

20.0%

40.0%

60.0%

80.0%

Event Arbitrage(2002)

STLC (2011) Delisting*(2009)

Insider Shadow(2010)

DVD (2013) Holdco (2014) Spin Off (2014) APJ 20 (2015)

CAGR Returns for all existing Funds

*closed for subscriptionPerformance as on 31st March

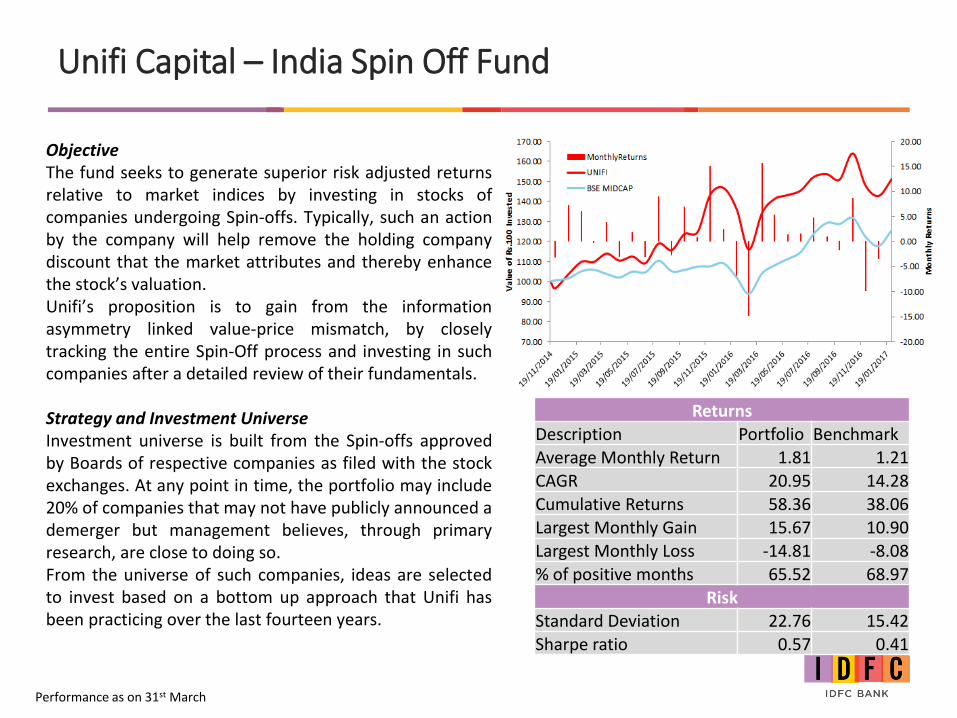

ObjectiveThe fund seeks to generate superior risk adjusted returnsrelative to market indices by investing in stocks ofcompanies undergoing Spin-offs. Typically, such an actionby the company will help remove the holding companydiscount that the market attributes and thereby enhancethe stock’s valuation.Unifi’s proposition is to gain from the informationasymmetry linked value-price mismatch, by closelytracking the entire Spin-Off process and investing in suchcompanies after a detailed review of their fundamentals.

Strategy and Investment UniverseInvestment universe is built from the Spin-offs approvedby Boards of respective companies as filed with the stockexchanges. At any point in time, the portfolio may include20% of companies that may not have publicly announced ademerger but management believes, through primaryresearch, are close to doing so.From the universe of such companies, ideas are selectedto invest based on a bottom up approach that Unifi hasbeen practicing over the last fourteen years.

Unifi Capital – India Spin Off Fund

ReturnsDescription Portfolio BenchmarkAverage Monthly Return 1.81 1.21CAGR 20.95 14.28Cumulative Returns 58.36 38.06

Largest Monthly Gain 15.67 10.90

Largest Monthly Loss -14.81 -8.08

% of positive months 65.52 68.97Risk

Standard Deviation 22.76 15.42Sharpe ratio 0.57 0.41

Performance as on 31st March

Objective The Fund seeks to achieve returns with below-average riskover a horizon of 4-5 years. The fund would invest insectors that will benefit from the next stage of India’sgrowth on the back of improvement in India’s economicand policy climate. The Fund endeavors to grow investors’capital by 3x in 5 years time or less.

Investment StrategyBuild a concentrated portfolio of 10-15 stocks from sectors poised to benefit from macro policy initiatives and demographic strengths.(a) agriculture, (b) specialty chemicals, (c) mining, (d) hi tech manufacturing (e) infrastructure

UniverseSet of all listed companies with market capitalization of INR 200 Crs and above.

Unifi Capital – APJ 20 Fund

ReturnsDescription Portfolio BenchmarkAverage Monthly Return 2.68 1.72

CAGR 34.60 20.91Cumulative Returns 60.07 35.06

Largest Monthly Gain 16.32 10.90Largest Monthly Loss -11.24 -8.08% of positive months 68.42 73.68

Standard Deviation 21.13 17.70

Sharpe ratio 1.26 0.73

Performance as on 31st March

Birla Sunlife Select Sector Portfolio

Identify sectors that grow faster than the GDP

Recurring Winners:

Focus on businesses that have consistently created

values

Unique strategy based on superior IP/ Screeners

Value investing approach to generate alpha

Sustainable wealth

creation

16

4 Pillars of the Investment Approach

■ Portfolio uses Piotroski – Score as an screener which measures the overall strength of thefirm’s financial position and improvement (delta) in the financial position of the firm

■ P score is one aggregate signal that captures three areas of the firm’s financial condition:

■ Profitability : +ve Net profit, +ve Operating Cash Flows, Cash flow>Net Profit, Change in ROA

■ Financial leverage/Liquidity: Change in Leverage, Change in Liquidity, and Equity Financing

■ Operating efficiency : Change in Operating Margins, Change in Turnover Ratio

Returns as on Mar 29th 2017: Inception Date: 01/08/09; Returns more than 1 year are annualized

30%

19%

39% 40%

32%

20%26%

8%

15% 16% 14%9%

0%5%

10%15%20%25%30%35%40%45%

Performance

Select Sector Portfolio CNX Nifty 500

FIXED INCOME

CPI increased with 10 yr yields in a narrow range

■ RBI surprised markets by hiking Reverse repo rate to6%, Repo was unchanged at 6.25%.

■ CPI inflation increased to 3.8% in March (3.7% inFeb), led by uptick in food inflation and higherinternational oil prices. WPI fell to 5.7% in Marchfrom 6.6%

■ IIP contracted by 1.2% led by manufacturing sectorwhich reported a decline of 2%

■ We believe that RBI is likely to stick to its wait andwatch approach, leading to a long pause in rates forthe rest of 2017.

18

6.8%

6.00%

6.20%

6.40%

6.60%

6.80%

7.00%

7.20%

7.40%

7.60%

10 yr G Sec

6.97% GOI 2026 (New Ten Year)

3

3.5

4

4.5

5

5.5

6

6.5

7

Repo and Reverse Repo Rates

CPI Repo Rate (%) Reverse Repo Rate (%)

55.86

2530354045505560

BRENT CRUDE ($)

BRENT CRUDE ($)

Source: IDFC MF, RBI

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

01

-01

-20

16

01

-02

-20

16

01

-03

-20

16

01

-04

-20

16

01

-05

-20

16

01

-06

-20

16

01

-07

-20

16

01

-08

-20

16

01

-09

-20

16

01

-10

-20

16

01

-11

-20

16

01

-12

-20

16

01

-01

-20

17

01

-02

-20

17

01

-03

-20

17

01

-04

-20

17

CP CD rates

1 Year CD 1 Yr CP

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

10 yr G Sec vs 10 yr AAA (PSU)

6.97% GOI 2026 (New Ten Year) 10 YEAR AAA(PSU)

Spreads higher than average; US 10 yr yields fell because of geopolitical tensions

■ Spreads have widened to 90 bps between 10yr G Sec and 10 yr AAA PSU which averages76 bps over the last 1 year

■ CP CD rates remained stable during themonth

■ US Treasury yields softened considerablypost the geopolitical tensions in North Koreaand Middle East

74

5190 57

19

2.23%

1.20%

1.40%

1.60%

1.80%

2.00%

2.20%

2.40%

2.60%

2.80%

01

-01

-20

16

01

-02

-20

16

01

-03

-20

16

01

-04

-20

16

01

-05

-20

16

01

-06

-20

16

01

-07

-20

16

01

-08

-20

16

01

-09

-20

16

01

-10

-20

16

01

-11

-20

16

01

-12

-20

16

01

-01

-20

17

01

-02

-20

17

01

-03

-20

17

01

-04

-20

17

US 10 Year

Source: IDFC MF, RBI

Debt – Our View

■ We believe that RBI is likely to stick to its mandate and remain focussedon Headline CPI inflation with close watch on monsoon trends andhence expect rate cuts to remain on a long pause (till year end 2017)

■ Higher accruals from Corporate bond funds/FMP’s/NCD’s with aboveaverage spreads make it attractive for fresh allocations ( G Sec yields areat approx 6.8%, relative to Corp bond yields of 8-8.75%)

■ Hence, we would recommend overweight on accrual funds and lock inhigher yields available currently. Going ahead, lower credit growth willalso lead to reduction in borrowing cost for corporates and reduceyields on Corp bonds

■ We would also recommend NCDs / 3 year FMPs which can generatehigher returns on a post tax basis.

■ Utilize Arbitrage funds as a replacement for cash: Clients with a higherthan 1month horizon should prefer allocations to arbitrage funds overliquid funds

20

Debt– Our solutions

NCD’s – NBFC

Accrual Funds

Non convertible debentures issued by listed NBFC’s Yields range between 8 -8.75% across tenors Higher tax efficiency lead to outperformance of 1.5-2% over MF’s

Suited for investors with a 1 month or higher horizon Better after tax accruals compared to short term funds

Arbitrage Funds

Fall in the lending rates should lead to improvement of the creditenvironment which should benefit accrual strategies.

21

Edelweiss NCD

Product Bank FD’s Edelweiss NCD’s FMP’s ( 3 Years )YTM 7.50 % 8.75 % 7.75 %

Taxation 30 % 10 % 20 % with IndexationPost Tax 5.25% 7.88%** 7.40%

Outperformance

- 2.63% - - 0.48%

22

■ In the current Market scenario of lowering Interest rate the fixed income market is very delicately poised

■ Edelweiss NCD provides a unique opportunity to earn higher post Tax returns as seen below

Edelweiss as an Issuer

■ Edelweiss Financial Services Ltd is one of India’s leading diversified financial services organization

■ Present in the Market-Linked Debentures market since 2007 with gross issuance of over $ 1 Billion

■ Largest issuer in this industry with a market share of more than 40% as per an independent report published by CARE

** Assuming taxation rate of 10% without indexation basis opinion received from issuer Not to be construed as tax advice. Please speak to your tax representative for details

Recommended Debt Mutual Funds

23

Scheme Name YTMExpense ratio

Mod Duration

SOVAAA and Eq

AA and Eq

A and Eq

Liquid

Kotak Floater - Short Term 6.71 0.16 0.0 0.0 100.0 0.0 0.0

Reliance Liquid Fund - Treasury Plan 6.46 0.17 0.1 0.0 99.1 0.8 0.0

Ultra Short Term

ICICI Prudential Flexible Income Plan 7.32 0.27 1.2 16.7 60.2 23.0 0.0

Kotak Low Duration Fund 8.02 1 0.0 0.2 30.7 59.2 10.0

UTI Treasury Advantage Fund 7.62 0.31 0.0 2.5 68.6 28.8 0.0

Short Term

Birla Sun Life Short Term Fund 7.42 0.3 2.2 17.0 73.2 9.9 0.0

ICICI Prudential Short Term Plan 7.65 1.22 2.9 37.3 50.9 11.8 0.0

HDFC Short Term Opportunities Fund 7.23 0.36 1.3 10.6 79.2 10.3 0.0

UTI Income Opportunities Fund 9.04 1.93 0.0 3.4 29.7 56.3 10.6

Portfolio Details as on 31st March

Recommended Debt Mutual Funds

24

Scheme Name YTMExpense ratio

Mod Duration

SOVAAA and Eq

AA+AA and below

Accrual

IDFC Corporate Bond Fund 7.36 0.57 2.7 0.0 100.0 0.0 0.0

SBI Corporate Bond Fund 8.63 1.41 2.2 2.0 30.9 35.1 32.0

HDFC Corporate Debt Opportunities Fund 8.89 1.83 2.9 0.0 24.7 39.3 36.0

Kotak Medium Term Fund 8.53 1.7 0.0 0.4 31.2 59.7 8.7

Dynamic

Birla Sun Life Dynamic Bond Fund 7.8 1.49 7.5 63.9 13.2 21.9 1.0

IDFC Dynamic Bond Fund 6.7 1.52 2.1 66.7 33.3 0.0 0.0

SBI Dynamic Bond Fund 6.42 1.57 3.0 71.8 28.2 0.0 0.0

Portfolio Details as on 31st March

Recommended Debt Funds - Performance

25

Scheme Name AUMExit load period

1M 3M 6M 12 M

Arbitrage

ICICI Prudential Equity-Arbitrage Fund 7,185.30 1M 5.63 5.63 5.61 6.32

IDFC Arbitrage Fund 2,621.18 1M 6.03 5.80 5.62 6.11

Kotak Equity Arbitrage Scheme 6,177.44 30D 5.52 5.65 5.51 6.17

Crisil Liquid Fund Index 6.78 6.66 6.58 7.09

Category Average(Arbitrage Funds) 5.09 5.29 5.51 6.21

Liquid

Kotak Floater - Short Term 11,004.45 0 6.74 6.67 6.73 7.24

Reliance Liquid Fund - Treasury Plan 22,657.36 0 6.82 6.68 6.71 7.21

Crisil Liquid Fund Index 6.78 6.66 6.58 7.09

Category Average(Liquid) 6.27 5.64 6.01 6.65

Ultra Short Term

ICICI Prudential Flexible Income Plan 17,775.30 0 9.60 6.87 7.58 8.61

Kotak Low Duration Fund 4,498.84 0 9.17 7.14 7.51 8.74

UTI Treasury Advantage Fund 8,861.11 0 8.53 7.28 7.51 8.45

Crisil Liquid Fund Index 6.78 6.66 6.58 7.09

Category Average(UST) 7.97 5.76 6.49 7.60

Performance as on 13th April; Portfolio Details as on 31st March

Recommended Debt Funds - Performance

26

Scheme Name AUM Exit load period

1M 3M 6M 12 M

Short Term

Birla Sun Life Short Term Fund 16,190.58 0 12.44 4.63 6.77 9.13

ICICI Prudential Short Term Plan 8,776.47 7D 15.17 3.86 6.82 9.47

HDFC Short Term Opportunities Fund 9,564.13 0 8.99 5.67 6.99 8.50

UTI Income Opportunities Fund 2,578.75 12M 11.22 6.24 7.73 9.78

Crisil Short Term Bond Fund Index 11.68 4.94 6.74 8.80

Category Average(Short Term ) 11.27 3.93 6.18 8.50

Accrual

IDFC Corporate Bond Fund 7,307.49 0 12.81 2.96 6.03 9.03

SBI Corporate Bond Fund 3,272.11 36M 13.44 6.20 7.61 9.59

HDFC Corporate Debt Opportunities Fund 11,092.15 36M 15.11 5.36 7.09 10.00

Kotak Medium Term Fund 3,701.32 18M 16.21 4.66 6.57 9.95

Crisil Composite Bond Fund Index 21.80 -0.21 5.16 10.31

Category Average(Accural/Long) 13.57 4.00 6.39 9.36

Dynamic

Birla Sun Life Dynamic Bond Fund 14,306.36 90D 23.65 -6.92 0.32 8.72

IDFC Dynamic Bond Fund 4,319.80 0 19.26 4.77 8.26 12.23

SBI Dynamic Bond Fund 3,090.40 1M 14.52 2.20 8.36 13.04

Crisil Composite Bond Fund Index 21.80 -0.21 5.16 10.31

Category Average(Gilt/Income/Dynamic) 17.23 -2.70 4.43 10.21

Performance as on 13th April; Portfolio Details as on 31st March

OUR PORTFOLIO CONSTRUCTION APPROACH

What determines equity allocation ?

28

View on Equity Markets:

Over valued or Under Valued?

Your Risk Profile

Equity Markets: Over Valued or Under Valued?

Aim: Invest in equity when markets are undervalued and book profits, when overvalued

Decision on under/over valued: in-house model which takes into account Price to Earnings and Price to Book ratio for

more than 20 years

Higher the valuation score, lower the allocation to equities

Valuation Score

29

One Size Does Not Fit All – Select your Risk Profile

50,000

1,50,000

2,50,000

3,50,000

4,50,000

5,50,000

6,50,000

7,50,000

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Jan

-17

Aggressive

50000

150000

250000

350000

450000

550000

650000

750000

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Jan

-17

Growth

■ CAGR (since 1995): 9.1%

■ Min 1yr Calendar Return: -51%

■ Max 1yr Calendar Return: 77%

■ Avg 5 year Rolling Return: 11.8%

■ CAGR (since 1995): 9.2%

■ Min 1yr Calendar Return: -39%

■ Max 1yr Calendar Return: 58%

■ Avg 5 year Rolling Return: 11.1%

High Returns with high fluctuations

30Aggressive: 100% Sensex; Growth: 75% Sensex + 25% Debt (7% FD)

One Size Does Not Fit All – Select your Risk Profile

■ CAGR (since 1995): 9.0%

■ Min 1yr Calendar Return: -26%

■ Max 1yr Calendar Return: 40%

■ Avg 5 year Rolling Return: 10.1%

■ CAGR (since 1995): 8.3%

■ Min 1yr Calendar Return: -10%

■ Max 1yr Calendar Return: 23%

■ Avg 5 year Rolling Return: 8.8%

Moderate Returns with Moderate/ Low fluctuations

50000

150000

250000

350000

450000

550000

650000

750000

Jan

-95

Jan

-98

Jan

-01

Jan

-04

Jan

-07

Jan

-10

Jan

-13

Jan

-16

Balanced

0

100000

200000

300000

400000

500000

600000

700000

Jan

-95

Jan

-98

Jan

-01

Jan

-04

Jan

-07

Jan

-10

Jan

-13

Jan

-16

Semi Conservative

31

50000

150000

250000

350000

450000

550000

650000

750000

Jan

-95

Jan

-98

Jan

-01

Jan

-04

Jan

-07

Jan

-10

Jan

-13

Jan

-16

Conservative

■ Assumed to invested in long term FD at static growth rate of 7%

Balanced: 50% Sensex + 50% Debt (7% FD); Semi Conservative: 25% Sensex + 75% Debt (7% FD)

Model Portfolios: Portfolio Constraints

32

Profile Aggressive Growth Balanced Semi Cons Conservative

Equity Allocation (Max) 100% 75% 50% 25% 0%

Equity Allocation (Min) 0% 0% 0% 0% 0%

Equity allocation leads to fluctuations in the portfolio and hence we cap the exposure to equity portfolios for different risk profiles

However, as mentioned before, recommended equity exposure is combination of valuation score and risk profile as seen on the following slide

Recommended Equity Allocation

33

Valuation Score

(Current highlighted)

Aggressive Growth Balanced Semi Conservative

Conservative

1 100% 75% 50% 25% 0%

2 90% 70% 45% 20% 0%

3 80% 60% 40% 15% 0%

4 70% 55% 35% 15% 0%

5 60% 45% 30% 10% 0%

6 50% 40% 25% 10% 0%

7 40% 30% 20% 5% 0%

8 30% 20% 15% 0% 0%

9 20% 10% 10% 0% 0%

10 0% 0% 0% 0% 0%

Model Portfolio – Track Record

16.1%

14.4%

12.1%

9.6%

11.8%11.1%

10.1%8.8%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

aggressive growth Balanced SemiConservative

5 Yr Avg Rolling Return

Portfolio benchmark

211

196

177

158

174 170

162 152

140

160

180

200

220

aggressive growth Balanced SemiConservative

Investment of 100 over 5 years

Portfolio Benchmark

1.6%3.1%

4.6%6.5%

-7.4%

-3.2%

0.7%

4.2%

-10.0%-7.5%-5.0%-2.5%0.0%2.5%5.0%7.5%

aggressive growth Balanced SemiConservative

Minimum 5 Yr Return

Portfolio Benchmark

80.7% 80.0%

77.1%

72.2%

66.0%

68.0%

70.0%

72.0%

74.0%

76.0%

78.0%

80.0%

82.0%

aggressive growth Balanced SemiConservative

% outperformance over Benchmark

34Updated on 31st December 2016

RECOMMENDED MODEL PORTFOLIOS

35

Model Portfolio: Aggressive

Scheme (%)

Birla Frontline Equity 7.5%

SBI Blue chip 7.5%

IDFC Classic Equity 7.5%

Kotak Select Focus 7.5%

ICICI Pru Balanced Advantage 10%

HDFC Life Balanced Fund 10%

Unifi Capital PMS 5%

India Opportunities Portfolio – Motilal 5%

Total Equity** 60%

IDFC Arbitrage Fund 7.5%

ICICI Pru Equity Arbitrage Fund 7.5%

IDFC Corporate Bond Fund 10%

Kotak Medium Term Fund 5%

Edelweiss NCD/ FMPs 10%

Total Debt 40%

TOTAL 100%

** Both balanced funds have ~50%allocation to equity, so overallportfolio exposure to equity is 50%

19,47,053

6,60,707.16

-1,00,000

2,00,000

5,00,000

8,00,000

11,00,000

14,00,000

17,00,000

20,00,000

Aggressive Vs Benchmark

Aggressive Portfolio Benchmark

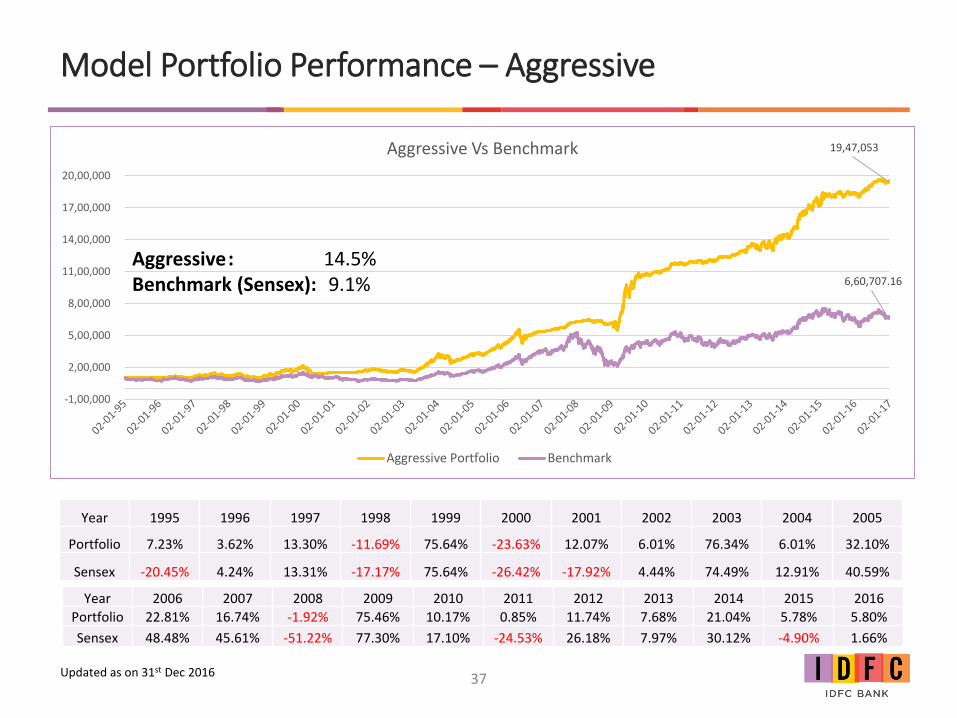

Model Portfolio Performance – Aggressive

Aggressive: 14.5%Benchmark (Sensex): 9.1%

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Portfolio 7.23% 3.62% 13.30% -11.69% 75.64% -23.63% 12.07% 6.01% 76.34% 6.01% 32.10%

Sensex -20.45% 4.24% 13.31% -17.17% 75.64% -26.42% -17.92% 4.44% 74.49% 12.91% 40.59%

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Portfolio 22.81% 16.74% -1.92% 75.46% 10.17% 0.85% 11.74% 7.68% 21.04% 5.78% 5.80%

Sensex 48.48% 45.61% -51.22% 77.30% 17.10% -24.53% 26.18% 7.97% 30.12% -4.90% 1.66%

37Updated as on 31st Dec 2016

Model Portfolio: Growth

Scheme (%)

Birla Frontline Equity 5%

SBI Blue chip 5%

IDFC Classic Equity 5%

Kotak Select Focus 5%

ICICI Pru Balanced Advantage 10%

HDFC Life Balanced Fund 10%

Unifi Capital PMS 5%

India Opportunities Portfolio -Motilal

5%

Total Equity** 50%

IDFC Arbitrage Fund 10%

ICICI Pru Equity Arbitrage Fund 10%

IDFC Corporate Bond Fund 10%

Kotak Medium Term Fund 10%

Edelweiss NCD/ FMPs 10%

Total Debt 50%

TOTAL 100%

** Both balanced funds have ~50%allocation to equity, so overallportfolio exposure to equity is 40%

15,08,935

6,84,655.49

-

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

12,00,000

14,00,000

16,00,000

Growth Vs Benchmark

Growth Portfolio Benchmark

Model Portfolio Performance – Growth

Growth: 13.1%Benchmark: 9.2%(75% Equity; 25% Debt)

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Portfolio 7.23% 4.31% 12.21% -6.75% 58.79% -18.49% 11.00% 6.13% 60.26% 5.61% 27.43%

Benchmark -13.99% 5.56% 12.43% -10.91% 56.55% -18.27% -11.64% 5.43% 55.03% 12.17% 31.75%

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Portfolio 18.87% 11.99% 2.68% 60.44% 9.19% 4.04% 10.05% 7.57% 17.61% 6.71% 6.31%

Benchmark 37.74% 35.64% -39.45% 58.08% 14.82% -17.27% 21.40% 8.09% 24.16% -1.75% 3.25%

39Updated as on 31st Dec 2016

Model Portfolio: Balanced

40

Scheme (%)

Birla Frontline Equity 5%

SBI Bluechip 5%

IDFC Classic Equity 2.5%

Kotak Select Focus 2.5%

ICICI Pru Balanced Advantage 5%

HDFC Life Balanced Fund 5%

Unifi Capital PMS 2.5%

India Opportunities Portfolio -Motilal

2.5%

Total Equity** 30%

IDFC Arbitrage Fund 15%

ICICI Pru Equity Arbitrage Fund 15%

SBI Corporate Bond Fund 15%

IDFC Corporate Bond Fund 15%

Edelweiss NCD/ FMPs 10%

Total Debt 70%

TOTAL 100%

** Both balanced funds have ~50%allocation to equity, so overallportfolio exposure to equity is 25%

10,54,008

6,53,615.85

-

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

02

-01

-95

02

-01

-96

02

-01

-97

02

-01

-98

02

-01

-99

02

-01

-00

02

-01

-01

02

-01

-02

02

-01

-03

02

-01

-04

02

-01

-05

02

-01

-06

02

-01

-07

02

-01

-08

02

-01

-09

02

-01

-10

02

-01

-11

02

-01

-12

02

-01

-13

02

-01

-14

02

-01

-15

02

-01

-16

02

-01

-17

Balanced Vs Benchmark

Balanced Portfolio Benchmark

Model Portfolio Performance – Balanced

Balanced: 11.3%Benchmark: 9.0%50% Debt; 50% Equity

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Portfolio 7.23% 5.55% 10.48% -1.94% 41.78% -12.07% 9.66% 6.90% 43.94% 4.65% 20.69%

Sensex -7.21% 6.51% 11.11% -4.71% 38.78% -9.87% -5.32% 6.24% 37.42% 10.98% 23.23%

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Portfolio 15.61% 11.99% 2.68% 41.44% 8.70% 4.04% 9.45% 7.47% 14.17% 6.68% 6.56%

Sensex 27.24% 25.88% -25.80% 39.95% 12.41% -9.55% 16.64% 8.01% 18.36% 1.32% 4.72%

41Updated as on 31st Dec 2016

Model Portfolio: Semi Conservative

42

Scheme (%)

Birla Frontline Equity 2.50%

SBI Bluechip 2.50%

IDFC Classic Equity 2.50%

ICICI Pru Balanced Advantage 2.50%

HDFC Life Balanced Fund 2.50%

Total Equity** 12.5%

IDFC Arbitrage Fund 17.5%

ICICI Pru Equity Arbitrage Fund 17.5%

IDFC Corporate Bond Fund 17.5%

SBI Corporate Bond Fund 17.5%

Edelweiss NCD/ FMP 17.5%

Total Debt 87.5%

TOTAL 100%

** Both balanced funds have ~50%allocation to equity, so overallportfolio exposure to equity is 10%

Model Portfolio Performance – Semi Conservative

Year 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Portfolio 7.23% 6.72% 8.87% 3.99% 24.62% -3.80% 8.32% 7.53% 26.45% 4.58% 13.28%

Benchmark -0.14% 7.08% 9.38% 1.37% 22.36% -1.34% 1.00% 6.84% 21.54% 9.35% 15.06%

Year 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Portfolio 10.65% 7.23% 7.27% 22.52% 7.72% 7.23% 7.69% 7.32% 9.56% 7.10% 7.05%

Benchmark 17.06% 16.40% -10.22% 23.00% 9.88% -1.38% 11.92% 7.73% 12.72% 4.33% 6.07%

7,06,632

5,74,915.93

-

2,00,000

4,00,000

6,00,000

8,00,000

10,00,000

Semi Conservative Vs Benchmark

Semi Conservative Portfolio Benchmark

Semi Conservative: 9.3%Benchmark: 8.3%75% Debt; 25% Equity

43Updated as on 31st Dec 2016

Disclaimer

This document has been prepared by IDFC Bank Limited based on information obtained from public sources and sources believed to bereliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. The contents of this report are solelyfor informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe forsecurities or other financial instruments or any other product. Nothing in the report constitutes investment, legal, accounting and tax advice ora representation that any investment or strategy is suitable or appropriate to the investor's circumstances. While due care has been taken inpreparing this document, IDFC Bank and its affiliates accept no liabilities for any loss or damage of any kind arising out of any inaccurate,delayed or incomplete information nor for any actions taken in reliance thereon.

The securities/funds discussed and opinions expressed in this mail may not be suitable for all investors, who must make their own investmentdecisions, based on their own investment objectives & financial position. Please be informed that past performance is not necessarily a guide tofuture performance. Actual results may differ materially from those set forth in projections. Unless expressly stated, performance of products isnot guaranteed by IDFC Bank or its affiliates. The information provided may not be taken in substitution for the exercise of independentjudgement by any investor.

This document is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in anylocality, state, country, or other jurisdiction, where such distribution, publication, availability, or use would be contrary to law, regulation orwhich would subject IDFC Bank and affiliates to any registration or licensing requirement within such jurisdiction.

Please note that Mutual Fund Investments are subject to market risks, please read the Statement of Additional Information & SchemeInformation Document carefully before investing for full understanding and detail. IDFC Bank Limited shall receive brokerage for Mutual fundtransactions through AMC’s as permitted under the extant regulations. For the applicable brokerage rates for each transaction, please visitidfcbank.com or contact your IDFC Bank representative.

The information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way,transmitted to, copied, or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior writtenconsent of IDFC Bank Limited. IDFC Bank limited accepts no liability nor responsibility whatsoever with respect to the use of the informationprovided hereinabove.

The customers acknowledge that none of the Information has been subject to verification and neither IDFC Bank nor any of its representativesaccepts responsibility for or makes any representation, expressed or implied, or gives any warranty with respect to the accuracy orcompleteness of the Information. The Customers shall be responsible for making their own decision on the Information and acknowledge thatit shall not have any right of action against IDFC Bank or any of its Representatives in relation to the accuracy, reasonableness, or completenessof any of the Information. Accordingly, IDFC Bank and any of its Representatives will not be liable for any direct, indirect, or consequential lossor damage suffered by any person as a result of any reliance on any statement contained in or omitted from the Information.

44